Active Pharmaceutical Ingredients Market Size & Growth

Active pharmaceutical ingredients are the value-defining core of drug manufacturing. As pharmaceutical companies expand branded drugs, generics, biologics, biosimilars, oncology therapies and specialty medicines, API supply has become a strategic issue for cost control, quality assurance, regulatory compliance and supply chain resilience.

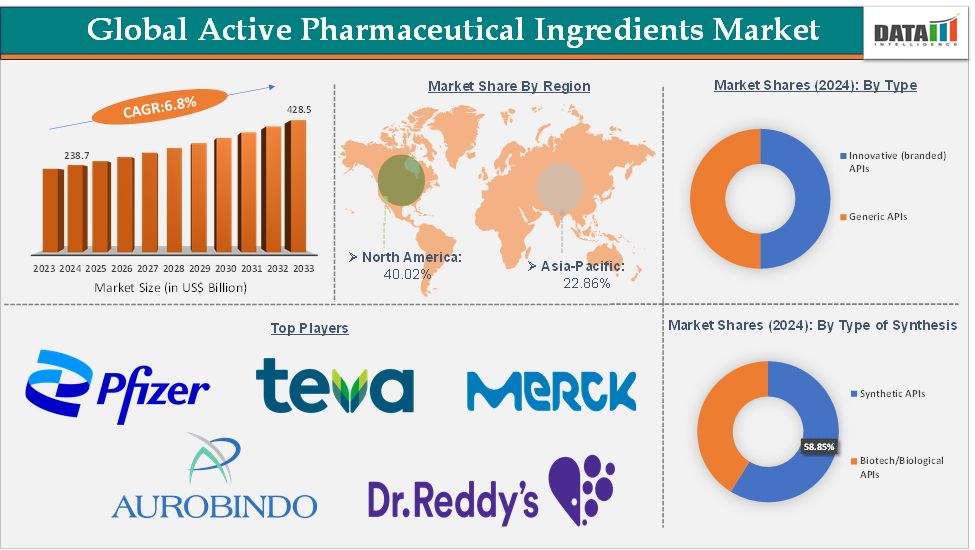

Active Pharmaceutical Ingredients Market is valued at US$ 254.92 billion in 2025 and is projected to reach US$ 492.17 billion by 2035, growing at a CAGR of 6.8% during 2026–2035.

The market is commercially important because APIs sit at the intersection of drug availability, manufacturing economics and therapeutic innovation. Chronic disease prevalence, aging populations and expanding access to healthcare continue to increase medicine consumption, while biologics and biosimilars are raising the value intensity of API production. For pharmaceutical executives, investors and procurement teams, the Active Pharmaceutical Ingredients Market 2025 baseline reflects a sector where scale, regulatory capability, vertical integration and advanced synthesis expertise are becoming critical competitive advantages.

Active Pharmaceutical Ingredients Market Key Takeaways

The Active Pharmaceutical Ingredients Market is projected to increase from US$254.92 billion in 2025 to US$492.17 billion by 2035, supported by a 6.8% CAGR.

Synthetic APIs held the leading position with 58.85% share, equivalent to approximately US$150.03 billion in 2025 when applied to the total market size.

North America led the global Active Pharmaceutical Ingredients Market Share with 40.02%, equivalent to approximately US$102.02 billion in 2025 when applied to the total market size.

Biotech APIs are the fastest-growing API category in the source analysis, supported by biologics, biosimilars, monoclonal antibodies, recombinant proteins, vaccines and advanced therapies.

Price erosion and margin compression remain major restraints in commoditized APIs such as antibiotics, analgesics and common cardiovascular products.

- Recent strategic activity points to three priorities: supply chain control, AI-assisted formulation development and green chemistry adoption.

