Introduction: June 2026 Shows the Battery Industry Is No Longer Just an EV Story

The global battery industry entered a new phase in June 2026. For most of the last decade, battery demand was largely discussed through the lens of electric vehicles. That is now changing. Batteries are becoming a core infrastructure layer for power grids, AI data centers, renewable energy integration, industrial electrification, electric freight, critical minerals security, and national manufacturing strategy.

The most important message from June 2026 is clear: the battery market is moving from a vehicle-led growth cycle to a multi-application energy infrastructure cycle. EVs remain central, but they are no longer the only demand engine. Grid-scale battery energy storage systems, long-duration storage, data center backup power, vehicle-to-grid platforms, sodium-ion batteries, and battery recycling are becoming strategic growth areas.

This shift matters for every participant in the battery value chain. Battery manufacturers are being pushed to diversify beyond automotive cells. Automakers are reassessing battery chemistries, cost structures and supply agreements. Utilities are looking for storage systems that can support renewable-heavy grids. Investors are evaluating whether the next major battery returns will come from EV cells, stationary storage, recycling, battery management systems, battery materials or manufacturing equipment.

June 2026 also highlighted a major competitive reality: China continues to lead the battery supply chain, but the rest of the world is trying to reduce dependency through localization, alternative chemistries and new manufacturing models. CATL’s sodium-ion and energy storage moves, GM’s sodium-ion partnership with Peak Energy, Panasonic’s U.S. data center battery push and UK long-duration storage support all point to the same structural trend: battery demand is spreading across sectors, regions and chemistries.

