Life Science Instruments and Consumables Market Size & Industry Outlook

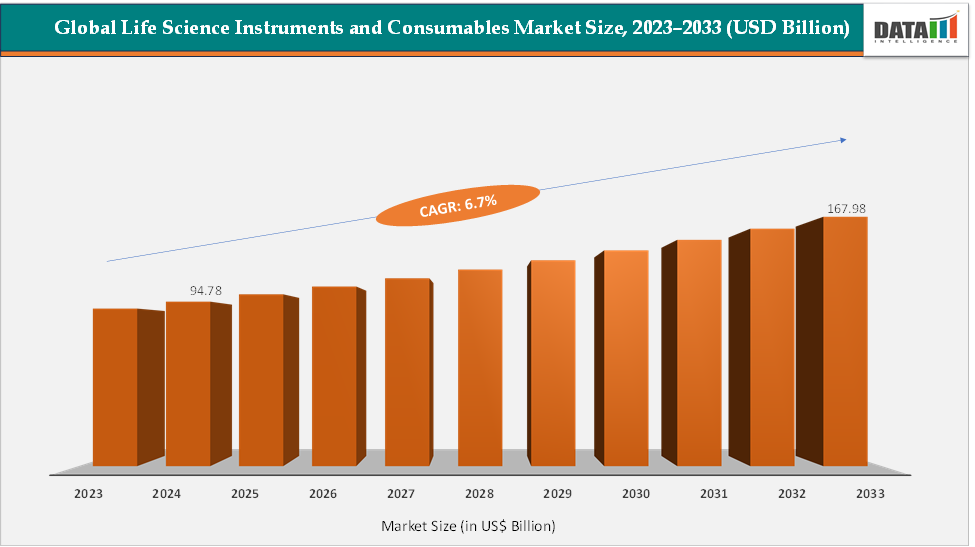

The global life science instruments and consumables market size reached US$ 94.78 Billion in 2024 from US$ 89.37 Billion in 2023 and is expected to reach US$ 167.98 Billion by 2033, growing at a CAGR of 6.7% during the forecast period 2025-2033. The market is witnessing significant growth, driven by technological advancements and rising investments in healthcare and research. Consumables such as pipette tips, cell culture plates, and centrifuge tubes are essential for daily laboratory operations, supporting breakthroughs in areas like genomics, proteomics, and molecular diagnostics.

Advanced technologies like Next-Generation Sequencing (NGS) and Polymerase Chain Reaction (PCR) are pivotal for a significant share in genomics research. Leading products, including Thermo Fisher’s Ion GeneStudio S5 System and Agilent’s SureSelectXT Target Enrichment System, exemplify approved instruments driving innovation in diagnostic and research applications. Overall, the market’s growth is propelled by the adoption of cutting-edge technologies and supportive regulatory frameworks.

Key Takeaways

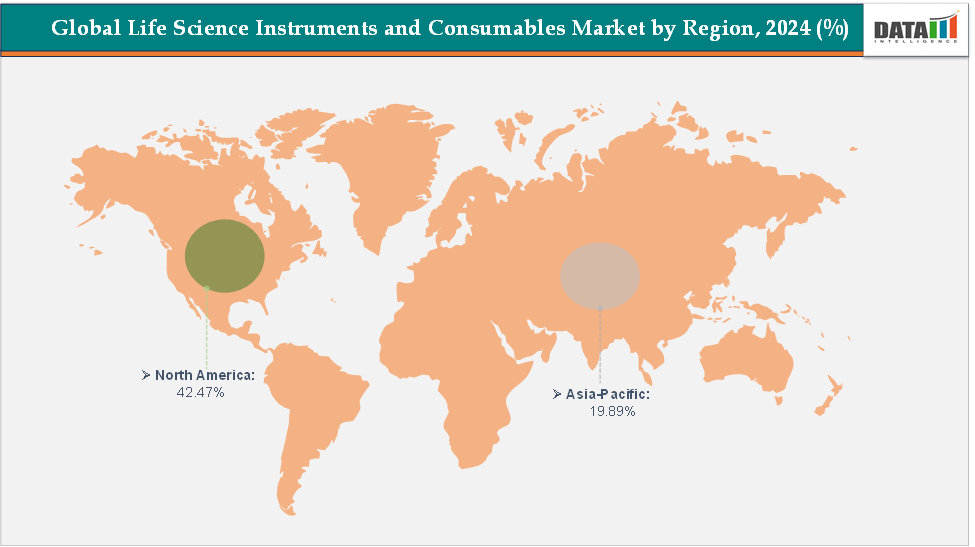

- North America dominates the life science instruments and consumables market with the largest revenue share of 42.47% in 2024.

