Battery Components Market Overview

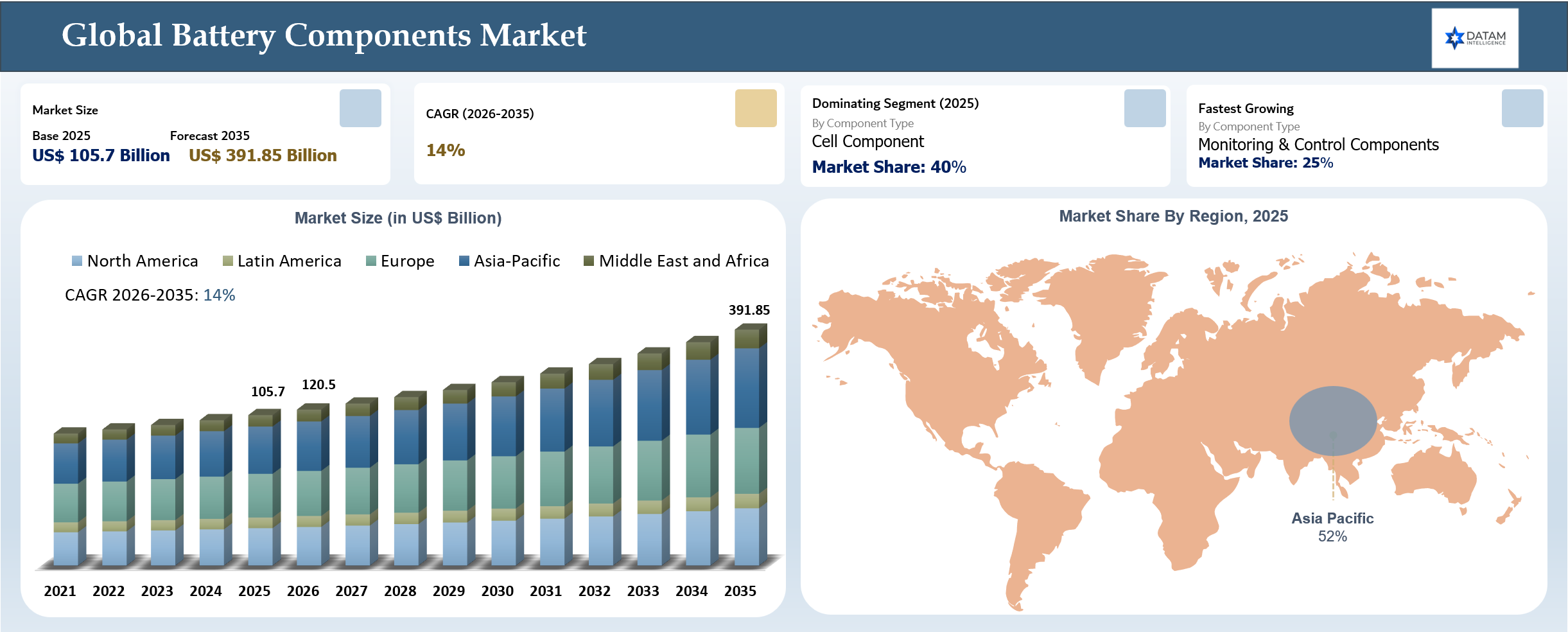

The global battery components market reached US$ 105.7 billion in 2025 and is expected to reach US$ 391.85 billion by 2035, growing with a CAGR of 14% during the forecast period 2026-2035. The battery chemicals market is witnessing robust growth owing to increased electric vehicle uptake, energy storage installation, and battery production investments globally. Lithium chemicals, cathode materials, electrolyte materials, anode materials, and speciality additives are experiencing growing demand as companies look for greater energy density, faster charging capability, and safer batteries. Market growth is being further stimulated through the expansion of battery gigafactories and localisation initiatives within leading markets. In May 2025, for instance, POSCO Future M developed mass production capabilities of silicon anode materials in order to support the production of high-energy-density next-generation batteries.

