Global Cutting Tools and Inserts Market Overview

The global cutting tools and inserts market reached US$ 11.05 billion in 2025 and is expected to reach US$ 19.94 billion by 2035, growing with a CAGR of 6.2% during the forecast period 2026-2035.

OEM’s are focusing on use of carbides, ceramics, CBN and PCD to increase accuracy, efficiency, tool life, reduce cost, minimize downtime and reduce material wastage. The shift towards electric cars, aircraft, energy and automation is causing a sharp rise in demand for tools that can machine metals such as titanium, aluminum and steel, along with composite materials, within tight tolerances. Advancements in industrial automation and smart manufacturing have also contributed greatly to increased adoption within both developed and developing nations.

As per the World Steel Association, the global crude steel production amounted to around 1.88 million tons in 2024, emphasizing the ongoing industrial manufacturing operations that contribute towards the use of metal cutting and machining. In addition, governments globally have been encouraging localization of semiconductor & defense manufacturing and pushing industry independence schemes, thus providing prospects for advanced tooling systems utilizing Industry 4.0 frameworks.

Cutting Tools and Inserts Industry Trends and Strategic Insights

- The utilization of multi-axis CNC machining centers and automated production systems is driving up the need for high-speed technology with superior dimensional accuracy, with the help of carbide and ceramic inserts.

- Tooling systems with IoT capabilities and smart sensors for predicting and maintaining machine performance through efficient processes are becoming more commonplace among manufacturers.

- The growing trend of aerospace manufacturing, as well as electric vehicle manufacturing, means there is an increased demand for cutting tools with high heat resistance and precision capabilities.

- Concerns regarding environmental sustainability are driving up the demand for sustainable tools, such as those made from recyclable materials and dry machining technologies.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 11.05 Billion | |

| 2035 Projected Market Size | US$ 19.94 Billion | |

| CAGR (2026-2035) | 6.2% | |

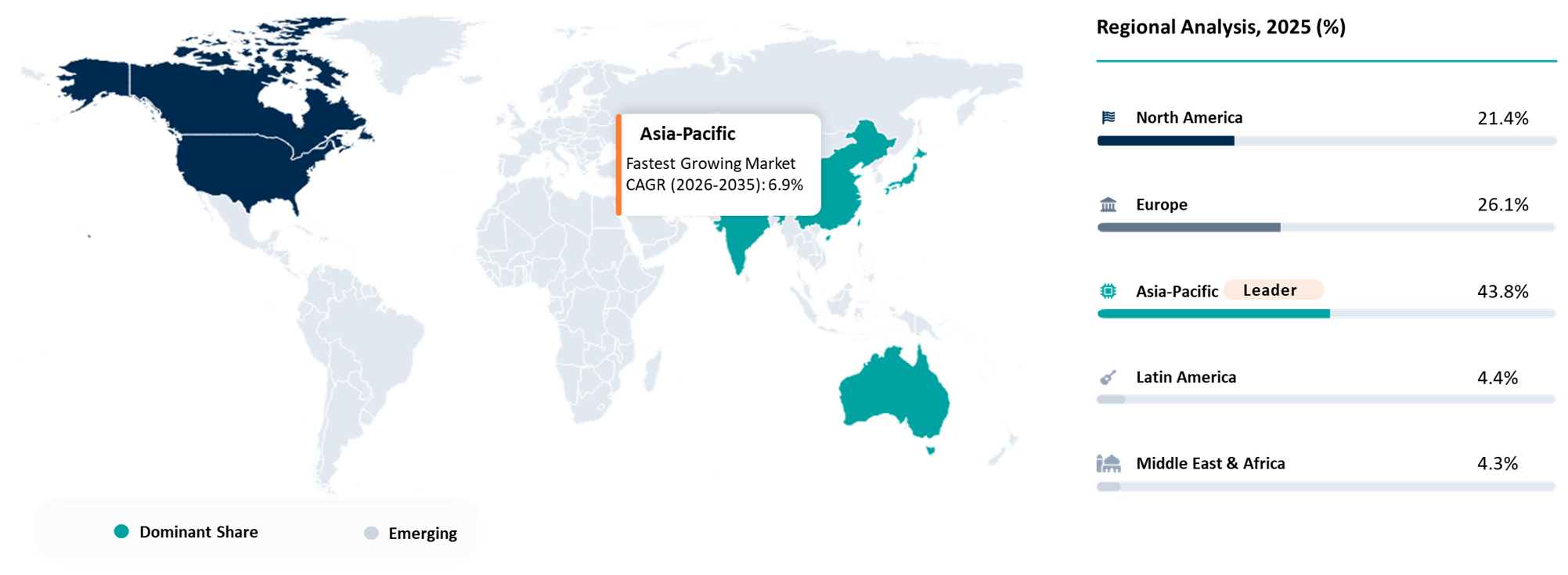

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Form | Solid Cutting Tools, Indexable Tools | |

