AI in Edge Computing Market Overview

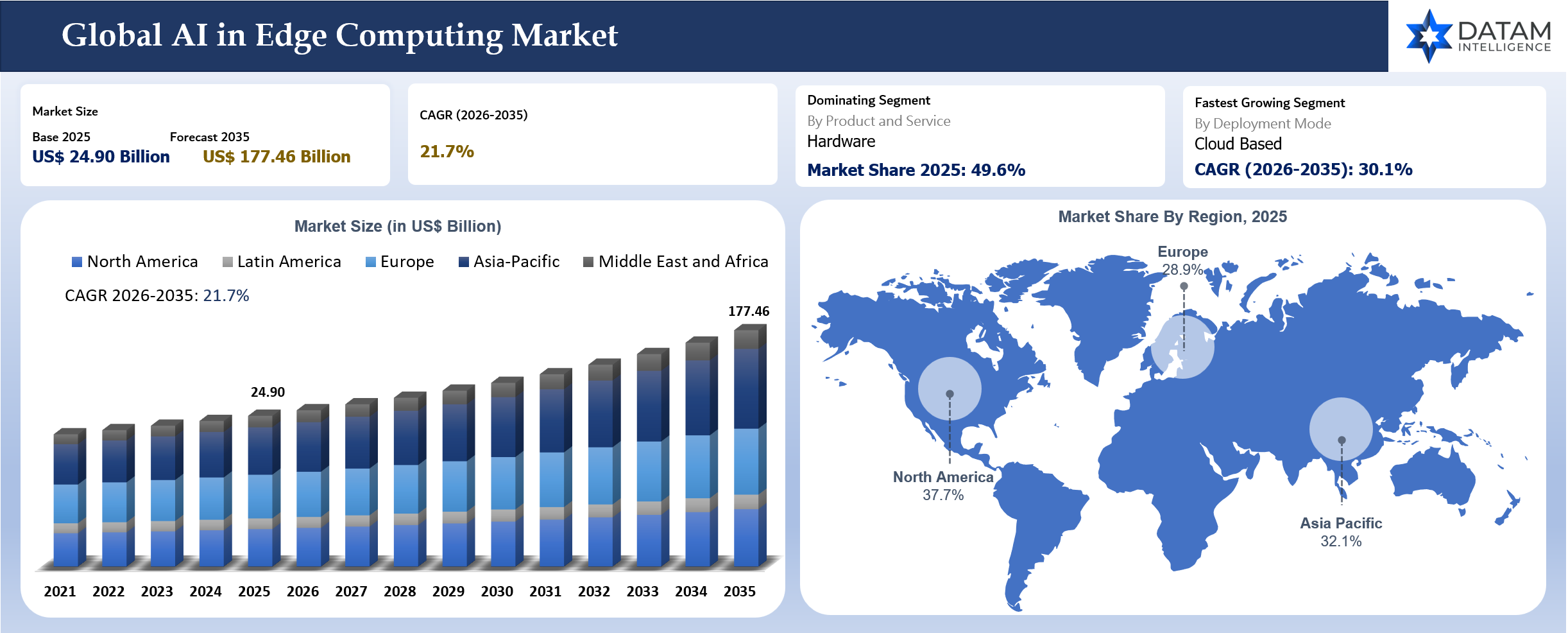

The global AI in Edge Computing Market reached US$ 24.90 billion in 2025 and is projected to reach US$ 177.46 billion by 2035, growing with a CAGR of 21.7% during 2026-2035. Enterprise architecture is moving from cloud-only processing toward distributed intelligence that keeps time-sensitive decisions near devices, gateways, enterprise data centers, and telecom edge sites. The most active buyers are not purchasing AI as a standalone idea. They are building repeatable infrastructure for local inference, model deployment, data filtering, monitoring, security and offline operation.

The market is best understood as a convergence of cloud platforms, edge infrastructure, AI accelerators, runtime middleware and domain-specific applications. Google Distributed Cloud supports low-latency and data residency needs at data centers and edge locations. AWS IoT Greengrass and Microsoft Azure IoT Edge bring cloud-trained models and application logic to local devices. Intel OpenVINO supports model optimization across hardware targets. NVIDIA Jetson and industrial AI systems from Advantech, ADLINK, and Supermicro show how compute hardware is being packaged for production environments.