Key Takeaways

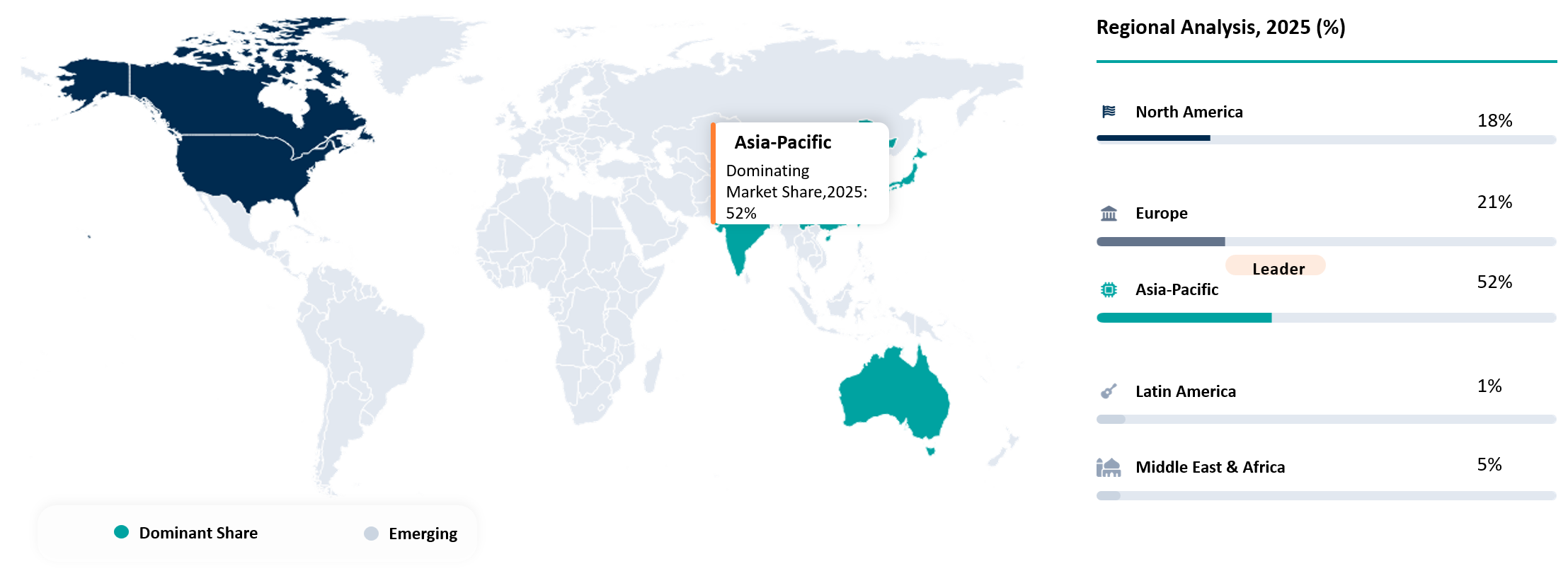

- Asia-Pacific is dominating the global battery chemicals market, accounting for a share of 61.2% in 2025.

- In 2025, cell components type led the market with a share of approximately 40%.

- Monitoring and control components are the fastest-growing product type in 2025, with market share of 25%.

- Battery components growth in 2025 is heavily anchored in electric vehicles, with EVs contributing most of the lithium-ion battery deployment and upstream components like cathodes and cells capturing dominant market shares. This makes OEMs and EV supply chains the primary demand engine, driving rapid scale-up of cathode, electrolyte, and structural component production.

- Localization of battery chemical supply chains is increasing rapidly across North America and Europe to reduce dependency on China-dominated refining and precursor processing capacity.

- Sodium-ion and solid-state battery development is creating demand for next-generation electrolyte and coating chemistries.

