Veterinary Vaccines Market Overview

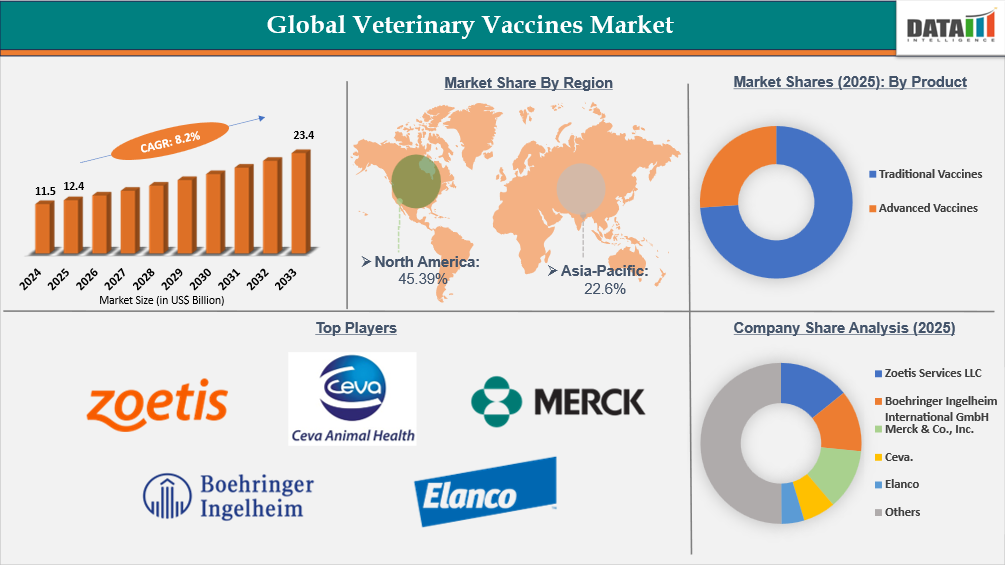

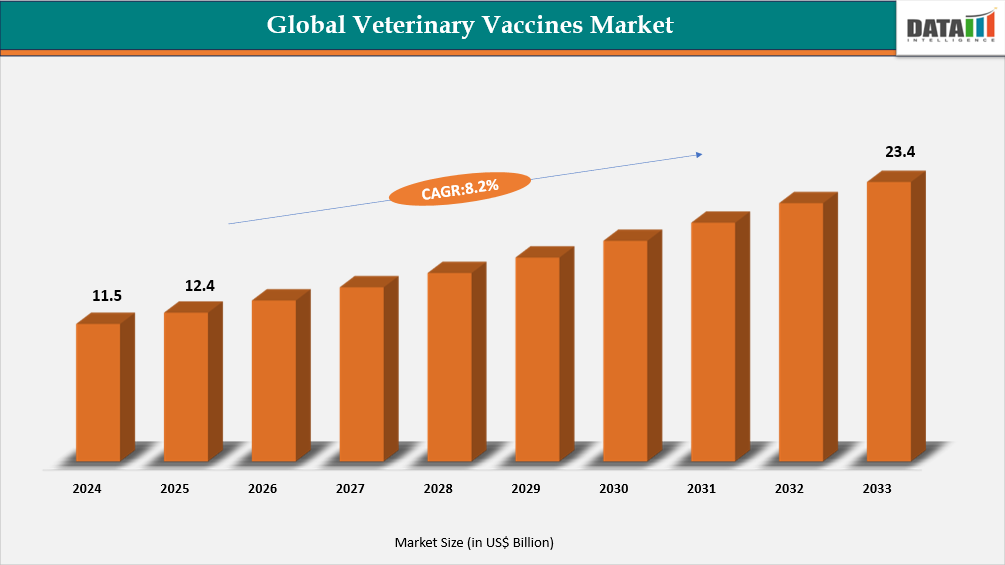

The Global Veterinary Vaccines market reached US$11.5 Billion in 2024, rising to US$12.4 Billion in 2025 and is expected to reach US$23.4 Billion by 2033, growing at a CAGR of 8.2% from 2026 to 2033.

Market growth is largely driven by the increasing need to control infectious diseases across livestock, poultry, and companion animals, along with rising awareness of preventive animal healthcare. Veterinary vaccines play a crucial role in maintaining animal health, improving livestock productivity, and protecting global food supply chains.

