Zero Trust Security Market Overview

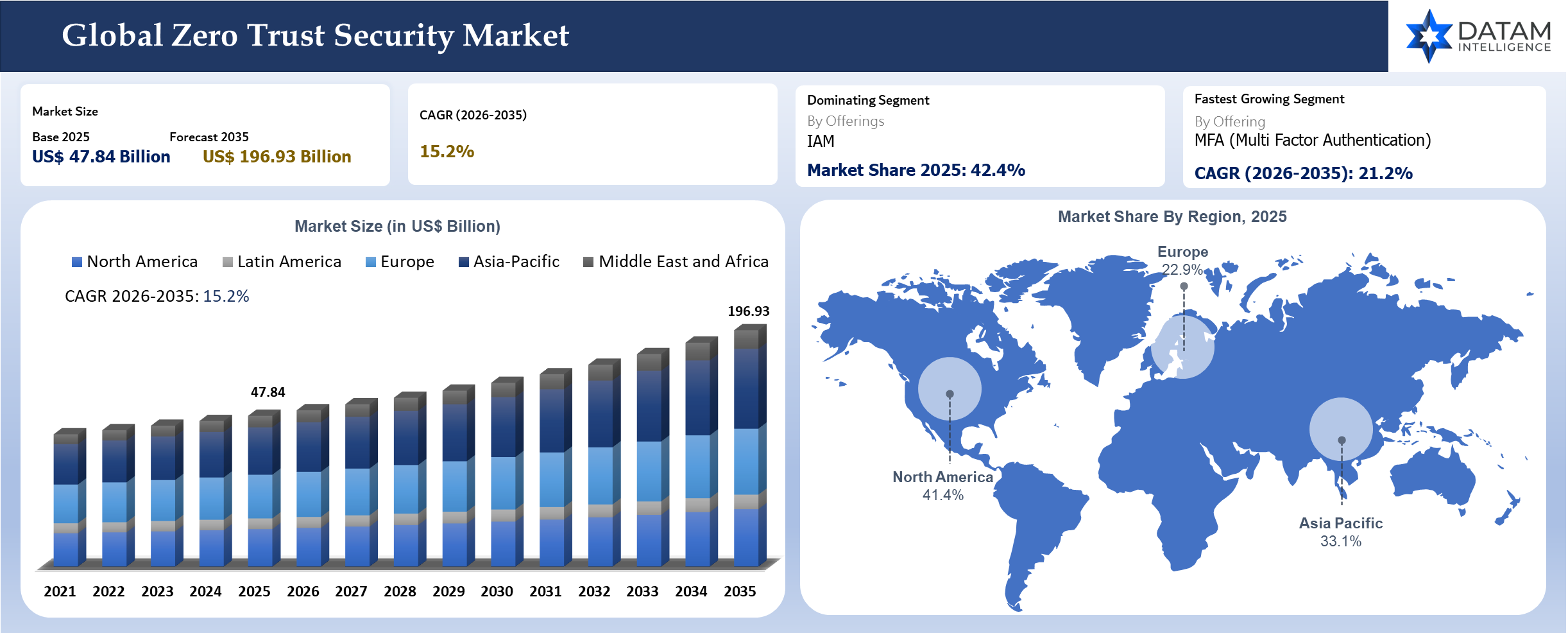

The global zero trust security market was valued at US$ 47.84 Billion in 2025 and is expected to reach US$ 196.93 Billion by 2035, growing at a CAGR of 15.2% during 2026 to 2035. Enterprise security spending is moving away from perimeter-heavy infrastructure toward identity-led access control, continuous device verification, cloud workload protection and policy-driven security operations. Large organizations are no longer treating VPN replacement as the only commercial driver. Security teams are now buying broader programs that combine ZTNA (Zero Trust Network Access), IAM (Identity and Access Management), PAM (Privileged Access Management), endpoint posture, data protection, cloud security, micro segmentation and analytics into enterprise security architecture.

The strongest demand is coming from organizations with multi-cloud environments, distributed branches, third party access needs, regulated data and hybrid workforce models. Financial institutions, government agencies, healthcare networks, telecom providers and manufacturers are prioritizing identity governance and privileged access control because attackers increasingly use valid credentials rather than only malware payloads.

NIST SP 800-207 frames the shift clearly by moving defenses from static network perimeters toward users, assets and resources. NIST also highlights that authentication and authorization for subjects and devices should happen before access to enterprise resources is established.

Executive Summary

- The market is entering a platform consolidation phase. Vendors are combining network access, identity security, cloud security, endpoint telemetry and analytics into unified commercial offers. Buyers still purchase individual tools but board-level security programs now require integration across policy, identity, device health, workload access and data visibility.

- Identity has become the commercial center of gravity. Microsoft’s 2024 Digital Defense Report states that its customers face more than 600 million cybercriminal and nation-state attacks every day and Microsoft Entra data shows password-based attacks account for more than 99 Percent of daily identity attacks.

- Government policy is strengthening enterprise demand. OMB memorandum M-22-09 required U.S. federal agencies to meet specific Zero Trust security goals by the end of FY 2024 and organized the federal path around identity, devices, networks, applications and workloads and data.

