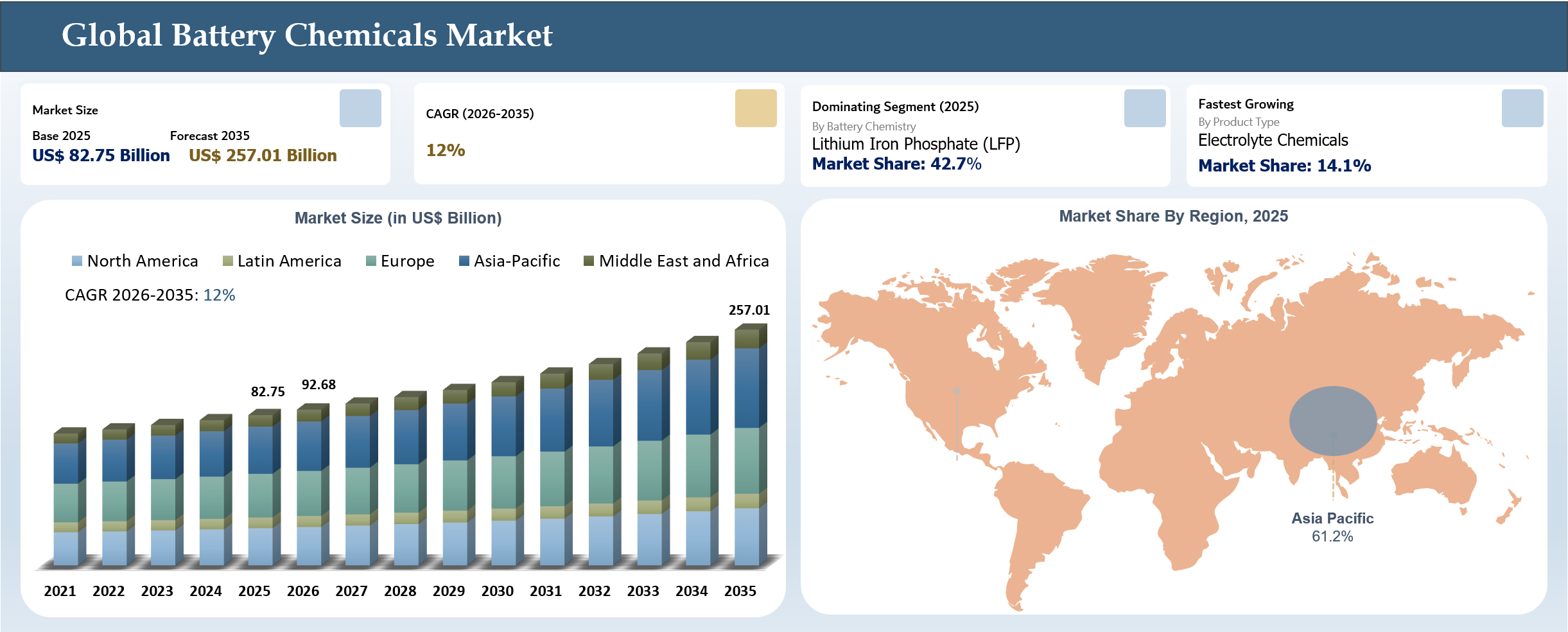

Battery Chemicals Market Size

The global battery chemicals market reached US$ 82.75 billion in 2025 and is expected to reach US$ 257.01 billion by 2035, growing with a CAGR of 12% during the forecast period 2026-2035. The battery chemicals market is witnessing robust growth owing to increased electric vehicle uptake, energy storage installation, and battery production investments globally. Lithium chemicals, cathode materials, electrolyte materials, anode materials, and speciality additives are experiencing growing demand as companies look for greater energy density, faster charging capability, and safer batteries. Market growth is being further stimulated through the expansion of battery gigafactories and localisation initiatives within leading markets. In May 2025, for instance, POSCO Future M developed mass production capabilities of silicon anode materials in order to support the production of high-energy-density next-generation batteries.

