Decentralized Clinical Trials Market Size & Share

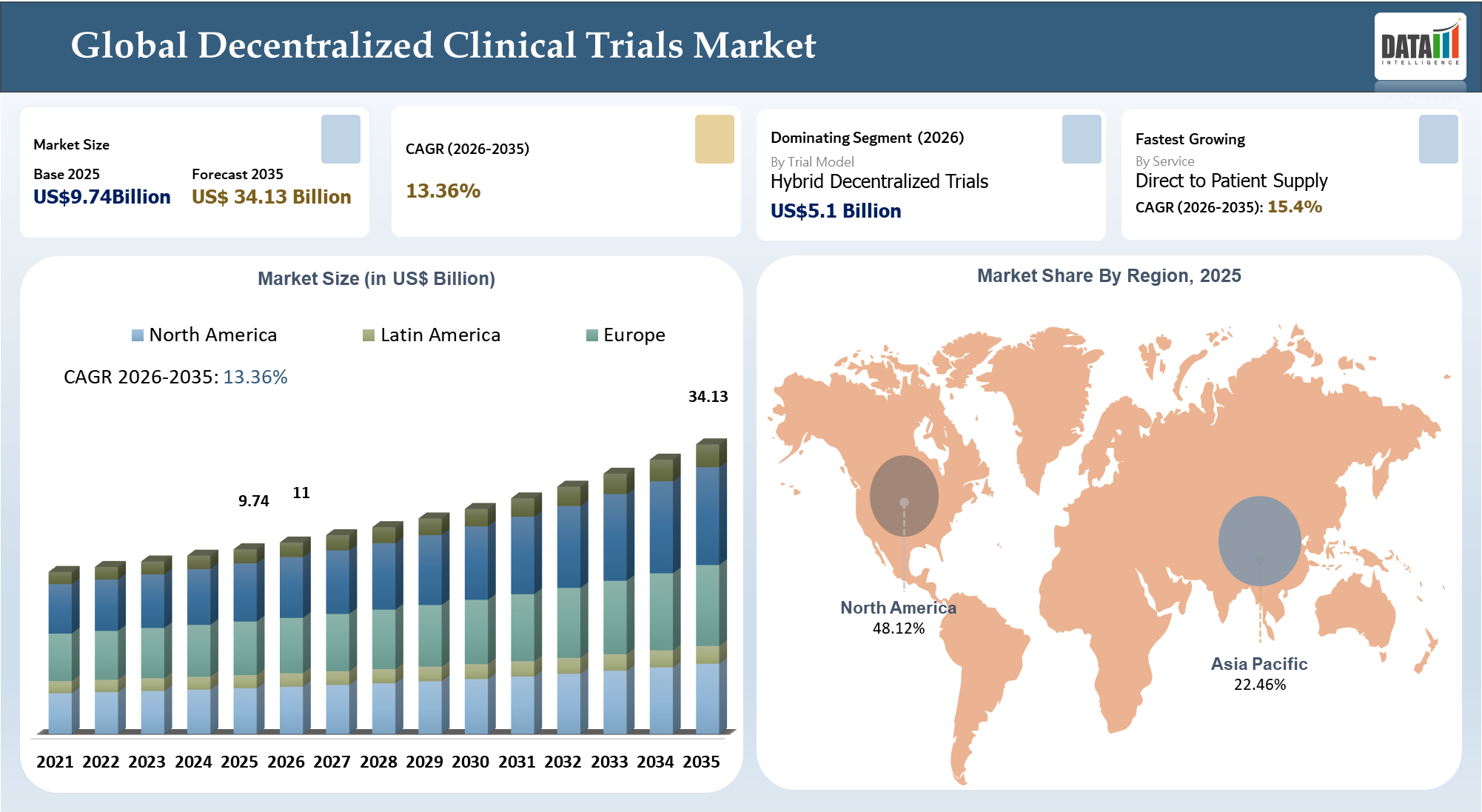

The decentralized clinical trials market size has been estimated to be US$ 9.74 billion in 2025 and is expected to reach US$ 34.13 billion by 2035, exhibiting a CAGR of 13.36% during the forecast period 2026–2035.

The market is undergoing a radical change where the sponsors, CROs, and the technology vendors move away from their conventional site-based clinical trials into more flexible and digitally driven models. This growth is supported by the increasing adoption of various digital technologies for clinical research, such as telehealth solutions, eConsent solutions, wearable devices, remote patient monitoring systems, eCOA platforms, and others.

