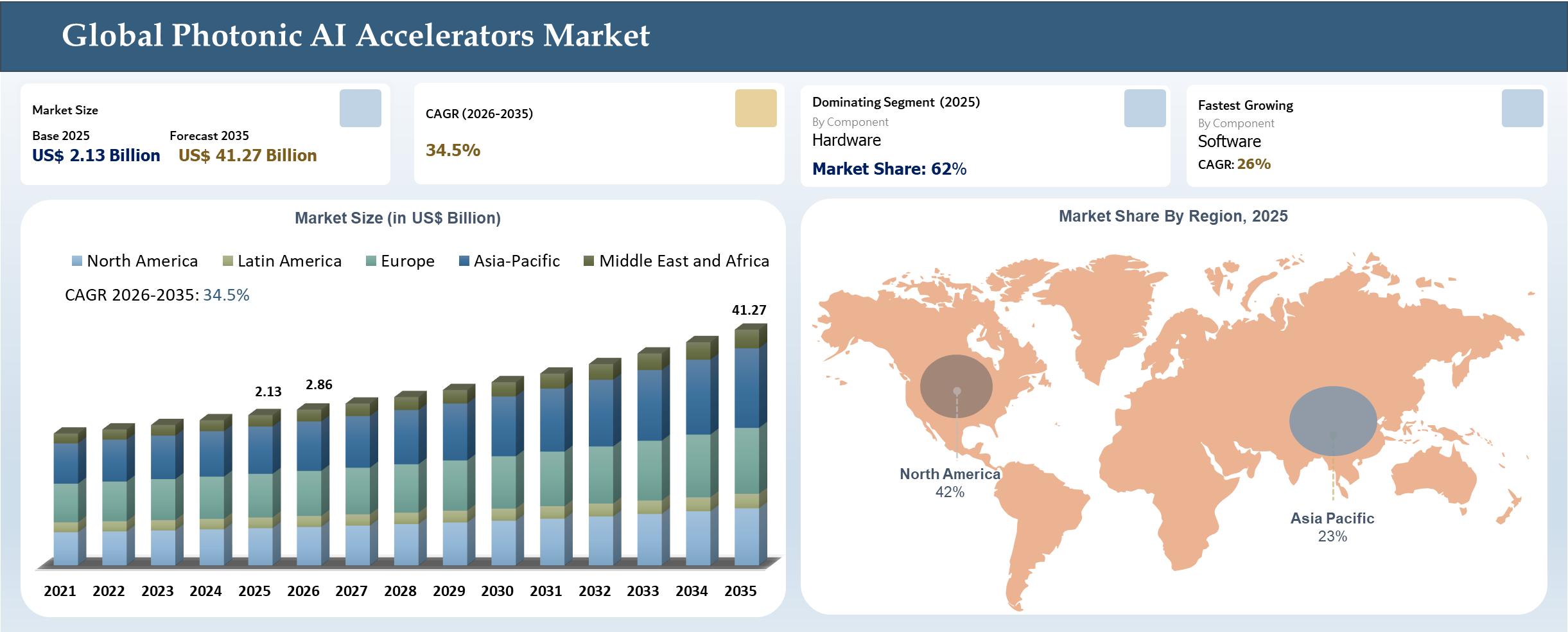

Photonic AI Accelerators Market Size

The Global Photonic AI Accelerators Market reached US$ 2.13 billion in 2025 and is expected to reach US$ 41.27 billion by 2035, growing at a CAGR of 34.5% during the forecast period 2026-2035.

The global photonic AI accelerators market is expanding due to rising demand for high-performance AI workloads, including large-scale training, real-time inference, and GPU-intensive applications that push the limits of electronic accelerators. Hardware and cloud providers are responding with photonic-enabled solutions. For example, in March 2025, Ayar Labs, a U.S.-based optical AI hardware company, introduced the world’s first UCIe optical chiplet for AI scale-up architectures, highlighting industry movement toward integrating photonic co-processors into high-density AI clusters. This trend is reflected in strategic acquisitions, partnerships, and pilot deployments, demonstrating that photonic accelerators are becoming a practical, energy-efficient alternative for hyperscalers and enterprises seeking scalable, next-generation AI infrastructure.

