Global Edge AI Chip Market Overview

The global Edge AI chips market is rapidly expanding, driven by the rising need for on-device AI processing in sectors such as autonomous vehicles, IoT, industrial automation, and smart healthcare. By enabling real-time computation, these chips reduce latency, enhance data privacy, and improve energy efficiency. Technological advancements, coupled with supportive government policies particularly in the Asia-Pacific region are further accelerating adoption, positioning edge AI chips as a key component of next-generation intelligent systems.

Edge AI Chip Industry Trends and Strategic Insights

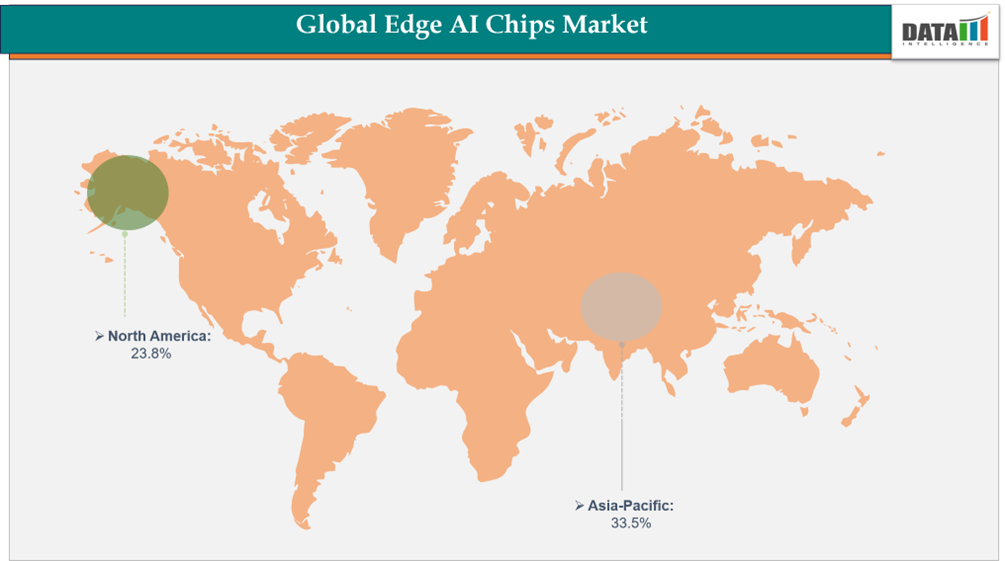

- Asia-Pacific dominates the edge AI chip market, capturing the largest revenue share of 33.5% in 2024.

- By end-user, the consumer electronics segment is projected to be the largest market, holding a significant share of 22.4% in 2024.

