Edge Data Center Infrastructure Market Overview

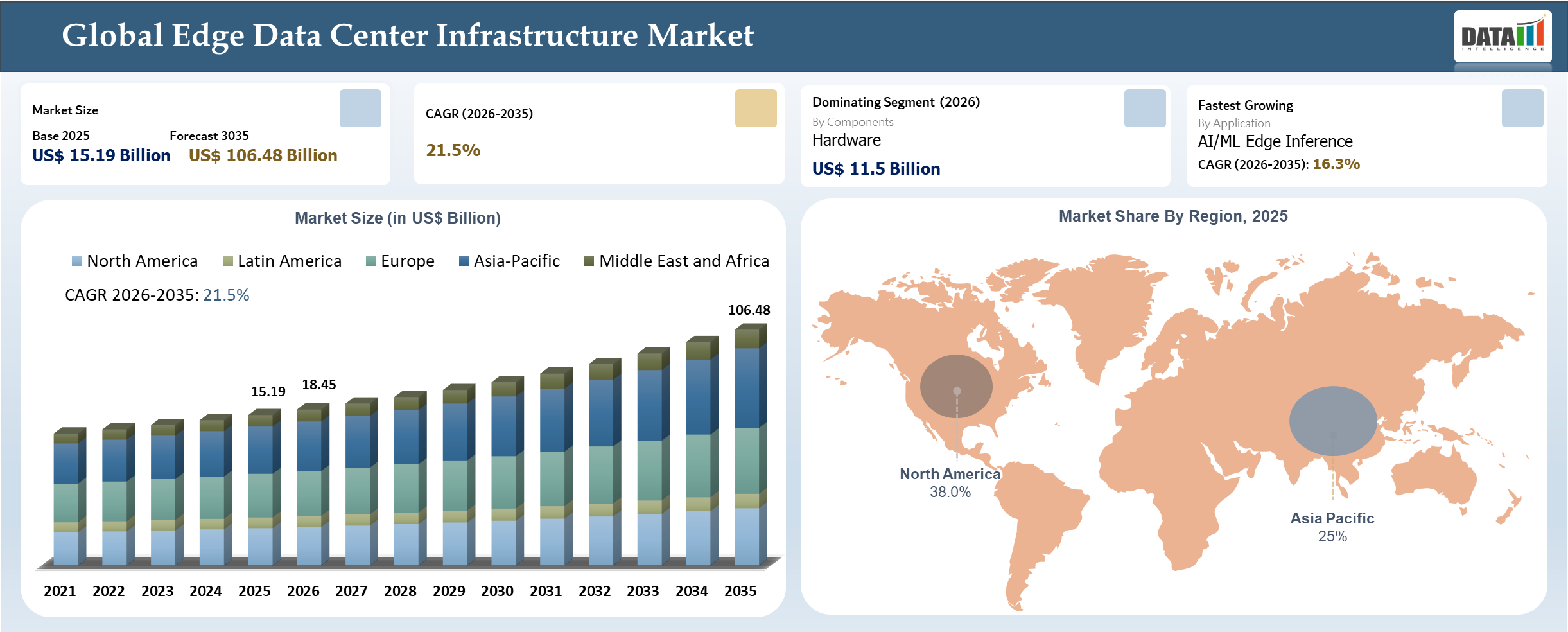

The global Edge data center infrastructure market reached US$ 15.19 billion in 2025 and is expected to reach US$ 106.48 billion by 2035, growing with a CAGR of 21.5% during the forecast period 2026-2035. The edge data center market is experiencing explosive growth in the light of the transition of firms from centralized cloud-based models to decentralized ones which provide real-time processing of data. Factors driving growth include increasing demands for low-latency operations, expanding volume of IoT data, and the emergence of 5G technologies. The degree of market consolidation is moderate, and there is activity by collocation facilities, telecommunication firms, and infrastructure providers.

The fusion of artificial intelligence (AI), edge computing, and connectivity has the power to revolutionize businesses by enabling autonomous and intelligent decision-making in sectors such as telecommunications, manufacturing, and smart cities. While infrastructure equipment currently holds a significant share in the market, edge solutions based on AI and edge-as-a-service are emerging growth areas.

Key Takeaways

- The market is expected to expand by more than US$91 billion in incremental revenue opportunity between 2025 and 2035, creating significant investment potential across infrastructure, software, and services.

