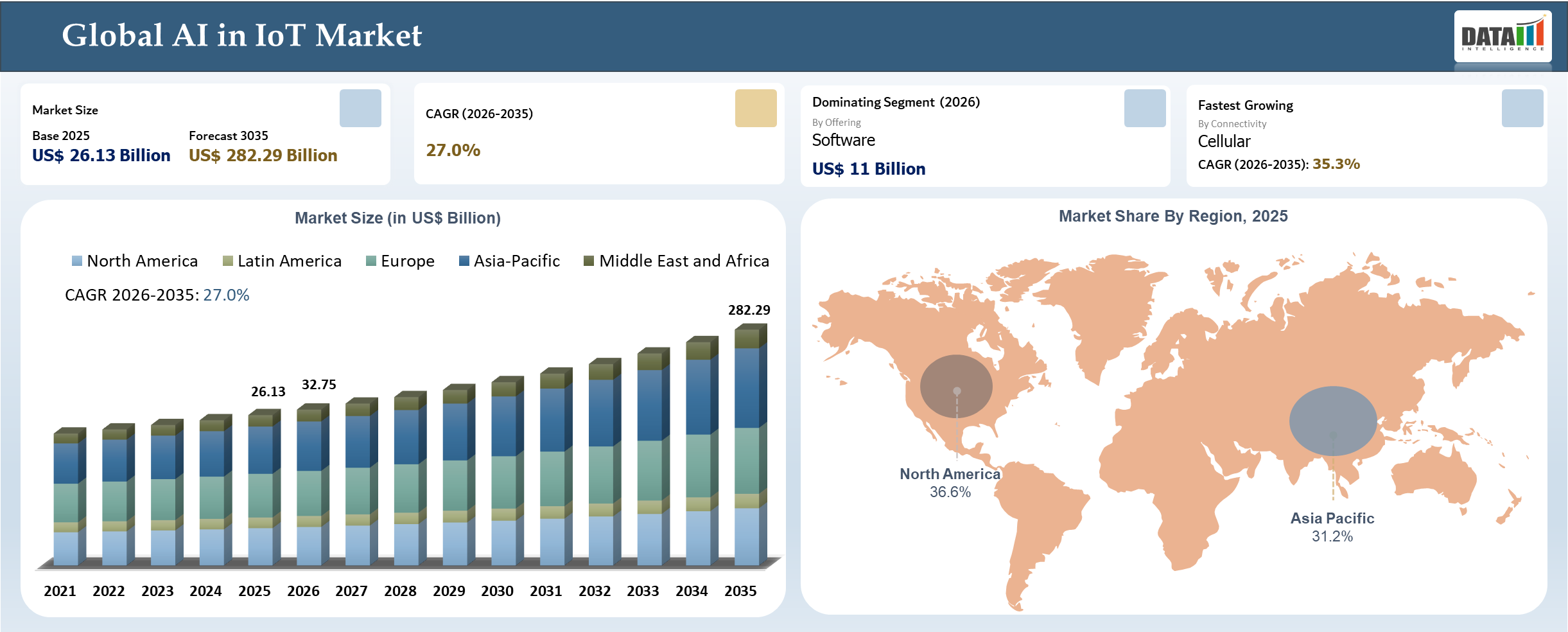

AI in IoT Market Size

The global AI in IOT market reached US$ 4.08 billion in 2025 and is expected to reach US$ 6.45 billion by 2035, growing with a CAGR of 4.8% during the forecast period 2026-2035. Witnessing fast-paced developments since businesses are shifting their focus from deploying technologies that just facilitate connections to intelligent solutions that interpret and act on the collected data. The market is very fragmented, yet the AI-powered IoT ecosystem is rapidly growing, fueled by rising adoption of AI among enterprises and widespread adoption of IoT in a range of industry verticals, from manufacturing and retail to consumer markets. The combination of AI and IoT leads to predictive, prescriptive, and autonomous decision-making in asset-heavy industries. Major vendors in the market include cloud hyperscalers, industrial automation vendors, and semiconductor players; software, edge AI, and services are key value areas.

AI in IOT Industry Trends and Strategic Insights

- AI IoT Market is undergoing an intense move towards edge-first intelligence solutions due to the necessity of low latency and real-time decisions. Firms like Microsoft Corporation and Amazon Web Services have been extending AI-powered IoT solutions where analytics will be embedded in their devices' ecosystem.