According to the Food and Agriculture Organization (FAO), the livestock sector contributes around 40% of global agricultural output, highlighting the economic importance of maintaining animal health through vaccination and disease prevention programs. In addition to livestock vaccination, the expanding companion animal population and increasing spending on pet healthcare are further strengthening market demand. At the same time, rapid advancements in biotechnology are enabling the development of next-generation vaccines, including recombinant, subunit, vector-based, and nucleic acid vaccines that offer improved safety and targeted immune responses. Supported by stronger disease surveillance systems, government immunization initiatives, and increasing investment in animal health innovation, the global veterinary vaccines market is expected to experience sustained growth in the coming years.

Veterinary Vaccines Industry Trends and Strategic Insights

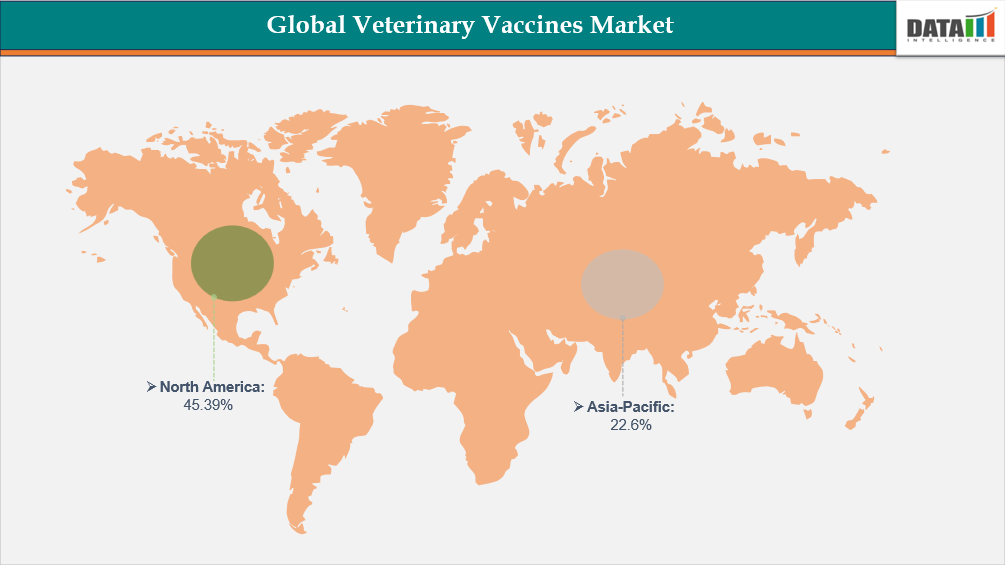

- North America leads the global veterinary vaccines market, capturing the largest revenue share of 45.39% in 2025.

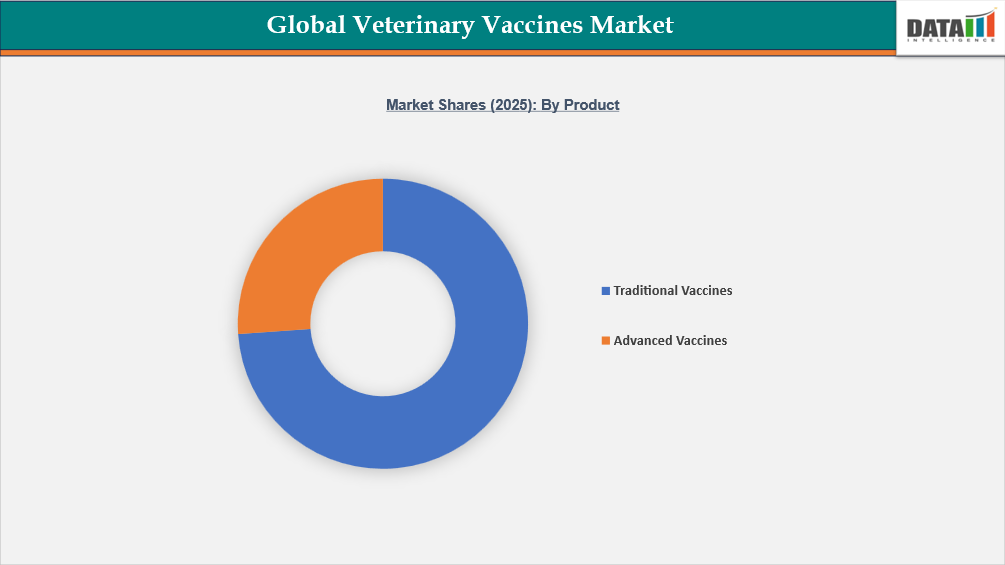

- By Product, traditional vaccines led the global veterinary vaccines market, capturing the largest revenue share of 73.87% in 2025.