- AI/ML edge inference is emerging as one of the most commercially valuable application segments due to growing demand for localized intelligence and real-time decision-making.

- Telecom operators are evolving beyond connectivity providers and increasingly positioning themselves as edge infrastructure operators through 5G-integrated deployments.

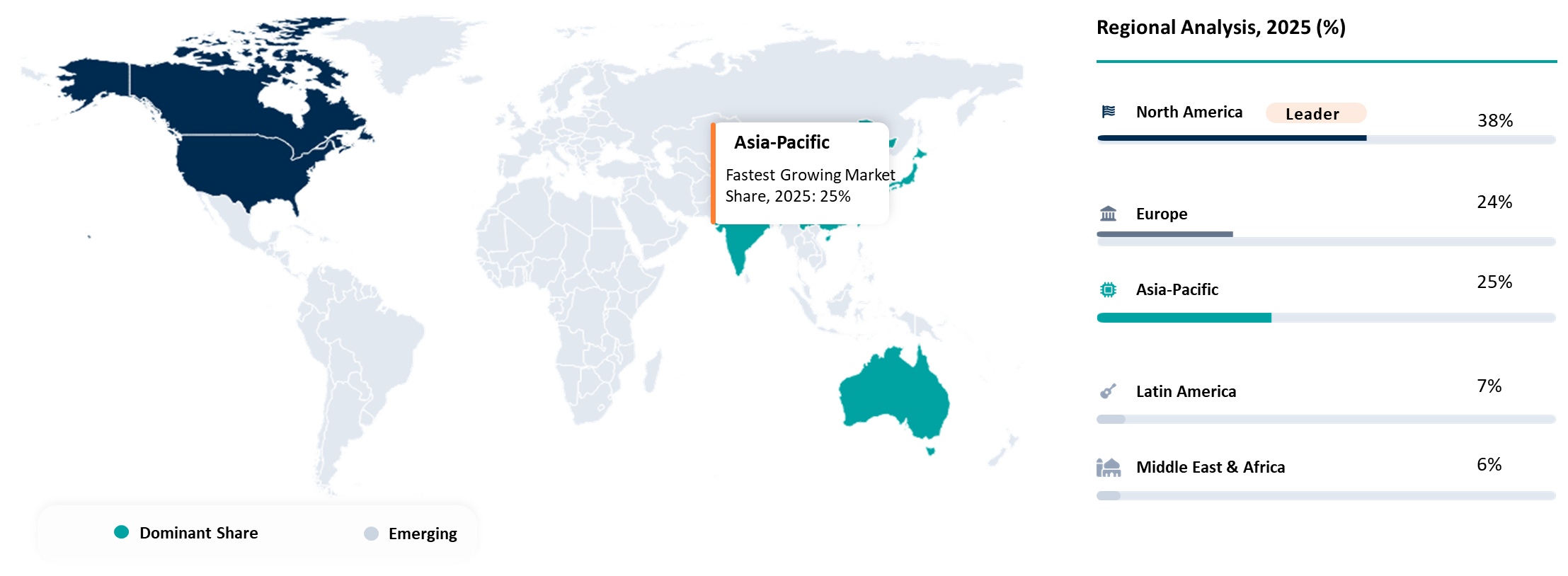

- North America maintains leadership due to hyperscale cloud presence, mature digital ecosystems, and substantial investments in distributed computing architecture.

- Asia-Pacific is projected to record the fastest expansion, supported by smart city programs, industrial digitalization initiatives, and accelerating 5G adoption.

- Modular and containerized edge facilities are becoming preferred deployment models because they reduce deployment timelines and improve scalability.

- Energy efficiency, liquid cooling technologies, renewable-powered facilities, and AI-driven infrastructure management are becoming key competitive differentiators.

Edge Data Center Infrastructure Industry Trends and Strategic Insights

- Telecom firms are in the process of becoming edge infrastructure vendors via the implementation of edge nodes in the 5G network.

- Increased use of AI/ML workloads on the edge, necessitating GPU micro data centers.

- Modular and containerized data centers are common since they can be deployed easily and scaled up.

- Hybrid approaches that entail the use of cloud computing along with edge nodes are preferred by businesses.

- Energy-efficient cooling solutions, including liquid and free cooling systems are now common.

- Edge data centers that utilize renewable energy sources have gained popularity.