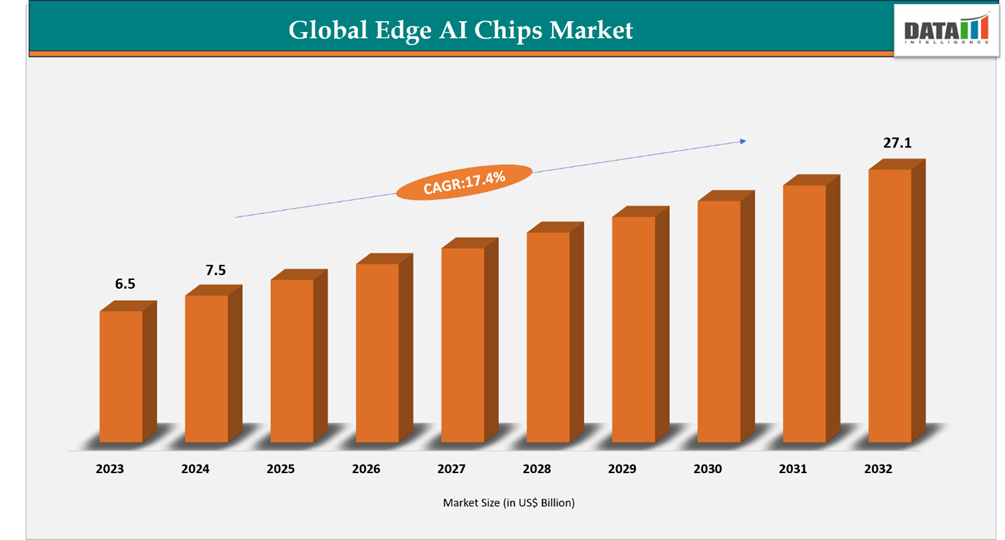

Edge AI Chip Market Size and Future Outlook

- 2025 Market Size: US$ 8.80 billion

- 2033 Projected Market Size: US$ 31.75 billion

- CAGR (2026-2033): 17.4%

- Largest Market: Asia-Pacific

- Fastest Market: North America

Key Takeaways

- Asia-Pacific continues to dominate Edge AI chip manufacturing and deployment, driven by strong semiconductor ecosystems in Taiwan, South Korea, and China. The region benefits from large-scale electronics production, rapid 5G penetration, and aggressive national AI semiconductor strategies, particularly in China where domestic chip self-sufficiency policies are accelerating edge AI accelerator adoption across surveillance, consumer devices, and industrial IoT.

- North America remains the innovation and architecture leadership hub for Edge AI chips. The U.S. is driving demand through hyperscale AI ecosystems, on-device generative AI integration in smartphones and PCs, and automotive AI compute platforms. Companies are shifting from cloud-first AI toward hybrid inference models where latency-sensitive workloads are processed at the edge using NPUs, TPUs, and custom silicon.

- A major structural shift is underway from cloud-centric AI to distributed inference at the edge. AI workloads are increasingly being executed directly on devices such as smartphones, cameras, vehicles, drones, and industrial sensors to reduce latency, bandwidth costs, and privacy risks. This is accelerating demand for low-power, high-efficiency neural processing units (NPUs) embedded in SoCs.

- The smartphone industry has become the primary scaling engine for Edge AI chips. Flagship devices from Apple, Qualcomm-powered Android OEMs, and MediaTek-based ecosystems are integrating dedicated AI accelerators for real-time translation, image generation, voice assistants, and multimodal AI processing directly on-device without cloud dependency.

- Automotive applications are emerging as a high-value growth frontier. Advanced driver-assistance systems (ADAS), in-cabin monitoring, and autonomous driving stacks increasingly rely on edge AI compute to process sensor fusion data in real time. This is driving demand for automotive-grade AI accelerators with strict power, thermal, and safety certifications.

- Industrial and IoT deployment is expanding rapidly, particularly in smart manufacturing, predictive maintenance, and video analytics. Edge AI chips are enabling real-time decision-making in environments where cloud connectivity is limited, expensive, or too slow for mission-critical operations.

- The competitive landscape is shifting from general-purpose GPUs toward specialized edge AI accelerators. Companies like NVIDIA, Qualcomm, Apple, Intel, Google (Edge TPU), and emerging pure-play startups such as Hailo and Kneron are competing on power efficiency, inference speed, and software ecosystem integration rather than raw compute alone.

- Geopolitical semiconductor fragmentation is reshaping supply chains. The U.S., China, and EU are all investing heavily in domestic chip design and packaging capabilities, leading to parallel ecosystems for AI silicon. This is accelerating regional diversification but also increasing cost and duplication of R&D efforts

Edge AI Chip Market Scope

| Metrics | Details |

| By Chip Type | CPU, GPU, NPU, ASIC, Others |

| By Function | Inference, Training |

| By End-User | Consumer electronics, Automotive, Healthcare, Retail & e-commerce, Manufacturing, Telecommunications, Others |

| By Region | North America, South America, Europe, Asia-Pacific, Middle East and Africa |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth |

Edge AI Chip Market Dynamics

Growth of IoT and Connected Devices

The surge in IoT and connected devices is driving demand for Edge AI chips. From smart wearables and home appliances to industrial sensors and autonomous vehicles, the growing volume of edge-generated data requires on-device processing to reduce latency, enhance privacy, and limit reliance on cloud infrastructure.In March 2025, Illustrating this trend, at Embedded World in Germany, Qualcomm announced plans to acquire Edge Impulse to strengthen its developer platform and solidify its position in the IoT AI space. Such initiatives underscore the critical role of edge AI chips in enabling intelligent, connected devices across automotive, healthcare, industrial, and consumer applications.