Active Pharmaceutical Ingredients Market Scope

| Report Attribute | Details |

| Market Size in 2025 | US$254.92 billion |

| Market Size by 2035 | US$492.17 billion |

| CAGR | 6.8% during 2026 to 2035 |

| Historic Years | 2023 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Segments Covered | Type, Type of Synthesis, Application, End User and Region |

| Leading Region | North America, with 40.02% share |

| Fastest Growing Region | Asia-Pacific |

Active Pharmaceutical Ingredients Market Dynamics

Why Are Biologics and Biosimilars Driving Growth in the Active Pharmaceutical Ingredients Market

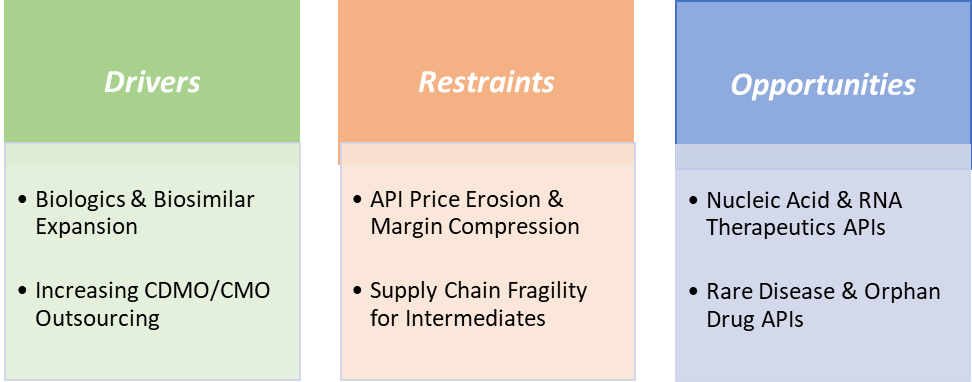

The rapid expansion of biologics and biosimilars is one of the strongest growth drivers of the Active Pharmaceutical Ingredients (API) Market. Unlike traditional small-molecule drugs, biologic medicines require highly specialized APIs produced through advanced biotechnological processes such as cell culture, microbial fermentation, recombinant DNA technology, and sophisticated purification systems.

The increasing adoption of monoclonal antibodies, recombinant proteins, vaccines, antibody-drug conjugates (ADCs), therapeutic peptides, fusion proteins, and cell and gene therapies is significantly increasing demand for high-value biologic APIs. These complex products require advanced manufacturing capabilities, stringent quality control, and regulatory compliance, creating substantial opportunities for API manufacturers with biotechnology expertise.

The growing commercialization of biosimilars is further accelerating demand. As patents expire for major biologic drugs, manufacturers are expanding biosimilar development and large-scale production, increasing the need for reliable biologic API manufacturing capacity. Since biologic APIs typically generate significantly higher value per kilogram than conventional APIs, manufacturers with integrated chemical and biological production capabilities are well positioned to capitalize on long-term growth in the Active Pharmaceutical Ingredients Market.

Why Do Synthetic APIs Continue to Dominate the Active Pharmaceutical Ingredients Market

Despite the rapid growth of biologics, synthetic APIs continue to account for the largest share of the Active Pharmaceutical Ingredients Market due to their widespread use across numerous therapeutic areas. Synthetic APIs remain essential for treating cardiovascular diseases, infectious diseases, central nervous system disorders, metabolic diseases, respiratory conditions, and gastrointestinal disorders.

Their well-established manufacturing processes, scalability, cost efficiency, and extensive global supply chains make synthetic APIs particularly important for generic drug production and high-volume pharmaceutical manufacturing. Compared with biologic APIs, synthetic APIs generally offer lower production costs, greater chemical stability, longer shelf life, and broader supplier availability, making them highly attractive in both developed and emerging pharmaceutical markets.

Manufacturing innovations are further strengthening the competitiveness of synthetic APIs. Technologies such as continuous flow chemistry, process automation, green chemistry, and advanced catalytic synthesis are improving production efficiency, increasing yields, reducing solvent consumption, and minimizing environmental impact. These advancements continue to reinforce the strategic importance of synthetic APIs even as biologic APIs experience faster growth.