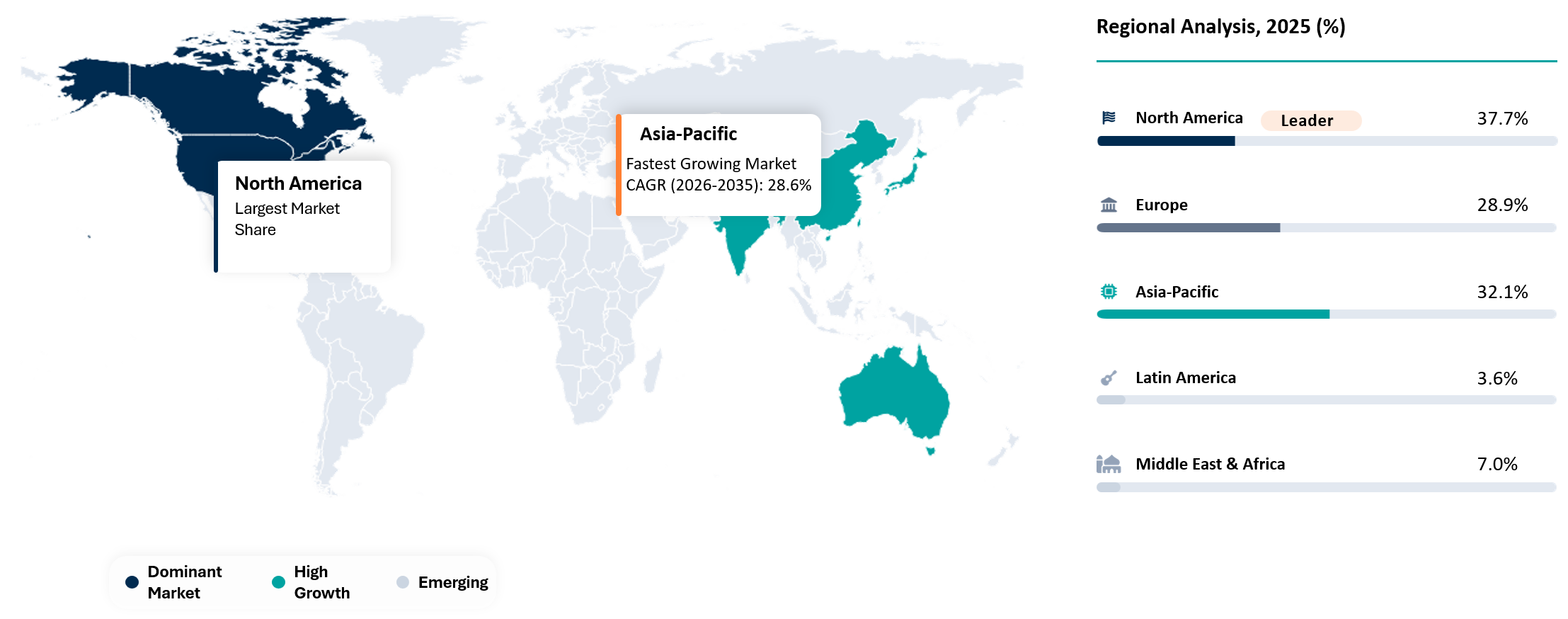

North America remains the largest market because cloud providers, chip designers, and enterprise technology companies shape platform standards. Asia-Pacific is the fastest-growing region because electronics manufacturing, smart factories, robotics, telecom deployments, and connected devices are scaling quickly. Europe is gaining traction through manufacturing automation and regulation-driven requirements for trustworthy AI, cybersecurity, and local data control.

Architecture choices now decide commercial value. A workload can run on an endpoint, a gateway, an enterprise edge cluster, or a telco node. Each choice changes the power budget, security responsibility, data flow, service contract, and integration complexity. Research that separates those locations gives clients a more useful basis for pricing, partnership, and product planning.

AI in Edge Computing Market : Key Takeaways

- North America held the largest revenue share at 37.7% in 2025 because cloud hyperscalers, semiconductor leaders, industrial edge vendors, and enterprise software providers are concentrated around high-value deployments in the U.S. and Canada.

- Asia-Pacific is the fastest-growing region with a CAGR of 26.8% because electronics manufacturing, robotics, connected factories, smart cameras, and telecom edge infrastructure are scaling rapidly across Japan, China, South Korea, India, and Southeast Asia.

- Europe accounted for a 28.9% share in 2025, supported by industrial automation demand, automotive software development, manufacturing quality inspection, energy infrastructure monitoring, and stricter data governance requirements across Germany, France, Italy, Spain, and the UK.

- Software is becoming the main control layer because model optimization, inference runtime, device orchestration, security patching, and lifecycle management decide whether distributed devices can be updated safely across factories, stores, hospitals, and telecom sites.

- Hardware remains a critical buying decision because GPU, NPU (Neural Processing Unit), TPU (Tensor Processing Unit), FPGA (Field Programmable Gate Array), and ASIC (Application Specific Integrated Circuit) choices directly influence latency, power draw, thermal design, and bill of materials.

- Managed operations will gain stronger commercial relevance as enterprises move from isolated pilots to large fleets of cameras, gateways, industrial PCs, robots, and medical devices that need monitoring, patching, cybersecurity, and performance tuning.

- Device edge and gateway edge deployments are gaining traction because manufacturers, retailers, logistics operators, and healthcare facilities need faster local inference where cloud-only processing can create latency, bandwidth, privacy, or uptime limitations.

Global AI in Edge Computing Market Industry Trends and Strategic Insights

The architecture trend is clear: training, large-scale analytics, and fleet learning remain cloud-centered, while inference, filtering, and urgent operational decisions move closer to equipment and users. A camera feed in a factory, a sensor stream in an energy site, or a robot navigation task cannot always wait for a distant region cloud. Distributed intelligence reduces delay, lowers data transfer volume, and supports operations during connectivity loss.

Hybrid cloud to local infrastructure is becoming the default operating pattern. Google Distributed Cloud, Azure IoT Edge, AWS IoT Greengrass, Red Hat Device Edge, and Dell NativeEdge show that enterprises want central policy control with local execution. The commercial question is no longer whether edge locations can run AI. The question is which control plane manages them across thousands of sites.

Telco edge and MEC (Multi Access Edge Computing) remain strategically important but must be sized carefully. Telecom sites can host low-latency workloads but many commercial applications still depend on enterprise buyer budgets, application developer ecosystems and reliable service-level agreements. The most monetizable opportunities are likely to combine telecom connectivity with manufacturing, retail, public safety or logistics applications.

AI in Edge Computing Market Scope

| Metrics | Details |

| 2025 Market Size | US$ 24.90 Billion |

| 2035 Projected Market Size | US$ 177.46 Billion |

| CAGR 2026-2035 | 21.7% |

| Largest Market | North America |

| Fastest Growing Market | Asia-Pacific |

| By Solution | Hardware, Software, Professional and Managed Services |

| By Edge Location | Device and Endpoint Edge, Gateway and Industrial Edge, Enterprise Edge and On Prem Data Center, Telco Edge and MEC (Multi Access Edge Computing) |

| By Deployment Mode | On Premises, Cloud Based, Hybrid |

| By Channel Route | Direct Enterprise Sales, Cloud Marketplace, OEM (Original Equipment Manufacturer) and Embedded Design Wins, System Integratos and Managed Service Providers, Value Added Resellers and Distributors |

| By Organization Size | Large Enterprises, Small and Medium Enterprises |

| By Application | Vision and Perception, Industrial and Operational Intelligence, Autonomy and Interaction, Others |

| By End-User | Manufacturing and Industrial, Automotive and Mobility, Healthcare and Medical Devices, Retail and QSR (Quick Service Restaurants), Telecom and Service Providers, Energy and Utilities, Smart Cities and Public Safety, Logistics and Warehousing, Consumer Electronics and Wearables, Others |

| By Region | North America: U.S., Canada, Mexico Europe: Germany, UK, France, Russia, Spain, Italy, Netherlands Asia-Pacific: China, India, Japan, Australia, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam Latin America: Brazil Middle East and Africa: UAE, Saudi Arabia, Israel, Turkiye |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth, Pricing Intelligence, Technology Benchmarking, Partner Mapping |

Strategic Indicators For Global AI in Edge Computing Market

High Regulation Impact

Regulation is rising around AI safety, cybersecurity and critical infrastructure. EU AI Act rules affect high-risk systems and product-integrated AI. EU Cyber Resilience Act obligations also matter because edge devices often combine hardware, embedded software and network access.