- The Asia Pacific is the fastest-growing region and is expected to grow at the fastest CAGR of 6.9% over the forecast period.

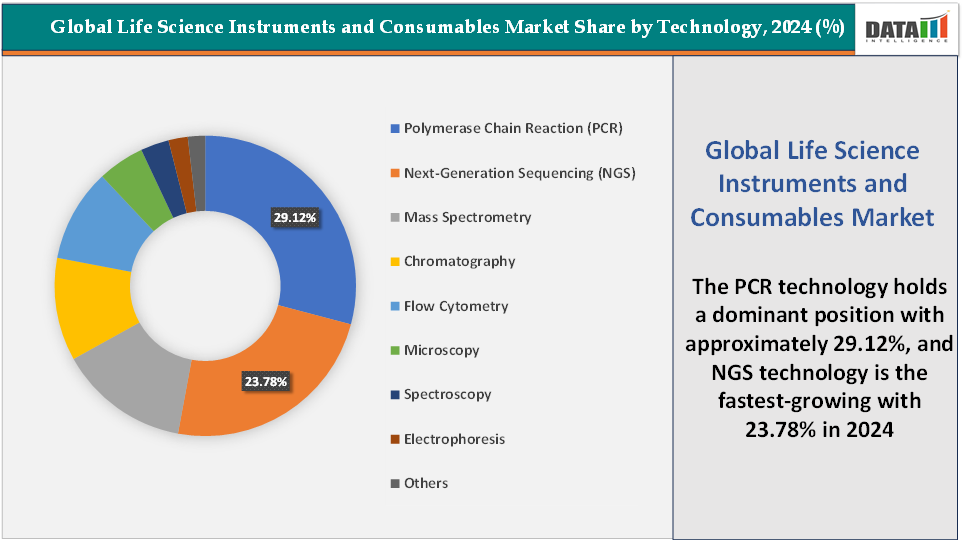

- Based on technology, the polymerase chain reaction (PCR) segment led the market with the largest revenue share of 29.12% in 2024.

- The major market players in the life science instruments and consumables market are Thermo Fisher Scientific Inc., Agilent Technologies, Inc., Danaher Corporation, Illumina, Inc., Bio-Rad Laboratories, Inc., PerkinElmer, Waters Corporation, QIAGEN, F. Hoffmann-La Roche Ltd, and Eppendorf SE, among others

Market Scope

| Metrics | Details | |

| CAGR | 6.7% | |

| Market Size Available for Years | 2022-2033 | |

| Estimation Forecast Period | 2025-2033 | |

| Revenue Units | Value (US$ Bn) | |

| Segments Covered | Product Type | Instruments and Consumables |

| Technology | Polymerase Chain Reaction (PCR), Next-Generation Sequencing (NGS), Mass Spectrometry, Chromatography, Flow Cytometry, Microscopy, Spectroscopy, Electrophoresis, and Others | |

| Application | Genomics, Proteomics, Cell Biology, Molecular Biology, Clinical Diagnostics, Pharmaceuticals, and Others | |

| End-User | Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, Hospitals, Diagnostic Laboratories, and Others | |

| Regions Covered | North America, Europe, Asia-Pacific, South America and the Middle East & Africa | |

