Edge Computing for Autonomous Vehicles Market Overview

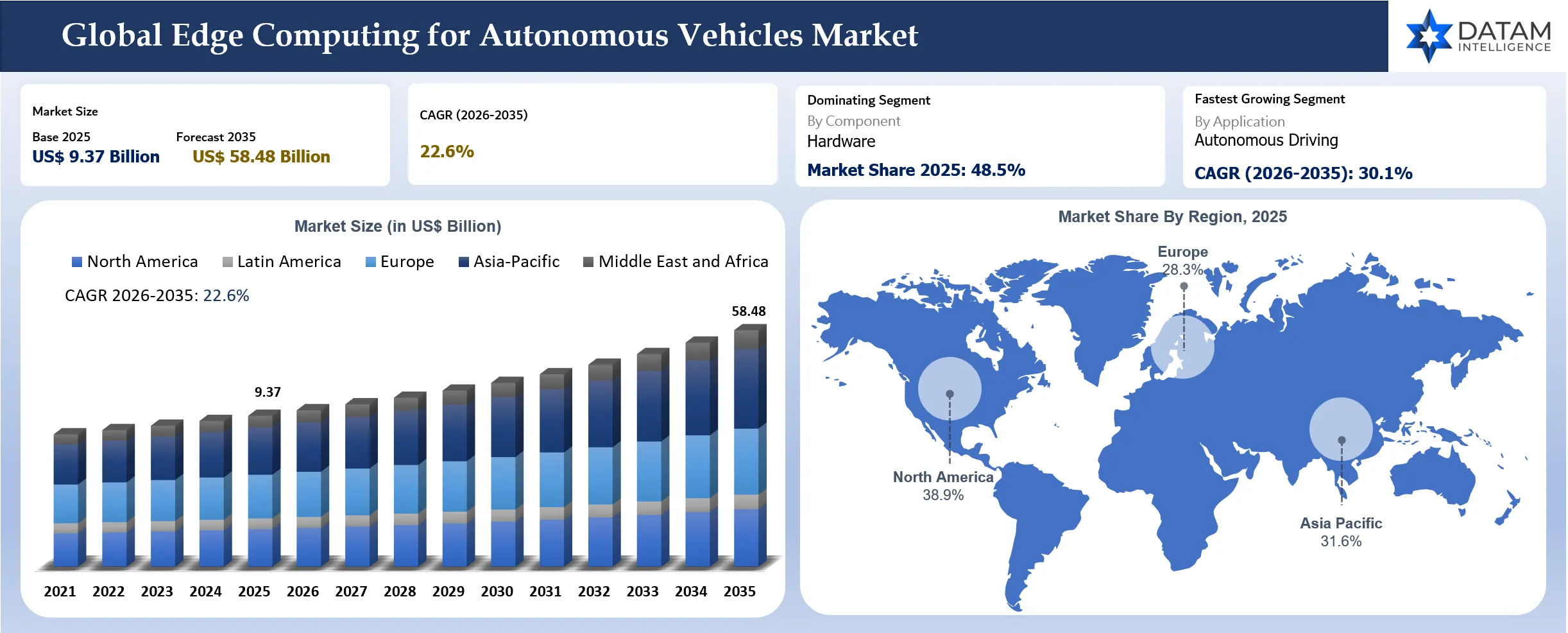

The global edge computing for autonomous vehicles market reached US$ 9.37 billion in 2025 and is expected to reach US$ 58.48 billion by 2035, growing at a CAGR of 22.6% during 2026 to 2035. Demand is being shaped by the shift from assisted driving toward software-defined, sensor-rich and AI-defined vehicle platforms. Autonomous vehicles cannot wait for every perception, planning and control decision to travel to a distant cloud. Cameras, radar, LiDAR, ultrasonic sensors, driver monitoring systems, navigation data and vehicle telemetry must be processed close to the vehicle so that braking, steering, lane changes, object detection and fallback decisions happen within safe response windows. Edge computing therefore becomes a core autonomy layer rather than a supporting IT function.

Market growth is moving across three connected layers: in-vehicle AI compute, roadside and telecom edge infrastructure and cloud-edge data pipelines for fleet learning. Passenger vehicles and robotaxis are the strongest early demand centers because they require high-performance inference, sensor fusion, safety monitoring and continuous software updates. Commercial fleets, autonomous trucks and delivery vehicles will add value as operators use edge systems for route optimization, predictive maintenance, fleet health monitoring and real-time operations. Supplier differentiation will depend on compute performance per watt, safety certification readiness, data filtering capability, cybersecurity controls, software stack maturity and ability to integrate with OEM and Tier 1 vehicle programs.

Edge Computing for Autonomous Vehicles Market Scope

| Metrics | Details | |

| Market Size In 2025 | US$ 9.37 Billion | |

| Market Size By 2035 | US$ 58.48 Billion | |

| CAGR During 2026 To 2035 | 22.6% | |

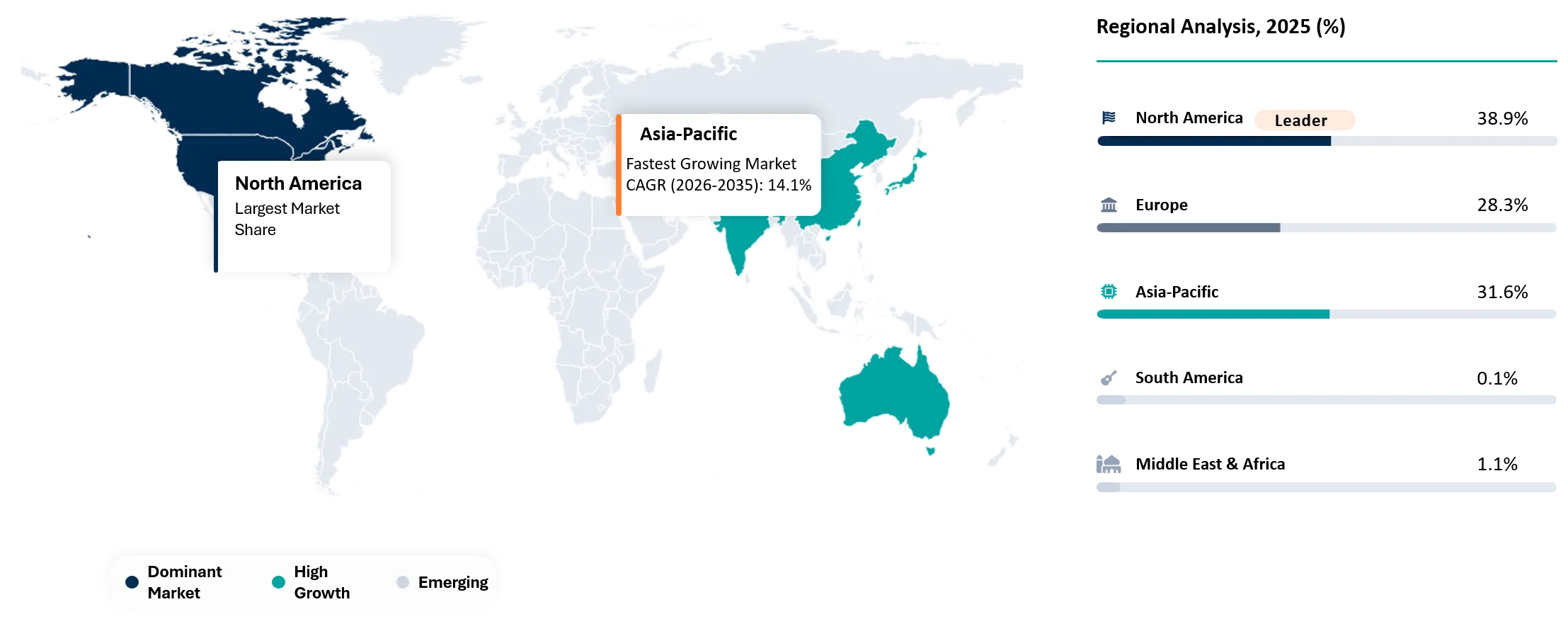

| Largest Region In 2025 | North America, 38.9% market share in 2025 | |

| Fastest Growing Region | Asia-Pacific, 26.4% CAGR between 2026 and 2035 | |

| Key Regional Shift | Asia-Pacific is expected to increase from 31.6% market share in 2025 to 41.7% market share by 2035 | |

