Oral Obesity Drugs Market Overview

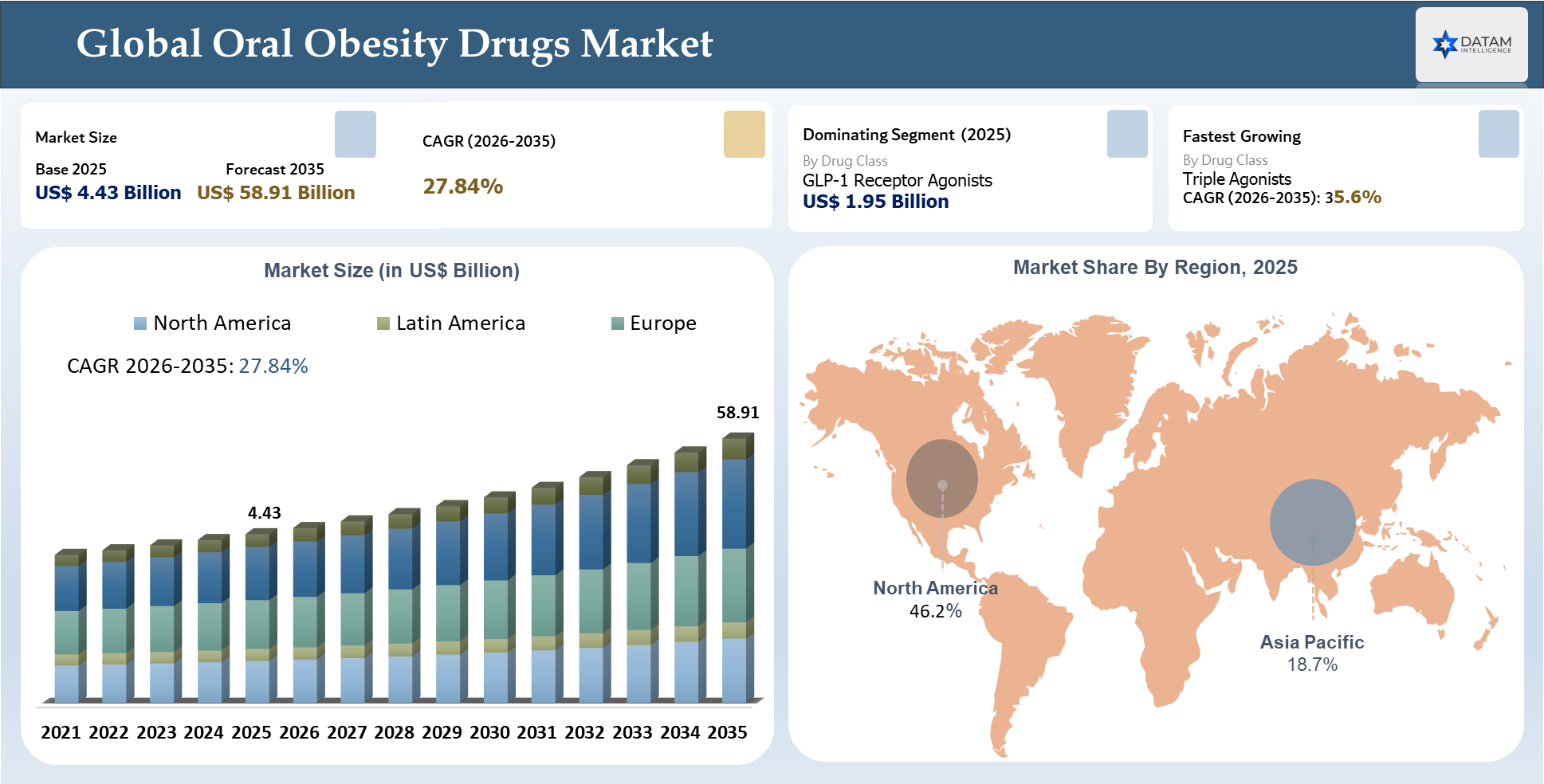

The Global Oral Obesity Drugs Market stood at US$ 4.43 billion in 2025 and is expected to reach US$ 58.91 billion by 2035, growing with a CAGR of 27.84% during the forecast period 2026-2035. This market is shifting from a traditional weight loss pill market to a new, more targeted chronic metabolic disease market. Traditional oral weight loss medications mainly included drugs that suppressed appetite or inhibited fat absorption, but the market is now being defined by new oral GLP-1 receptor agonists, incretin dual agonists, triple agonists, and other metabolic disease medications. This transition in the market arises due to the changing approach towards obesity being considered as a chronic disease, with comorbidities such as type 2 diabetes and other diseases.

Key Takeaways

- Oral GLP-1 receptor agonists are now the primary areas of innovation with the promise of giving patients a more practical alternative to injectable obesity therapies and, hopefully, higher rates of long-term adherence growing from $1.95 billion revenue in 2025 to account for more than 48% of the market by 2035.

- Eli Lilly's orforglipron and Pfizer's daily acting danuglipron represent the latest oral non-peptide GLP-1 agonists, striving for parity in efficacy with the injectables, with the advantage of being more readily manufactured.

