Operational Technology (OT) Security Market Size

Operational environments that once operated in isolation are now deeply connected to enterprise IT systems, cloud platforms, and remote monitoring networks. This convergence has significantly expanded the cyberattack surface across manufacturing plants, energy grids, transportation systems, and utilities, pushing Operational Technology (OT) security into a mission-critical category of industrial investment.

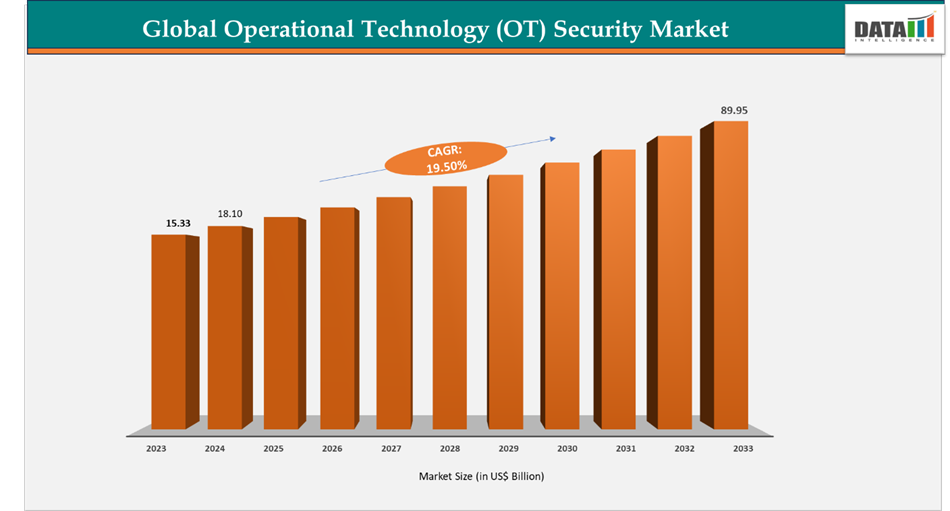

The Operational Technology (OT) Security Market will reach US$ 25.85 billion in 2026, up from US$ 21.63 billion in 2025, and is projected to reach US$ 128.43 billion by 2035, registering robust growth at a CAGR of 19.5% during the forecast period from 2026 to 2035.

Demand is being shaped by rapid Industry 4.0 deployment, smart factory expansion, and rising cyberattacks targeting industrial control systems (ICS) and supervisory control and data acquisition (SCADA) environments. For industrial operators and cybersecurity vendors, OT security is shifting from a compliance-driven expenditure to a core operational resilience strategy.

Investment timing is particularly strong as enterprises move from perimeter-based protection models toward continuous monitoring, zero-trust architectures, and AI-driven anomaly detection systems tailored for industrial environments.

Key Takeaways

- North America accounted for approximately 38-42% of the global OT Security Market share in 2025, driven by increasing investments in critical infrastructure protection, stringent cybersecurity regulations, and the widespread adoption of Industry 4.0 technologies across manufacturing, energy, and utilities sectors.

- The Manufacturing industry held nearly 28-32% of the total market share in 2025, making it the largest end-user segment owing to rapid smart factory deployments, increasing industrial automation, and rising cyberattacks targeting operational environments.

- Network Security solutions contributed approximately 30-35% of the global market revenue in 2025, supported by growing demand for industrial network segmentation, asset visibility, and real-time threat monitoring capabilities across OT infrastructures.

- Large enterprises represented approximately 65-70% of the total market demand in 2025, primarily due to higher cybersecurity spending, increasing regulatory compliance requirements, and substantial investments in securing critical industrial assets.

- Cloud-based OT security solutions accounted for nearly 35-40% of the market share in 2025 and are expected to witness significant growth during the forecast period due to increasing adoption of hybrid industrial environments and remote monitoring capabilities.

- Managed OT Security Services are projected to register a CAGR exceeding 18% during the forecast period, making them one of the fastest-growing segments as organizations increasingly outsource industrial cybersecurity management to address workforce shortages and evolving threat landscapes.

- More than 75% of industrial organizations globally are expected to implement Zero Trust security frameworks across their OT environments by 2030, significantly increasing investments in identity management, access controls, and continuous threat monitoring solutions.

- Industrial ransomware attacks accounted for approximately 40% of all reported cyber incidents targeting critical infrastructure sectors in 2025, accelerating investments in OT-specific cybersecurity technologies across manufacturing, utilities, transportation, and oil & gas industries.