Photonic AI Accelerators Industry Trends and Strategic Insights

- Photonic AI accelerators are emerging as a strategic solution to overcome power efficiency and bandwidth limitations associated with conventional GPU-based AI infrastructure, particularly in large-scale generative AI and hyperscale computing environments.

- Commercial momentum is shifting from pure research initiatives toward early-stage infrastructure deployment, supported by growing investments from hyperscalers, semiconductor manufacturers, and optical networking companies focused on next-generation AI compute ecosystems.

- Hybrid electro-photonic computing architectures are gaining significant industry attention due to their ability to combine electronic processing flexibility with the speed and energy efficiency advantages of optical computation.

- Increasing energy consumption associated with large language models and AI supercomputing clusters is creating strong demand for low-power optical computing technologies, positioning photonic AI accelerators as a high-potential segment within next-generation AI infrastructure development.

Photonic AI Accelerators Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 2.13 Billion | |

| 2035 Projected Market Size | US$ 41.27 Billion | |

| CAGR (2026-2035) | 34.5% | |

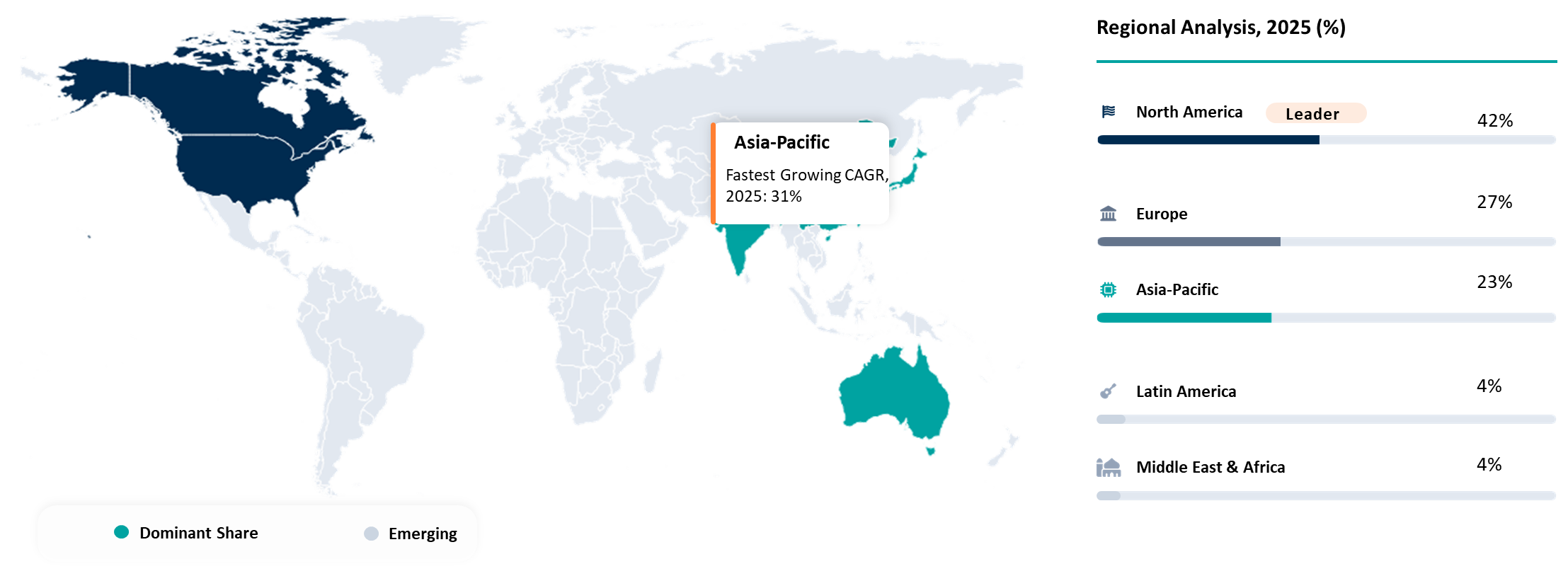

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Component | Hardware, Software and Services | |

| ByTechnology | Silicon Photonics (SiPh), Hybrid Photonic-Electronic Integration, Thin-Film Lithium Niobate (TFLN) and Others | |

| By Deployment Mode | On-Premises and Cloud-Based | |

| By End-User | Data Centers, IT and Telecommunications, Healthcare and Life Sciences, Aerospace and Defense, BFSI and Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Disruption Analysis

Growing Shift Toward Optical AI Computing Infrastructure

The photonic AI accelerators market is witnessing a substantial shift due to the rising utilization of optical computing solutions within AI infrastructure settings. Traditional GPU and CPU architectures are encountering escalating challenges in terms of power usage, heat dissipation, memory throughput, and data movement efficiency as generative AI algorithms and AI training clusters grow in size. Photonic AI accelerators capitalize on the use of photons for information transport and optical computation, offering enhanced speeds, reduced latency, and increased efficiency.