The market continues to remain somewhat fragmented with increasing competition among CROs, decentralized trial platform vendors, and other general eClinical solutions vendors. The convergence of remote service provision, connectivity in data acquisition, and the analysis-driven approach is making possible for the industry to execute clinical trials in a more efficient and scalable manner. The key vendors operating in the decentralized clinical trials market include global CROs, decentralized trial solutions providers, and eClinical solutions providers. Value areas include platform integration, patient engagement, remote monitoring, and data management.

Decentralized Clinical Trials Industry Trends and Strategic Insights

- The market for decentralized clinical trials is currently undergoing a significant change towards hybrid clinical trials and patient-centric approaches owing to the growing popularity of technologies related to digital health including telemedicine, electronic consent forms, wearables, and patient remote monitoring. Major companies in the market like IQVIA Inc., ICON plc, and Parexel International Corporation have been investing in developing an integrated system for conducting decentralized trials.

- The key players focused on providing solutions based on advanced technologies, such as Medable Inc., Science 37 Holdings, Inc., Signant Health, and Veeva Systems Inc., have been contributing to the development of the market with their offerings of virtual consultations, remote interaction and digital workflow orchestration. In addition, vendors offering eClinical solutions and platform vendors such as Clario, Castor, and Viedoc Technologies AB have been contributing to the development of decentralized clinical trial infrastructure.

- Moreover, increasing collaboration between CROs and home healthcare organizations is facilitating the transition towards hybrid trials among decentralized clinical trials players.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 9.74Billion | |