Global Veterinary Vaccines Market Size and Future Outlook

- 2025 Market Size: US$12.4 Billion

- 2033 Projected Market Size: US$23.4 Billion

- CAGR (2026–2033): 8.2%

- Dominating Market: North America

- Fastest Growing Market: Asia-Pacific

For more Information, Request for Sample

Market Dynamics

Rising threat of zoonotic disease transmission between animals and humans, accelerating preventive vaccination adoption

According to the World Health Organization, approximately 60% of known human infectious diseases and nearly 75% of emerging infectious diseases originate in animals, underscoring the strong link between animal and human health. This growing risk of zoonotic disease transmission has significantly increased the importance of veterinary vaccination programs worldwide. In regions with high livestock density and frequent human–animal interaction, infectious diseases can easily spread from animals to humans if proper preventive measures are not in place. Diseases such as rabies, avian influenza, brucellosis, and swine-origin viral infections demonstrate how animal disease outbreaks can quickly evolve into broader public health and economic challenges.

Veterinary vaccination plays a critical role in controlling pathogen circulation within animal populations and reducing the risk of cross-species transmission. Preventing zoonotic outbreaks through vaccination is far more cost-effective than managing large-scale epidemics that can disrupt food supply chains and livestock production systems. In addition, the global adoption of the “One Health” approach, which integrates human, animal, and environmental health management, is further reinforcing the importance of preventive animal healthcare and supporting the long-term growth of the veterinary vaccines market. As a result, governments, livestock producers, and international health organizations are increasingly prioritizing structured vaccination programs and strengthening veterinary healthcare infrastructure.

Segmentation Analysis

The global veterinary vaccines market is segmented based on animal type, product, route of administration, end user, disease indication, and region.

Traditional Vaccines Lead While Advanced Vaccines Drive Fastest Growth in the Global Veterinary Vaccines Market

The global veterinary vaccines market is broadly divided into traditional vaccines and advanced vaccines, reflecting the evolution of immunization technologies in animal healthcare. Traditional vaccines, which include live attenuated, inactivated, and toxoid vaccines, currently dominate the market, accounting for approximately 73.87% of global revenue. Their widespread adoption is driven by established efficacy, lower manufacturing costs, and large-scale use in livestock vaccination programs for diseases such as rabies, foot-and-mouth disease, and avian influenza. These vaccines remain the backbone of animal health initiatives, particularly in emerging regions where affordability and accessibility are critical factors.

In contrast, advanced vaccines, including recombinant, subunit, vector-based, DNA, and mRNA vaccines, account for around 26.13% of the market but represent the fastest-growing segment. These next-generation vaccines offer improved safety, targeted immune responses, and the ability to address emerging and complex animal diseases. Increased investment in biotechnology, rising awareness of zoonotic disease prevention, and the growing focus on companion animal healthcare are accelerating the adoption of advanced vaccines. As a result, while traditional vaccines maintain their market dominance, advanced vaccines are expected to expand rapidly, reshaping the competitive landscape of the global veterinary vaccines market.

Geographical Penetration

Largest Market:

Rising Demand for Veterinary Vaccines in North America

North America represents the largest market for veterinary vaccines, accounting for approximately 45.39% of global market revenue. The strong demand in the region is primarily driven by well-established veterinary healthcare infrastructure, high adoption of preventive animal healthcare practices, and robust livestock and companion animal populations.

The United States and Canada have extensive vaccination programs aimed at controlling infectious diseases in livestock and companion animals, thereby supporting consistent demand for veterinary vaccines. In addition, high pet ownership rates and increasing expenditure on animal health further contribute to market growth. The presence of leading animal health companies, continuous investment in research and development, and supportive regulatory frameworks also strengthen North America’s leadership in the global veterinary vaccines market.

U.S. Veterinary Vaccines Market Outlook

The U.S. veterinary vaccines market is the largest and most technologically advanced segment of the global animal health industry, driven by strong livestock production, high companion animal ownership, and widespread adoption of preventive veterinary care. The country benefits from a highly structured animal disease surveillance and vaccination ecosystem led by regulatory bodies such as the USDA, which promotes routine immunization programs for livestock, poultry, and companion animals.

According to the 2025 APPA National Pet Owners Survey, 94 million U.S. households own a pet, significantly boosting demand for routine vaccinations and preventive veterinary services. In addition, continuous investment in vaccine innovation, including recombinant, subunit, vector-based, and nucleic acid vaccines, along with growing awareness of zoonotic disease risks, is further fueling market expansion. As a result, the U.S. veterinary vaccines market is expected to maintain steady growth, supported by both livestock biosecurity initiatives and increasing expenditure on companion animal healthcare.

