Pediatric Clinical Trials Market Size & Industry Outlook

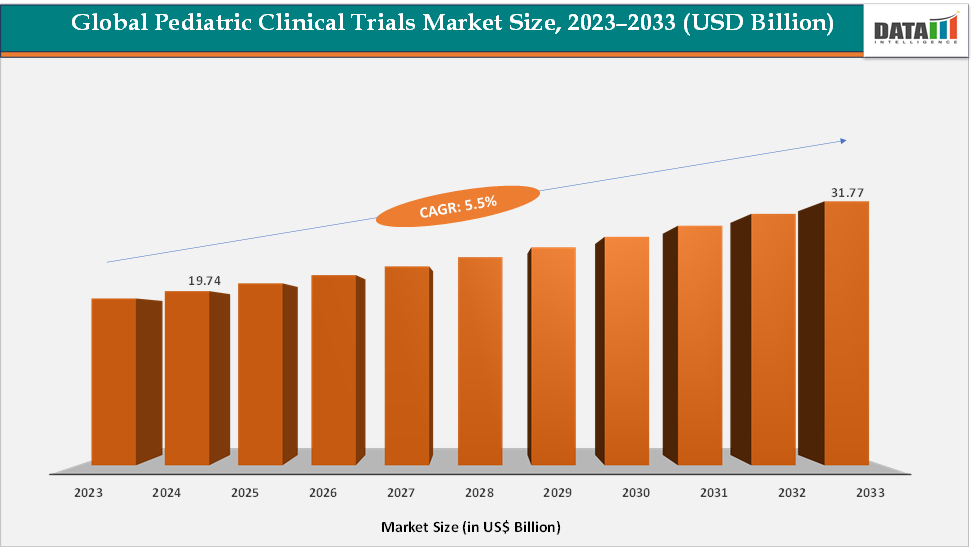

The global pediatric clinical trials market size reached US$ 19.74 Billion in 2024 from US$ 18.79 Billion in 2023 and is expected to reach US$ 31.77 Billion by 2033, growing at a CAGR of 5.5% during the forecast period 2025-2033. The market is being driven by the rising prevalence of chronic and rare childhood diseases such as Duchenne muscular dystrophy and spinal muscular atrophy, coupled with stronger regulatory mandates that require pediatric data for drug approvals. Demand for pediatric oncology and rare disease studies is also accelerating, especially with the growth of cell and gene therapies targeting inherited conditions. Contract Research Organizations are seeing an increase in outsourcing as sponsors seek specialized expertise in recruiting children and designing age-specific protocols. Additionally, decentralized trial technologies and digital recruitment are helping address long-standing challenges in pediatric enrollment and retention. Together, these trends are driving steady market growth, with North America leading and the Asia-Pacific region emerging as the fastest-growing.

