Multi Cancer Early Detection Market Overview

The market is making tremendous progress due to the rising requirement for non-invasive cancer screening, increasing awareness about preventative oncology, and the increasing need for early-stage detection of cancer when symptoms do not arise yet. The significance of multi-cancer detection tests is increasing since such tests allow one to screen for several cancer types using a single sample of blood.

The market growth is propelled by advancements in liquid biopsy, cancer genomics, and precision medicine diagnostic techniques that allow detection of early-stage cancers with increased sensitivity and specificity. Techniques like DNA methylation profiling, fragmentomics, proteomics, and multiomics have become more effective in detecting cancer signals for a broad array of tumors. Concurrently, there are also advances in artificial intelligence and machine learning in analyzing biological data to improve diagnostics and predict tissues of origin.

The market is also gaining advantages from growing clinical validation efforts, expanding diagnostic collaborations, and rising attention from healthcare organizations that are looking for solutions that can provide scalable preventive screening opportunities. With a greater emphasis on early intervention and personalized treatment paths in health care facilities, MCED platforms are proving to be an integral part of oncology diagnostics approaches in the future. Innovation in blood testing techniques, integration with laboratory processes, and biomarker research can help drive the early cancer screening market growth and oncology diagnostics market trends.

AI Impact Analysis

AI is playing an increasingly pivotal role in the development of the global MCED market through enhanced identification of subtle and complex signals associated with cancer from liquid biopsies. More frequently, AI techniques are being deployed to interpret methylation, fragmentomics, and multiomics data in order to support the identification of early-stage cancers characterized by the presence of subtle signals. For instance, GRAIL, Inc has applied machine learning algorithms to detect cancer signals as well as determine tissue origins based on methylation techniques. On the other hand, Freenome Holdings, Inc. has been focusing on scaling up its deep learning algorithms to analyze fragment-level and multiomics data to achieve higher levels of accuracy in early detection.

Additionally, AI enhances the business case for MCED tests in terms of improving diagnostic accuracy, facilitating the interpretation of vast genomic datasets, and allowing for more personalized testing. However, the application of AI in MCED tests also increases the requirements for validation, explanation, and regulation due to the need for health care providers and payers to have faith in the reliability, repeatability, and usefulness of AI-driven test outputs.

Key Takeaways

- Liquid biopsy technology-based screening platforms will be the most promising commercial opportunity, with consumers favoring scalable blood tests capable of integration within an oncological prevention strategy.

- Clinical validation strength is set to become the key differentiator, with healthcare providers favoring test providers with a capability to provide high sensitivity, accurate tissue of origin, and seamless integration with current screening strategies.

- The North American market continues to be the benchmark when developing the commercialization strategy, regulation pathway, reimbursement dialogue, and partnership approach within the MCED space.

- There is continued white space within the un-screened cancers, providing a robust market pull for novel MCEDs to provide solutions for unserved diagnosis requirements.

- Going forward, test providers with the ability to integrate genomic cancer diagnostics into clinical workflows are poised to be the winners in the future MCED marketspace.

