Healthcare LLM Platform Market Size

Clinical data has become one of healthcare’s most underused strategic assets. Hospitals, payers, telehealth providers and digital health companies now generate large volumes of EHR data, clinical notes, physician narratives, coding records, patient messages and virtual care interactions. Healthcare LLM platforms are becoming commercially important because they help convert this unstructured information into documentation support, workflow automation, patient communication, coding improvement and clinical decision support.

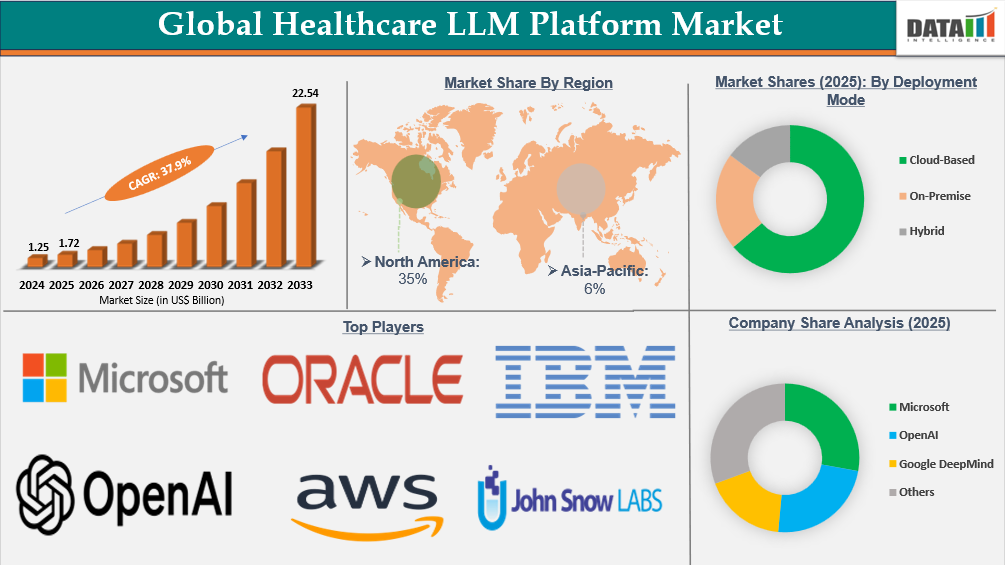

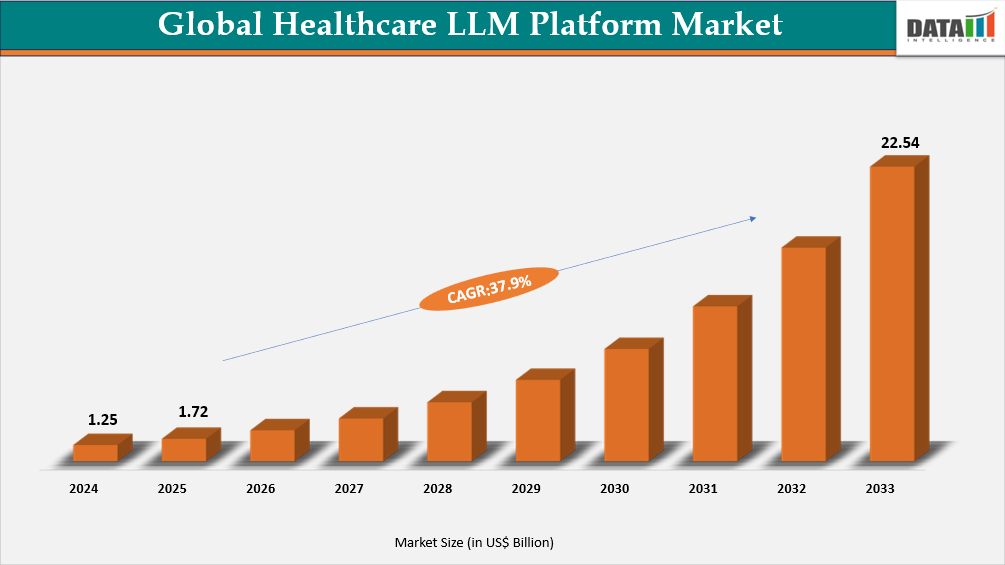

Healthcare LLM Platform Market is valued at US$ 1.72 billion in 2025 and is projected to reach US$ 42.81 billion by 2035, growing at a CAGR of 37.9% during 2026–2035.