Key Takeaways

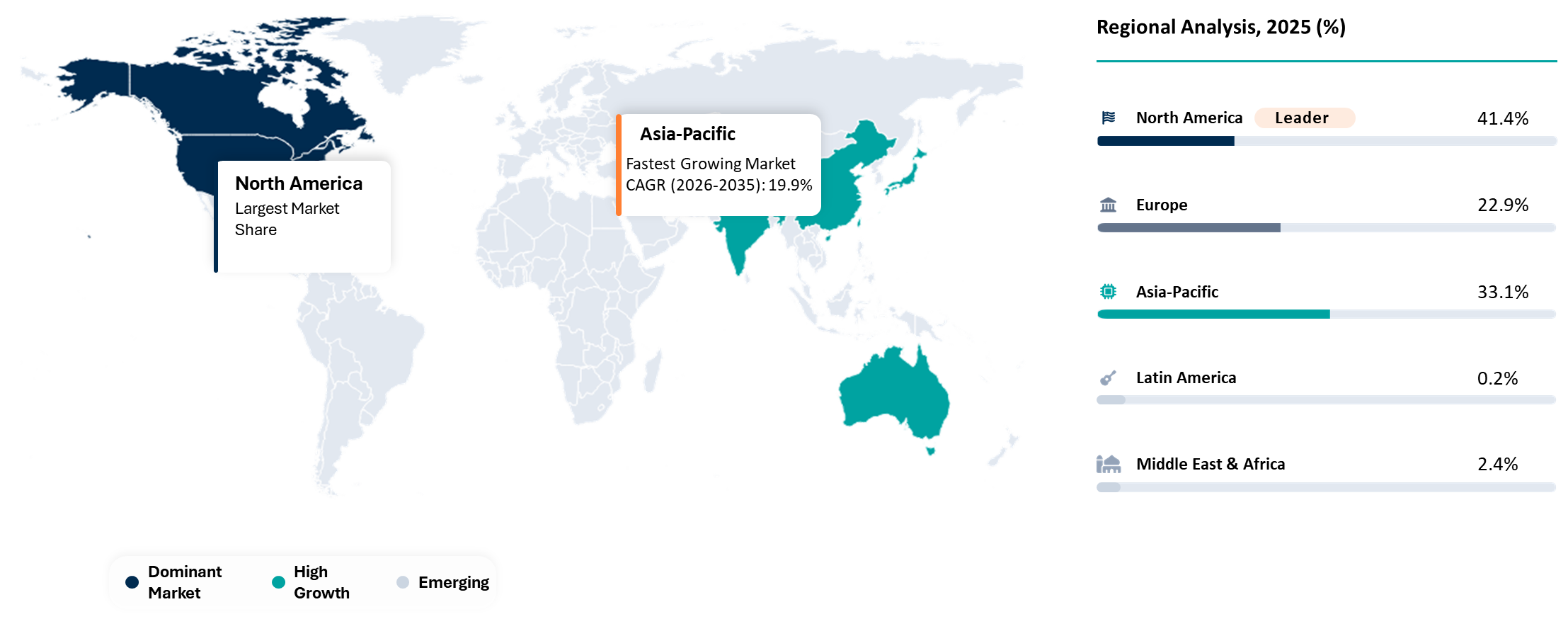

- North America accounted for 41.4% of the global market in 2025, supported by high enterprise cybersecurity spending, federal security modernization programs, strong cloud adoption and large-scale identity security deployments across BFSI, healthcare, government and technology enterprises.

- Asia-Pacific held 33.1% market share in 2025 and remains the strongest long-term expansion region. Japan, India, South Korea, Australia, Singapore and China are increasing spending on cloud security, IAM (Identity and Access Management), PAM (Privileged Access Management), SASE (Secure Access Service Edge), SSE (Security Service Edge) and managed security services.

- Europe represented 22.9% of the global market in 2025, driven by GDPR, NIS2, DORA and national cyber resilience priorities. Demand is strongest across banking, insurance, manufacturing, healthcare, telecom and government-linked organizations.

- Middle East and Africa accounted for 2.4% of the global market in 2025. UAE, Saudi Arabia, South Africa, Nigeria, Ghana, Kenya, Côte d’Ivoire and Senegal are becoming more relevant for identity-led security, secure branch access, cloud workload protection and managed cybersecurity services.

- South America accounted for 0.2% of the market in 2025, with Brazil, Chile and Argentina representing the most visible enterprise demand pockets. Adoption remains concentrated among financial institutions, telecom operators, digital retail platforms and large public sector modernization programs.

- IAM (Identity and Access Management) remains the leading spending anchor because enterprises are prioritizing SSO (Single Sign On), MFA (Multi Factor Authentication), IGA (Identity Governance and Administration) and ITDR (Identity Threat Detection and Response) to reduce credential misuse orphaned accounts and excessive access permissions.

- Managed Security Services are gaining stronger commercial traction as mid-sized enterprises and regional financial institutions look for managed ZTNA (Zero Trust Network Access), managed IAM, MDR (Managed Detection and Response) and managed policy operations rather than building large in-house security teams.

Zero Trust Security Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 47.84 Billion | |

| 2035 Projected Market Size | US$ 196.93 Billion | |

| CAGR (2026-2035) | 15.2% | |

| Largest Region | North America, 41.4% Market Share in 2025 | |

| Fastest Growing Region | Asia-Pacific | |

| By Offerings | Solutions: ZTNA (Zero Trust Network Access), IAM (Identity and Access Management), PAM (Privileged Access Management), Endpoint Security, Data Security, Network Security and Micro Segmentation, Cloud Security, Security Analytics and Policy Orchestration, Other Zero Trust Solutions Services: Consulting and Advisory, Enterprise Architecture Design and Roadmap, Integration and Deployment, Managed Security Services, Training and Education, Support and Maintenance, Other Zero Trust Services | |

| By Deployment Mode | Cloud, On Premises, Hybrid | |

| By Primary Enterprise Architecture Model | Standalone ZTNA (Zero Trust Network Access), SSE (Security Service Edge) Based Zero Trust, SASE (Secure Access Service Edge) Based Zero Trust, Identity Centric Zero Trust, Network Micro Segmentation Led Zero Trust, Cloud Workload Zero Trust, Enterprise Multi Pillar Zero Trust, Others | |

| By Primary Use Case | Remote Workforce Secure Access, Third Party and Vendor Access, Branch and Site Secure Access, Cloud Workload Access, Privileged Access To Critical Systems, Data Protection and Governance, OT (Operational Technology) and IoT (Internet of Things) Access Control, Others | |

| By Enterprise Size | SMEs (Small and Medium Enterprises), Large Enterprises | |

| By Distribution Channel | Direct Sales, Distributor Led Sales, VAR (Value Added Reseller) and SI (System Integrator) Led Sales, MSSP (Managed Security Service Provider) Led Sales, Cloud Marketplace Sales, Other Indirect Sales | |

| By End-User | BFSI (Banking, Financial Services and Insurance), IT (Information Technology) and Telecom, Healthcare, Government and Defense, Retail and E Commerce, Manufacturing, Energy and Utilities, Education, Transportation and Logistics, Others | |