Industrial buyers increasingly ask suppliers to prove secure updates, access control, model documentation and vulnerability handling. Such requirements are strongest in healthcare, public safety, telecom, energy and factory environments where local decisions can affect safety or continuity.

Vendors with documented governance, auditable model release processes and secure device management will earn stronger procurement trust. Regulation will not stop adoption but it will raise the bar for poorly documented embedded software.

High Investment Activity

Investment is concentrated around chips, runtime software, orchestration, industrial AI applications and developer ecosystems. NVIDIA, Intel, Qualcomm, AMD, Arm and cloud providers are shaping the stack from silicon to model deployment tools.

Capital is also moving into rugged systems, compact servers, industrial PCs and gateway hardware. Advantech, ADLINK, Supermicro, Dell and HPE are positioning products for plants, stores, hospitals, telecom sites and remote facilities.

Investment quality should be judged by production readiness rather than announcements. Stronger signals include supported model libraries, reference designs, validated partner devices, update tools and field deployments with measurable uptime.

Supply Chain Disruption

Supply risk is tied to advanced chips, memory, sensors, industrial PCs and thermal components. Export controls, semiconductor lead times and platform certification delays can affect deployment schedules even when software is ready.

Edge hardware is harder to substitute after validation because a new accelerator may change latency, model accuracy, power draw or thermal behavior. A medical device, inspection camera or robot controller may require new testing if hardware changes mid-cycle.

Buyers are therefore asking for second-source options, long-life industrial SKUs, module availability and security patch guarantees. Suppliers with stable roadmaps and broad channel access can defend share during capacity stress.

Pricing Volatility

Pricing is split across modules, edge servers, software licenses, runtime subscriptions and managed services. Hardware costs can fall with larger production runs but ruggedization, certification and GPU availability can keep deployed system prices high.

Software pricing is moving toward per device, per workload and enterprise subscription models. Model optimization tools and runtime middleware command value when they reduce cloud compute cost or prevent operational downtime.

A useful pricing view should separate accelerator bill of materials from orchestration software and services. Bundled platform pricing can hide margin movement and make supplier benchmarking weak.

Procurement Pressure

Procurement teams are no longer buying isolated devices. They are buying update paths, support windows, cybersecurity posture, ecosystem compatibility and the ability to run multiple models across distributed locations.

Manufacturers and retailers often face pressure from operations teams that want quick payback but limited disruption to existing OT (Operational Technology). A model that works in a lab can fail commercially if installation, training and device monitoring are difficult.

Vendors that package validated reference architectures for inspection, safety, predictive maintenance and video intelligence can reduce buyer risk. Generic AI claims carry less weight than deployed workflow evidence.

New Technology Adoption

Adoption is shifting toward multimodal workloads that combine video, audio, sensor signals and language interfaces. A store, machine cell or vehicle may need several smaller models working together rather than one large model running in the cloud.

Model compression, quantization and distillation are now core to field deployment. OpenVINO, TensorRT style workflows and vendor SDKs help teams fit models within local power and memory limits.

The next adoption wave will favor hybrid patterns. Training and heavy analytics stay in the cloud while inference, alerting and immediate control run locally where latency, privacy or network resilience is critical.

Why AI in Edge Computing Market Matters in 2026

The global AI in Edge Computing market is entering a new phase of accelerated adoption as organizations prioritize real-time intelligence, low-latency processing, and secure data handling at the edge.

AI in edge computing is transforming how businesses process and analyze data by enabling intelligent decision-making closer to where data is generated. This reduces reliance on centralized cloud infrastructure, minimizes latency, enhances privacy, and improves operational efficiency across industries.

Several macroeconomic and technology trends are driving market growth:

- Increasing demand for real-time AI inference and analytics

- Expansion of 5G and next-generation wireless networks

- Growing need for low-latency applications

- Increasing deployment of Edge Computing autonomous vehicles and connected mobility

- Growing adoption of edge AI in healthcare and remote patient monitoring

- Advancements in AI accelerators, edge processors, and semiconductor technologies

- Increasing cybersecurity concerns driving localized data processing

- Government initiatives supporting AI, digital infrastructure, and smart city development

Analyst View

DataM Intelligence Analyst Perspective

The AI in Edge Computing market is rapidly evolving from isolated edge deployments into a scalable intelligent computing ecosystem that powers next-generation digital transformation.

The long-term success of the market will depend on:

- Continuous advancements in AI chipsets and edge processors

- Expansion of high-speed 5G and edge infrastructure

- Robust cybersecurity and data privacy frameworks

- Efficient AI model optimization and deployment

- Seamless integration with cloud and hybrid computing environments

- Industry-specific AI applications and software ecosystems

- Strategic partnerships among semiconductor, cloud, and AI technology providers

The United States continues to lead in AI innovation, semiconductor development, and enterprise edge deployments, while China is accelerating commercialization through large-scale smart manufacturing, AI infrastructure, and government-backed digital transformation initiatives. Japan and South Korea are expanding edge AI adoption across robotics, industrial automation, and connected mobility. India is emerging as a high-growth market, driven by digital transformation programs, expanding 5G networks, smart city initiatives, growing IoT adoption, and increasing investments in AI-enabled enterprise solutions.

Regional Expansion Opportunity in AI in Edge Computing Market

North America Holds the Largest AI in Edge Computing Market Share

North America dominates the AI in Edge Computing Market, driven by rapid adoption of AI-powered edge devices, strong cloud and semiconductor ecosystems, widespread Industrial IoT (IIoT) deployment, and significant investments in 5G, autonomous systems, and enterprise AI. The region benefits from the presence of leading AI chip manufacturers, hyperscale cloud providers, and edge computing innovators.

United States

The United States is the largest contributor to regional growth, supported by extensive deployment of AI at the edge across manufacturing, healthcare, retail, automotive, telecommunications, and defense sectors.

Organizations are increasingly implementing edge AI to enable real-time data processing, reduce latency, improve cybersecurity, and minimize cloud bandwidth costs. AI-enabled cameras, autonomous robots, smart factories, connected vehicles, and intelligent healthcare devices continue to accelerate demand.

Federal investments in AI research, semiconductor manufacturing, digital infrastructure, and next-generation networking further strengthen the country's leadership in edge computing innovation.