The change is impacting investment plans of many players in the semiconductors industry, hyperscale data centers, and AI hardware industry significantly. Investment plans in silicon photonics, optical interconnects, and photonic integrated circuits for providing support to AI computing systems infrastructure have been made by technology giants, cloud service providers, and semiconductor companies. This also indicates the growing adoption of optical AI technology, which further promotes developments in semiconductor packaging, systems integration, and high-bandwidth networking solutions, resulting in greater growth opportunities for photonic AI accelerators.

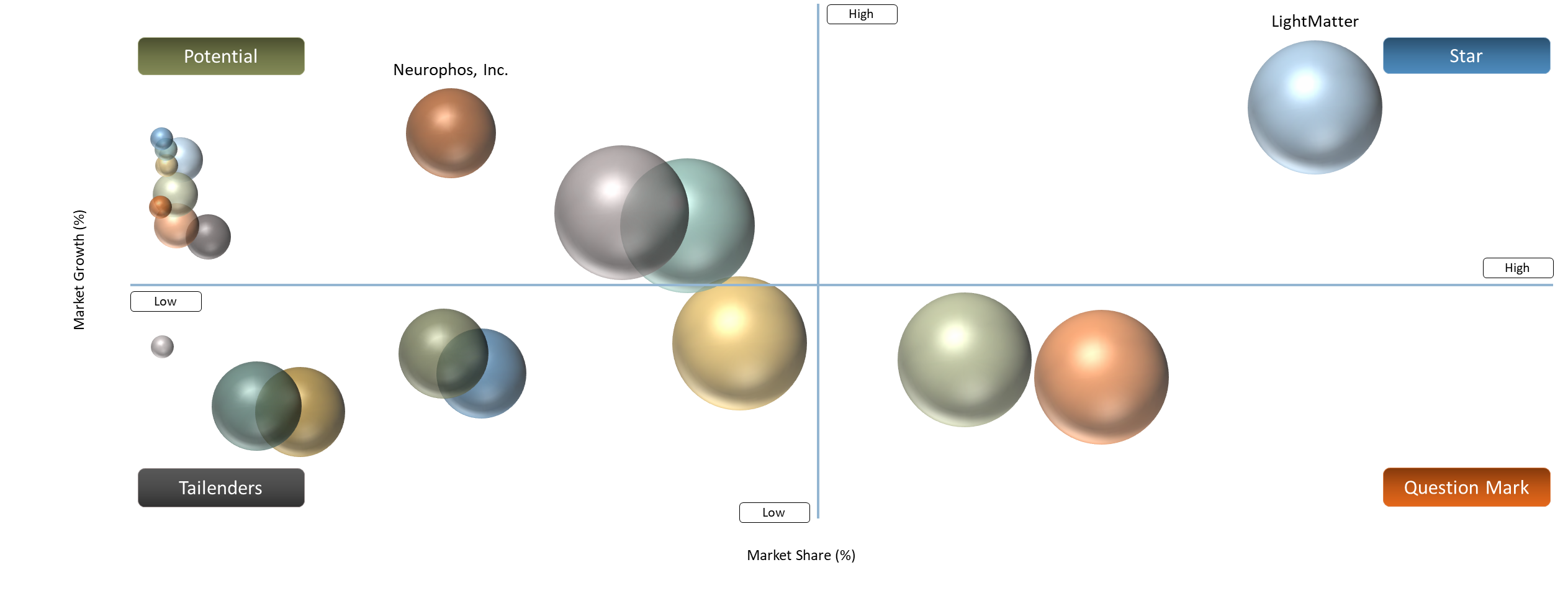

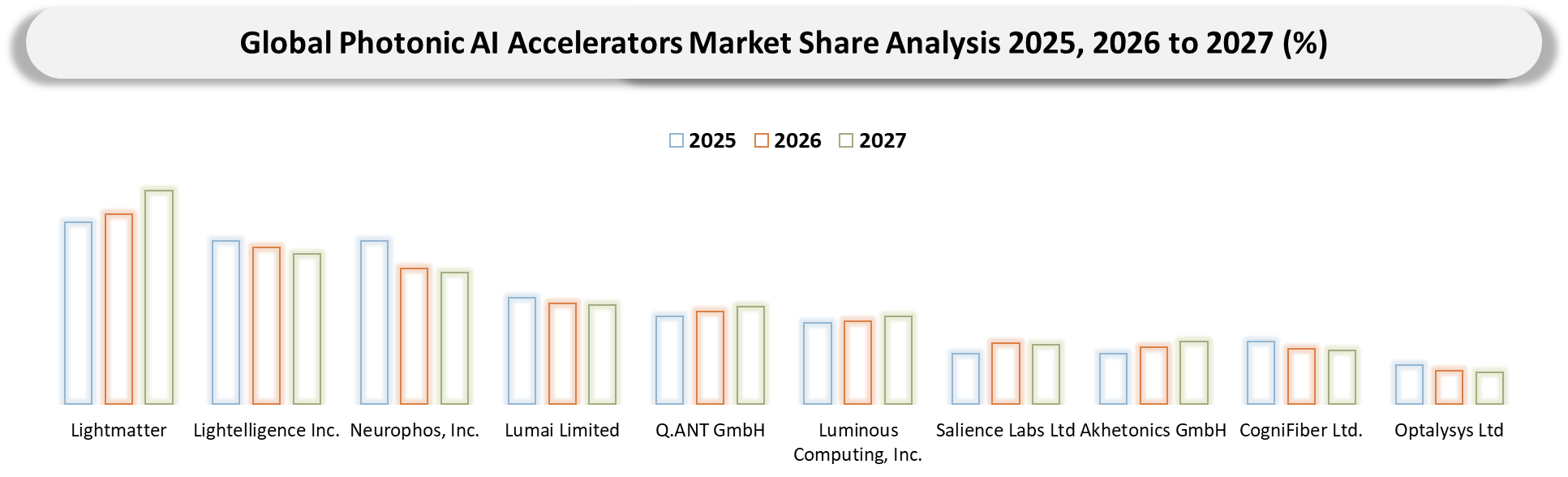

BCG Matrix: Company Evaluation

Market leaders like Lightmatter and Lightelligence Inc. fall under Stars due to their technological superiority, significant investment flows, and early success in reaching out to hyperscalers looking for energy-efficient AI computing options. This group benefits from rapid adoption in advanced AI computing architecture and strong IP positioning.

Companies such as Luminous Computing, Inc., Q.ANT GmbH, Salience Labs Ltd, and Akhetonics GmbH can be considered as Question Marks since they are in high growth but still commercialization phases with immense technical capabilities and little large-scale applications. The final market position of these firms relies heavily on fabrication readiness and ecosystem integration.

Novel innovators like Neurophos, Inc., Lumai Limited, CogniFiber Ltd., and Optalysys Ltd belong to the category of Potential since they have innovative pipelines but lack commercial footprint and adoption at an early stage for niche applications.