Key Takeaways

- Asia-Pacific is dominating the global battery chemicals market, accounting for a share of 61.2% in 2025.

- In 2025, Lithium Iron Phosphate (LFP) battery chemistry led the market with a share of approximately 42.7%.

- Electrolyte chemicals are the fastest-growing product type in 2025, with a CAGR 15.3%.

- The rapid adoption of electric vehicles, energy storage systems, and advanced battery technologies is a major driver accelerating demand for battery chemicals, driven by the need for higher energy density, improved safety, longer battery life, and cost-effective energy storage solutions.

- Companies such as LG Chem, and Albemarle Corporation are strengthening market growth through continued investments in lithium chemicals, cathode materials, advanced electrolytes, and next-generation battery technologies that support electric vehicles, energy storage systems, and emerging battery applications.

Battery Chemicals Industry Trends and Strategic Insight

- The battery chemicals industry is witnessing a strong shift toward advanced battery chemistries, particularly Lithium Iron Phosphate (LFP), high-nickel cathodes, sodium-ion, and solid-state batteries, driven by the need for improved safety, lower costs, and higher energy density. Companies such as CATL and LG Chem are investing in next-generation battery materials and cathode innovations to support evolving electric vehicle and energy storage requirements.

- The industry is increasingly moving toward localized and vertically integrated battery supply chains, with companies including Albemarle Corporation, Ganfeng Lithium, and Tianqi Lithium expanding lithium refining, battery material processing, and strategic partnerships to strengthen raw material security and reduce supply chain risks.

- Electric vehicles, grid-scale energy storage systems, and battery gigafactory expansions are driving demand for high-performance cathode materials, electrolytes, and specialty battery chemicals. Companies such as POSCO Future M, EcoPro BM, and CNGR Advanced Material are increasing investments in cathode active materials and precursor technologies to address growing requirements for fast-charging, high-energy-density, and long-duration battery applications.

Battery Chemicals Market Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 82.75 Billion | |

| 2035 Projected Market Size | US$ 257.01 Billion | |

| CAGR (2026-2035) | 12% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Product Type | Cathode Active Material (CAM) Precursors, Lithium Chemicals, Electrolyte Chemicals, Anode Materials & Conductive Additives, Binder Chemicals, Separator Coating Materials | |

| By Battery Chemistry | Lithium Iron Phosphate (LFP), Nickel Manganese Cobalt (NMC), Nickel Cobalt Aluminum (NCA), Lithium Cobalt Oxide (LCO), Lithium Manganese Oxide (LMO), Sodium-ion, Solid-state, Others | |

| By Application | Automotive, Energy Storage Systems (ESS), Consumer Electronics, Industrial Equipment, Medical Devices, Aerospace & Defense, Telecommunications, Marine, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