Battery Components Industry Trends and Strategic Insight

- The battery components industry is witnessing a strong shift toward advanced EV architectures such as cell-to-pack (CTP), cell-to-chassis (CTC), and structural battery pack designs, driven by the need for higher energy density, reduced weight, and improved vehicle efficiency. This transition is reducing dependence on conventional module-level components such as housings, frames, and intermediate structural parts while increasing demand for integrated structural materials and multifunctional components. Companies such as Bosch and Continental AG are advancing integrated battery systems and electronic control solutions to support next-generation EV platforms.

- The industry is increasingly moving toward smart, sensor-driven, and software-enabled battery systems, with companies including Infineon Technologies, Analog Devices, and Sensata Technologies strengthening capabilities in battery management systems (BMS), power electronics, and real-time monitoring technologies. This shift is enhancing battery safety, performance optimization, and predictive maintenance across electric vehicles and energy storage systems while increasing the importance of semiconductor-based and electronic components within the battery value chain.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 105.7 Billion | |

| 2035 Projected Market Size | US$ 391.85 Billion | |

| CAGR (2026-2035) | 14% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Component Type | Cell Components, Module & Pack Components, Monitoring & Control Components | |

| By Battery Type | Lithium-ion Battery, Sodium-ion Battery, Solid-state Battery, Lead-acid Battery, Nickel-based Battery, Flow Battery, Others | |

| By Cell Therapy | Cylindrical, Prismatic, Pouch, Coin Cell, Others | |

| By Application | Automotive, Energy Storage Systems (ESS), Consumer Electronics, Industrial Equipment, Medical Devices, Aerospace & Defense, Telecommunications, Marine, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