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Increasing Demand for High-Speed, Energy-Efficient AI Compute Infrastructure Across Hyperscale Data Centers | 5% | North America, Europe, Asia-Pacific hyperscalers | AI training, LLM inference, HPC workloads | Accelerates optical AI infrastructure adoption |

Rising Adoption of Cloud Computing and Edge Computing Architectures | 4% | Cloud providers, telecom, industrial sectors | Edge AI, real-time analytics, autonomous systems | Expands low-latency AI computing deployment |

Increasing Power Consumption Constraints in Conventional GPU and CPU Architectures | 5% | AI data centers, supercomputing facilities | AI supercomputing, generative AI processing | Drives shift toward energy-efficient photonic computing |

Rapid Advancements in Silicon Photonics and Optical Interconnect Technologies | 4% | Semiconductor and optical networking ecosystems | Optical AI networking, data center acceleration | Strengthens the commercialization of photonic AI solutions |

Increasing Demand for High-Speed, Energy-Efficient AI Compute Infrastructure Across Hyperscale Data Centers

The increasing demand for high-speed, energy-efficient AI compute infrastructure across hyperscale data centers is a primary driver of the photonic AI accelerators market. As generative AI training clusters scale to thousands of GPUs, traditional electrical interconnects are becoming performance bottlenecks due to bandwidth ceilings, rising latency, and excessive power consumption. Hyperscalers now require ultra-high-bandwidth, low-latency communication fabrics that can scale horizontally without proportionally increasing energy usage or thermal output. Photonic-based accelerator and interconnect architectures address this challenge by transmitting data in light, enabling significantly higher bandwidth density and lower energy per bit than conventional copper-based systems.