- Organizations like Siemens AG and Schneider Electric have been integrating AI within their operations technology for improving asset management and predictive maintenance.

- Further, semiconductor firms like NVIDIA Corporation and Intel Corporation are launching AI chips that are specifically designed for IoT computing, making edge inference possible. Moreover, there have been synergies between telecommunication operators and IoT platform companies to incorporate AI within 5G networks.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 4.08 Billion | |

| 2035 Projected Market Size | US$ 6.45 Billion | |

| CAGR (2026-2035) | 4.8% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Offering | Hardware, Software, and Services | |

| By Deployment layer | Endpoint Device, Edge Node, On Premises Platform, Cloud Platform, and Hybrid Distributed | |

| By AI Technology | Machine Learning, Deep Learning, Computer Vision, Speech and Audio, Natural Language and LLM, Reinforcement and Optimization, Federated Learning, and Generative AI | |

| By Connectivity | Cellular, Short Range (Wi-Fi and Bluetooth), Mesh (Zigbee, Thread, Matter Adjacent Device Layer), LPWAN (LoRaWAN and proprietary LPWAN), Wired (Ethernet, Industrial Ethernet, Fieldbus, Serial), and Satellite IoT | |

| By Organization Size | Large Enterprise, Mid-Market, and SME | |

| By Business Model | CAPEX Led, Subscription Led, Usage Led, and Outcome Led | |

| By Data Modality | Vision (Image and Video), Audio (Acoustic and Speech), Time Series, Location (GNSS and RTLS), and Multimodal (Vision, Audio, Sensor Fusion) | |

| By Application | Industrial Operations, Asset and Fleet, Energy and Utilities, Healthcare, Retail and Consumer, Agriculture, and Buildings and Cities | |

| By End-User | Manufacturing, Energy and Utilities, Transportation and Logistics, Healthcare, Retail, Buildings, Agriculture, Automotive and Mobility, Mining, and Public Sector | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

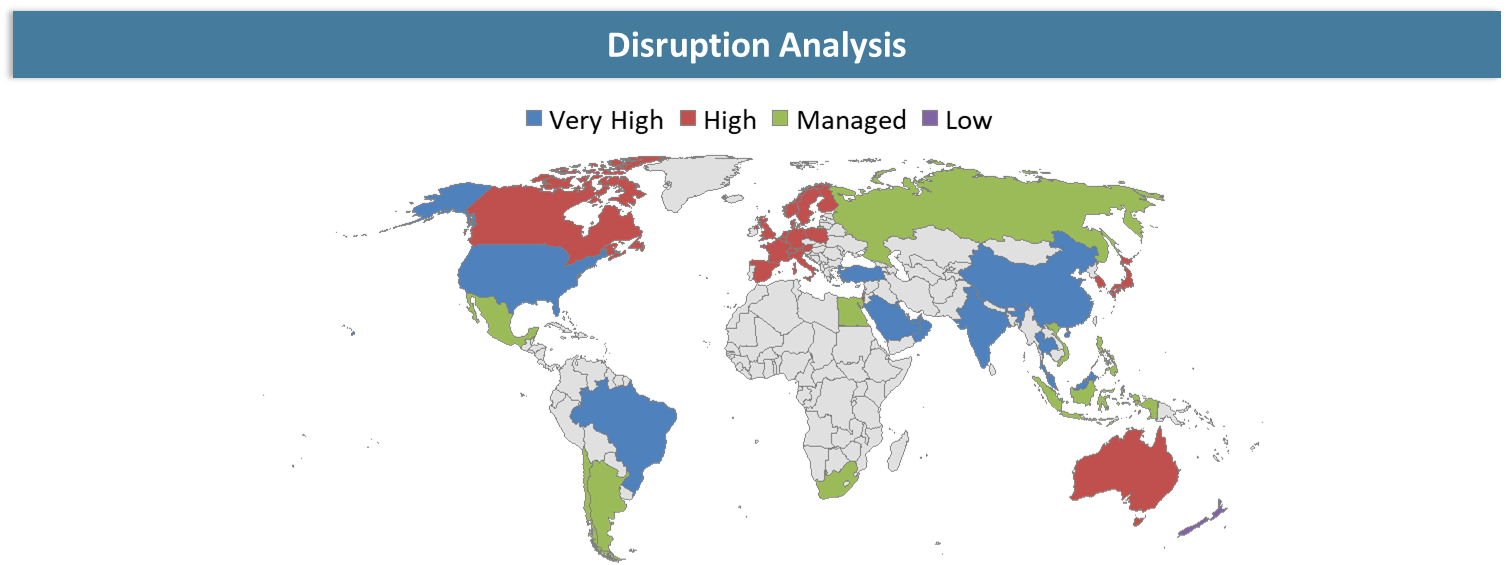

Disruption Analysis

Shift from Cloud-Centric IoT to Distributed Edge AI Architectures Reshaping Decision-Making Models