| By Make | Standard, Custom | |

| By Product | Turning, Milling, Drilling, Threading, Hole Finishing Tools, Gear Cutting Tools, Broaching Tools | |

| By Tool Grade | High Speed Steel (HSS), Solid Carbide, Cermet, Ceramics, Cubic Boron Nitride (CBN)/PCBN Tools, Diamond Tools | |

| By Machine Type | 5-Axis Machining Center, Machining Center, CNC Turning Machines (Turning Center), Swiss Type Automatic Lathes (Sliding Head Lathes), Multi-Tasking Machines (Mill Turn Machines), Other | |

| By Workpiece Detail | P Steel, M Stainless Steel, K Cast Iron, N Non-Ferrous Metals, S Super Alloys and Titanium, H Hardened Materials, Composites, Plastic, Wood | |

| By End-User | Automotive and Electric Vehicles, Aerospace and Defense, General Machining, Job Shops, Die and Mold, Industrial Machinery, Construction and Agriculture Equipment, Energy and Power Generation, Oil and Gas, Mining, Rail, Marine and Shipbuilding, Electronics and Consumer Appliances, Semiconductor Equipment and Precision Parts, Medical Devices, Dental, Bearing Manufacturing, Others | |

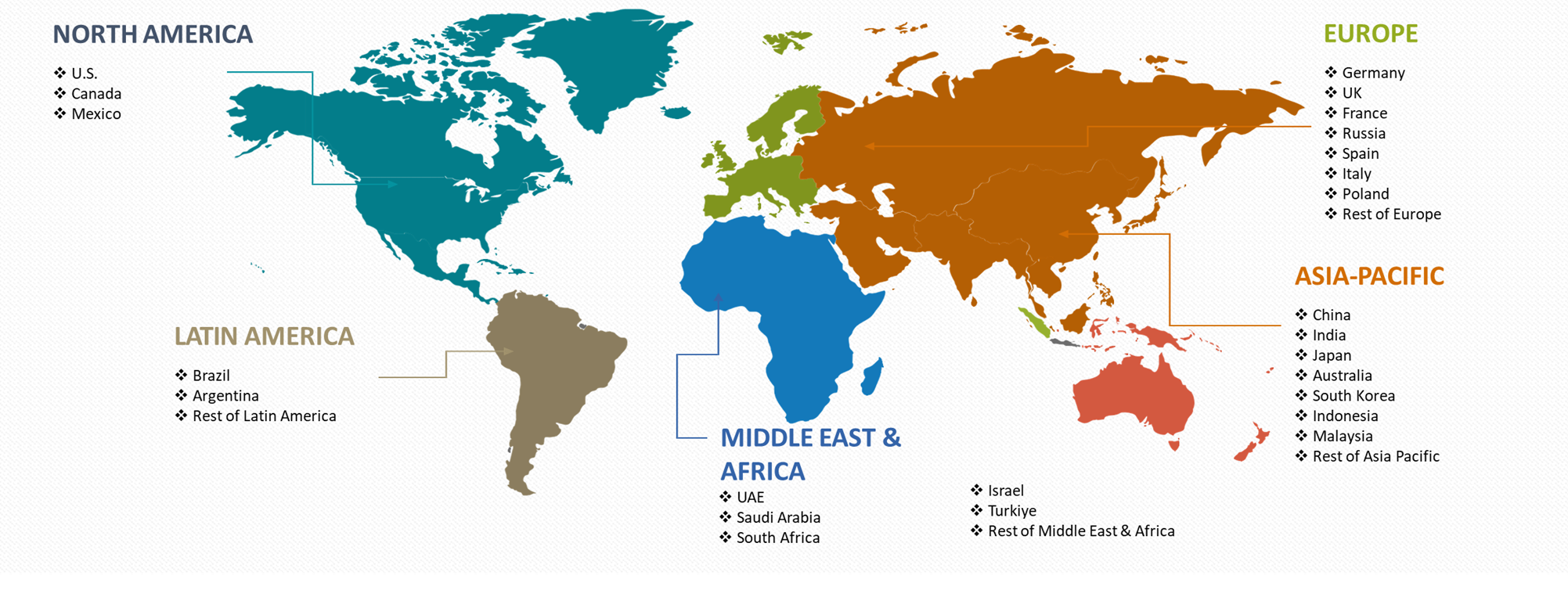

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Disruption Analysis

Leading companies are moving away from conventional tooling vendors to intelligent manufacturing partners by integrating tools that support monitoring and predictive maintenance, cloud-based tooling systems and digital twins into their machining processes. The other important disruption happening now is the rapid development of the aerospace, EV and medical devices industry, which involves machining of titanium, nickel-based alloys, composite and hard metals. It is creating an increased demand for ceramic, CBN, PCD and nanocoated inserts that can handle higher speeds and temperatures. On the other hand, there is aggressive price disruption by low-cost Asian players due to their growth in exports and localized carbide production.

The use of automated systems and unmanned machining cells has changed the buying behavior, too, with customers now showing more interest in complete tooling systems that work with CNC machinery and robotic arms rather than single pieces of equipment. The need for advanced capabilities has led customers to prefer not only tools but also systems that provide analysis of tool life and real-time monitoring of their performance, along with the necessary optimization software. Sustainability issues have also disrupted the traditional manufacturing landscape with an increased focus on recycling of carbide materials, reduced coolant usage, efficient energy machining and tool circularity programs.

