Pharmaceuticals Market Size

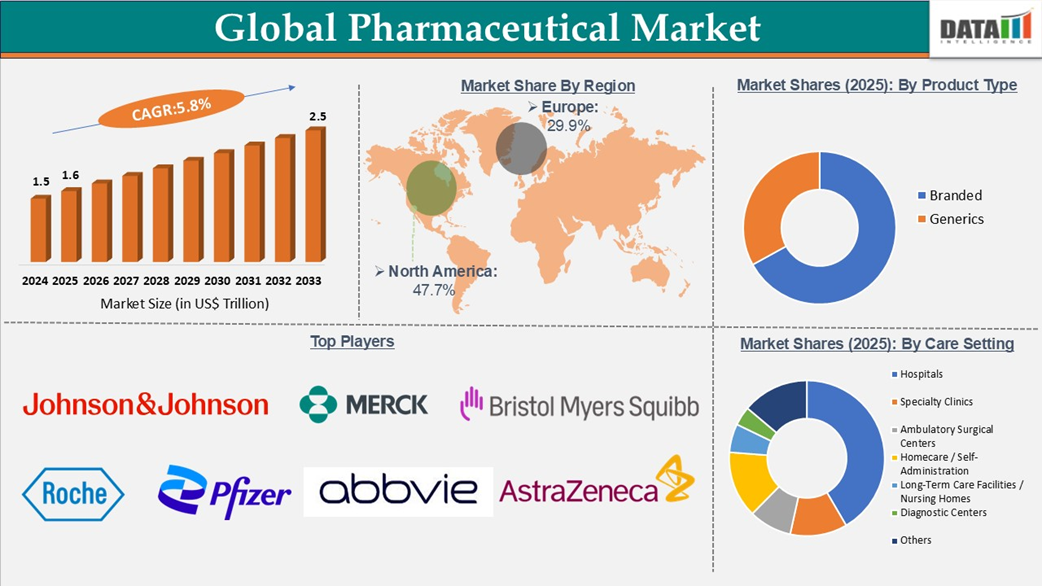

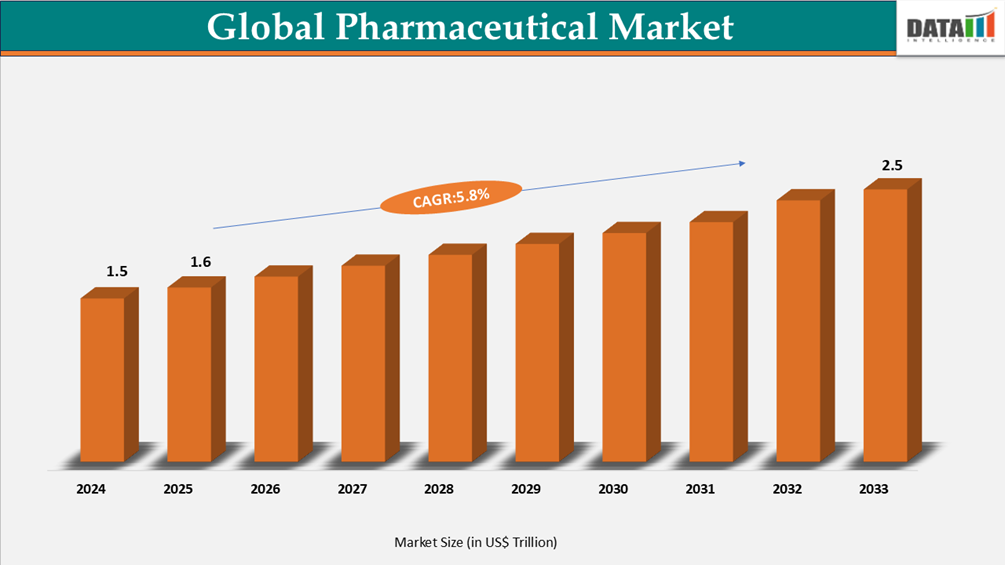

The Pharmaceuticals Market will reach US$ 1.69 trillion in 2026, up from US$ 1.60 trillion in 2025, and is projected to reach US$ 2.80 trillion by 2035, registering steady growth at a CAGR of 5.8% during the forecast period from 2026 to 2035.

