Industrial AI Copilots Market Size & Growth

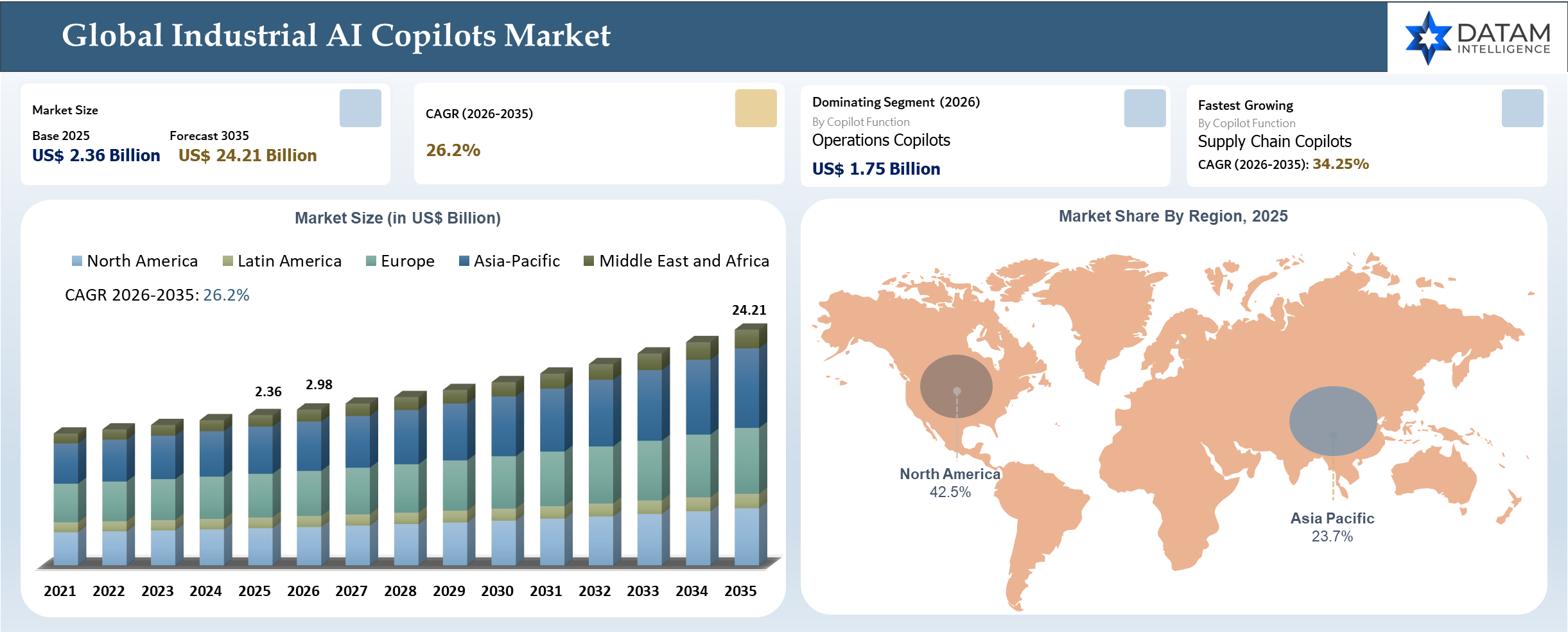

The global Industrial AI Copilots market reached US$ 2.36 billion in 2025 and is expected to reach US$ 24.21 billion by 2035, growing with a CAGR of 26.20% during the forecast period 2026-2035. The industrial AI copilot is one of the quickly growing markets in the world of industrial artificial intelligence and digital transformation, which has resulted in a combination of the latest developments in generative AI technologies, industrial automation solutions, and enterprise software.

Adoption trends further reinforce the structural importance of this market. Enterprise-level data from 2025-2026 indicates that AI copilots are transitioning from pilot deployments to scaled implementations, with average enterprise adoption rates reaching around 30 to 38% of licensed users actively using copilot systems within 90 days, and leading organizations achieving adoption rates as high as 65–78%.

Industrial AI Copilots Industry Trends and Strategic Insights

- A significant transformation that can be observed in the industrial AI copilot ecosystem includes its shift towards intelligence through the use of edge technologies. This change reflects the requirement for fast decision-making that can be provided by utilizing edge computing for immediate analysis of the situation in the factories.