U.S. AI in Edge Computing Market

The U.S. market is characterized by strong adoption of AI accelerators, edge servers, embedded processors, and intelligent IoT devices that support real-time analytics and autonomous decision-making.

Manufacturing companies deploy AI at the edge for predictive maintenance and quality inspection, while healthcare providers utilize edge AI for medical imaging, patient monitoring, and clinical diagnostics.

Telecommunication providers leverage Multi-access Edge Computing (MEC) to support low-latency 5G services, and automotive manufacturers integrate edge AI into connected and autonomous vehicles.

Enterprises increasingly prioritize secure, scalable, and energy-efficient edge AI platforms capable of processing sensitive data locally while meeting regulatory and cybersecurity requirements.

Asia-Pacific Registers the Fastest Growth

Asia-Pacific is projected to record the fastest CAGR during the forecast period, fueled by rapid industrial digitalization, smart manufacturing initiatives, expanding 5G infrastructure, AI adoption across enterprises, and increasing deployment of connected devices.

China, Japan, South Korea, and India are the major growth engines.

China leads the region through aggressive investments in AI infrastructure, smart cities, intelligent manufacturing, and autonomous mobility.

Japan and South Korea continue expanding AI-powered robotics, industrial automation, semiconductor innovation, and intelligent electronics.

India represents one of the fastest-growing opportunities due to:

- Rapid digital transformation across industries

- Expansion of smart manufacturing initiatives

- Increasing adoption of AI-enabled IoT solutions

- Growing investments in 5G networks and edge infrastructure

- Rising demand for real-time analytics across healthcare, retail, and logistics

Europe AI in Edge Computing Market

Europe is witnessing steady market expansion, supported by Industry 4.0 adoption, digital sovereignty initiatives, AI regulations, and increasing investments in industrial automation and intelligent transportation.

Germany, France, the United Kingdom, Italy, and the Netherlands are leading regional adoption across manufacturing, automotive, energy, healthcare, and smart infrastructure.

European enterprises increasingly deploy edge AI to improve operational efficiency, enhance cybersecurity, support predictive maintenance, and enable privacy-preserving AI applications that comply with evolving data protection regulations.

Latin America AI in Edge Computing Market Outlook

Latin America is steadily expanding its AI in edge computing adoption through digital transformation initiatives, industrial automation, smart retail, financial services modernization, and growing investments in telecommunications infrastructure.

Brazil, Mexico, and Chile are key markets adopting edge AI for manufacturing, logistics optimization, intelligent surveillance, and smart city applications.

Middle East & Africa AI in Edge Computing Market Outlook

The Middle East & Africa region presents significant long-term growth opportunities, driven by smart city projects, AI-powered public services, expanding 5G deployments, and digital economy initiatives.

Saudi Arabia and the UAE are leading investments in AI-enabled infrastructure, autonomous transportation, intelligent energy management, and smart government services, while African nations are increasingly adopting edge AI for healthcare, agriculture, telecommunications, and industrial automation.

Government Policy Support

Policy support comes from semiconductor funding, 5G infrastructure, industrial digitization, smart city programs and AI governance frameworks. The U.S. CHIPS Act supports domestic semiconductor capacity while NIST frameworks guide risk management.

Europe supports trustworthy AI and cybersecurity through horizontal regulation. The approach increases compliance work but also creates a premium for secure and auditable deployments in regulated environments.

Japan, South Korea and China support industrial automation and robotics through national technology agendas. Policy support is strongest where local inference improves resilience, productivity and data control.

Recent Merger Activity Or Funding in AI in Edge Computing Market

- In June 2026, Supermicro expanded its AI at the Edge portfolio with new Intel-powered platforms optimized for low-latency AI inference across manufacturing, retail, logistics, and industrial automation. The systems feature Intel Core Ultra Series processors, Intel Arc Pro GPUs, and scalable GPU configurations to accelerate enterprise edge AI deployments.

- In June 2026, indie Semiconductor introduced the iND881 Edge AI System-on-Chip (SoC), designed for automotive smart cameras, robotics, and intelligent perception systems. The new processor combines AI acceleration with advanced image signal processing to enable real-time edge inference.

- In June 2026, Kontron AG partnered with Intel to expand its industrial Edge AI portfolio using Intel Core Ultra Series 3 (Panther Lake) processors. The collaboration focuses on delivering energy-efficient AI platforms for industrial automation, smart factories, and IoT applications.

- In May 2026, Hanwha Vision and Ambarella signed a long-term strategic agreement valued at over US$800 million to accelerate Edge AI adoption across robotics, industrial automation, surveillance, and life sciences using Ambarella's edge AI platform.

- In January 2026, Datavault AI expanded its collaboration with IBM and Available Infrastructure to deploy enterprise-grade AI at the edge through the SanQtum AI platform, enabling secure, low-latency AI processing across distributed micro edge data centers in the United States.

- In January 2026, Scale Computing showcased its AI-ready edge computing solutions at NRF 2026, highlighting infrastructure designed to support AI workloads, point-of-sale systems, video analytics, and digital retail applications at distributed edge locations.

- In January 2026, Lantronix unveiled its SmartEdge.ai Gateway and SmartSwitch.ai at CES 2026, introducing an integrated Edge AI platform that combines AI inference, connectivity, and real-time video analytics for enterprise and industrial environments.

New Product Launches in AI in Edge Computing Market

- NVIDIA Jetson Thor positioned advanced local compute for physical AI, humanoid robotics and multimodal sensor processing.

- Canonical introduced Ubuntu Core 26 for secure and attested edge workloads with a focus on device fleets and critical infrastructure.

- Siemens Industrial AI Suite became generally available to support model deployment, connectivity, inference and monitoring on the shop floor.

- Advantech launched additional industrial systems for high-performance local inference in robotics, advanced medical imaging and factory automation.

- Supermicro continued expanding edge systems that support predictive and generative workloads near data sources.

- ADLINK promoted GenAI-ready computing and high-performance inference platforms for industrial, medical and supply chain use cases.

Company Coverage Preview

Alphabet Inc. deserves detailed coverage because Google Cloud is one of the most relevant platform providers for distributed AI workloads. Google Distributed Cloud extends infrastructure and AI services to data centers and edge locations where customers need low latency, data residency, survivability and consistent management. The company has a differentiated position when buyers want one governance model across cloud and local execution environments.