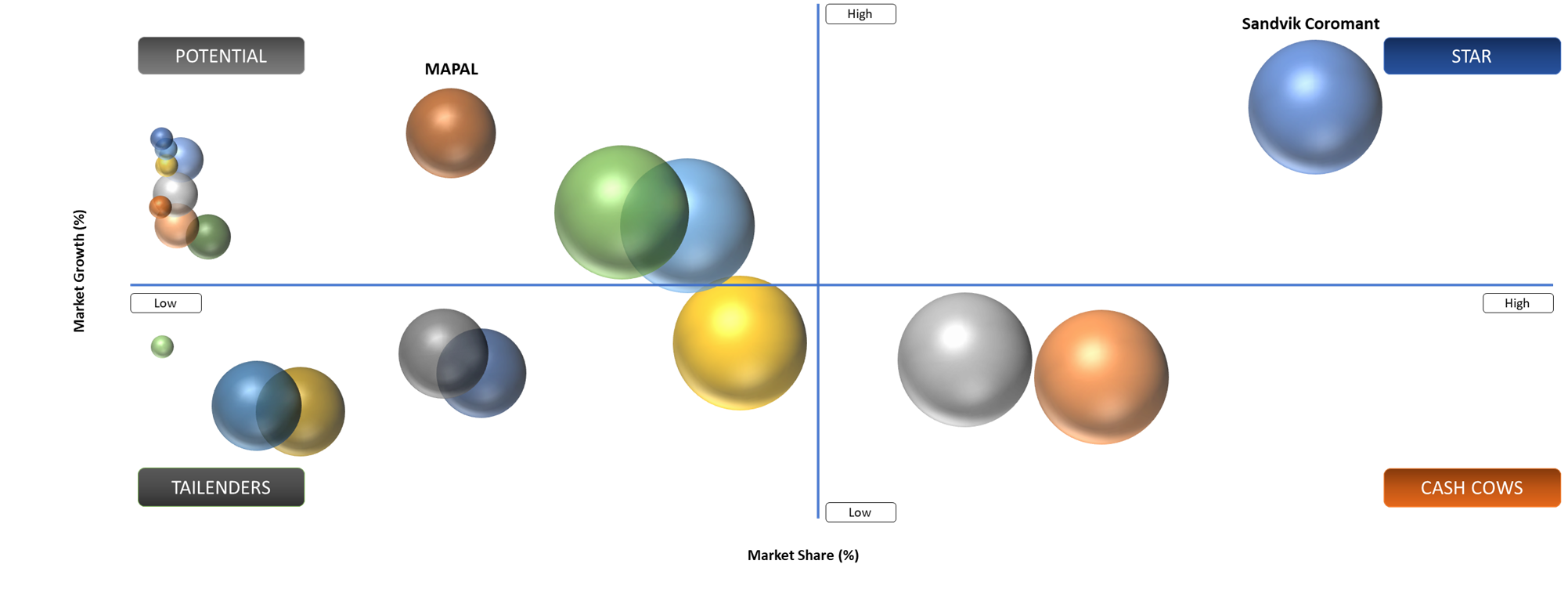

BCG Matrix: Company Evaluation

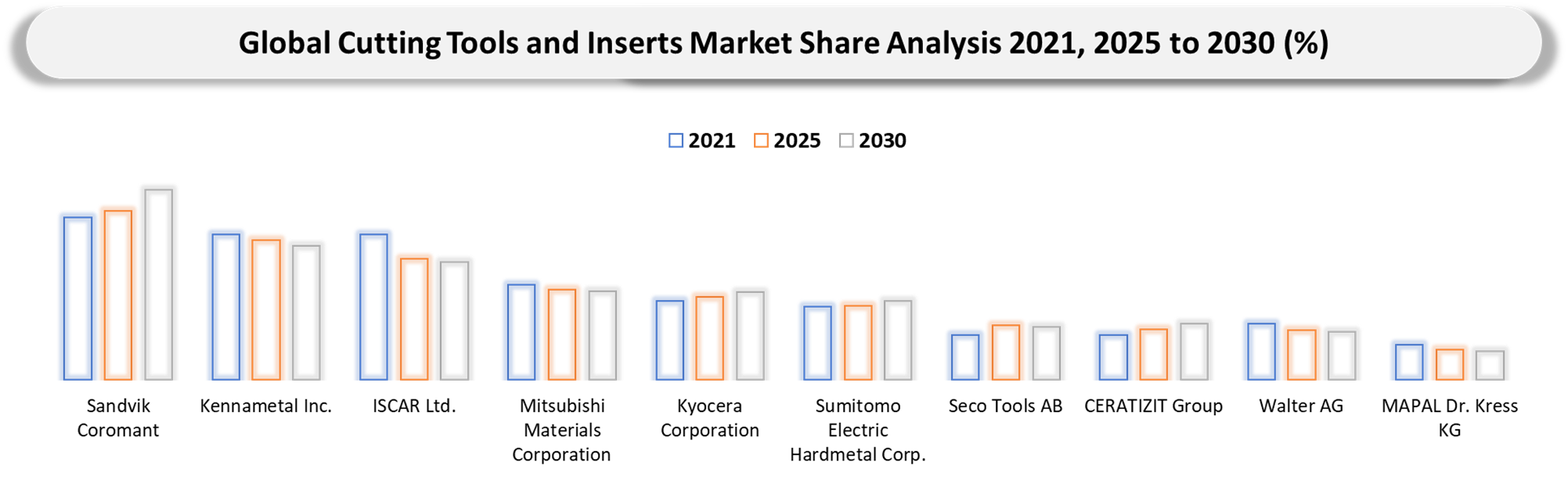

The market is characterized by a high degree of market consolidation and multinational corporations that take different positions in the BCG Matrix, considering their innovativeness, penetration, digitization and regional expansion strategies. Companies such as Sandvik Coromant, Kennametal Inc. and ISCAR Ltd. fall into the category of stars due to high market share, sophisticated carbide and coated inserts product lineups and high investments in Industry 4.0 technologies for operations. Cash Cow companies has relatively steady revenues, achieved due to wide distribution channels and solid OEM relationships, especially in the Asia-Pacific markets of precision engineering.

Market Dynamics

Growing Demand from Automotive and Electric Vehicle Manufacturing

Growth factors such as the rapid growth of automotive manufacturing in general and electric vehicle manufacturing in particular are among the major driving forces behind the global cutting tools and inserts market. High precision in the manufacture of battery housing, electric drives, aluminum parts, transmissions and thermal management systems is one of the requirements made by electric vehicle producers. Cutting tool geometries as well as coatings capable of withstanding high temperatures are essential when manufacturing aluminum and steel hard metals used in electric cars.