Investment timing is highly relevant because healthcare systems are no longer evaluating generative AI only as a pilot technology. Buyer demand is shifting toward secure, compliant and integrated Healthcare LLM Platform solutions that can connect with EHR systems, telehealth platforms, clinical documentation workflows and administrative revenue cycle tools. With over 95% of U.S. non-federal acute care hospitals using certified EHR systems, 82% online digital health service availability in 2024 and strong digital record adoption across Canada, China, Japan and India, the market has a strong infrastructure base for LLM deployment.

Key Takeaways

- The Healthcare LLM Platform Market is projected to expand from US$1.72 billion in 2025 to US$42.81 billion by 2035, supported by a 37.9% CAGR.

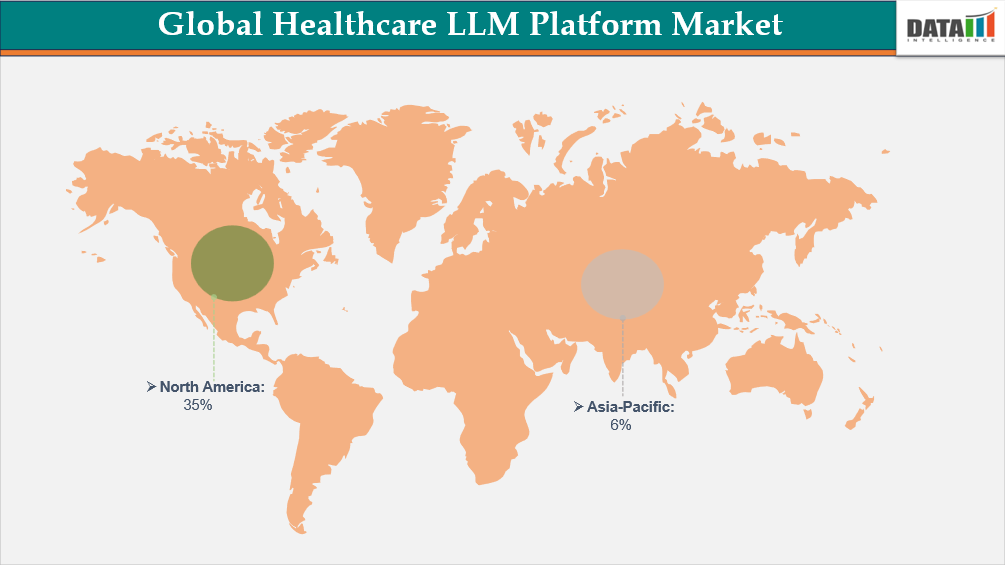

- North America accounted for the largest Healthcare LLM Platform Market Share at 35% in 2025, supported by high EHR penetration, AI readiness and enterprise healthcare IT spending.

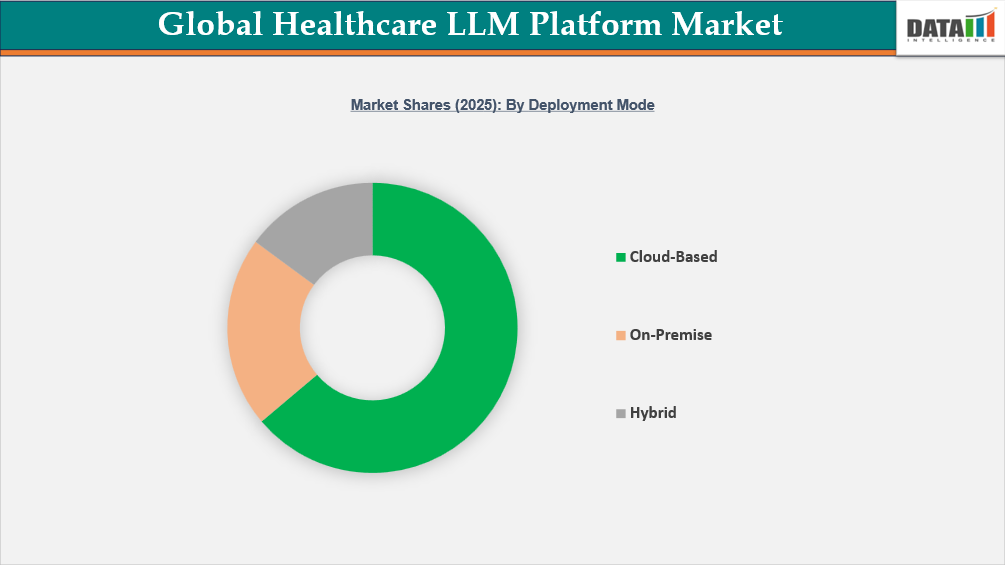

- Cloud-based deployment led the market with 63.84% share in 2025 because healthcare buyers prefer scalable SaaS and API-based models over heavy on-premise infrastructure.