How Is Innovation Transforming the Active Pharmaceutical Ingredients Market

Continuous innovation in pharmaceutical manufacturing is enhancing the efficiency, sustainability, and quality of API production. Manufacturers are investing in advanced process technologies, digital manufacturing, artificial intelligence (AI), process analytical technology (PAT), continuous manufacturing, and automation to improve production consistency while reducing operational costs.

Growing demand for highly potent active pharmaceutical ingredients (HPAPIs), precision medicines, personalized therapeutics, and complex biologics is encouraging companies to expand specialized manufacturing capabilities. At the same time, increased adoption of green chemistry principles, sustainable solvent recovery, and energy-efficient production processes is helping manufacturers meet environmental regulations while improving long-term operational efficiency.

Innovation is also strengthening supply chain resilience through advanced quality management systems, digital traceability, and integrated manufacturing platforms. These developments are enabling pharmaceutical companies to improve regulatory compliance, accelerate product development, and support the growing demand for next-generation medicines across the Active Pharmaceutical Ingredients Market.

What Challenges Are Limiting Growth in the Active Pharmaceutical Ingredients Market

Despite strong demand, the Active Pharmaceutical Ingredients Market continues to face significant pricing and operational challenges. Price erosion remains a major concern in mature therapeutic categories such as antibiotics, analgesics, and widely used cardiovascular drugs, where intense competition among large-scale manufacturers has reduced profit margins.

In addition to competitive pricing pressures, API manufacturers must comply with increasingly stringent regulatory requirements related to Good Manufacturing Practices (GMP), environmental protection, product quality, and supply chain transparency. Investments in regulatory compliance, quality assurance systems, environmental controls, and facility modernization significantly increase operating costs, particularly for small and mid-sized manufacturers.

Global supply chain disruptions, dependence on key raw materials, and geographic concentration of API manufacturing also present ongoing risks. As a result, pharmaceutical companies are increasingly prioritizing supplier diversification, regulatory reliability, manufacturing resilience, and long-term strategic partnerships. Manufacturers that differentiate through complex APIs, biologic APIs, highly potent APIs (HPAPIs), sustainable manufacturing practices, and consistent regulatory compliance are expected to strengthen their competitive position and support long-term growth in the Active Pharmaceutical Ingredients Market.

Active Pharmaceutical Ingredients Market Opportunities

The most attractive opportunities in the Active Pharmaceutical Ingredients Market Report are concentrated in biologics, biosimilars, high-potency APIs, oncology APIs, complex molecules and sustainable synthesis. These areas offer stronger margin potential than commoditized small molecules and require capabilities that are harder to replicate.

Manufacturers can benefit by expanding complex molecule synthesis, biologic production, peptide APIs and antibody drug conjugate capabilities. Investors should track companies with vertical integration strategies, regulatory strength and exposure to high-value therapeutic pipelines. Procurement teams should evaluate supplier resilience, quality track record, geographic diversification and ability to support long-term supply agreements.

Technology companies also have a role in API development. The 2025 partnership between PatSnap and Uncountable to launch an AI-powered Formulation Agent signals growing interest in digital tools that help automate and optimize complex pharmaceutical formulation work. AI-assisted R&D may support faster development cycles and more precise API structure design over the long term.

Economic and Investment Analysis

Macroeconomic demand for APIs is supported by aging populations, chronic disease burden and expanding access to medicines. Healthcare systems need large volumes of cost-efficient generics while pharmaceutical companies also require high-value APIs for biologics and specialty therapies. This creates a two-speed market: scale-driven synthetic APIs on one side and innovation-driven complex APIs on the other.

Investment is moving toward vertical supply chain control, advanced synthesis, biologic API production and environmentally efficient manufacturing. The January 2026 acquisition of a specialty API manufacturer by a global pharmaceutical leader reflects a broader strategic need to secure critical pharmaceutical precursors and reduce reliance on external suppliers.