| 2035 Projected Market Size | US$ 34.13 Billion | |

| CAGR (2026-2035) | 13.36% | |

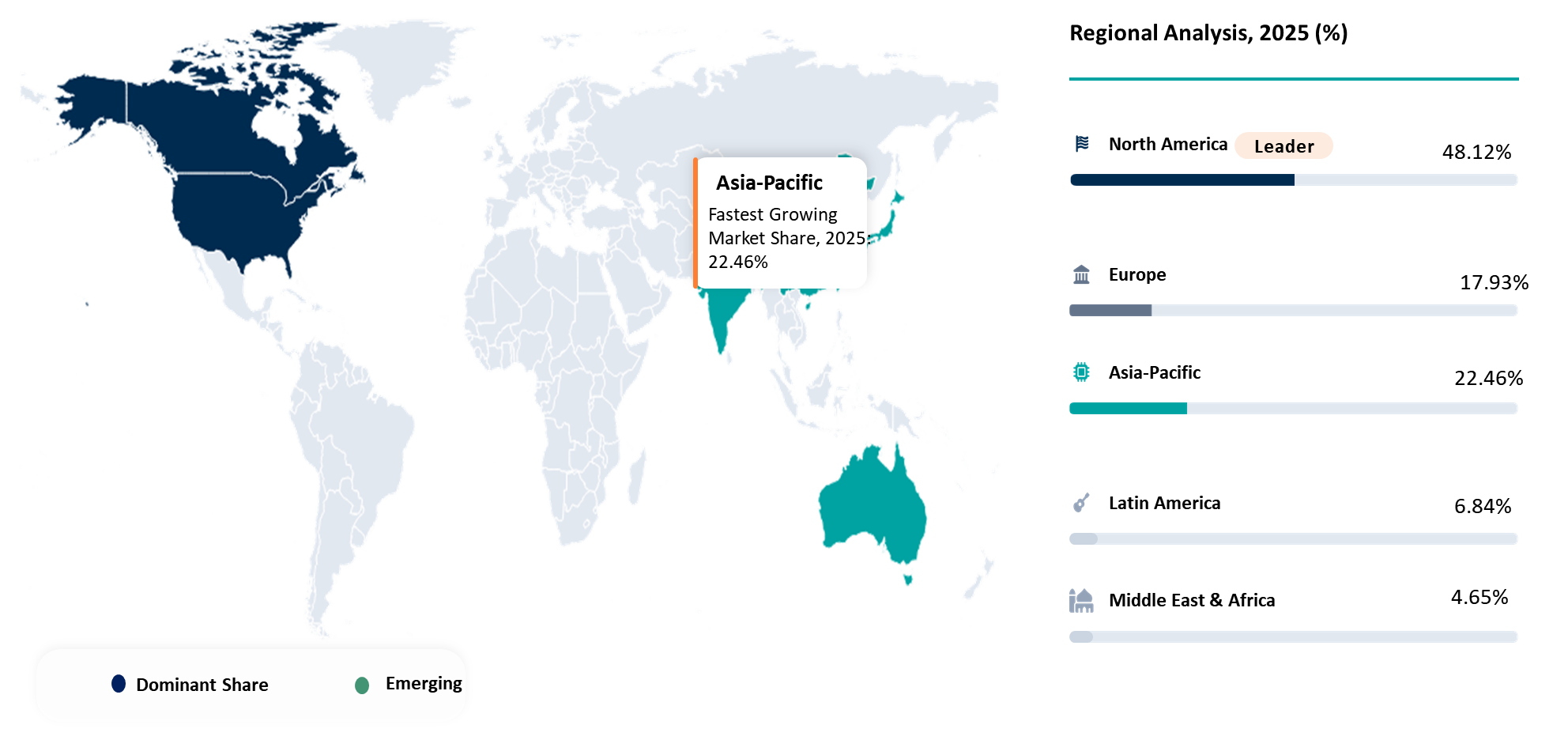

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Trial Model | Fully Decentralized Trials, Hybrid Decentralized Trials, Site Based Trials with Remote Components | |

| By Phase | Phase I, Phase II, Phase III, Phase IV | |

| By Service | Telemedicine and Virtual Visits, eConsent, Remote Patient Monitoring, Home Healthcare, Direct to Patient Supply, Data Management, Patient Recruitment and Engagement, Regulatory and Compliance Support | |

| By Technology | eClinical Platforms, Telehealth Platforms, eConsent Platforms, eCOA Platforms, Wearables and Biosensors, Mobile Health Applications, Data Integration and Analytics Platforms | |

| Therapeutic Area | Oncology, Cardiovascular Diseases, Neurology, Infectious Diseases, Rare Diseases | |

| By End-User | Pharmaceutical Companies, Biotechnology Companies, CROs, Academic and Research Institutes, Medical Device Companies | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Disruption Analysis

Shift from Site-Centric Clinical Trials to Hybrid and Decentralized Models Reshaping Clinical Research Delivery

The current trend towards disruptive changes in the decentralized clinical trials space involves the replacement of the more site-focused clinical trials model with the integration of a hybrid and patient-centered operating model. There is increased reliance on digital health solutions, which include telehealth, eConsent, wearables, remote monitoring, and direct-to-patient services in trials. This has led to reduced need for physical visits at trial sites, making it easier for sponsors to collect real-time information about patients. As such, there has been a disruption of the traditional workflow that involved heavy physical and logistical operations.

Concurrently, integrated platforms for decentralized trials are facilitating fast-paced and scalable launching of clinical studies through the use of remote and efficient service models. Through virtual engagement tools, remote data gathering, and advanced analytics, there have been innovative service models. Hence, the growth of the decentralized clinical trials market size will be facilitated by hybrid deployment, whereas the future decentralized clinical trials market share will be taken up by those companies combining regulatory reliability, end-to-end solution deployment, and digital health technology.