- Asia-Pacific is the fastest-growing regional market, with China, India and Japan building stronger digital health foundations through EHR adoption, telemedicine usage and public digital health programs.

- Clinical documentation, EHR summarization, coding support, patient communication and decision support are among the most commercially relevant application areas.

- Regulatory compliance, cybersecurity, data residency and interoperability are not secondary concerns. They directly influence vendor selection, hospital procurement cycles and enterprise-scale adoption.

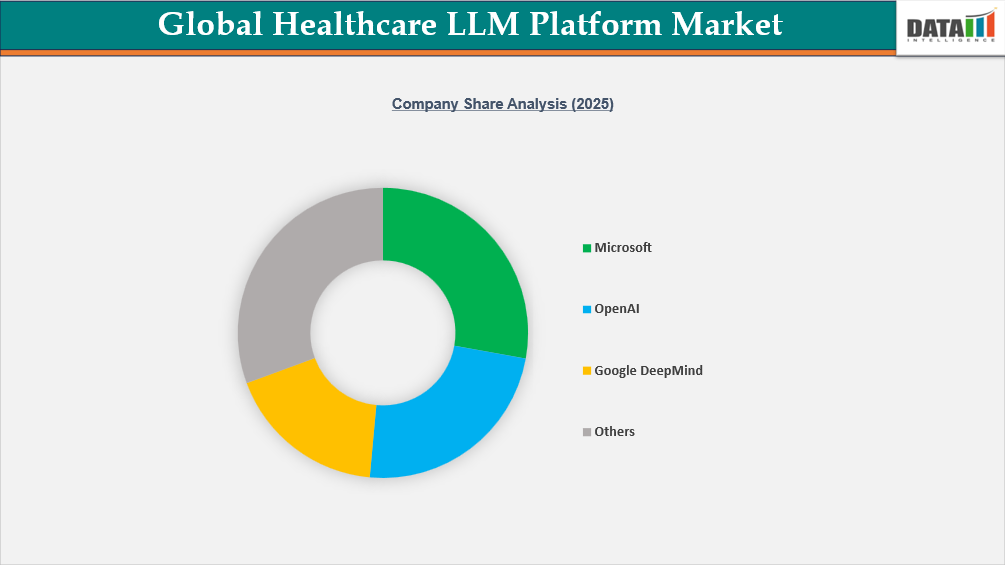

- Microsoft, OpenAI, Google DeepMind, AWS, Anthropic, John Snow Labs, Truveta, Yseop and NVIDIA are positioned across foundation models, cloud infrastructure, medical NLP and healthcare-specific AI deployment.

Healthcare LLM Platform Market Scope

| Report Attribute | Details |

| Market Size in 2025 | US$1.72 billion |

| Market Size by 2035 | US$42.81 billion |

| CAGR | 37.9% |

| Historic Years | 2023 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Segments Covered | Component, Deployment Mode, Model Type, Application, End User, Organization Size and Region |

| Leading Region | North America, with 35% revenue share in 2025 |

| Fastest Growing Region | Asia-Pacific |

Digital Infrastructure Is Setting the Market Baseline

Healthcare LLM Platform Market Growth is closely tied to the digital maturity of hospitals and care networks. EHR adoption has already created the core data layer in many developed healthcare systems. In the United States, more than 95% of non-federal hospitals use certified EHR systems. Canada reports EHR use among approximately 95% of physicians. Japan has certified digital health records across around 95% of large hospitals while more than 85% of China’s major tier-1 hospitals have implemented electronic health record systems.

The commercial value of LLM platforms comes from their ability to work across this digital foundation. Hospitals can use these platforms to summarize clinical notes, reduce repetitive documentation, support coding accuracy, automate record updates and improve patient-facing communication. For executives, the investment case is linked to administrative burden reduction, faster clinician workflows and more scalable digital care operations.