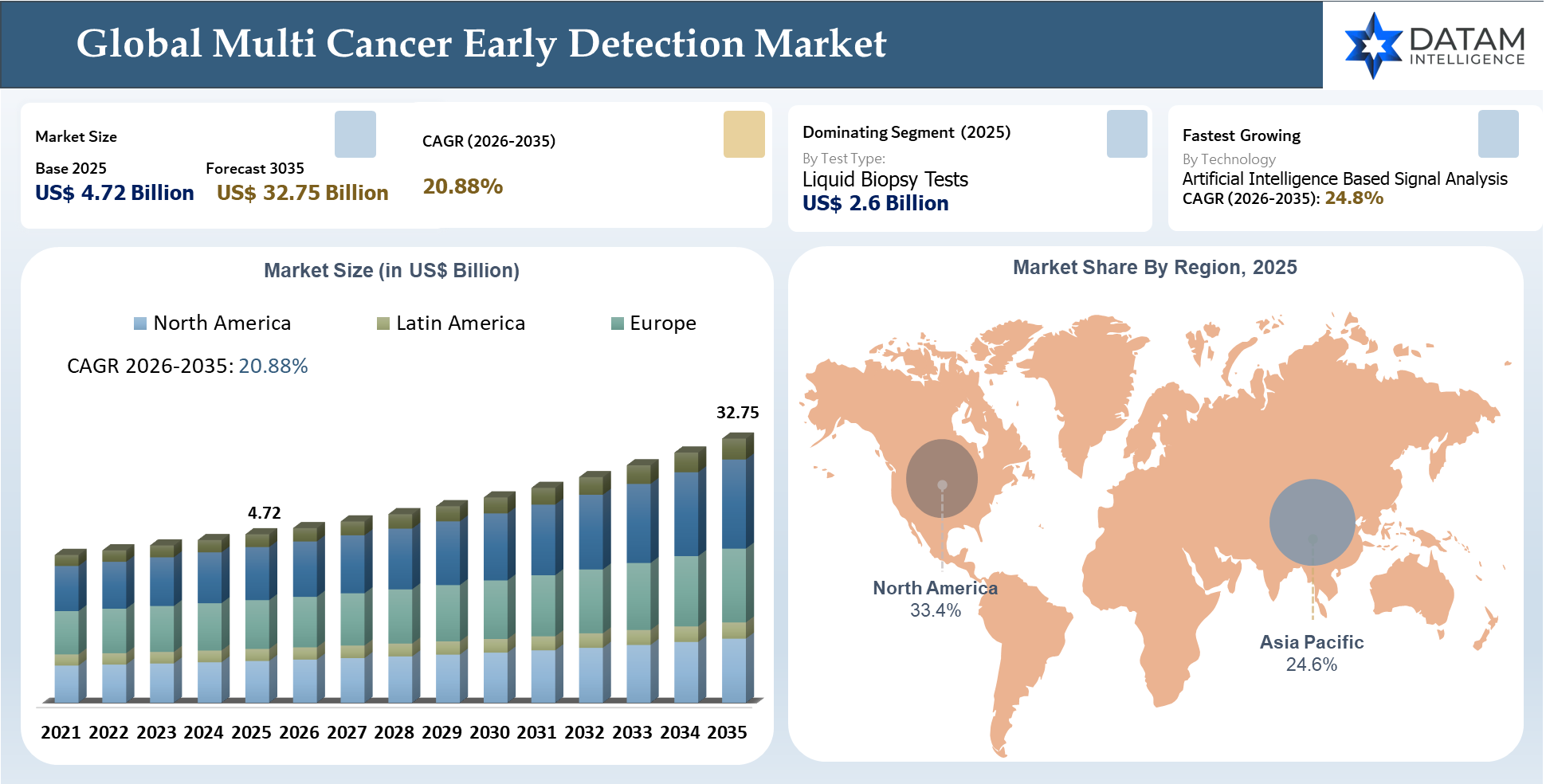

Multi Cancer Early Detection Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 4.72 Billion | |