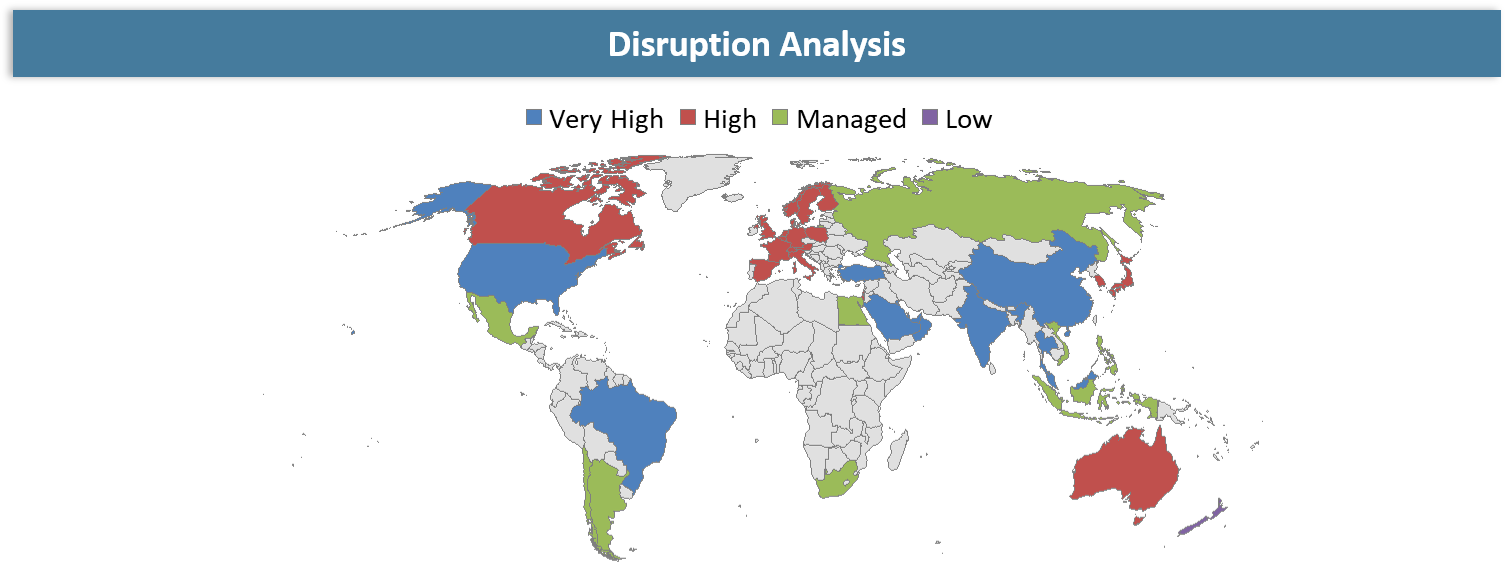

Disruption Analysis

Emergence of Sodium-Ion Battery Technology Reshaping Long-Term Battery Material Demand

A disruption in the battery chemicals market is increasingly being linked to the rise in the commercialization of sodium-ion batteries as an alternative to lithium-ion batteries. Sodium-ion batteries make use of low-cost materials, making them less dependent on the expensive lithium, nickel, and cobalt-based supply chains that had been driving the need for battery chemicals. The introduction of more affordable sodium-ion batteries for manufacturing energy storage systems in basic electric vehicles and stationary storage systems is beginning to disrupt existing material supply practices within the battery industry.

Furthermore, rising investment in sodium-ion battery cells and advanced batteries is causing uncertainties regarding future growth in demand for lithium chemicals in the market. Battery companies are looking into other types of batteries to avoid lithium-related price fluctuations and risks from geopolitical events, which in turn has led to a rethinking of capacity growth within the battery chemicals market.