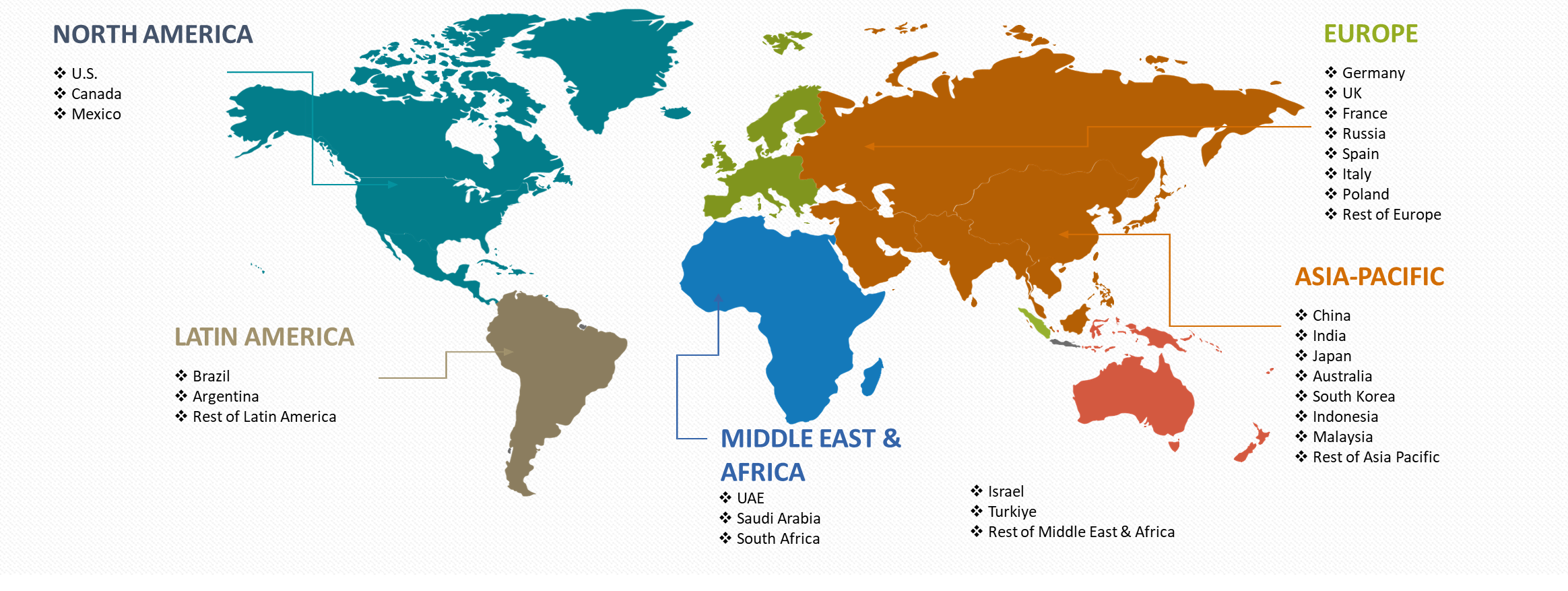

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Why This Report Matters in 2026

Enterprise security buyers enter 2026 with higher pressure to modernize access control without disrupting daily operations. Cybersecurity teams are no longer evaluating Zero Trust as a narrow VPN replacement project because identity misuse, unmanaged devices, cloud workloads, third party access and privileged accounts now sit at the center of enterprise risk. Procurement teams need a clearer view of which offerings matter first, where platform consolidation can reduce tool overlap and how service partners can support implementation across complex hybrid environments.

Enterprise architecture teams are also facing a practical execution challenge. Security leaders must choose between standalone ZTNA, SSE based Zero Trust, SASE based Zero Trust, identity centric Zero Trust, network micro segmentation led Zero Trust, cloud workload Zero Trust and enterprise multi pillar Zero Trust models. Each model carries different implications for legacy infrastructure, branch connectivity, cloud migration, user experience, application access and long term operating cost. A strong market view helps buyers compare architecture pathways instead of treating every Zero Trust program as a single technology purchase.

Zero Trust implementation is becoming more outcome driven as boards and regulators expect measurable progress around access governance, privileged account control, sensitive data protection and threat response. BFSI, government, healthcare, telecom, manufacturing and energy organizations need reliable benchmarks on vendor portfolios, country opportunity, use case priority, channel routes and managed service fit. The report supports clients in identifying where demand is moving, which vendors are best positioned and which implementation priorities should be addressed first to reduce security exposure while improving enterprise resilience.

Strategic Indicators For Zero Trust Security

High Regulation Impact

Regulatory influence is high because public sector guidance has made access modernization a practical requirement. U.S. federal policy created a clear model around identity, devices, networks, applications and data while NIST SP 800-207 gave enterprises a common reference language for architectural planning. Financial regulators, healthcare privacy rules and critical infrastructure guidance are also pushing organizations to prove user authentication, privileged access control, encryption, logging and third party access governance. Compliance pressure is not only increasing product demand; it is also changing procurement scoring. Buyers now ask vendors for audit evidence, control mapping, policy reporting, data residency support and integration with existing governance workflows. The result is a market where technical functionality and compliance readiness are increasingly evaluated together.

High Investment Activity

Investment activity remains high because security platform vendors are trying to own larger portions of the enterprise control plane. Identity security, AI agent security, non human identity governance, DSPM, cloud workload protection and managed detection remain active investment themes. Platform buyers prefer vendors that can reduce tool fragmentation and provide a coherent roadmap across access, endpoint, cloud, data and analytics. Large vendors are also investing in internal AI capabilities for detection engineering, automated policy recommendation, alert triage and user behavior analysis. Smaller firms with strong identity analytics, machine identity security, agent access control or automated micro segmentation capabilities are attractive acquisition targets because they solve gaps that broad platforms still struggle to address.

Recent Mergers and Funding

- Palo Alto Networks announced its intent to acquire CyberArk for identity security expansion and privileged access control depth.

- Okta announced the acquisition of Axiom Security to strengthen privileged access controls across cloud, SaaS and database environments.

- Saviynt raised growth capital to scale identity governance and access management capabilities for human and non-human identities.

New Product Launches

- Cloudflare One expanded its SASE and Zero Trust coverage around workforce access, AI agents, infrastructure and application security. Cloudflare positions its platform as a unified control plane for ZTNA, CASB, SWG, network services, DLP and email security.

- Okta expanded its product portfolio around IAM, adaptive MFA, device access, PAM, ITDR, IGA and AI agent identity coverage.

- CyberArk continued to broaden identity security around workforce access, SSO, MFA, PAM, endpoint privilege management, secrets management, certificate management and workload identity.

- Microsoft continued to position Entra, Defender, Sentinel and Intune as integrated pillars for identity, endpoint, cloud and analytics driven security architecture.

- Zscaler continued to advance Zero Trust Exchange capabilities across secure access, data protection, workload connectivity and AI-driven security operations.

Supply Chain Disruption

Software supply chain disruption is pushing more organizations toward stricter access policies for developers, contractors, service accounts and CI (Continuous Integration) pipelines. Attackers increasingly target build systems, secrets, package repositories and third party software access because one compromised identity can affect many downstream users. Security buyers are responding by prioritizing secrets management, endpoint privilege management, workload identity, developer access governance and session recording. Supply chain pressure is also changing vendor selection. Buyers are asking for SBOM (Software Bill of Materials), secure development practices, vulnerability disclosure programs, tenant isolation controls and stronger audit trails. Procurement teams no longer evaluate access products only by features; they evaluate vendor resilience and operational transparency.

Procurement Pressure

Procurement teams are applying stronger pressure because CISOs need measurable reduction in tool overlap. Many enterprises already have firewalls, VPNs, SIEM, endpoint tools, identity platforms, cloud security tools and DLP products. Budget approval now depends on whether a new platform can retire legacy tools, reduce incident response effort, improve audit evidence or simplify branch security. Vendor evaluation is becoming more outcome-based. Buyers ask about time to deploy, directory integration, application onboarding speed, policy migration, managed service support and total cost over three to five years. Procurement pressure favors vendors with transparent bundles, strong partner ecosystems and clear migration playbooks.

New Technology Adoption

AI is changing the product roadmap for access security. Vendors are adding AI-assisted policy recommendations, anomaly detection, automated investigation summaries, identity risk scoring and natural language security operations. Enterprise buyers are also preparing for AI agents that can access internal systems, retrieve sensitive documents, trigger workflows and interact with external applications. The next commercial wave will focus on non-human identity governance and agent access control. Security teams will need to verify agent identity, constrain permissions, log every action and revoke access quickly. Cloudflare’s positioning around securing AI agents and MCP server connections reflects how fast access architecture is expanding beyond human users.