- Today's oral GLP-1s give 13-15% weight loss at 36 weeks (orforglipron Phase 2). This is less than semaglutide (Rybelsus 15-17%) and high-dose Wegovy injection 15-18%. New drug pipeline from Eli Lilly, Novo Nordisk and Pfizer targets that parity.

- Oral obesity pipeline targets focusing on GLP-1/GIP dual agonists (Ecnoglutide, CT-388, DAPIGLP-1 ), amylin analogs (Pramlintide, Cagrilintide, Petrelintide) and CB1 inverse agonists (Inv-101, JD-5037, MRI-1867) provide alternative mechanisms and possible complementary actions.

- It's anticipated that the new standard in efficacy, commanding top-tier pricing and enormous R&D, will transition from dual agonists (e.g., tirzepatide) to triple agonists, and every single Big Pharma player will be invested. Triple agonists will grow at the fastest rate at 35.6% CAGR

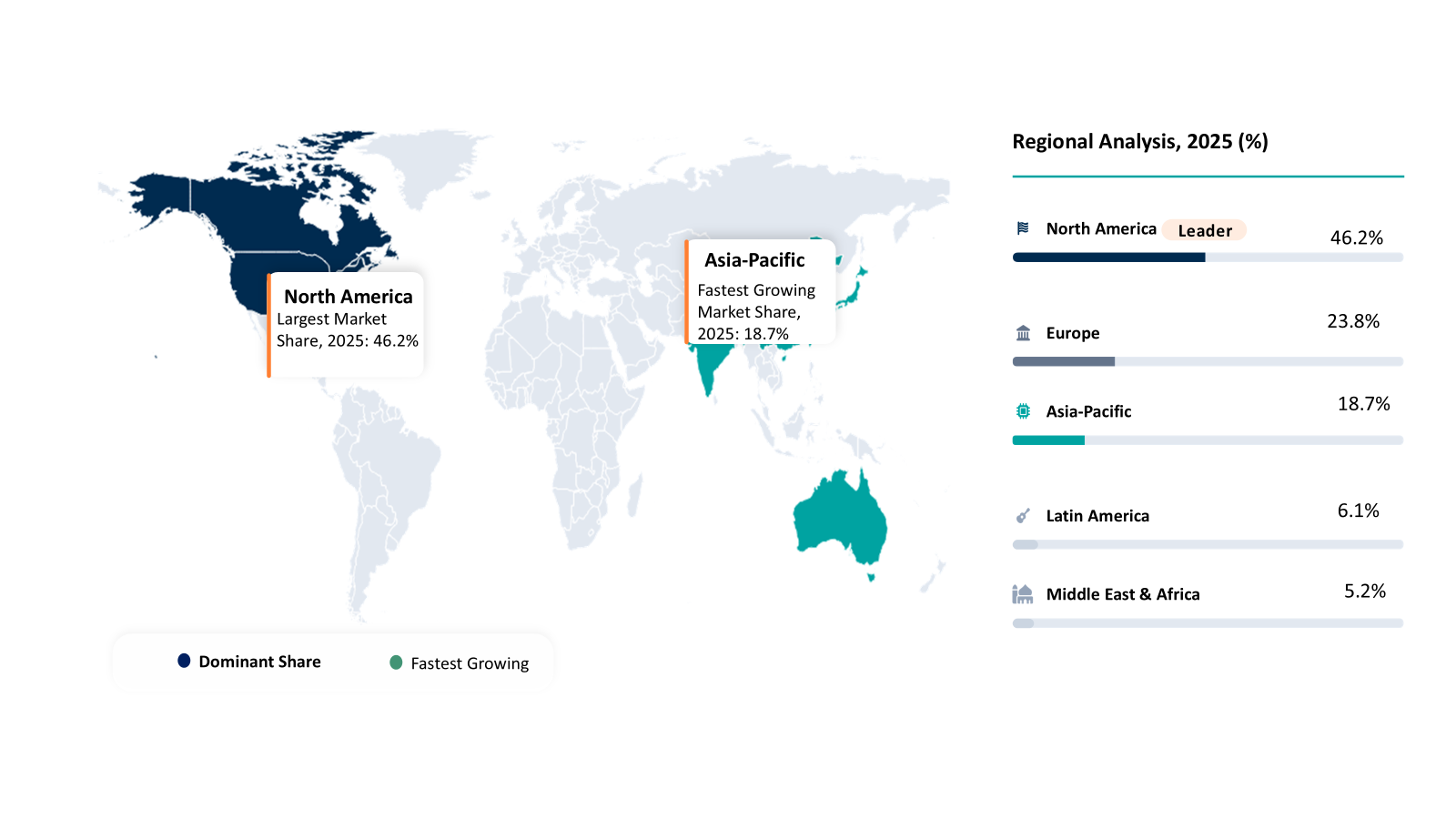

- U.S. FDA has a more rapid approach for approval of chronic weight management drugs, permitting short phase 3 trials of 52 to 68 weeks without requiring pre-approval cardiovascular outcomes trials (CVOTs) whereas Europe insists on such trials. This has driven North America to account for 46.2% share of the Oral Obesity Drugs market in 2025.