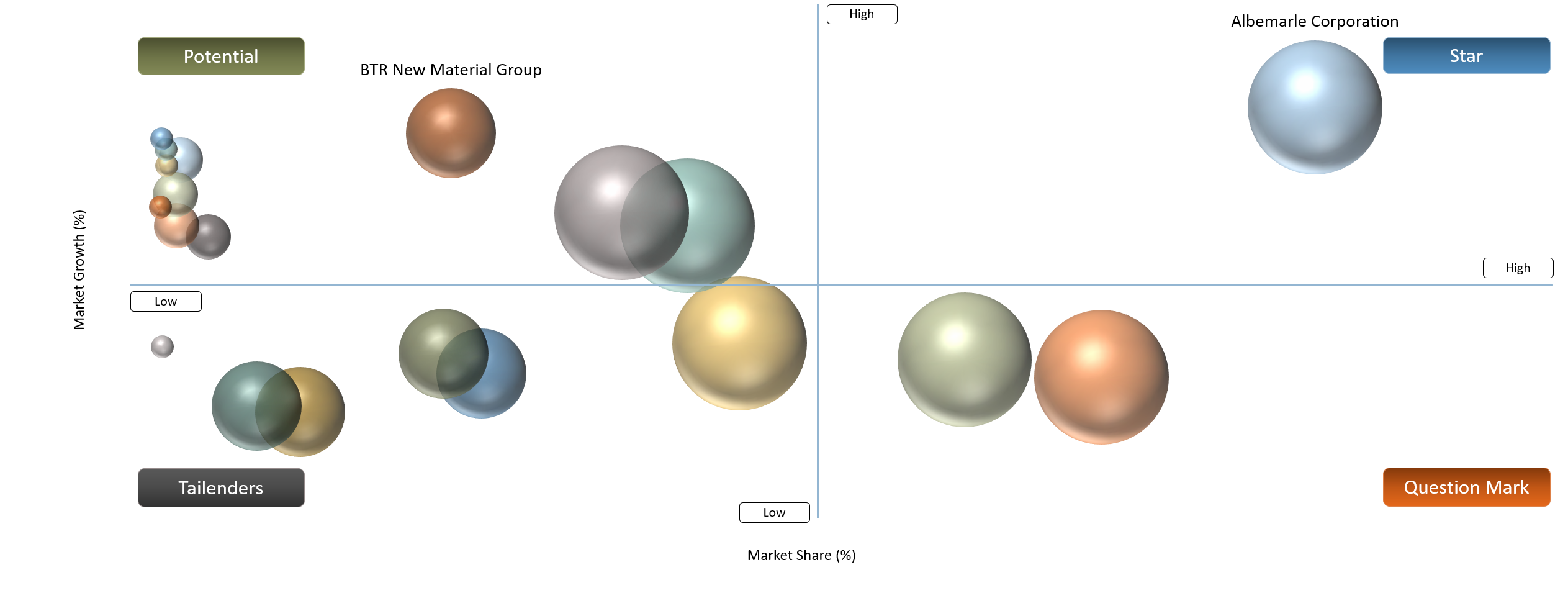

BCG Matrix: Company Evaluation

Star companies comprise Albemarle Corporation, SQM, Ganfeng Lithium, Tianqi Lithium, and LG Chem because of their significant market share and dominance in lithium chemicals, cathode materials, and battery materials manufacturing. These companies have significant production capabilities, existing relationships with battery producers, and continued investment in materials used in electric vehicles. The Question Marks involve POSCO Future M, EcoPro BM, CNGR Advanced Material, Umicore, and BASF since they are building competencies related to cathode and precursors while dealing with stiff competition and changing dynamics in battery chemistry.

The Potential Leaders include BTR New Material Group, Shanshan Corporation, Mitsubishi Chemical Group, and Sumitomo Metal Mining since these organizations are developing competencies in anode materials, performance chemical, and batteries' metal processing owing to growing demand for advanced battery materials. Finally, the Tailenders involve Arkema, which is still playing a role in battery chemicals through participation in binders and performance additives while excluding lithium and cathodes. This company is not dominant in battery chemicals despite growth in the whole battery sector.

Battery Chemicals Market Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Expansion of Battery Gigafactories Increasing Requirement for Advanced Analytical Testing | 5.4% | China, United States, Europe, India, and major battery manufacturing hubs | Battery material validation, quality assurance, impurity analysis, cathode and electrolyte characterization | Strengthens demand for battery-grade chemical testing, quality control frameworks, and material certification to ensure consistency across large-scale battery manufacturing operations |

Rising Adoption of Electric Vehicles and Electrified Transportation | 6.1% | China, Europe, North America, and emerging EV manufacturing markets | Passenger EVs, commercial EVs, electric buses, two- and three-wheelers | Accelerates consumption of lithium chemicals, cathode materials, electrolytes, and advanced battery materials required for large-scale vehicle electrification |

Growing Deployment of Grid-Scale Energy Storage Systems | 4.9% | China, United States, Europe, Australia, and renewable energy-intensive regions | Utility-scale battery storage, renewable energy integration, backup power systems | Increases demand for LFP batteries and associated battery chemicals to support long-duration energy storage and grid stability applications |