Grab Exculsive Report, Request Here

Edge Data Center Infrastructure Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 15.19 Billion | |

| 2035 Projected Market Size | US$ 106.48 Billion | |

| CAGR (2026-2035) | 21.5% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Component | Hardware, Software, and Services | |

| By Deployment | On-Premises, Hybrid Edge, Colocation | |

| By Application | Content Delivery Networks (CDN) and Streaming, IoT Data Processing and Analytics, Artificial Intelligence or Machine Learning (AI/ML) Edge Inference, Smart City Infrastructure Systems, Autonomous Vehicles and V2X Communication, Augmented Reality or Virtual Reality (AR or VR) and Gaming, Industrial Automation and Predictive Maintenance, Others | |

| By End-User Industry | Information Technology (IT) and Telecom, BFSI, Healthcare and Life Sciences, Manufacturing and Industrial (Industry 4.0), Retail and E-commerce, Transportation and Logistics, Energy and Utilities, Government and Smart Cities, Media and Entertainment, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

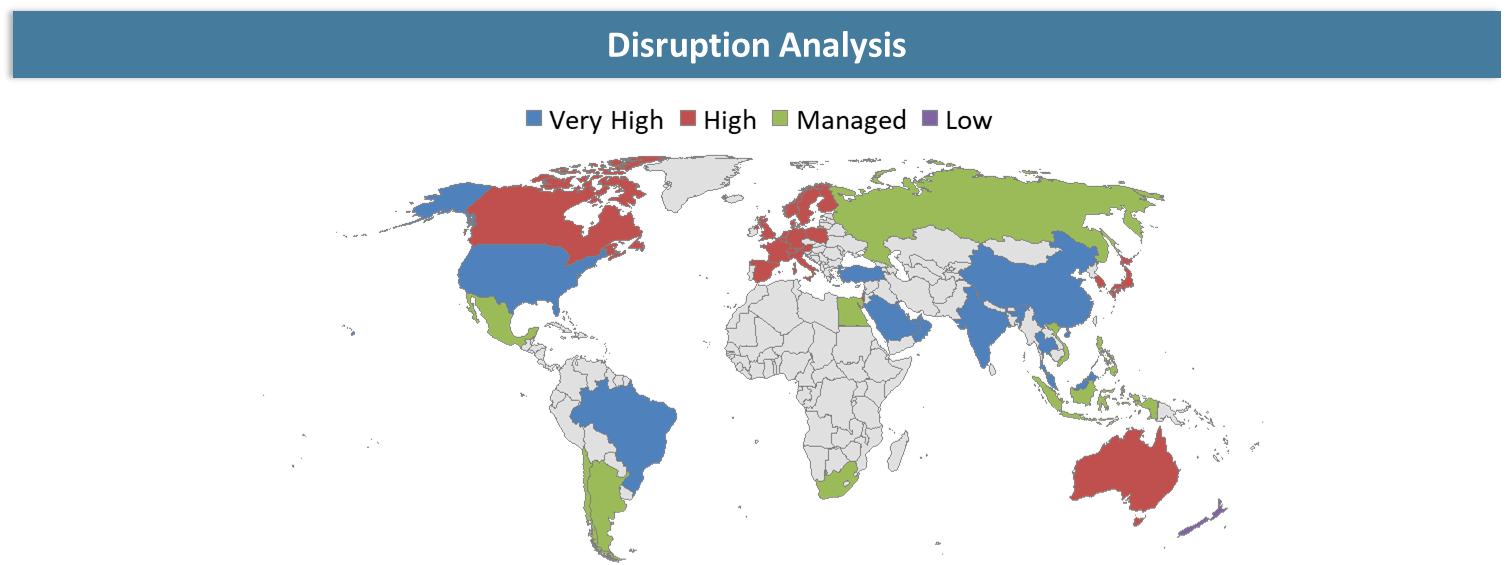

Disruption Analysis

Shift from Centralized Hyperscale Data Centers to Distributed Edge Infrastructure Transforming Digital Workloads

One significant disruptor within the edge data center infrastructure market is the shift from centralized cloud computing towards edge computing architectures. Many companies have been adopting micro and modular data centers located nearer to end-users for real-time and ultra-low-latency operations. This is causing a disturbance in traditional approaches based on hyperscale cloud-based architectures, making it necessary for companies in cloud computing and traditional data centers to adapt.