- The oral obesity drugs are set to grow commercially due to their greater convenience compared to injectable forms, which minimize issues such as fear of needles, the complexity of administering injections, and weariness from continued use. It is projected that the rise of these drugs will be driven by increased penetration in primary care facilities, availability via pharmacies, obesity treatment through telehealth, and higher consumer demand for more accessible forms of treatment. Nonetheless, market growth will require a combination of effectiveness, tolerability, safety, acceptability among payers, and proof of cardiometabolic benefits.

AI Impact Analysis

AI is set to have an important role in transforming the global oral obesity drugs market given the rush of drug manufacturers to come up with differentiating oral GLP-1 drugs, dual incretins, triple agonists, and other metabolic drugs. As far as drug discovery is concerned, AI technology is capable of providing assistance during target discovery, molecule discovery, and lead molecule optimization, as well as bioavailability prediction, since many of the peptide-based obesity drugs struggle with stability and absorption in their oral form.

In addition, AI is also playing an increasingly critical role in clinical trial designs and patient selection. Obesity is a complex disease with diverse patient populations characterized by metabolic differences, comorbidity status, compliance, and responsiveness to therapy. With the use of AI-powered analytics, companies will be able to identify responsive patient segments, optimize recruitment for their clinical trials, detect safety concerns, and build evidence from real-world data. AI will also play a commercial role in helping engage payers by demonstrating that certain therapeutic outcomes can help prevent type 2 diabetes, reduce cardiovascular risks, and save on overall health costs.

Oral Obesity Drugs Industry Trends and Strategic Insights

- Commercial value is shifting from “weight-loss efficacy” to differentiated obesity care positioning, as companies compete on oral GLP-1 receptor agonists, dual incretin agonists, triple agonists, amylin-based drugs and other metabolic therapies that can deliver durable outcomes, better tolerability and stronger patient convenience.

- Non-injectable treatment formats are becoming a strategic entry point for wider patient adoption, particularly for patients who are hesitant to start injectable GLP-1 therapies or may struggle with long-term injection adherence, storage requirements, and administration fatigue.

- Oral small-molecule GLP-1 and multi-agonist pipelines are redefining competitive intensity, as pharmaceutical companies seek therapies that can combine injectable-like clinical performance with easier dosing, scalable manufacturing, and broader use across primary care, pharmacy and telehealth channels.

- North America remains the key commercialization hub, supported by stronger prescription-based obesity care adoption, advanced pharmacy infrastructure, active clinical research, higher payer engagement and faster uptake of next-generation metabolic therapies.

- Winning companies will be those that build a full obesity care value proposition, not just a drug portfolio. Long-term success will depend on clinical differentiation, real-world evidence, payer value, patient support programs, adherence tools, physician education, and clear positioning across obesity, type 2 diabetes, cardiovascular risk and metabolic syndrome.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 4.43 Billion | |

| 2035 Projected Market Size | US$ 58.91 Billion | |

| CAGR (2026-2035) | 27.84% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Drug Class | GLP-1 Receptor Agonists, Dual Incretin Agonists, Triple Agonists, Amylin-Based Drugs, Lipase Inhibitors, CNS-Acting Anti-Obesity Drugs, Melanocortin-4 Receptor Agonists and Others | |

| By Molecule Type | Small Molecules, Peptide-Based Molecules, Peptidomimetics and Others | |

| By Product Type | Branded and Generic | |

| By Prescription Type | Prescribed and OTC | |

| By Patient Group | Adolescents, Adults and Geriatric | |

| By Indication | Obesity, Overweight with Comorbidities, Obesity with Type 2 Diabetes, Obesity with Cardiovascular Risk, Obesity with Metabolic Syndrome and Others | |

| By Distribution Channel | Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Specialty Pharmacies, Telehealth and Others | |

| By End-User | Hospitals, Obesity and Weight Management Clinics, Endocrinology Clinics, Homecare Settings and Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