Disruptive change is occurring within the AI IoT market due to the replacement of traditional IoT approaches with a decentralized computing model. Edge AI technology is causing changes in the way data is computed, with the focus now on computing close to where data is captured, thus resulting in a reduction in latency. These developments have led to disruptions among traditional system integrators as well as vendors who were used to deploying IoT solutions through centralized cloud computing and manual analysis of data.

AI-enabled platforms are making it easier for firms to launch projects quickly while minimizing any need for customized integration. The combination of AI, IoT, and connectivity technologies such as 5G is leading to innovative business models involving the provision of outcome-based and autonomous operations. Organizations that will not align themselves to these trends within the market will become irrelevant in future.

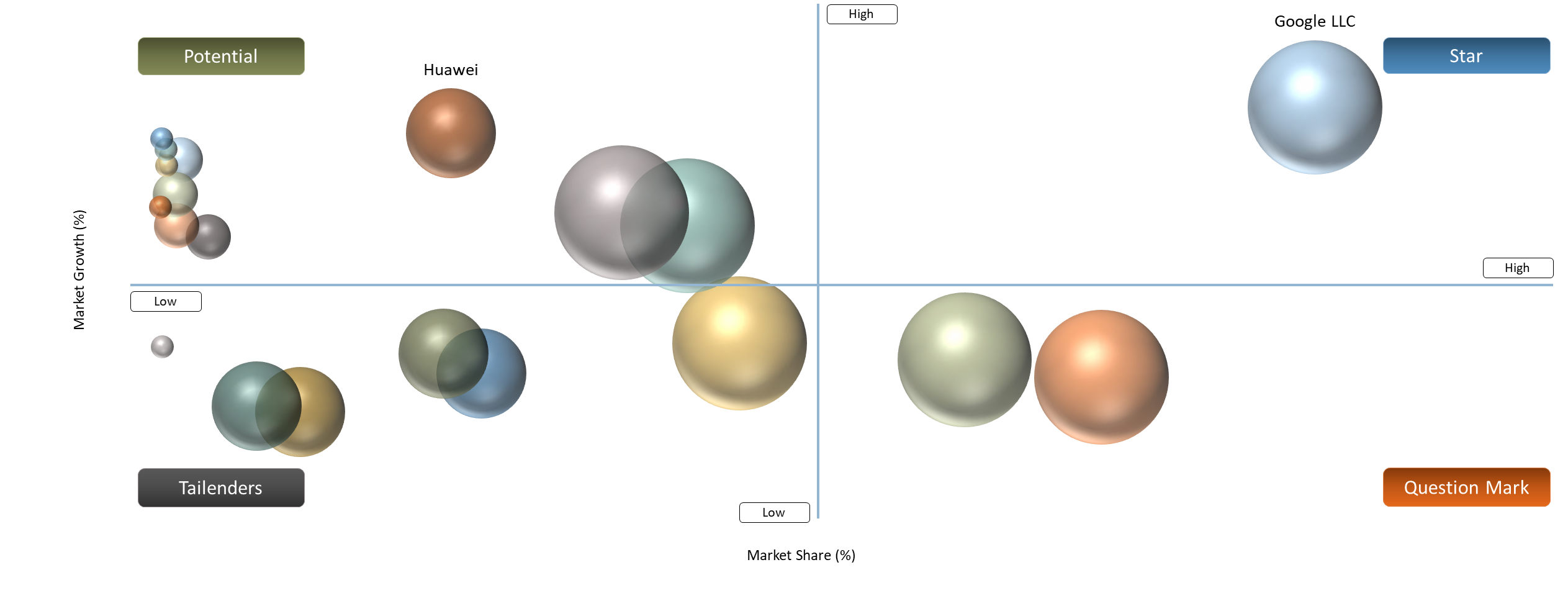

BCG Matrix: Company Evaluation

Hyperscalers such as Google LLC and Microsoft Corporation would be classified as Star, due to their high AI capabilities and scalability of their IoT offering. Companies specializing in industrial automation such as ABB Ltd and Siemens AG would be considered as Question Mark, based on their existing footprint and industry know-how.