Key Market Highlights

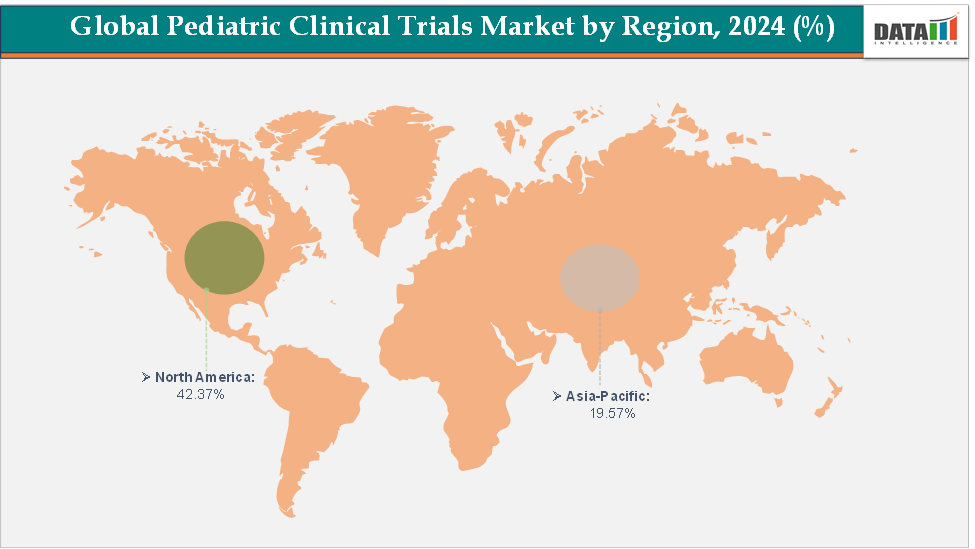

North America dominates the pediatric clinical trials market with the largest revenue share of 42.37% in 2024.

The Asia Pacific is the fastest-growing region and is expected to grow at the fastest CAGR of 6.1% over the forecast period.

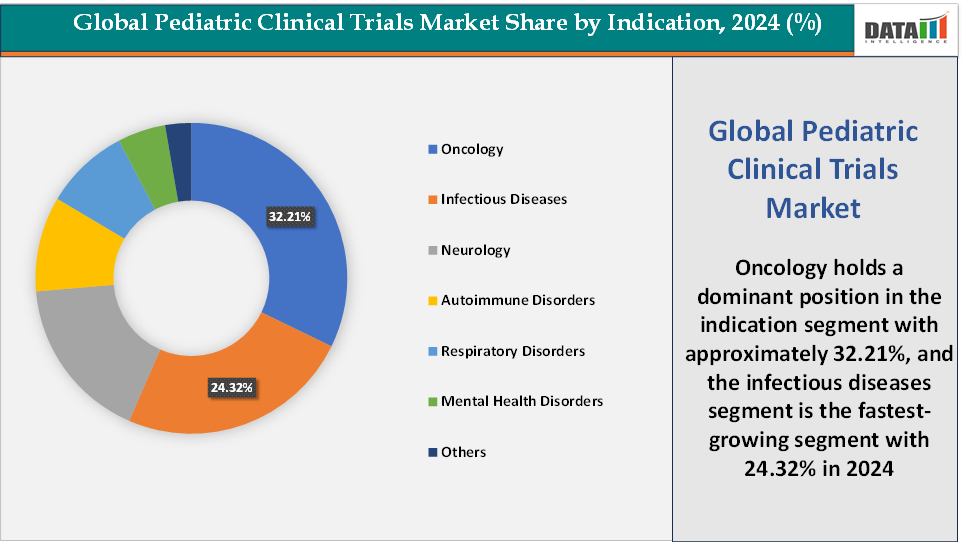

Based on indication, the oncology segment led the market with the largest revenue share of 32.21% in 2024.

The major market players in the pediatric clinical trials market are ICON plc, Pfizer Inc., Syneos Health, Thermo Fisher Scientific Inc., Medpace, Bristol-Myers Squibb Company, IQVIA Inc., Parexel International Corporation, and Charles River Laboratories, among others