Request for Exclusive Sample on Circular Battery Economy Market

Quick Highlights: Battery Industry News June 2026

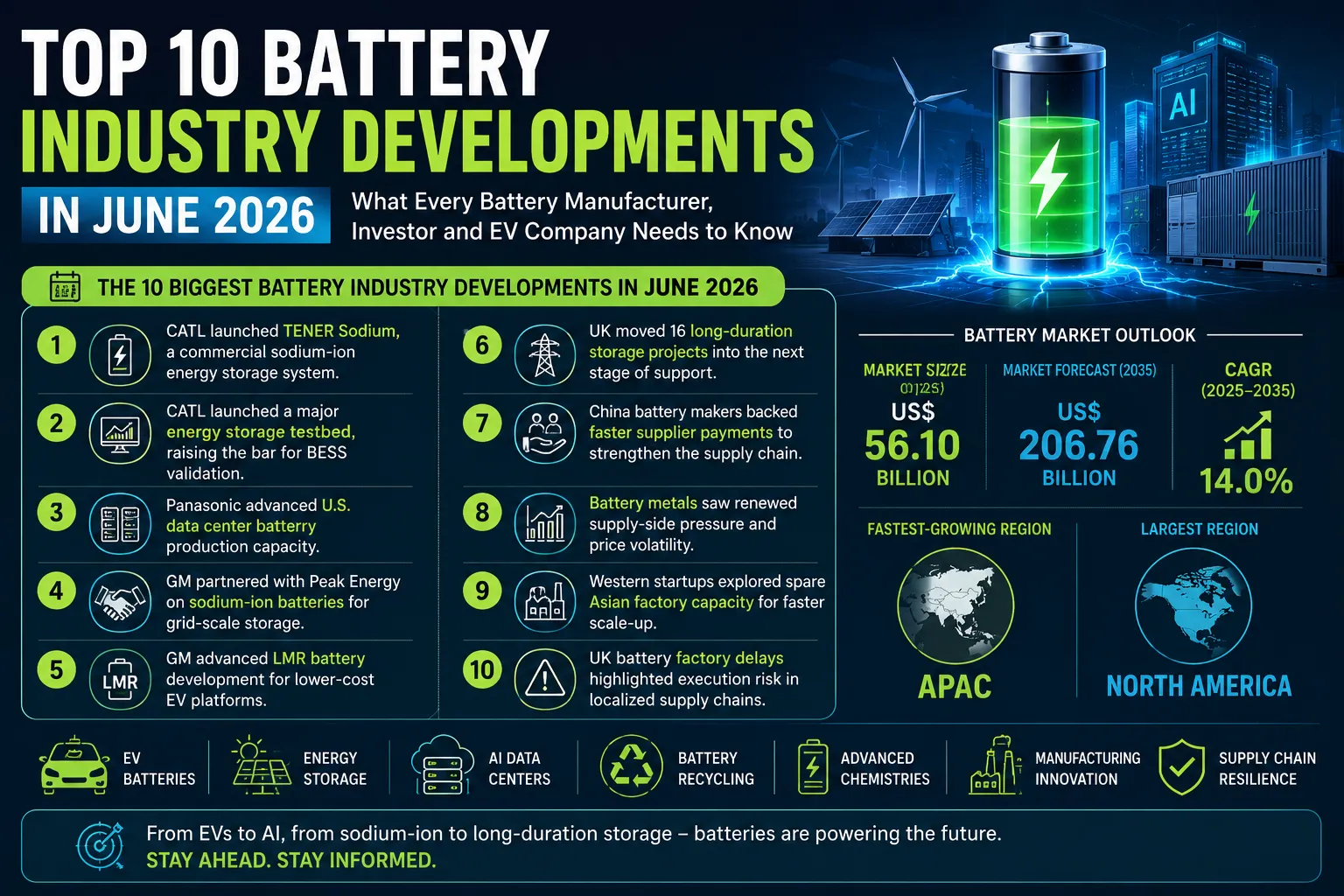

| Topic | What Happened | Strategic Impact |

CATL Sodium-Ion Storage | CATL launched TENER Sodium, a commercial sodium-ion energy storage system. | Sodium-ion moved closer to grid-scale commercial deployment. |

CATL Energy Storage Testbed | CATL launched a large energy storage validation platform. | Testing and bankability are becoming major differentiators in BESS procurement. |

Panasonic U.S. Manufacturing | Panasonic moved toward data center battery production in the U.S. | AI data centers are becoming a serious battery demand driver. |

| GM and Peak Energy | GM partnered with Peak Energy on sodium-ion batteries for stationary storage. | Automakers are entering the grid storage value chain. |

GM LMR Battery Strategy | GM advanced lithium-manganese-rich battery development. | Next-generation EV chemistries are targeting lower cost and higher energy density. |

UK Long-Duration Storage | Ofgem moved 16 long-duration storage projects into the next stage. | Storage is becoming critical grid infrastructure, not just a renewable add-on. |

China Supplier Payments | Major Chinese battery makers backed faster supplier payments. | Financial discipline is becoming important in the battery manufacturing supply chain. |

| Battery Metals | Lithium, cobalt and nickel markets showed renewed supply-side pressure. | Procurement teams must prepare for more volatile raw material pricing. |

Asian Manufacturing Model | Western startups explored spare Asian factory capacity. | Asset-light battery manufacturing is emerging as an alternative to costly gigafactory bets. |

UK Battery Factory Risk | JLR faced potential battery supply delays linked to Agratas factory issues. | Localized supply chains still carry execution and construction risk. |

Top 10 Battery Industry Developments in June 2026

1. CATL Moved Sodium-Ion Energy Storage Toward Commercial Reality

What Happened

In June 2026, CATL unveiled the TENER Sodium Energy Storage System in Munich. CATL described it as a field-validated sodium-ion energy storage solution designed for commercial deployment. The system is positioned for grid-scale applications, with commercial deliveries in China planned before broader global deliveries.

Why It Matters

This is one of the most important battery industry developments of June 2026 because sodium-ion batteries are moving from laboratory discussion to real commercial infrastructure. Sodium-ion technology is attractive because it reduces reliance on lithium, nickel and cobalt, while offering potential advantages in cost, material availability and cold-weather performance. For grid storage, where weight and energy density are less critical than cost, safety and lifecycle economics, sodium-ion can become a serious alternative to lithium-ion.

CATL’s move also signals that sodium-ion is not only a startup opportunity. Large battery manufacturers are now building complete sodium-ion ecosystems that include cell design, materials, battery management systems, system integration and deployment support.