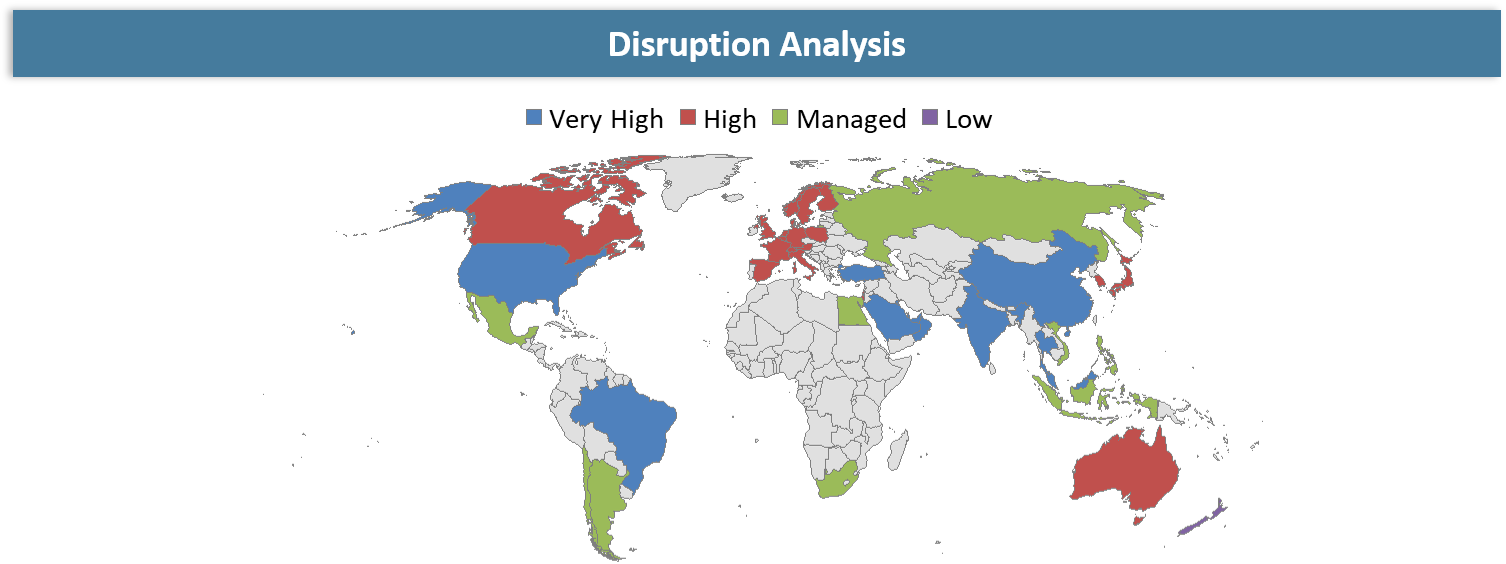

Disruption Analysis

Structural Battery Packs Reducing Conventional Module Component Demand

Disruption is evident in the battery component market due to new technology known as structural battery pack systems. The technology involves building the battery pack system into the structural system of the automobile itself without the use of module casing. The innovation does away with the need for module housing, frames, thermal interface material, and other intermediate structural parts. It is therefore clear that conventional battery packs require less component input from the market, leading to declining sales of such parts.

Moreover, the design of structural battery packs is largely propelled by electric vehicle manufacturers looking to minimize vehicle weight and maximize energy density as well as optimize space. Such firms include Tesla which is developing cell-to-chassis batteries along with other integrated designs that have the benefit of simplifying parts while at the same time optimizing efficiencies in the process. As a result, established providers of battery pack parts are facing disruption as they become increasingly reliant on multifunctional components.