Regional Expansion Opportunity

Regional expansion opportunities are strongest in Asia-Pacific, the Middle East and Africa and selected South American countries where cloud adoption and digital public services are expanding faster than mature security staffing. Banking, telecom, insurance, healthcare and government digital platforms are creating demand for cloud delivered security and managed services. Local compliance, data residency and reseller networks are important success factors. Vendors that offer sovereign cloud options, local support, regional data centers and MSSP partnerships can convert demand faster than vendors selling only centralized enterprise contracts. Regional banks and insurers are likely to prioritize managed IAM, managed ZTNA and incident response integrated with security operations.

Government Policy Support

Public sector policy has become a strong market catalyst. OMB M-22-09 created specific U.S. federal goals around enterprise-managed identities, phishing-resistant MFA, device inventory, encrypted traffic, application testing and data categorization.

NIST SP 800-207 provides the architecture language used by many private and public organizations. The document emphasizes no implicit trust based on network location and positions resource protection as a central goal.

Government guidance is also influencing private sector procurement because regulated industries often align with public frameworks. Buyers increasingly request maturity models, policy roadmaps, audit mappings and implementation plans that align with NIST, CISA, ISO and sector-specific requirements.

Pricing Intelligence

Commercial pricing is primarily subscription based. IAM, ZTNA, SASE, SSE and endpoint capabilities are commonly sold per user per month while cloud workload security, CSPM, CWPP and DSPM may use workload, asset, data volume or cloud account pricing. SIEM and security analytics may rely on data ingestion, event volume or capacity tiers. Managed services are typically priced per user, endpoint, monitored account, protected workload or monthly retainer.

Enterprise contracts often bundle software, integration, advisory services and support. Larger buyers negotiate multi-year discounts and cloud marketplace private offers. Mid-market buyers often select MSSP-led sales because managed operations reduce internal staffing pressure. Pricing sensitivity rises when vendors bundle several features that buyers already own from another provider.

Cloud marketplace sales are becoming more relevant because buyers can use existing cloud commitments from AWS, Microsoft Azure and Google Cloud. Marketplace procurement can shorten contracting cycles but may limit flexibility when future scope changes require different modules or usage tiers.

AI Impact Analysis

AI is affecting demand on two sides of the market. Security vendors are using AI to improve detection, identity risk scoring, alert triage and policy automation. Buyers are using AI assistants and internal automation tools that require controlled access to applications, data and workflows. Both trends increase demand for stronger identity governance and fine-grained authorization.

AI agents create a new class of access risk. A human user may access one application at a time but an agent can interact with multiple systems quickly and repeatedly. Traditional access models are not designed to decide whether an agent should read a claim file, trigger a payment workflow, query a customer database or summarize regulated data. Security architecture must evolve toward context-aware authorization and complete action-level logging.

AI also increases social engineering and phishing risk. Microsoft’s threat reporting already shows scale across phishing and identity attacks. Strong MFA, phishing-resistant authentication, conditional access and ITDR are becoming essential because AI tools can help attackers create more convincing messages and automate credential attack campaigns.

Disruption Analysis

VPN replacement remains an important disruption theme but it is no longer the only one. Security buyers are now replacing broad network access with application-level access, device posture checks and identity-aware policies. Branch security is also changing as SASE and SSE reduce dependency on on premises appliances and MPLS-based routing.

SIEM and SOAR purchasing is also being disrupted. Enterprises want analytics that connect identity behavior, endpoint telemetry, network access and cloud events in one workflow. Traditional log collection is not enough when attackers move through legitimate sessions and stolen tokens.

Data protection is shifting toward posture management and governance rather than only DLP at the network boundary. DSPM and encryption controls are gaining relevance because sensitive data is spread across SaaS applications, cloud storage, databases and collaboration tools. A security program cannot protect data effectively without knowing where it is stored and who can access it.

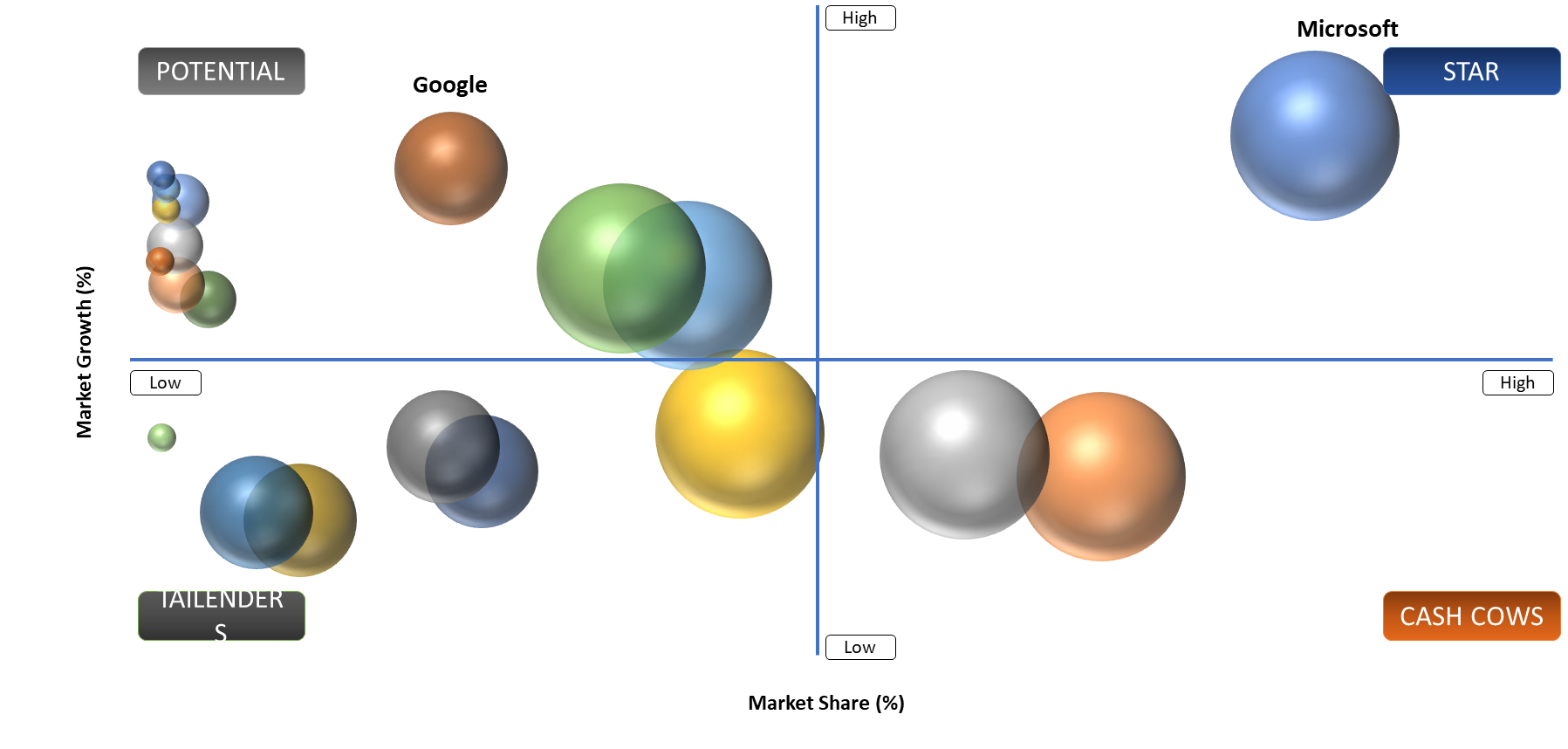

BCG Matrix: Company Evaluation

Stars

Microsoft, Palo Alto Networks, Zscaler, Cloudflare, Cisco and CrowdStrike are positioned as Stars because they combine strong enterprise reach with expanding product coverage. Microsoft benefits from the installed base across Entra, Defender, Sentinel, Intune and Microsoft 365. Palo Alto Networks has broad platform depth across network security, cloud security, Cortex analytics and SASE. Zscaler and Cloudflare have strong cloud-native secure access positioning while Cisco and CrowdStrike bring security operations, identity, endpoint and network telemetry into broader enterprise programs.