- Key players in the field of industrial automation such as Siemens AG and Schneider Electric have started integrating generative AI copilots into OT environments to support various tasks. This process leads to turning traditional automation tools into the decision-making ecosystem enhanced by AI.

- The development of semiconductor hardware optimized for AI is enhancing the industrial copilot ecosystem. Such organizations have already begun to release chips that allow for inference and real-time industrial analytics. Thus, copilots are enabled to process large amounts of data locally.

- It becomes increasingly obvious that there is an emerging connection between the industrial copilot market and advanced connectivity infrastructure. For example, telecom operators collaborate with industrial platform suppliers to enable copilots to operate in an environment based on 5G-enabled industrial network infrastructure.

Industrial AI Copilots Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 2.36 Billion | |

| 2035 Projected Market Size | US$ 24.21 Billion | |

| CAGR (2026-2035) | 26.20% | |

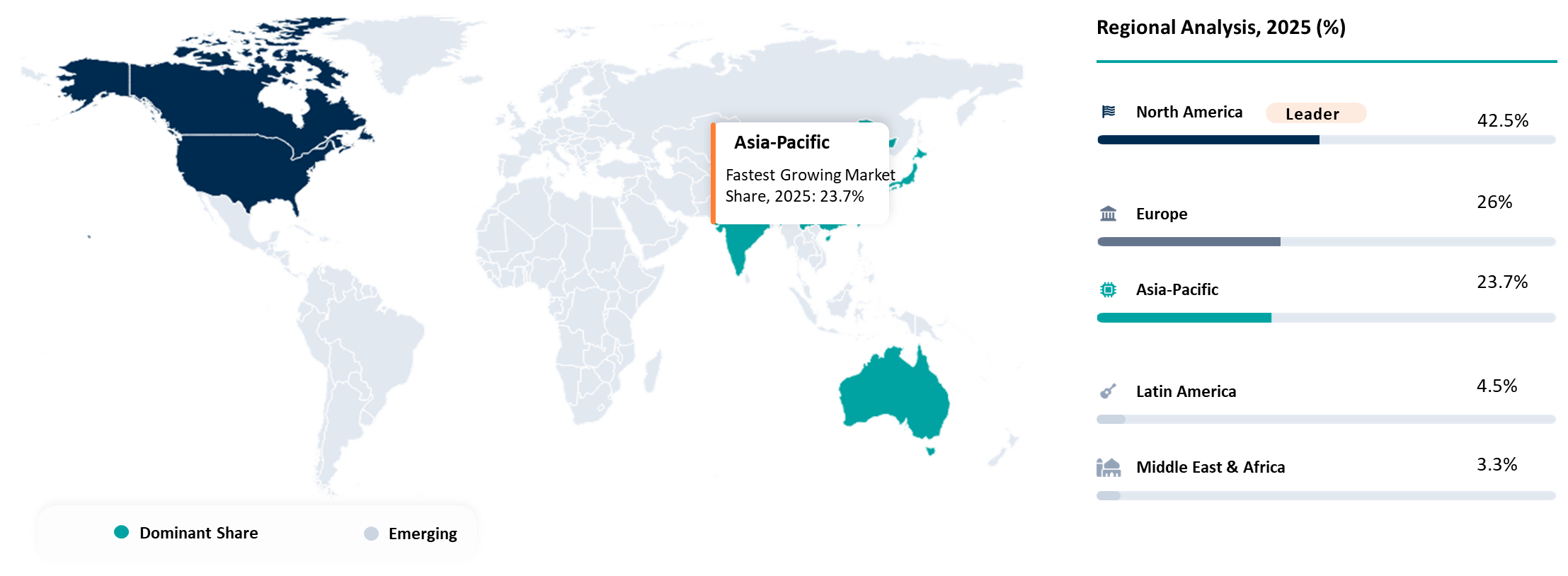

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Copilot Function | Operations Copilots, Maintenance Copilots, Engineering Copilots, Supply Chain Copilots, Others | |

| By Deployment | On-Premises, Cloud-Based | |

| By Integration Type | Standalone Copilot Platforms, Embedded Copilot, Copilot-as-a-Service | |

| By Pricing Model | Subscription (SaaS) Copilots, Perpetual License Copilots, Usage-Based or Outcome-Based Models, AI + Services Bundled Model | |

| By Organization Size | Large Enterprises, Small & Medium Enterprises (SMEs) | |

| By End-Use Industry | Manufacturing, Energy and Utilities, Logistics and Warehousing, Construction and Infrastructure, Semiconductor and High-Tech, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Disruption Analysis