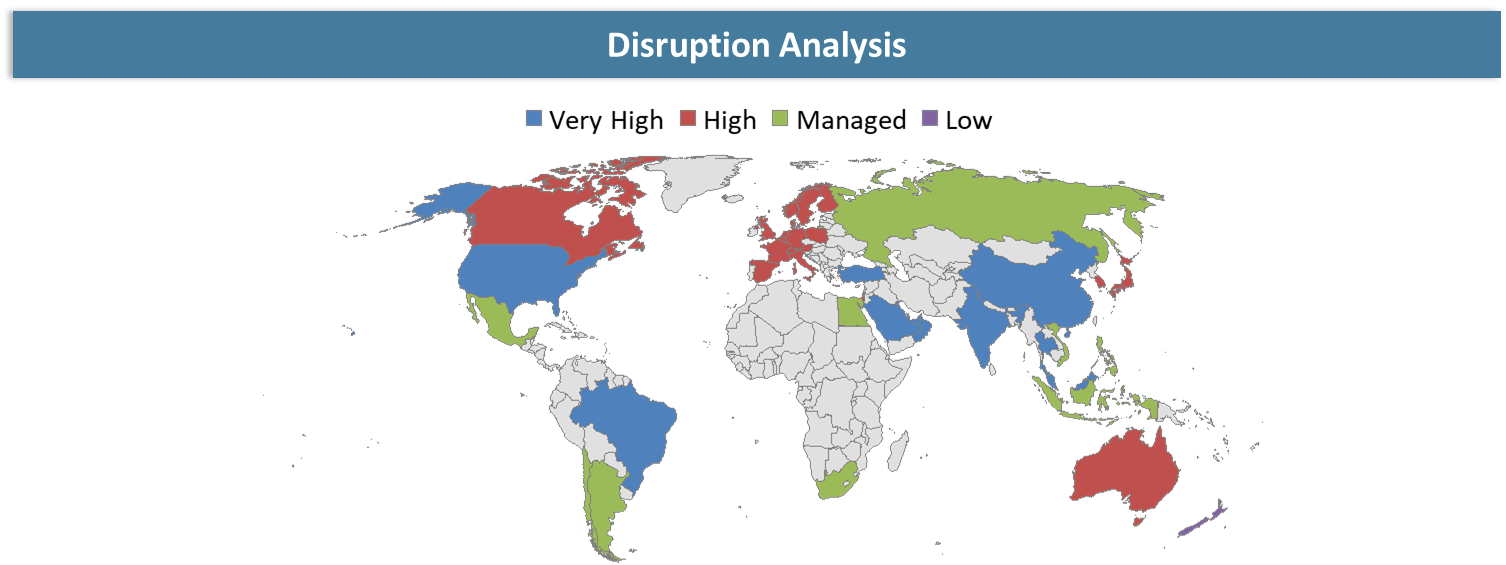

Disruption Analysis

Next-Generation Oral GLP-1 Drugs Disrupting the Obesity Treatment Value Chain

The oral obesity medication market globally has faced a paradigm shift from conventional weight management products towards advanced metabolic treatment products, which will pose competition to GLP-1 and incretin-based injectable treatments. Conventional oral treatment methods focused mainly on appetite suppression or fat blocking; however, the market scenario has shifted focus towards oral GLP-1 receptor agonists, incretin agonists, triple agonists, and amylin-based approaches targeting obesity as a metabolic disease rather than merely focusing on its weight management.

The major disruption will undoubtedly come from oral medications that provide injectable-level effectiveness while enjoying greater convenience and scalability compared to injectables. This disruption will enable reduced reliance on specialty-led injectable treatment regimes and increase access for those hesitant about starting with injections. On the other hand, payer pressure, concerns around safety, and expensive treatments will act as disruptions for companies planning their commercialization strategy. The companies that distinguish themselves clinically, have easy-to-use medication, and provide affordable access models will stand out among others.