| 2035 Projected Market Size | US$ 32.75 Billion | |

| CAGR (2026-2035) | 20.88% | |

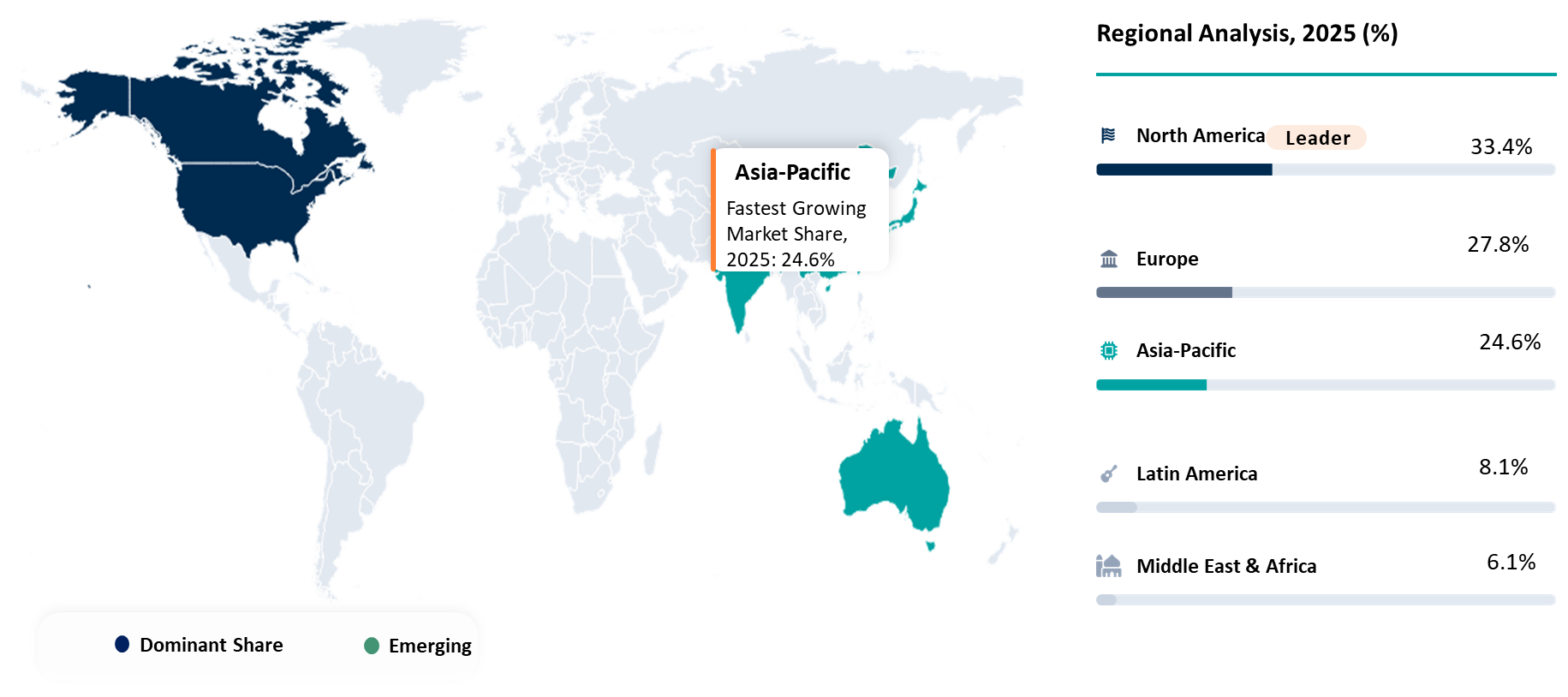

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Test Type | Liquid Biopsy Tests, Gene Panels, DNA Methylation Tests, Multi-omics Assays, Proteomic Biomarker Tests, Laboratory Developed Tests (LDTs), Circulating Tumor DNA Tests, Circulating Tumor Cell Tests, and Others. | |

| By Technology | DNA Methylation Analysis, Next Generation Sequencing, Targeted Sequencing, Fragmentomics, Epigenomics, Proteomics, Transcriptomics, Artificial Intelligence Based Signal Analysis, Machine Learning Pattern Recognition, and Bioinformatics Algorithms. | |

| By Sample Type | Blood, Plasma, Serum, Saliva or Buccal Swab, Urine, Tissue, Cerebrospinal Fluid, and Others. | |

| By Cancer Type | Breast Cancer, Lung Cancer, Colorectal Cancer, Prostate Cancer, Liver Cancer, Ovarian Cancer, Pancreatic Cancer, Gastric Cancer, Blood Cancer, and Others. | |

| By End-User | Hospitals and Clinics, Diagnostic Laboratories, Specialty Cancer Centers, Academic and Research Institutes, Reference Laboratories, Preventive Health Screening Providers, and Others. | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