| Leading Component | Hardware | |

| Fastest Growing Component | Software | |

| Leading Compute Location | In-Vehicle Edge | |

| Fastest Growing Compute Location | Roadside Edge | |

| Leading Application | Autonomous Driving | |

| Fastest Growing Application | HD Mapping and Localization | |

| Market Maturity | High-Growth Stage | |

| Key Buying Question | Which edge architecture can process sensor data safely, cheaply and fast enough for autonomous decision-making? | |

| By Component | Hardware, Software, Services | |

| By Compute Location | In-Vehicle Edge, Roadside Edge, Telecom Edge, Cloud-Edge Hybrid | |

| By Deployment Mode | On-Premises, Cloud-Based, Hybrid | |

| By Connectivity | 5G, 4G LTE, Wi-Fi, DSRC, C-V2X, Ethernet, Satellite-Enabled Connectivity | |

| By Vehicle | Passenger Vehicles, Commercial Vehicles, Robotaxis and Autonomous Shuttles, Autonomous Trucks, Delivery Robots and Low-Speed Autonomous Vehicles | |

| By Application | Autonomous Driving, ADAS, Predictive Maintenance, Vehicle Telematics, Traffic Management, Fleet Management, HD Mapping and Localization, Infotainment and Digital Cockpits, Driver and Occupant Monitoring, Others | |

| By End-User | Automotive OEMs, Tier 1 Suppliers, Robotaxi Operators, Fleet Operators, Cloud and Telecom Providers, Smart City and Road Infrastructure Authorities, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| South America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Key Takeaways

- North America dominated the market with 38.9% market share in 2025, supported by robotaxi pilots, AV software companies, cloud infrastructure, automotive AI chip adoption and stronger autonomy investment across the U.S.

- Asia-Pacific is expected to be the fastest-growing region with 26.4% CAGR between 2026 and 2035, driven by China’s intelligent vehicle ecosystem, Japan’s advanced ADAS programs, South Korea’s connected mobility strategy and India’s emerging automotive software base.

- Hardware remains the leading component because in-vehicle AI computers, domain controllers, central compute units, GPUs, SoCs, storage and networking modules remain essential for real-time autonomy.

- Software is expected to be the fastest-growing component as perception, sensor fusion, fleet learning, edge orchestration, data filtering, cybersecurity and over-the-air update platforms become more valuable than raw compute alone.

- In-vehicle edge remains the leading compute location because safety-critical decisions such as braking, object detection, free-space estimation and path planning must happen inside the vehicle.

- Roadside edge is expected to grow fastest as smart corridors, V2X pilots, urban traffic management and robotaxi service areas require localized infrastructure for map updates, traffic coordination and connected safety.

- Supplier differentiation is moving toward performance per watt, ASIL-ready compute platforms, integrated sensor pipelines, trusted data handling, vehicle software middleware, OTA support and fleet-scale edge management.

Why Does This Report Matter In 2026?

Edge computing for autonomous vehicles matters in 2026 because vehicle intelligence is no longer limited to basic ADAS. Vehicles are becoming rolling AI systems that must perceive, reason, plan, communicate and update continuously. A car equipped with cameras, radar, LiDAR and driver monitoring can generate enormous data volume, but only a small part of that data should be uploaded to the cloud. The vehicle must decide locally what is safety-critical, what should be stored and what should be sent for fleet learning.

The market is also being reshaped by robotaxi commercialization. Robotaxi operators need safe in-vehicle autonomy, local fleet operations, map freshness, depot data pipelines and service area management. Edge computing supports the economics of these fleets because operators cannot rely only on cloud infrastructure for real-time driving decisions or upload every sensor stream at full fidelity. Intelligent data filtering and local inference reduce bandwidth pressure and make fleet learning more manageable.

Automotive OEMs are also redesigning vehicle electronics. Older vehicles used many distributed electronic control units. New software-defined vehicles are moving toward centralized compute, zonal architectures and high-speed vehicle networks. It creates a stronger role for edge platforms that can run autonomy, cockpit, diagnostics, connectivity and safety workloads in coordinated domains. A strong RD must therefore evaluate in-vehicle compute, connectivity, software, fleet data workflows and infrastructure readiness together.

Strategic Indicators For Edge Computing For Autonomous Vehicles Market

High Regulation Impact

Regulation has strong influence because autonomous driving features operate within safety-critical environments. Vehicle platforms need to satisfy functional safety, cybersecurity, data privacy, homologation, software update and operational design domain requirements. Edge computing platforms must support reliable decision-making, protected data handling and verifiable software behavior. OEMs and Tier 1 suppliers therefore evaluate edge platforms through safety case evidence rather than only compute performance.

Driver monitoring and supervised autonomy requirements are becoming more important as L2 Plus and L3 systems scale. Regulators and safety assessment programs expect clear driver engagement logic, fallback behavior and system limitations. Edge compute is central because driver attention, object detection, sensor fusion and alert escalation must run locally with high reliability.

Data governance is another regulatory concern. Autonomous vehicles collect images, location data, sensor logs and fleet performance data. Automakers and mobility providers must decide which data stays in the vehicle, which data moves to the cloud and how personally sensitive information is protected. Edge data filtering can reduce unnecessary cloud transfer and support privacy-focused architectures.

High Investment Activity

Investment is concentrated in AI automotive SoCs, centralized vehicle compute, robotaxi platforms, software-defined vehicle middleware, V2X infrastructure, edge data pipelines and simulation-linked fleet learning. NVIDIA, Mobileye, Qualcomm and Tesla are shaping the in-vehicle compute layer, while cloud providers and telecom operators are supporting connected vehicle and edge infrastructure layers.

Robotaxi and autonomous trucking programs are driving high-value investment because fleet economics depend on autonomy performance, uptime and fast learning loops. Edge platforms help operators capture important disengagement, edge-case and maintenance data without overwhelming cloud storage and network budgets. It creates demand for intelligent logging, local analytics and automated data selection.

Investment is also moving toward integrated cockpit and ADAS platforms. OEMs want fewer hardware boxes, lower wiring complexity and easier software updates. Centralized compute can lower long-term architecture complexity, but it raises safety partitioning and thermal management requirements. Vendors that can combine compute consolidation with safety isolation will gain stronger interest.

Supply Chain Disruption

Supply-chain risk is tied to advanced automotive semiconductors, high-bandwidth memory, automotive-grade storage, sensors, Ethernet switches, thermal management components and manufacturing capacity. Edge compute units for autonomous vehicles require high reliability and long qualification cycles. Shortages or redesigns can delay vehicle programs because platforms are validated years before launch.

Geopolitical exposure is also important. Advanced AI chips, automotive processors and network modules are sensitive to export controls, regional sourcing rules and technology restrictions. OEMs increasingly evaluate regional supply continuity, second sourcing and software portability across compute platforms. Compute platform dependency has become a strategic risk.

Software supply chain is just as important. Autonomous vehicle edge systems rely on operating systems, middleware, AI models, perception software, cybersecurity libraries and OTA infrastructure. A weakness in one layer can affect vehicle safety or service availability. Suppliers with secure development processes and long-term software maintenance support will be preferred.