Commercialization of Advanced Battery Chemistries and Fast-Charging Technologies | 4.6% | Asia-Pacific battery innovation hubs, North America, and Europe | LFP batteries, sodium-ion batteries, solid-state batteries, fast-charging EV platforms | Supports development of next-generation cathode materials, electrolytes, anode materials, and specialty battery chemicals that enhance battery performance and safety |

Expansion of Battery Gigafactories Increasing Requirement for Advanced Analytical Testing and Quality Validation Standards

The battery materials market is going through major changes as the global capacity to manufacture batteries increases rapidly due to massive investments in gigafactories. According to the data from the International Energy Agency (IEA), by the end of 2025, the global capacity for manufacturing lithium-ion batteries had reached beyond 4 TWh, representing an approximate 30% increase over the previous year, 2024, despite further planned projects in manufacturing batteries. With the rapid increase in production of batteries, there has been an increased need for analyzing, identifying, testing, and characterizing battery materials.

The increasing scale of battery manufacturing facilities is creating greater requirements for standardized testing and quality assurance across the battery value chain. For instance, in September 2025, Reliance Industries announced plans to launch its 40 GWh battery gigafactory in India during 2026. In November 2025, CATL and Stellantis advanced development of their 50 GWh battery gigafactory in Zaragoza, Spain, while in December 2025, Volkswagen commenced battery cell production at its Salzgitter facility in Germany, with a planned annual capacity of 40 GWh. As gigafactories continue to scale production volumes and adopt diverse battery chemistries, manufacturers are increasing investments in material validation, process monitoring, and analytical testing capabilities to maintain product quality and regulatory compliance.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

Rapid Design Evolution in Battery Modules Reducing Standardization | 4.3% | Battery material qualification and supply chain harmonization | Cell-to-pack, cell-to-chassis, LFP, NMC, sodium-ion, and solid-state battery platforms | Increases material customization requirements and complicates standardization across battery manufacturing ecosystems |

Volatility in Critical Raw Material Prices | 4.8% | Battery chemical production costs and procurement planning | Lithium chemicals, nickel, cobalt, manganese, and graphite sourcing | Creates cost uncertainty for battery manufacturers and affects long-term investment and supply agreements |

Stringent Environmental and Regulatory Compliance Requirements | 3.9% | Chemical processing, refining operations, and waste management | Lithium refining, cathode material production, and battery chemical manufacturing | Raises operational costs and increases compliance burdens across battery material supply chains |

Long Qualification Cycles for Battery Materials and Chemistries | 4.1% | Commercialization timelines and product development | New cathode materials, electrolytes, sodium-ion batteries, and solid-state batteries | Delays market entry of advanced battery materials due to extensive testing, validation, and certification requirements from battery manufacturers and automotive OEMs |

Rapid Design Evolution in Battery Modules Reducing Standardization

One of the challenges that the battery chemicals industry may encounter is the fast development of the battery cell, module, and pack structure in EVs and batteries used in energy storage solutions. In addition to new structures like cell-to-pack or cell-to-chassis designs, there are also many types of battery cells, such as high-nickel or LFP, sodium-ion, and even solid-state batteries. Each of them will require unique chemicals to be manufactured.

Moreover, fast changes in designs make testing of these materials more costly since the suppliers have to qualify their products repeatedly and adjust the production process. Also, the lack of unified standards across different types of batteries results in more complications in the supply chain due to the need to address the individual needs of each customer. Hence, fast-paced battery designs may limit the productivity of battery chemicals.

Battery Chemicals Market Segmentation Analysis

The global battery chemicals market is segmented based on product type, battery chemistry, application, and region.

Increasing Use of LFP Batteries in Electric Vehicles and Energy Storage Systems Supporting Segment Dominance

Lithium Iron Phosphate (LFP) Battery Chemistry dominates the battery chemicals market owing to factors such as cost-effectiveness, better thermal stability, increased cycle life, and reduced reliance on nickel and cobalt. There has been an increase in the usage of LFP batteries across applications ranging from electric vehicles, energy storage solutions, commercial vehicle applications, and two-wheeler and three-wheeler vehicles owing to their superior performance and cost-effectiveness when compared with nickel-based batteries.