Cloud Deployment Defines the Current Buying Pattern

Cloud-based deployment accounted for 63.84% of the Healthcare LLM Platform Market Share in 2025. The preference for cloud delivery is practical. Large language models require scalable computing power, frequent model updates, security controls, governance frameworks and integration with enterprise applications. Cloud-based SaaS and API models reduce the need for hospitals to maintain high-cost GPU infrastructure internally.

Healthcare buyers also value cloud environments that support HIPAA, GDPR, regional data residency and cybersecurity requirements. Cloud deployment improves implementation speed for clinical documentation assistants, revenue cycle management tools, telehealth bots and EHR summarization platforms. For vendors, the cloud model also supports recurring revenue through subscription and usage-based pricing.

On-premise deployment remains relevant where data sovereignty, internal governance or highly sensitive clinical workloads limit external hosting. However, cloud-based platforms currently have stronger commercial traction because they provide faster scaling, centralized governance and lower infrastructure barriers.

Segmentation Analysis and Use Case Economics

The Healthcare LLM Platform Market is segmented by component, by deployment mode, by model type, by application, by end user, by organization size, and by Region - Share, Trends, and Forecast to 2035.

Deployment mode is the clearest quantified segment in the current market dataset. Cloud-based platforms lead because they align with healthcare’s need for scalable computing, model updates, EHR connectivity and controlled implementation costs. On-premise models remain important for organizations with strict data governance requirements, but higher infrastructure costs may limit broad adoption.

By application, clinical documentation is one of the strongest use cases because physician documentation burden is a direct operational pain point. LLM platforms can assist with note summarization, record structuring and workflow support inside EHR environments. Revenue cycle management and coding accuracy also offer a clear ROI angle because better documentation and coding support can reduce administrative inefficiency. Patient engagement tools, virtual assistants and telehealth communication systems are gaining attention as digital care interactions continue to rise.

By end user, hospitals, clinics, telehealth providers and healthcare organizations with mature digital health infrastructure are likely to remain early adopters. Large enterprises have stronger budgets, IT teams and governance structures, while smaller and rural facilities may face slower adoption due to interoperability constraints and legacy infrastructure.

Cloud-Based Deployment Dominates the Global Healthcare LLM Platform Market

In 2025, cloud-based deployment represents for 63.84% of the worldwide healthcare LLM platform market, making it the dominant deployment model. This method involves hosting LLM platforms on secure, medically-compliant cloud infrastructure and delivering them via SaaS or API-based services, removing the need for hospitals or healthcare organizations to maintain costly on-premise hardware.

Several reasons contribute to its dominance. LLMs need high-performance GPU clusters, which are more affordable and scalable in the cloud than on-premises. Most healthcare AI technologies, such as clinical documentation assistants, revenue cycle management tools, and patient interaction bots, are SaaS-based and prefer cloud delivery. Furthermore, cloud providers provide HIPAA- and GDPR-compliant environments with regional data residency choices, which reduces regulatory hurdles. Cloud solutions also allow for quick interface with EHRs, telemedicine systems, and analytics platforms, reducing implementation times.

Cloud deployment enables continual model changes, centralized governance, and predictable recurring income via subscription or usage-based models. Although problems such as data sovereignty, cybersecurity threats, and potential vendor lock-in persist, the scalability, compliance, and quick implementation benefits make cloud-based LLM systems the preferred choice for healthcare institutions throughout the world.

Economic and Investment Analysis

Macroeconomic pressure on healthcare systems is increasing interest in technologies that can improve productivity without expanding headcount at the same rate. LLM platforms address cost-sensitive areas such as documentation time, administrative workflow load, coding support and patient communication. For CFOs and procurement teams, ROI will depend on implementation cost, integration complexity, clinician adoption and measurable productivity gains.

Capital expenditure is shifting toward cloud-based operating models, reducing upfront hardware investment while increasing recurring software and usage costs. This creates a more flexible procurement path for hospitals, although buyers must evaluate vendor lock-in, data governance controls and long-term subscription economics.

Investment opportunities are strongest in healthcare-specific model fine-tuning, clinical workflow integration, data governance, cybersecurity, medical NLP and EHR-native copilots. Economic risks include delayed procurement cycles, cautious compliance review, uneven AI adoption across smaller institutions and potential cost inflation for advanced compute resources.