The market is anticipated to rise steadily due to factors such as an aging population, an increase in the frequency of chronic illnesses, and a growing need for sophisticated therapies in hospitals, specialized clinics, and homecare settings. Global pharmaceutical leaders are concentrated in North America, which facilitates the quick commercialization of novel medications and vaccines. Long-term market stability is also being supported by government programs targeted at bolstering domestic medication production, supply chain resilience, and crucial pharmaceutical availability. Johnson & Johnson and the US government signed a voluntary agreement in January 2026 to reduce the cost of medications for millions of Americans. The agreement also included USD 55 billion in investments in U.S. pharmaceutical manufacturing and innovation, including two new facilities in North Carolina and Pennsylvania.

Pharmaceuticals Industry Trends and Strategic Insights

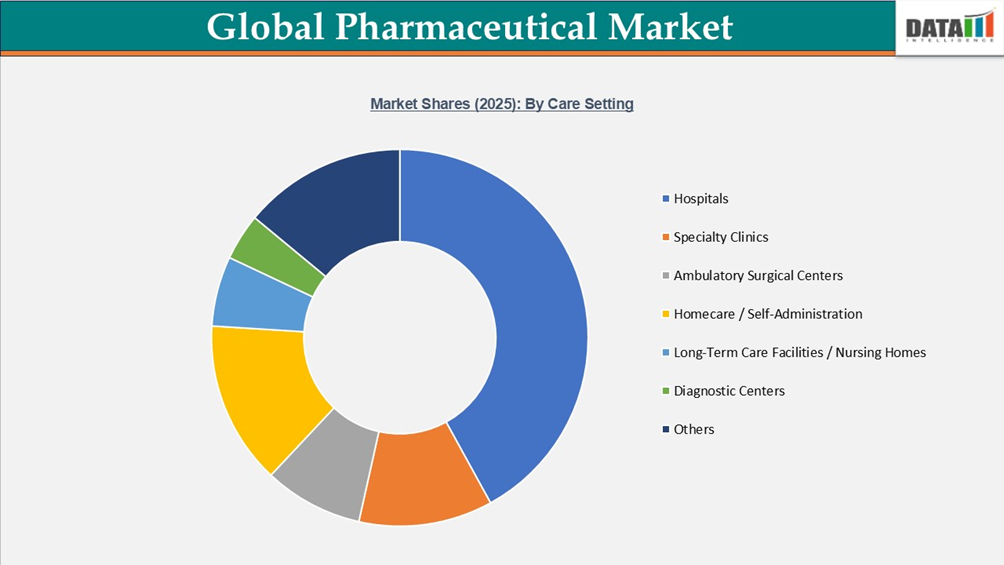

- By Care Setting, the hospitals segment is projected to be the largest market, holding a significant share of 42% in 2025.