Start-ups that provide edge AI as well as AI chipsets are classified as Potential, having high growth potential, although a small market share at this time. Companies providing IoT connectivity solutions, as well as hardware providers transitioning into AI-based offerings, are classified as Tailenders.

Market Dynamics

Industrial Edge AI Adoption in Asset-Intensive Industries

Rapid integration of edge AI in asset-heavy industries like manufacturing, energy, and logistics will fuel the growth of the AIoT market. Increasing use of AI models at the edge of IoT devices will help enterprises monitor operations in real time, predict maintenance requirements, and automate decision making. It not only saves time but also helps minimize costs involved in sending the data to cloud-based AI models. Companies such as Siemens AG and Schneider Electric are increasingly adopting AI in their industrial IoT systems to enhance the performance of their assets while reducing downtime.

Fragmented Data Ecosystems and Integration Complexity

Even though it has huge growth opportunities, the AI in IoT (AIoT industry) is plagued by issues associated with data ecosystem fragmentation and system integration. Most companies use their legacy systems that have disparate data, thus limiting the ability to deploy AI in the environment. The non-interoperable nature of the platforms used by the devices also presents a challenge.

Moreover, the deployment of AI models through various IoT devices needs knowledge of data engineering, model training, and deployment. Such processes are costly and hinder small to medium-sized companies from using the technology. While firms like Cisco Systems have been developing architectures that would allow a unified approach to the problem, system integration still poses significant restraints to the industry's growth.

Segment Analysis

The global AI in IOT market is segmented based on offerings, deployment layer, AI technology, connectivity, organization size, business model, data modality, application, end-user and region.

Edge AI Emerging as the Core Value Layer Enabling Real-Time Intelligence in IoT Ecosystems

Edge AI is considered the most significant and fastest-growing portion of the AI in the Internet of Things market, which stems from the necessity to process data and make decisions promptly. In contrast to cloud AI, edge AI provides opportunities to perform calculations directly on devices or closer to them, thus making it possible to lessen reliance on centralized infrastructures. The necessity to have a prompt reaction becomes especially relevant in industrial settings.

In order to facilitate the widespread implementation of edge AI, there is an active development of hardware solutions, such as AI chips produced by firms like NVIDIA Corporation and Intel Corporation. With the help of AI chips, it becomes possible to execute models of AI on devices that lack computing power. Moreover, there is a growing variety of scenarios in which edge AI is employed. Smart city, healthcare, and autonomous vehicles industries benefit from combining edge AI with IoT, making the latter more efficient.