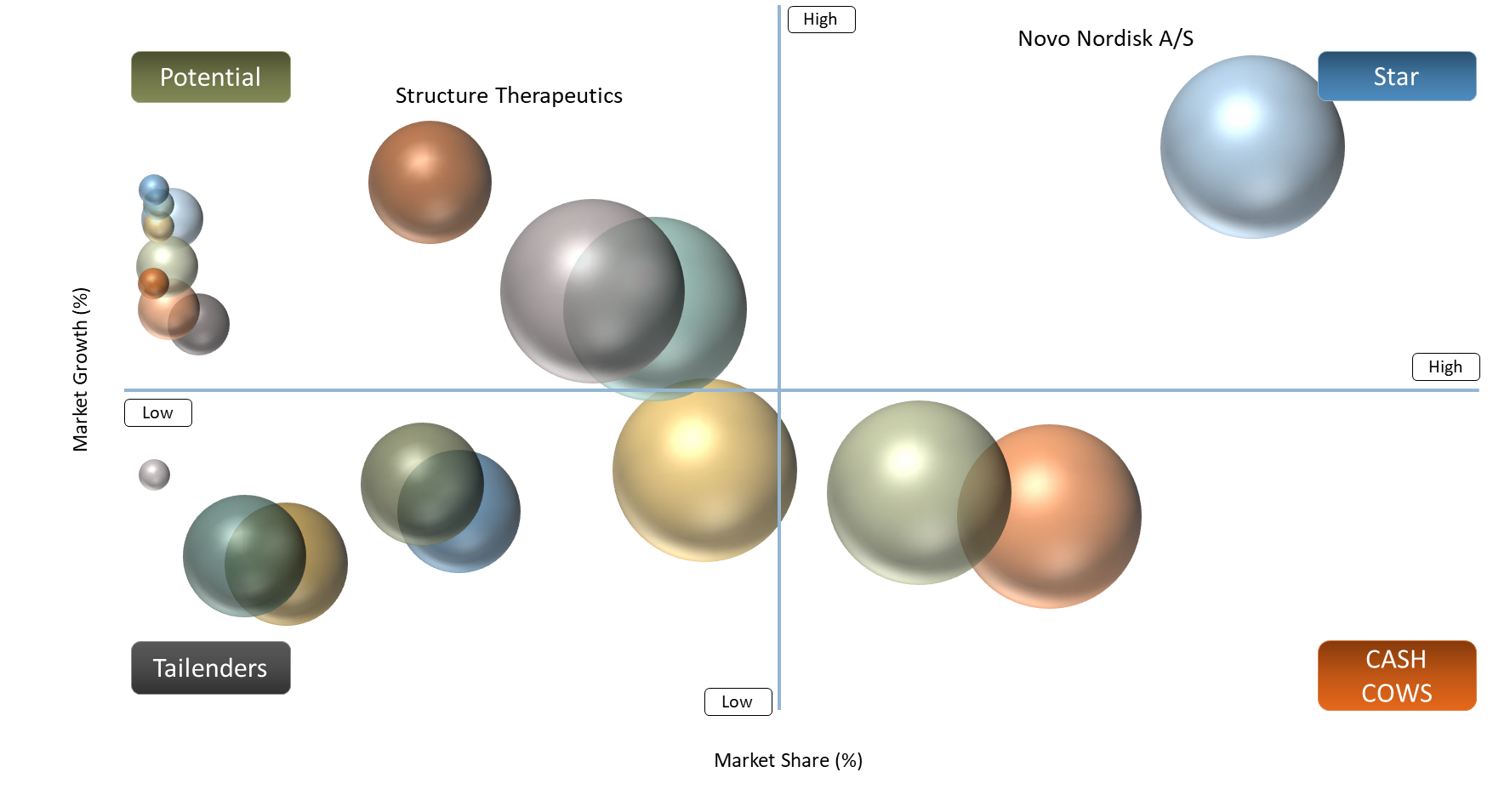

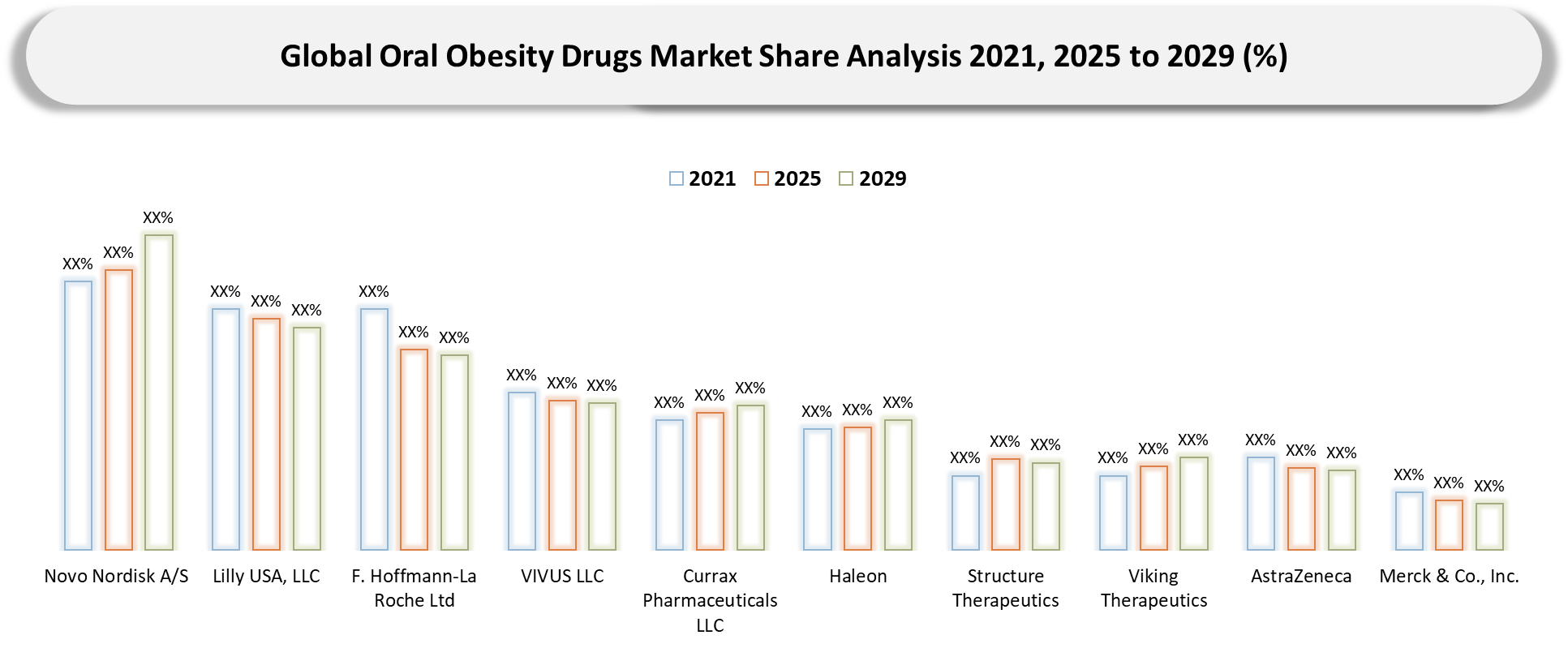

BCG Matrix: Company Evaluation

As for the BCG matrix, Stars are organizations that are characterized by large global scale, innovative metabolic disease portfolio, clinical expertise, and a clear positioning in the next-generation oral obesity drugs market. Novo Nordisk A/S, Lilly USA, LLC, and F. Hoffmann-La Roche Ltd fall into this quadrant since they are the leading innovators of GLP-1, have a competitive oral obesity drug portfolio, global commercial capabilities and physician access.