Market Dynamics

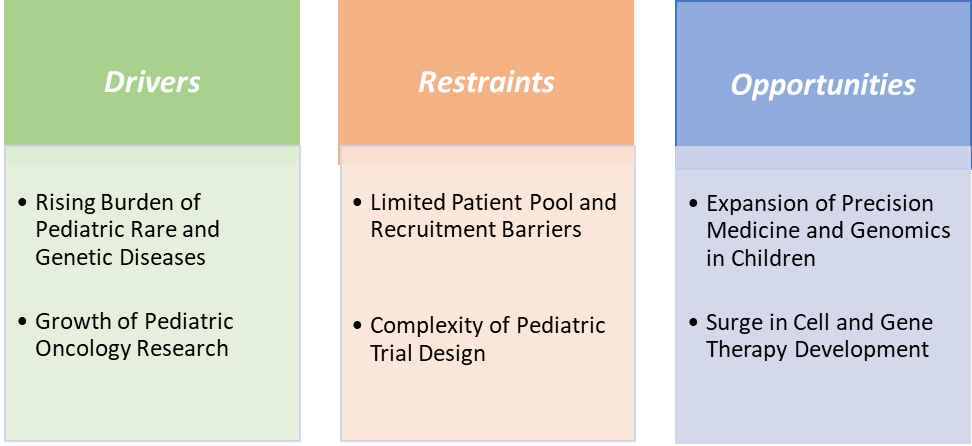

Drivers:The rising burden of pediatric rare and genetic diseases is significantly driving the pediatric clinical trials market growth

The rising burden of pediatric rare and genetic diseases is a key driver of the pediatric clinical trials market growth. According to the National Institutes of Health (NIH), to date, more than 7,000 rare diseases have been identified, highlighting their significant global impact. Approximately 30 million people in the United States, 29 million in the Europe, and an estimated 400 million individuals worldwide are affected by various rare diseases. Approximately 80% of rare diseases are genetic in origin. Of these, approximately 70% manifest during childhood, with approximately 3% manifesting in the neonatal period, underscoring the urgent need for effective therapies.

This has fueled advancements in therapeutics such as Sarepta’s Elevidys for Duchenne muscular dystrophy, whose expanded indication now covers up to 80% of patients, driving the market. Academic centers are also advancing innovations, with Great Ormond Street Hospital’s gene therapy for adenosine deaminase-deficient severe combined immunodeficiency (ADA-SCID) demonstrating over 95% success in trials. Reflecting these needs, registered pediatric clinical trials increased from 7,029 in 2008–10 to 11,738 in 2017–19, highlighting the momentum in rare and genetic disease research. Together, the prevalence, severity, and high unmet demand for pediatric rare diseases are accelerating clinical trial activity and reshaping the market landscape.

Restraints:The complexity of pediatric trial design is hampering the growth of the market

The complexity of pediatric trial design is a major factor hampering the growth of the pediatric clinical trials market. Unlike adults, children cannot be treated as a homogeneous group, as their pharmacokinetics, metabolism, and dosing vary widely across neonates, infants, children, and adolescents. This forces sponsors to create multiple study arms or stratified cohorts, making trial design more expensive and time-consuming.

For instance, in pediatric oncology, trials often need separate dosing regimens for different age brackets, which slows enrollment and increases costs. The requirement for child-friendly formulations such as flavored liquids, mini-tablets, or dispersible powders adds further complexity. Additionally, the small patient pools for rare diseases like Duchenne muscular dystrophy or spinal muscular atrophy mean global, multi-site trials must be designed to meet statistical significance, further complicating execution.

Regulatory agencies also demand paediatric investigation plans (PIPs) or pediatric study plans (PSPs) before adult approvals, which lengthens timelines and increases documentation burdens. These design hurdles not only delay drug development but also raise per-patient costs, discouraging smaller biotech firms from pursuing pediatric programs despite unmet needs. Consequently, the structural complexity of pediatric trial design continues to act as a restraint on overall market growth.

For more details on this report – Request for Sample

Segmentation Analysis

The global pediatric clinical trials market is segmented based on phase, study design, indication, and region.

Indication:The oncology segment is dominating the pediatric clinical trials market with a 32.21% share in 2024

The oncology segment commands leadership in the pediatric clinical trials market. This concentration is driven by the rising incidence. For instance, according to the National Cancer Institute, it is estimated that, in 2024, a total of 14,910 children and adolescents ages 0 to 19 will be diagnosed with cancer and 1,590 will die of the disease in the United States. Among children (ages 0 to 14 years), it is estimated that 9,620 will be diagnosed with cancer and 1,040 will die of the disease, spurring investment in age-specific therapies.