Potential

Okta, CyberArk, Netskope, Akamai, Fortinet, Check Point and SentinelOne represent Potential because they hold strong positions in important growth pockets. Okta has depth in identity and access management while CyberArk is highly relevant for privileged access and machine identity. Netskope is well aligned with SSE and data protection. Akamai has enterprise access and application security reach. Fortinet and Check Point have strong installed bases that can support hybrid network security migration while SentinelOne can benefit from endpoint and identity convergence.

Zero Trust Security Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact | Demand Concentration | Impacted Use Case | Strategic Impact |

Identity Sprawl Across Multi Cloud Estates | High impact | BFSI, IT and Telecom, Government and Defense, Healthcare | Data Protection and Governance | Accelerates spending on IAM, IGA, MFA, ITDR and PAM because identity has become the main control point for enterprise security architecture |

VPN Retirement In Regulated Branch Networks | High impact | BFSI, Retail and E Commerce, Government and Defense, Transportation and Logistics | Branch and Site Secure Access | Drives ZTNA and SASE adoption by helping organizations reduce legacy VPN exposure and improve secure access across branches and remote locations |

Privileged Access Exposure In AI Enabled Workflows | Medium to high impact | BFSI, IT and Telecom, Manufacturing, Energy and Utilities | Privileged Access To Critical Systems | Expands demand for PAM, secrets management, endpoint privilege management and session monitoring as enterprises tighten access to critical systems and automation workflows |

Identity Sprawl Is Turning Access Control Into A Board Level Security Priority

Identity sprawl is now one of the strongest commercial drivers for the market. Enterprises run thousands of identities across employees, contractors, developers, service accounts, cloud workloads, APIs, devices and emerging AI agents. A single identity breach can create access to several systems because cloud applications and internal tools often share federated identity paths.

Security teams are spending more on IAM, IGA, ITDR and PAM because business operations now depend on fast access without exposing the organization to privilege abuse. Password reuse, phishing, helpdesk social engineering orphaned accounts and excessive permissions create repeatable attack paths for adversaries. Microsoft’s threat reporting shows the scale of password-based attacks and underlines why buyers are shifting from static authentication to continuous identity protection.

Financial services, healthcare and government buyers are especially exposed because internal users, external partners, auditors, administrators and third party service providers need access to sensitive applications. Identity controls are becoming procurement prerequisites rather than optional add-ons. Budget owners are increasingly asking whether each user, device and workload can be verified before access and monitored during access.

Restraint Impact Analysis

| Restraint | Drag On Market Growth | Primary Impact Area | Impacted Use Case | Strategic Impact |

| Legacy Directory Debt | High | IAM Integration, Access Governance, Application Onboarding | Remote Workforce Secure Access | Increases implementation cost and delays Zero Trust maturity because buyers need directory cleanup, role redesign and phased migration before full policy enforcement |

Policy Overlap Across Security Tools | Medium to high | Tool Consolidation, Policy Governance, Procurement Planning | Data Protection and Governance | Slows procurement decisions because buyers need clarity on which platform owns each policy layer and how new tools reduce rather than add complexity |

Legacy Infrastructure Slows Enterprise Wide Rollout

Legacy systems remain a major restraint because several enterprises still depend on older directories, thick-client applications, branch firewalls, private data centers and VPN-based access models. Security teams may purchase modern platforms but implementation becomes slow when applications cannot support federation, certificate-based access, granular policy control or modern logging.

Migration challenges are larger in banking, insurance, utilities and public sector environments because core systems often run on older platforms with strict uptime requirements. A phased rollout becomes necessary but that increases services cost, change management effort and internal coordination. Deployment can also create operational friction when security teams try to enforce MFA, device checks or least privilege rules across users who were previously granted broad access.

Vendor consolidation can create another implementation challenge. Enterprises often own overlapping capabilities across endpoint security, SIEM, cloud security, IAM and firewall vendors. Procurement teams may want a unified platform but security architects still need to integrate products already embedded in operations. As a result, projects often move slower than vendor sales cycles suggest.

Segmentation Analysis

Identity Security Is Becoming The Commercial Control Point For Enterprise Architecture

IAM (Identity and Access Management) is the most prominent revenue anchor because every major security program starts with who gets access, which device is used, what resource is requested and whether the session remains trustworthy. Enterprises cannot move toward mature access control without SSO, MFA, IGA and ITDR working together.

SSO helps enterprises simplify user access across SaaS, internal applications and cloud portals. Strong SSO programs reduce password fatigue and help centralize policy enforcement. Buyers value SSO when it integrates easily with Microsoft 365, Google Workspace, Salesforce, ServiceNow, SAP, Workday and internal applications. High integration depth is often more important than standalone authentication features because fragmented sign-in flows create helpdesk cost and security blind spots.

MFA is now a baseline requirement rather than a premium feature. Demand is moving toward phishing-resistant authentication, adaptive MFA and device-aware controls. Basic one-time passwords are losing favor in high-risk environments because attackers use fatigue attacks, SIM swap and adversary-in-the-middle tactics. Financial institutions and government agencies are increasingly asking for FIDO-based methods, certificate-based authentication and conditional access tied to device posture.

IGA is gaining weight because organizations need lifecycle control. User onboarding, role changes, access reviews and deprovisioning are now high-risk workflows. Orphaned accounts and excessive entitlements are common sources of breach exposure. IGA demand is especially strong in BFSI, healthcare, government and manufacturing because auditors want evidence of who approved access and why access remains necessary.

ITDR is emerging as an advanced layer inside identity security. Traditional IAM can authenticate a user but may not detect suspicious behavior after access is granted. ITDR focuses on identity infrastructure exposure, risky privileges, abnormal sign-ins, token misuse and compromised accounts. Demand is rising because attackers increasingly target identity systems directly.

SSO (Single Sign On)

SSO creates commercial value by reducing the number of credentials users must remember and by giving security teams a central point for access policy enforcement. Enterprises with hundreds of SaaS applications need SSO because fragmented logins create inconsistent controls and make employee offboarding difficult.

SSO also supports user productivity. A well-integrated access layer allows employees to move across approved applications with less friction while security teams enforce rules in the background. Employee experience matters because overly difficult access processes often push users toward workarounds.