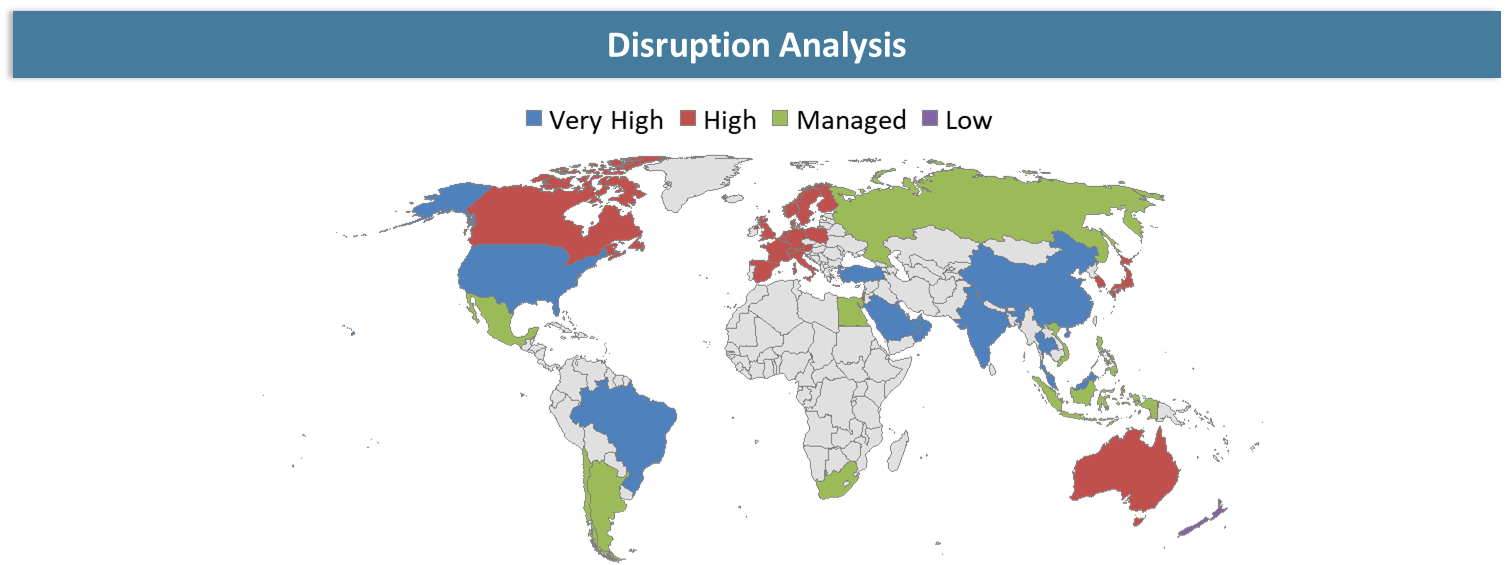

Disruption Analysis

Shift from Single-Cancer Screening to Preventive Multi-Cancer Detection Ecosystems

The main disruption in the Multi Cancer Early Detection industry is not only the development of novel diagnostic assays but also the change in focus from organ-specific cancers towards comprehensive multi-cancer detections that can be done via blood tests. The conventional cancer screenings have been very fragmented in their nature where one may need different kinds of screenings like mammograms, colonoscopies, or imaging studies for each kind of cancer.

Another disruption is through the integration of genomic data, machine learning algorithms, and multi-omics analysis tools. These diagnostic providers are now competing on the basis of tissue-of-origin detection capabilities, false positive rates, and accurate prediction abilities besides just being sensitive in their assay design.

Another disruption is associated with the changes in healthcare provision and healthcare reimbursement. Healthcare facilities, insurance providers, and preventive care services are starting to consider if early screening for cancer would lower healthcare costs and lead to better patient outcomes in the future. This puts conventional healthcare systems under pressure due to their dependence on symptomatology and interventions conducted later. Providers who can integrate into healthcare processes, produce evidence and show the benefits from an economical point of view have a chance to succeed in the market.