Canada Veterinary Vaccines Market Trends

The Canadian veterinary vaccine market is experiencing steady growth, supported by the expansion of the livestock and poultry industries, increasing awareness of animal health, and a large companion animal population. Livestock producers are prioritizing preventive vaccines against diseases such as bovine respiratory disease, porcine reproductive and respiratory syndrome, and avian influenza, backed by strong veterinary infrastructure and government programs.

On the companion animal side, Canada has approximately 8.5 million cats and 7.9 million dogs, according to the CVMA, creating strong demand for routine vaccinations and advanced vaccine technologies. The market is also witnessing a shift toward biological and recombinant vaccines that provide improved safety and targeted immune responses. Combined with stringent regulations, active disease surveillance, and growing “One Health” initiatives, these factors are driving both market expansion and innovation in animal healthcare across the country.

Fastest Growing Market:

Asia-Pacific Emerges as the Fastest Growing Veterinary Vaccines Market

The Asia-Pacific veterinary vaccines market is emerging as the fastest-growing regional segment globally, driven by rising livestock and poultry production, increasing pet ownership, and growing awareness of animal health and biosecurity. Countries such as China, India, Japan, and Southeast Asian nations are witnessing strong demand for both traditional and advanced vaccines, fueled by government-led immunization programs and the expansion of commercial livestock farming. On the companion animal side, rising pet adoption and increasing expenditure on preventive veterinary care are further accelerating market growth.

According to industry estimates, the Asia-Pacific region accounts for roughly 22.6% of the global veterinary vaccines market, reflecting the rapid adoption of vaccines and rising investment in animal healthcare infrastructure. Additionally, the shift toward recombinant, vector-based, and nucleic acid vaccines, coupled with active disease surveillance and growing awareness of zoonotic risks, is reinforcing the region’s position as a key growth driver in the global veterinary vaccines market.

India Veterinary Vaccines Market Insights

The Indian veterinary vaccines market is witnessing significant growth, driven by the country’s vast livestock population and the increasing emphasis on animal disease prevention. India is home to more than 536 million livestock, the largest livestock population globally, and nearly 70% of rural households depend on animals for income, food, and livelihood security. This heavy dependence on livestock has made disease prevention through vaccination a critical component of the country’s animal health strategy.

Government-led vaccination initiatives are playing a central role in strengthening the market. Large-scale programs targeting major livestock diseases have accelerated vaccine adoption across the country. In 2024 alone, around 44.57 crore doses of Foot-and-Mouth Disease (FMD) vaccines and 1.6 crore doses of Brucella vaccines were administered in India, highlighting the scale of national immunization efforts. These initiatives, combined with the rapid expansion of the dairy, poultry, and livestock sectors, are significantly driving demand for veterinary vaccines.

China Veterinary Vaccines Market Industry Growth

The Chinese veterinary vaccines market is expanding steadily, supported by the country’s large livestock population, increasing meat consumption, and strong government focus on animal disease prevention. China has one of the world’s largest pork and poultry industries, creating substantial demand for vaccines to control infectious diseases and protect food supply chains. The rapid industrialization of livestock farming and improved veterinary healthcare infrastructure are further accelerating vaccine adoption across large-scale commercial farms.

Government-led disease prevention programs and stricter biosecurity regulations are also strengthening vaccination demand. According to the National Bureau of Statistics of China, the total output of pork, beef, mutton, and poultry reached 96.41 million tons in 2023. The scale of meat production highlights the critical importance of disease prevention strategies, including vaccination, to maintain livestock productivity and ensure food security. As China continues to modernize its animal husbandry sector and strengthen disease surveillance systems, the demand for veterinary vaccines is expected to remain strong, supporting continued growth of the market.