Vendor differentiation in SSO is moving beyond basic login. Buyers evaluate integration catalogs, uptime, adaptive access, conditional policies, admin experience and reporting. Okta’s product portfolio lists Single Sign On, Adaptive MFA, Device Access, API Access Management and Universal Directory under its IAM offerings.

MFA (Multi Factor Authentication)

MFA is the most visible identity control for executives because it directly reduces credential misuse. Phishing-resistant MFA is becoming more important as attackers bypass weaker methods through push fatigue, proxy phishing and stolen session cookies. Enterprises are now looking at stronger factors that support regulated access without creating excessive user friction.

MFA adoption also affects insurance and audit discussions. Cyber insurers often ask whether MFA is applied to privileged accounts, remote access, email, VPN alternatives and cloud administrator roles. A weak rollout can leave gaps even when the product is installed.

Strong MFA programs are increasingly tied to device posture and risk scoring. Access decisions may depend on whether a device is managed, whether the location is expected, whether the user behavior is unusual and whether the requested application contains sensitive data. MFA is no longer only a login step; it is part of continuous access evaluation.

Geographical Penetration

North America Zero Trust Security Market

North America leads because enterprises have mature cloud usage, high security spending and strong regulatory pressure. U.S. federal guidance has shaped private sector buying behavior because agencies and contractors need stronger identity controls, encryption, endpoint visibility and application security. The region also has a dense vendor ecosystem across IAM, PAM, SASE, endpoint, cloud security and managed services.

Enterprise buyers in the region are moving from point projects to platform roadmaps. Security leaders increasingly want fewer tools, faster deployment and better visibility across identity, endpoint and cloud. Demand is especially strong among banks, insurers, healthcare systems, technology companies and government contractors.

U.S. cyber loss data continues to support preventive investment. FBI IC3 reported US$ 16.6 Billion in reported losses in 2024 and phishing, spoofing, personal data breaches, business email compromise and ransomware remained major reported categories.

U.S. Zero Trust Security Market

U.S. demand is driven by federal mandates, cyber insurance requirements, cloud modernization and persistent identity attacks. Public sector procurement favors solutions that map to CISA and NIST maturity models. Private sector buyers often use similar language because boards and audit committees recognize those frameworks.

BFSI, healthcare and technology companies are investing heavily in identity controls. Banks and insurers need secure access for employees, agents, branches, payment partners and claims systems. Healthcare organizations need strict access around patient records, medical devices, remote care platforms and third party billing systems.

U.S. vendors also shape global product direction. Microsoft, Palo Alto Networks, Zscaler, Cloudflare, Cisco, Okta, CrowdStrike and Fortinet influence pricing models, partner programs and product integration standards. Strong domestic vendor presence makes the U.S. a launch market for AI-assisted access security and identity threat protection.

Europe Zero Trust Security Market

Europe is a strong market because of GDPR, NIS2, DORA, banking resilience requirements and strong public sector security programs. Buyers care about data residency, audit evidence, sovereignty and supplier risk. European enterprises are often cautious about broad platform lock-in but remain active buyers of IAM, PAM, ZTNA, SASE and data security.

Germany, France, the UK, Netherlands and Switzerland show strong demand from financial services, manufacturing, healthcare and government. Industrial buyers are increasingly looking at OT and IoT access control because operational systems are becoming connected to enterprise IT.

European procurement favors vendors that can support hybrid environments and local compliance expectations. MSSPs and SIs play a major role because enterprises often need advisory support, migration planning and policy design across complex multi-country operations.

Asia-Pacific Zero Trust Security Market

Asia-Pacific is expected to grow fastest due to cloud expansion, digital banking, telecom modernization, e government programs and rising security awareness. Japan, Australia, India, Singapore and South Korea are strong commercial markets while Southeast Asia is moving toward managed and cloud-delivered models.

Financial institutions and telecom operators are important buyers. Mobile banking, digital wallets, customer onboarding, 5G networks and SaaS adoption increase exposure to credential misuse and data leakage. Regional enterprises often prefer phased rollouts beginning with IAM, MFA and ZTNA before moving into SASE and analytics.

Channel partnerships are critical in Asia-Pacific. Local integrators and MSSPs help global vendors adapt to language, compliance and implementation requirements. Cloud marketplace procurement is also gaining relevance where enterprises already consume Microsoft Azure, AWS and Google Cloud.

Japan Zero Trust Security Market

Japan is a high-quality market because large enterprises value reliability, vendor stability and integration support. Demand is tied to cloud migration, supply chain security, manufacturing digitization, financial services modernization and public sector resilience. Japanese enterprises often prefer structured implementation roadmaps rather than rapid rip-and-replace projects.

Identity and privileged access are key priorities. Japanese manufacturers and financial institutions need secure access for employees, suppliers, plants, cloud workloads and administrative accounts. OT (Operational Technology) connectivity also creates demand for access control that avoids broad network trust.

Local partnerships matter strongly. Global vendors need Japanese language support, local implementation partners, regional compliance alignment and long-term service commitments. Buyers often evaluate proof of deployment quality and operational support more heavily than aggressive feature claims.

Middle East and Africa Zero Trust Security Market

Middle East and Africa represented 2.4% of the global Zero Trust Security Market in 2025, placing the region behind North America, Europe and Asia Pacific in total spending but ahead in several service-led growth pockets. Demand is not evenly distributed. UAE, Saudi Arabia and South Africa account for a large share of enterprise-grade security spending while Nigeria, Ghana, Kenya, Côte d’Ivoire and Senegal are becoming important for BFSI, telecom, public services and digital insurance use cases.

UAE remains one of the most advanced markets in the region because cybersecurity is tied closely to digital government, smart city infrastructure, banking digitization and cloud migration. Large enterprises in Dubai and Abu Dhabi are investing in IAM, PAM, ZTNA, SASE and cloud security to secure hybrid workforces, customer-facing portals and multi-cloud environments. Procurement often favors platform-led solutions with strong compliance mapping, local partner support and managed service options.

Saudi Arabia is developing as a high-value enterprise security market because Vision 2030 has accelerated digital infrastructure, cloud services, fintech, government platforms and critical infrastructure modernization. National cybersecurity controls and cloud security expectations are pushing public agencies and regulated enterprises toward identity governance, privileged access control, device posture management and continuous monitoring. Large government-linked enterprises and financial institutions are expected to remain core buyers for enterprise architecture design, integration and managed security services.

South Africa is the most mature cybersecurity market in Sub-Saharan Africa because of its banking sector, telecom infrastructure, insurance industry and established enterprise technology base. POPIA (Protection of Personal Information Act) has increased attention on personal data handling, breach accountability and privacy governance. Financial institutions and healthcare groups are expected to prioritize IAM, PAM, DLP (Data Loss Prevention), endpoint security and SIEM (Security Information and Event Management) because customer data, claims records, payment systems and internal privileged accounts need stronger access control.

Nigeria is the most important West African opportunity by enterprise volume. Banks, fintechs, telecom operators, payment processors and large insurers operate across a high-transaction digital ecosystem where account takeover, fraud, social engineering and credential theft are persistent risks. CBN’s public digital finance visibility includes Bank Verification Number, cashless services and financial inclusion initiatives which reinforces the need for identity-led controls around customers, agents, internal users and third party processors.