Market Impact

The near-term impact will be strongest in stationary storage, renewable integration, backup power and data center support. Sodium-ion is unlikely to replace lithium-ion in premium EVs immediately, but it can reduce pressure on lithium supply chains and create a new cost-competitive category for utility-scale storage.

Who Benefits

Battery manufacturers, energy storage developers, utilities, grid operators, raw material suppliers for sodium-based chemistries and investors focused on non-lithium energy storage platforms.

Request for Exclusive Sample on Sodium-Ion Battery Market

2. CATL Launched a Major Energy Storage Testbed, Raising the Bar for BESS Validation

What Happened

CATL announced the launch of a large energy storage testbed in June 2026, positioning it as a move toward real-world validation for energy storage systems. The announcement reflects a broader industry need for tested, bankable and performance-verified BESS products.

Why It Matters

As battery energy storage systems scale from megawatt-level projects to multi-gigawatt portfolios, buyers are becoming more demanding. Utilities, independent power producers, data center operators and infrastructure investors need proof of safety, degradation performance, dispatch reliability, thermal management and long-term operating economics.

This is especially important because battery storage projects are increasingly being financed as infrastructure assets. In that environment, validated performance can influence insurance costs, project finance terms, warranty structures and procurement decisions.

Market Impact

Testing infrastructure will become a competitive advantage. Battery companies that can prove performance under real operating conditions will be better positioned in large utility tenders and long-duration storage procurement programs. This trend also creates opportunities for testing companies, certification providers, battery analytics platforms and battery management system suppliers.

Who Benefits

Utility-scale storage developers, insurers, infrastructure investors, battery management system companies, testing labs and battery manufacturers with strong safety and validation capabilities.

Request for Exclusive Sample on Battery Management System Market

3. Panasonic’s U.S. Data Center Battery Push Shows AI Is Becoming a Battery Demand Driver

What Happened

Panasonic’s U.S. battery strategy gained attention in June 2026 as reports highlighted its plan to increase battery production capacity for data center applications, including the use of its Kansas manufacturing footprint. Panasonic’s Kansas lithium-ion battery factory began mass production in 2025 with a planned annual capacity of around 32 GWh, strengthening its U.S. manufacturing base.

Why It Matters

This development shows that AI data centers are becoming a new battery growth market. Data centers require backup power, power smoothing, energy storage, grid support and resilience infrastructure. As AI workloads increase electricity demand, batteries can help manage peak load, support renewable power usage and reduce dependence on conventional backup systems.

For Panasonic, this is also a strategic diversification move. EV demand remains important, but battery manufacturers are increasingly looking at stationary storage and data center power as higher-stability demand pools.

Market Impact

The battery manufacturing industry will increasingly serve two large customers: automakers and energy infrastructure operators. This may change cell design priorities. Data center batteries may prioritize safety, cycle life, thermal stability, availability and predictable operating cost over extreme energy density.

Who Benefits

Battery manufacturers, data center developers, AI infrastructure operators, U.S. battery component suppliers, energy storage integrators and investors tracking AI power infrastructure.

Request Exclusive Sample on AI Data Center BESS Market

4. GM Partnered With Peak Energy on Sodium-Ion Batteries for Grid Storage

What Happened

General Motors announced work with Peak Energy to develop sodium-ion battery cells for grid-scale stationary storage systems. GM described the move as part of a broader energy strategy focused on a power grid under pressure from AI data centers and large electricity users.

Why It Matters

GM’s sodium-ion move shows that automakers are no longer thinking about batteries only as EV components. Battery know-how, manufacturing systems and cell development capability can be applied to stationary energy storage. This is a strategic expansion of the automaker role from vehicle manufacturer to energy ecosystem participant.

Sodium-ion batteries are particularly relevant for stationary storage because they can use more abundant materials and may offer cost advantages in applications where weight is not the main constraint.

Market Impact

GM’s move may encourage more automakers to explore energy storage markets. It also increases competitive pressure on dedicated BESS companies. If automakers use their manufacturing expertise to scale grid batteries, the battery storage market could become more competitive and more industrialized.