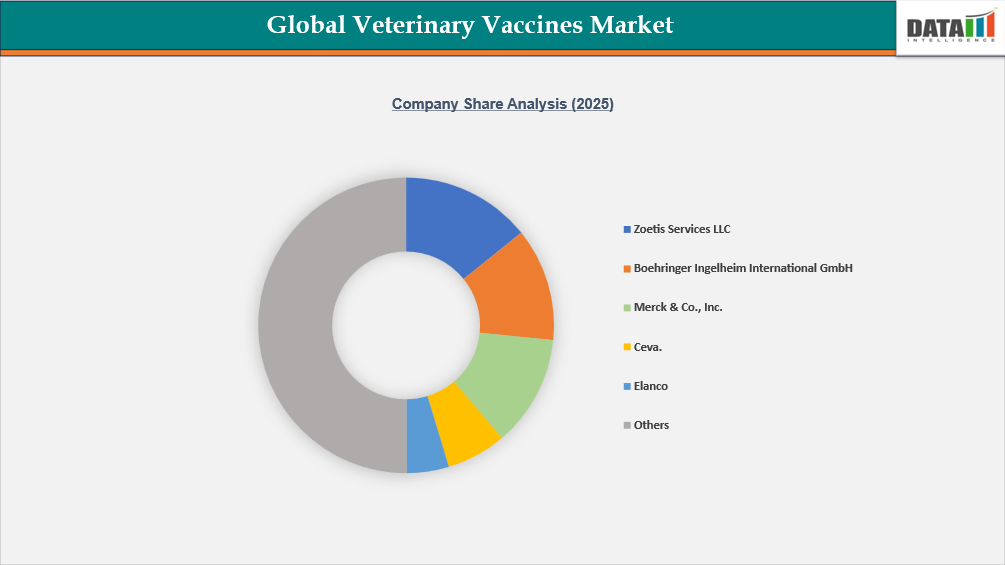

Competitive Landscape

The global veterinary vaccines market is moderately consolidated, with several multinational animal health companies dominating the competitive landscape through strong product portfolios, global distribution networks, and continuous investment in research and development. Leading players such as Merck & Co., Inc., Zoetis Services LLC, and Boehringer Ingelheim International GmbH hold significant market shares due to their extensive vaccine portfolios covering livestock, poultry, and companion animals. These companies focus on innovation and the development of advanced vaccines to address emerging animal diseases and improve preventive healthcare in animal populations.

Other important participants, including Ceva, Elanco, Virbac, Phibro Animal Health Corporation, Biogénesis Bagó, Neogen Corporation, and Bimeda Biologicals, contribute to the market through specialized vaccine products, regional manufacturing capabilities, and strategic collaborations. These companies are expanding their presence in emerging markets and investing in advanced vaccine technologies to strengthen their competitive positioning in the global veterinary vaccines industry.

Key Developments

- In February 2025, Zoetis received a conditional license from the United States Department of Agriculture (USDA), Center for Veterinary Biologics (CVB) for its Avian Influenza Vaccine, H5N2 Subtype, Killed Virus, specifically formulated for use in chickens. The conditional license was granted based on demonstrated safety, purity, and a reasonable expectation of efficacy, supporting poultry producers in their efforts to manage and control outbreaks of highly pathogenic avian influenza.

- In February 2025, Elanco Animal Health entered into a strategic agreement with South Dakota‑based Medgene to jointly commercialize a highly pathogenic avian influenza (HPAI) H5N1 vaccine for dairy cattle in the United States. Under the agreement, Elanco will leverage Medgene’s USDA‑approved vaccine platform technology to bring this HPAI vaccine to market, with the vaccine already meeting all U.S. Department of Agriculture platform technology guidelines and being in the final stages of review for conditional license approval.

What Sets This Global Veterinary Vaccines Market Intelligence Report Apart

- Latest Data & Forecasts – Comprehensive and up-to-date market intelligence with forecasts through 2033, covering global demand segmented based on animal type, vaccine product (traditional vs advanced), route of administration, end user, and disease indication, with region-wise analysis across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa.

- Regulatory Intelligence – In-depth assessment of global veterinary regulatory frameworks impacting vaccine development and commercialization, including FDA (Center for Veterinary Biologics), EMA (Veterinary Medicines Division), NMPA, PMDA, and CDSCO requirements, clinical trial pathways, safety and labeling standards, licensing, and post-marketing surveillance.

- Competitive Benchmarking – Structured benchmarking of leading veterinary vaccine manufacturers based on product portfolios, pipeline strength, geographic reach, pricing strategies, technological differentiation (biologicals, recombinant vaccines), and partnerships in animal health.

- Geographic & Emerging Market Coverage – Regional analysis highlighting livestock and companion animal disease prevalence, vaccination adoption rates, access to veterinary vaccines, and distribution infrastructure, with special focus on growth opportunities in Asia-Pacific, Latin America, and Middle Eastern markets.

- Actionable Strategies & Cost Dynamics – Strategic insights into product lifecycle management, adoption of advanced vaccines, cost structures of manufacturing biological and recombinant vaccines, pricing pressures, and market entry opportunities, supported by expert perspectives from veterinary specialists, regulatory advisors, and animal health executives.