The advent of applications with low tolerance for latency like artificial intelligence, autonomous vehicles, and immersive technologies is driving this trend. In this era, localized computation takes precedence over centralized computation. Failure to adapt to these trends and offer solutions will make companies irrelevant.

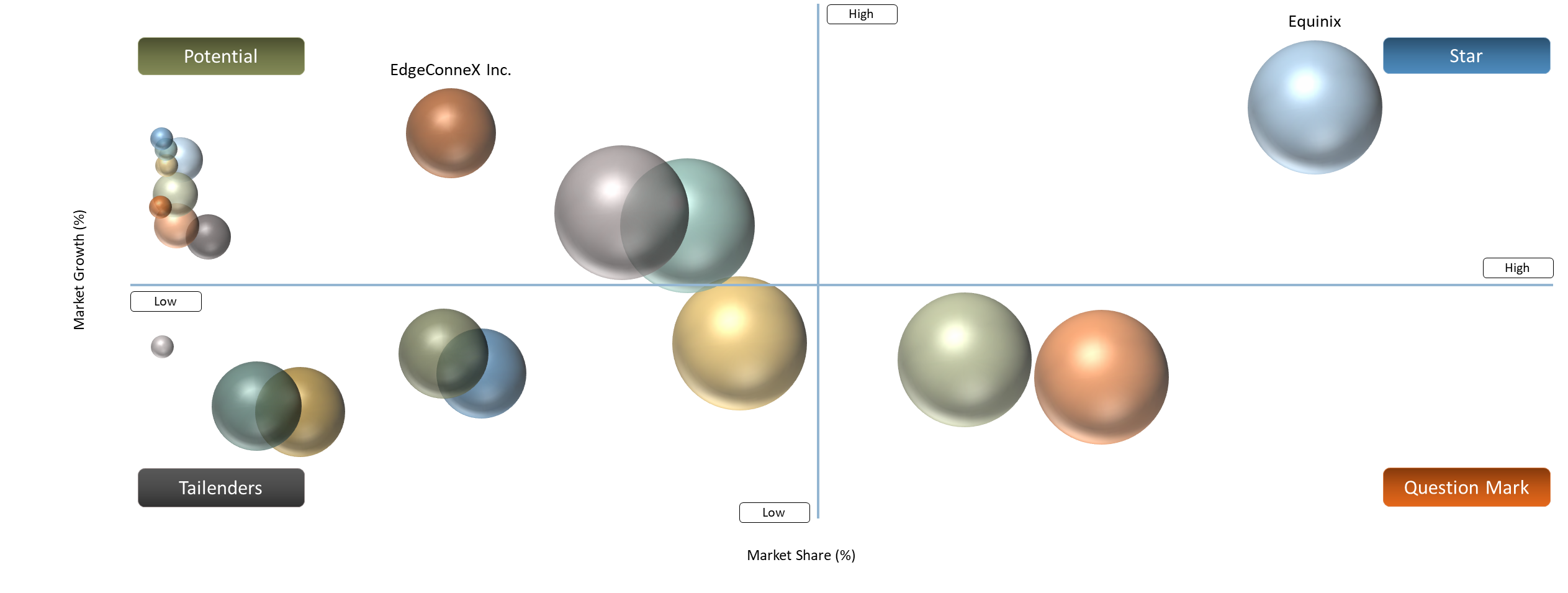

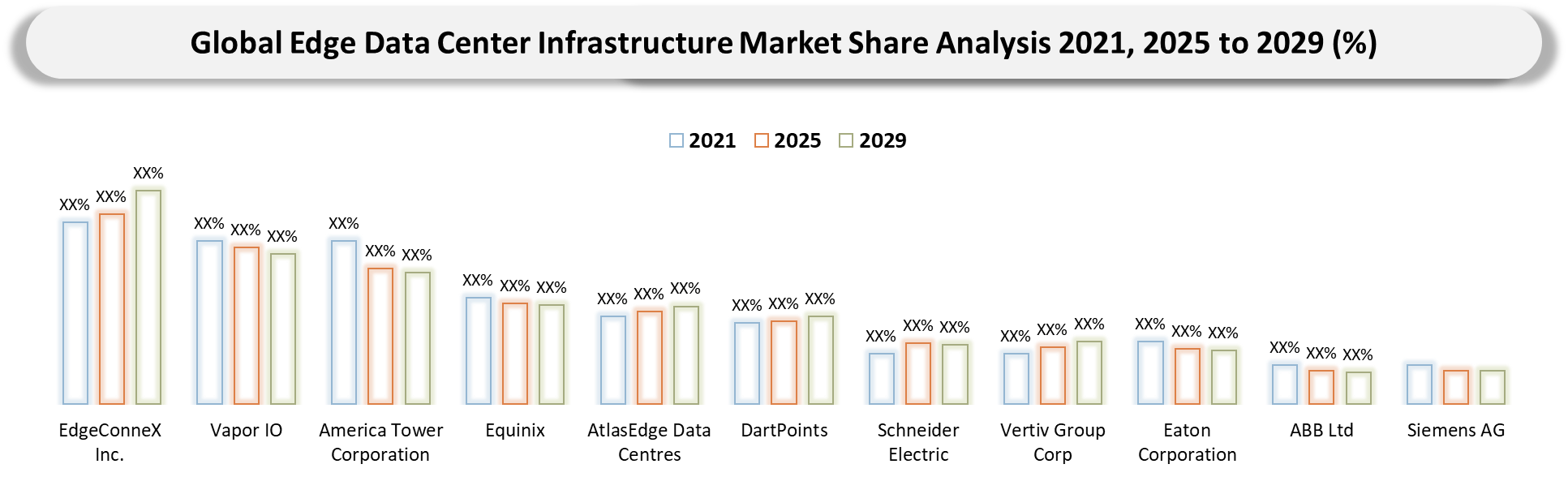

BCG Matrix: Company Evaluation

The companies that belong to the Star category include Equinix, American Tower Corporation, and Schneider Electric because of their global footprint, scalability of edge deployment, and investment in distributed infrastructure. Companies like Vertiv Group Corp and Eaton Corporation are placed in the category of Cash Cows owing to steady revenue generation and well-established positions in the power and cooling sectors

The newly rising companies including EdgeConneX Inc., Vapor IO, AtlasEdge Data Centres, and DartPoints come under the Potential category because of their high growth potential but low market penetration. Companies such as ABB Ltd and Siemens AG are categorized as Question Marks because of their significant expertise level but still growing edge footprint.

Edge Data Center Infrastructure Market Dynamics

Rising Demand for Low-Latency Computing and 5G-Enabled Applications

The growing trend towards real-time processing of data in technology solutions such as AI inference, streamlining services, and autonomous vehicles is pushing the growth of edge data centers. Companies are choosing to place their services closer to their customers so that latency can be minimized for improved performance. High-speed and low-latency 5G networks are also aiding in the same. Edge computing is being used to improve operations by companies like Siemens AG and Schneider Electric.

High Capital Investment and Deployment Complexity