Global Pharmaceuticals Market Size and Future Outlook

- 2026 Market Size: US$ 1.69 trillion

- 2035 Projected Market Size: US$ 2.80 trillion

- CAGR (2026-2035): 5.8%

- Largest Market: North America

Fastest Market: Asia-Pacific

Source: DataM Intelligence

For More Detailed information Request for Sample

Key Takeaways

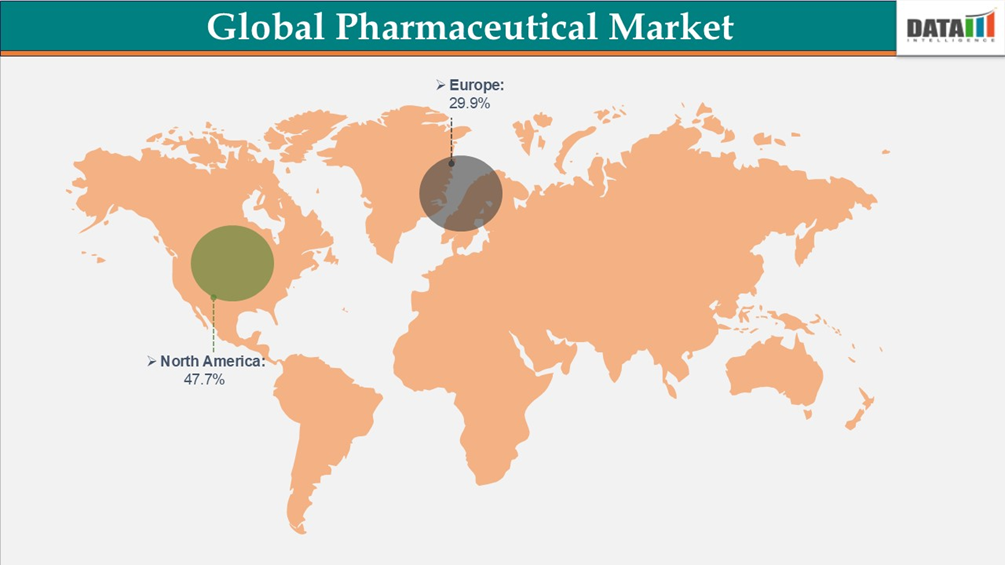

- North America accounts for approximately 49% of the global market, supported by high healthcare spending, strong R&D investments, and rapid adoption of innovative therapies.

- Asia-Pacific is the fastest-growing regional market, driven by expanding healthcare infrastructure, increasing pharmaceutical manufacturing, and rising demand for affordable medicines.

- Small-molecule drugs continue to account for over 55% of global pharmaceutical revenue, while biologics and advanced therapies are experiencing the fastest growth.

- Oncology remains the largest therapeutic segment, contributing over 18% of global pharmaceutical sales, fueled by continuous innovation in targeted therapies and immuno-oncology.

- Growing prevalence of chronic diseases is increasing demand for innovative pharmaceuticals worldwide.

- Rising investments in biologics, biosimilars, gene therapies, and personalized medicine are transforming the pharmaceutical landscape.

- Artificial intelligence and digital technologies are accelerating drug discovery, clinical trials, and manufacturing efficiency.

- Expansion of specialty pharmaceuticals and orphan drugs is creating new revenue opportunities for manufacturers.

- Increasing adoption of contract development and manufacturing organizations (CDMOs) is improving production scalability and reducing development timelines.

- Regulatory agencies continue to accelerate approvals for breakthrough therapies addressing unmet medical needs.

- Sustainable manufacturing practices and digital supply chain optimization are becoming strategic priorities across the pharmaceutical industry.

Analyst Viewpoint

The Pharmaceuticals Market continues to expand as global healthcare systems prioritize innovative treatments, precision medicine, and improved patient outcomes. Growth is being driven by increasing disease prevalence, aging populations, expanding healthcare access, and continuous pharmaceutical innovation.

Major pharmaceutical companies are investing heavily in biologics, cell and gene therapies, mRNA technologies, AI-driven drug discovery, and digital manufacturing. Organizations that successfully combine scientific innovation with efficient commercialization strategies are expected to maintain long-term market leadership.

Pharmaceuticals Market Scope

| Metrics | Details |

| By Molecule Type / Product Modality | Small Molecules (Conventional Drugs), Large Molecules (Biologics), Biosimilars, Advanced Therapies |

| By Product Type | Branded, Generics |

| By Prescription Type | Prescription, Over-the-Counter |

| By Therapeutic Area / Disease Class | Oncology, Cardiovascular Diseases, Metabolic Diseases, Immunology & Autoimmune Diseases, Infectious Diseases, Neurology, Mental Health Disorders (Psychiatry), Respiratory Diseases, Gastrointestinal Disorders, Women’s Health Diseases, Men’s Health / Urology, Dermatological Conditions, Ophthalmology (Eye Conditions), Hematological Disorders, Endocrine Disorders, Renal Diseases, Liver Conditions, Musculoskeletal Disorders / Pain Management, Allergy & Immunology (Allergies), Genetic & Rare Diseases (Orphan), Dental / Oral Health (optional), Others |

| By Route of Administration | Oral, Parenteral, Topical / Dermal, Inhalation, Ophthalmic, Transdermal, Rectal, Vaginal, Buccal / Sublingual, Intrathecal / CNS Delivery (niche), Others |

| By Dosage Form | Tablets, Capsules, Powders / Granules, Liquids, Injectables, Inhalers, Topicals, Drops (Ophthalmic / Otic), Suppositories, Sprays (Nasal/Oral), Implants (niche), Others |

| By Age Group | Children & Adolescents, Adults, Geriatric |

| By Distribution Channel | Hospital Pharmacy, Retail Pharmacy, Online Pharmacy / E-Pharmacy, Specialty Pharmacy, Clinic Pharmacy / Physician Dispensing, Government / Public Procurement & Tenders, Wholesalers & Distributors, Others |

| By Care Setting | Hospitals, Specialty Clinics, Ambulatory Surgical Centers, Homecare / Self-Administration, Long-Term Care Facilities / Nursing Homes, Diagnostic Centers, Others |

| By Region | North America, Latin America, Europe, Asia-Pacific, Middle East and Africa |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth |

Pharmaceuticals Market Dynamics

Changing food habits and sedentary lifestyle increase chronic and lifestyle diseases

Lifestyle-related illnesses have become more prevalent worldwide in recent years, mostly as a result of increasing stress, bad eating habits, and decreased physical exercise. One of the health issues with the quickest rate of growth is diabetes, which currently affects 537 million adults worldwide and is predicted to increase to 783 million by 2045. The majority of diabetics reside in low- and middle-income nations, and in 2021, the condition resulted in 6.7 million fatalities and approximately USD 966 billion in medical expenses. Heart attacks and strokes contribute to 17.9 million fatalities, or almost one-third of all deaths globally, from cardiovascular illnesses, which remain the leading cause of mortality. By 2030, the economic cost of these circumstances is expected to exceed $1 trillion annually. With 890 million individuals categorized as obese and 2.5 billion overweight, obesity has also grown pervasive. By 2035, it is predicted that over 3 billion people may be overweight or obese, with an estimated USD 2 trillion in economic effect. In addition to physical ailments, mental health disorders impact more than 1 billion people globally, account for about 800,000 suicide deaths annually, and cause USD 1 trillion in lost productivity, demonstrating the increasing strain that lifestyle-related diseases are placing on economies and health systems around the world.

Patent expirations and generic competition (patent cliff)

One of the key restraints in the global pharmaceuticals market is the patent expirations and generic competition. The field of oncology is anticipated to be among the most affected, since top medications like Johnson & Johnson's Darzalex/Faspro and Merck's Keytruda are anticipated to lose their US exclusivity by 2029. By 2030, such drugs are predicted to continue to be among the best-selling medications, but as competition increases their earnings are predicted to drop.

Segmentation Analysis

The global pharmaceuticals market is segmented based on the Molecule type / Product modality, Product type, Prescription type, Therapeutic area/Disease class, Route of administration, Dosage form, Age group, Distribution channel, Care setting and region.

Rising Shift Toward Hospital-Based Treatment Drives Segment Growth

Hospitals as a care setting are expected to hold about 42% of the global market in 2025. High-value medications, such as injectables, biologics, cancer therapies, antibiotics, and critical care medicines, are most often used in hospitals for inpatient treatment, emergency care, and surgical operations. A growth in the number of patients admitted to hospitals, an increase in the number of complicated surgical procedures, an expansion of critical care units, and an increase in the incidence of diseases such as cancer, infectious diseases, and cardiovascular diseases are all factors that are contributing to an increase in the demand for pharmaceuticals in hospital settings.

Growing Preference for Homecare and Outpatient Settings Accelerates Market Expansion

The shift toward homecare, self-administration, and ambulatory care settings is accelerating pharmaceutical demand as healthcare systems prioritize cost reduction, patient comfort, and long-term illness treatment. The advent of oral medications, self-injectable treatments, and remote monitoring technologies has allowed patients to obtain treatment outside of traditional hospitals, resulting in quicker development in the outpatient and home-based care sectors.

The AHA (American Hospital Association) endorses the cost-effectiveness of hospital-at-home programs, noting that Johns Hopkins Medicine claims savings of 19%-30% when compared to in-patient treatment.

Geographical Penetration

Presence of Advance Industrial Infrastructure in North America

North America is expected to be a significant region of the global market, holding about 47.7%of the market in 2025. The market in the region is helped by improved infrastructure for making pharmaceuticals, a strong regulatory framework, and a strong research and development environment, especially in the US and Canada. Large drug factories, biologics plants, and clean injectable production units help keep pharmaceutical output steady and speed up the release of new treatments to the market.