Pricing Volatility

Pricing volatility is driven by automotive AI compute cost, sensor count, memory, thermal design, software licensing, safety certification work and cloud-edge data handling. High-performance in-vehicle compute can materially increase vehicle bill of materials. OEMs must balance performance against cost, power draw and packaging constraints.

Robotaxi operators may accept higher compute cost because autonomous service revenue depends on safety, utilization and operating uptime. Mass-market passenger vehicles face more pressure. A compute platform that fits a premium EV may be too costly for a mid-market vehicle unless it scales across multiple trims and software feature packages.

Software pricing is becoming more important. OEMs increasingly buy platform software, perception modules, maps, simulation tools, OTA systems and fleet data services. Vendors that can monetize through software updates and recurring services may capture stronger value than hardware-only suppliers.

Procurement Pressure

Procurement teams must evaluate hardware, software, safety and lifecycle support together. A cheaper chip can become costly if it lacks software maturity, toolchain support, safety documentation or long-term availability. OEMs need suppliers that can support vehicle programs over many years and multiple geographies.

Platform lock-in is another procurement concern. Automakers want high-performance compute, but they also want flexibility to change software stacks, sensor configurations and cloud partners. Open middleware, reusable toolchains and modular architectures reduce lock-in risk. Suppliers that provide strong integration while preserving OEM control will gain trust.

Thermal and power constraints also shape buying decisions. Edge compute must fit inside vehicle packaging and operate across temperature extremes. Higher TOPS alone is not enough. Buyers compare performance per watt, cooling complexity, system redundancy and total architecture cost.

New Technology Adoption

New technology adoption is strongest in centralized vehicle compute, AI accelerators, zonal electrical architectures, C-V2X, vehicle Ethernet, edge orchestration software, synthetic data pipelines and AI-assisted fleet learning. Autonomous vehicle platforms need a compute architecture that can scale from L2 Plus to L4 readiness without full redesign.

Roadside edge and telecom edge are gaining attention in smart corridors and urban robotaxi zones. The systems can support local traffic analytics, map update distribution, hazard alerts and V2X messages. Adoption will depend on public infrastructure funding, telecom partnerships and standardization.

AI model compression and edge optimization are also important. Automakers need perception and planning models that run within strict power and latency budgets. Efficient inference, quantization, neural network accelerators and workload scheduling will shape competitiveness.

Regional Expansion Opportunity

North America remains the largest market because the U.S. has a strong base of autonomous driving developers, robotaxi operations, AI chip vendors, cloud providers and software-defined vehicle innovation. California, Arizona, Texas and Michigan are especially relevant because testing, engineering talent and automotive partnerships are concentrated there.

Asia-Pacific offers the strongest growth opportunity. China has rapid intelligent EV adoption, strong domestic ADAS suppliers and large connected vehicle data flows. Japan and South Korea support advanced automotive electronics and sensor integration. India is becoming more relevant through automotive software, cloud engineering and mobility platforms.

Europe remains a high-value market because Germany, UK, France and Sweden are strong in automotive engineering, functional safety, regulation and premium vehicle platforms. Adoption may be slower than China in some consumer autonomy features, but safety and software validation discipline will support high-value technology demand.

Government Policy Support

Government policy supports demand through autonomous vehicle testing frameworks, smart road infrastructure, 5G deployment, connected mobility programs and road safety initiatives. Public agencies are increasingly interested in V2X, traffic management and automated mobility pilots where edge infrastructure can improve response times and data handling.

Data sovereignty rules can also support localized edge computing. Vehicles operating in regulated markets may need to keep certain data within national or regional boundaries. Edge processing allows OEMs and fleet operators to reduce raw data transfer while still extracting useful insights.

Urban mobility policy will influence robotaxi and autonomous shuttle adoption. Cities that permit controlled service areas, smart intersections and autonomous transit pilots can accelerate roadside edge demand. Deployment will be strongest where regulators, operators and infrastructure owners coordinate early.

Opportunities in Edge Computing for Autonomous Vehicles Market

Edge AI Platforms For L3 and L4 Autonomous Driving Programs

L3 and L4 programs create strong opportunity because higher automation requires stronger in-vehicle inference, redundancy and safety partitioning. OEMs and robotaxi developers need compute platforms that can run perception, planning, localization, driver monitoring and fail-operational logic. Vendors that provide validated hardware and software stacks can capture long program cycles.

Roadside Edge Infrastructure For V2X and Smart Corridor Deployment

Smart intersections, highways, ports and controlled urban zones can use roadside edge nodes to process local sensor data and support V2X alerts. Roadside edge can help identify hazards that vehicles cannot see directly, such as blocked lanes, emergency vehicles or pedestrians beyond line of sight. Growth will depend on municipal budgets, telecom partnerships and standardization.

Edge Computing For Autonomous Vehicles Market Trends

Cockpit and ADAS Compute Consolidation Into Central Vehicle Platforms

Automakers are reducing fragmented vehicle electronics by consolidating cockpit, ADAS and connectivity workloads onto more powerful central platforms. The shift can reduce wiring and hardware complexity, but safety isolation becomes more important. Vendors that can support mixed-criticality workloads will gain share.

Fleet Data Filtering Moving From Cloud Upload To Vehicle-Level Intelligence

Fleet learning depends on high-quality data rather than maximum data upload. Vehicles are increasingly expected to select unusual scenes, sensor faults, disengagement events and map changes locally. Edge-based filtering will become a major software value layer as fleets scale.

Technology Landscape

The technology landscape combines in-vehicle AI compute, sensor fusion software, vehicle Ethernet, C-V2X, 5G, telecom edge nodes, cloud data platforms, OTA software, simulation and fleet learning. In-vehicle edge remains the core layer because safety-critical decisions must be made locally. Roadside and telecom edge support connected safety, fleet operations and local data services.

Centralized compute is becoming more important as vehicles shift toward software-defined architectures. Instead of many distributed processors, OEMs are moving to domain or zonal controllers with high-speed networking, which supports software reuse and OTA updates, but it also concentrates safety and cybersecurity risk into fewer systems.

Cloud-edge hybrid architectures are becoming the practical model. Vehicles process immediate decisions locally, roadside nodes process local traffic and event data and the cloud supports training, simulation and fleet-scale analytics. The strongest platforms will connect all three layers with reliable data governance.

Innovation and Research & Development Trends

Research and development are focused on efficient AI inference, sensor fusion, model compression, safety-certified compute, deterministic middleware, neural simulation, edge data selection and connected mobility infrastructure. Companies are trying to run larger models inside the vehicle without exceeding power, heat or cost limits.

Simulation-linked edge learning is gaining importance. Autonomous developers need to convert real-world edge cases into simulation scenarios, retraining workflows and validation datasets. Better data selection at the edge reduces the cost of finding useful training examples.

Safety-oriented software is also advancing. Autonomous platforms need operating systems, hypervisors, container orchestration and middleware that can separate safety-critical workloads from infotainment and cloud-connected features. Mixed-criticality compute will be a defining architecture challenge.

Sustainability and ESG Analysis

Edge computing can support sustainability by reducing unnecessary cloud data transfer. Vehicles that filter and compress data locally use networks and cloud storage more efficiently. Fleet operators can also use edge analytics to optimize routes, reduce idle time and improve maintenance timing. Autonomous EV fleets can benefit from predictive maintenance and energy-aware driving. Edge systems can monitor battery health, tire condition, sensor cleanliness and charging behavior. Better maintenance can extend component life and reduce waste.

Data center energy use remains a challenge. Autonomous development requires cloud training and simulation at scale. The most sustainable architectures will combine efficient in-vehicle inference, selective data upload and renewable-powered cloud infrastructure. ESG evaluation should therefore cover both vehicle-level compute and back-end training workloads.