The construction of edge data center infrastructure entails high capital expenditure, mainly in hardware resources such as servers, storage equipment, energy devices, and sophisticated cooling mechanisms. The use of an edge infrastructure implies that multiple distributed centers need to be built compared to a single centralized location; therefore, higher costs would accrue in relation to land acquisition, installation procedures, and connections to the network. Thus, scaling becomes difficult, especially among new players and smaller companies, even if there is considerable demand in some regions.

Besides financial barriers, the other constraint to edge implementation relates to difficulties associated with the operation of the edge infrastructure. Challenges will arise in relation to integrating the edge environment with existing IT infrastructure, maintaining performance levels, and minimizing any security threats due to the increased decentralization. Efforts by major technology companies like Cisco Systems, Inc., to develop an integrated edge platform are yet to bear fruit.

Edge Data Center Infrastructure Market Segmentation Analysis

The global Edge data center infrastructure market is segmented based on component, deployment, application, end-user and region.

AI/ML Edge Inference Emerging as the Core Value Layer Enabling Real-Time Intelligence

The inference of AI/ML edge is considered to be the fastest-growing segment of edge data center infrastructure owing to the constant increase in real-time computing demand. The key difference between cloud AI technologies is associated with local processing and analysis of information, which helps decrease computing time as well as lower the bandwidth necessary for operations. This kind of technology is particularly useful in such industries as industrial automation, security systems, and autonomous cars that need rapid machine response. Therefore, many enterprises have been implementing edge AI in their edge strategy.