Geographical Penetration

Largest Market:

Demand for Healthcare LLM Platform Market in North America

The need for Healthcare LLM platforms in North America is robust and growing, due to improved digital health infrastructure, extensive EHR usage, and expanding AI integration across healthcare settings. In the United States, more than 95% of non-federal hospitals and 85% of office-based physicians utilize electronic health records, and 71% of hospitals have integrated predictive AI technologies to help with clinical decision-making and administrative processes. In Canada, about 95% of physicians utilize EHRs, and approximately 87% of healthcare organizations use AI in patient care, such as data analysis and documentation automation. Virtual care is a crucial driver in both nations. In 2023, over 40% of Canadian patients accessed virtual consultations, with over 78.5% obtaining the provided appointments. Telehealth adoption in the U.S. continues to be common post-pandemic. These factors, combined with high EHR penetration, rising AI adoption, and sustained virtual care engagement, create a strong market for LLM platforms that can streamline documentation, improve patient communication, enhance clinical decision-making, and optimize administrative efficiency across North America.

U.S. Healthcare LLM Platform Market Outlook

The healthcare industry in the US is continuing to accelerate its digital transformation, setting the stage for wider use of AI-enabled solutions and (LLM) platforms. (EHRs) are already almost ubiquitous in non-federal hospitals, with over 95% of institutions using approved EHR systems, creating a foundational digital architecture that LLMs may expand upon. The use of generative and predictive AI is growing quickly; in 2024, over 31.5% of U.S. hospitals were early adopters of GenAI connected with EHRs, and another 24.7% want to do so within a year, indicating a trend for broader LLM integration. Further evidence of the expanding usage of AI for risk prediction, scheduling, and administrative activities comes from the fact that 71% of U.S. hospitals reported utilizing predictive AI in 2024, up from 66% in 2023.Telehealth is a significant feature of care delivery and digital engagement, with many Americans having utilized virtual care services and continuing to rely on digital platforms. Despite this progress, obstacles including as interoperability, legacy infrastructure limitations, and unequal adoption among smaller and rural hospitals remain. High EHR penetration, increased AI use, and continuous digital care engagement indicates a growing interest in LLM platforms to expedite clinical documentation, help decision-making, decrease administrative load, and improve patient communication in U.S. healthcare systems.

Canada Healthcare LLM Platform Market Trends

Large language model (LLM) platforms are becoming more and more popular in Canada as the healthcare industry continues its digital revolution. There is a strong trend toward intelligent automation, as evidenced by the fact that 87% of Canadian healthcare institutions already employ artificial intelligence in some capacity for patient care, including processing and analyzing medical data and updating records.95% of doctors say they use electronic medical or health records, demonstrating the broad use of digital records that LLM technology may take use of for process automation and documentation. Even with increasing acceptance, there are still issues with interoperability and legacy infrastructure, since many systems remain fragmented and restrict smooth data transmission. With over 40% of patients getting virtual treatment in 2023 and over 78.5% of those offered virtual appointments completing them, virtual care is still a significant part of Canadian healthcare delivery, demonstrating the country's sustained dependence on digital service delivery. The expanding use of AI, the widespread use of digital records, and the ongoing participation in virtual care all contribute to the increased interest in LLM platforms as a means of improving clinical decision-making, patient communication, and documentation efficiency in Canadian healthcare settings.

Fastest Growing Market:

Asia-Pacific Records the Fastest Growth in the Healthcare LLM Platform Market

The market for healthcare LLM platforms is growing at the quickest rate in the Asia-Pacific region because to several factors, such as growing healthcare infrastructure, AI integration, and the quick adoption of digital health. A solid basis for AI-driven platforms is provided by the fact that more than 85% of China's major tier-1 hospitals have adopted electronic health record systems. In India, government programs like the National Digital Health Mission have expanded digital patient data coverage to over 40% of the population, especially in metropolitan areas. In Japan, approximately 95% of large hospitals utilize certified digital health records. In 2023, over 50% of urban patients in key APAC nations reported utilizing virtual consultations at least once, indicating a considerable increase in the use of telemedicine throughout the area.

These developments make it possible for LLM-driven systems to automate clinical documentation, boost patient involvement, and facilitate better decision-making in Asia-Pacific hospitals and clinics.