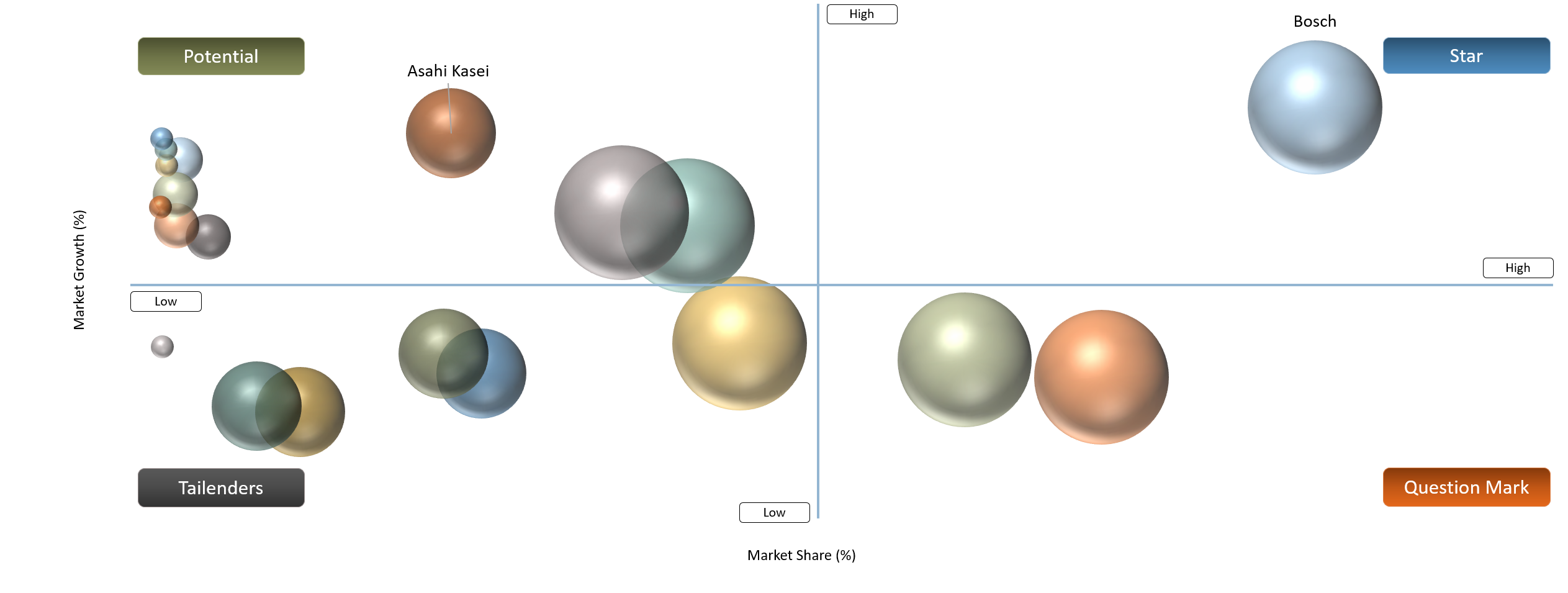

BCG Matrix: Company Evaluation

The battery component industry is composed of material providers, separator manufacturers, automotive systems integrators, and semiconductor-based battery electronics providers. Stars include Bosch, Continental AG, Valeo, and Hanon Systems since they have a strong position in EV thermal management systems and battery-integration platforms, as well as technologies that align with large-scale OEMs' needs for electrification. Question Marks include Infineon Technologies, Analog Devices, Sensata Technologies, and TE Connectivity because these firms contribute significantly to battery management systems, sensing, and power electronics but still depend on the integration of new EV architectures. These players expand their portfolio in terms of electrification but are uncertain about gaining dominance within the battery components segment.

The Potential includes Asahi Kasei, Toray Industries, Celgard, and UBE Corporation owing to the dominant positions in separators, polymers, and battery chemicals. These are important but highly dependent on battery manufacturer requirements and chemistry development. Tailenders include less prominent players or those that focus on other industrial segments instead of battery component development.

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Rising EV adoption driving battery component demand | 6.1% | China, Europe, North America, and emerging EV manufacturing markets | EV battery packs, BMS systems, thermal management, power electronics | Accelerates demand for advanced battery components including sensors, separators, connectors, and thermal systems |

Growth of energy storage systems supporting component usage | 4.9% | China, United States, Europe, Australia | Grid-scale storage, renewable integration, backup power systems | Increases requirement for durable and high-efficiency battery components for long-duration storage applications |

Increasing integration of smart battery management systems | 4.5% | Global EV platforms, automotive OEM clusters, and electronics manufacturers | Battery monitoring systems, predictive diagnostics, safety control modules | Enhances demand for semiconductor-based components and intelligent sensing systems in battery packs |

Expansion of high-performance electronics in EV platforms | 4.3% | North America, Europe, China, South Korea | Advanced EV electronics, ADAS systems, connected mobility platforms | Drives adoption of high-precision connectors, control units, and electronic battery control components |

Rising EV Adoption and Shift Toward BEVs Driving Demand for Advanced Battery Components

Rising electric vehicle adoption is significantly accelerating demand for advanced battery components such as battery management systems, sensors, connectors, and power electronics. According to the International Energy Agency (IEA), in 2025 battery electric cars strengthened their dominance, with BEVs accounting for around 65% of total electric car sales, marking a clear shift back toward full battery-electric platforms. This increasing dominance of BEVs is expanding the need for complete battery systems and thereby boosting demand for integrated electronic control and safety components across EV architectures.

Companies are also accelerating innovation in battery electronics to support this shift toward full electrification and higher system complexity. For instance, in July 2025, NXP Semiconductors launched its 18-channel lithium-ion battery cell controller IC family (BMx7318/7518) designed for EV battery management systems and energy storage applications. NXP BMx7318/7518 launch. The solution improves cell-level monitoring accuracy, enhances safety compliance (ASIL-C), and reduces external component count by integrating multiple functions into a single IC. This reflects the broader industry transition toward highly integrated, semiconductor-driven battery architectures that support next-generation EV performance, efficiency, and scalability.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

Complex battery architectures limit standardization | 4.3% | Battery pack design and component integration | Cell-to-pack, cell-to-chassis, structural battery packs | Reduces compatibility of standard components and increases customization requirements across OEM platforms |

Volatile raw material and electronics pricing affecting supply stability | 4.8% | Component manufacturing and procurement | Sensors, connectors, thermal systems, power electronics | Creates cost uncertainty and disrupts long-term supply agreements for battery component manufacturers |

Stringent safety and regulatory compliance requirements | 3.9% | Battery system certification and quality control | EV battery safety systems, thermal management, electrical protection components | Increases compliance costs and lengthens product validation cycles |