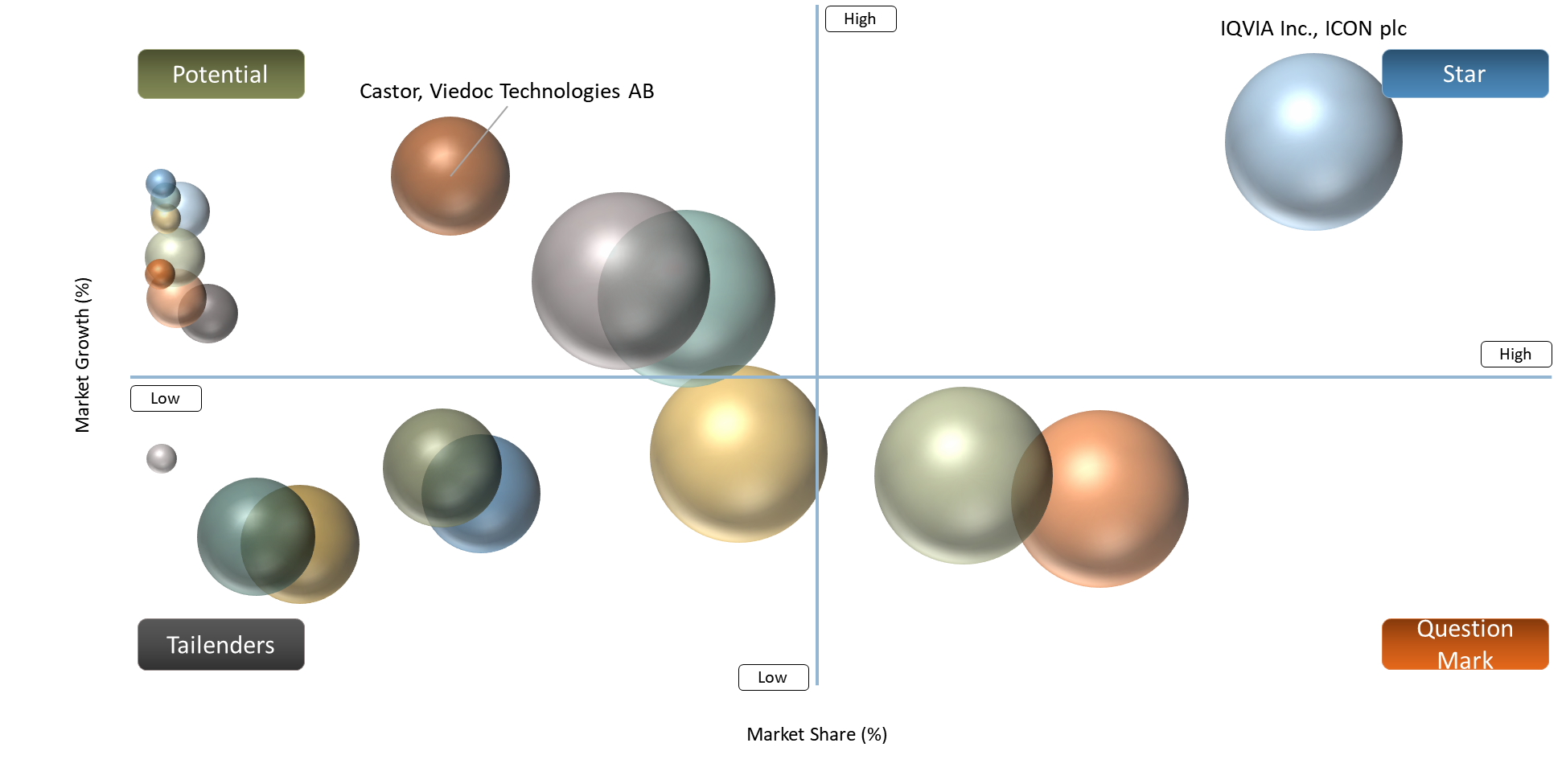

BCG Matrix: Company Evaluation

The major players in the global CROs space, namely, IQVIA Inc., ICON plc, Labcorp Holdings Inc., Parexel International Corporation, Thermo Fisher Scientific Inc., and Veeva Systems Inc. would fall under the category of Stars (high market share and high growth) owing to their ability to execute well on a global scale and dominant market shares in the decentralized clinical trials segment along with scalability for hybrid and decentralized clinical trials.

Technological platform providers such as Oracle Corporation, Dassault Systèmes SE, Medable Inc., Science 37 Holdings, Inc., Signant Health, and Syneos Health, Inc. would be classified as Question Mark (low market share and high growth) owing to their high level of innovations, digital capabilities, and increasing influence in decentralized clinical trial enablements, even though the contributions made by these companies towards the entire decentralized clinical trials market are still forming.

The emerging decentralized clinical trials solution providers, including Castor, Viedoc Technologies AB, THREAD Research, Medrio, Inc., OpenClinica, LLC, and Clinion IT Services Pvt. Ltd. are categorized under Potential (new entrants with potential high growth, low market share) owing to their high level of innovations and growing presence within specific digital health technology domains.

Medpace Holdings, Inc. and Clario can be identified as examples of Tailenders, which are characterized by Low Market Share and Low Growth/Niche Positioning, because these companies operate using the more traditional approach, have a low level of decentralization capabilities, and are progressively moving towards hybrid models within their market analysis of decentralized clinical trials.