India Healthcare LLM Platform Market Insights

The India Healthcare LLM Platform Market is expanding rapidly, driven by fast digital health transformation, AI integration, and the growing use of large language models (LLMs) in clinical and administrative workflows. The government's Ayushman Bharat Digital Mission (ABDM) has established a strong digital health ecosystem, with over 67.19 crore health records linked to ABDM accounts and more than 4.18 lakh health institutions registered, offering a large structured database for LLM-powered apps. Telemedicine usage is also rising, with India's national telehealth network eSanjeevani supporting hundreds of millions of remote consultations, producing unstructured patient data that LLM systems may handle for documentation, summarization, and decision assistance.

A favorable climate for LLM integration has been created by the sharp rise in AI usage among Indian physicians, with 41% of them now utilizing AI technologies to improve treatment quality and expedite processes. With over 50% of providers committing 20–50% of IT funds to cutting-edge technology like LLM-enabled documentation, coding, and patient communication systems, hospitals are making significant investments in digital innovation. In India, there is a high demand for LLM platforms to improve clinical documentation, patient engagement, and data-driven decision-making across healthcare facilities. These trends include the widespread adoption of digital health records, the rise in telemedicine use, the growing integration of AI, and the increased investment in healthcare IT.

China Healthcare LLM Platform Market Industry Growth

LLM use in China's healthcare industry is expanding quickly due to the country's extensive digital health infrastructure and growing need for sophisticated clinical solutions. By 2024, around 58% of community health centers and over 85% of top-tier hospitals in China had implemented electronic medical records (EMRs), creating a strong foundation of structured data for LLM-driven clinical documentation and analytics. Telemedicine has expanded rapidly, with 418 million digital healthcare users nationwide, representing about 37% of China’s internet population. More than 3,300 internet hospitals now conduct over 100 million online consultations annually. Additionally, AI integration is growing in patient interaction, workflow automation, and diagnostics, especially in tertiary hospitals and urban healthcare facilities.

High EMR usage, significant telemedicine use, and expanding AI integration are the drivers that are causing China's need for LLM platforms to increase. These variables allow for better decision-making, automated clinical recording, and increased patient engagement across clinics and hospitals.

Regulatory and Policy Analysis

Healthcare LLM platforms operate in one of the most regulation-sensitive AI markets. HIPAA, GDPR, local patient data residency rules, telemedicine compliance, cybersecurity requirements and AI certification expectations influence platform architecture, procurement approval and vendor qualification.

Policy support for digital health is also material. WHO initiatives such as the Global Digital Health Monitor support national efforts to build interoperable and secure digital health systems. India’s ABDM, China’s internet hospital ecosystem and North America’s EHR infrastructure create a stronger environment for LLM deployment. Regulatory pressure will likely increase through 2035 as governments sharpen rules around clinical AI accountability, patient data use, model transparency and safety validation.

Competitive Landscape

The Global Healthcare LLM Platform market is very competitive, with major technology companies including as Microsoft, OpenAI, and Google DeepMind dominating through foundation models, cloud integration, and strong collaborations with healthcare providers. Amazon Web Services and Anthropic expand the ecosystem by offering scalable, compliant LLM infrastructure for regulated healthcare contexts.

At the same time, healthcare AI companies like John Snow Labs, Truveta, and Yseop specialize in domain-specific medical NLP, EHR-trained language models, and regulatory paperwork automation. Infrastructure providers such as NVIDIA enable large-scale model training and deployment.

Rapid advancement in generative AI is driving competition, as is the growing deployment of clinical documentation copilots, EHR summarizing tools, and AI-powered decision support systems. Strategic alliances, regulatory compliance, and healthcare-specific model fine-tuning continue to be critical for retaining market share and capitalizing on growth prospects.

Key Developments

- June 2026 – NVIDIA expands healthcare-specific AI model development

NVIDIA partnered with Abridge to develop a healthcare-specific large language model trained on de-identified clinical conversations using Nemotron models. The platform is designed to improve clinical documentation, ambient note generation, and real-time clinical decision support, strengthening NVIDIA's healthcare AI infrastructure portfolio. - June 2026 – Truveta expands AI-powered healthcare data capabilities

Truveta continued expanding its AI-enabled healthcare data platform by enhancing access to large-scale electronic health record (EHR) datasets for clinical research, real-world evidence generation, and healthcare foundation model development, supporting advanced healthcare LLM applications. - March 2026 – John Snow Labs advances regulatory-grade healthcare AI platform