The continued investment and innovation by leading battery manufacturers also play a part in reinforcing the leadership. For instance, in September 2025, CATL launched its new battery series, named the Shenxing Pro battery series at IAA Mobility 2025. The company claimed the battery to be the first lithium iron phosphate (LFP) battery to be able to deliver a long-term, sustained high voltage supply while maintaining higher levels of safety through thermal runaway prevention. Moreover, the company introduced another LFP battery model which could achieve a WLTP range of 758 kilometers and has a service life of either 12 years or 1,000,000 kilometers. This indicates how fast LFP technology is advancing in EVs.

Battery Chemicals Market Geographical Penetration

Strong Battery Manufacturing Ecosystem and Advanced Material Investments Supporting Asia-Pacific Market Dominance

Asia Pacific leads in the production and consumption of battery chemicals due to the prevalence of battery manufacturing plants, capacity to produce anode and cathode materials in massive quantities, and availability of battery cells producers in China, South Korea, Japan, and other parts of Southeast Asia. The region has an advanced supply chain for the refining of lithium, production of precursors and cathodes, and assembly of batteries, allowing it to quickly commercialize emerging battery technologies. The rise in the production of EVs, energy storage solutions, and the support provided by governments for localized battery material chains has been contributing to the dominant position of Asia Pacific in global battery chemical markets.

The dominance of Asia Pacific in the global battery material market is further enhanced through investments made towards the development of advanced battery materials. For instance, in March 2025, LG Chem revealed that the company will begin the mass production of precursor-free cathode material in South Korea. As a result, the new batteries can be produced using a simple process, which decreases the cost of cathode material manufacturing and eliminates carbon emissions. The company continues to lead in innovation within battery materials technology, especially given increasing demand for battery chemicals.

China Battery Chemicals Market Trends

China maintains its leading position in the battery chemicals market due to its dominance in lithium processing, cathode material production, battery cell manufacturing, and electric vehicle supply chains. The country accounts for a significant share of global battery material refining and battery manufacturing capacity, supported by strong domestic demand, government-backed industrial policies, and the presence of major battery manufacturers. Continuous investments in gigafactories and advanced battery production facilities further reinforce China’s role as the global center for battery chemicals manufacturing and commercialization.

For instance, in May 2025, CATL commenced operations at its battery production base in Shandong, China, with the first phase designed to deliver 60 GWh annual battery production capacity and additional expansion phases planned through 2026. The facility strengthens domestic battery supply chains, increases demand for cathode materials, lithium chemicals, electrolytes, and other battery inputs, and supports China’s continued dominance across the global battery chemicals value chain.