On the other hand, many types of hardware, which can perform AI models on the edge, become widely used, such as GPU processors produced by NVIDIA Corporation and Intel Corporation. On top of this, edge AI starts being utilized more often in order to address specific issues, including healthcare, smart cities, and retail markets. Overall, the combination of AI and Internet-of-things technology turns out to be the trend affecting edge infrastructure.

Edge Data Center Infrastructure Market Geographical Penetration

North America Dominating Edge Data Center Infrastructure Market Through Hyperscale Presence and Advanced Digital Ecosystems

North America dominates the edge data center infrastructure market owing to the availability of hyperscalers, well-established cloud ecosystem, and early adoption of edge computing technologies. The region is also leading in implementing distributed systems for facilitating artificial intelligence (AI) inference, content distribution, and real-time analytics. Edge deployment is gaining popularity among enterprises to improve speed and efficiency for telecommunications, media, and autonomous functions.

The high investments made in 5G and digital infrastructure also contribute to North America's dominance in the edge data center infrastructure market. Some of the players investing heavily in North America include Amazon Web Services Inc. and Microsoft Corporation.

United States Edge Data Center Infrastructure Market Trends

The United States holds dominance in the regional market owing to huge investments made in edge deployment and state-of-the-art digital technology. The US is known for its innovation in AI, IoT, and cloud technologies with high adoption rates of edge technology solutions in verticals like the media industry, telecom industry, and self-driving cars.

Canada Edge Data Center Infrastructure Market Outlook

Canada is becoming a promising market driven by higher data usage, implementation of 5G networks, and digitally-driven government policies. Canada is experiencing an increased use of edge computing in the development of smart cities, healthcare, and businesses. Also, favorable policies and connectivity will provide room for scalable edge computing deployments.

Asia-Pacific Emerging as the Fastest Growing Region Driven by Digital Expansion and 5G-Led Edge Adoption

The APAC region is projected to experience exponential growth in the infrastructure for edge data centers market due to an increase in digitalization, data consumption, and massive adoption of 5G networks. Various nations in this region are experiencing a high demand for localized processing of data because of the rise in the number of IoT devices, smart cities projects, and industrial automation.

Authorities in various countries within the region are working on several digital transformation projects like smart infrastructure, industry 4.0, and intelligent transport systems. This will propel the growth of edge data centers as an important part of the next generation of digital infrastructures. There is also a continuous expansion of telecom infrastructure and increased penetration of the internet in the region.

Other factors that are fueling the growth of the market include the presence of a strong manufacturing sector and favorable costs associated with implementing hardware infrastructures. There are also various regional vendors and startups in the tech industry, which is stimulating competition in the market. In addition, the need for latency-sensitive applications will result in the rapid growth of the market.

China Edge Data Center Infrastructure Market Trends

China has taken a leading role in the Asia-Pacific edge data center infrastructure due to the deployment of 5G systems, the presence of strong governmental backing, and investments in digital infrastructure. There have been a lot of investments in edge computing in China, which have helped create smart city systems as well as improvements in manufacturing and telecommunication sectors.

China’s efforts to establish itself as a pioneer in advanced technologies have helped it invest heavily in various areas like artificial intelligence (AI), Internet of Things (IoT), and edge infrastructure. Edge deployment has been fueled by the integration of edge systems within smart cities and industrial automation processes. Furthermore, the availability of domestic tech giants and users have accelerated its growth.

India Edge Data Center Infrastructure Market Outlook

Edge data centers are becoming one of the promising markets for high growth in India, driven by digitization, data consumption, and various government initiatives such as Digital India. The increasing usage of telecommunication networks and cloud technologies is making it important for companies to adopt data centers for processing purposes.

There have been instances where various industries in India are deploying edge computing capabilities. For example, there is an increased adoption of edge data center capabilities in media, retail, and smart cities. Companies are looking to reduce latency issues and enhance the customer experience, especially when dealing with video streaming and real-time analysis.

Edge Data Center Infrastructure Market Competitive Landscape

- The three core sets of participants involved in the market include edge colocation and infrastructure providers, telecom-integrated platforms, and power and cooling solution providers. Some of the companies active within these segments include Equinix, American Tower Corporation, EdgeConneX Inc., Vapor IO, AtlasEdge Data Centres, and DartPoints. On the other hand, companies like Schneider Electric, Vertiv Group Corp, Eaton Corporation, ABB Ltd, and Siemens AG operate within the segment that provides infrastructure for powering and managing cooling of edge data centers. Competitiveness in the market is mainly driven by the ecosystems.