Power Consumption and Thermal Management

Managing power consumption and thermal performance remains a key challenge for the Edge AI chips market. Edge devices like wearables, smart cameras, and autonomous sensors often have compact designs with limited battery life and minimal cooling, making high-performance AI processing prone to heat buildup, which can impact reliability and longevity. Nevertheless, innovations in energy-efficient chip designs, optimized NPUs, and advanced thermal management are helping to overcome these limitations. Techniques such as model quantization and pruning further enable efficient on-device AI inference without compromising accuracy, supporting continued market growth despite these constraints.

Edge AI Chip Market Segment Analysis

The global edge AI chip market is segmented based on chip type, function, end-user and region.

Rising Demand for Smart Devices in Consumer Electronics Fuels Segment Growth

The consumer electronics segment is a key driver of the Edge AI chips market, propelled by the rising adoption of smart devices such as smartphones, wearables, smart cameras, and home assistants. These devices increasingly depend on on-device AI processing to deliver features like voice recognition, image analysis, health tracking, and real-time personalization, which require low latency and energy-efficient performance. For instance, In August 2024, Amazon acquired Edge chip and AI model compression company Perceive in an US$ 80 Billion deal, aiming to strengthen AI capabilities in its consumer devices. This move underscores the growing importance of edge AI chips in enabling responsive, privacy-conscious, and intelligent electronics.

With the rapid expansion of connected IoT ecosystems, the demand for smarter devices continues to rise. Manufacturers are focusing on compact, energy-efficient chips capable of performing advanced computations without draining battery life. Moreover, the increasing emphasis on personalized, context-aware AI experiences is driving the integration of sophisticated AI directly into devices, reducing reliance on cloud processing and further accelerating market growth.

Rising Adoption of Connected and Autonomous Vehicles Drives Demand in Automotive End-User Segment

The automotive segment is a key driver of the Edge AI chips market, fueled by the rising adoption of connected, smart, and autonomous vehicles (SDVs). Edge AI chips play a vital role in vehicles by supporting advanced driver-assistance systems (ADAS), in-vehicle infotainment, predictive maintenance, and real-time safety monitoring, where on-device AI processing ensures low latency and high reliability.

For Instance, In January 2025, NXP strengthened its automotive portfolio through the acquisition of TTTech Auto, a leading software provider specializing in systems, safety, and security for SDVs. TTTech Auto complements and enhances the NXP CoreRide platform, helping automakers reduce system complexity, improve performance, and accelerate time-to-market. This move reflects NXP’s strategic goal to become a leader in intelligent edge systems for automotive and Industrial IoT, emphasizing the growing importance of edge AI chips in next-generation vehicles.

With the increasing focus on autonomous, connected, and intelligent vehicles, automakers are investing in high-performance, energy-efficient edge AI chips capable of handling complex computations locally. The demand for real-time decision-making, enhanced safety, and system optimization continues to fuel the automotive segment, establishing it as a major contributor to overall market growth.

Why Edge AI Chip Market Matters in 2026

The global semiconductor and AI computing landscape is undergoing a major transformation, driven by the rapid shift from cloud-only processing to real-time, on-device intelligence.

Edge AI chips are enabling ultra-low latency decision-making by processing data locally on devices, reducing dependency on centralized cloud infrastructure, improving privacy, and significantly enhancing energy efficiency across applications.

Several macroeconomic and technological factors are driving market growth:

- Explosive growth in IoT-connected devices across industries

- Expansion of 5G and emerging 6G connectivity infrastructure

- Increasing adoption of autonomous systems and robotics

- Growing need for data privacy and on-device processing

- AI model optimization for low-power semiconductor architectures

- Rapid deployment of smart cities and intelligent infrastructure

- Surge in edge-enabled healthcare, industrial automation, and automotive AI

- Semiconductor miniaturization and advanced chip design innovations

Analyst View

DataM Intelligence Analyst Perspective

The edge AI chip market is transitioning from early-stage adoption to large-scale commercial integration, becoming a foundational layer of the global AI infrastructure ecosystem.

The long-term success of the edge AI chip market will depend on:

• Advancements in low-power AI semiconductor architectures

• Cost-efficient chip manufacturing and supply chain resilience

• Integration of AI accelerators into mainstream consumer devices

• Strong ecosystem development between chipmakers, OEMs, and AI platforms

• Data security and privacy compliance requirements

• Expansion of edge computing infrastructure globally

• Performance optimization for real-time inference workloads

The United States continues to lead in AI chip design and innovation, while Taiwan and South Korea dominate semiconductor manufacturing. China is rapidly scaling domestic AI chip capabilities, while India is emerging as a strategic hub for semiconductor design, AI startups, and edge computing adoption driven by digital infrastructure growth.