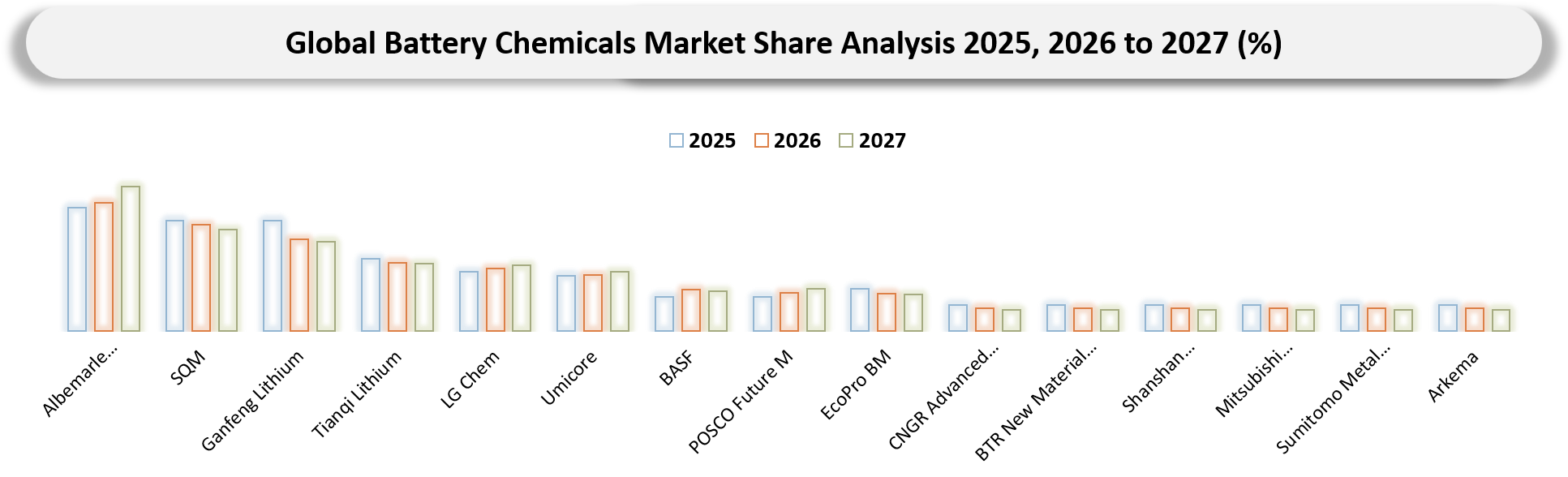

Competitive Landscape

- The market is characterized by three key participant groups: lithium chemical producers and refiners, battery material manufacturers, and specialty chemical suppliers. Albemarle Corporation, SQM, Ganfeng Lithium, and Tianqi Lithium lead the market through large-scale lithium extraction, refining, and battery-grade lithium chemical production; LG Chem, POSCO Future M, EcoPro BM, CNGR Advanced Material, BTR New Material Group, and Shanshan Corporation are prominent suppliers of cathode materials, precursors, and anode materials; while BASF, Umicore, Mitsubishi Chemical Group, Sumitomo Metal Mining, and Arkema focus on advanced battery materials, specialty chemicals, binders, and recycling solutions. This creates a highly integrated market landscape where raw material access, technological innovation, production scale, and strategic partnerships with battery manufacturers determine competitive positioning.

- Key players include Albemarle Corporation, SQM, Ganfeng Lithium, Tianqi Lithium, LG Chem, Umicore, BASF, POSCO Future M, EcoPro BM, CNGR Advanced Material, BTR New Material Group, Shanshan Corporation, Mitsubishi Chemical Group, Sumitomo Metal Mining, and Arkema.

Key Developments

- June 2025: BASF, together with Gotion, China Gas, and BASF Shanshan, formed a strategic partnership for a new-energy ecosystem focused on energy storage systems, next-generation battery materials, and commercialization of clean-energy projects in China.

- July 2025: BASF signed a global cathode active materials framework agreement with CATL, under which BASF will support CATL’s battery manufacturing expansion through its international cathode materials production network.

- August 2025: BASF, through BASF Shanshan Battery Materials, delivered its first mass-produced cathode active materials (CAM) for semi-solid-state batteries to WELION New Energy, supporting the commercialization of next-generation solid-state battery technologies.

- September 2025: BASF renewed a long-term cathode active materials supply agreement for its Schwarzheide facility in Germany, strengthening Europe's localized battery materials supply chain and large-scale cathode production capabilities.

Key Procurement Priorities and Buyer Evaluation Criteria

- Organizations that invest in battery chemicals seek out suppliers who will provide them with highly pure battery-grade materials which are reliable in terms of consistency, supply chain security, and the ability to cater to mass-scale battery manufacturing needs. The procurement of battery chemicals is increasingly focusing on suppliers who can offer highly pure lithium chemicals, cathodes, electrolytes, and anodes, among other components.