Market Dynamics

Growing regulatory acceptance of decentralized elements

The increased acceptance of decentralized components within regulatory frameworks is expected to contribute to the future expansion of the decentralized clinical trials market significantly. The guidance document published by the U.S. FDA explicitly describes the nature of activities associated with conducting remote trials, including telehealth visits, home visits by the trial staff, and interaction with local medical professionals, defining the latter activities as acceptable under conditions where patient safety, data integrity, and proper investigation supervision remain ensured. Additionally, according to the FDA's definition, a decentralized clinical trial means any clinical trial incorporating activities conducted outside the regular trial centers.

Similarly, the European regulators have started developing frameworks aimed at supporting the adoption of decentralized clinical trials. Thus, EMA claims that decentralized clinical trials will allow increasing the flexibility and convenience of clinical research for participants thanks to home health visits, home delivery of investigational medicines, and e-consent. Moreover, in accordance with EMA's recommendation framework for decentralized clinical trials, each EU state outlines regulations concerning certain decentralized elements used during the research process. At the same time, starting from 2025, Annex 2 to ICH E6(R3) became applicable. In turn, Annex 2 discusses decentralized clinical trials and some other innovative trial designs.

Digital access and participant technology barriers

The barrier of digital access and patient technology is another restraint in the decentralized clinical trials industry since remote trials require the use of technology such as the internet and devices and patients must have the capability to use such technologies. Although the decentralized clinical trial concept enhances accessibility to some participants, it can also be less favorable to senior citizens, rural communities, poor people, and those without sufficient knowledge about digital technology and languages. The FDA guidelines show that the components of decentralized trials depend on the application of technologies through which patients participate remotely. This implies that the availability of technologies is essential in enhancing trial success and can influence recruitment rates, adherence, data loss, and participant diversity..

Segment Analysis

The global decentralized clinical trials market is segmented based on trial model, phase, service, technology, therapeutic area, end user, and region/countries.

Hybrid Decentralized Trials Emerging as the Largest Value Layer in the Decentralized Clinical Trials Market

The Hybrid Decentralized Trials occupy the largest decentralized clinical trials market share among the trial models in the decentralized clinical trials market since they offer the benefits of flexibility offered by remote clinical activities, coupled with those of clinical supervision at physical sites. In the decentralized clinical trials market, sponsors have shown increasing preference for hybrid models over pure virtual models as hybrid models permit the use of telemedicine visits, electronic consents, remote monitoring visits, and home visits alongside other decentralized techniques but not replacing the clinically essential physical procedures. The FDA guidelines favor the inclusion of decentralized components like telehealth visits, in-home visits, and visits to local healthcare providers.

From a decentralized clinical trials market analysis standpoint, full decentralized trials are still on the rise, especially those that have low intervention or are digitally suited, although the hybrid model of decentralized trials has the upper hand in terms of its commercial feasibility due to its scalability across different phases and therapeutic areas. This trend makes the decentralized clinical trials market size rely more heavily on hybrid models, especially for clinical trials that need digital health technology..

Geographical Penetration

North America Leading the Decentralized Clinical Trials Market Through Regulatory Maturity and Digital Health Technology Adoption

North America represents one of the key leaders in terms of decentralized clinical trials market share due to the advanced clinical trials environment and the high number of sponsors in this region, along with the presence of innovative digital healthcare technologies in routine clinical trials. According to the recent guidelines provided by FDA, the country can be viewed as the main growth driver in the decentralized clinical trials market size in the region since the guidelines provide official recognition of decentralized clinical trial components such as telemedicine visits, at-home clinical trial support, and remote data collection. For example, as evidenced by the analysis of case studies in 2025, 30.1% of all decentralized clinical trials originated from the USA, and only 5.7% were launched in Canada. At the same time, the healthcare system of North America can be described as digital-ready since 37% of adults in the United States utilized telemedicine in 2021. Moreover, according to the NHLBI, approximately one-third of Americans use wearable devices for health and fitness monitoring purposes. All these factors make North America a highly promising place for implementing decentralized clinical trials and combining components such as eConsent, virtual visits, remote monitoring, and sensor-driven endpoints.

United States Accelerating Decentralized Clinical Trials Growth Through Innovation in Digital Health and Clinical Research

The dominant position of the decentralized clinical trials market share in North America is occupied by the United States, driven by the well-developed clinical research environment, effective regulation, and fast digitalization of clinical trials in the country. The United States makes a crucial contribution to the growth of the entire decentralized clinical trials market, owing to the involvement of major players in the pharmaceutical sector, CROs, and technology providers who apply different strategies of hybrid or decentralized approaches to conducting trials. The guidance on decentralized aspects, issued by the U.S. Food and Drug Administration, includes provisions regarding telehealth, remote monitoring, and home care support; thus, it is considered a catalyst for the implementation of decentralization technologies.