U.S. Pharmaceuticals Market Insights

The U.S. accounts for the largest share of the North American pharmaceuticals market, driven primarily by high healthcare expenditure, strong insurance coverage, and rapid adoption of innovative medicines. Specialized medications, biologics, and advanced treatments are in high demand in the United States due to outpatient care settings, specialized clinics, and hospitals. The nation's thriving biotechnology industry and significant investments in pharmaceutical R&D are driving market expansion, especially in the areas of immunotherapy, cancer, and rare disorders.

Canada Pharmaceuticals Industry Growth

In Canada, the pharmaceutical market is smaller compared to the U.S. but remains important due to its universal healthcare system and stable demand for prescription medicines. Pharmaceuticals are widely used in the nation to treat chronic illnesses, such as diabetes, neurological disorders, and cardiovascular diseases. Additionally, Canada promotes clinical research and pharmaceutical manufacturing, especially in areas like Ontario and Quebec that are home to important production facilities and life sciences clusters. Government programs to promote access to necessary medications and bolster the domestic drug supply also support consistent market expansion.

Sustainability Analysis

The global pharmaceutical sector is rapidly incorporating sustainability into key business strategies, as businesses strive to combine medication innovation with environmental and social responsibility. Pharmaceutical manufacturers are projected to accelerate the use of energy-efficient production techniques, green chemistry, and waste-reduction measures in order to reduce carbon emissions and increase resource efficiency.

In FY 2025, Piramal's 240 kWp rooftop solar system produced 607 GJ of renewable energy and reduced onsite emissions by 123 tCO₂e, demonstrating significant advances in energy efficiency and carbon reduction.

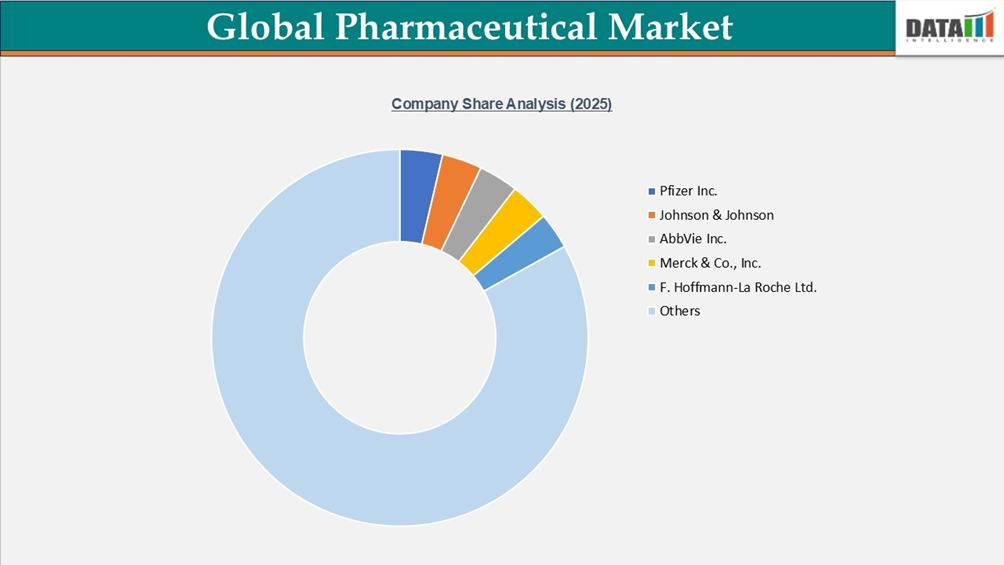

Competitive Landscape

- The global pharmaceuticals market is characterized by a competitive landscape that includes both large multinational pharmaceutical companies and specialized biotechnology firms, operating across branded, generic, and specialty drug segments

Key players include:

Johnson & Johnson (J&J), F. Hoffmann-La Roche Ltd, Merck & Co., Inc., Pfizer Inc., AbbVie Inc., AstraZeneca, Novartis AG, Bristol-Myers Squibb Company, Eli Lilly and Company, Sanofi, Novo Nordisk A/S, GSK plc, Amgen Inc., Takeda Pharmaceutical Company Limited, Boehringer Ingelheim International GmbH, Gilead Sciences, Inc., Bayer AG, Merck KGaA, Teva Pharmaceutical Industries Ltd., Daiichi Sankyo Company, Ltd., and Biogen.