Cash Cows are companies with existing oral obesity weight management drugs that serve mature oral treatment categories. Examples of organizations falling into this quadrant include VIVUS LLC, Currax Pharmaceuticals LLC, and Haleon. The companies have product portfolios tied to existing oral obesity drugs, pharmacy access and treatment use cases like appetite reduction and inhibition of fat absorption. Such companies are relevant commercially, though not highly innovative compared to GLP-1 organizations.

Question Marks are organizations that have a relatively good oral obesity drugs portfolio, though their performance has not been fully exploited. Some of the examples include Structure Therapeutics, Viking Therapeutics, AstraZeneca, and Merck & Co., Inc. Such organizations are exposed to various areas of next-generation metabolic drugs, including oral GLP-1 and dual incretins.

Market Dynamics

Injection Fatigue Creating a Clear Commercial Opening for Oral Obesity Therapies

Injection fatigue has emerged as an evident business opportunity driving the Global Oral Obesity Drugs Market, as the obesity drug market evolves from being a solution primarily focused on short-term weight loss to being involved in the treatment of obesity as a chronic disease. Some patients who need continuous treatments may prefer oral products since they minimize needle phobia, hassle associated with injections, storage difficulties, and injection fatigue that comes with GLP-1 injectables. There is tremendous potential here due to the World Obesity Federation’s World Obesity Atlas forecast stating that by 2030, there will be one billion individuals worldwide suffering from obesity, including 20% of women and 14% of men. This shows that the number of patients who would benefit from a more convenient therapy model is substantial. Oral obesity treatments have the ability to solve several issues by delivering a familiar format of drug delivery that will fit well into the model of primary-care-based, retail-based, and tele-health led management of obesity patients.

Payer Resistance to Long-Term Weight-Loss Drug Coverage Limits Mass Adoption

Resistance from payers continues to be one of the top barriers faced by the Global Oral Obesity Drugs Market since obesity drugs are becoming more like chronic medicines. With the emergence of such drugs, it means that the need to have them reimbursed by payers becomes paramount since they will be administered long-term as opposed to being short-term solutions. Payers are still implementing some strict policies when it comes to reimbursing treatment with oral obesity drugs. Prior authorization and step therapy protocols, as well as body mass index and medical conditions-based criteria, remain some of the major factors affecting patients’ access to reimbursement. If the patient needs to take the medication continuously to ensure that he or she loses weight, the high costs of the treatment will discourage patients from continuing to take it even if recommended by a doctor. Health economic benefits are essential if the manufacturers are going to make oral obesity drugs popular on the market.

Segmentation Analysis

The Global Oral Obesity Drugs Market is segmented based on drug class, molecule type, product type, prescription type, patient group, indication, distribution channel, end-user, and region.

GLP-1 Receptor Agonists Are Emerging as the Core Growth Engine of the Oral Obesity Drugs Market

Oral GLP-1 receptor agonists have become the most strategically relevant category within the global market for oral obesity drugs, since they effectively address the paradigm change in the industry from conventional obesity drugs to treatment options addressing metabolic diseases. Previously available oral obesity drugs were mostly known for their ability to suppress hunger and fat absorption, but GLP-1-based treatments provide more far-reaching health effects through satiety and food intake modification, blood sugar regulation, and reduced risk factors for heart diseases.

The oral GLP-1 component is becoming commercially important as it allows combining the promise of efficacy generated by injectable GLP-1 drugs with the convenience of the oral route of administration. This enhances the possibilities for broader applicability in primary care, retail, and online pharmacy-based obesity services. The most successful corporations are taking advantage of the oral GLP-1 breakthrough to position themselves based on the convenience and adherence offered. With intensifying competition, GLP-1 receptor agonists will continue to be the core growth driver influencing the development of pipelines and market entry strategies.

Geographical Penetration

North America’s Mature Obesity Care Ecosystem Driving Adoption of Oral Weight Management Therapies

North America would continue dominating the global market for Oral Obesity Drugs due to its well-developed system of treating obesity and the increased acceptability of the use of medication in obesity management and metabolic disorders as well. The region possesses a good number of hospitals and endocrinology practices, specialized obesity treatment centers, pharmacies, specialized dispensing, and digital healthcare systems. This makes launching oral obesity drug products easier than in less developed regions.

Other factors contributing to leadership in the region include increased awareness about the co-morbid diseases associated with obesity, greater physician involvement, vigorous scientific research, and pharmaceutical investment in oral GLP-1 drugs, incretin-based, and multi-agonist drugs. The oral formulation of these drugs may be advantageous because it would eliminate the challenges associated with injections and increase compliance. Nevertheless, reimbursement constraints, financial considerations, and payer pressure to achieve sustained results could remain influential factors. On the whole, the North American region has the most comprehensive potential with regard to all these factors combined.

U.S Oral Obesity Drugs Market Trends

The U.S. Oral Obesity Drugs Market is evolving from its status as a niche weight loss drugs market into one that is characterized by a high-value chronic metabolic disease treatment market. The most prominent growth trend involves the transition from reliance on injectables for GLP-1 treatment towards oral agents that may increase patient convenience as well as help address issues associated with injection fatigue. There is a considerable need for such a drug in this market based on the CDC statistics, which showed that all states and territories in the U.S. registered adult obesity prevalence rates of 25% and above in 2024.