Edge AI Chip Market Geographical Penetration

Rising Adoption of Edge AI Solutions in Asia-Pacific

The Asia-Pacific Edge AI chips market is the largest globally, representing around 33.5% of the total market in 2024, fueled by rapid industrialization, widespread IoT deployment, and growing demand from smart electronics and automotive sectors. China leads the region in production, supported by its robust semiconductor manufacturing ecosystem and government initiatives promoting AI and chip development. Japan and South Korea, despite smaller volumes, dominate the high-value segment with advanced chip design capabilities, serving industries such as autonomous vehicles, consumer electronics, and industrial automation.

For instance, In July 2025, SAC Group, a member of WPG Holdings, partnered with Axelera AI to expand into the Edge AI market and establish a new framework for smart applications. This collaboration underscores the increasing focus on innovation and strategic partnerships to accelerate the deployment of edge AI technologies across diverse applications in the region.

India Edge AI Chip Market Outlook

India's Edge AI Chip market is witnessing rapid growth, driven by expanding technology and industrial sectors and government initiatives supporting domestic semiconductor and AI development. Increasing adoption of AI-driven solutions across data centers, cloud platforms, automotive, and smart devices has significantly boosted the demand for edge AI chips. The growth of digital infrastructure, enterprise AI applications, industrial automation, and IoT deployment is further fueling the need for high-performance, low-latency edge computing solutions.

For instance, In October 2024, Indian companies are placing large-scale orders for Nvidia chips, with Tata Communications, Reliance Industries, and Yotta Data Services acquiring Nvidia H100s to strengthen their AI processing and edge computing capabilities. These strategic investments emphasize India’s push toward developing robust edge AI ecosystems and enhancing technological self-reliance.

China Edge AI Chip Market Trends

China's Edge AI Chips market outlook remains highly positive, as the country continues to be the dominant player. Leading Chinese companies such as Huawei, Horizon Robotics, and Cambricon are expanding production and R&D to meet the rising demand for cost-effective and high-performance edge AI solutions. At the same time, global firms including Nvidia, Intel, and Qualcomm maintain a strong presence in China through local subsidiaries, partnerships, and collaborations to cater to enterprise, automotive, and consumer electronics sectors. Japanese and South Korean firms also continue to serve the high-value premium segment, leveraging advanced chip design and manufacturing expertise.

Presence of Advanced Industrial and AI Infrastructure in North America

North America is projected to be a key region in the global Edge AI Chips market, accounting for around 23.8% of the market in 2024. The region’s growth is driven by strong demand from sectors such as automotive, aerospace, industrial automation, and manufacturing. With advanced industrial infrastructure, a mature semiconductor ecosystem, and a robust AI and IoT technology base, North America ensures consistent adoption of edge AI chips for diverse high-performance applications.

Although alternative AI computing architectures are emerging, edge AI chips remain essential for low-latency, energy-efficient, on-device processing. The region’s strong presence of chipmakers, technology innovators, and end-user industries reinforces its position as a major market for edge AI solutions.

Supporting this trend, in February 2025, NXP Semiconductors announced its acquisition of US edge AI chipmaker Kinara for $307 Billion. Kinara, known for its energy-efficient neural processing units (NPUs), will have its edge NPUs and AI software integrated into NXP’s industrial and IoT processors. Both companies focus on IoT and AI systems for industrial and automotive applications, with the deal expected to close in the first half of 2025, underscoring North America’s strategic importance in advancing edge AI technology..

US Edge AI Chip Market Insights

The US holds the largest share of the North America Edge AI Chips market, driven by strong demand from the automotive, aerospace, and industrial technology sectors. The automotive industry, producing Billions of connected and autonomous vehicles, relies on edge AI chips for real-time data processing, ADAS, and in-vehicle intelligence. Likewise, the aerospace sector is increasingly deploying edge AI for predictive maintenance, avionics, and mission-critical applications. Investments in industrial IoT and smart manufacturing further support consistent demand for high-performance, energy-efficient edge AI chips. While alternative computing solutions are emerging, edge AI chips remain essential due to their on-device processing, low latency, and adaptability across diverse applications.