- Some of the key players within the market segment include EdgeConneX Inc., Vapor IO, American Tower Corporation, Equinix, AtlasEdge Data Centres, DartPoints, Schneider Electric, Vertiv Group Corp, Eaton Corporation, ABB Ltd, and Siemens AG.

Key Developments

- 2026: Equinix continued expanding its global edge footprint through new metro edge deployments and interconnection hubs to support AI and low-latency workloads.

- 2026: Schneider Electric introduced advanced modular edge data center solutions focused on energy efficiency and rapid deployment for distributed environments.

- 2026: ABB Ltd introduced its Automation Extended program, a strategic evolution of distributed control systems (DCS) designed to enable industrial modernization without operational disruption.

- 2026: American Tower Corporation expanded its edge data center strategy by integrating edge nodes into its telecom tower infrastructure to support 5G applications.

- 2025: Vertiv Group Corp announced the acquisition of Great Lakes Data Racks & Cabinets for ~$200 million to strengthen its AI-ready and edge infrastructure portfolio.

- 2025: Vertiv Group Corp acquired Waylay NV to integrate AI-driven software into data center power and cooling systems, enhancing automation and efficiency.

- 2025: EdgeConneX Inc. expanded hyperscale-to-edge data center deployments across key global markets to support cloud and content delivery demand.

- 2024: Vertiv Group Corp launched the SmartRow 2 edge data center system, reducing deployment time and improving operational efficiency.

Why Choose DataM?

Technological Innovations: Explores the latest advancements in edge data center infrastructure, including modular and prefabricated designs, AI-enabled edge management, liquid cooling systems, and integration with 5G networks that enable low-latency, high-performance computing across distributed environments.

Infrastructure Performance & Market Positioning: Evaluates how different providers perform across edge deployments such as micro data centers, colocation edge, and on-premise installations. The analysis compares scalability, energy efficiency, deployment speed, reliability, and integration capabilities, highlighting how leading players differentiate globally.

Real-World Evidence: Highlights practical use cases across content delivery networks, AI/ML inference, smart cities, and industrial automation. It demonstrates measurable benefits such as reduced latency, improved data processing efficiency, optimized bandwidth usage, and enhanced user experience.

Market Updates & Industry Changes: Tracks key developments including new edge deployments, expansion of edge zones, partnerships between telecom operators and cloud providers, and advancements in energy-efficient infrastructure across major regions like North America, APAC, China, and India.

Competitive Strategies: Analyzes how key players such as Equinix, Schneider Electric, and Vertiv Group Corp are expanding through modular solutions, strategic partnerships, and edge ecosystem integration.

Cost Structures & Market Access: Explains cost components including hardware, deployment, and operational expenses, along with colocation and edge-as-a-service models. It also reviews regional accessibility, site selection strategies, and infrastructure scalability.

Market Entry & Expansion: Identifies growth opportunities driven by 5G rollout, AI adoption, and increasing data localization requirements. It outlines strategies for companies to expand through regional edge deployments, partnerships with telecom providers, and scalable infrastructure models.

Target Audience 2026

• Telecom Operators & Network Providers: Companies deploying 5G networks and integrating edge infrastructure to enable low-latency connectivity and real-time data processing.

• Cloud Service Providers & Hyperscalers: Organizations such as Amazon Web Services and Microsoft Corporation expanding edge zones and hybrid cloud capabilities.

• Colocation & Data Center Providers: Firms like Equinix and EdgeConneX Inc. focusing on distributed edge deployments and interconnection services.

• Enterprises Across Industries: Manufacturing, media, healthcare, retail, and logistics companies leveraging edge infrastructure for AI/ML, IoT, and real-time analytics applications.

• Government & Smart City Authorities: Public sector organizations investing in smart infrastructure, surveillance, and digital services requiring localized data processing.

• Infrastructure & Technology Providers: Companies such as Schneider Electric, Vertiv Group Corp, and Eaton Corporation supplying power, cooling, and modular solutions.

• Investors & Private Equity Firms: Stakeholders tracking growth opportunities in edge computing, 5G infrastructure, and AI-driven data center expansion.

• System Integrators & Managed Service Providers: Firms enabling deployment, integration, and lifecycle management of edge data center solutions across enterprise environments.A