With respect to the decentralized clinical trials market analysis, it is worth noting that adults in the United States demonstrate high levels of digital readiness, as almost 37% of them use telehealth services, while about 32% of individuals use wearables to track their health status. This fact contributes to the integration of new digital tools into trial processes. Moreover, a considerable number of clinical trials are conducted in the U.S., both decentralized and hybrid. Current decentralized clinical trials market trends indicate a strong shift toward hybrid models, increased use of digital endpoints, and growing reliance on AI-driven trial optimization, positioning the United States as the most mature and scalable DCT market globally.

Canada Decentralized Clinical Trials Market Outlook

The decentralized clinical trials market share in North America has been witnessing a gradual growth in Canada owing to its excellent public healthcare services, increased usage of digital health technologies, and a suitable environment for carrying out clinical trials. Though relatively small when compared with the U.S., Canada also makes a significant contribution to the decentralized clinical trials market size in the region through its participation in around 5-6% of the decentralized and hybrid clinical trials across the world, according to available data from multiple studies.

Canada has several factors that play favorably to its advantage in relation to the decentralized clinical trials market analysis. These include a high internet usage rate, advanced telemedicine use, as well as digital health projects funded by the government, allowing virtual consultations, eConsents, and patient monitoring remotely. The legal system in the nation has also been found to align itself more with decentralized clinical trials by allowing for flexible design of such trials while observing strict protocols when it comes to ensuring privacy and safety for patients involved. Some of the current trends in the decentralized clinical trials market in Canada include hybrid trial approaches, wearable medical devices, and collaborations.

Competitive Landscape

- The decentralized clinical trials market is influenced by three distinct yet interrelated categories of participants: global contract research organizations (CROs) and clinical development services providers, decentralized trials technologies platform providers, and more general electronic clinical (eClinical) or life sciences software vendors. The likes of IQVIA, ICON, Labcorp, Parexel, Thermo Fisher Scientific, Syneos Health, and Medpace add muscle in the form of broad clinical trial execution capabilities, patient recruitment, site management, regulatory coordination, and global clinical operation execution. On the other hand, Medable, Science 37, Signant Health, Castor, Viedoc, THREAD Research, Medrio, OpenClinica, and Clinion excel at helping run decentralized or hybrid trials using tools for eConsent, virtual visits, remote patient monitoring, eCOA, direct patient engagement, and digital workflow. Lastly, Oracle, Dassault Systèmes, Veeva Systems, and Clario contribute to the market via clinical data platforms, trial management solutions, data integration, analytics, and digital ecosystem support. In effect, the competitive environment appears very partnership-based as opposed to winner takes all where sustainability hinges on a combination of technology, regulatory excellence, patient focus, and end-to-end clinical trials execution.

- Key players include IQVIA Inc., ICON plc, Labcorp Holdings Inc., Parexel International Corporation, Thermo Fisher Scientific Inc., Oracle Corporation, Dassault Systèmes SE, Medable Inc., Science 37 Holdings, Inc., Signant Health, Syneos Health, Inc., Medpace Holdings, Inc., Veeva Systems Inc., Clario, Castor, Viedoc Technologies AB, THREAD Research, Medrio, Inc., OpenClinica, LLC, and Clinion IT Services Pvt. Ltd.

Key Developments

- Jan 2026 - Medable Inc. debuted its TMF Agent, an AI-powered solution designed to automate trial master file processes and reduce manual document management burden in clinical development.

- Jan 2026 - Veeva Systems Inc. announced Veeva eSource, a new SiteVault application aimed at eliminating paper-based processes and improving clinical trial data flow through EHR and EDC integration.

- March 2026 - Science 37 Holdings, Inc. launched a dedicated Pediatrics Department to expand access to specialized pediatric clinical research through home- and school-based trial support models.

- Jan 2025 - Medable Inc. announced new Tufts CSDD PACT Consortium data showing that decentralized clinical trial components improved representation across several underrepresented participant groups.

- Sep 2024 - Signant Health joined IQVIA’s One Home for Sites initiative to expand access to its eClinical solutions and simplify site workflows across multi-vendor clinical trial environments.