- Asia-Pacific is projected to register the fastest market growth with an estimated CAGR of 17-19% through 2033, driven by increasing government investments in industrial modernization programs, expanding smart manufacturing initiatives, and growing cybersecurity awareness across emerging economies.

- Artificial Intelligence-enabled threat detection platforms are expected to capture approximately 20-25% of new OT security deployments by 2030, reflecting the increasing adoption of behavioral analytics, anomaly detection systems, and automated incident response capabilities across industrial environments.

Operational Technology (OT) Security Market Scope

| Metric | Details |

| Market Size (2025) | USD 21.63 billion |

| Market Size (2033) | US$ 128.43 billion |

| CAGR (2026-2033) | 19.50% |

| Historic Years | 2023-2024 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Segments Covered | Solutions, Services |

| Deployment | On-Premises, Cloud-Based |

| Organization Size | Large Enterprises, SMEs |

| End-Users | Manufacturing, Energy & Utilities, Oil & Gas, Transportation, Government, Healthcare |

| Largest Region | North America |

| Fastest Growing Region | Asia-Pacific |

Operational Technology (OT) Security Market Dynamics

Expansion of IT-OT Convergence and Industrial Connectivity

The integration of IT systems with OT environments is fundamentally reshaping industrial cybersecurity requirements. Manufacturing execution systems, cloud-based analytics platforms, and remote operational tools are now directly connected to industrial control networks.

This convergence improves operational efficiency but significantly increases vulnerability to cyber intrusions. As a result, enterprises are prioritizing segmentation, access control, and real-time monitoring solutions designed specifically for industrial environments.

Rising Industrial Cyber Threat Landscape

OT environments are increasingly targeted by ransomware groups, state-sponsored attackers, and supply chain-based intrusion campaigns. Unlike traditional IT breaches, OT attacks can disrupt physical operations, damage equipment, and create safety risks.

Threat actors are focusing on SCADA systems, programmable logic controllers (PLCs), and industrial IoT endpoints due to their historical lack of built-in cybersecurity protections.

Zero-Trust Architecture Adoption in Industrial Networks

Zero-trust frameworks are becoming a foundational model for OT security deployment. Enterprises are shifting from perimeter-based defenses to continuous verification systems that authenticate users, devices, and machine communications.

This approach is particularly relevant for distributed industrial networks, where remote access and third-party vendor connectivity are common.

Legacy Infrastructure and Integration Barriers

A significant portion of industrial infrastructure still relies on legacy OT systems that were not designed for cybersecurity integration. These environments often lack encryption, authentication protocols, and real-time monitoring capabilities.

Upgrading these systems requires high capital investment and operational downtime, slowing adoption in sectors such as utilities, oil & gas, and transportation.

Regulatory and Compliance Pressure

Governments and regulatory bodies are tightening cybersecurity requirements for critical infrastructure operators. Frameworks such as industrial cybersecurity standards and national infrastructure protection programs are increasing compliance-driven OT security spending.

This is particularly evident in energy and government-controlled sectors, where auditability and operational resilience are becoming mandatory procurement criteria.

Why This Report Matters in 2026

Enterprise security buyers enter 2026 facing increased pressure to protect critical infrastructure from rapidly evolving cyber threats targeting industrial environments. Organizations are no longer treating Operational Technology security as a standalone plant-floor initiative because connected factories, industrial IoT devices, remote operations, cloud-enabled industrial systems and converged IT-OT networks have significantly expanded the attack surface. Procurement teams require greater visibility into which technologies should be prioritized first, where security investments can be consolidated and how implementation partners can support modernization across complex industrial ecosystems.

Industrial operators are also confronting a major architectural challenge. Security leaders must decide between network segmentation-led OT security, industrial Zero Trust frameworks, asset visibility-driven security, threat detection and monitoring platforms, secure remote access models, cloud-enabled industrial security and comprehensive defense-in-depth strategies. Each approach creates different implications for production continuity, legacy equipment integration, regulatory compliance, operational efficiency and long-term security spending. A comprehensive market perspective enables organizations to compare deployment pathways rather than treating OT security as a single product purchase.

OT security programs are increasingly becoming outcome focused as regulators, boards and critical infrastructure operators demand measurable improvements in asset visibility, incident response readiness, ransomware resilience and supply chain security. Manufacturing, energy, utilities, oil and gas, transportation, healthcare and critical infrastructure organizations require reliable benchmarks on vendor capabilities, regional opportunities, deployment models, channel strategies and managed security service alignment. The report helps clients identify where market demand is shifting, which vendors are strengthening their competitive positions and which implementation priorities should be addressed first to minimize operational disruption while improving cyber resilience.