Demand-Supply Gap

Demand for high-performance automotive edge compute is rising faster than the supply of validated platforms that combine compute, safety, power efficiency and software maturity. Many suppliers can provide processors, but fewer can support the full vehicle autonomy lifecycle from development to validation and fleet operations.

Automotive-grade AI talent is also limited. OEMs need engineers who understand embedded AI, vehicle networks, functional safety, cybersecurity and cloud data pipelines. The shortage increases dependence on technology partners. Roadside edge deployment faces a different gap. Cities and road operators often lack funding, standardization and operational ownership models for edge infrastructure. Growth will depend on public-private partnerships and clear use cases such as smart intersections, ports, logistics corridors and robotaxi service zones.

Risk Mitigation Framework

Risk mitigation should begin with architecture selection. OEMs should choose compute platforms based on latency, redundancy, ASIL readiness, power draw, thermal limits, cybersecurity and long-term supplier support. A platform chosen only for peak compute may create downstream integration risk.

The second step is data governance. Vehicles should process raw sensor data locally, upload only selected events and protect privacy-sensitive information. Clear rules are needed for retention, anonymization, access control and data residency. The third step is continuous validation. Autonomous systems should be monitored after launch through event logs, disengagement data, software version tracking and fleet performance analytics. Edge computing should support the feedback loop between real-world operation and model improvement.

Compliance Roadmap

The first phase is platform readiness. OEMs and suppliers should verify functional safety requirements, cybersecurity design, sensor interfaces, compute redundancy, power budget and thermal performance. Architecture decisions should be aligned with target autonomy level and operational design domain.

The second phase is integration and validation. Perception, planning, driver monitoring, localization, maps, OTA and fleet logging should be tested together. Simulation, hardware-in-loop testing and road testing should create evidence that the edge platform performs under expected conditions.

The third phase is post-deployment governance. Vehicles need continuous monitoring, secure updates, incident review, data quality control and performance benchmarking. Fleet operators should maintain a clear link between edge events, cloud training and software release decisions.

Strategic Implications

Automotive value is shifting from mechanical differentiation toward compute, software and data. Edge computing suppliers will gain influence because vehicle autonomy depends on local intelligence. OEMs that control edge architecture will have stronger flexibility in software features and fleet learning.

Semiconductor vendors will compete not only on TOPS but also on software ecosystem and safety documentation. Cloud providers will compete by helping OEMs manage fleet data and AI training. Telecom operators will compete where roadside and 5G edge infrastructure becomes commercially viable. Robotaxi growth will create new infrastructure demand. Cities and operators will need edge-supported maps, remote assistance, local analytics and incident response systems. The strongest suppliers will serve both vehicle programs and fleet operations.

Edge Computing For Autonomous Vehicles Maket Emerging Opportunities

Autonomous Fleet Edge Operations

Robotaxi, autonomous shuttle and autonomous trucking operators need edge systems that support depot diagnostics, local map updates, fleet health monitoring and service area control, which creates demand beyond the vehicle bill of materials. Fleet edge operations can become a recurring service category for technology providers.

Privacy-Preserving Vehicle Data Pipelines

Automakers and fleet operators need to learn from road data without uploading unnecessary personal or location-sensitive information. Edge filtering, anonymization and event selection can reduce privacy risk while preserving model training value, which creates opportunity for software vendors focused on trusted vehicle data pipelines.

Smart Roadside Edge For Complex Urban Zones

Intersections, school zones, tunnels, ports and logistics corridors are attractive locations for roadside edge. These environments have complex traffic patterns and safety challenges. Local edge nodes can process infrastructure sensor data and support V2X alerts, traffic optimization and AV service area operations.

Adoption Trends

Adoption is moving from pilot programs toward production vehicle platforms. Premium EVs, robotaxis and high-end ADAS packages are early adopters because they can absorb compute cost. Mass-market adoption will depend on compute cost reduction and software reuse across vehicle lines.

OEMs are adopting hybrid edge architectures. Safety-critical autonomy runs in the vehicle; fleet learning runs in the cloud and selected infrastructure use cases run at the roadside or telecom edge. The balanced model is more realistic than full cloud dependence. Edge software adoption is accelerating because hardware alone is not enough. Automakers need orchestration, data filtering, OTA, cybersecurity, simulation links and developer tools. Software maturity increasingly determines design-win quality.

AI Impact Analysis

AI is the core force behind the market because autonomous vehicles depend on perception, prediction, planning, localization, driver monitoring and fleet learning. Edge AI allows vehicles to identify objects, estimate free space, track pedestrians, interpret traffic signals and respond to sudden hazards without cloud dependency.

Generative AI and world models are also becoming relevant in development workflows. AV developers can use simulation, synthetic data and scenario generation to test edge cases more efficiently. In-vehicle models will remain more constrained than cloud models because power and latency requirements are strict. AI also improves data selection. Instead of uploading every mile of driving data, vehicles can identify unusual events, rare objects, sensor failures and human interventions, which makes fleet learning more efficient and reduces storage cost.

Disruption Analysis

Centralized vehicle compute is disrupting the traditional electronic control unit model. OEMs are redesigning electrical architectures around high-performance compute and zonal networks. The shift changes supplier power because semiconductor and software vendors become more central to vehicle differentiation.

Robotaxis are disrupting edge requirements because fleets need more than vehicle autonomy. They need local operations, map freshness, remote assistance and service area optimization. The edge stack must support commercial uptime, not only driving intelligence. Data economics are disrupting cloud-first assumptions. Autonomous vehicles generate too much data for unrestricted upload. Edge filtering becomes a business requirement because it lowers bandwidth, storage and annotation costs. Suppliers that can reduce data burden will gain stronger commercial relevance.