John Snow Labs announced new regulatory-grade healthcare AI and governance capabilities ahead of the 2026 Applied Healthcare AI Summit, expanding support for generative AI, agentic healthcare workflows, model governance, and compliant clinical NLP applications. - March 2026 – John Snow Labs expands healthcare agentic AI workflows

John Snow Labs introduced enhanced Patient Journey Intelligence and autonomous healthcare agent capabilities designed to improve clinical workflow automation, medical NLP, and enterprise healthcare LLM deployment while maintaining regulatory compliance. - February 2026 – Yseop strengthens AI-powered regulatory medical writing platform

Yseop enhanced its enterprise AI platform by expanding composite AI capabilities that combine large language models, symbolic AI, and retrieval-augmented generation (RAG) to automate clinical study reports, regulatory submissions, and medical writing workflows for life sciences organizations. - January 2026 – NVIDIA expands BioNeMo ecosystem for life sciences AI

NVIDIA strengthened its BioNeMo platform through expanded collaborations supporting pharmaceutical research, molecular modeling, and healthcare foundation models, reinforcing infrastructure for healthcare LLM development and biomedical AI workloads.

Strategic Insights and Analyst Perspective

Healthcare LLM platforms are becoming a board-level technology decision because they touch clinician productivity, patient engagement, coding performance, data governance and digital care delivery. Investors should track companies that sit close to clinical workflows rather than only model developers. Manufacturers and technology companies should prioritize secure integration, healthcare-specific training, compliance tooling and measurable workflow outcomes.

Risk mitigation will be central. Healthcare organizations must manage cybersecurity exposure, data sovereignty, interoperability, model reliability and clinician trust. Procurement teams should evaluate total cost of ownership, vendor lock-in risk, implementation timeline, governance controls and whether the platform improves actual workflow efficiency.

Through 2035, the market is likely to evolve from early GenAI pilots into embedded healthcare operating infrastructure. The winning platforms will be those that combine foundation model strength with clinical context, compliant deployment and practical integration into daily care delivery.

Report Benefits

This Healthcare LLM Platform Market report helps manufacturers and technology providers identify high-value use cases, deployment models and regional demand patterns. Investors can use it to understand adoption timing, competitive positioning and AI infrastructure opportunities. Suppliers and cloud providers can assess demand for compute, compliance and integration services. Procurement teams can benchmark vendor readiness, cost dynamics and implementation risks. Strategy teams can evaluate where Healthcare LLM Platform Market Growth is supported by EHR adoption, telehealth usage and healthcare AI investment.

What Sets This Global Healthcare LLM Platform Market Intelligence Report Apart

- Latest Data & Forecasts – Comprehensive and up-to-date market intelligence with forecasts through 2033, covering global demand by component, deployment mode, model type, application, end user, organization size, with region-wise analysis across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa.

- Regulatory Intelligence – In-depth analysis of global healthcare and data regulations that affect LLM adoption, including HIPAA, GDPR, local patient data residency restrictions, telemedicine compliance, AI certification standards, and cybersecurity requirements.

- Competitive Benchmarking – A structured review of prominent LLM platform providers based on product features, AI model sophistication, deployment reach, clinical integration, subscription/pricing strategies, collaborations, and enterprise acceptance across healthcare systems.

- Geographic & Emerging Market Coverage – Regional perspectives on healthcare digitalization, EHR adoption, telehealth penetration, AI readiness, and infrastructure maturity, with a particular emphasis on high-growth possibilities in Asia-Pacific, Latin America, and the Middle East and Africa.

- Actionable Strategies & Cost Dynamics – Strategic assistance on LLM implementation, workflow integration, data governance, cybersecurity management, deployment cost optimization, and adoption strategies, backed up by professional input from healthcare IT specialists, hospital administrators, and AI implementation consultants.

Target Audience

- Healthcare AI companies

- Cloud infrastructure providers

- Hospital systems

- Telehealth platforms

- Electronic Health Record (EHR) vendors

- Digital health companies

- Healthcare IT service providers

- Investors in healthcare technology sector

- Private equity firms

- Venture capital firms

- Procurement heads

- Chief Information Officers (CIOs)

- Chief Technology Officers (CTOs)

- Chief Financial Officers (CFOs)

- Clinical operations leaders

- Revenue cycle management companies

- Strategy consulting teams