Capital expenditure opportunities are strongest in biologic API capacity, HPAPI containment, complex molecule synthesis, continuous manufacturing, green chemistry and quality systems. ROI depends on therapeutic focus, regulatory approval cycles, utilization rates, customer contracts and ability to avoid pure commodity pricing exposure.

Economic risks include API price erosion, margin compression, environmental compliance costs, supply concentration and capacity oversupply in commoditized categories. Scenario planning should therefore distinguish between high-volume generic APIs and high-value specialty APIs, as the economics of each category are materially different.

Active Pharmaceutical Ingredients Market Segmentation Analysis

The Active Pharmaceutical Ingredients Market is segmented by type, by type of synthesis, by application, by end user, and by Region - Share, Trends, and Forecast to 2035.

By Type of Synthesis

Synthetic APIs lead the market with 58.85% share. Their business value lies in scalability, cost efficiency, manufacturing maturity and broad use in generic and branded small-molecule drugs. They are widely used by pharmaceutical companies and generic manufacturers serving chronic disease and mass-market therapeutic categories.

Biotech APIs are the faster-growing category in the source analysis. Growth is supported by biologics, biosimilars, monoclonal antibodies, recombinant proteins, vaccines and advanced therapies. These APIs require specialized production infrastructure and stronger technical know-how, but they offer higher value potential and strategic differentiation.

By Application

Application demand is strongly linked to chronic disease treatment, oncology, cardiovascular diseases, diabetes, infectious diseases and specialty therapies. Oncology and biologic drug pipelines increase demand for high-value APIs, while cardiovascular and metabolic disorders support large-volume demand for synthetic APIs.

The future growth potential through 2035 will likely be strongest where therapeutic innovation intersects with manufacturing complexity. APIs used in biologics, biosimilars, HPAPIs and advanced therapies are expected to remain strategically important because they support higher-value drug categories.

By End User

Pharmaceutical companies, generic drug manufacturers, biotechnology companies and contract manufacturers are the primary end users. Large pharmaceutical companies often use APIs to support branded pipelines and vertical integration strategies. Generic manufacturers depend on cost-effective synthetic APIs to compete in price-sensitive markets. Biotechnology companies need specialized API capabilities for biologics and complex therapeutic platforms.

For end users, API selection affects product cost, regulatory risk, supply continuity, speed to market and product quality. Supplier qualification and long-term reliability are therefore central to procurement decisions.

Active Pharmaceutical Ingredients Market Regional Analysis

North America Leads on High-Value APIs and Regulatory Strength

North America accounted for 40.02% of the global market share. When applied to the 2025 market size, this equals approximately US$102.02 billion. The region’s leadership is supported by a strong pharmaceutical manufacturing base, advanced R&D infrastructure, high regulatory standards and major pharmaceutical companies such as Pfizer and Merck.

The United States is particularly important due to its demand for branded and generic drugs, aging population and chronic disease burden across cancer, diabetes and cardiovascular disorders. North America is also positioned strongly in high-value API categories such as biologics, HPAPIs and innovative oncology APIs.

FDA-driven quality expectations create higher compliance requirements, but they also strengthen the global competitiveness of North American API production. The region’s strategic focus is increasingly tied to supply chain security, high-value product portfolios and advanced manufacturing technologies.

Europe Focuses on Quality, Specialty Manufacturing and Compliance

Europe remains an important API market because of its pharmaceutical manufacturing base, regulated production standards and demand for high-quality APIs. Although no regional share is quantified for Europe in the source dataset, the region is commercially relevant for specialty APIs, complex molecules, biologics and regulated manufacturing.

European buyers typically prioritize quality assurance, traceability, environmental compliance and supplier reliability. The October 2025 industry transition toward green chemistry and eco-efficient synthesis routes is especially relevant to Europe’s long-term manufacturing direction, as sustainability and regulatory compliance are increasingly linked.