Who Benefits

Automakers with battery expertise, energy storage startups, utilities, data center operators, sodium-ion material suppliers and investors focused on grid-scale storage.

Request for Exclusive Sample on Sodium-Ion Battery Market

5. GM Advanced LMR Battery Development for Lower-Cost EV Platforms

What Happened

GM advanced its lithium-manganese-rich battery strategy in June 2026. Reports indicated that GM is focusing on LMR chemistry as a way to reduce EV battery costs while improving energy storage capacity compared with some lower-cost alternatives.

Why It Matters

LMR batteries matter because EV companies are under pressure to reduce costs without sacrificing driving range. Lithium iron phosphate has gained traction because of cost and safety benefits, but automakers still need chemistries that can deliver higher energy density for larger vehicles, trucks and long-range EVs.

GM’s LMR strategy suggests that the next phase of EV battery competition will not be only about LFP versus NMC. Instead, automakers may build multi-chemistry portfolios where LFP, LMR, high-nickel lithium-ion, sodium-ion and eventually solid-state batteries serve different vehicle and storage segments.

Market Impact

If LMR scales successfully, it could reduce cobalt dependence, improve cost competitiveness and support long-range EV adoption. However, commercial success will depend on cycle life, manufacturing yield, thermal performance and integration into existing battery production lines.

Who Benefits

EV manufacturers, cathode material suppliers, manganese producers, battery R&D companies and investors seeking exposure to next-generation EV battery chemistries.

Request for Exclusive Sample on Battery Chemicals Market

6. UK Long-Duration Storage Support Reinforced the Role of Batteries in Grid Modernization

What Happened

On June 26, 2026, Ofgem moved 16 long-duration electricity storage projects into the next stage of its support mechanism. The selected projects include a mix of technologies, including lithium-ion batteries, flow batteries, compressed air and pumped storage.

Why It Matters

This development matters because it confirms that storage is now a central part of national energy security. Renewable power systems need storage to balance intermittent generation, reduce curtailment, manage peak demand and maintain grid stability.

For the battery industry, the important insight is that not all storage demand will be short-duration lithium-ion. Governments and utilities are increasingly looking at duration, reliability, dispatchability and system-level value.

Market Impact

The UK’s move supports demand for long-duration storage technologies and may encourage other countries to create similar support mechanisms. This benefits lithium-ion batteries in some applications, but it also creates room for flow batteries, sodium-ion systems and hybrid storage platforms.

Who Benefits

Battery storage developers, utilities, long-duration storage technology providers, grid operators, renewable project developers and infrastructure investors.

Request for Exclusive Sample on Grid-Scale Battery Market

7. China Pushed Battery Makers Toward Faster Supplier Payments

What Happened

In late June 2026, major Chinese battery makers including CATL, BYD and CALB backed an initiative to pay suppliers faster, with reports highlighting a 60-day payment target. The move was linked to broader efforts to stabilize competition and cash flow across the battery supply chain.

Why It Matters

This may look like a financial detail, but it is strategically important. The battery manufacturing industry is capital-intensive, price-competitive and supplier-dependent. Long payment cycles can weaken smaller material suppliers, equipment providers and component manufacturers.

Faster payments can improve supplier health, reduce production disruption risk and strengthen the resilience of the battery manufacturing ecosystem. It also indicates that China is trying to manage the risks of intense price competition in its battery sector.

Market Impact

Procurement leaders should watch payment terms as closely as cell prices. Financially weak suppliers can become a hidden risk in large battery programs. Stable supplier payment practices may become a differentiator for battery manufacturers competing for global OEM and energy storage contracts.

Who Benefits

Battery material suppliers, component makers, equipment companies, smaller vendors, battery manufacturers with stronger supplier networks and OEMs seeking reliable delivery.

Request for Exclusive Sample on Battery Material Market

8. Battery Metals Remained Volatile as Lithium, Cobalt and Nickel Supply Risks Continued

What Happened

June 2026 showed continued movement in battery metals. Reports highlighted that lithium prices were lower during the month, while broader commentary indicated that cobalt, nickel and lithium had recovered from 2024–2025 lows due to supply restraint and policy-driven supply controls.