Shift from Rule-Based Automation to Agentic AI Copilots Transforming Industrial Decision-Making Systems

The industrial AI copilot market is currently experiencing a paradigm shift due to the rapid adoption of advanced AI algorithms to replace traditional automation and rule-based decision-making. Unlike industrial legacy software that operates using logic-based rules, copilots use advanced AI to understand unstructured information, make decisions based on learning processes within operations, and suggest actions in context. This means that current automated workflows will be revolutionized, thus reducing the need for specialized human intervention, as well as increasing operational efficiency.

The second disruption that will significantly influence the market is the transformation towards an ecosystem model of integration and interoperability of AI technologies. Copilots will be able to run in various environments including cloud computing, on-premise solutions, as well as edge computing platforms. This is a huge step towards the convergence of IT and operational technologies through seamless communication and real-time operation in industrial environments. The market will see an increase in competitive pressure amongst platform vendors, semiconductor vendors, and industrial automation firms fighting for their share of the stack.

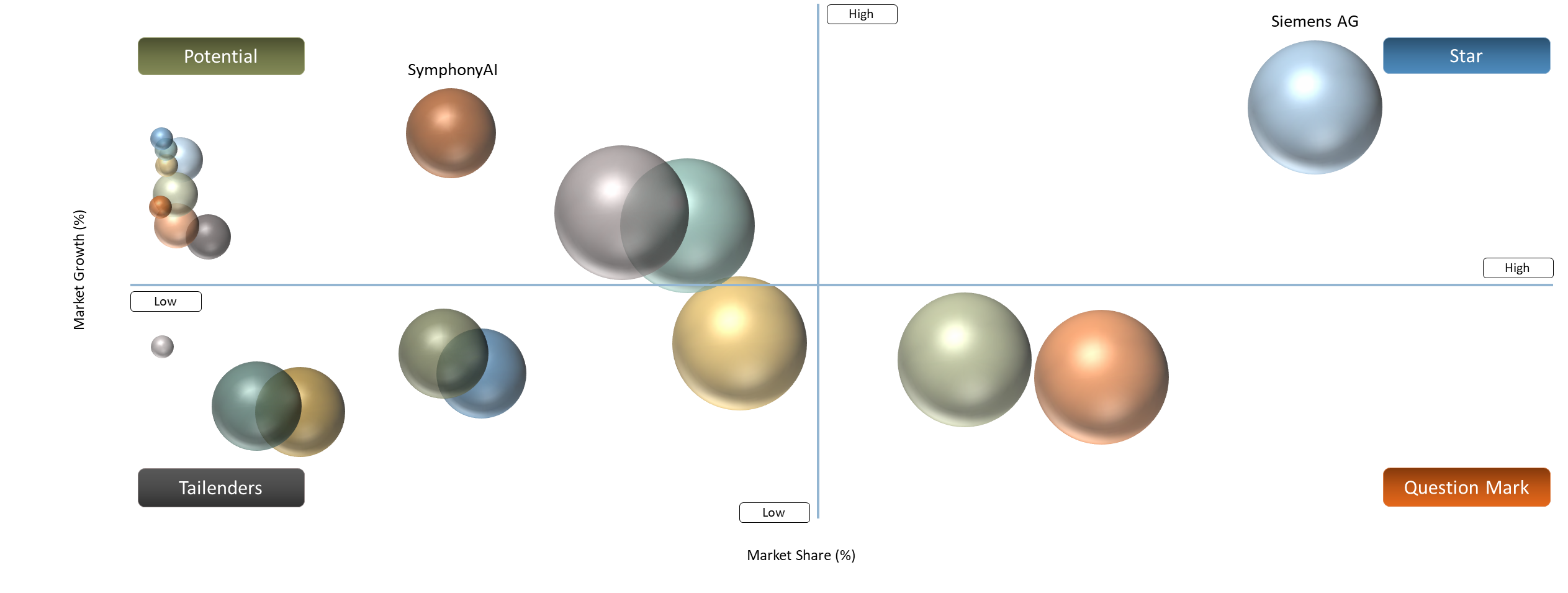

BCG Matrix: Company Evaluation

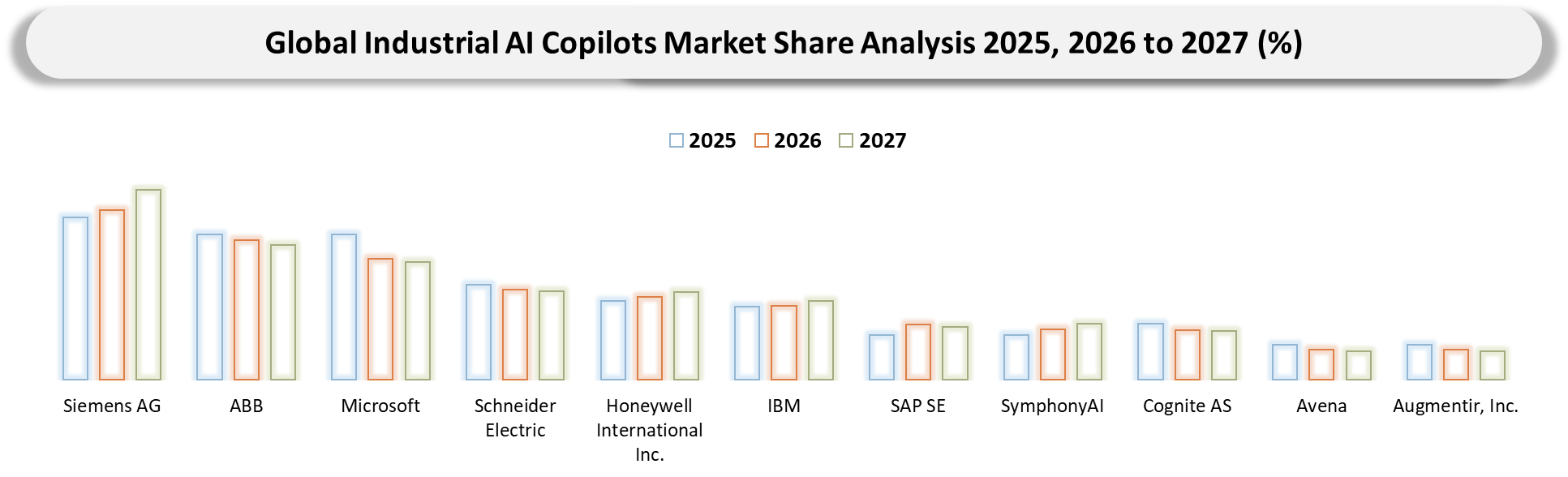

Evaluating portfolios based on market leadership and growth alignment, Siemens AG and Microsoft stand out due to their capacity to provide comprehensive industrial AI copilot ecosystems and platforms. In second place come Schneider Electric and Honeywell International Inc., who build their market leadership and growth strategies based on their strong presence in the industrial automation sector but gradually introduce AI copilots into operations. IBM and SAP SE also have their markets covered through enterprise software and further AI-enabled industrial processes that ensure continued growth momentum.