- Sep 2024 - Veeva Systems Inc. released a major upgrade to Veeva Site Connect, adding new capabilities to streamline sponsor-site collaboration and improve trial execution efficiency.

- May 2024 - Science 37 Holdings, Inc. announced the successful FDA inspection of its Metasite model, marking a major compliance milestone for virtual site quality assurance in decentralized clinical trials.

Why Choose DataM?

- Technological Innovations: Highlights the most recent developments in the decentralized clinical trials market, including eConsent solutions, telemedicine adoption, wearables, remote patient monitoring, eCOA technologies, AI-driven analytics, and cloud-based trial management platforms. Digital health technology innovations are enhancing protocol compliance, real-time data collection, patient engagement, and trial efficiency, thus driving the long-term decentralized clinical trials market size.

- Product Performance & Market Positioning: Assesses the performance of key vendors within diverse settings of clinical trials, such as cancer, rare diseases, cardiology, and observational research. Analysis of decentralized clinical trials industry highlights key vendors' differences by assessing their proficiency in patient enrollment, support for virtual visits, capability to provide remote monitoring services, data integration, regulatory compliance, and conducting hybrid clinical trials.

- Real-World Evidence: Provides real-world use cases for decentralized and hybrid clinical trials in various fields and locations. It explains how digital health technology contributes to increasing patient adherence, gaining access to understudied demographics, decreasing site reliance, and continuously monitoring endpoints, supporting the positive decentralized clinical trials market trends.

- Market Updates & Industry Changes: The key industry developments tracked include guidelines, launch of platforms, partnerships, incorporation of AI, wearable monitoring, and growth in hybrid clinical trials. All these developments have a direct impact on the market share dynamics within decentralized clinical trials among CROs, platform companies, and eClinical players.

- Competitive Strategies: Discusses how key organizations are building up their competitive stance within the decentralized clinical trials ecosystem by expanding platforms, focusing on therapeutic areas, designing patient-friendly trials, forming sponsorships, mergers and acquisitions, and integrating services. The ability to leverage the power of technology, regulatory robustness, and global trials is now a crucial factor in competitiveness.

- Pricing & Market Access: Discusses pricing mechanisms within decentralized trial services such as platform licensing, per-trial pricing, modular offerings, and full-outsourcing services. In addition, this section addresses access-related issues like regulatory readiness, digital health technology readiness, investigator adoption, and patient access to technologies. All of these play an important role in determining the market size and adoption rate for decentralized clinical trials.

- Market Entry & Expansion: Market Growth Strategies and Opportunities: Highlights market expansion opportunities that arise in developing markets with evolving health technology digital infrastructure and where sponsors have an interest in expanding their patient pools. Also includes information on how organizations can expand through a hybrid business model, partnering with healthcare providers in a region, using multi-language digital platforms, and deploying devices.

Target Audience 2026

- Pharmaceutical and Biotechnology Companies: Pharmaceutical companies developing drugs or sponsors sponsoring clinical trials using digital health technologies to enhance the process of recruiting patients, retaining them, and streamlining trials in the decentralized clinical trials industry.

- Contract Research Organizations (CROs): International and regional contract research organizations delivering services from trial execution to patient management and hybrid and decentralized trial models, being significant players in contributing to the growth of the decentralized clinical trials market.

- Healthcare Facilities: Clinics, hospitals, and investigative sites utilizing decentralized aspects, such as virtual visits, remote monitoring, and provision of treatment locally.

- Technology and Platform Providers: eClinical platforms, eConsent, telehealth, wearable technologies, and data analytics firms providing solutions that facilitate decentralized and hybrid trial approaches, impacting decentralized clinical trials market trends.

- Regulatory and Government Bodies: Health organizations setting up guidelines and policies that will determine decentralized clinical trials market trends and their adoption in different regions.

- Patients and Patient Advocacy Organizations: Patients who use decentralized trials, as well as organizations advocating for patients' rights to benefit from these new methods of conducting trials.

- Investment Funds and Venture Capitalists: Investment firms interested in expanding in clinical trials platforms, digital health technologies, and CRO services, hence contributing to innovations in the decentralized clinical trials market.

- Logistics and Home Healthcare Providers: Service providers who ensure smooth drug delivery to patients and remote care for them, facilitating seamless conduct of trials.

Suggestions for Related Report