Why It Matters

Battery metals are entering a more complex pricing environment. Demand still matters, but supply policy, export controls, quotas, mining approvals and geopolitical positioning are increasingly influencing price formation. For battery manufacturers and EV companies, this creates procurement uncertainty.

The battery industry cannot rely only on spot-market purchasing. Long-term supply contracts, recycling, chemistry diversification and regional sourcing strategies are becoming essential.

Market Impact

Lithium-ion batteries will remain dominant, but raw material volatility strengthens the business case for sodium-ion batteries, LFP chemistry, recycling, second-life batteries and alternative cathode strategies. Battery companies with diversified material exposure will have stronger cost control.

Who Benefits

Battery recyclers, sodium-ion developers, LFP producers, material traders, mining companies with secure supply and OEMs with long-term offtake agreements.

Request For Exclusive Sample on Battery Components Market

9. Western Battery Startups Turned to Spare Asian Manufacturing Capacity

What Happened

In June 2026, reports showed that Western battery startups were exploring spare production capacity in Asia instead of building expensive greenfield gigafactories. Examples included sodium-ion and solid-state battery companies looking at contract manufacturing or leased production lines.

Why It Matters

This development reflects a post-Northvolt reality. Battery manufacturing is expensive, technically complex and risky. Startups with promising technology may not have the capital or operational maturity to build large factories independently. Using existing Asian manufacturing capacity can accelerate commercialization while reducing capital risk.

However, this model also creates strategic concerns. It may increase dependence on Asian supply chains, raise intellectual property risks and slow the development of local manufacturing expertise in Europe and North America.

Market Impact

The battery manufacturing industry may split into two models. Large incumbents will continue building integrated gigafactories, while smaller innovators may use an asset-light production model. Investors will likely become more selective, favoring companies that can prove manufacturability before committing to full-scale plants.

Who Benefits

Battery startups, contract manufacturers, Asian cell production partners, investors seeking lower-capex scale-up models and specialty battery customers.

Request an Exclusive Sample on China EV Battery Market

10. UK Battery Factory Delays Highlighted the Execution Risk in Localized Supply Chains

What Happened

In June 2026, reports indicated that Jaguar Land Rover could face battery supply delays linked to construction and execution challenges at the Agratas battery factory in Somerset. The project is significant for the UK’s domestic battery manufacturing ambitions and JLR’s electric vehicle transition.

Why It Matters

Battery localization is a powerful strategic theme, but local supply chains are not easy to build. Gigafactories require complex construction, equipment procurement, skilled labor, utility infrastructure, quality systems and long-term customer commitments. A delay in one major plant can affect automaker launch plans, compliance with EV targets and regional industrial strategy.

This is a reminder that battery supply chain localization is not only a policy issue. It is an execution challenge.

Market Impact

Automakers may keep multi-region sourcing strategies even when they support domestic production. Battery manufacturers must demonstrate not only technology strength but also project delivery capability, financial discipline and operational reliability.

Who Benefits

Established battery manufacturers, project execution partners, battery equipment suppliers, construction specialists, supply chain risk consultants and OEMs with diversified sourcing strategies.

Biggest Battery Industry Trends Emerging After June 2026

Trend 1: Battery Storage Is Becoming as Strategically Important as EV Batteries

The biggest trend from June 2026 is the rise of stationary storage. CATL, GM, Panasonic and UK energy regulators all pointed toward a market where grid batteries, AI data center batteries and long-duration storage become major growth areas.

Energy storage is no longer a supporting application. It is becoming a core demand center for the global battery market.

Trend 2: AI Data Centers Are Creating a New Battery Demand Pool

AI infrastructure is increasing electricity demand and grid stress. This is creating opportunities for battery systems that provide backup power, load balancing, renewable integration and grid support. Panasonic’s U.S. data center battery push and GM’s sodium-ion storage strategy both reflect this shift.

Trend 3: Sodium-Ion Batteries Are Moving From Pilot to Commercial Strategy

Sodium-ion batteries are gaining traction because they reduce lithium dependency and offer advantages for stationary storage. CATL’s TENER Sodium launch and GM’s Peak Energy partnership show that sodium-ion is no longer a niche chemistry. It is becoming part of mainstream battery strategy.