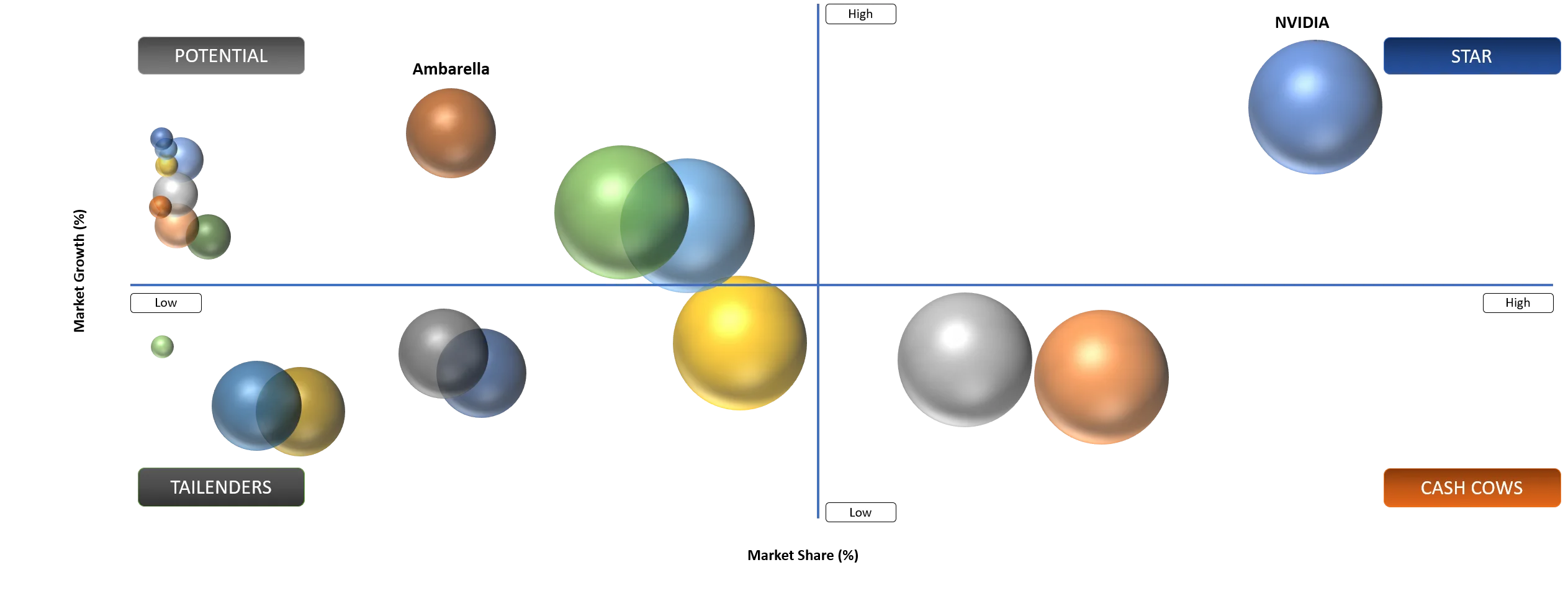

BCG Matrix: Company Evaluation

Star

Star players include NVIDIA Corporation, Mobileye Global Inc., Qualcomm Incorporated, Tesla, Inc., Alphabet Inc., Amazon Web Services, Inc. and Microsoft Corporation. The companies have strong positions across in-vehicle AI compute, autonomous driving software, robotaxi operations, cloud-edge infrastructure and fleet learning. NVIDIA and Mobileye are especially strong in autonomy compute and software ecosystems, while AWS and Microsoft support cloud-edge data pipelines for connected mobility.

Potential

Potential companies include Ambarella, Inc., BlackBerry Limited and Wind River Systems, Inc. Ambarella can gain share through edge AI SoCs and vision processing where power efficiency matters. BlackBerry can expand through QNX, safety software and cybersecurity capabilities used in software-defined vehicles. Wind River can benefit from edge operating systems and mission-critical software platforms for connected and autonomous vehicle programs.

Edge Computing For Autonomous Vehicles Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact | Demand Concentration | Impacted Application | Strategic Impact |

Autonomous Driving Stacks Need Low-Latency In-Vehicle AI Compute | High | North America, China, Europe and Japan | Autonomous Driving | Drives high-performance in-vehicle edge platforms |

Software-Defined Vehicles Are Moving Toward Centralized Edge Architectures | High | Global OEMs | ADAS and Digital Cockpits | Supports central compute and zonal architecture adoption |

Robotaxi and Fleet Operators Need Faster Local Decision-Making | Medium To High | U.S., China, UAE and Europe | Fleet Management and Robotaxis | Expands edge operations and local data pipelines |

Autonomous Driving Stacks Need Low-Latency In-Vehicle AI Compute

Autonomous driving creates one of the clearest technical cases for edge computing. Vehicle perception and control cannot depend on remote cloud latency. The system must process sensor data locally, classify objects, estimate vehicle path and trigger safe responses in real time. It makes in-vehicle edge compute a foundational layer for ADAS, L3 autonomy and L4 robotaxi systems.

Sensor richness is increasing. Cameras, radar, LiDAR, ultrasonic sensors, inertial systems and driver monitoring cameras create large data flows. Edge compute reduces the need to transfer raw data outside the vehicle and allows immediate fusion of sensor streams. A stronger edge architecture improves responsiveness and bandwidth efficiency at the same time.

The commercial effect is visible in vehicle program design. OEMs are selecting higher-performance central compute and domain controllers to support future software features. Suppliers that provide AI inference, safety software and developer ecosystems will capture stronger value than hardware vendors alone.

Restraint Impact Analysis

| Restraint | Drag On Market Growth | Primary Impact Area | Impacted Application | Strategic Impact |

High Compute Cost and Thermal Load Slow Mass-Market Deployment | High | Vehicle Bill Of Materials | Passenger Vehicles | Limits adoption in low-cost trims |

Safety Validation and Cybersecurity Requirements Extend Platform Qualification | High | OEM Vehicle Programs | Autonomous Driving and ADAS | Lengthens design-win cycle |

Infrastructure Fragmentation Slows Roadside Edge Adoption | Medium | Smart Corridors and Cities | V2X and Traffic Management | Delays network-side monetization |

High Compute Cost and Thermal Load Slow Mass-Market Deployment

Advanced autonomous computing platforms are expensive and power-intensive. High-end processors, memory, sensors, storage and cooling systems add cost to the vehicle. Premium EVs and robotaxis can justify this investment more easily, but mass-market passenger vehicles need lower-cost configurations.

Thermal load is a practical issue. Vehicle compute must operate reliably in hot cabins, sealed modules and harsh driving conditions. More compute performance can require stronger cooling, larger enclosures and higher energy use. EV range and packaging constraints make this a serious design consideration. Safety and cybersecurity validation also slow adoption. OEMs cannot install a new platform without extensive testing across software, sensors, fallback behavior and OTA update paths., which creates long sales cycles and makes automotive design wins difficult for new entrants.

Edge Computing For Autonomous Vehicles Market Segmentation Analysis

Hardware Will Continue To Dominate The Current Revenue Base

Hardware will continue to dominate because autonomous edge computing requires physical processors, GPUs, AI accelerators, central compute units, storage, memory and networking modules inside the vehicle. In-vehicle hardware remains the first layer of market spending because autonomy cannot operate without reliable local compute.

NVIDIA, Mobileye, Qualcomm, Tesla, Renesas, NXP and Ambarella are important because they supply or influence compute architectures used in ADAS and autonomous programs. The suppliers compete on compute performance, power efficiency, safety support, sensor compatibility and software ecosystem.

Hardware dominance does not mean hardware is the only source of value. Buyers increasingly evaluate hardware as part of a platform that includes operating systems, middleware, perception software, simulation tools and OTA workflows. The strongest hardware suppliers will be those that reduce software integration risk.

Software Will Grow Fastest As Vehicle Intelligence Moves To The Edge

Software is expected to grow fastest because perception, localization, planning, driver monitoring, OTA, cybersecurity and data filtering define how edge hardware creates value. OEMs need software that can manage sensor streams, run AI models and support continuous improvement after vehicle launch.

Edge data software is becoming especially important. Vehicles need to select useful data for cloud training, not upload every mile. Software that identifies rare scenarios, disengagements, map changes and sensor faults can reduce data costs and speed model improvement. Cybersecurity software is also critical. Edge systems connect to vehicle networks, cloud systems and OTA platforms. Secure update pipelines, intrusion detection, encryption and identity controls are mandatory for future autonomous fleets.

In-Vehicle Edge Will Remain The Leading Compute Location

In-vehicle edge will remain the leading compute location because safety-critical autonomy happens inside the vehicle. Braking, steering, object classification and path planning must operate even when connectivity is weak or unavailable. Cloud and telecom edge can support learning and fleet services, but they cannot replace vehicle-local decision-making.

Vehicle-local compute also supports privacy and data efficiency. Sensitive raw sensor data can be processed locally and converted into selected events or metadata before cloud upload and reduces data movement & supports stronger governance. Autonomous trucks, robotaxis and premium passenger vehicles will remain the strongest adopters. The platforms have higher safety and performance requirements and can justify stronger compute. Over time, lower-cost ADAS vehicles will adopt more efficient edge processors.

Roadside Edge Will Gain Share In Smart Corridors and Robotaxi Zones

Roadside edge is expected to grow faster from a smaller base because smart roads, intersections and urban robotaxi zones need localized infrastructure. Roadside systems can process camera, radar, LiDAR and signal data near the road. The systems can alert vehicles to hazards beyond line of sight and support traffic coordination.

Robotaxi operators may benefit from roadside edge in dense service areas. Local edge nodes can support map changes, construction detection, traffic events and remote operations. Cities may also use edge infrastructure for safety analytics and congestion management. Deployment will be uneven. High-value corridors such as ports, airports, logistics hubs and dense urban zones are more likely to adopt roadside edge before broad highway networks. Suppliers should target locations where the safety and operational payoff is measurable.