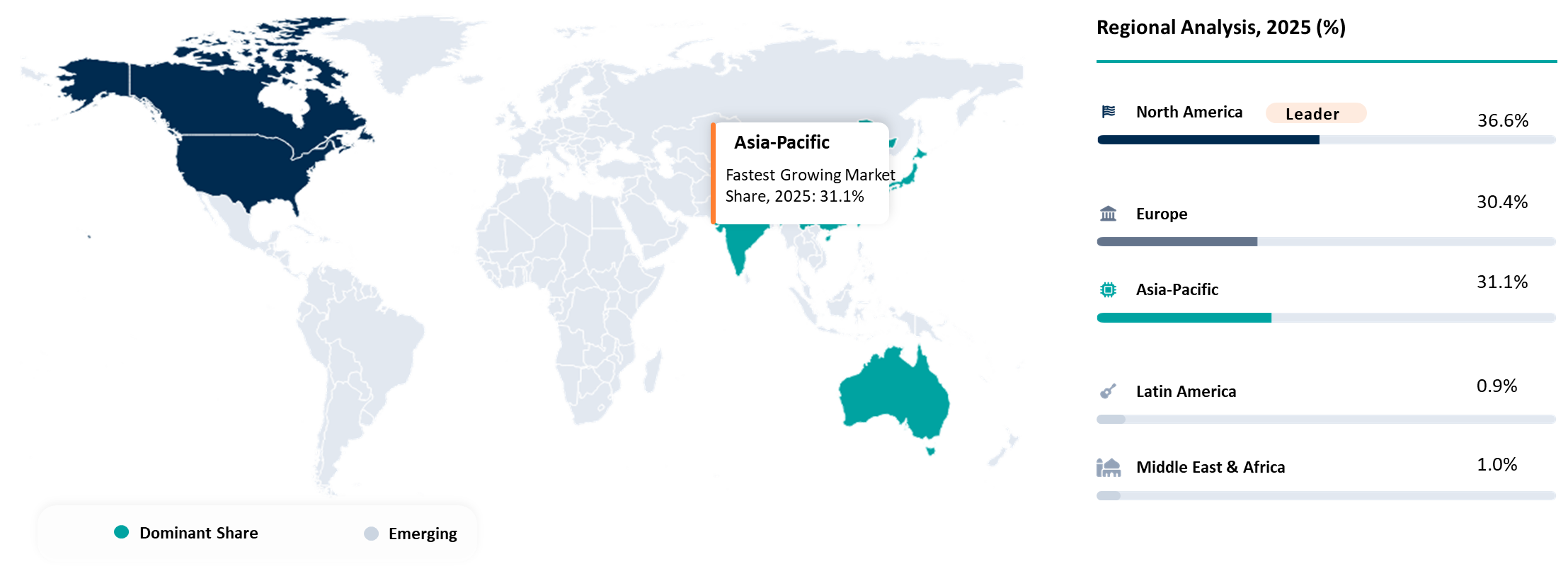

Geographical Penetration

Asia-Pacific Leading AI in IoT Scale-Up Through Manufacturing Dominance and Government-Led Digital Transformation

As compared to any other geographical region, Asia-Pacific appears to be the most aggressive when it comes to the implementation of artificial intelligence in IoT, owing to the powerful manufacturing base, fast-paced urbanization, and digitally transformative government initiatives in the region. While the countries in this region have already begun using the concept of IoT, they are now rapidly moving towards implementing the concept of IoT in conjunction with AI, mainly in smart factories, energy grids, logistics, and smart cities.

The most important thing about the Asia-Pacific is the fact that they are doing it in a way where AI is used at the entire system level rather than being confined to any particular use case. The governments of the nations in the region are heavily investing in various projects in relation to industry 4.0, smart mobility, and intelligent infrastructure, which facilitates the adoption of AI. With 5G network expansion in the region, even edge AI implementation is made easier with low latency communication between devices.

Moreover, Asia-Pacific has emerged as an important center for manufacturing hardware for AI IoT, such as sensors, edge computing devices, and AI processors, making the area less reliant on imports and making installation costs more economical. With strong competition from local companies in addition to fast-developing startups, the region stands out as an innovator of AI in IoT applications.

China AI in IOT Market Trends

China dominates the AI in IoT landscape in Asia-Pacific due to the scale of adoption by the country, along with government involvement and an integrated tech ecosystem in China. AI-powered solutions have been widely adopted by Chinese companies across various industries, including smart city operations, automated industrial operations, surveillance operations, and energy management operations.

It should be noted that China has been using AI and IoT solutions extensively at a mass level. There is a wide network of interconnected devices, as well as good availability of data. In addition to this, the country has made it its aim to lead the world in AI solutions through extensive investments in AI-based research and innovations. The adoption of AI-based solutions for the purpose of predicting, managing and optimizing processes in industries like manufacturing and energy generation has been increasing rapidly.

Moreover, China has been a leader in smart city development, where AI IoT solutions are being applied for real-time decision-making purposes related to traffic management, security, environmental monitoring, etc..

India AI in IOT Market Outlook

The country shows rapid development trends in terms of AI adoption in IoT due to the growth of digitalization efforts, government policies, and enterprise-level adoption in various industries. There are multiple use cases for AI-powered IoT in India in such segments as manufacturing, logistics, agriculture, and smart city solutions. Enterprises such as Tata Consultancy Services and Infosys Limited are working actively on IoT solutions empowered by AI.

The key driver of growth in India is the focus on operational efficiency and cost optimization that can be ensured with the help of AI solutions for IoT. Such a trend is supported by the work carried out under the Digital India policy implemented by the government and the growing development of IoT infrastructure in the region.

There is also a wide range of opportunities in agriculture and other rural areas for AI in IoT implementation in India. Such a diverse market makes it possible to develop cost-efficient and scalable AI solutions for IoT. Moreover, the growing entrepreneurial activity in the country along with the growing talent pool creates an excellent basis for further progress.