Google’s USP is the cloud-backed control plane combined with AI tooling, Kubernetes lineage and data services. The product story is not only about running models locally. It is about managing policy, security, updates and application consistency across locations that may include stores, factories, telecom facilities and public sector environments.

Competitive benchmarking should compare Google against AWS, Microsoft, Red Hat, Dell, HPE and industrial platforms. Google can be strong where customers value managed cloud practices at the edge, but account wins will depend on partner hardware, vertical application depth, integration support and procurement alignment with existing cloud commitments.

AI Impact Analysis

AI changes edge computing from a latency solution into an operating intelligence layer. Earlier edge infrastructure projects focused on moving compute closer to users. Current deployments increasingly focus on inference, anomaly detection, automated inspection, video understanding, local language assistance and robotics support.

Generative AI is expanding the conversation but enterprise use will be selective. Local small language models can support technician instructions, voice interaction, document search and context summaries. Larger models remain better suited to cloud or enterprise data centers because compute, memory and governance demands are higher.

The highest-value impact comes from closed-loop operations. A local system can detect an anomaly, notify an operator, update a work order and send summarized data to the cloud. Such workflows create measurable value because they reduce reaction time without removing enterprise governance.

Disruption Analysis

Disruption is occurring in workload ownership. Cloud teams, plant engineers, telecom operators and device OEMs are now sharing responsibility for AI-enabled operations. The boundary between cloud software and embedded systems is becoming less clear.

A second disruption comes from the shift in data economics. Sending every image, audio event or machine signal to the cloud creates bandwidth, storage and privacy costs. Local filtering changes the cost structure by transmitting only events, metadata or compressed insights.

The third disruption is platform lock-in at the control plane. Once a customer standardizes on cloud to local orchestration, device identity and runtime monitoring, the platform can influence future application choices. Market share should therefore track where enterprises place their operational control.

BCG Matrix: Company Evaluation

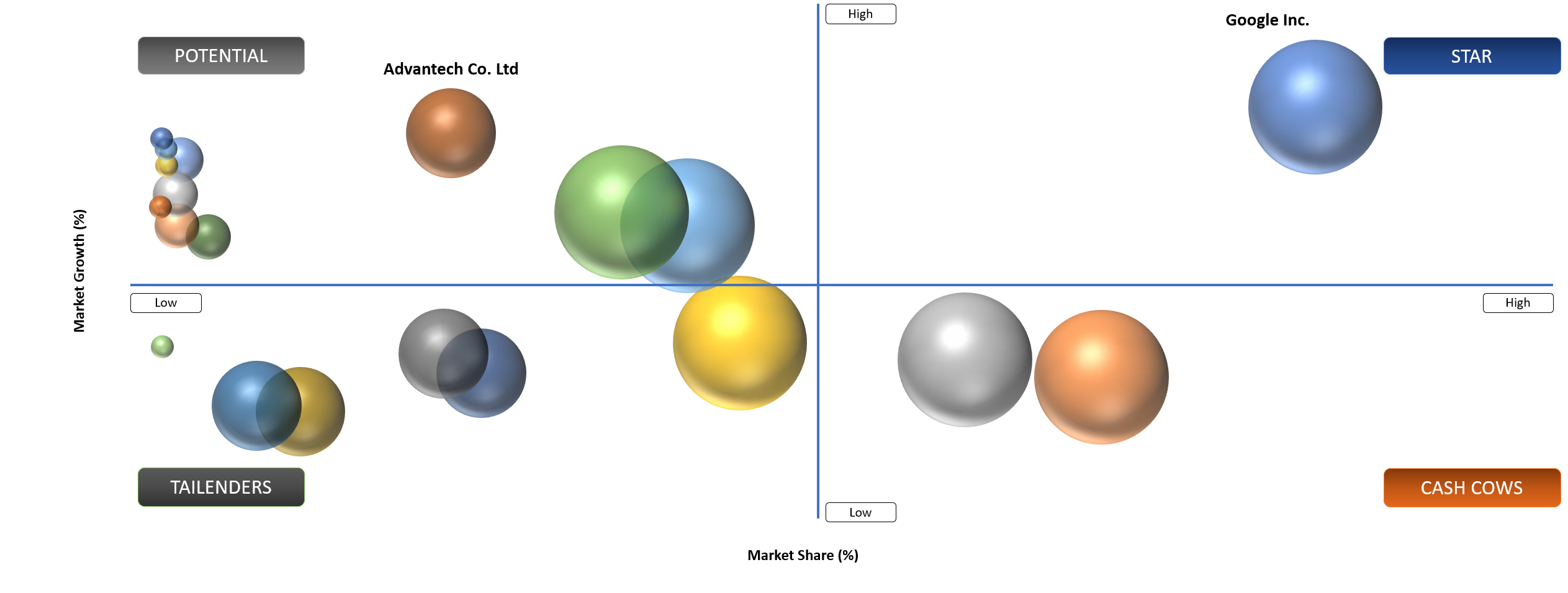

Stars

Stars include Google LLC, Amazon.com Inc., Microsoft Corporation and NVIDIA Corporation because they control the most commercially valuable layers of edge intelligence deployment. Google LLC, Amazon.com Inc. and Microsoft Corporation extend cloud governance, AI model deployment, device management and enterprise security toward distributed infrastructure. NVIDIA Corporation holds a strong position through GPU (Graphics Processing Unit) acceleration, Jetson modules, AI software tools and developer adoption across robotics, computer vision, industrial inspection and autonomous systems.

Potential

Potential companies include Qualcomm Incorporated, Intel Corporation, NXP Semiconductors N.V., Hailo Technologies Ltd. and Dell Technologies Inc. because they are well placed to capture design wins in embedded devices, gateways, industrial PCs, edge servers and low power inference workloads. Qualcomm Incorporated and Intel Corporation support broad compute adoption across devices and enterprise hardware. NXP Semiconductors N.V. strengthens automotive and industrial embedded use cases. Hailo Technologies Ltd. brings focused accelerator capabilities for vision AI while Dell Technologies Inc. supports enterprise edge infrastructure through AI ready servers and managed deployment channels.

AI in Edge Computing Market Dynamics & Trends

Driver Impact Analysis

Enterprise AI Workloads Are Moving From Central Clouds To Local Execution Points

The strongest growth driver is the need to place AI workloads where data is created. Manufacturing equipment, cameras, sensors, vehicles and telecom nodes generate streams that become expensive or risky when moved fully to the cloud.