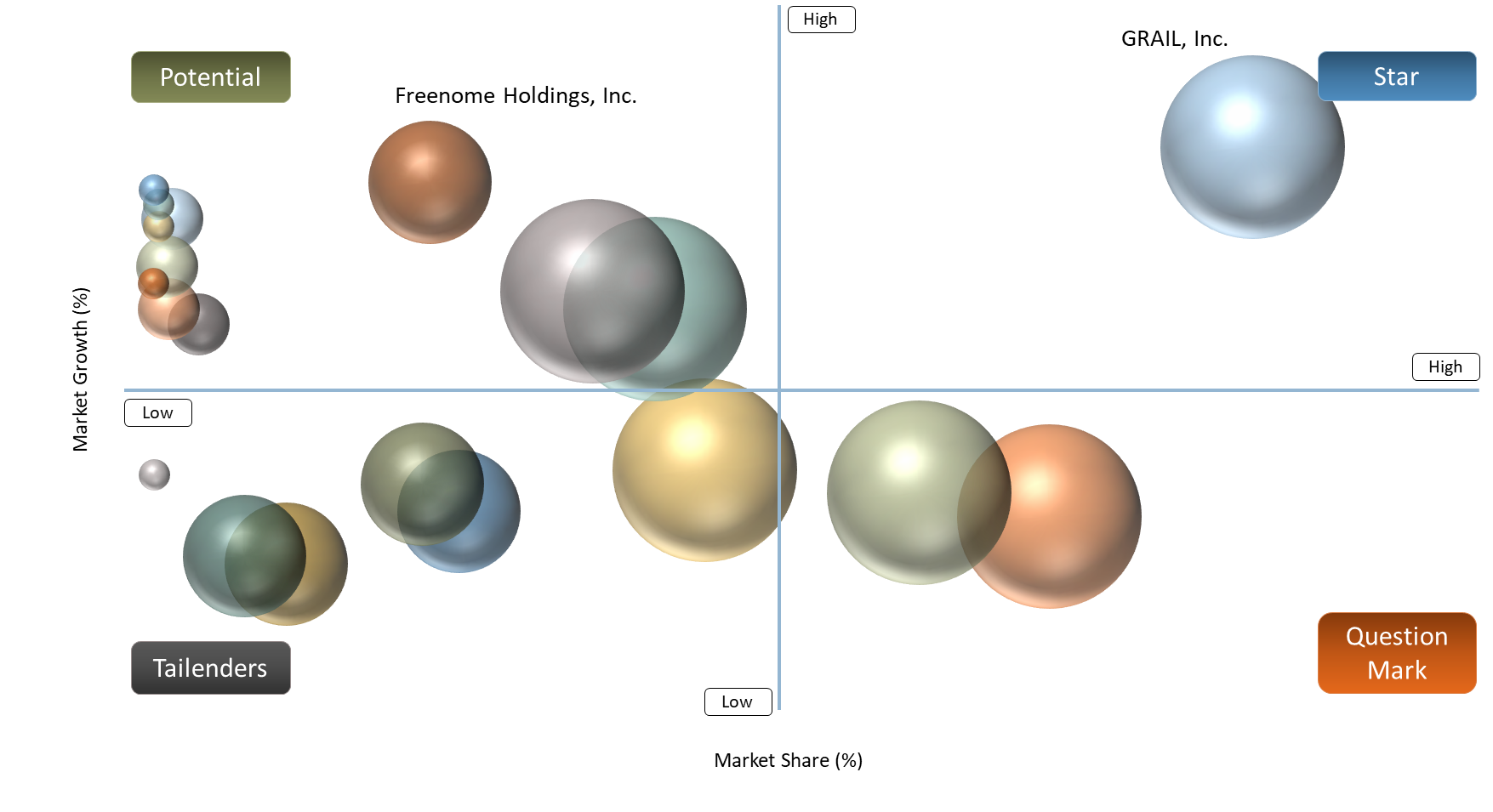

BCG Matrix: Company Evaluation

Under the BCG matrix of the Global Multi Cancer Early Detection Market, Stars include companies with validated clinical pipelines, advanced biomarker platforms, and improving strengths in commercialization. These companies are currently influencing the growth of the market through the conduct of huge-screening studies, working with the healthcare delivery system, and technology differentiation. Companies such as GRAIL, Inc., Guardant Health, Inc., and Exact Sciences Corporation belong in this category owing to their pioneering status in blood-based cancer detection, methylation analysis, and increased adoption by physicians.

The Cash Cows are the companies with well-developed genomics infrastructure, laboratory platforms, and ongoing revenues from their molecular diagnostics operations. These companies take advantage of their strong customer base and established ties with oncology diagnostic markets that facilitate their ability to drive MCED growth via current technologies. Some of the companies under this category include Illumina, Inc. and Foundation Medicine, Inc..

Question Marks are those companies with innovative multi-cancer detection technology with potential for market entry and/or reimbursement but lacking the same at present. These companies are mostly involved in biomarker research, artificial intelligence, and next-generation screening systems; however, further development is needed before they can become commercially viable. Some examples of Question Mark companies are Freenome Holdings, Inc., Burning Rock Dx, Singlera Genomics Inc., and SeekIn Inc.

Multi Cancer Early Detection Market Dynamics

Expansion of AI and Multi-Omics Applications in Cancer Detection

The increased development and applications of artificial intelligence technology and multi-omics technology are important factors behind the growing global multi cancer early detection market Size. Multi-omics involves a combination of data obtained through genomics, epigenomics, proteomics, and transcriptomics analysis, whereas artificial intelligence/machine learning assists in analyzing large and complex datasets for detection of minimal early stage cancer biomarkers, especially at the initial stages of tumor development when the levels of tumor biomarkers are relatively low.

As the global cancer burden increases, the significance of this factor becomes increasingly apparent. In "Cancer Statistics, 2026," by Rebecca L. Siegel et al., it was mentioned that in 2025, the United States had around 2,041,910 new cancer diagnoses, along with 618,120 deaths; however, the estimated figures for 2026 show a significant increase to nearly 2,114,850 cancer incidences and 626,140 deaths. Due to an increasing number of new cancer cases and deaths, there is an urgent need for advanced early detection technologies to provide better health outcomes for patients by enabling earlier treatments and reducing the cost of treatments in the long run..

Moreover, AI-driven multi-omics MCED systems have the capacity to sense biomarkers for more than 50 types of cancer based on only one blood draw, with specificity reported above 99% by various clinical trials, providing a basis for building population-scale screening tools. On the other hand, from a commercial standpoint, the combination of AI with multi-omics technology is enhancing sensitivity, tissue of origin prediction, and diagnostic accuracy, leading to increased differentiation among the MCED diagnostic tool makers.