Edge Computing For Autonomous Vehicles Market Segmentation

- By Component

- Hardware

- Software

- Services

- By Compute Location

- In-Vehicle Edge

- Roadside Edge

- Telecom Edge

- Cloud-Edge Hybrid

- By Deployment Mode

- On-Premises

- Cloud-Based

- Hybrid

- By Connectivity

- 5G

- 4G LTE

- Wi-Fi

- DSRC

- C-V2X

- Ethernet

- Satellite-Enabled Connectivity

- By Vehicle

- Passenger Vehicles

- Commercial Vehicles

- Robotaxis and Autonomous Shuttles

- Autonomous Trucks

- Delivery Robots and Low-Speed Autonomous Vehicles

- By Application

- Autonomous Driving

- ADAS

- Predictive Maintenance

- Vehicle Telematics

- Traffic Management

- Fleet Management

- HD Mapping and Localization

- Infotainment and Digital Cockpits

- Driver and Occupant Monitoring

- Others

- By End-User

- Automotive OEMs

- Tier 1 Suppliers

- Robotaxi Operators

- Fleet Operators

- Cloud and Telecom Providers

- Smart City and Road Infrastructure Authorities

- Others

Edge Computing For Autonomous Vehicles Market Geographical Penetration

North America Edge Computing For Autonomous Vehicles Market Landscape

North America dominated the global market with 38.9% market share in 2025. The region benefits from autonomous driving developers, robotaxi operations, AI chip vendors, cloud providers and strong venture investment. The U.S. remains the center of demand because technology companies and automakers are testing and deploying advanced autonomy systems across selected cities and corridors.

The U.S. market is shaped by robotaxi operations, software-defined vehicle programs and cloud-edge infrastructure. Companies across California, Arizona, Texas and Michigan are developing autonomous software, vehicle platforms, simulation tools and fleet data pipelines. Buyers value safety evidence, real-world data and the ability to scale from pilots to production.

Canada supports demand through AI research, automotive technology and smart mobility programs. Mexico contributes through vehicle manufacturing and Tier 1 supply chains, where edge-enabled electronic architectures will become more relevant as autonomous and connected vehicle features move into mass production.

North America will remain a high-value market because OEMs and technology firms are willing to invest in compute-heavy platforms. Growth will depend on regulatory confidence, robotaxi expansion, compute cost reduction and public acceptance of autonomous mobility.

U.S. Edge Computing For Autonomous Vehicles Market Demand Analysis

The U.S. is the most important country market because autonomous driving development, robotaxi commercialization and cloud-edge infrastructure are concentrated there. Leading companies are using the U.S. as a testing and deployment base for robotaxi services, driver assistance systems and high-performance automotive AI compute.

Demand is strongest in robotaxi operations, premium EV platforms, autonomous trucking pilots and fleet analytics. Vehicles need local compute for perception and planning, while operators need cloud-edge pipelines for fleet learning and maintenance, which creates demand across hardware, software and services. U.S. buyers are also focused on safety and liability. A compute platform must support traceability, secure updates, incident investigation and regulatory evidence, which favors suppliers that provide mature software ecosystems and safety documentation.

Europe Edge Computing For Autonomous Vehicles Market Regulatory Outlook

Europe is a high-value market because automotive engineering, safety validation and regulatory discipline are strong. Germany, UK, France, Sweden and Italy are important for ADAS development, premium vehicle platforms and software-defined vehicle programs. Edge computing demand is shaped by functional safety, cybersecurity and data privacy requirements.

Germany remains the strongest European market because premium OEMs, Tier 1 suppliers and semiconductor partners are deeply involved in ADAS and autonomous vehicle programs. Buyers prioritize safety, long-term platform support and integration with existing vehicle architectures.

UK and France support autonomous mobility pilots, simulation, AI research and connected infrastructure programs. Europe’s stricter privacy and safety expectations create stronger demand for edge data filtering and secure vehicle software. Europe may grow slower than Asia-Pacific in volume, but value per vehicle can remain high. Premium vehicle platforms and advanced ADAS features will continue to support compute investment.

Asia-Pacific Edge Computing For Autonomous Vehicles Market Growth Outlook

Asia-Pacific is expected to be the fastest-growing region with 26.4% CAGR between 2026 and 2035. China, Japan, South Korea and India are driving demand through intelligent EVs, ADAS adoption, smart mobility programs, connected infrastructure and automotive software development.

China is the strongest volume engine. Domestic EV brands, autonomous driving software companies and technology platforms are deploying high-performance compute across intelligent vehicles. Fast model refresh cycles and consumer demand for smart driving features create strong edge compute adoption.

Japan and South Korea support high-value electronics and vehicle technology development. Japanese suppliers and automakers emphasize safety and reliability, while South Korea combines automotive, semiconductor and telecom capabilities. India is an emerging opportunity. Automotive software talent, mobility platforms and connected vehicle services are expanding. Near-term demand will focus more on ADAS, telematics and fleet analytics than fully autonomous driving, but the long-term potential is strong.

India Edge Computing For Autonomous Vehicles Market Expansion Outlook

India’s edge computing opportunity is developing through connected vehicle platforms, fleet analytics, ADAS adoption, automotive software engineering and mobility services. Full autonomous driving deployment is still at an early stage, but edge-based telematics, predictive maintenance and driver monitoring are gaining practical relevance.

Commercial fleets are an attractive entry point. Logistics, ride-hailing, buses and delivery fleets need route optimization, fleet health monitoring and safety analytics. Edge processing can reduce data transfer while improving real-time vehicle visibility. India also has a strong engineering base. Global OEMs and technology firms use India for automotive software, validation and cloud development, which creates an ecosystem that can support future edge platform integration. Growth will depend on road infrastructure, regulation and local cost sensitivity.

Japan Edge Computing For Autonomous Vehicles Market Technology Adoption

Japan is a premium technology market where reliability, safety and long-term supplier trust shape adoption. Automakers and Tier 1 suppliers are careful with autonomous system deployment because brand reputation and safety expectations are high. Edge computing platforms must provide strong documentation and stable operation.

ADAS and driver assistance features are the most practical near-term growth areas. Higher autonomy will depend on operational design domain clarity, map support and regulatory approval. Edge compute will support perception, driver monitoring and connected safety features. Japan also has opportunities in autonomous shuttles, logistics, aging-population mobility and smart city pilots. The applications can use edge computing in controlled routes before broader public road autonomy scales. Suppliers with proven safety and local partnerships will be best positioned.