For instance, in 2025, Lightmatter, a U.S.-based technology company, unveiled its Passage M1000 photonic superchip, designed to deliver massive chip-to-chip bandwidth for AI clusters. The platform integrates large photonic interposers to enable optical communication across AI processors, reducing electrical congestion and improving cluster-scale efficiency. The development reflects a broader infrastructure shift toward optical compute and interconnect technologies to support high-speed, energy-optimized AI deployment at hyperscale.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

| Complexity in Integration with Legacy IT Systems | 3.7% | AI infrastructure integration | Enterprise AI deployment, hybrid data centers | Slows large-scale adoption across legacy environments |

| High Initial Infrastructure Investment and Deployment Costs | 4.1% | Capital expenditure and scalability | Hyperscale AI clusters, optical AI infrastructure | Limits adoption among cost-sensitive enterprises |

| Limited Commercialization and Standardization Across Photonic Computing Ecosystems | 3.5% | Technology interoperability | Photonic AI platforms, optical computing systems | Delays ecosystem maturity and commercial scalability |

| Dependence on Advanced Semiconductor Fabrication Infrastructure | 3.9% | Semiconductor manufacturing | Photonic chip production, advanced packaging | Increases supply chain and production risks |

Complexity in Integration with Legacy IT Systems

Despite rising demand for high-speed, energy-efficient infrastructure, integration with legacy IT systems remains a major challenge. Many enterprises operate on outdated hardware and monolithic architectures not designed for cloud-native or edge-based environments. This creates compatibility issues, extended deployment cycles, and higher implementation risks. Organizations often require customized middleware, APIs, and system reconfiguration to enable interoperability, increasing overall costs. Data migration from traditional systems to hybrid or distributed models can also lead to downtime and compliance concerns.

Legacy platforms frequently lack scalability to support AI-driven analytics and real-time processing workloads. As a result, enterprises adopt phased modernization strategies, delaying full infrastructure transformation. These complexities make companies cautious about rapid upgrades, particularly for mission-critical operations. Businesses, therefore, prioritize vendors that offer seamless integration, backward compatibility, and strong technical support.

Segment Analysis

The global photonic AI accelerators market is segmented based on component, technology, deployment mode, end-user, and region.

Integrated Photonic Hardware Accelerators Enabling Scalable AI Datacenter Architectures

The hardware segment is dominant with approximately 62% market share, driven by hyperscalers demanding ultra-high-bandwidth, energy-efficient interconnects to scale AI clusters beyond electrical limitations. Photonic co-packaged optics enable direct optical connectivity between accelerators, significantly reducing power consumption and latency in multi-rack AI deployments. This is particularly critical for large language model training environments and AI supercomputing systems where interconnect bandwidth defines overall cluster performance. Industries such as cloud computing, advanced research, and high-performance AI infrastructure are leading adoption.

For instance, in 2025, Ayar Labs, a U.S.-based optical I/O solutions company, partnered with Alchip to unveil a co-packaged optics solution for AI datacenter scale-up architectures, integrating TeraPHY optical I/O with advanced ASIC platforms. The solution enables more than 100 Tbps bandwidth per accelerator and supports hundreds of optical scale-up ports, addressing the bandwidth bottlenecks of traditional copper interconnects. This development highlights how hardware innovation is directly enabling scalable, energy-efficient AI infrastructure at hyperscale.

AI-Optimized Software and Orchestration Platforms Accelerating Hybrid Compute Adoption

The software segment is the fastest growing, accounting for approximately 26% of the market, as AI infrastructure increasingly depends on intelligent orchestration layers to manage hybrid electronic-photonic environments. Demand is driven by the need to integrate advanced accelerators into AI workflows using optimized compilers, runtime environments, and performance-tuned frameworks. Software abstraction reduces deployment complexity while maximizing accelerator efficiency across AI training, scientific simulation, and advanced computing workloads.