Another significant trend includes the commercialization of oral GLP-1 and small-molecule obesity medications. The launch of Wegovy by Novo Nordisk in the United States as the first-ever oral GLP-1 medication for treating obesity, as well as the advancement of orforglipron by Eli Lilly, will affect competition, as companies strive to develop more convenient and better-tolerated medications that can provide good payer value. Nevertheless, adoption will still be affected significantly by reimbursement challenges, affordability concerns, and prior authorization requirements. Generally speaking, the United States is expected to continue serving as a launch and adoption hotspot for oral obesity medications.

Japan Oral Obesity Drugs Market Outlook

Japan Obesity Oral Drug Market will likely emerge as an opportunity-oriented segment in the Asia Pacific region owing to the increasing concerns regarding metabolic disorders, an aging population, and obesity-related complications. There is a growing necessity for convenient drugs in oral form for effective weight control without any obstacles related to the administration of injections. Oral formulations can be highly beneficial for patients who need continuous therapy, managed care of obesity under physician supervision, and ease of drug administration.

The future oral GLP-1 receptor agonists, incretin dual agonists, triple agonists, and other new oral metabolic products will become popular only if they prove themselves capable of producing sustained results in obesity disease, type 2 diabetes, hypertension, dyslipidemia, cardiovascular risks, and metabolic syndromes through their effectiveness and safety. On the other hand, acceptance will be limited because of the stringent guidelines that prevail in Japan for prescription drug use. In general terms, Japan can be termed a market with emphasis on quality in oral obesity drugs.

Competitive Landscape

The Oral Obesity Drugs Market is facing increasing competition as traditional pharma giants and emerging biotechnology firms compete to gain a piece of the pie for easy-to-use weight loss treatments that do not involve any injections. Novo Nordisk A/S, Lilly USA, LLC and F. Hoffmann-La Roche Ltd enjoy a leading market position because of their strengths in the areas of obesity, diabetes and metabolic conditions, global reach, and emphasis on GLP-1-based innovations. Novo Nordisk and Lilly are especially competitive players because of the oral obesity drugs as an extension of the incretin therapy trend, while Roche can benefit from its participation in the existing oral anti-obesity drugs market.

Mature players like VIVUS LLC, Currax Pharmaceuticals LLC and Haleon are competing in the segment through approval of their oral drugs and pharmacy channel distribution. On the other hand, Structure Therapeutics, Viking Therapeutics, AstraZeneca and Merck & Co., Inc. continue increasing competition by introducing oral GLP-1, dual incretin and novel metabolic drugs.

Key Developments

- March 2026: Structure Therapeutics reported positive Phase II ACCESS II results for aleniglipron, its once-daily oral small-molecule GLP-1 receptor agonist, showing placebo-adjusted mean weight loss of up to 16.3% at 44 weeks in obesity patients.

- February 2026: Eli Lilly reported that orforglipron, its once-daily oral GLP-1 receptor agonist, is being evaluated in Phase III studies for weight management in adults with obesity or overweight with at least one weight-related medical condition.

- January 2026: Novo Nordisk planned the U.S. launch of Wegovy pill, an oral semaglutide 25 mg once-daily formulation, following U.S. approval for chronic weight management.

- December 2025: Ascletis Pharma announced that ASC30, an oral small-molecule GLP-1 receptor agonist, demonstrated 7.7% placebo-adjusted weight loss in a 13-week U.S. Phase II study in participants with obesity or overweight.

- September 2025: Eli Lilly announced complete Phase III ATTAIN-1 results for orforglipron, reporting meaningful weight loss and cardiometabolic improvements in adults with obesity or overweight.

- August 2025: Viking Therapeutics announced positive topline Phase II VENTURE-Oral results for VK2735 tablet, a once-daily oral dual GLP-1/GIP receptor agonist, with up to 12.2% mean weight loss after 13 weeks.

- December 2024: Merck & Co. entered into an exclusive global license agreement with Hansoh Pharma for HS-10535, an investigational preclinical oral small-molecule GLP-1 receptor agonist.

- July 2024: Roche reported early clinical data for CT-996, its once-daily oral GLP-1 receptor agonist, showing clinically meaningful weight loss after four weeks and supporting further development in obesity and type 2 diabetes.

- June 2024: Structure Therapeutics reported positive Phase IIa obesity data for GSBR-1290, an oral non-peptide small-molecule GLP-1 receptor agonist, achieving 6.2% placebo-adjusted mean weight loss at 12 weeks.

White Space Opportunities

There are several white spaces present in the Global Oral Obesity Drugs Market, including the need for patient convenience, access expansion, and distinctive clinical positioning. The primary area of white space is the creation of oral options for treating GLP-1 and incretin disorders as an alternative to injection. There would be considerable untapped demand for companies capable of delivering excellent weight loss results along with high tolerability, flexible dosing, and reduced administration needs.

Another important white space is represented by the emergence of comorbidity-driven positioning of oral obesity drugs, which allows marketing such medicines as treatment not only for weight loss but also for obesity associated with type 2 diabetes, cardiovascular risks, metabolic syndrome, and MASH. Such approaches will lead to higher acceptability among payers and support premium prices, depending on real-life results. Emerging markets also represent a white space since there are many affordability, awareness, and reimbursement-related problems.