Ghana is becoming a more structured cybersecurity market because the Cyber Security Authority was established under the Cybersecurity Act 2020 to regulate cybersecurity activity and promote national cybersecurity development. Licensing and accreditation of cybersecurity service providers, critical information infrastructure protection and incident reporting are visible national priorities on the CSA platform. Regulated buyers in banking, insurance, telecom and public administration are expected to favor IAM, managed security services, policy operations and third party access controls as Ghana’s cybersecurity governance becomes more formal.

Kenya is commercially attractive because mobile money, digital banking, e government and startup activity have created a large identity and transaction risk surface. Enterprises are increasingly looking for cloud-delivered security, endpoint monitoring, fraud-aware access controls and managed detection services. Local banks, telcos, health platforms and logistics companies are likely to use ZTNA, MFA, PAM and cloud security to secure employees, partners, APIs and distributed branch environments.

Côte d’Ivoire and Senegal are emerging as relevant Francophone West African markets for secure branch access, digital insurance, banking modernization and regional group operations. Regional insurers, banks and telecom groups need consistent access policies across subsidiaries, agents and service providers. Managed IAM, managed ZTNA and MDR can gain traction because several organizations need enterprise-level protection without building large internal security operations teams.

Ghana and Nigeria also matter because cybersecurity awareness is moving beyond large banks into smaller financial institutions, public agencies, universities, retailers and professional service firms. Ghana’s CSA platform highlights advisories and alerts covering online business impersonation, banking malware and phishing-related risks which directly support the commercial case for MFA, ITDR, endpoint security and user behavior analytics.

Middle East and Africa will remain service-intensive compared with North America and Europe. Buyers often need assessment, enterprise architecture roadmap, migration planning, integration, training and managed operations together. Vendors with strong MSSP partnerships, local regulatory understanding, Arabic and French language support, regional cloud availability and practical deployment playbooks will be better positioned than vendors selling only software licenses.

South America Zero Trust Security Market

South America is gradually expanding due to digital banking, retail modernization, cloud adoption and rising fraud exposure. Brazil leads regional demand because of enterprise scale, financial services depth and cloud adoption. Argentina and Chile follow with growing demand from banks, telecom providers and technology firms.

Procurement remains price sensitive. Buyers often seek bundled services and flexible subscription models. MSSPs and regional integrators play an important role because many organizations need implementation support and ongoing monitoring.

Financial services and retail are the most commercially visible demand areas. Digital payment expansion, e commerce growth and customer data protection are pushing organizations toward identity governance, fraud-aware access controls and cloud security.

Competitive Landscape of Zero Trust Security Market

The market is highly competitive and increasingly platform-led. Microsoft holds a strong position because identity, endpoint, cloud productivity and SIEM can be connected across enterprise environments. Palo Alto Networks competes through network security, Prisma Cloud, Prisma Access, Cortex analytics and platform consolidation. Zscaler and Cloudflare are strong in cloud-delivered secure access and SSE style architectures. Okta and CyberArk remain critical identity specialists.

Security buyers are not choosing vendors only by feature depth. Deployment speed, product integration, policy consistency, partner support, incident response quality and pricing transparency are becoming important differentiators. Large enterprises may buy from several vendors but they increasingly want fewer consoles and clearer ownership of each control layer.

Competition is also shifting toward managed outcomes. MSSPs and SIs influence vendor selection because implementation complexity remains high. Vendors with strong partner programs and training ecosystems are better positioned in mid-market and emerging regions.

Company Coverage Preview: Microsoft

Microsoft is one of the most influential players because its security portfolio is embedded across productivity, identity, endpoint, cloud and analytics workflows. Entra supports identity and access management. Defender strengthens endpoint and cloud workload protection. Sentinel supports SIEM and security operations while Intune enables device management and posture enforcement. Strong integration with Microsoft 365 and Azure gives the company a natural route into enterprise security budgets.

Microsoft’s advantage comes from control point density. Many enterprises already rely on Microsoft for email, collaboration, productivity, directory services and cloud infrastructure. Security teams can extend existing licensing and telemetry into identity protection, endpoint detection, access control and analytics without starting from zero, which lowers procurement friction and improves adoption speed.

Technological differentiation comes from telemetry scale, identity intelligence and integrated policy workflows. Microsoft reports 78 trillion security signals per day in its 2024 Digital Defense Report and highlights large-scale visibility across cloud, endpoint and partner ecosystems. The scale supports detection, automation and identity risk scoring across enterprise environments.

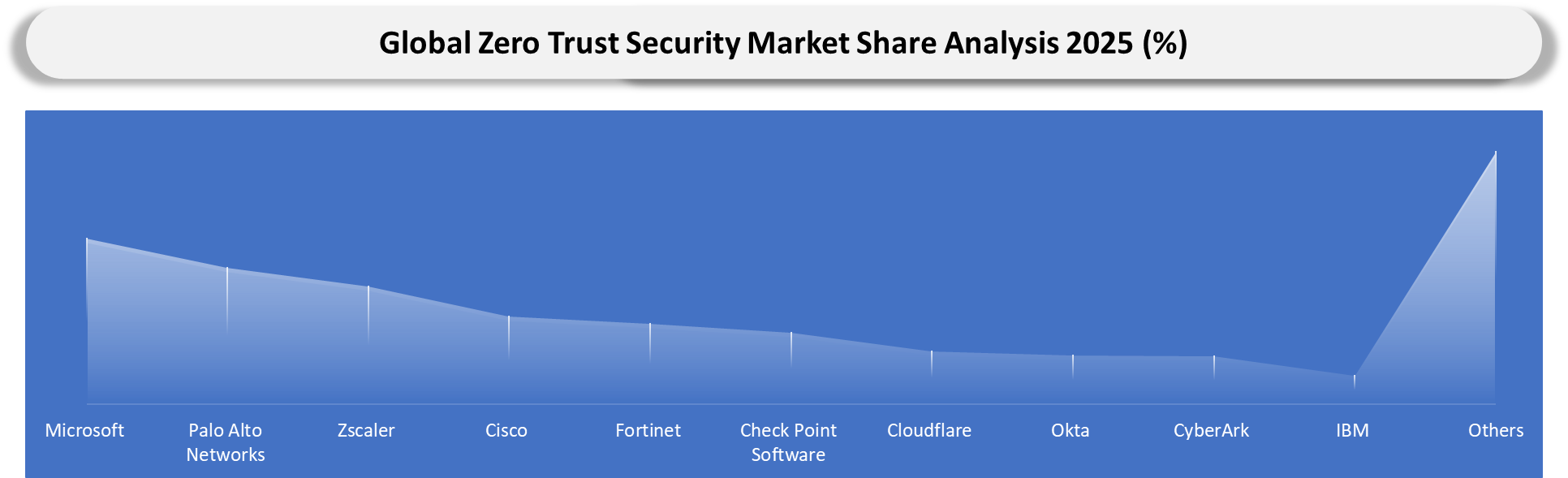

Key Companies

- Microsoft

- Palo Alto Networks

- Zscaler

- Cisco

- Fortinet

- Check Point Software

- Cloudflare

- Okta

- CyberArk

- IBM

- Google Cloud

- AWS

- Akamai

- Netskope

- CrowdStrike

- Broadcom Symantec

- Trend Micro

- F5

- Proofpoint

- SentinelOne

Latest Developments

- April 2026: Okta announced Okta For AI Agents to help enterprises register, monitor and control AI agents through identity access management workflows. The launch also addressed “shadow agents” and introduced stronger lifecycle controls for agentic AI environments.