Market Dynamics

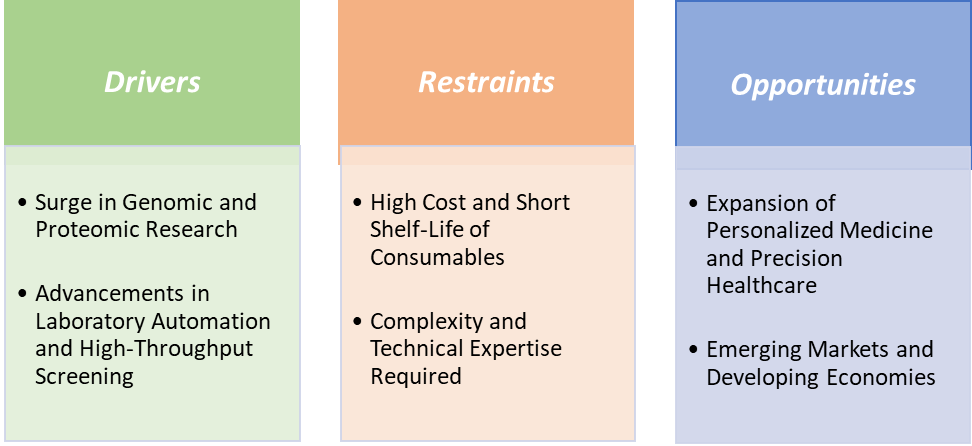

Drivers: Surge in genomic and proteomic research is significantly driving the life science instruments and consumables market growth

The rapid expansion of genomic and proteomic research has emerged as a pivotal force propelling the life science instruments and consumables market, as both fields are increasingly recognized as the backbone of precision medicine, early disease detection, and biomarker discovery. The growth is fueled by the declining costs and rising throughput of sequencing technologies, which have democratized access to powerful platforms such as Illumina’s MiSeq i100 and NovaSeq series, widely adopted for whole genome sequencing, RNA sequencing, and clinical diagnostics.

Similarly, in proteomics, demand for advanced Orbitrap and Q-TOF mass spectrometers has surged due to their unmatched sensitivity in protein analysis, while consumables such as PCR Biosystems’ VeriFi Library Amplification Mix and Thermo Fisher’s broad proteomic reagent kits ensure recurring revenue streams by supporting high-throughput workflows.

Strategic moves like Thermo Fisher’s acquisition of Olink Holding, a leader in protein biomarker technologies, demonstrate how industry giants are consolidating capabilities to strengthen their role in multi-omics research. Collectively, the convergence of technological innovation, supportive funding, regulatory validation, and expanding clinical applications underscores how genomic and proteomic research is not only driving demand for sophisticated instruments and consumables but also reshaping the very foundations of modern healthcare and drug discovery.

Restraints: Complexity and technical expertise required are hampering the growth of the market

The complexity and technical expertise required for operating advanced life science instruments and consumables are significant factors hampering market growth, particularly in developing regions and smaller research settings. Many platforms, such as next-generation sequencing (NGS) systems, mass spectrometers, and flow cytometers, demand highly trained personnel for sample preparation, instrument calibration, data analysis, and troubleshooting, which limits their accessibility beyond well-funded institutions.

For instance, NGS workflows often involve multiple steps such as DNA/RNA extraction, library preparation, sequencing, and bioinformatics interpretation, each requiring specialized skills and software expertise, creating barriers for labs lacking dedicated bioinformaticians. Similarly, proteomic analyses using Orbitrap or Q-TOF mass spectrometry require precise handling of sample complexity, ionization techniques, and computational modeling, which can delay adoption in clinical laboratories. The steep learning curve and the necessity for continuous training also add operational costs, especially in regions with a shortage of skilled professionals.

Moreover, improper handling or misinterpretation of data can compromise results, posing risks in sensitive applications such as clinical diagnostics or pharmacogenomics. Additionally, the integration of AI and advanced bioinformatics tools, though promising, further increases the complexity of workflows, necessitating multidisciplinary expertise. Consequently, the high dependency on specialized knowledge and training not only slows adoption but also widens the gap between advanced research hubs and under-resourced facilities, ultimately restraining the overall growth of the life science instruments and consumables market.

Life Science Instruments and Consumables Market, Segmentation Analysis

The global life science instruments and consumables market is segmented based on product type, technology, application, end-user, and region.

Technology: The polymerase chain reaction (PCR) segment is dominating the life science instruments and consumables market with a 29.12% share in 2024

The polymerase chain reaction (PCR) segment is dominating the life science instruments and consumables market owing to its unparalleled role as a gold-standard technique for amplifying DNA and RNA, making it indispensable across research, diagnostics, forensics, and drug discovery. PCR remains the most widely adopted molecular tool because of its simplicity, reliability, and versatility, offering applications in everything from infectious disease testing and genetic analysis to oncology and agricultural biotechnology.