More white spaces include those that exist in telehealth-enabled prescriptions, digital compliance, companion diagnostics, and personalized treatment programs for obesity. Pharmaceutical firms that integrate advancements in oral medications with patient monitoring and payer information can differentiate themselves better in the future.

DMI Opinion

As per DataM, the major hurdle in the Global Oral Obesity Drugs Market is not to generate demand, but the capacity of the players to demonstrate enduring clinical efficacy along with ease of use and acceptance among patients/payers in an extensively reviewed therapy area. The industry will no longer be limited to appetite suppressants and fat absorption inhibitors, as there are many promising oral GLP-1 receptor agonists, dual incretin agonists, triple agonists, and more to take on against the competition from injectables.

Commercial success would require more than just effectiveness at reducing weight. Pharmaceutical companies would have to show safety, cardiometabolic benefits, adherence benefits, scalable manufacturing capabilities, and sound health economics. It is more probable that payers would evaluate whether or not there are reductions in obesity-related comorbidities like type 2 diabetes, heart disease, metabolic syndrome, and MASH through oral medication, and not just reductions in weight.

While certain competitors may engage in price or generic competition, the sustainability of such leadership will only be achieved by players who have differentiated oral delivery systems, solid trial data, robust real-world evidence, wide distribution reach, and proper positioning in the obese care pathway. DataM expects that oral obesity medicines will prove themselves as one of the fastest-growing pockets owing to the move from specialist-driven injectable therapy to more primary care-oriented therapy.

Why Choose DataM?

- Innovation in Oral Obesity Drug Design: Analyses the transition from conventional weight loss medicines to innovative oral GLP-1 agonists, dual incretin agonists, triple agonists, amylin and small molecule obesity drug classes. The study assesses the improvements that manufacturers have been making in oral bioavailability, patient ease of use, dosing regimen, side effects and adherence over time.

- Drug Effectiveness and Market Positioning Evaluation: Reviews oral obesity drugs by analyzing weight loss performance, safety concerns, tolerability, cardiometabolic profile, drug regimen, patient suitability and competition with injectables. The assessment assists in determining the most appropriate therapies for obesity, obesity associated with comorbidities, obese diabetics and prevention of cardiac risks.

- Clinical Implementation for Obesity and Metabolic Management: Pinpoints how oral obesity drugs have been adopted in the management of chronic obesity, obesity in diabetic patients, metabolic syndrome conditions, prevention of cardiometabolic risks and under professional guidance weight loss programs. The assessment covers the clinical implementation in hospitals, endocrinology practices, obesity centers, retail pharmacy and virtual pharmacy settings.

- Developments within the Market and Industry: Covers notable events like the expansion of the pipeline for oral GLP-1, license agreements by big pharmaceuticals, developments in clinical studies, payer attention, the reimbursement situation, the role of telemedicine in prescribing and increasing preference for non-injectable options. Additionally, the impact of treating obesity as a metabolic disease and not merely a lifestyle choice is analyzed.

- Competitive Strategies of Leading Companies: Provides an overview of how the top companies are establishing competitive advantages in the market based on product improvements, accelerated pipelines, differences in clinical trials, licensing agreements, expansion into new geographic markets, generating real-world evidence and managing product lifecycles. In addition, it includes comparisons of approved drugs, late-stage drugs and emerging oral obesity drugs.

- Pricing, Reimbursement and Market Access: Discusses issues related to pricing, payer restrictions, prior authorization, patient costs, lack of insurance coverage and health economic considerations. The emphasis is on how reimbursement and associated cost implications may affect market penetration in the transition of oral obesity drugs from specialty care to primary care and pharmacy settings.

- Opportunities in Markets & Expansion Strategies: Highlights growth prospects in the oral GLP-1 segment, oral dual incretins, oral triple agonists, oral small-molecule obesity drugs, tele pharmacy distribution, developing markets & new comorbidity-based treatment routes. The study offers key strategies for entering markets, positioning products, targeting patients, partnerships & commercialization in the changing oral obesity drugs space.

Target Audience

- Pharmaceutical Companies Developing Obesity and Metabolic Drugs

- Oral GLP-1, Dual Incretin and Triple Agonist Drug Developers

- Biotechnology Companies with Obesity and Cardiometabolic Pipelines

- Generic Drug Manufacturers Targeting Mature Oral Obesity Therapies

- CDMOs and API Manufacturers Supporting Oral Peptide and Small Molecule Production

- Obesity, Endocrinology and Metabolic Disease Clinics

- Retail, Specialty and Online Pharmacy Chains

- Telehealth and Digital Weight Management Platforms

- Health Insurance Companies, PBMs and Reimbursement Decision-Makers

- Investors, Venture Capital Firms and Strategic Healthcare Investors

Suggestions for Related Report

- Anti-Obesity Drugs Market

- Weight loss therapeutics Market

- Glucagon-like Peptide 1 (GLP-1) Analogues Market

- Global Diabetes Drugs Market

- Insulin Resistance Market

- NASH/MASH Treatment Market

- Global Metabolic Dysfunction-Associated Steatohepatitis (MASH) Drugs Market

- Cardiovascular Therapeutics Drugs Market

- Global Biosimilar Market