According to the International Energy Agency (IEA), there were more than 17 million sales of electric vehicles globally in 2024, demonstrating consistent growth in the production of vehicles that run on electricity. The growth is resulting in significant investments in CNC machine centers and efficient cutting technology. Aerospace and automotive companies are also making additional purchases of carbide inserts and solid carbide tools that can perform at high speeds without vibration and heat dissipation.

High Raw Material Costs and Tool Replacement Challenges

Carbide, tungsten, cobalt, cubic boron nitride and polycrystalline diamond are costly materials associated with changes in their availability resulting from variations in mineral ore production, political instabilities and import/export policies. Material cost increases have a direct effect on the cost of producing tools, thus negatively affecting the profit margins of tool producers and distributors. Further, advanced tools such as the high-performance inserts and tooling systems must be frequently replaced while hard metals and superalloys in extremely challenging conditions. Small and medium-sized factories may experience financial problems in implementing advanced tool technology despite its efficiency, since it results in long-term gains. However, tool reconditioning is currently assisting in addressing some of these costs. Nonetheless, it is difficult to maintain a quality machining process while ensuring long life for the tools. According to AMT and USCTI, there was a slight decrease of 0.6% in cutting tool shipments in the United States in 2025 relative to 2024 due to sluggishness in the manufacturing of transportation and aerospace industries.