Local execution improves response time and supports continuity when connectivity is weak. A factory inspection system or energy asset monitoring workflow cannot depend on an unstable network during production-critical events.

Cloud platforms remain essential because they manage training, governance and fleet learning. The commercial opportunity lies in connecting cloud discipline with local action through runtime software, orchestration and services.

Restraint Impact Analysis

Ownership Boundaries Between Cloud, IT, OT And Telecom Teams Create Deployment Friction

The main restraint is organizational complexity. Cloud teams manage AI models and policies. IT teams manage security and networks. OT teams protect uptime and plant safety. Telecom teams manage connectivity and MEC sites. Deployment can slow when ownership is unclear.

Technical integration also creates friction. Workloads may require containers, device drivers, hardware acceleration, data pipelines and local failover. A small mismatch between enterprise security policy and field device capability can delay rollout.

Vendors that reduce handoffs across teams will gain advantage. Clear reference architectures, integration templates, managed operations and domain-specific partner ecosystems can shorten the path from pilot to scaled rollout.

AI in Edge Computing Market Segmentation Analysis

Software Layer Becomes The Commercial Control Point

The enterprise edge and on prem data center layer is the most important architecture view because many customers want cloud-like governance without sending every operational data stream to a distant region. Factories, hospitals, retailers, logistics hubs and telecom facilities need controlled local execution with central policy visibility.

The layer bridges two worlds. Data science teams build and test models in cloud or data center environments while site teams need reliable local execution. The bridge requires runtime, middleware, security, monitoring and lifecycle management rather than only hardware procurement.

Google Distributed Cloud, Azure IoT Edge, AWS IoT Greengrass, Red Hat Device Edge and Dell NativeEdge demonstrate a shared direction. Customers want consistent management across distributed sites but they also need local speed, data control and resilience.

Hardware still matters because local nodes must match workload intensity. Vision-heavy operations require GPU or NPU acceleration while maintenance analytics may work on smaller industrial PCs. Architecture choices decide cost and future flexibility.

Two areas deserve closer treatment: runtime and middleware and model optimization and compression software. Both determine whether a distributed workload can be moved, monitored and updated across different edge locations.

Model Optimization And Compression Software Becomes The Deployment Gatekeeper

Model optimization decides whether a trained model can run within the memory, power and latency limits of a real device. Quantization, pruning, distillation and graph optimization reduce compute load while preserving accuracy. The value is practical because a smaller model can fit on a lower-cost device or run faster on an existing industrial PC.

OpenVINO illustrates the direction of travel because it targets deployment from cloud to edge across multiple hardware types. NVIDIA, Qualcomm and Arm also support optimization workflows through their developer ecosystems. Buyers increasingly ask whether a vendor can support existing PyTorch, TensorFlow or ONNX models without forcing a full rebuild.

Commercial demand is strongest in computer vision, audio event detection, robotics and predictive maintenance. Each workload generates high data volume but does not always need cloud processing. Optimization software becomes a bridge between data science teams and plant engineers.

Pricing can follow developer seats, enterprise subscriptions, runtime bundles or professional services. Supplier evaluation should track model coverage, accelerator support, accuracy retention, update process and integration with fleet monitoring tools.

Runtime And Middleware Control The Long-Term Customer Relationship

Runtime and middleware decide how models are packaged, deployed, monitored and updated after the first installation. The layer handles containers, device identity, data routing, local messaging, security policies and integration with cloud services or plant systems.

AWS IoT Greengrass, Azure IoT Edge, Google Distributed Cloud and Red Hat Device Edge show how enterprise platforms are extending cloud-native practices to distributed endpoints. Siemens Industrial Edge shows how industrial automation vendors are building shop-floor deployment environments that fit OT expectations.

The business value lies in lifecycle management. A failed model update can halt inspection, miss a safety event or create noisy alerts that operators ignore. Strong middleware reduces downtime by enabling staged rollouts, rollback, monitoring and policy control.

Runtime ownership is strategically sensitive because it can determine which cloud, chip or systems integration partner stays embedded in the account. Companies that control this layer can influence future applications, support revenue and customer data architecture.

Geographical Penetration

North America Market Landscape

North America leads because cloud control planes, AI chip design, enterprise software and private network ecosystems are concentrated in the U.S. The region is also home to early adopters in advanced manufacturing, logistics, retail, healthcare and energy.

Enterprise demand is increasingly tied to data governance and infrastructure resilience. Buyers want to keep sensitive video, medical, industrial or public sector data close to the source while still using cloud-based policies and model management.

The region also benefits from private 5G, campus networks and defense-related edge use cases. Vendors that can combine local inference with secure networking and compliance evidence have an advantage in high-value accounts.

U.S. Market Landscape

The U.S. is the leading country because Google, AWS, Microsoft, NVIDIA, Intel, Qualcomm, IBM, Dell, HPE and Cisco influence platform direction. The country has strong demand for distributed AI in stores, plants, hospitals, energy assets and public infrastructure.

Public policy shapes supply and risk management. Semiconductor incentives, NIST AI RMF guidance and cybersecurity expectations encourage enterprises to treat distributed AI as critical infrastructure rather than experimental software.

Commercial adoption is strongest where local execution cuts cost or protects privacy. Retail video analytics, manufacturing inspection, hospital workflow support and remote asset monitoring are key examples where buyers can see operational returns.

Asia-Pacific Market Landscape

Asia-Pacific is the fastest-growing region because electronics production, robotics, smart cameras, telecom infrastructure and industrial automation are concentrated across Japan, China, South Korea, Taiwan, India and Southeast Asia. The region also has strong demand for cost-optimized deployment bundles.

Japanese and South Korean firms bring precision manufacturing, sensors and robotics expertise. Chinese suppliers scale cameras, embedded systems and AI hardware quickly. Indian demand is rising through manufacturing digitization, logistics automation and smart city projects.

Competitive intensity is high because local hardware ecosystems can reduce system cost. International vendors need partner-led deployment models, language support, ruggedized hardware and strong after-sales service to win outside premium accounts.

Japan Market Landscape

Japan is a high-value technical market because robotics, machine vision, automotive electronics and precision manufacturing require reliable local intelligence. Factory operators value low downtime, quality consistency and long product lifecycles more than headline AI claims.

Aging workforce pressures also support automation. Local inference can help operators monitor equipment, guide technicians and maintain output quality where skilled labor is constrained. Robotics and inspection use cases fit Japan’s industrial base especially well.