For instance, products like Abbott’s RealTime SARS-CoV-2 Assay, Thermo Fisher Scientific’s TaqPath COVID-19 Combo Kit, and Roche’s cobas SARS-CoV-2 PCR Test represent some of the most commercially successful PCR-based diagnostic kits. PCR also plays a critical role in cancer diagnostics (detection of EGFR, BRAF, and KRAS mutations), pharmacogenomics (CYP450 genotyping), and prenatal testing, which has expanded its market presence further. The continued evolution of PCR technologies, such as digital PCR (dPCR) for absolute quantification and enhanced sensitivity, has opened new opportunities in liquid biopsy, rare mutation detection, and precision oncology, reinforcing the dominance of this segment.

PCR technology advancements by market players like Thermo Fisher, Bio-Rad, Qiagen, Quest, and Agilent are further accelerating the growth of the market. For instance, in July 2025, Quest Diagnostics launched a new diagnostic laboratory test for the Oropouche virus. Quest's advanced laboratory developed the diagnostic and performed the test using polymerase chain reaction (PCR) technology, with serology testing. Reverse transcription PCR testing can identify the RNA of the virus during the early stages of infection to aid diagnosis.

The next-generation sequencing (NGS) segment is the fastest-growing in the life science instruments and consumables market, with a 23.78% share in 2024

The next-generation sequencing (NGS) segment is the fastest-growing area of the life science instruments and consumables market, propelled by its transformative role in genomics, precision medicine, and large-scale population studies. Unlike traditional methods, NGS enables massively parallel sequencing, allowing billions of DNA or RNA fragments to be sequenced simultaneously with unmatched speed and cost-efficiency. This technological leap has accelerated its adoption in clinical diagnostics, oncology, infectious disease surveillance, reproductive health, and pharmacogenomics.

Novel technological advancements have further accelerated adoption. For instance, in February 2025, Roche unveiled its proprietary, breakthrough sequencing by expansion (SBX) technology, establishing a new category of next-generation sequencing. SBX chemistry, combined with an innovative sensor module, offers ultra-rapid, high-throughput sequencing that is both flexible and scalable for a broad range of applications. Next-generation sequencing provides detailed insights into genetics, genomics and cell biology.

Additionally, in July 2025, QIAGEN announced the launch of its new QIAseq xHYB Long Read Panels, a suite of target enrichment solutions designed to unlock long-read sequencing of genomically complex regions. This new offering strengthens QIAGEN’s position as a provider of differentiated solutions for use on any next-generation sequencing (NGS) platforms spanning both short- and long-read technologies.

Geographical Analysis

North America is expected to dominate the global life science instruments and consumables market with a 42.47% in 2024

North America is the dominant region in the global life science instruments and consumables market, driven by its high healthcare spending and early adoption of advanced technologies. North America leads in proteomics advancements, with Thermo Fisher’s Orbitrap Exploris series gaining wide adoption in biomarker discovery and drug development studies. The presence of established academic institutions, cutting-edge hospitals, and a robust network of contract research organizations (CROs) ensures steady demand for instruments and consumables across applications. Collectively, the combination of technological leadership, FDA-approved product pipelines, well-funded healthcare systems, and extensive clinical research programs makes North America the most dominant region in the global life science instruments and consumables market.

US Life Science Instruments and Consumables Market Trends

The United States accounts for the largest share, supported by a concentration of leading players such as Thermo Fisher Scientific, Illumina, Agilent Technologies, and Bio-Rad, all headquartered in the US and consistently launching innovative platforms. The dominance is fueled by significant investments in genomics, proteomics, and precision medicine, with initiatives like the All of Us Research Program aiming to sequence over a million genomes to advance personalized healthcare.

Moreover, strong regulatory frameworks and frequent FDA approvals accelerate technology adoption, such as Illumina’s TruSight Oncology (TSO) Comprehensive Test, the first FDA-approved comprehensive genomic profiling kit, and Thermo Fisher’s Ion Torrent Genexus System, which simplified next-generation sequencing (NGS) for clinical use. North America’s healthcare providers are also early adopters of PCR-based diagnostics, with FDA-approved kits like Abbott’s RealTime SARS-CoV-2 Assay and Roche’s cobas PCR Tests playing a vital role in the COVID-19 response and cementing the US leadership in molecular diagnostics.