For instance, in 2024, NVIDIA, a U.S.-based semiconductor and AI computing company, expanded its AI-supercomputing ecosystem through partnerships advancing CUDA-Q and hybrid quantum-AI workflows, demonstrating how optimized software stacks enhance accelerator performance. Such developments reflect a broader ecosystem shift toward software-defined acceleration, where orchestration and toolchains play a decisive role in unlocking the full potential of next-generation compute architectures, including photonic-enabled systems.

Geographical Penetration

Rising Strategic Semiconductor Investments in Asia‑Pacific to Accelerate Photonic AI Adoption

Asia‑Pacific is rapidly emerging as the fastest-growing region in the global photonic AI accelerators landscape, driven by strategic government and industry investments aimed at strengthening domestic semiconductor ecosystems and reducing reliance on foreign compute technologies. Countries across the region are boosting advanced fabrication capabilities, AI chip manufacturing, and technology transfer partnerships to support next‑generation compute infrastructure that integrates photonic and electronic accelerator components. For example, in 2025, GlobalFoundries completed its acquisition of Singapore’s Advanced Micro Foundry to accelerate AI data‑processing chip production within Asia‑Pacific, reinforcing regional capability to produce advanced logic and photonics‑ready semiconductor technologies at scale. This move highlights the commitment of both public and private stakeholders to localize cutting‑edge compute supply chains and expedite commercialization of photonic accelerators capable of supporting high‑performance AI workloads across data centers, telecom, and industrial applications.

Japan Photonic AI Accelerators Market Outlook

Japan is advancing photonic AI accelerators through coordinated semiconductor strategy and deep investments in next‑generation compute infrastructure. National and industry bodies are prioritizing photonic‑ready fabrication and co‑packaged optics to support future AI workloads, reflecting a shift from research experimentation to pilot‑level buildouts. For instance, in 2025, Rapidus, a Japan‑based semiconductor technology company, expanded its advanced process development roadmap to include photonics‑ready fab capabilities designed to support integrated photonic accelerators and optical interconnect technologies for AI and high‑performance computing systems. This move aligns with Japan’s broader semiconductor sovereignty goals and positions the country to bridge photonics research with scalable, domestic manufacturing capacity for energy‑efficient AI acceleration.

China Photonic AI Accelerators Market Trends

China’s photonic AI accelerator landscape is rapidly evolving around performance breakthroughs and indigenous hardware innovation targeted at energy‑efficient generative AI and compute‑intensive workloads. Research groups and technology developers are showcasing optical compute modules that dramatically raise throughput and reduce energy demands compared with traditional electronics. For instance, in December 2025, a Chinese research‑based initiative demonstrated a custom optical AI chip capable of up to 100× faster performance and superior energy efficiency relative to certain legacy electronic accelerators in generative inference tasks, signaling China’s push to embed photonic computing into domestic AI infrastructure. These advances underscore the strategic focus on self‑reliant semiconductor ecosystems that can accelerate photonic AI deployment across data centers, telecom networks, and edge compute environments.

Rising Hyperscale AI Connectivity and Photonic Integration Momentum in North America

North America accounts for approximately 38% of the global photonic AI accelerators market in 2025, positioning it as the leading regional hub driven by hyperscale AI cluster expansion, generative AI model training, and energy-aware infrastructure strategies. For instance, in 2025, Astera Labs, a U.S.-based semiconductor company, acquired aiXscale Photonics to integrate optical fiber-chip coupling technology into AI accelerator ecosystems, enabling higher throughput and lower power consumption. This move reflects broader regional trends toward consolidating photonic capabilities to meet growing AI performance and infrastructure needs

U.S. Photonic AI Accelerators Market Insights

The United States continues to lead in photonic AI hardware commercialization, emphasizing interoperability and high-performance scale-up solutions. For instance, in 2025, Ayar Labs, a U.S.-based optical AI hardware company, introduced the world’s first Universal Chiplet Interconnect Express (UCIe) optical chiplet, delivering multi-terabit-per-second bandwidth for AI scale-up architectures. This innovation reduces data movement bottlenecks, enables energy-efficient high-speed links between accelerators, and accelerates adoption of photonic co-processors within hyperscale AI systems.