Procurement tends to favor validated suppliers with strong support and product reliability. International providers can succeed when they integrate with Japanese automation practices and show clear lifecycle support for industrial environments.

Europe Market Landscape

Europe is shaped by industrial automation and regulation-driven trust. Germany, France, the UK, Italy, Spain, Netherlands and Nordic countries are attractive for manufacturing, energy, logistics and healthcare deployments that need security and explainability.

EU AI Act and Cyber Resilience Act requirements increase documentation needs for suppliers. Vendors selling into Europe need stronger evidence around model governance, cybersecurity and product lifecycle management than in less regulated markets.

Germany is especially important because machine builders and plant operators need local analytics that connect with existing automation assets. Siemens and other OT suppliers have an advantage because they understand shop-floor integration and industrial service models.

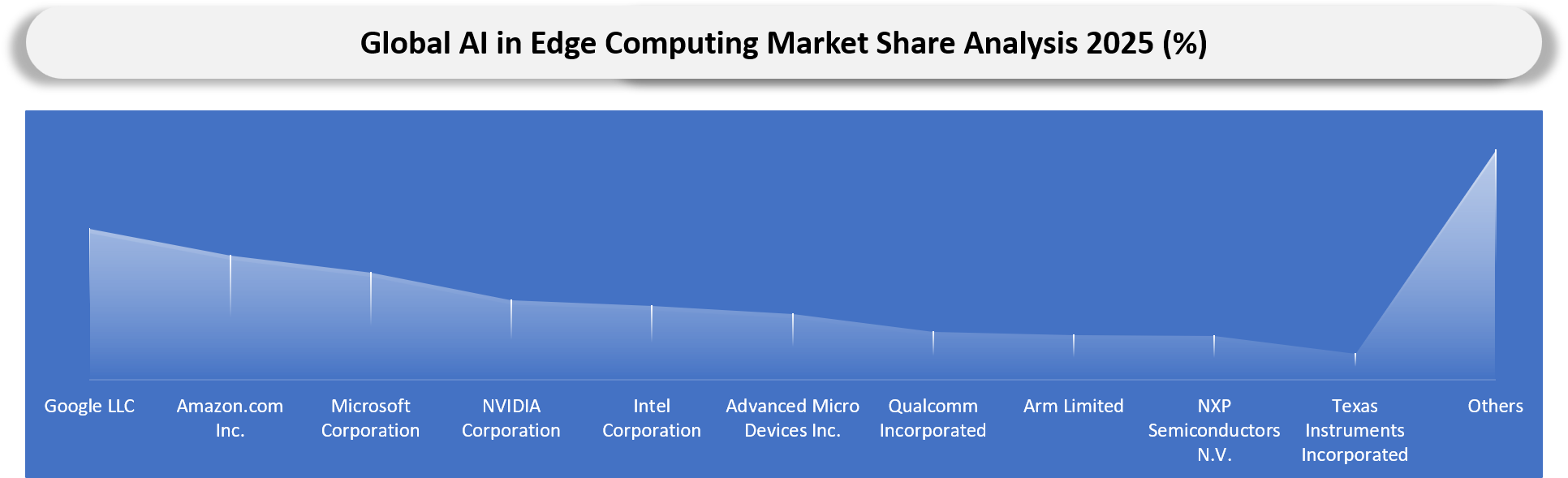

Top Companies in AI in Edge Computing Market

Competition is split across hardware accelerators, embedded modules, platform software, cloud control planes, industrial automation ecosystems and systems integration. NVIDIA, Intel, Qualcomm, AMD and Arm compete around compute performance, power efficiency and developer tooling. Google, AWS and Microsoft compete around cloud governance and distributed workload management.

Industrial vendors and hardware specialists compete on deployment realism. Siemens, Advantech, ADLINK, Supermicro, Dell and HPE matter because production systems need enclosures, thermal design, remote management, security and field service. A model that runs in a demo environment still needs a durable box, a secure update process and support across years of operation.

Competitive benchmarking should avoid a single global leaderboard. A chip vendor can lead in robotics modules while a hyperscaler leads in fleet management and an industrial automation vendor leads in factory deployment. Better ranking measures include deployment location, supported workloads, runtime control, partner depth, security posture and recurring revenue potential.

Commercial competition will increasingly be decided by the quality of control planes and partner routes. A provider that can onboard devices, enforce policy, monitor model health and coordinate field service gains a stronger account position than a supplier offering only compute capacity. Google, AWS and Microsoft will compete against industrial platforms in accounts where plant engineers want OT familiarity and IT leaders want cloud governance. The strongest proposals will blend both requirements without forcing customers into separate operating models while keeping pricing transparent, security ownership clear and deployment responsibility acceptable for both corporate IT and site operations teams.

AI in Edge Computing Market - Company Profiles & Strategy Analysis

- Key Company Evaluation - Analyze leading AI in edge computing companies based on market position, innovation, financial performance, and competitive strengths.

- Business Strategy Analysis - Evaluate growth strategies including AI investments, strategic partnerships, acquisitions, and global expansion initiatives.

- Product Portfolio Assessment - Compare AI edge hardware, software, processors, platforms, and edge AI solutions across major market players.

- Expansion & Partnership Strategy - Track collaborations, ecosystem partnerships, regional expansion, and technology alliances shaping the AI in edge computing market.

Market Disruption & Structural Shift Analysis - AI in Edge Computing Market

- Market Disruption & Structural Shift Analysis - Evaluates how AI-driven edge intelligence is reshaping enterprise computing, real-time analytics, and decentralized IT infrastructure.

- Technology Disruption Impact - Assesses the impact of generative AI, edge AI chips, 5G, IoT, and TinyML on next-generation edge computing deployments.

- Industry Structural Changes - Examines evolving cloud-edge architectures, AI hardware ecosystems, strategic partnerships, and industry adoption across manufacturing, healthcare, automotive, telecom, and smart cities.

Recent Developments - AI in Edge Computing Market

- In June 2026, Supermicro expanded its AI at the Edge portfolio with new Intel-powered platforms optimized for low-latency AI inference across manufacturing, retail, logistics, and industrial automation. The systems feature Intel Core Ultra Series processors, Intel Arc Pro GPUs, and scalable GPU configurations to accelerate enterprise edge AI deployments.