Enterprise Adoption Landscape and Buyer Behavior

OT security adoption is increasingly driven by structured enterprise risk management frameworks rather than isolated IT security upgrades.

Large enterprises lead adoption due to higher exposure to critical infrastructure risk and regulatory oversight. These organizations typically deploy multi-layered security stacks including network segmentation, endpoint protection, and threat intelligence platforms.

SMEs are adopting cloud-based OT security solutions at a slower pace, primarily due to cost sensitivity and integration complexity with existing industrial systems.

Key buyer personas include:

- Chief Information Security Officers (CISO)

- OT Security Architects

- Industrial Automation Engineers

- Plant Operations Directors

- Infrastructure Risk and Compliance Officers

Procurement decisions are increasingly influenced by ROI metrics such as downtime reduction, incident response time, and compliance cost avoidance.

Operational Technology (OT) Security Market Opportunities

Vendors focusing on AI-driven OT security platforms are gaining traction as enterprises seek predictive threat detection capabilities rather than reactive monitoring tools.

Managed security service providers are expanding in industrial cybersecurity due to talent shortages in OT-specific security expertise.

System integrators and automation vendors are also capturing value by embedding security directly into industrial control system deployments.

Emerging opportunities are concentrated in smart factory deployments, energy grid modernization, and transportation digitization programs, where security is now embedded at the design stage rather than added post-deployment.

Operational Technology (OT) Security Market Segmentation Analysis

Segmented by Offering (Solutions, Services), by Deployment (On-Premises, Cloud-Based), by Organization Size (Large Enterprises, SMEs), by End-User (Manufacturing, Energy & Utilities, Oil & Gas, Transportation, Government, Healthcare), and by Region - Market Share, Trends, and Forecast to 2033.

By Offering

The solutions segment dominates the market, driven by strong demand for network security, endpoint protection, IAM, encryption, and threat intelligence platforms tailored for industrial environments.

Services are gaining momentum as enterprises require consulting, integration, and managed security support to operationalize OT security frameworks across complex industrial networks.

Operational Technology (OT) Security Market Regional Analysis

Operational Technology (OT) Security Market North America

North America leads the global market due to strong cybersecurity infrastructure, regulatory enforcement, and early adoption of OT security frameworks. The United States is the primary growth engine, supported by government initiatives focused on critical infrastructure protection.

Industrial sectors such as energy, defense, and manufacturing are rapidly adopting zero-trust OT architectures and AI-based monitoring systems.

Operational Technology (OT) Security Market Asia-Pacific

Asia-Pacific is the fastest-growing region, driven by rapid industrialization and large-scale deployment of smart factories. Countries such as China, Japan, and South Korea are investing heavily in industrial cybersecurity to protect advanced manufacturing ecosystems.

Partnerships between automation vendors and cybersecurity providers are accelerating deployment across automotive, electronics, and energy sectors.

Operational Technology (OT) Security Market Europe

Europe is experiencing steady adoption driven by strict regulatory frameworks and increasing industrial digitization. Germany, France, and the UK are leading markets, particularly in manufacturing and energy infrastructure security.

Operational Technology (OT) Security Market Competitive Landscape and Vendor Strategy

The OT security ecosystem is dominated by global cybersecurity providers and industrial automation leaders.

Key companies include:

- Siemens

- Palo Alto Networks, Inc.

- Zscaler, Inc.

- Cisco Systems, Inc.

- Fortinet, Inc.

- SentinelOne

- Forcepoint

- Broadcom

- Qualys, Inc.

- Kyndryl Inc.

Market leaders are increasingly focusing on integrated OT security architectures that combine:

- AI-based threat detection and behavioral analytics

- Zero-trust network segmentation for industrial environments

- Secure access service edge (SASE) for distributed OT networks

- Deep industrial protocol inspection capabilities

- Cloud-managed security orchestration platforms

Competitive differentiation is shifting toward ecosystem integration, where cybersecurity vendors align with industrial automation providers to secure end-to-end production environments.

Operational Technology (OT) Security Market Recent Developments

- June 2026: Siemens AG strengthened its industrial OT cybersecurity capabilities by enhancing its Industrial Operations X portfolio with advanced threat detection, asset visibility, and secure industrial networking solutions for critical infrastructure and manufacturing environments.

- June 2026: Palo Alto Networks, Inc. expanded its OT security offerings through AI-driven threat prevention technologies and collaborative research focused on securing industrial control systems and critical infrastructure.