Complex Clinical Validation Requirements for Multi-Cancer Screening Tests

The complex validation process is another major factor limiting growth within the global multi-cancer early detection testing industry because MCED tests have to be tested and proven to work effectively for numerous kinds of cancer before obtaining broad clinical validation. In contrast to the conventional screening test for a specific kind of cancer, which focuses on assessing analytical and clinical characteristics, these tests aim to identify several dozen forms of cancer based on analysis of one blood sample while being highly specific and predicting accurately the location of primary lesions, which significantly complicates validation process.

The validation task is further complicated by the fact that early-stage cancers tend to excrete very low levels of biomarkers, thus raising difficulties in their detection and significantly increasing the likelihood of a false-negative result. As stated in Multicancer Early Detection Testing: Guidance for Primary Care Discussions with Patients by Richard M. Hoffman et al. (2025), there were some MCED tests which showed an overall sensitivity of about 51.5% in detecting cancers at any stage even with high specificity. This indicates the necessity for comprehensive long-term research conducted with large groups of patients.

Therefore, developers would be required to allocate significant amounts of resources in conducting clinical trials, validating test processes, and collecting population-level evidence, which in turn will increase development costs and prolong the process of commercialization.

Multi Cancer Early Detection Market Segmentation Analysis

The global multi cancer early detection market is segmented based on test type, technology, sample type, cancer type, end-user, and region.

Liquid Biopsy Tests Lead the Market Through Non-Invasive Multi Cancer Detection and Broad Screening Capability

Liquid biopsy tests have a leading market share within the by test type category in the global multi-cancer early detection market since they symbolize the commercially maturest and most scalable strategy for detecting cancers by using non-invasive cancer testing. Liquid biopsy-based multi-cancer detection tests examine circulating tumor DNA, epigenetic biomarkers, circulating tumor cells, and other biomarkers of early-stage cancer by analyzing a single blood sample to detect multiple cancers without requiring invasive biopsy methods. Their ability to support repeated testing and population-level screening makes liquid biopsy a critical component of the expanding Multi Cancer Early Detection Market Size and a major contributor to Early Cancer Screening Market Growth.

Moreover, the prominence of liquid biopsy is further bolstered by key trends in the oncology diagnostics market, which indicate a preference for less-invasive tests using blood samples that increase patient adherence while allowing for early treatment. As per GRAIL, the Galleri test is capable of detecting over 50 types of cancers in a single blood draw, pointing to the improved capabilities of liquid biopsy systems for widespread cancer screening. On the other hand, the growing prevalence of cancer worldwide is driving demand for genomics cancer diagnostics and precision oncology testing services. All of these trends together reaffirm the results of liquid biopsy cancer detection market analysis, which identifies liquid biopsy as the dominant technology segment in the overall Cancer Screening Market Forecast.

Multi Cancer Early Detection Market Geographical Penetration

North America Leading Multi Cancer Early Detection Advancement Through Innovation Density and Commercial Execution Leadership

North America is considered as one of the foremost regions in the global multi cancer early detection market owing to the well-developed oncology diagnostics market research landscape, developed infrastructure for molecular diagnostics, and advanced technologies for innovative screening procedures. North America's oncology diagnostics market research landscape is further enhanced due to the presence of prominent diagnostic manufacturers, well-structured laboratories, and interaction between hospitals, cancer centers, and research organizations. With respect to the development of multi cancer detection tests, genomics-based cancer diagnostics, and personalized oncology diagnostics, North America is considered to be a frontrunner in Oncology Diagnostics Market Trends.

The opportunity in this region is enhanced further by the overall burden of cancer. As per GLOBOCAN 2022, Northern America reported around 2.7 million new cases of cancer in 2022. The high burden of disease increases the demand for innovative solutions to detect the presence of cancer biomarkers at an early stage using only one sample of blood. Hence, North America remains at the forefront of early cancer screening market growth.

U.S. Multi Cancer Early Detection Market Trends

The U.S. Multi Cancer Early Detection Market is driven by increasing focus on non-invasive cancer testing, greater funding for genomic cancer diagnosis, and an increased number of clinics looking at the role of blood-based multi cancer testing in addition to traditional methods of screening. The United States continues to be the most commercially focused market due to its superior diagnostics infrastructure for oncology, higher research activity, and the presence of prominent MCED players. Clinicians are now assessing the use of liquid biopsy solutions that detect cancer markers using only one blood draw.