Concurrently, in terms of portfolio evaluation opportunities in a high-growth segment, SymphonyAI, Cognite AS, Augmentir, Inc., and Avena show promising growth potential through their innovative technologies that facilitate industrial AI copilot solutions despite lower market penetration rates. The areas in which these companies can potentially expand include connected workers' platforms, industrial data intelligence, and operational AI. On the other hand, ABB can be considered a company that bridges both segments by being firmly rooted in the industrial automation industry and building up its capacities regarding AI solutions.

Industrial AI Copilots Market Dynamics

Rising Cost of Downtime & Need for Predictive Maintenance

The growing expenses related to downtime have become structurally quantifiable factors contributing to faster AI copilot implementation in manufacturing maintenance and operations. According to recent data from the manufacturing industry, the expense of downtime is estimated at USD 1.4 trillion each year for global manufacturers, accounting for 11% of total revenue, while costs per incident may vary between USD 25,000 and 2.3 million depending on the industry .

Overall, more than 61% of all surveyed manufacturers suffered from an unplanned stoppage within the last year, generating total losses amounting to USD 852 million per week . Predictive maintenance based on the use of AI copilots has proved its ability to provide savings of 30 to 50% downtime and 18 to 25% in terms of maintenance costs based on the estimates provided by McKinsey. Such tangible expenses have forced companies to prioritize investment in AI assistance within maintenance activities, thus making industrial AI copilots vital tools for businesses..