Segment Analysis

The global cutting tools and inserts market is segmented based on the form, make, product, tool grade, machine type, workpiece detail, end-user and region.

Carbide Inserts Segment Leads Industrial Adoption

Carbide inserts rule over industrial machining processes because of their high hardness, wear resistance, heat resistance and productivity rates. Carbide inserts are widely employed in processes, including turning, milling, drilling and boring in automotive, aerospace, heavy industry, oil and gas and general metal manufacturing sectors. New carbide inserts featuring multiple layers like TiAlN, TiCN and Al2O3 coatings have increased the speed and durability of carbide cutting tools in machining environments.

With the growing adoption of automated systems and unmanned production operations, the market is witnessing an increasing need for indexable carbide inserts that can maintain dimensional accuracy even when subjected to long hours of machining processes. In the case of the aerospace industry, companies involved in the machining process of titanium engine parts and nickel alloys require high-performance carbide and ceramic inserts to achieve high-speed cutting. Several prominent tool manufacturers are focusing on researching innovative tools, including nano-coating and artificial intelligence-enabled tool paths optimization techniques.

Aerospace and Defense Applications Accelerate Precision Machining Demand

The aerospace and defense industry is among the fastest-growing consumer markets for cutting tools and inserts owing to growing aircraft production, defense modernization initiatives and the growing need for lighter materials. Machining of aircraft engine parts, landing gear assemblies, turbine blades and other structures require specific machining operations using titanium alloys, composite materials, stainless steel and high-temperature resistant superalloys.

AMT’s U.S. Manufacturing Technology Orders Report states that there was an increase in the demand for machine tools in the aerospace industry to a record high level within three years during December 2024. Increasing use of high-feed rate mills, PCD tools and five-axis machining is seen by aerospace OEMs and Tier-1 aerospace suppliers to increase efficiency and ease the manufacturing process. Increased defense expenditure by the U.S., European countries, India and East Asian nations is also driving the purchase of special-purpose tooling systems in the manufacturing of military aircraft, naval vessels, missiles and armaments.

Geographical Penetration

U.S. Cutting Tools and Inserts Market Trends

The growth in investments in manufacturing operations, aerospace modernization projects, electric vehicles production capacities and government policy to enhance industrial activities in advanced technologies is fueling the growth in the U.S. cutters and inserts market. There have been massive investments in manufacturing operations and precision engineering facilities under programs like the CHIPS and Science Act and the Inflation Reduction Act, especially in semiconductor fabrication, aerospace systems, the automotive industry and electric vehicle manufacturing, which need high-performance carbide inserts, milling tools, drilling equipment and advanced operations.

The NIST also indicated increasing investment in machining facilities using the latest Industry 4.0 machining operations, including CNC systems, digital twins and advanced tool monitoring technologies. The aerospace industry also continues to generate demand for machining operations, with Boeing projecting deliveries of about 43,000 commercial aircraft worldwide over the next two decades and this will drive demand for titanium and nickel alloys machining inserts. The U.S. Department of Energy also mentioned additional investments in manufacturing electric vehicle batteries and drivetrains that need machining operations for aluminum housing and motor shafts, among other components.

According to the Association for Manufacturing Technology (AMT), U.S. demand for machine tools continued to grow in 2024, especially for multi-axis CNC equipment and machining centers capable of handling high-speed metal cutting operations. Moreover, the U.S. automobile industry produced about 10.6 million units of motor vehicles in 2024 based on data from OICA, which would result in higher demands for hard-wearing cutting tools and tooling systems suitable for use in production processes.

At the same time, additive manufacturing is creating new possibilities through the adoption of hybrid machining involving the use of 3D printing techniques alongside subtractive operations. The U.S. Department of Defense has also intensified its procurements of difficult-to-cut aerospace and defense platform equipment, thus boosting the adoption of coated carbide, ceramic, CBN and PCD machining tools. Lastly, sustainability practices are also driving tool design as manufacturers now favor environmentally friendly machining, such as the use of dry machining and recycling cutting materials to meet set sustainability benchmarks in North American industries.

Japan Cutting Tools and Inserts Market Trends

Japan continues to be one of the major centers of production of cutting tools and inserts due to its leadership in the development of automotive technology, robotics, semiconductor equipment manufacturing and ultraprecision machining technologies. The support within Japan’s industrial framework is needed for high-quality cutting tools because of their usage in advanced manufacturing industries such as automotive, electronics and industrial machinery.