Canada Edge AI Chip Industry Growth

In Canada, the Edge AI Chips market is smaller than in the US but remains important, supported by the country’s technology-driven industries, aerospace cluster, and expanding data center infrastructure. Major aerospace companies like Bombardier and Pratt & Whitney Canada are increasingly leveraging edge AI for operational efficiency and real-time monitoring. Industries such as mining, energy, and advanced manufacturing are also adopting edge AI for automation and predictive analytics. With a growing focus on AI research, industrial IoT, and smart manufacturing, demand for edge AI chips in Canada is expected to rise steadily, though at a slightly slower pace compared to the US.

Technology Analysis

The Edge AI Chips market is being shaped by innovations in energy-efficient computing, AI accelerators, and TinyML technologies, which enable real-time, on-device intelligence across applications such as automotive, industrial automation, consumer electronics, and healthcare. Modern edge AI chips emphasize low latency, high performance, and seamless integration with IoT and smart devices.

For instance, on June 17, 2025, Nordic Semiconductor announced the acquisition of Neuton.AI’s intellectual property and core technology, a leader in fully automated TinyML solutions for edge devices. By combining Nordic’s ultra-low-power nRF54 Series SoCs with Neuton’s neural network framework, the partnership brings scalable, high-performance AI to even the most resource-constrained edge devices, showcasing the fast-paced technological advancements in the market.

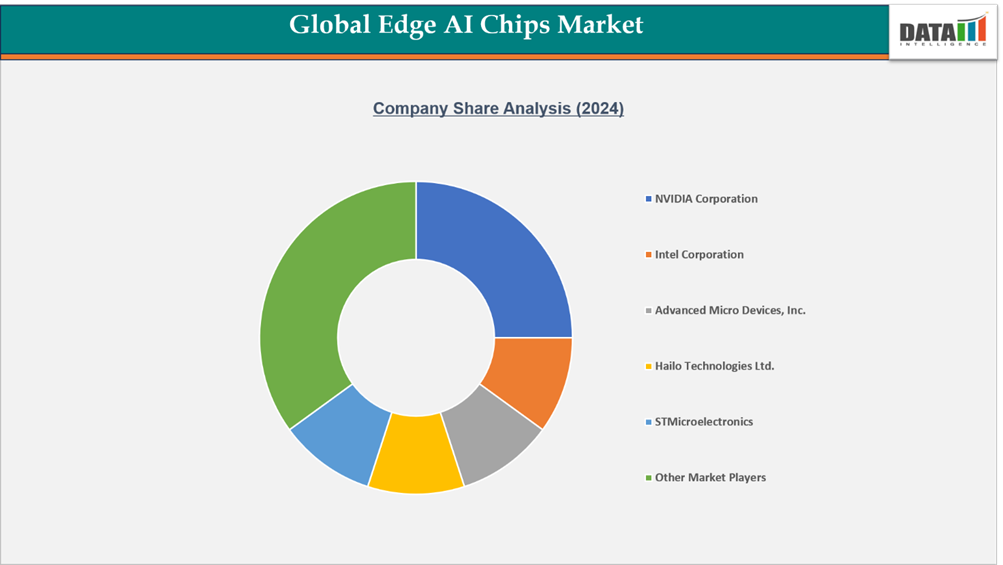

Edge AI Chip Market Competitive Landscape

- The global Edge AI Chips market is characterized by a competitive landscape comprising both established semiconductor giants and innovative AI hardware startups.

- Key players include NVIDIA Corporation, Intel Corporation, Advanced Micro Devices, Inc., Hailo Technologies Ltd., STMicroelectronics, Texas Instruments Incorporated, Mythic, Qualcomm Technologies, Inc, Samsung, MediaTek.

- These companies focus on product differentiation by offering high-performance, energy-efficient chips with advanced AI accelerators, low-latency processing, and on-device intelligence suitable for applications in automotive, industrial, and consumer electronics.

- Strategic investments in R&D, AI model optimization, energy-efficient architectures, and software-hardware integration are critical, as the industry faces competition from alternative AI computing solutions and emerging edge-focused architectures.

Key Developments

- In May 2026, NVIDIA Corporation expanded its Edge AI ecosystem by strengthening collaborations with global automotive OEMs and robotics firms, enhancing real-time inference capabilities for autonomous machines and industrial edge deployments using next-generation Jetson platforms.