Trend 4: Battery Manufacturing Localization Is Necessary but Difficult

The U.S., Europe, India and the UK all want localized battery supply chains. However, the JLR-Agratas situation shows that localization involves real execution risk. Factory delays, cost overruns, talent shortages and equipment bottlenecks can affect EV timelines.

Trend 5: China Still Leads the Battery Supply Chain

China remains the most powerful battery manufacturing ecosystem. CATL, BYD, CALB and other Chinese companies continue to influence pricing, supplier terms, production capacity and technology direction. The supplier payment initiative also shows China’s focus on stabilizing its domestic battery ecosystem.

Trend 6: Battery Chemistry Strategies Are Becoming More Segmented

There is no single winning battery chemistry. LFP may dominate lower-cost EVs and stationary storage. LMR may support long-range EVs. Sodium-ion may grow in grid storage. Solid-state batteries may target premium mobility and high-performance applications. Flow batteries may expand in long-duration storage.

The future battery market will be multi-chemistry, not one-chemistry.

Expert Analysis: What June 2026 Reveals About the Future of Battery Manufacturing

June 2026 revealed three important realities about the future of the battery industry.

First, the battery market is moving toward application-specific manufacturing. In the early EV boom, manufacturers focused heavily on producing cells for vehicles. Now, battery design must match different end uses. A data center battery does not need the same performance profile as an EV battery. A long-duration grid battery does not need the same energy density as a pickup truck battery. This will force manufacturers to create more flexible production platforms.

Second, supply chain resilience is becoming as important as cell chemistry. The companies that win after 2030 will not be those with only the best chemistry. They will be the ones with secure materials, strong supplier relationships, validated performance, manufacturing discipline and regional production capacity.

Third, investors are becoming more selective. Battery startups can no longer raise capital only on technology promises. They must prove commercial readiness, production scalability, customer demand and cost competitiveness. This is why contract manufacturing, validation testbeds and asset-light production models are becoming more relevant.

The smartest investments in the battery industry are likely to move toward four areas:

- Grid-scale and long-duration energy storage

- Battery materials and recycling

- Battery management systems and safety intelligence

- Alternative chemistries such as sodium-ion and LMR

Technologies losing momentum are not disappearing, but they are being repositioned. High-cost EV-only strategies are under pressure. Battery companies that depend on one customer segment, one chemistry or one region face higher risk.

Market Forecast: Battery Demand Is Expanding Across EVs, Storage, AI and Industrial Electrification

According to DataM Intelligence, the lithium-ion battery market is projected to grow from USD 56.10 billion in 2025 to USD 206.76 billion by 2035, supported by EV adoption, energy storage systems and consumer electronics demand.

The sodium-ion battery market is also entering a high-growth phase. DataM Intelligence estimates the sodium-ion battery market at USD 1,263.70 million in 2025 and forecasts it to reach USD 8,643.11 million by 2035, driven by grid storage, EVs, lithium supply-chain risk and cold-climate battery demand.

The battery components market is projected to expand from USD 105.7 billion in 2025 to USD 391.85 billion by 2035, reflecting rising demand for cell components, battery management systems, sensors, connectors and gigafactory expansion.

These forecasts support one conclusion: battery demand is no longer dependent on a single application. EVs, energy storage systems, AI data centers, aerospace, marine electrification, industrial equipment and renewable power infrastructure are collectively expanding the global battery market.

Related Market Reports

- Circular Battery Economy Market

- Lithium-Ion Battery Market

- Sodium-Ion Battery Market

- Battery Energy Storage System Market

- Grid-Scale Battery Market

- Solid-State Battery Market

- Battery Recycling Market

- Battery Materials Market

- Battery Components Market

- Battery Chemicals Market

- Battery Management Systems Market

- Graphite Market

- Cobalt Market

- Lithium Market

These related reports help readers understand the full battery value chain, from raw materials and cell chemistry to energy storage, recycling and manufacturing equipment.