Data Quality and Availability Issues

The efficiency and scalability of industrial AI copilots have been highly limited by the existing problem of low data quality and availability. Data in the industrial environment are usually scattered in different legacy systems and have inconsistencies in sensor calibrations and missing historical data, which affect the accuracy of the analysis based on machine learning algorithms.

According to research, more than 80% of industrial companies are not able to correctly estimate their expenses associated with downtime. At the same time, predictive maintenance requires a steady stream of time series data. Any problems with its availability and poor quality will make it impossible for the algorithm to generate accurate recommendations and failure forecasts. Although firms are trying to fill this gap through IoT and data solutions, the lack of standards for industrial data makes this process complicated and costly.

Industrial AI Copilots Market Segmentation Analysis

The global Industrial AI Copilots market is segmented based on copilot function, deployment, integration type, pricing model, organization size, end-use industry and region.

Operations Copilots Driving Market Dominance Through Real-Time Process Optimization and Continuous Industrial Deployment

The operations-based sector still remains the dominant player in the AI copilot market among other segments in the industrial applications of AI due to its ability to integrate seamlessly into real-life production processes, increasing their speed and efficiency and reducing costs. The nature of engineering and supply chain AI copilots, which are used occasionally or during preproduction planning, does not allow them to be utilized as often as operations-oriented copilots, which are incorporated in the continuous flow of processes and can be used by control room personnel, manufacturing execution systems, and process optimization layers.

According to industrial benchmarks, real-time process optimization and operational analytics help increase production efficiency by up to 20 to 30% and lower energy consumption by 15 to 20%. This applies mainly to the chemical, metal, and energy-intensive manufacturing industries. Companies like Siemens AG and Honeywell International Inc. have focused on integrating their AI copilots into continuous operations through distributed control systems and plant-level software.

Industrial AI Copilots Market Geographical Penetration

North America Leading Industrial AI Copilot Adoption Through Enterprise AI Investment and Advanced Digital Infrastructure

North America is the most developed market for industrial AI copilots, thanks to substantial investments in enterprise AI and cloud ecosystem advancements. The leading country in this region, the United States, is characterized by the development of manufacturing under the CHIPS and Science Act with more than USD 52 billion invested in semiconductor capacity expansion. As a result, there is an increase in demand for AI engineering and operations copilots in valuable industries through policy-induced growth. The adoption of industrial AI is additionally motivated by efficiency improvements between 20% and 30% in operations according to the International Energy Agency.

The regional dominance is enhanced by technological suppliers like Microsoft and Amazon Web Services providing AI copilot solutions through cloud computing and edge platforms. There are also instances where industrial companies, such as Honeywell International Inc., integrate AI assistants in control systems to enhance decision-making at the factory level. Canada contributes to the environment with its national AI initiatives, such as over CAD 2 billion funding within the Pan-Canadian AI Strategy framework..

U.S. Industrial AI Copilots Market Trends

United States holds dominance in the regional market due to large industrial investments and active participation of the private sector. Over 50 industrial projects worth more than USD 200 billion related to semiconductors have been reported. This leads to growing need for AI-powered operations tools such as industrial copilots. As a result, the usage of AI-based copilots becomes prominent in manufacturing, logistics, and energy industries.

Advanced digital infrastructure and widespread cloud adoption facilitate the implementation of copilots in the region. The International Energy Agency claims that AI and digital technologies have become popular to optimize energy use and operations in the industry. Nonetheless, some challenges arise in implementing copilots due to integration difficulties and issues associated with data security. Usage levels differ by sector, with automated sectors being advanced adopters of the technology, whereas others lag behind in implementation.

Canada Industrial AI Copilots Market Outlook

Canada is becoming a developing market because of the existence of well-supported government-led AI ventures and innovative industrial applications. For instance, the Pan-Canadian Artificial Intelligence Strategy involves more than CAD 2 billion worth of investments in efforts to accelerate the deployment of AI in the manufacturing and extraction industry sectors. The government backing will compel the companies to deploy AI copilots to make sure that they predict maintenance issues and optimize processes. Significant industrial sectors like mining and energy generation are beginning to leverage AI to boost efficiency and reduce risks.