The Machinery Orders Index and Factory Automation Investments have been on an upward trend throughout 2024 as per data provided by Japan’s Ministry of Economy, Trade and Industry (METI), driven by growing demand for precision equipment and robotics systems. Japan is well known for its proficiency in ultrahard cutting material, micro-machining tool bits and nano-precision insert technology, which find wide application in semiconductor manufacturing and aerospace industries. The Japan Machine Tool Builders' Association (JMTBA) has noted high export demand for Japan’s CNC machines from Southeast Asia and North America.

The Japanese manufacturing companies are interested in hard-to-cut materials like titanium alloys, carbon fiber composite materials and heat-resistant superalloys used in aerospace engines, medical products and electric vehicles. According to JETRO, industrial firms in Japan made significant investments in manufacturing equipment for semiconductors and advanced electronics in 2024, driving up the demand for ultrasonic micro-cutting tools and precision inserts.

Robotics represents yet another key market driver, with IFR estimating that Japan ranks among the top countries in global industrial robot manufacturing. Manufacturing electric vehicles and machining of their components will drive the market towards lightweight material cutting tools and thermal resistance coatings. Furthermore, efforts by Japanese manufacturers to become more environmentally sustainable are encouraging the development of inserts with extended life, reduced material waste and efficient machining. In addition, there has been an increase in the development of advanced insert coatings, including TiAlN and diamond-like coatings, for enhanced speed and machining performance in large-volume industrial machining processes.

China Cutting Tools and Inserts Market Trends

China stands out as the biggest manufacturing economy across the globe and still maintains its position as a leading center for the supply of cutting tools and inserts because of its large industrial manufacturing, automation adoption and investments in high-tech manufacturing. China’s leading position in manufacturing automobiles, electronics, aerospace products, heavy equipment and consumer electronic devices has led to a rise in demand for carbide inserts, milling cutters, drills and machining tools.

The National Bureau of Statistics of China showed that production levels were growing in China in 2024, specifically in advanced equipment manufacturing and electronics production industries. China maintained its position as the world’s biggest car manufacturer, producing about 31 million cars in 2024 as reported by OICA, resulting in increased demand for advanced cutting operations and precision tools. Government-driven initiatives like Made in China 2025 have accelerated modernization and investments in CNC machine centers, robots, aerospace and semiconductor manufacturing. Furthermore, the China Machine Tool & Tool Builders’ Association has noted growing demand for intelligent machining tools.

Expansion in semiconductor manufacturing, EV battery manufacturing and renewable energy infrastructure has been identified as some of the growth sectors that will drive demand for ultra-hard cutting tools and coated inserts in China. For instance, according to the IEA, China has continued to dominate investment into the manufacturing of renewable energy components and batteries throughout 2024. The trend is expected to create machining needs for wind turbines, solar power equipment and EV drivetrains.

The deployment of industrial robots continues to increase as well. According to the International Federation of Robotics, China leads the world in industrial robot purchases and deployment. As more manufacturers embrace robotic technology, there will be increased demand for automated monitoring of tools, predictive maintenance technologies and other smart technologies. Chinese firms are increasingly incorporating advanced coating technologies, such as chemical vapor deposition and physical vapor deposition technologies, in their machining operations. In addition, the expanding aerospace sector and growing commercial aircraft manufacturing efforts are placing higher demands on machining operations dealing with difficult materials such as titanium alloys, hardened steels and composite materials.

Competitive Landscape

- The global cutting tools and inserts market is highly competitive and characterized by the presence of multinational tooling manufacturers specializing in carbide tools, indexable inserts, precision machining systems and advanced tooling materials.

- Key market participants include Sandvik Coromant, Kennametal Inc., ISCAR Ltd., Mitsubishi Materials Corporation, Kyocera Corporation, Sumitomo Electric Hardmetal Corp., Seco Tools AB, CERATIZIT Group, Walter AG and MAPAL.

- Companies compete based on cutting performance, coating technologies, tool life, digital machining integration, customization capabilities and global distribution networks.

Strategic priorities increasingly include AI-enabled machining optimization, sustainable tooling materials, additive manufacturing compatibility, advanced coatings and cloud-connected tool management systems to improve productivity and reduce manufacturing costs across industrial operations.

MAJOR PAIN POINTS

- Volatility in Raw Material Prices: Fluctuating prices of tungsten, cobalt, carbide and high-speed steel significantly increase manufacturing costs and pressure profit margins for cutting tool and insert manufacturers.

- Supply Chain Disruptions & Material Shortages: Dependence on globally sourced raw materials and components creates risks from geopolitical tensions, export restrictions, logistics bottlenecks and transportation delays.