- May 2026: Zscaler, Inc. enhanced its Zero Trust security platform with new AI-powered capabilities that strengthen secure access and cloud-delivered protection for industrial and operational technology environments.

- May 2026: Fortinet, Inc. advanced its OT security portfolio by expanding industrial firewall, intrusion prevention, and real-time threat intelligence capabilities designed for converged IT/OT networks across manufacturing and energy sectors.

- April 2026: Cisco Systems, Inc. strengthened its industrial cybersecurity solutions through enhanced zero-trust network segmentation and secure connectivity technologies tailored for Industrial IoT and smart factory deployments.

- April 2026: Broadcom Inc. continued expanding its enterprise cybersecurity capabilities through investments in infrastructure software solutions that support secure hybrid cloud and industrial networking environments.

- March 2026: SentinelOne enhanced its AI-powered cybersecurity platform by strengthening autonomous threat detection and protection capabilities for OT endpoints and industrial workloads.

- March 2026: Kyndryl Inc. expanded its cybersecurity consulting and managed security services portfolio to help industrial organizations secure converged IT/OT infrastructures and accelerate digital transformation initiatives.

- February 2026: Qualys, Inc. strengthened its cyber risk management platform by expanding vulnerability management and asset discovery capabilities applicable to industrial and operational technology environments.

Operational Technology (OT) Security Market Investment Landscape (2024-2026)

Strategic investments across industrial cybersecurity continue to accelerate globally as organizations modernize legacy infrastructure and strengthen operational resilience capabilities. Significant investments are being directed toward zero-trust architectures, AI-enabled cybersecurity platforms, industrial network segmentation technologies, and managed security services. Public and private sector investments supporting smart manufacturing initiatives and critical infrastructure protection programs are expected to create substantial growth opportunities across the OT security ecosystem throughout the forecast period.

Country-Level Critical Infrastructure Spending Analysis

The United States continues to invest significantly in critical infrastructure modernization and industrial cybersecurity initiatives across energy, transportation, healthcare, and manufacturing sectors. Europe is witnessing increasing cybersecurity investments driven by stringent regulatory frameworks protecting industrial infrastructure. Meanwhile, Asia-Pacific is emerging as the fastest-growing regional market owing to rapid industrialization, increasing smart factory deployments, and government-led cybersecurity initiatives across China, Japan, South Korea, and India. These developments are expected to substantially increase demand for OT security solutions globally.

Industrial Cybersecurity Skills Gap Analysis

The shortage of skilled cybersecurity professionals capable of managing complex OT environments remains one of the major challenges confronting industrial organizations worldwide. Increasing demand for professionals possessing expertise across industrial automation systems, cybersecurity frameworks, and incident response capabilities continues to exceed available talent pools. Consequently, organizations are increasingly relying on managed security service providers and cybersecurity consulting firms to address workforce limitations while strengthening operational resilience.

Strategic Recommendations

Market participants should prioritize investments in AI-enabled threat detection technologies, managed security services, and zero-trust architectures to address evolving industrial cybersecurity requirements. Strengthening partnerships between cybersecurity vendors, industrial automation providers, and cloud infrastructure companies will remain essential for delivering integrated OT security solutions globally. Organizations should further focus on expanding regional capabilities, investing in industrial threat intelligence platforms, and developing industry-specific cybersecurity offerings tailored to critical infrastructure sectors. Additionally, proactive regulatory compliance strategies and workforce development initiatives are expected to provide long-term competitive advantages within the rapidly evolving OT security market.

Report Benefits

This report supports:

- Cybersecurity vendors targeting industrial OT environments

- Critical infrastructure operators assessing security modernization strategies

- Investors evaluating cybersecurity and industrial software opportunities

- Government agencies focused on infrastructure resilience

- Industrial automation providers integrating embedded security solutions

- Enterprise security teams managing IT-OT convergence risks

Target Audience

- Cybersecurity Companies

- Industrial Automation Providers

- Manufacturing Enterprises

- Energy and Utility Operators

- Government Infrastructure Agencies

- Critical Infrastructure Security Teams

- Managed Security Service Providers

- Technology Investors

Related Reports

- Industrial Cybersecurity Market

- Critical Infrastructure Protection Market

- Zero Trust Security Market

- Identity and Access Management (IAM) Market

- Network Security Market

The global operational technology (OT) security market report delivers a detailed analysis with 70 key tables, more than 63 visually impactful figures, and 195 pages of expert insights, providing a complete view of the market landscape.