The Asia Pacific region is the fastest-growing region in the global life science instruments and consumables market, with a CAGR of 6.9% in 2024

The Asia Pacific region is the fastest-growing market for life science instruments and consumables, driven by rapid healthcare modernization, expanding biotechnology and pharmaceutical industries, and rising investments in genomic and proteomic research. Countries like China, India, Japan, and South Korea are at the forefront, with governments heavily funding national genomics initiatives, clinical research infrastructure, and precision medicine programs. For instance, China’s Precision Medicine Initiative, backed by multi-billion-dollar funding, aims to accelerate large-scale genome sequencing.

The COVID-19 pandemic further accelerated growth, with Asian countries becoming large-scale users of PCR test kits and sequencing platforms, supported by global leaders like Thermo Fisher, Illumina, and Qiagen, as well as local players such as BGI in China and Takara Bio in Japan. BGI’s DNBSEQ platforms and Illumina’s NovaSeq series are widely adopted in Asian genomic labs, while Thermo Fisher’s PCR-based assays have gained regulatory clearance in multiple APAC markets for infectious disease testing. Rising prevalence of chronic diseases such as cancer and diabetes is also fueling demand for NGS-based oncology panels, liquid biopsy kits, and proteomic assays, particularly in urban hospitals across India and China.

Europe Life Science Instruments and Consumables Market Trends

Europe represents one of the most dynamic regions for the life science instruments and consumables market, with growth driven by strong research infrastructure, government-funded genomics and proteomics projects, and a well-established pharmaceutical and biotechnology sector. Key initiatives such as the 1+ Million Genomes Initiative (1+MG), which brings together over 20 EU countries to enable secure genomic data access, and the European Proteomics Infrastructure Consortium (EPIC-XS) are fueling the adoption of advanced instruments like next-generation sequencers, mass spectrometers, and high-throughput flow cytometry systems.

The European Medicines Agency (EMA) has also accelerated regulatory approvals of molecular diagnostics and genomic tests, enhancing clinical adoption for Roche’s cobas PCR test kits and Illumina’s TruSight Oncology test have been cleared for use across European markets, supporting precision oncology programs. Rising cancer incidence, with over 4 million new cases annually in Europe, and an aging population are increasing the demand for molecular diagnostics and biomarker discovery tools, further boosting instrument and consumable sales. Overall, Europe’s growth in the life science instruments and consumables market is being propelled by high disease burden, favorable regulatory frameworks, and strong demand for precision medicine, making it a key global hub for innovation and adoption.

Competitive Landscape

Top companies in the life science instruments and consumables market include Thermo Fisher Scientific Inc., Agilent Technologies, Inc., Danaher Corporation, Illumina, Inc., Bio-Rad Laboratories, Inc., PerkinElmer, Waters Corporation, QIAGEN, F. Hoffmann-La Roche Ltd, and Eppendorf SE, among others.

Key Developments

April 2026 – Thermo Fisher Scientific and Danaher expanding advanced laboratory automation solutions

Thermo Fisher Scientific Inc. and Danaher Corporation enhanced automated laboratory platforms and analytical instruments to improve research efficiency, sample throughput, and data accuracy across life science applications.

March 2026 – Illumina and QIAGEN advancing next-generation genomics technologies

Illumina, Inc. and QIAGEN expanded genomic sequencing and molecular diagnostics capabilities, supporting precision medicine, biomarker discovery, and clinical research initiatives.

February 2026 – Agilent Technologies and Waters strengthening analytical instrumentation portfolios

Agilent Technologies and Waters Corporation introduced enhancements in chromatography, mass spectrometry, and laboratory workflow solutions to meet growing demand from pharmaceutical and biotechnology research.

January–April 2026 – Rising investments in consumables and bioprocessing technologies

Companies such as Bio-Rad Laboratories, Roche, PerkinElmer, and Eppendorf increased focus on laboratory consumables, cell analysis tools, and bioprocessing solutions to support expanding drug discovery and life sciences research activities.

The global life science instruments and consumables market report delivers a detailed analysis with 70 key tables, more than 73 visually impactful figures, and 159 pages of expert insights, providing a complete view of the market landscape.