- High Competition & Price Pressure: Intense competition from regional and low-cost Asian manufacturers forces companies to reduce prices, impacting profitability and differentiation strategies.

- Rapid Tool Wear in Advanced Materials Machining: Machining aerospace alloys, hardened steels, composites and titanium increases tool wear rates, reducing tool life and increasing replacement frequency.

- Skilled Labor Shortages in Precision Machining: Lack of trained CNC machinists, tooling specialists and automation engineers limits efficient tool utilization and advanced manufacturing adoption.

- Increasing Demand for High-Precision Manufacturing: End-use industries such as aerospace, EVs and medical devices require ultra-precision machining, compelling manufacturers to invest heavily in R&D and advanced tooling technologies.

- Rising Adoption Costs of Smart & Automated Manufacturing: Integration of Industry 4.0 technologies, AI-enabled machining, IoT monitoring and automated tool management systems requires substantial capital investments and digital expertise.

- Environmental & Sustainability Compliance Pressure: Manufacturers face stricter regulations related to carbide recycling, hazardous material disposal, reduced coolant usage and carbon emission reduction targets.

- Counterfeit & Low-Quality Tool Penetration: Availability of low-cost counterfeit inserts and cutting tools impacts brand reputation, customer trust and market pricing structures.

Demand Uncertainty Across End-Use Industries: Slowdowns in automotive, industrial machinery, construction and energy sectors directly impact tooling demand, creating inventory and capacity planning challenges for manufacturers.

KEY DEVELOPMENTS

- January 2026: OSG Corporation launched upgraded indexable tooling solutions supporting high-speed machining requirements across semiconductor, automotive and industrial equipment manufacturing sectors.

- November 2025: Sumitomo Electric Hardmetal Corp. released advanced CBN insert grades for hardened-steel machining applications, improving surface finishing consistency and extending operational tool life.

- October 2025: Walter AG introduced Tiger·tec gold insert technologies supporting higher machining speeds, increased process security and superior heat-resistant alloy performance.

- October 2025: LMT Tools Group expanded additive-manufacturing technologies, improving customized insert development capabilities and production flexibility for industrial machining customers.

- October 2025: Sandvik Coromant expanded CoroMill MS20 with GC1230 inserts, improving steel shoulder-milling productivity, dimensional accuracy, wear resistance and machining stability.

- September 2025: ISCAR Ltd. expanded its LOGIQ tooling portfolio with advanced carbide inserts supporting aerospace machining efficiency, higher feed rates and process reliability.

- August 2025: Seco Tools AB expanded its recycled-carbide cutting tool program, strengthening sustainable insert production and circular-economy initiatives across European manufacturing operations.

- June 2025: Mitsubishi Materials Corporation introduced next-generation carbide grades for difficult-to-cut materials, enhancing wear resistance, thermal stability and tool life performance.

- May 2025: Kennametal Inc. invested strategically in Toolpath Labs, integrating AI-driven CAM optimization with cutting-tool engineering expertise for manufacturing productivity improvements.

March 2025: Kyocera Corporation expanded its high-feed milling insert lineup, targeting automotive and industrial machining applications requiring precision, productivity and longer tool durability.

ANALYST VIEW / OPINION

- Rising aerospace production and electric vehicle manufacturing are accelerating demand for ultra-precision cutting tools and high-performance carbide inserts capable of machining lightweight alloys, titanium and composite materials with tighter tolerances.

- Advanced coatings such as TiAlN, SCD diamond and nano-coatings are becoming critical competitive differentiators by improving tool life, thermal resistance and machining efficiency in high-speed industrial operations.

- Smart manufacturing adoption is increasing integration of IoT-enabled tool monitoring systems, allowing manufacturers to reduce downtime, optimize tool replacement cycles and improve predictive maintenance capabilities.

- Asia-Pacific continues to dominate global consumption due to expanding automotive, electronics and industrial machinery production bases, particularly across China, India, South Korea and Southeast Asia.

- Shift toward multi-axis CNC machining and automated production environments is driving preference for customized inserts and precision-engineered tooling solutions with higher operational flexibility.

- Sustainability initiatives in metalworking industries are encouraging the adoption of recyclable tool materials, dry machining technologies and energy-efficient cutting processes to reduce industrial waste and coolant usage.

- Volatility in tungsten carbide, cobalt and specialty metal prices remains a major operational challenge, pushing manufacturers toward material optimization strategies and alternative tooling compositions.