The region’s opportunity lies in complex APIs, premium-quality production, advanced process chemistry and environmentally efficient manufacturing systems.

Asia-Pacific Is a Manufacturing Scale Center

Asia-Pacific is highlighted as a major API manufacturing hub, particularly through India and China. The region benefits from cost advantages, production scale, supplier networks and policy support. India is especially important in biosimilar API production and partnerships with multinational pharmaceutical companies, while China remains a major global production base for numerous API categories.

The region’s manufacturing strength supports global pharmaceutical supply, especially in synthetic APIs and cost-sensitive products. However, price competition and margin pressure are also most visible in commoditized categories where large-scale suppliers compete aggressively.

Asia-Pacific’s future opportunity is not limited to low-cost production. Manufacturers in the region are moving toward complex APIs, biosimilars and higher-value capabilities, which could improve margins and strategic relevance through 2035.

Country-Level Market Analysis

The United States is the most important country-level market within North America because of its pharmaceutical R&D base, chronic disease drug demand, strong intellectual property framework and high-value biologics pipeline. Its main barriers include strict regulatory compliance costs and the need for resilient domestic and diversified supply chains.

India is a major API manufacturing country, supported by scale, cost advantages and growing biosimilar API production. Its future opportunity lies in moving from commoditized APIs toward complex molecules, biologics and regulated-market supply partnerships. Challenges include price competition, margin pressure and compliance investment requirements.

China remains a significant API production base, especially in large-scale and cost-driven categories. Its competitive advantage is manufacturing scale, but oversupply in certain therapeutic categories contributes to global price erosion. Future opportunities include higher-value APIs and improved environmental compliance.

Germany and other European pharmaceutical manufacturing countries remain relevant for specialty APIs, quality-driven production and regulated supply. Country-level market sizes are not provided in the source dataset, so the analysis is based on manufacturing role, regional positioning and demand drivers.

Regulatory and Policy Analysis

The API market is heavily influenced by regulatory standards governing manufacturing quality, drug safety, impurity control, environmental compliance and supply chain traceability. North America’s strong FDA-regulated environment supports high-quality production but also increases compliance costs for manufacturers.

Environmental policy is becoming more important. The October 2025 move by pharmaceutical manufacturers toward green chemistry and eco-efficient synthesis routes reflects rising pressure to reduce chemical waste, improve resource efficiency and prepare for long-term regulatory expectations. Manufacturers that invest early in sustainable synthesis may reduce future compliance risk and improve customer acceptance.

Trade policy and international supply chain dependency also matter because API supply is globally distributed. Buyers are placing more emphasis on supplier diversification, vertical integration and resilience planning. Expected regulatory changes are likely to increase attention on quality audits, data integrity, environmental controls and secure sourcing.

Competitive Landscape and Vendor Strategy

The Active Pharmaceutical Ingredients Market includes Pfizer Inc., Teva Pharmaceuticals USA, Inc., Merck KGaA, AbbVie Inc., Aurobindo Pharma Limited, Dr. Reddy’s Laboratories Ltd., Lupin, Sun Pharmaceutical Industries Ltd., Divi's Laboratories Limited and Cipla.

Competition differs sharply by API type. In commoditized synthetic APIs, scale, cost efficiency and process optimization are key. In complex APIs, biologics and HPAPIs, differentiation depends on technical capability, regulatory track record, containment infrastructure, manufacturing reliability and customer trust.

Large pharmaceutical companies are strengthening vertical control to protect critical portfolios and reduce dependence on external suppliers. Indian API leaders such as Aurobindo Pharma, Dr. Reddy’s, Lupin, Sun Pharmaceutical, Divi's Laboratories and Cipla are positioned around manufacturing scale, generic drug supply and regulated-market experience. Pfizer, Merck KGaA and AbbVie bring strength through innovation pipelines, branded portfolios and advanced therapeutic focus.