Long design and qualification cycles for new battery systems | 4.1% | Product development and commercialization timelines | Next-generation EV platforms, advanced BMS, integrated battery systems | Delays adoption of innovative components due to extended testing and OEM validation requirements |

Complex battery architectures limit standardization

The rapid evolution of battery architectures such as cell-to-pack (CTP), cell-to-chassis (CTC), and structural battery pack designs is significantly limiting standardization in the battery components market. In 2025, OEMs and battery manufacturers are increasingly adopting customized designs to achieve higher energy density, lower weight, and improved vehicle efficiency, which is reducing the use of uniform module-level components. This fragmentation across platforms is making it difficult for suppliers to scale standardized battery components across different EV and energy storage applications.

This shift is also increasing engineering complexity and customization requirements for key battery components such as connectors, thermal systems, separators, and battery management integration units. For instance, companies developing EV platforms are increasingly moving toward integrated designs that combine multiple functions within the battery pack, reducing interchangeability of components across OEMs. As a result, battery component suppliers face higher design variability, longer qualification cycles, and increased development costs, which collectively restrain large-scale standardization and slow down commercialization efficiency.

Segmentation Analysis

The global battery components market is segmented based on component type, battery type, cell format, application and region.

Increasing Use of Advanced Cathode Materials in EV Batteries Supporting Cell Components Dominance

Cell Components dominate the battery components market due to their fundamental role in enabling electrochemical energy storage, with strong demand for cathode materials, anode materials, separators, and cell casings. Rapid expansion of electric vehicles and energy storage systems is significantly increasing the consumption of high-performance cell-level materials, particularly lithium-based cathode systems that enhance energy density, safety, and lifecycle performance. The shift toward next-generation chemistries such as high-nickel, LFP, and precursor-free cathode systems is further strengthening the dominance of this segment in the overall battery value chain.

For instance, in 2025, LG Chem began mass production of precursor-free cathode materials, designed to simplify the cathode manufacturing process while improving cost efficiency and performance stability in lithium-ion batteries. LG Chem precursor-free cathode materials development This development reflects the growing industry focus on optimizing cathode active materials, which are a core part of cell components. Such innovations directly support higher energy density EV batteries and reinforce the dominance of cell-level materials in next-generation battery architectures.

Geographical Penetration

Strong Asia-Pacific Manufacturing Expansion and Integrated EV Battery Ecosystem Driving Regional Dominance

Asia-Pacific continues to dominate the global battery components market due to its deeply integrated EV battery manufacturing ecosystem, strong upstream material supply chains, and large-scale production of battery cells and packs. The region—particularly China, South Korea, and Southeast Asia—benefits from high concentration of EV manufacturers, battery gigafactories, and vertically integrated players, enabling efficient production of critical cell components such as cathodes, anodes, separators, and electrolyte systems. This strong industrial base supports rapid commercialization of advanced battery chemistries, making Asia-Pacific the global hub for both production and consumption of battery components.

For instance, in 2025, CATL broke ground on a new battery manufacturing facility in Indonesia, marking a significant expansion of its Southeast Asia footprint and strengthening regional supply chain integration for EV batteries. CATL Indonesia battery plant This development highlights CATL’s strategy to expand production capacity beyond China while reinforcing Asia-Pacific’s dominance in cell manufacturing and battery component supply. Such large-scale investments in regional gigafactories directly increase demand for core cell components, supporting the continued leadership of Asia-Pacific in the global battery components market.

For instance, in May 2025, CATL commenced operations at its battery production base in Shandong, China, with the first phase designed to deliver 60 GWh annual battery production capacity and additional expansion phases planned through 2026. The facility strengthens domestic battery supply chains, increases demand for cathode materials, lithium chemicals, electrolytes, and other battery inputs, and supports China’s continued dominance across the global battery chemicals and components value chain.