Regulatory frameworks like the U.S. RACE for Children Act mandate evaluation of molecularly-targeted oncology drugs in children, accelerating trial pipelines. Moreover, pediatric oncology trials are frequently at the forefront of innovation, incorporating CAR-T therapies, immunotherapy, and novel targeted agents that require specialized pediatric protocols and FDA-reviewed Pediatric Study Plans. Leadership in oncology is also reinforced by large hospital and research networks. Taken together, high disease burden, regulatory mandates, and innovation-driven therapeutic development make pediatric oncology the standout segment in clinical trials.

The infectious diseases segment is the fastest-growing segment in the pediatric clinical trials market, with a 24.32% share in 2024

The infectious diseases segment is rapidly becoming the most dynamic area of pediatric clinical trials, driven by the persistent and evolving threat of communicable illnesses in children worldwide. Pediatric populations remain especially vulnerable to infections such as RSV, influenza, meningitis, and diarrheal diseases, which continue to account for a significant share of childhood morbidity and mortality. The COVID-19 pandemic amplified the urgency of developing pediatric vaccines and therapeutics, as regulatory agencies and research organizations accelerated studies to ensure safety and efficacy across younger age groups.

Notable instances include the development of nirsevimab, a monoclonal antibody designed to protect infants against severe RSV infection in Europe in the year of 2022. Beyond pandemic-related products, ongoing clinical activity is centered on advancing next-generation vaccines, such as multivalent conjugate vaccines targeting pneumococcal and meningococcal diseases, which are tailored to prevent multiple strains in a single formulation.

At the same time, the global resurgence of preventable illnesses like measles and pertussis, fueled by gaps in routine immunization coverage, has underscored the importance of sustained pediatric infectious disease research. Collectively, the combination of high disease burden, accelerated innovation in immunization technologies, and renewed global health urgency positions infectious diseases as the fastest-growing and most strategically critical focus of pediatric clinical trials.

Geographical Analysis

North America is expected to dominate the global pediatric clinical trials market with a 42.37% in 2024

North America is a dominant region in the global pediatric clinical trials market due to its strong regulatory framework and high concentration of leading pharmaceutical companies and research institutions. North American institutions also benefit from substantial public and private funding for pediatric research, particularly through the NIH, which supports a wide range of studies in rare diseases, neurology, and autoimmune conditions. These combined factors, such as regulatory mandates, product innovation, research capacity, and funding strength, have positioned North America as the leading hub for pediatric clinical trials and a trendsetter in designing frameworks.

US Pediatric Clinical Trials Market Trends

The US, in particular, has established pediatric-focused legislation such as the Pediatric Research Equity Act (PREA) and the Best Pharmaceuticals for Children Act (BPCA), which mandate and incentivize the inclusion of pediatric populations in drug development. More recently, the RACE for Children Act has driven significant expansion in pediatric oncology trials by requiring evaluation of targeted cancer drugs in children when relevant mechanisms of action are identified. The US is also home to some of the world’s most advanced children’s hospitals and research networks, such as the collaborations between Texas Children’s Hospital and MD Anderson Cancer Center, which provide unparalleled access to pediatric oncology trials.

In infectious diseases, the US played a leading role in rapid pediatric evaluations of COVID-19 vaccines and the approval of Beyfortus (nirsevimab), a breakthrough monoclonal antibody to protect infants from RSV, showcasing its ability to conduct large-scale, time-sensitive pediatric trials. Furthermore, the US has been at the forefront of adopting decentralized clinical trial (DCT) models, with companies like Syneos Health and PPD deploying digital and hybrid approaches to improve participation and retention among children and their families.

The Asia Pacific region is the fastest-growing region in the global pediatric clinical trials market, with a CAGR of 6.1% in 2024

The Asia-Pacific region is rapidly emerging as the fastest-growing market for pediatric clinical trials, propelled by regulatory modernization, vast patient pools, and increasing healthcare investments. Countries such as Japan, India and China have introduced streamlined ethical review processes, fast-track approval pathways, and decentralized trial guidelines that significantly cut down trial setup timelines, making the region more attractive to multinational sponsors.