Edge Computing For Autonomous Vehicles Market Competitive Landscape

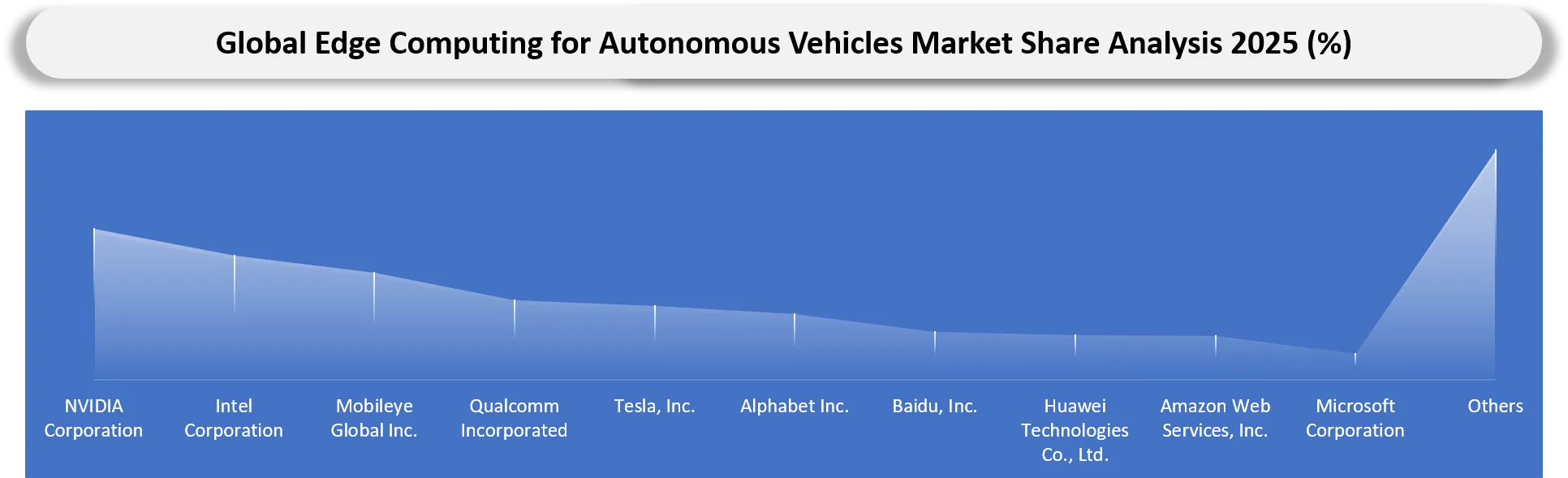

- Competition is split between semiconductor vendors, autonomy software companies, cloud providers, telecom edge players, robotaxi operators, Tier 1 suppliers and vehicle OEMs. NVIDIA, Mobileye, Qualcomm, Tesla, Alphabet, Baidu, Huawei, AWS and Microsoft represent different layers of the market.

- Semiconductor vendors compete on AI performance, power efficiency, safety readiness, sensor interface support and software ecosystem. NVIDIA competes through DRIVE Hyperion, DRIVE AGX, simulation and AI training infrastructure. Mobileye competes through EyeQ, REM, RSS and modular autonomy products. Qualcomm competes through Snapdragon Ride and digital chassis positioning.

- Cloud providers compete by supporting connected vehicle data pipelines, AI model training, simulation and fleet analytics. AWS and Microsoft are relevant where OEMs need scalable back-end platforms and edge deployment options. Cloud providers do not replace in-vehicle compute, but they influence fleet learning economics.

- Robotaxi operators compete through service area expansion, safety performance, fleet utilization, remote operations and data scale. Edge computing becomes a competitive asset because it supports safe driving, data selection and fleet uptime.

- Tier 1 suppliers compete through integration capability. Bosch, Continental, Aptiv, Valeo and ZF can bundle sensors, domain controllers, software and vehicle integration. Their advantage lies in OEM relationships and production engineering.

- Competitive benchmarking should track compute performance per watt, safety documentation, software stack maturity, sensor compatibility, OTA support, data filtering, cybersecurity, vehicle design wins, robotaxi deployments and ecosystem partnerships.

Edge Computing For Autonomous Vehicles Market Key Companies

- NVIDIA Corporation

- Intel Corporation

- Mobileye Global Inc.

- Qualcomm Incorporated

- Tesla, Inc.

- Alphabet Inc.

- Baidu, Inc.

- Huawei Technologies Co., Ltd.

- Amazon Web Services, Inc.

- Microsoft Corporation

- Robert Bosch GmbH

- Continental AG

- Aptiv PLC

- Valeo SE

- ZF Friedrichshafen AG

- Renesas Electronics Corporation

- NXP Semiconductors N.V.

- Ambarella, Inc.

- BlackBerry Limited

- Wind River Systems, Inc.

Major Pain Points

- High-performance automotive compute raises bill of materials and thermal management cost.

- Raw sensor data volume is too large for unrestricted cloud upload.

- OEMs face long validation cycles for safety-critical compute platforms.

- Software-defined vehicle architectures increase cybersecurity exposure.

- Roadside edge deployment lacks common ownership and funding models.

- Robotaxi operators need local map freshness and service-area intelligence.

- Compute platforms can become locked to specific software ecosystems.

- Mixed-criticality workloads require strong isolation between cockpit and autonomy.

- Sensor fusion performance can degrade when sensors are dirty, blocked or miscalibrated.

- Mass-market vehicles need lower-cost edge platforms that still support future software features.

Recent Developments

- May 2026: NVIDIA announced that DRIVE Hyperion was expanding as a robotaxi-ready platform with partners including Foxconn, VinFast, Uber, Autobrains and HUMAIN, supporting L4-ready autonomous fleet development across Asia, Europe and the Middle East.

- May 2026: NVIDIA launched Alpamayo 2 Super as an open reasoning model for robotaxi-ready autonomous vehicles, strengthening its AV software and simulation ecosystem for L4 development.

- May 2026: NVIDIA announced that BYD, Geely, Isuzu and Nissan adopted DRIVE Hyperion for Level 4 vehicle development, reinforcing the shift toward common autonomous driving reference platforms.

- May 2026: Mobileye’s official product material continued positioning SuperVision around 11-camera surround perception, REM-based AV maps, RSS driving policy and EyeQ 5 or EyeQ 6 High SoCs, supporting modular progression from supervised ADAS toward consumer autonomy.

- April 2026: AECC continued publishing work around automotive edge computing requirements and reference architecture, highlighting the industry need to solve large-scale connected vehicle data and network architecture challenges.

- April 2026: AWS stated that AWS IoT FleetWise would no longer be open to new customers after April 30, 2026, signaling a shift in connected vehicle data collection approaches while cloud providers continue supporting connected mobility architectures through alternative guidance and infrastructure.

Edge Computing for Autonomous Vehicles Market Investment & Funding Analysis

Global investments in edge AI and autonomous vehicle technologies continue to accelerate as automakers, semiconductor companies, cloud providers, and mobility innovators invest in real-time computing capabilities for next-generation autonomous transportation.

Major funding areas include:

- Edge AI processors and automotive chipsets

- Autonomous driving software platforms

- Vehicle-to-Everything (V2X) communication

- High-performance edge computing hardware

- Automotive cybersecurity solutions

- Intelligent transportation and smart road infrastructure

Strategic Recommendations

For Automotive OEMs

- Accelerate deployment of edge AI computing platforms

- Strengthen partnerships with semiconductor and software providers

- Expand autonomous vehicle testing and commercialization programs

For Investors

- Invest in scalable automotive edge computing platforms

- Monitor advancements in AI chips and V2X technologies

- Evaluate long-term opportunities in connected and autonomous mobility

For Governments

- Develop standards for connected and autonomous vehicle infrastructure

- Invest in smart transportation and edge-enabled road networks

- Support cybersecurity and AI safety regulations for autonomous mobility

Why Buy This Edge Computing for Autonomous Vehicles Market Report?

This report helps organizations:

- Understand emerging edge computing trends in autonomous vehicles

- Identify high-growth investment opportunities

- Benchmark leading technology providers

- Analyze regulatory and infrastructure developments

- Optimize market entry and expansion strategies

- Evaluate AI and edge computing innovations

- Assess regional market opportunities

- Track advancements in connected vehicle ecosystems

What's Included in the Edge Computing for Autonomous Vehicles Market Report?

The report provides:

- Market size and forecast analysis

- Regional market outlook

- Competitive intelligence

- Technology benchmarking

- Pricing analysis

- Regulatory landscape assessment

- Supply chain analysis

- Market share analysis

- Investment and funding landscape

- Strategic recommendations

- Emerging technology trends

- Company profiling

Who Should Buy This Report?