- In April 2026, Qualcomm Technologies Inc. announced advancements in its Edge AI chip portfolio, integrating upgraded neural processing units (NPUs) designed for ultra-low power performance in smartphones, smart cameras, and IoT edge devices, accelerating on-device generative AI adoption.

- In March 2026, Intel Corporation scaled its Edge AI strategy through enhancements in the Intel Movidius and Xeon edge platforms, enabling higher-performance AI inference for smart manufacturing, healthcare imaging, and retail analytics applications across distributed networks.

- In February 2026, MediaTek Inc. introduced new edge AI chipset solutions targeting consumer electronics and smart home ecosystems, with improved AI acceleration for voice recognition, vision processing, and real-time translation features integrated into connected devices.

- In January 2026, Hailo Technologies and SiMa.ai reported increased deployment of their dedicated edge AI accelerators across surveillance, industrial automation, and smart city infrastructure projects, focusing on high-efficiency AI processing at the edge with reduced cloud dependency.

- In September 2025, Grinn, a leader in advanced IoT and embedded systems, has formed a strategic partnership with MediaTek to drive the development of AI-powered edge solutions.

- In July 2025, Blaize secures a $120 Billion deal to expand the deployment of edge AI chips in Asia.

Edge AI Chip Market Investment & Funding Analysis

Global investments in Edge AI chip technologies are accelerating rapidly, driven by the expansion of real-time computing, IoT ecosystems, and on-device AI processing demand.

Major funding areas include:

- Edge AI processor development (NPU, ASIC, FPGA)

- Low-power semiconductor design

- AI inference optimization hardware

- IoT and embedded AI chipsets

- 5G + edge computing integration

- Smart device semiconductor ecosystems

Strategic Recommendations

For Semiconductor Manufacturers

- Accelerate development of low-power AI chip architectures

- Integrate edge AI capabilities into next-gen SoCs

- Strengthen partnerships with cloud and AI software providers

- Expand fabrication capabilities for advanced nodes

For Investors

- Focus on scalable edge AI semiconductor platforms

- Track innovations in AI inference and on-device processing

- Evaluate long-term demand from IoT, automotive, and industrial AI

- Monitor geopolitical and supply chain semiconductor risks

For Governments

- Support domestic semiconductor manufacturing initiatives

- Invest in AI + edge computing research ecosystems

- Strengthen chip design and fabrication incentives

- Develop AI hardware standardization frameworks

Why Buy This Edge AI Chip Market Report?

This report helps organizations:

- Understand next-generation edge computing trends

- Identify high-growth semiconductor investment opportunities

- Benchmark leading chipmakers and emerging startups

- Analyze AI hardware adoption across industries

- Optimize technology and market entry strategies

- Evaluate competitive positioning in the AI semiconductor space

- Assess global supply chain and fabrication dynamics

- Track innovation in AI inference and edge intelligence

What’s Included in the Edge AI Chip Market Report?

The report provides:

- Market size & forecast analysis

- Regional demand and growth outlook

- Competitive landscape and benchmarking

- Technology segmentation (ASIC, GPU, FPGA, NPU)

- Pricing and cost structure analysis

- Supply chain and manufacturing insights

- Regulatory and trade environment assessment

- Investment and funding landscape

- Patent and innovation tracking

- Strategic recommendations

- Emerging application trends (automotive, IoT, robotics, healthcare)

- Company profiling and ecosystem mapping

Who Should Buy This Report?

This Edge AI Chip Market report is ideal for:

- Semiconductor manufacturers

- AI chip startups

- Cloud computing companies

- Automotive OEMs and EV manufacturers

- Venture capital and private equity firms

- Technology investors

- IoT solution providers

- Industrial automation companies

- Defense and aerospace technology firms

- Government and policy agencies

- Market intelligence and strategy teams

Key Benefits for Stakeholders

Gain actionable intelligence to:

- Understand the future of edge AI computing

- Identify disruptive semiconductor innovations

- Evaluate global AI hardware adoption trends

- Discover high-growth investment opportunities

- Benchmark leading chipmakers and competitors

- Improve strategic planning and R&D direction

- Strengthen supply chain and sourcing decisions

- Anticipate shifts in AI-driven hardware demand

Target Audience 2025

- Manufacturers/ Buyers

- Industry Investors/Investment Bankers

- Research Professionals

- Emerging Companies