- Additive manufacturing growth is creating new opportunities for specialized finishing and post-processing cutting tools designed for complex geometries and high-strength engineered components.

- Industrial reshoring trends across North America and Europe are supporting investments in advanced machining infrastructure, strengthening long-term demand for premium cutting tools and inserts.

- Intense competition is encouraging manufacturers to expand digital tooling platforms, application engineering services and customized machining solutions to strengthen customer retention and operational value delivery.

TARGET AUDIENCE

| INDUSTRY | WHO SHOULD BUY THIS REPORT? | REASON TO BUY THIS REPORT |

| Automotive & Electric Vehicle Manufacturers | Manufacturing Engineering Teams, CNC Machining Managers and Procurement Heads | Analyze tooling demand for EV components, lightweight materials and precision machining operations. |

| Aerospace & Defense Companies | Aerospace Manufacturing Engineers, Production Heads, Supply Chain Teams | Evaluate advanced cutting solutions for titanium, superalloy and composite material machining |

| Industrial Machinery Manufacturers | Plant Operations Managers, Industrial Engineering Teams, Production Planning Departments | Optimize machining productivity, tooling efficiency and operational performance |

| Metal Fabrication & General Engineering Companies | Fabrication Managers, CNC Programmers, Workshop Supervisors | Identify cost-efficient cutting tools and inserts for high-volume metal processing |

| Die & Mold Manufacturing Companies | Tool Room Managers, Precision Machining Teams, Product Development Engineers | Assess high-precision tooling technologies for mold making and finishing applications |

| Oil & Gas Equipment Manufacturers | Heavy Machining Teams, Reliability Engineers and Procurement Departments | Understand wear-resistant tooling demand for harsh industrial machining environments |

| Energy & Power Generation Companies | Turbine Manufacturing Teams, Plant Engineering Departments, Strategic Sourcing Teams | Evaluate tooling requirements for critical power generation equipment manufacturing. |

| Construction & Agriculture Equipment Manufacturers | Production Managers, Industrial Operations Teams, Manufacturing Engineers | Analyze durable tooling solutions for heavy-duty machining applications |

| Mining Equipment Manufacturers | Machining Operations Teams, Maintenance Departments and Procurement Managers | Identify high-performance cutting inserts for abrasive and large-scale machining operations |

| Rail & Marine Equipment Manufacturers | Production Engineering Teams, Fabrication Managers, Supply Chain Departments | Track machining technologies for transportation and heavy engineering components |

| Medical Device Manufacturers | Precision Manufacturing Teams, Quality Assurance Managers, R&D Departments | Study ultra-precision cutting solutions for miniature and complex medical components. |

| Electronics & Semiconductor Equipment Manufacturers | Advanced Manufacturing Teams, Automation Engineers, Product Development Teams | Evaluate micro-machining and precision tooling trends for electronic components. |

| CNC Machine Tool Manufacturers | Product Strategy Teams, Automation Specialists, Business Development Managers | Identify collaboration opportunities and tooling integration trends. |

| Cutting Tool & Insert Manufacturers | Product Innovation Teams, Competitive Intelligence Departments, Sales Strategy Teams | Benchmark competitor offerings, coating technologies and material advancements |

| Carbide, Ceramic & Coating Material Suppliers | Technical Sales Teams, Market Intelligence Departments, R&D Teams | Analyze future demand for advanced tooling materials and coatings |

| Industrial Automation & Smart Manufacturing Companies | Industry 4.0 Teams, Smart Factory Engineers, Automation Consultants | Evaluate integration of cutting tools with automated machining systems |

| Industrial Distributors & Supply Companies | Category Managers, Regional Sales Teams, Inventory Planning Departments | Understand regional demand trends and optimize tooling product portfolios |

| Contract Manufacturing & Job Shops | Business Owners, CNC Workshop Managers, Production Supervisors | Identify profitable machining segments and tool investment opportunities |

| Research Institutions & Universities | Manufacturing Research Teams, Industrial Engineering Faculties, Material Science Researchers | Analyze emerging machine technologies and advanced manufacturing trends |

| Government & Defense Organizations | Industrial Development Authorities, Defense Manufacturing Units, Railway Workshops | Support strategic manufacturing modernization and industrial capability development |

| Investors & Private Equity Firms | Investment Analysts, Industrial Sector Consultants, Strategy Advisory Teams | Evaluate investment opportunities, competitive landscape and industrial growth potential |

| Consulting & Advisory Firms | Market Intelligence Teams, Strategy Consultants, Industrial Analysts | Support client benchmarking, market entry strategies and competitive analysis |

WHY CHOOSE DATAM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.