One of the key trends in the U.S. market involves increasing the use of clinically validated methods for diagnosing those cancers which do not have screening programs. As reported by the American Cancer Society, about one-half of all cancers diagnosed annually have no screening recommendations, and only rarely are MCED tests covered by health insurance, whether public or private. It is a combination of this significant unmet need for cancer screening combined with lack of coverage that characterizes today's analysis of the Liquid Biopsy Cancer Detection Market and Early Cancer Screening Market Growth in the United States.

Canada Multi Cancer Early Detection Market Outlook

Canada's Multi Cancer Early Detection Market Potential is based on increasing demand for non-invasive cancer testing, interest in genomic-based cancer diagnostics, and need for diagnostic tools that would allow for early detection of cancers which are usually diagnosed at an advanced stage. Prevention, screening, and early intervention are the main focuses of Canada's healthcare system, which creates a favorable environment for development of multi-cancer testing and precision oncology testing products. The country also offers great potential for the market because of its well-developed research landscape, public health approach to medicine, and growing recognition of the importance of early-stage cancer biomarkers in treatment success.

The prognosis is further fortified by the increasing incidence of cancer in the nation. According to Canadian Cancer Society projections, Canada was estimated to have 247,100 new cases of cancer patients in 2024. This underlines the increasing necessity for efficient methods of diagnosing cancer at an early stage. With health care systems increasingly assessing innovations in screening and diagnostic technologies, Canada appears poised to offer an ideal scenario for liquid biopsy cancer detection market analysis.

Multi Cancer Early Detection Market Competitive Landscape

- The competitive structure in the Global Multi Cancer Early Detection Market is highly concentrated yet extremely dynamic, as competition is now determined not only by the introduction of a novel diagnostic platform but also by clinical performance, number of biomarkers used, ease of integration into existing workflows, and market preparedness. In terms of visibility within the market, GRAIL, Inc. continues to maintain its position through the Galleri blood-based multi-cancer early detection (MCED) test, whereas Exact Sciences Corporation has created additional competition for this segment through the Cancerguard blood-based MCED test that caters to the provider market.

- Competitors in the next level will be made up of companies like Freenome Holdings, Inc., Burning Rock Dx, Singlera Genomics Inc., SeekIn Inc., Illumina, Inc., Foundation Medicine, Inc., and Natera, Inc. These players combine to form a group consisting of MCED developers, sequencing and genomics platforms, and companies that operate within the adjacent space of precision oncology testing. In the future, success in this market might hinge on things like validation, accuracy, payer support, and even incorporating non-invasive cancer screening into existing processes.

Key Developments of the Multi Cancer Early Detection Market

- In April 2026, GRAIL announced integration of the Galleri test into Epic’s electronic health record platform, enabling ordering and result access across approximately 450 health systems and expanding point-of-care access.

- In March 2026, Guardant Health launched its Shield Multi-Cancer Detection test in Hong Kong, Singapore, and the Philippines through a partnership with Manulife, marking an important step in Asian market expansion.

- In January 2026, GRAIL submitted a premarket approval application to the U.S. FDA for the Galleri multi-cancer early detection test, a major regulatory milestone for the MCED category.

- In January 2026, Freenome announced an expanded artificial intelligence and deep learning initiative with NVIDIA to improve the analytical speed and accuracy of its blood-based multi-cancer detection platform.

- In September 2025, Exact Sciences launched Cancerguard as a blood-based multi-cancer early detection test, positioning it as the first commercially available MCED test to analyze multiple biomarker classes.

- In December 2025, Exact Sciences announced the first participant enrollment in the CRANE study in Japan, a landmark clinical evaluation led by the National Cancer Center to assess its MCED blood test in that market.

- In October 2025, GRAIL reported PATHFINDER 2 results showing that adding Galleri to standard screening increased cancer detection more than seven-fold, with more than half of Galleri-detected cancers found at an early stage.

- In October 2025, Samsung and GRAIL entered a strategic collaboration to commercialize Galleri in South Korea, with possible expansion to Japan and Singapore, alongside a planned $110 million equity investment.

- In July 2024, Guardant Health received U.S. FDA approval for Shield as a primary blood-based screening option for colorectal cancer, helping validate blood-based early detection and strengthening adoption of liquid biopsy screening pathways.

- In June 2024, Illumina completed the divestiture of GRAIL, allowing GRAIL to operate independently and sharpen its focus on commercialization and regulatory progress for the Galleri MCED test.