FAQs: Battery Industry News and Market Trends 2026

1. What is the latest battery industry news in June 2026?

The biggest June 2026 battery industry news includes CATL’s sodium-ion energy storage launch, GM’s sodium-ion partnership with Peak Energy, Panasonic’s U.S. data center battery strategy, GM’s LMR battery development, UK long-duration storage support and China’s supplier payment reforms.

2. Why was June 2026 important for the battery industry?

June 2026 was important because it showed that the battery industry is moving beyond EVs into grid storage, AI data centers, long-duration storage, sodium-ion batteries and localized manufacturing.

3. Who is the largest battery manufacturer in 2026?

CATL remains one of the world’s leading battery manufacturers, with strong positions in EV batteries, energy storage systems and emerging sodium-ion battery technologies.

4. What is the future of sodium-ion batteries?

Sodium-ion batteries are expected to grow in stationary energy storage, backup power, cold-climate applications and lower-cost mobility segments. Their advantage is reduced dependence on lithium, nickel and cobalt.

5. Why is CATL investing in sodium-ion energy storage?

CATL is investing in sodium-ion energy storage to diversify battery chemistry, reduce raw material dependency and serve grid-scale storage markets where cost, safety and supply stability are critical.

6. What are LMR batteries?

LMR batteries are lithium-manganese-rich batteries. They are being developed to offer higher energy density and lower cost by reducing reliance on expensive materials such as cobalt and nickel.

7. Why are AI data centers increasing battery demand?

AI data centers consume large amounts of power and need reliable backup, peak-load management and grid support. Batteries help data centers improve resilience and manage electricity demand.

8. Is battery demand still growing in 2026?

Yes. Battery demand is growing across EVs, stationary energy storage, renewable integration, AI data centers, industrial electrification, marine applications and backup power systems.

9. Which countries dominate battery manufacturing?

China remains the dominant battery manufacturing hub, while the U.S., Europe, Japan, South Korea and India are investing in localized battery supply chains.

10. What are the latest battery technology trends?

Key battery technology trends include sodium-ion batteries, lithium-manganese-rich batteries, solid-state batteries, LFP expansion, long-duration storage, battery recycling and advanced battery management systems.

11. Why is battery recycling becoming important?

Battery recycling reduces dependence on mined lithium, nickel and cobalt. It also supports circular supply chains and helps manufacturers manage raw material volatility.

12. What is the outlook for the global battery market?

The global battery market outlook remains positive as demand expands from EVs to energy storage, AI infrastructure, grid modernization and industrial electrification.

13. Are EV batteries still the largest battery demand driver?

EV batteries remain a major demand driver, but stationary storage and AI data center power systems are becoming increasingly important growth areas.

14. What is the role of battery energy storage systems in renewable energy?

Battery energy storage systems store excess renewable power and release it when demand rises or generation falls. They help stabilize grids with high solar and wind penetration.

15. What should battery manufacturers focus on after June 2026?

Battery manufacturers should focus on chemistry diversification, validated performance, supply chain resilience, localized production, recycling partnerships and storage-specific product development.

Conclusion: June 2026 Marked a Strategic Turning Point for the Battery Industry

June 2026 was not just another month of battery industry news. It marked a strategic turning point.

CATL’s sodium-ion storage launch showed that alternative chemistries are entering commercial reality. Panasonic’s U.S. data center battery direction confirmed that AI infrastructure is becoming a serious battery demand driver. GM’s sodium-ion and LMR strategies showed that automakers are expanding their role in the energy ecosystem. UK long-duration storage support reinforced the importance of batteries in grid modernization. China’s supplier payment initiative highlighted the financial pressure inside the battery manufacturing supply chain.

For battery manufacturers, the message is clear: future growth will depend on serving multiple demand pools, not only EVs. For investors, the strongest opportunities may emerge in grid storage, alternative chemistries, battery materials, recycling and battery intelligence. For EV companies and procurement teams, the priority is to secure flexible, cost-effective and resilient battery supply chains.

The companies that adapt fastest to these shifts will be better positioned for the next decade of battery industry growth. The battery market after June 2026 is broader, more competitive and more infrastructure-driven than ever before.