Competitive Landscape

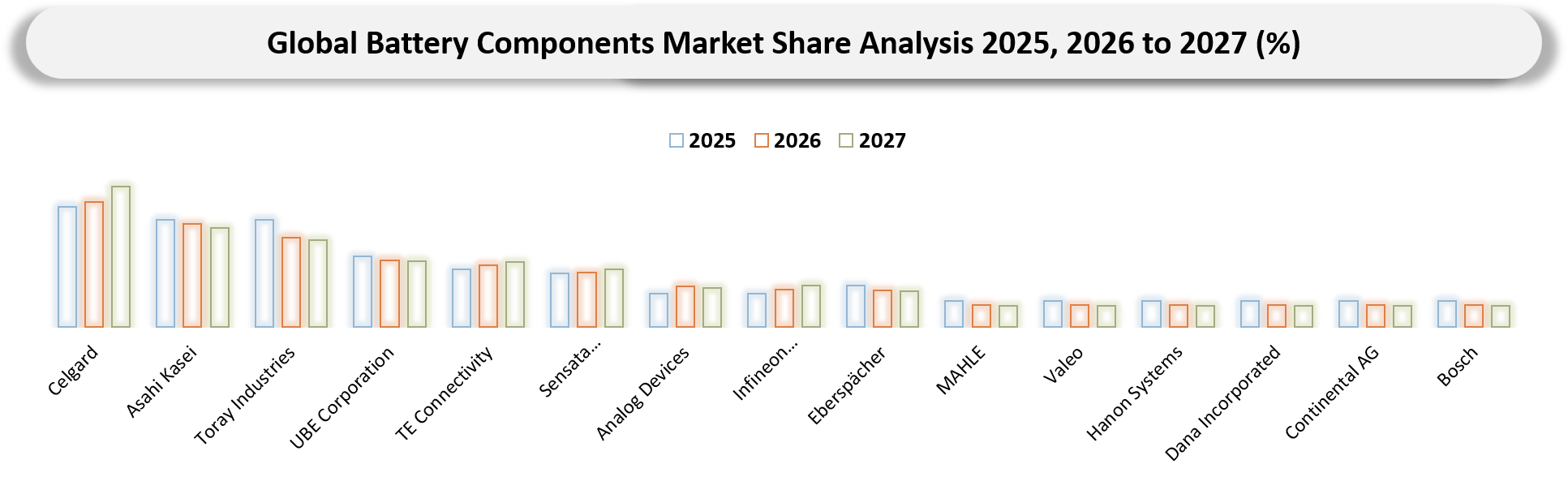

- Key players include Celgard, Asahi Kasei, Toray Industries, UBE Corporation, TE Connectivity, Sensata Technologies, Analog Devices, Infineon Technologies, Eberspächer, MAHLE, Valeo, Hanon Systems, Dana Incorporated, Continental AG, and Bosch.

Key Developments

- October 2025: NXP introduced an advanced battery health monitoring EIS chipset designed to improve real-time battery diagnostics and state-of-health estimation for electric vehicles and energy storage systems, enhancing accuracy and lifecycle performance management.

- November 2025: Infineon launched the PSoC™ 4 HVPA-SPM 1.0 microcontroller, designed for advanced automotive battery management systems, enabling zonal architectures through integrated edge intelligence, precision analog measurement, and reduced central ECU load in electric vehicle platforms.

- May 2025: Infineon announced a collaboration with NVIDIA to develop an 800 V HVDC power delivery architecture for next-generation AI data center racks, aimed at improving energy efficiency and scalable power distribution across high-performance computing infrastructure.

- July 2025: BASF signed a global cathode active materials framework agreement with CATL, under which BASF will support CATL’s battery manufacturing expansion through its international cathode materials production network.

Key Procurement Priorities and Buyer Evaluation Criteria

- Organizations investing in battery components prioritize suppliers capable of delivering high-precision, high-reliability parts such as separators, electrodes, current collectors, battery management systems (BMS), sensors, connectors, thermal management components, and power electronics, along with battery-grade chemicals. A strong emphasis is placed on material purity, electrochemical stability, and consistency across large-scale EV and energy storage production.