- March 2026: Google completed its US$ 32 Billion acquisition of Wiz and moved the cloud security company under Google Cloud while keeping Wiz available across multi-cloud environments.

- February 2026: Palo Alto Networks finalized its US$ 25 Billion acquisition of CyberArk, adding identity security, PAM (Privileged Access Management), SSO (Single Sign On) and MFA (Multi Factor Authentication) depth to its broader platform strategy.

- January 2026: CrowdStrike announced the acquisition of SGNL for approximately US$ 740 Million to strengthen real-time identity security and dynamic access control for human, machine and AI-based identities.

- December 2025: Saviynt raised US$ 700 Million in Series B funding led by KKR to support global expansion and R and D across IAM (Identity and Access Management), non-human identity governance and enterprise access security.

- September 2025: Okta announced the acquisition of Axiom Security to enhance Okta Privileged Access with cloud-native PAM capabilities, just-in-time access, automated approval workflows and secure access to databases, Kubernetes and cloud infrastructure.

- September 2025: Netskope completed its Nasdaq IPO and raised approximately US$ 908 Million, strengthening investor visibility for SSE (Security Service Edge), SASE (Secure Access Service Edge), cloud security and AI-era secure access platforms.

- August 2025: Zscaler introduced new AI-driven security capabilities at Zenith Live 2025, including automated segmentation, generative AI protection, sensitive data classification and Zscaler Cellular for IoT and OT device security through SIM-based connectivity.

- July 2025: Palo Alto Networks announced a definitive agreement to acquire CyberArk in a cash and stock transaction valued at approximately US$ 25 Billion, marking its formal entry into identity security as a core pillar of its multi-platform cybersecurity strategy.

- April 2025: Palo Alto Networks acquired Protect AI and unveiled the Prisma AIRS platform at RSA Conference to expand security coverage for AI applications, AI agents and emerging AI infrastructure risks.

Major Pain Points For Manufacturers and Service Providers

- Security vendors face long enterprise sales cycles because buyers require proof of integration with existing IAM, SIEM, endpoint, cloud and directory systems.

- Platform providers must prove that bundled products can reduce tool sprawl without lowering control quality in specialized areas such as PAM, DSPM or micro segmentation.

- MSSPs need skilled staff who understand identity policy, cloud workloads, endpoint telemetry and compliance reporting together.

- Product vendors must support hybrid environments because many enterprises cannot move every application to cloud-native access models at once.

- Regional channel partners often struggle with certification depth and implementation consistency across multiple countries.

- Vendors face pricing pressure when customers already own overlapping features through Microsoft, firewall vendors or endpoint security providers.

- Security teams expect measurable outcomes such as VPN retirement, reduced privileged accounts, faster access reviews and improved audit evidence.

Analyst View

DataM Intelligence opinion is that the market is shifting from “network access modernization” to “enterprise trust control.” Identity, device health, data sensitivity and workload context are becoming the core inputs for every access decision. Vendors that connect these inputs into a practical operating model will capture the strongest growth.

DataM Intelligence opinion is also that standalone ZTNA will remain important but growth will increasingly move toward identity centric and enterprise multi pillar architectures. Large buyers want programs that can scale across users, branches, third parties, cloud workloads, privileged accounts and sensitive data. Narrow tools can still win specific deals but broad platforms will influence budget planning.

DataM Intelligence opinion is that Africa, the Middle East and parts of Asia-Pacific will create strong service-led demand. Several organizations in these regions need outcomes more than tool ownership. Managed IAM, managed ZTNA, MDR and enterprise architecture advisory services are likely to become strong commercial entry points.

What DataM Uniquely Provides

DataM connects market sizing with practical buying logic. The study helps readers understand which offerings are driving spending, which architecture models are gaining traction and how buying behavior changes across BFSI, healthcare, government, manufacturing, telecom and regional markets.

DataM adds actionable views around enterprise architecture design, managed security routes, cloud marketplace adoption, identity governance priorities, third party access control and regional vendor opportunity. The report is designed to support product positioning, partnership planning, country prioritization and go to market strategy.

DataM also provides competitive benchmarking across major platforms and specialists. Coverage includes Microsoft, Palo Alto Networks, Zscaler, Cisco, Fortinet, Check Point, Cloudflare, Okta, CyberArk, IBM, Google Cloud, AWS, Akamai, Netskope, CrowdStrike and other key providers.

Conclusion

The market is becoming a core part of enterprise security transformation. Buyers are no longer looking only for VPN alternatives. Decision makers now want identity-first access, privileged control, endpoint posture, data protection, cloud workload visibility and analytics working together.

Identity security will remain the strongest commercial anchor because attackers continue to exploit passwords, tokens, privileged accounts and misconfigured access paths. PAM, IGA, ITDR and MFA will become more strategic as organizations expand cloud workloads and deploy AI-enabled workflows.

Vendors that provide practical implementation support, clear architecture roadmaps, regional partner coverage and measurable security outcomes will be best positioned. Platform breadth will matter but execution quality will decide long-term customer retention.

Questions This Report Answers

- Which Zero Trust offerings are capturing the largest enterprise security budgets?

- How are IAM, PAM, ZTNA, cloud security and analytics converging into enterprise architecture programs?

- Which regions and countries are most attractive for vendors and service providers?

- How are BFSI, government, healthcare and manufacturing buyers prioritizing identity and access security?

- Which vendors are best positioned across platform coverage, identity depth, cloud access and managed services?

- How is AI changing identity governance, policy enforcement and non human access control?

- Which distribution routes are gaining share across direct sales, MSSPs, SIs, VARs and cloud marketplaces?

Target Audience

- Cybersecurity Vendors: Useful for product positioning, portfolio planning, regional prioritization and competitive benchmarking.

- IAM And PAM Providers: Useful for understanding demand around SSO, MFA, IGA, ITDR, privileged session management, endpoint privilege management and secrets management.

- SASE And SSE Platform Providers: Useful for evaluating branch security, cloud access, remote workforce access and enterprise architecture opportunities.

- MSSPs And System Integrators: Useful for building service packages around assessment, architecture roadmap, integration, managed access and policy operations.

- Cloud Service Providers: Useful for understanding cloud marketplace sales, workload security and cloud-native access controls.

- BFSI Security Leaders: Useful for planning identity governance, secure branch access, customer data protection, third party access and audit readiness.

- Government And Defense Buyers: Useful for evaluating policy-driven implementation, maturity models, secure application access and privileged access controls.

- Investors And Strategy Teams: Useful for tracking platform consolidation, high-growth categories, M&A activity and emerging security control points.