Canada Photonic AI Accelerators Industry Growth

Canada is expanding its role in advanced photonic and quantum computing technologies through strategic collaborations and pilot deployments. For instance, in 2025, Xanadu, a Canada-based quantum photonics company, expanded its partnership with A*STAR to advance integrated photonic quantum computing platforms, covering hardware, algorithms, and light-source technologies. This initiative strengthens Canada’s innovation ecosystem, positions the country for future photonic AI and quantum-enabled high-performance computing applications, and underscores the regional emphasis on sustainable and scalable AI infrastructure solutions.

Competitive Landscape

- The global market for photonic AI accelerators is marked by the presence of firms that specialize in photonic computing and optical semiconductors, which are involved in the research and development of advanced AI processing techniques using silicon photonics, optical neural networks, and photonic integrated circuits. Some of the leading firms in this market include Lightmatter and Lightelligence, which are engaged in innovations related to optical AI processors, photonic interconnects, and co-packaged optics aimed at hyperscale AI computing systems and large language models. Additionally, Luminous Computing is considered an important player in this market, which develops optical computing systems to enhance AI processing efficiency and minimize energy use.

- Emerging companies such as Neurophos, Lumai Limited, Q.ANT GmbH, Salience Labs Ltd., Akhetonics GmbH, CogniFiber Ltd., and Optalysys Ltd. have been enhancing the competitive scenario with new developments in the field of photonic tensor processing, optical inference acceleration, neuromorphic photonics, and AI communication. Competition in the market has intensified due to the increasing demand for innovations in terms of optical computing scalability, energy-efficient AI acceleration, photonic chip fabrication technology, and the ability to integrate with existing semiconductor platforms. The strategic alliances and venture funding by these firms, alongside partnerships with AI infrastructure vendors and semiconductor foundries, will contribute to increased competition in the optical AI computing industry.

Major Pain Points

- High Infrastructure and Development Costs: Development of photonic AI accelerators requires substantial investments in silicon photonics, advanced semiconductor fabrication, optical packaging, and high-performance AI infrastructure, creating cost barriers for commercialization and adoption.

- Complexity in Integration with Existing Electronic Systems: Integration of photonic processors with conventional GPU-, CPU-, and electronic-based AI environments remains technically complex due to interoperability limitations and hybrid architecture requirements.

- Limited Software Ecosystem and Programming Compatibility: Lack of mature software frameworks, AI development tools, and standardized programming environments for photonic computing platforms restricts enterprise deployment and developer adoption.

- Scalability Challenges in Photonic Chip Manufacturing: Manufacturing photonic integrated circuits and optical AI processors at commercial scale remains challenging due to fabrication precision requirements, packaging complexity, and yield optimization limitations.

- Thermal Stability and Optical Signal Reliability Issues: Photonic computing systems are highly sensitive to thermal fluctuations, optical signal losses, and wavelength instability, impacting operational efficiency and processing accuracy.

- Dependence on Advanced Semiconductor Supply Chains: The market relies heavily on specialized semiconductor foundries, optical component suppliers, and advanced packaging ecosystems, increasing exposure to supply chain disruptions and production bottlenecks.

- Shortage of Skilled Photonics and Optical Engineering Talent: Limited availability of expertise in photonic circuit design, optical computing, semiconductor packaging, and AI hardware engineering is slowing product innovation and commercialization activities.

- High Competitive Pressure from Conventional AI Accelerators: Rapid advancements in GPUs, TPUs, ASICs, and other electronic AI accelerator technologies continue to create strong competitive pressure on emerging photonic computing platforms.

- Limited Commercial Maturity of Optical Computing Technologies: Many photonic AI accelerator technologies remain in research, prototype, or early commercialization stages, resulting in longer validation cycles and slower enterprise adoption rates.

- Rising Power and Cooling Requirements in AI Data Centers: Increasing AI workload density and large-scale model training requirements are intensifying data center energy consumption and cooling challenges, creating operational pressures for infrastructure providers.

Key Developments

- In April 2025, Lightmatter introduced a six-chip photonic AI processor capable of delivering high-performance AI computing with lower power consumption through integrated photonic tensor cores and optical interconnect technologies. The processor supports unmodified AI models, including ResNet and BERT, highlighting advancements in commercial photonic computing solutions for hyperscale AI infrastructure and energy-efficient data center applications.