- In June 2026, indie Semiconductor introduced the iND881 Edge AI System-on-Chip (SoC), designed for automotive smart cameras, robotics, and intelligent perception systems. The new processor combines AI acceleration with advanced image signal processing to enable real-time edge inference.

- In June 2026, Kontron AG partnered with Intel to expand its industrial Edge AI portfolio using Intel Core Ultra Series 3 (Panther Lake) processors. The collaboration focuses on delivering energy-efficient AI platforms for industrial automation, smart factories, and IoT applications.

- In May 2026, Hanwha Vision and Ambarella signed a long-term strategic agreement valued at over US$800 million to accelerate Edge AI adoption across robotics, industrial automation, surveillance, and life sciences using Ambarella's edge AI platform.

- In January 2026, Datavault AI expanded its collaboration with IBM and Available Infrastructure to deploy enterprise-grade AI at the edge through the SanQtum AI platform, enabling secure, low-latency AI processing across distributed micro edge data centers in the United States.

- In January 2026, Scale Computing showcased its AI-ready edge computing solutions at NRF 2026, highlighting infrastructure designed to support AI workloads, point-of-sale systems, video analytics, and digital retail applications at distributed edge locations.

- In January 2026, Lantronix unveiled its SmartEdge.ai Gateway and SmartSwitch.ai at CES 2026, introducing an integrated Edge AI platform that combines AI inference, connectivity, and real-time video analytics for enterprise and industrial environments.

Major Pain Points

- Many proof of concept projects fail to scale because model deployment, device provisioning and monitoring were not designed for multi-site operations.

- Accelerator changes can require model retesting, driver changes, thermal redesign and customer validation.

- Industrial buyers struggle to connect AI software with existing PLCs (Programmable Logic Controllers), SCADA (Supervisory Control and Data Acquisition) systems and plant cybersecurity rules.

- Video workloads generate high bandwidth and storage costs when raw feeds are pushed to the cloud without local filtering.

- Cybersecurity teams worry about unmanaged endpoints, weak update practices and software bills of materials across distributed devices.

- Procurement teams lack consistent pricing benchmarks because hardware, runtime software and managed services are often bundled together.

- Model drift is difficult to detect when devices are deployed across stores, factories, hospitals and outdoor public sites.

- Long industrial lifecycles conflict with fast AI model and chip refresh cycles.

Analyst View And Opinion

Analyst opinion is that the market will reward suppliers that make deployment boring, repeatable and safe. The winning vendors will not only sell accelerators or model demos. They will help customers operate fleets of intelligent devices with predictable performance, security and support.

The software layer deserves special attention because it can reshape account control. Once a customer standardizes on a runtime, orchestration method or model governance process, future applications are likely to follow that path. Chip vendors without strong software ecosystems may face margin pressure from platform vendors and systems integrators.

Demand will also become more selective. Buyers will fund applications that reduce scrap, downtime, labor intensity, theft, clinical delay or safety risk. Vague AI transformation narratives will lose attention unless they connect to operational payback and measurable site-level outcomes.

Target Audience

| Industry | Who Should Buy This Report | Reason To Buy This Report |

| Cloud Hyperscale's | Edge Platform Product Teams, Cloud Infrastructure Leaders, AI Product Managers | Assess where distributed inference, local data processing and cloud-backed control planes can create recurring platform revenue. |

| Semiconductor And AI Accelerator Vendors | Product Strategy Teams, Embedded Computing Leaders, Channel Heads | Evaluate demand for GPU, NPU (Neural Processing Unit), TPU (Tensor Processing Unit), FPGA (Field Programmable Gate Array) and ASIC (Application Specific Integrated Circuit) across edge workloads. |

| Industrial Automation Companies | OT Strategy Leaders, Factory Digitization Teams, Industrial Software Managers | Identify use cases for quality inspection, predictive maintenance, worker safety and local analytics across manufacturing sites. |

| Edge Hardware Manufacturers | Embedded System Teams, Industrial PC Product Managers, Sales Leaders | Benchmark product fit across gateways, edge servers, industrial PCs, smart cameras and rugged AI systems. |

| Telecom Operators | MEC (Multi Access Edge Computing) Product Teams, Private Network Leaders, Enterprise Sales Teams | Understand where telco edge sites can support manufacturing, public safety, logistics and smart city workloads. |

| Systems Integrators And Managed Service Providers | Solution Architects, Delivery Leaders, Managed Operations Teams | Map integration opportunities around device onboarding, runtime management, cybersecurity and lifecycle support. |

| Healthcare Technology Companies | Medical Device Product Teams, Hospital IT Leaders, Digital Health Strategy Teams | Assess local inference opportunities in medical imaging, monitoring, privacy-sensitive workflows and connected devices. |

| Retail And QSR (Quick Service Restaurant) | Store Technology Leaders, Loss Prevention Teams, Digital Operations Heads | Analyze local video intelligence, shelf analytics, drive-through optimization and store operations use cases. |

| Investors And Consulting Firms | Technology Investors, Corporate Strategy Teams, Market Intelligence Leaders | Evaluate growth pockets, stack ownership, company positioning and partnership opportunities across the distributed intelligence ecosystem. |

Why Choose DataM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

What DataM Uniquely Provides

- Stack ownership mapping across chips, modules, runtime, cloud control plane and managed operations.

- Workload cost model for computer vision, video analytics, predictive maintenance, speech and robotics.

- Accelerator fit matrix covering GPU, NPU (Neural Processing Unit), TPU (Tensor Processing Unit), FPGA (Field Programmable Gate Array) and ASIC (Application Specific Integrated Circuit).

- Runtime and middleware benchmarking for update control, rollback, offline operation and monitoring.

- Design win tracker for industrial PCs, embedded boards, gateways, cloud platforms and systems integrators.

- Customer qualification view for Google, chip vendors, OEMs, OT vendors and enterprise technology providers.

Suggestions For Related Report

- Edge AI Market

- AI in Edge Computing Market

- Edge Computing Market

- AI in IoT Market

- Edge AI Chip Market

- Artificial Intelligence Chip Market

- Edge AI Processor Market

- Edge Data Center Infrastructure Market

- Edge Infrastructure Market

- Cloud To Edge Data Services Market

- Decentralized Edge Cloud Market

- Artificial Intelligence Market

- Artificial Intelligence Robots Market

- Edge Computing For Autonomous Vehicles Market

- Mobile Edge Computing Market