- The above companies concentrate on product differentiation by developing novel drug formulations, biologics, targeted treatments, and specialty medicines, particularly in high-growth therapeutic areas including cancer, immunology, cardiovascular disease, and rare illnesses.

- As pharmaceutical companies deal with growing competition from generic drugs, biosimilars, and alternative treatment approaches, as well as pricing pressures and regulatory scrutiny, strategic investments in R&D, sustainability initiatives, digital manufacturing, and supply-chain efficiency are becoming more and more important.

Key Developments

- June 2026 - Eli Lilly and Company: Announced positive Phase 3 clinical trial results for its next-generation obesity treatment, supporting future regulatory submissions.

- June 2026 - Novo Nordisk A/S: Expanded manufacturing capacity for GLP-1 medicines to meet increasing global demand for obesity and diabetes treatments.

- June 2026 - Pfizer Inc.: Received regulatory approval for a new indication expanding the use of one of its oncology therapies.

- May 2026 - Merck & Co., Inc.: Announced positive late-stage clinical trial data for an investigational vaccine, reinforcing its infectious disease pipeline.

- May 2026 - AstraZeneca: Entered a strategic collaboration to accelerate the development of AI-enabled precision medicines for oncology and rare diseases.

- April 2026 - Johnson & Johnson (J&J): Received regulatory approval for an expanded indication of a key immunology therapy, broadening treatment options for autoimmune diseases.

- April 2026 - Roche: Reported positive Phase 3 results for a neuroscience drug candidate, advancing its pipeline for neurological disorders.

- March 2026 - GSK plc: Launched a next-generation respiratory treatment in selected global markets following regulatory approvals.

Latest Industry Intelligence & Future Growth Catalysts (2026)

Biologics Continue Rapid Expansion

Biologic medicines, monoclonal antibodies, and advanced therapies continue to capture a growing share of pharmaceutical revenues.

AI Accelerates Drug Discovery

Artificial intelligence is reducing research timelines while improving target identification and clinical success rates.

Personalized Medicine Gains Momentum

Precision therapies based on genetic and molecular profiling are improving treatment effectiveness across multiple disease areas.

Cell and Gene Therapies Expand

Commercialization of advanced therapies is creating significant opportunities in oncology and rare disease treatment.

Digital Manufacturing Improves Efficiency

Automation, digital quality systems, and continuous manufacturing are improving pharmaceutical production and supply chain resilience.

Biosimilar Adoption Increases

Growing biosimilar approvals are improving patient access while reducing healthcare costs.

Emerging Markets Drive Future Demand

Expanding healthcare infrastructure and increasing pharmaceutical access across emerging economies continue to support long-term growth.

Market Opportunities and Investment Hotspots

Key investment opportunities include:

- Biologics and biosimilars

- Oncology therapeutics

- Cell and gene therapies

- mRNA technologies

- Rare disease treatments

- Vaccine development

- AI-powered drug discovery

- Contract development and manufacturing (CDMO)

- Digital pharmaceutical manufacturing

Companies investing in precision medicine, advanced biologics, digital transformation, and innovative therapeutic platforms are expected to benefit from sustained market expansion.

Strategic Questions Answered by This Report

This report evaluates technological innovations, regulatory developments, competitive dynamics, therapeutic advancements, and investment opportunities shaping the Pharmaceuticals Market. It analyzes demand across molecule types, therapeutic areas, distribution channels, and regional markets while assessing the long-term impact of biologics, precision medicine, AI-driven drug discovery, and advanced manufacturing.

Why Buy This Report?

This report provides comprehensive market intelligence to help pharmaceutical companies, biotechnology firms, investors, healthcare organizations, and industry stakeholders identify emerging opportunities, evaluate technology trends, understand competitive developments, and support strategic decision-making.

The study supports product development, portfolio expansion, regulatory planning, partnership strategies, manufacturing optimization, and long-term investment planning.

Why Choose DataM?

- Data-Driven Insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

Target Audience 2026

- Manufacturers/ Buyers

- Industry Investors/Investment Bankers

- Research Professionals

- Emerging Companies