- In February 2025, STMicroelectronics, a France‑based semiconductor company, introduced a next‑generation data centre photonics chip developed in collaboration with Amazon Web Services to improve AI data‑processing speeds and energy efficiency through optical connectivity for high‑bandwidth AI workloads.

- In April 2025, Lightmatter launched its Passage L200 and M1000 silicon photonics platforms to improve GPU interconnect efficiency in AI data centers using optical communication technologies. The development strengthens adoption of co-packaged optics and high-bandwidth optical interconnects aimed at accelerating AI model training, reducing GPU idle time, and improving scalability across hyperscale AI infrastructure.

- In May 2025, AMD, a U.S.‑based semiconductor company, acquired Enosemi to accelerate co‑packaged optics innovation, enhancing its ability to integrate high‑speed optical interconnects into future AI accelerator and data‑centre platforms.

Analyst Opinion

- Rapid expansion of generative AI, large language models, and hyperscale AI clusters is significantly increasing demand for high-bandwidth, energy-efficient computing architectures, accelerating industry interest in photonic AI accelerators as an alternative to conventional GPU-centric systems.

- Silicon photonics, co-packaged optics (CPO), and optical I/O technologies are emerging as critical infrastructure components for next-generation AI data centers, particularly as AI networking bandwidth requirements move toward 800G and 1.6T environments.

- Increasing GPU power consumption and thermal management challenges are encouraging hyperscale operators and semiconductor companies to invest in optical interconnect technologies capable of improving AI training efficiency and reducing infrastructure energy costs.

- North America continues to lead technological innovation due to strong investments from hyperscale cloud providers, semiconductor companies, and AI infrastructure developers, while Asia-Pacific is strengthening its position through semiconductor manufacturing expansion and silicon photonics research initiatives.

- Advancements in photonic integrated circuits, optical neural networks, and chiplet-based architectures are improving the commercial viability of photonic AI accelerators for large-scale AI training and inference applications.

- Growing investments in AI supercomputing facilities and hyperscale AI factories are creating long-term opportunities for optical computing technologies capable of addressing bandwidth bottlenecks and GPU interconnect limitations.

- Increasing research activity across neuromorphic photonics, optical tensor processing, and low-power AI acceleration technologies is expected to support long-term evolution of the market toward commercially scalable optical computing ecosystems.

Why Choose DataM?

- Data-Driven Insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, you benefit the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. This approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. This personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. These insights complement and go beyond what is typically available in generic databases.

Target Audiance

| INDUSTRY | WHO SHOULD BUY THIS REPORT? | REASON TO BUY THIS REPORT |

| Hyperscale Cloud & Data Center Operators | AI Infrastructure Teams, Data Center Architects, CTOs, Network Engineering Managers | Analyze adoption of photonic AI accelerators for high-bandwidth AI workloads, power-efficient computing, and optical interconnect optimization |

| Semiconductor & AI Chip Companies | Semiconductor R&D Teams, Product Strategy Heads, AI Hardware Engineers | Evaluate advancements in silicon photonics, co-packaged optics, and next-generation AI accelerator technologies |

| Optical Networking & Photonics Companies | Photonics Engineers, Optical System Designers, Technology Innovation Teams | Assess market opportunities in optical I/O, photonic integrated circuits, and AI networking infrastructure |

| AI Software & Platform Providers | AI Platform Developers, Enterprise AI Teams, Cloud Solution Architects | Understand evolving AI infrastructure requirements for large language models, AI inference, and hyperscale computing environments |

| Telecommunications & Edge Computing Providers | Telecom Infrastructure Teams, Edge Computing Strategists, Network Operators | Evaluate low-latency optical computing solutions for edge AI, real-time analytics, and distributed AI processing |

| Aerospace & Defense Organizations | Advanced Computing Teams, Defense Technology Strategists, Research Laboratories | Analyze adoption potential of photonic AI accelerators for autonomous systems, secure AI processing, and high-performance computing applications |

| Research Institutions & Universities | AI Researchers, Photonics Research Teams, Semiconductor Innovation Centers | Assess emerging trends in neuromorphic photonics, optical AI computing, and next-generation semiconductor technologies |

| Investors & Venture Capital Firms | Technology Investors, Strategic Investment Teams, Market Intelligence Professionals | Identify high-growth investment opportunities across silicon photonics, optical AI infrastructure, and advanced semiconductor ecosystems |