White Space Opportunities

There are many white space opportunities available within the Global Multi Cancer Early Detection Market because of the wide variety of cancers which do not yet have routine screening processes and the increasing need for technologies that screen for cancer non-invasively. As the currently employed screening methods are mainly limited to cancers like breast cancer, colorectal cancer, cervical cancer, and lung cancer, a number of cancers with very high mortality rates are often discovered at late stages because of their lack of effective screening techniques. There is great potential for the development of multi cancer tests capable of picking up several tumor markers in one blood sample.

Another important whitespace opportunity is in the realm of integration and preventive health ecosystems. The fact is, some of the healthcare systems out there do not have any kind of workflow process for incorporating MCED technologies into their annual screening processes. This means that there will be more room for firms who can streamline the integration of the technology on the part of physicians as well as patients. Payers have yet to catch up when it comes to education and reimbursement models, giving more room for firms to provide evidence of cost savings from outcomes.

DMI Opinion

According to DataM, the key issue within the global multi cancer early detection market is less about demand for early cancer screening and more about the ability of suppliers to convert the clinical interest in such screening into something feasible, reproducible, and scalable while avoiding complexity that escalates faster than clinical benefits. The market favors suppliers who are able to render multi cancer detection test solutions operational for clinicians, laboratories, and healthcare organizations and not only technologically advanced.

Thus, factors such as clinical validation quality, the accuracy of identifying tissues of origin, compatibility with laboratory procedures, reimbursement opportunities, and clarity concerning next steps receive as much attention as biomarker sensitivity. Healthcare professionals value reliable tests that are easy to integrate into existing practices more than anything else.

Most players within the market remain highly reliant on innovation stories while failing to appreciate the actual dynamics involved in the adoption process. On the contrary, noninvasive cancer screening systems that present robust validation backing, clinical endorsement, and realistic adoption strategies have higher chances of success. Competitive advantage is derived from the ability to implement genomic cancer diagnostics and precision oncology testing solutions.

Why Choose DataM?

- Multi Cancer Detection Test Technology Deep Dives: Covers breakthrough technologies that can be applied in multiple MCED technologies such as liquid biopsies, methylated DNA analysis, fragmentomics technology, multiomics, ctDNA testing, protein-based markers, and artificial intelligence tools for signal interpretation in diagnostics.

- Biomarker Performance and Market Differentiation Factors: Measures the performance of different competitors in the context of developing and selling MCED products in the marketplace. This involves assessment of biomarker sensitivity, predictive ability of origin of tissue, robustness of clinical validation, workflow, laboratory preparedness, regulatory compliance, and scalability of solutions.

- Market Implementation Cases of Real-World Evidence: Highlights use cases where non-invasive cancer screening and genomic cancer diagnostics are being used in preventative oncology initiatives, research studies, and clinical settings.

- Industry Developments and Market Updates: Covers developments in major market activities, such as product launch, validation, regulatory development, payor development, partnership activities, clinical trial expansion, and commercialization in important markets like North America, Europe, Asia Pacific, and China.

- Competitive Strategy: Covers competitive actions taken by important companies to solidify their position through innovations in biomarkers, artificial intelligence applications, collaboration, market expansion, clinical data generation, and healthcare ecosystem collaboration.

- Value Creation and Product Pricing: Offers insights into value creation from blood-based MCED technologies, laboratory-developed tests, and prevention of diseases through preventive screenings. It also covers commercialization strategies, payer, and provider engagements.

- Market Penetration and Expansion Strategy: Covers market penetration through cancer types with under penetration, high-risk individuals, preventive checkups, and emerging regional markets. It also discusses strategies for scaling through validation, workflow enablement, and commercialization.

Target Audience

- Oncology diagnostics companies

- Liquid biopsy and biomarker developers

- Genomic cancer diagnostics and precision oncology testing providers

- Hospital and cancer center leadership teams

- Clinical laboratory and pathology network leaders

- Preventive health screening providers

- Corporate strategy and market intelligence teams

- Business development and partnership leaders

- Investors and private equity firms

- Payers and reimbursement strategy teams

- Regulatory and clinical affairs teams

- Consulting and advisory teams

Suggestions for Related Reports

- Liquid Biopsy Early Cancer Detection Market

- Global Liquid Biopsy Market

- Oncology Molecular Diagnostics Market

- Global Molecular Diagnostics Market

- Global Cancer Biomarker Testing Market

- Cancer Diagnostic Market

- Cancer Tumor Profiling Market

- Noninvasive Cancer Diagnostics Market

- Breast Cancer Screening and Diagnostic Techniques Market