The vendor landscape is expected to reward companies that can balance cost efficiency with complex manufacturing, quality systems, sustainable production and long-term supply assurance.

Recent Developments in Active Pharmaceutical Ingredients Market

- June 2026 – Pfizer expands API manufacturing capabilities for innovative and specialty medicines

Pfizer strengthened its pharmaceutical manufacturing network by expanding active pharmaceutical ingredient (API) production capacity and process optimization technologies to support innovative medicines, biologics, and global supply chain resilience. - June 2026 – Divi's Laboratories expands high-potency API manufacturing

Divi's Laboratories enhanced its API manufacturing capabilities through capacity expansion and advanced process technologies for high-potency APIs (HPAPIs), custom synthesis, and contract manufacturing to meet growing global pharmaceutical demand. - May 2026 – Merck KGaA advances pharmaceutical manufacturing technologies

Merck KGaA expanded its pharmaceutical manufacturing portfolio by strengthening API process development, continuous manufacturing technologies, and digital production capabilities to improve efficiency and product quality. - May 2026 – Aurobindo Pharma strengthens API production infrastructure

Aurobindo Pharma expanded its active pharmaceutical ingredient manufacturing operations by increasing production capacity and enhancing process efficiency to support generic and specialty pharmaceutical products for global markets. - April 2026 – Dr. Reddy's Laboratories expands API manufacturing and sustainability initiatives

Dr. Reddy's strengthened its API business by advancing green chemistry practices, process optimization, and manufacturing capacity to improve supply reliability and support global pharmaceutical customers. - March 2026 – Sun Pharmaceutical Industries enhances vertically integrated API operations

Sun Pharma expanded its integrated API manufacturing capabilities by improving process technologies, operational efficiency, and quality systems to support its specialty and generic medicine portfolio. - February 2026 – Teva Pharmaceuticals advances global API supply chain strategy

Teva strengthened its pharmaceutical manufacturing network by optimizing API sourcing, expanding manufacturing efficiency initiatives, and enhancing supply chain resilience to ensure reliable medicine production worldwide.

Strategic Insights and Analyst Perspective

The Active Pharmaceutical Ingredients Market Analysis points to a sector where volume growth alone is not enough. Companies need to decide whether they want to compete in scale-driven synthetic APIs, high-value biologics and complex APIs, or integrated portfolios that combine both.

For investors, the most attractive API businesses are likely to be those with exposure to biologics, biosimilars, HPAPIs, oncology APIs, advanced synthesis and regulated-market supply. For manufacturers, the strategic priorities are vertical integration, green chemistry, complex molecule capability, supply reliability and margin protection. For procurement teams, the key issue is balancing cost efficiency with supplier resilience and regulatory quality.

Risk mitigation should focus on avoiding excessive supplier concentration, assessing long-term viability of low-cost API sources, monitoring environmental compliance exposure and building dual-sourcing strategies for critical ingredients.

Report Benefits

This Active Pharmaceutical Ingredients Market Report helps pharmaceutical manufacturers evaluate supply-side risks, therapeutic growth areas and synthesis trends. Investors can use it to assess margin pools, complex API opportunities and consolidation themes. Suppliers can identify where demand is moving across synthetic APIs, biologics, biosimilars and specialty ingredients. Procurement teams can benchmark regional supply dynamics, cost pressures and supplier resilience. Strategy teams can use the report to evaluate API outsourcing, vertical integration and long-term manufacturing positioning.

Target Audience

- API (Active Pharmaceutical Ingredient) manufacturers

- Pharmaceutical companies

- Biotechnology firms

- Generic drug manufacturers

- Contract Development and Manufacturing Organizations (CDMOs)

- Investors in pharmaceutical and biotechnology sector

- Private equity firms

- Procurement heads

- Supply chain leaders

- Regulatory affairs teams

- Product managers

- Strategy and planning teams

- Research and Development (R&D) leaders

- Healthcare industry consultants