Competitive Landscape

- The market is defined by three intersecting categories: hyperscalers/enterprise AI platform players, industrial automation firms, and silicon/connectivity suppliers. Cloud to edge orchestration, device management capabilities, and AI capabilities added onto an IoT infrastructure make Microsoft and AWS strong; Siemens, Schneider Electric, ABB, Honeywell, Rockwell Automation, Bosch, Hitachi, and PTC stand out for their expertise in industrial applications like predictive maintenance, digital twin technologies, industrial connectivity, and asset optimization; and NVIDIA, Intel, Qualcomm, Cisco, Nokia, Ericsson, Huawei, Samsung, and Advantech offer expertise in edge compute platforms, industrial AI chipsets, industrial networking solutions, private wireless systems, and embedded computing devices. It makes the competitive landscape strongly ecosystem-based rather than winner-takes-all, where competitiveness will be increasingly determined by who is able to integrate edge AI, domain knowledge, connectivity, and lifecycle software management.

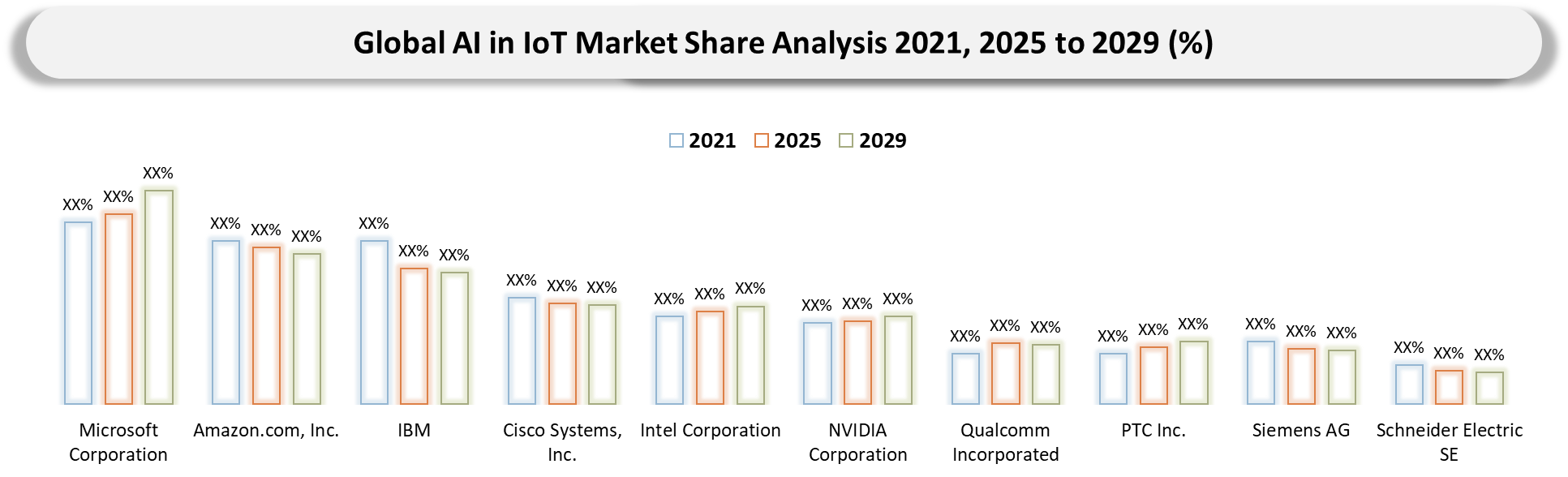

- Key players include Microsoft Corporation, Amazon.com, Inc., IBM, Cisco Systems, Inc., Intel Corporation, NVIDIA Corporation, Qualcomm Incorporated, PTC Inc., Siemens AG, Schneider Electric SE, ABB Ltd, Robert Bosch GmbH, Hitachi, Ltd., Huawei Investment and Holding Co., Ltd., Samsung Electronics Co., Ltd., Advantech Co., Ltd., Nokia Corporation, Telefonaktiebolaget LM Ericsson, Honeywell International Inc. and Rockwell Automation, Inc.