The industrial infrastructure, coupled with growing digital adoption, makes Canada an ideal environment for adopting AI copilots. However, the country still trails the United States in terms of industrialization levels. There is inadequate data on the degree of AI copilot utilization in Canada's industrial firms.

Industrial AI Copilots Market Competitive Landscape

- The competitive landscape is defined by a mix of industrial automation leaders and AI platform providers, where companies like Siemens AG, ABB, and Schneider Electric leverage strong installed bases to embed AI copilots into operational systems. Technology firms such as Microsoft, IBM, and SAP SE focus on scalable, cloud-driven copilot platforms through partnerships and ecosystem expansion. Meanwhile, players like SymphonyAI, Cognite AS, Augmentir, Inc., and Avena compete through niche, domain-specific solutions and faster innovation cycles. Overall, competition centers on platform integration, data ownership, and the ability to deliver measurable industrial outcomes.

- Key players include Siemens AG, ABB, Microsoft , Schneider Electric, Honeywell International Inc., IBM, SAP SE, SymphonyAI, Cognite AS, Avena, Augmentir, Inc.

Key Developments in Industrial AI Copilots Market

- May 2025: Siemens AG expanded its Industrial Copilot with generative AI-powered predictive maintenance capabilities, extending AI support across engineering, operations, and service lifecycle to improve maintenance efficiency and reduce reactive downtime.

- May 2025: Siemens AG introduced a new generation of Industrial Copilot capabilities through AI agent enhancements designed to automate industrial workflows and improve productivity across manufacturing and engineering environments.

- May 2025: Schneider Electric showcased an industrial copilot developed with Microsoft Azure AI at Automate 2025, integrating generative AI into software-defined automation systems to enhance productivity and workforce efficiency in manufacturing operations.

- February 2025: Honeywell launched an AI-powered assistant designed to support industrial operations, enabling predictive insights, operational guidance, and improved decision-making in process industries through its digital operations platform.

- May 2024: IBM introduced enhanced Microsoft Copilot capabilities aimed at integrating generative AI into enterprise workflows, enabling AI-driven business transformation across supply chain and manufacturing-related operations.

- April 2026: Schneider Electric unveiled next-generation agentic manufacturing capabilities powered by Microsoft Azure AI at Hannover Messe 2026, introducing industrial copilot-driven workflows that integrate engineering, commissioning, and operations into a unified AI-enabled manufacturing system.

- April 2026: Siemens showcased advanced industrial AI systems at CES 2026, highlighting expanded Industrial Copilot applications and AI-driven automation technologies aimed at accelerating industrial transformation across the manufacturing value chain.

Why Choose DataM?

- Technological Innovations: Explores advancements in industrial AI copilots, including generative AI integration, natural language interfaces, edge AI deployment, digital twin connectivity, and real-time decision engines. These innovations are enabling autonomous recommendations, improved process optimization, predictive maintenance accuracy, and seamless interaction between human operators and complex industrial systems.

- Product Performance & Market Positioning: Evaluates how different vendors perform across manufacturing, energy, logistics, and semiconductor environments. The analysis compares parameters such as response accuracy, integration depth with MES/ERP systems, scalability, latency in edge environments, and contextual decision-making capabilities, highlighting how leading providers differentiate through platform ecosystems and domain expertise.

- Real-World Evidence: Highlights practical use cases of industrial AI copilots across smart factories, predictive maintenance, supply chain optimization, and energy management. It demonstrates measurable outcomes such as reduced downtime, improved asset utilization, enhanced workforce productivity, and faster decision-making across industrial operations.

- Market Updates & Industry Changes: Tracks key developments such as product launches, expansion of AI copilots into engineering and operations workflows, partnerships between industrial firms and cloud providers, and increasing adoption of edge AI architectures. It also captures regulatory and policy influences supporting industrial digitalization across major regions including North America, Europe, and Asia-Pacific.

- Competitive Strategies: Analyzes how leading companies are strengthening their market position through platform integration, partnerships with hyperscalers, vertical-specific AI solutions, and expansion of industrial software ecosystems. Strategies also include embedding copilots into existing automation systems and leveraging proprietary industrial data for differentiation.