This Edge Computing for Autonomous Vehicles Market report is ideal for:

- Automotive OEMs

- Autonomous vehicle technology companies

- Semiconductor manufacturers

- Edge computing solution providers

- AI software developers

- Cloud service providers

- Venture capital and private equity firms

- Smart mobility companies

- Government transportation agencies

- Smart city planners

- Market intelligence teams

Key Benefits for Stakeholders

Gain actionable market intelligence to:

- Understand the future of edge-enabled autonomous mobility

- Analyze global deployment and commercialization strategies

- Evaluate advancements in automotive AI and edge computing

- Identify strategic growth and investment opportunities

- Benchmark competitors across the autonomous vehicle ecosystem

- Improve business planning and investment decision-making

Analyst View and Opinion

- Edge computing will remain a core requirement for autonomous vehicles because real-time perception and planning cannot depend on cloud latency.

- In-vehicle edge will dominate spending because safety-critical decisions must be made inside the vehicle.

- Software will grow faster than hardware as OEMs places more value on perception, orchestration, data filtering and OTA governance.

- Robotaxi fleets will create the strongest proof points for high-performance edge architectures because uptime and service-area operations are directly monetized.

- Passenger vehicles will drive volume, but premium EVs will absorb advanced compute earlier than entry-level vehicles.

- Roadside edge will remain targeted rather than universal, with early deployment focused on smart intersections, ports, airports and robotaxi operating zones.

- Cloud providers will remain important, but their role will center on fleet learning, simulation and data management rather than real-time driving control.

- Data cost will become one of the strongest commercial drivers for edge filtering and event-based logging.

- Safety certification, cybersecurity and update governance will shape vendor selection as much as compute performance.

- Asia-Pacific will be the strongest growth engine due to China’s intelligent vehicle adoption and broader regional electronics strength.

Why Edge Computing for Autonomous Vehicles Market Matters in 2026

The global automotive industry is rapidly shifting toward intelligent, software-defined mobility.

Edge computing is becoming a critical technology for autonomous vehicles by enabling real-time data processing, minimizing latency, enhancing vehicle safety, and reducing dependence on cloud connectivity. As autonomous driving systems become more advanced, edge intelligence is essential for making split-second driving decisions.

Several macroeconomic and technological factors are driving market growth:

- Increasing demand for ultra-low-latency computing

- Expansion of 5G and Vehicle-to-Everything (V2X) communication networks

- Growth in smart city and intelligent transportation infrastructure

- Increasing deployment of advanced driver assistance systems (ADAS)

- Growing investments in automotive semiconductor and edge AI technologies

- Government support for autonomous mobility and connected vehicle ecosystems

- Increasing collaboration between automotive OEMs, cloud providers, and semiconductor companies

The United States continues to lead innovation in autonomous driving software, AI platforms, and automotive edge computing technologies. China is rapidly expanding connected vehicle deployments through strong government support and smart mobility initiatives. Japan and South Korea are investing heavily in intelligent transportation systems, automotive electronics, and next-generation semiconductor technologies. Europe is accelerating adoption through stringent vehicle safety regulations and connected mobility programs, while India is emerging as a promising market driven by digital infrastructure expansion, 5G rollout, increasing EV adoption, and government initiatives supporting smart mobility.

Target Audience

| Industry | Who Should Buy This Report? | Reason To Buy This Report |

| Automotive OEMs | ADAS Leaders, Software-Defined Vehicle Teams, Product Strategy Teams | Evaluate edge compute architectures, platform partners and vehicle program strategy |

| Tier 1 Suppliers | Domain Controller Teams, Sensor Fusion Teams, Business Development Leaders | Track demand for compute integration, sensors, software and safety-ready platforms |

| Semiconductor Companies | Automotive Product Teams, Strategy Leaders | Understand demand for automotive AI SoCs, GPUs, NPUs and edge processors |

| Robotaxi Operators | Fleet Operations Teams, Autonomy Leaders | Assess edge infrastructure, vehicle compute and data pipeline requirements |

| Cloud Providers | Automotive Cloud Teams, Edge Computing Leaders | Identify cloud-edge opportunities for fleet learning and connected vehicle data |

| Telecom Providers | 5G Edge Teams, Enterprise Mobility Teams | Evaluate roadside and telecom edge opportunities for V2X and smart corridor use cases |

| Smart City Authorities | Transport Innovation Teams, Infrastructure Planners | Understand roadside edge needs for autonomous mobility and traffic coordination |

| Investors | Automotive Technology Investors, Semiconductor Funds | Identify high-growth categories across vehicle compute, software and infrastructure |

| Consulting Firms | Mobility, Technology and Automotive Advisory Teams | Support market entry, partnership, sourcing and platform benchmarking |

What DataM Uniquely Provides

- DataM maps edge computing for autonomous vehicles by component, compute location, deployment mode, connectivity, vehicle, application, end-user and region.

- DataM separates in-vehicle edge from roadside edge, telecom edge and cloud-edge hybrid architectures to avoid mixing safety-critical compute with infrastructure services.

- DataM evaluates demand across passenger vehicles, robotaxis, autonomous trucks, delivery robots and commercial fleets.

- DataM benchmarks suppliers across AI compute, autonomy software, cloud-edge data platforms, vehicle middleware and fleet operations.

- DataM connects edge computing demand with ADAS, L3 autonomy, L4 robotaxi development, HD mapping, driver monitoring and predictive maintenance.

- DataM tracks buyer pain points around compute cost, thermal design, data transfer cost, cybersecurity, validation and vendor lock-in.

- DataM provides procurement guidance covering performance per watt, safety documentation, OTA readiness, software maturity and long-term platform support.

- DataM includes import-export indicators for automotive compute hardware, processors, networking equipment, vehicle electronics and autonomous vehicle-related components.

Related Reports

The edge computing for autonomous vehicles ecosystem is evolving rapidly as automakers, technology providers, and mobility companies invest in artificial intelligence, real-time data processing, connected vehicle infrastructure, and advanced autonomous driving systems. Understanding adjacent markets provides valuable insights into the technologies enabling next-generation autonomous transportation. Explore the following related reports for a deeper understanding of the trends shaping the future of connected and self-driving vehicles.

Autonomous Vehicle Market

Autonomous vehicles are transforming the future of mobility through advanced sensing technologies, AI-driven decision-making, and real-time vehicle intelligence. As the industry moves toward higher levels of autonomy, edge computing plays a crucial role in enabling low-latency processing and safer driving operations.

Edge Computing Market

Edge computing is becoming a foundational technology across industries by bringing computing power closer to data sources. In autonomous vehicles, edge computing enables real-time analytics, reduces latency, and supports mission-critical applications that require instant decision-making.

AI in Edge Computing Market

The convergence of artificial intelligence and edge computing is unlocking new capabilities in autonomous driving. AI-powered edge systems enable vehicles to process sensor data, recognize objects, predict road conditions, and make split-second decisions without relying on cloud connectivity.

Automotive Artificial Intelligence Market

Artificial intelligence is at the heart of autonomous vehicle innovation, powering perception systems, driver assistance technologies, predictive analytics, and vehicle decision-making. Growing investments in automotive AI are accelerating the development of safer and more intelligent transportation systems.

Automotive V2X Market

Vehicle-to-Everything (V2X) communication enables autonomous vehicles to exchange real-time information with surrounding vehicles, infrastructure, and road users. Combined with edge computing, V2X enhances situational awareness, traffic management, and overall road safety.

Software Defined Vehicle Market

Software-defined vehicles are reshaping the automotive industry by enabling continuous software updates, advanced digital services, and centralized computing architectures. Edge computing supports these vehicles by providing the processing capabilities required for autonomous functions and connected mobility services.

Edge AI Chips Market

Edge AI chips are powering the next generation of autonomous vehicles by enabling high-performance processing directly within the vehicle. These chips support sensor fusion, computer vision, machine learning inference, and real-time decision-making essential for autonomous driving applications.