- Electric vehicle expansion, grid-scale storage deployment, and next-generation battery architectures are reshaping procurement priorities. Buyers increasingly prefer suppliers that can support advanced battery system integration, including thermal management systems, HV components, BMS chips, separators, and interconnect solutions, while enabling compatibility with LFP, high-nickel, sodium-ion, and solid-state platforms.

- Procurement decisions are strongly driven by performance validation, safety compliance, traceability, and scalability. Buyers evaluate suppliers based on reliability under high charge-discharge cycles, thermal resistance, fast-charging compatibility, defect control, and adherence to global automotive and energy storage regulatory standards, alongside cost efficiency and long-term supply security.

- Battery manufacturers and EV OEMs also assess suppliers based on R&D strength, co-development capability, system integration support, customization flexibility, and ability to deliver components that enhance energy density, safety, thermal efficiency, and battery lifespan across next-generation platforms.

Why Choose DataM?

- Battery Technology and Material Innovations: Covers advancements in battery separators, cathode/anode structures, electrolytes, silicon-based materials, BMS systems, sensors, connectors, thermal management systems, and HV semiconductor integration, enabling higher energy density, improved safety, faster charging, and longer lifecycle performance across EV and energy storage systems.

- Material Performance & Market Positioning: Evaluates differentiation across separators (porosity, shutdown safety), electrodes (conductivity, stability), BMS chips (accuracy, intelligence), power electronics (efficiency, switching losses), and thermal systems (heat dissipation, reliability), highlighting competitive advantages across the battery value chain.

- Real-World Industry Adoption: Highlights deployment across electric vehicles, grid-scale storage systems, consumer electronics, industrial energy systems, and aerospace applications, where advanced battery components improve safety, efficiency, thermal stability, and system integration.

- Market Updates & Industry Changes: Tracks developments including gigafactory expansion, separator capacity additions, BMS semiconductor innovation, HV architecture integration, battery pack modularization, and localization of supply chains across Asia-Pacific, Europe, and North America.

- Competitive Strategies: Analyzes how leading companies strengthen positions through vertical integration, semiconductor-battery convergence, thermal system innovation, strategic partnerships with OEMs, and investments in intelligent battery system architectures.

- Pricing & Supply Chain Dynamics: Explains cost structures influenced by raw materials, semiconductor content, precision manufacturing, and logistics, while assessing supply chain resilience, localization strategies, and sustainability-driven procurement shifts.

- Market Entry & Expansion Opportunities: Identifies growth opportunities driven by EV penetration, energy storage scaling, advanced battery chemistries, and smart battery systems, with strategies including regional manufacturing, technology partnerships, and system-level integration capabilities.

Target Audience

- Battery Manufacturers: Cell and pack producers requiring advanced separators, electrodes, electrolytes, thermal systems, BMS, and interconnect components.

- Electric Vehicle Manufacturers: OEMs and EV platform developers integrating high-performance battery packs and intelligent battery management systems.

- Energy Storage Companies: Developers of grid-scale and commercial storage systems requiring reliable, safe, and scalable battery component ecosystems.

- Semiconductor and Electronics Companies: Suppliers of BMS chips, power semiconductors, sensors, and control systems for smart battery architectures.

- Automotive Component Suppliers: Manufacturers of thermal management systems, connectors, enclosures, and power distribution units for EV battery packs.

- Chemical and Material Suppliers: Producers of cathode/anode materials, separators, electrolytes, binders, and specialty additives for battery production.

- Mining and Resource Companies: Suppliers of lithium, nickel, cobalt, graphite, and other critical minerals supporting battery component manufacturing.

- Government & Regulatory Bodies: Agencies supporting EV transition, energy storage deployment, and critical material supply chain security.

- Investors & Private Equity Firms: Stakeholders focused on battery technology, EV ecosystem, semiconductor-battery convergence, and energy storage innovation.

- Battery Recycling & Circular Economy Companies: Firms engaged in recovery and reuse of battery materials and components for sustainable supply chains.