India offers cost advantages, large treatment-naïve pediatric populations, and collaborations with organizations like Gavi, which are working to reduce the proportion of unvaccinated children. These dynamics are further reinforced by the expansion of regional CROs and global service providers such as WuXi AppTec and Novotech, who are enhancing recruitment networks and data management capabilities across Asia-Pacific. The region has also become a key site for the development of innovative pediatric products, from next-generation vaccines against infectious diseases to novel cell and gene therapies, supported by both government funding and private R&D partnerships.

Europe Pediatric Clinical Trials Market Trends

Europe’s pediatric clinical trials market is being steadily propelled by a combination of strong regulatory frameworks, coordinated research networks, and increasing investment in child-specific healthcare innovations. Central to this growth is the EU Paediatric Regulation, which mandates a Paediatric Investigation Plan (PIP) for all new drug applications unless explicitly waived or deferred, compelling sponsors to generate pediatric data early in the drug development lifecycle.

Complementing this, the ICH E11(R1) addendum provides clear guidance on age-appropriate study designs, safety monitoring, and extrapolation of adult data to pediatric populations, enabling researchers to conduct scientifically rigorous yet feasible trials across diverse member states. Europe’s long-standing commitment to coordinated research through initiatives such as Horizon 2020/FP7 projects and networks like the European Network of Paediatric Research at the European Medicines Agency (Enpr-EMA) facilitates multicountry recruitment, standardized protocols, and high-quality data collection, thereby accelerating trial timelines and improving study reliability.

Moreover, in areas such as oncology and rare diseases, EMA guidance combined with member-state research consortia has spurred mechanism-based pediatric studies, including targeted therapies and gene/cell treatments, mirroring global regulatory initiatives like the U.S. RACE for Children Act. Additional driving factors include well-defined consent and assent procedures across the European Economic Area (EEA), growing public–private funding streams, and a culture of collaborative, multicenter research, all of which reduce administrative hurdles and make Europe a policy-savvy and scientifically productive hub for pediatric clinical trials. Collectively, these regulatory, infrastructural, and collaborative elements create a highly conducive environment, ensuring sustained growth and innovation in the European pediatric clinical trials market.

Competitive Landscape

Top companies in the pediatric clinical trials market include ICON plc, Pfizer Inc., Syneos Health, Thermo Fisher Scientific Inc., Medpace, Bristol-Myers Squibb Company, IQVIA Inc., Parexel International Corporation, and Charles River Laboratories, among others.

ICON plc:

ICON plc is a leading player in the pediatric clinical trials market due to its comprehensive global presence, deep expertise in pediatric study design, and strong partnerships with pharmaceutical and biotech companies. The company offers end-to-end services, including protocol development, regulatory support, patient recruitment, and data management, which are critical for complex pediatric studies. ICON has successfully conducted numerous pediatric trials across oncology, infectious diseases, and rare genetic disorders, leveraging its network of sites and experienced clinical teams to ensure timely and high-quality data collection. Its focus on innovative trial solutions, such as decentralized and hybrid study models, further strengthens its position.

Market Scope

Metrics | Details | |

CAGR | 5.5% | |

Market Size Available for Years | 2022-2033 | |

Estimation Forecast Period | 2025-2033 | |

Revenue Units | Value (US$ Bn) | |

Segments Covered | Phase | Phase I, Phase II, Phase III, and Phase IV |

Study Design | Treatment Studies and Observational Studies | |

Indication | Oncology, Infectious Diseases, Neurology, Autoimmune Disorders, Respiratory Disorders, Mental Health Disorders, and Others | |

Regions Covered | North America, Europe, Asia-Pacific, South America and the Middle East & Africa | |

The global pediatric clinical trials market report delivers a detailed analysis with 59 key tables, more than 55 visually impactful figures, and 159 pages of expert insights, providing a complete view of the market landscape.

Suggestions for Related Report

For more pharmaceuticals-related reports, please click here