- Pricing & Market Access: Explains pricing structures across subscription-based (SaaS), usage-based, and bundled AI-plus-services models. It also reviews enterprise adoption patterns, cloud versus on-premise preferences, and go-to-market strategies including direct sales, partner ecosystems, and platform-based distribution.

- Market Entry & Expansion: Identifies growth opportunities driven by increasing adoption in SMEs, expansion into emerging markets, and rising demand for AI-driven operational efficiency. It outlines strategies such as localized partnerships, industry-specific solutions, and scalable deployment models to accelerate global market penetration.

Target Audience

- Manufacturing & Industrial Enterprises: Automotive manufacturers, process industries, electronics producers, and discrete manufacturing firms deploying AI copilots for operations, maintenance, and engineering optimization.

- Energy & Utilities Companies: Power generation firms, oil & gas operators, and renewable energy providers utilizing AI copilots for asset monitoring, predictive maintenance, and grid optimization.

- Logistics & Supply Chain Operators: Warehousing companies, third-party logistics providers, and distribution networks leveraging AI copilots for demand forecasting, inventory optimization, and route planning.

- Technology & Industrial Software Providers: Companies developing industrial platforms, automation systems, and AI solutions seeking integration capabilities and competitive intelligence.

- Government & Industrial Authorities: Regulatory bodies, smart manufacturing initiatives, and public sector agencies supporting Industry 4.0 adoption and digital transformation programs.

- Investors & Private Equity Firms: Investment groups tracking growth in industrial AI, enterprise software, and digital transformation technologies across global markets.

- System Integrators & Consulting Firms: Firms involved in deployment, customization, and integration of industrial AI copilots across enterprise environments.

Related Reports

AI agents for IT operations and industrial AI copilots both leverage autonomous AI to automate complex workflows, improve decision-making, and reduce manual intervention. Organizations are increasingly deploying intelligent AI assistants to optimize infrastructure, maintenance, and enterprise operations. The rapid evolution of agentic AI is accelerating adoption across industrial and IT environments.

AIOps platforms provide the intelligent analytics, automation, and observability capabilities that complement industrial AI copilots. By combining predictive analytics with real-time operational insights, organizations can minimize downtime and improve system performance. Growing adoption of AI-driven enterprise automation is fueling demand across both markets.

Artificial intelligence serves as the core technology behind industrial AI copilots, enabling predictive maintenance, process optimization, natural language interaction, and autonomous decision support. Continuous advancements in generative AI, machine learning, and foundation models are expanding industrial AI applications. Enterprises are rapidly integrating AI into manufacturing and industrial operations to improve productivity.

Industrial AI copilots rely on IIoT sensors and connected devices to collect real-time operational data from manufacturing equipment and production lines. This continuous flow of industrial data enables AI copilots to deliver predictive insights, anomaly detection, and intelligent recommendations. Increasing Industry 4.0 adoption is strengthening demand for IIoT-enabled AI solutions.

Edge AI enables industrial AI copilots to process production data locally, reducing latency and supporting real-time operational decisions. Local AI inference improves factory automation, predictive maintenance, and equipment monitoring while minimizing dependence on cloud connectivity. The convergence of edge computing and industrial AI is accelerating smart manufacturing initiatives.

Cloud infrastructure provides the scalable computing environment required for industrial AI copilots to analyze operational data, manage digital twins, and deploy AI models across manufacturing facilities. Hybrid and multi-cloud deployments allow enterprises to scale AI-powered industrial automation efficiently. Increasing cloud adoption is supporting next-generation industrial AI platforms.

Industrial AI copilots continuously analyze sensitive operational, production, and engineering data, making robust cybersecurity essential. Big data security solutions protect industrial AI systems through encryption, access control, and AI-powered threat detection. As industrial environments become more connected, securing AI-driven operations is becoming a strategic priority.

Industrial AI copilots are becoming a key component of smart manufacturing by assisting engineers, operators, and maintenance teams with real-time recommendations and workflow automation. These AI-powered assistants improve production efficiency, reduce downtime, and enhance workforce productivity. Increasing investments in digital factories continue to drive adoption.

Industrial automation systems increasingly integrate AI copilots to support production planning, machine optimization, quality inspection, and maintenance operations. AI-driven automation improves operational efficiency while enabling human workers to make faster, more informed decisions. The continued adoption of Industry 4.0 technologies is creating significant growth opportunities for both industrial automation and AI copilots.