Key Developments

- Mar 2026 - Amazon Web Services rolled out advanced AI features in AWS IoT Core, such as automated anomaly detection and predictive analysis of devices

- Feb 2026 - NVIDIA Corporation updated its edge AI solution through additional GPU units suitable for IoT workloads

- Jan 2026 - Microsoft Corporation improved Azure IoT by incorporating AI copilots that allow device analytics and predictive analysis of industrial use cases

- Jan 2026 - Siemens AG implemented AI-driven predictive maintenance solutions for its entire industrial automation offering, with a focus on smart factories

- Dec 2025 - Schneider Electric launched an AI-based IoT solution aimed at energy optimization via real-time analytics of connected energy devices

- Nov 2025 - Cisco Systems introduced an AI-driven IoT networking solution that improves enterprise IoT networks' security and automation

- Oct 2025 - Intel Corporation developed AI chips for IoT purposes, making edge AI computation more effective and efficient

- Sep 2025 - Google LLC extended its AI analytics capabilities within Google Cloud IoT to enable AI-driven device data processing

- August 2025 - ABB Ltd incorporated AI in its IoT automation solutions in the field of industrial operations, with emphasis on predictive analytics and process optimization.

- July 2025 - Huawei Technologies used AI-driven IoT solutions in their city infrastructure projects, including traffic control and surveillance systems.

- June 2025 - Alibaba Cloud improved its AIoT solutions with industry-focused applications in manufacturing and logistics.

- May 2025 - Bosch Group developed its AI IoT solutions in the realm of industrial operations, particularly manufacturing and automation.

- April 2025 - IBM Corporation launched its AI IoT analytics solutions integrated with its hybrid cloud solution for corporate organizations.

- March 2025 - Oracle Corporation improved its IoT cloud solutions with AI functionalities to provide real-time data analytics and automation.

- February 2025 - SAP SE integrated its AI-based IoT solutions in its enterprise software applications for supply chain and asset management.

Why Choose DataM?

- Technological Innovations: Explores the latest advancements in AI in IOT design, including improved hydraulic systems, advanced operator controls, telematics integration, electric and hybrid powertrains and enhanced attachment versatility that are driving higher productivity and lower operating costs across construction and industrial applications.

- Product Performance & Market Positioning: Evaluates how different OEMs perform in real-world construction, landscaping, agriculture and municipal environments. The analysis compares lifting capacity, breakout force, fuel efficiency, durability, operator comfort and attachment compatibility, highlighting how leading manufacturers differentiate themselves globally.

- Real-World Evidence: Highlights practical use cases of AI in IOT across infrastructure development, road maintenance, warehouse handling and smart city projects. It demonstrates measurable improvements in jobsite efficiency, reduced labor dependency, faster material handling and optimized equipment utilization.

- Market Updates & Industry Changes: Tracks important industry developments such as new product launches, electrification initiatives, localized manufacturing expansions, tightening emission standards (Stage V, Tier 4 Final) and shifts in construction spending across major regions, including North America, APAC, China and India.

- Competitive Strategies: Analyzes how leading manufacturers are expanding their footprint through dealer network strengthening, localized production, electric model introductions, strategic partnerships and technology-driven differentiation such as AI-enabled monitoring and autonomous-ready platforms.

- Pricing & Market Access: Explains pricing structures across standard, high-capacity and electric skid steer models, including outright purchase, leasing and rental models. It also reviews regional availability, distribution networks and financing strategies that enhance market penetration.

- Market Entry & Expansion: Identifies growth opportunities in emerging economies driven by infrastructure development, urbanization, smart city programs and expanding rental ecosystems. It also outlines strategies for OEMs to scale operations globally through regional manufacturing hubs and after-sales service optimization.

Target Audience 2026

- Construction & Infrastructure Companies: EPC contractors, real estate developers, road construction firms and urban infrastructure agencies utilizing compact equipment for site preparation, excavation and material handling.

- Rental & Leasing Companies: Equipment rental providers expanding fleets to meet growing demand for compact, versatile machinery with high utilization rates.

- Agricultural & Landscaping Operators: Farm operators, orchard managers, landscaping firms and municipal maintenance departments using AI in IOT for multipurpose operations.

- Government & Municipal Authorities: Public works departments, urban development authorities and smart city mission teams responsible for infrastructure upgrades and maintenance.

- OEMs & Equipment Manufacturers: Global and regional construction equipment manufacturers seeking competitive intelligence, innovation benchmarking and regional expansion strategies.

- Investors & Private Equity Firms: Investment groups tracking growth in construction equipment manufacturing, rental markets and electrification of compact machinery.

- Dealers & Distribution Networks: Authorized distributors, service providers and aftermarket suppliers involved in sales, financing, spare parts and maintenance services.