- Electric vehicle adoption, grid-scale batteries, and emerging battery technologies are influencing procurement trends. The buyers increasingly seek suppliers who demonstrate high technical proficiency, sustainability, localization, and the ability to meet the needs for emerging battery chemistries such as LFP, high-nickel cathodes, sodium-ion, and solid-state batteries.

- The buyers assess the suppliers' capacity to deliver materials with high purity levels, perform electrochemically, be scalable and reliable in their supplies, have traceable raw material sources, and comply with environmental and regulation standards. Other procurement factors include cost-competitiveness, long-term supply contracts, and the ability to deliver materials of consistent specifications across production batches.

- Battery manufactures and cell producers evaluate their suppliers on the basis of their R&D capabilities, innovation capacity, technical collaboration, customization capabilities, and ability to deliver highly pure batteries with high energy densities and advanced charging capabilities.

Why Choose DataM?

- Battery Technology and Material Innovations: Explores advancements in battery chemicals including high-performance cathode materials, advanced electrolytes, silicon-based anodes, sodium-ion chemistries, and solid-state battery materials, enabling higher energy density, improved safety, faster charging, and longer battery life across electric vehicles and energy storage applications.

- Material Performance & Market Positioning: Evaluates how battery chemical manufacturers differentiate through material purity, energy density enhancement, thermal stability, cycle life improvement, and cost optimization, highlighting competitive advantages across lithium chemicals, cathode materials, anodes, electrolytes, and specialty battery additives.

- Real-World Industry Adoption: Highlights the deployment of battery chemicals across electric vehicles, grid-scale energy storage systems, consumer electronics, industrial equipment, and emerging mobility applications, demonstrating their role in improving battery performance, reliability, and operational efficiency.

- Market Updates & Industry Changes: Tracks key developments including lithium refining expansions, cathode and anode material capacity additions, battery gigafactory investments, next-generation battery chemistry commercialization, and regional supply chain localization initiatives across Asia-Pacific, North America, Europe, and emerging markets.

- Competitive Strategies: Analyzes how leading companies strengthen market positions through lithium resource development, battery material innovation, vertical integration, strategic partnerships, supply agreements, recycling initiatives, and investments in next-generation battery technologies.

- Pricing & Supply Chain Dynamics: Explains pricing trends influenced by lithium, nickel, cobalt, graphite, and electrolyte feedstock costs, while assessing supply chain resilience, raw material availability, sustainability requirements, and evolving procurement strategies across the battery ecosystem.

- Market Entry & Expansion Opportunities: Identifies growth opportunities driven by electric vehicle adoption, renewable energy storage deployment, battery manufacturing expansion, and emerging battery chemistries, while outlining strategies such as regional production expansion, technology differentiation, and strategic partnerships.

Target Audience

- Battery Manufacturers: Cell producers, battery pack manufacturers, and gigafactory operators seeking reliable sources of lithium chemicals, cathode materials, electrolytes, and anode materials.

- Electric Vehicle Manufacturers: Automotive OEMs and EV platform developers requiring advanced battery materials to improve range, safety, charging speed, and overall battery performance.

- Energy Storage Companies: Organizations developing grid-scale and commercial energy storage systems utilizing advanced battery chemistries and battery materials.

- Chemical and Material Suppliers: Producers of lithium compounds, cathode materials, electrolytes, binders, separators, specialty chemicals, and battery raw materials seeking market intelligence and growth opportunities.

- Mining and Resource Companies: Lithium, nickel, cobalt, manganese, graphite, and critical mineral producers supporting global battery material supply chains.

- Government & Regulatory Bodies: Agencies promoting battery manufacturing, energy transition initiatives, critical mineral security, domestic supply chains, and industrial development programs.

- Investors & Private Equity Firms: Stakeholders evaluating opportunities in battery materials, lithium production, battery recycling, energy storage, electric mobility, and next-generation battery technologies.

- Battery Recycling & Circular Economy Companies: Organizations focused on battery material recovery, recycling technologies, resource sustainability, and closed-loop battery supply chains.