Green Hydrogen Testing Market Overview

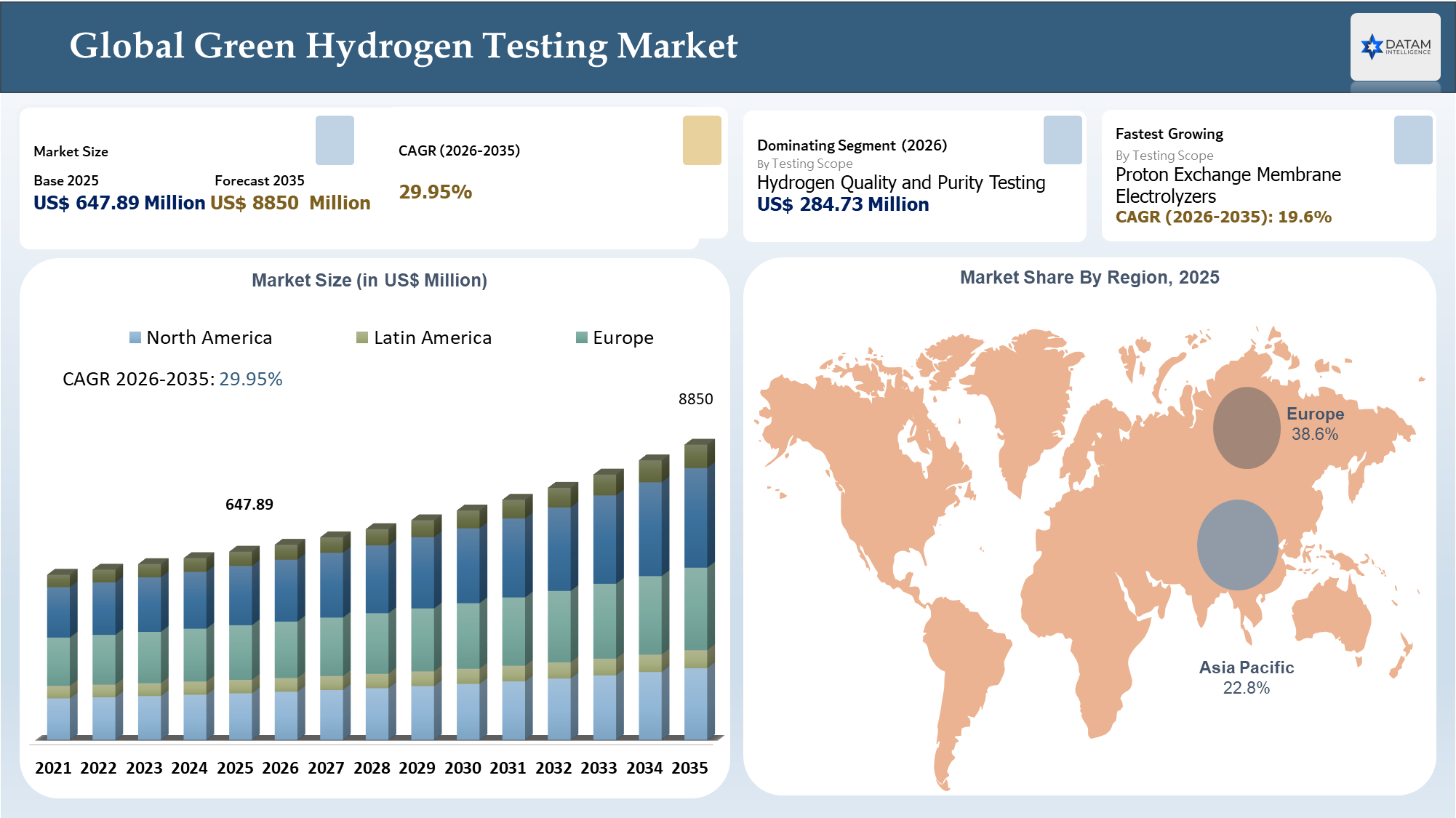

The Global Green Hydrogen Testing Market reached US$ 647.89 million in 2025 and is expected to reach US$8850 million by 2035, growing with a CAGR 29.95% during the forecast period 2026-2035. The Green Hydrogen Testing Market represents an emerging market segment that acts as an important layer of assurance in respect of commercial scale hydrogen production, storage, transport, and consumption. Hydrogen purity testing, impurity testing, electrolyzer performance validation, safety assessment, hydrogen leak detection, material compatibility testing, metering and calibration validation services form the basis of this market. Testing demands are growing in light of the growth in electrolyzer installations and the demand for validated information from electrolysis projects in order to make offtakes, raise financing, and obtain safety approvals.

According to the International Energy Agency (IEA), global electrolyzer manufacturing capacity grew to 25 GW per year in 2023, while annual pipeline project capacity to 2030 is over 165 GW per year. Regulation is also adding to demand, particularly in Europe, where renewables-derived hydrogen needs to reach at least 70% greenhouse gas emissions reduction compared to natural gas.

AI Impact Analysis

The AI market is boosting the green hydrogen testing market by moving testing from being merely a validation process to becoming a predictive one that uses data. Using AI, testing agencies can detect issues such as electrolyzer performance decline, impurity levels, pressure changes, leakage possibilities, and materials that have been exposed to extreme temperatures, all of which could lead to safety problems. For manufacturers of electrolyzers and green hydrogen companies, AI helps make the test cycle more efficient through analysis of operational data, including variations in voltage, efficiencies of stacks, water quality, temperatures, pressures, and hydrogen flow consistency. On the other hand, when it comes to infrastructure testing, the AI-powered testing process includes creating digital twins, automatic inspection, sensors, and anomaly detection for compressors, storage tanks, valves, dispensers, and pipelines. The biggest business impact of AI would be quicker certification, less failure possibility, lower reliance on manual inspections, and higher asset reliability.

Green Hydrogen Testing Industry Trends and Strategic Insights

- Demand for green hydrogen testing will increase because governments are introducing stricter regulations in the form of certifications of renewable hydrogen, carbon intensity, safety, and traceability standards, thus requiring third-party testing for green hydrogen projects and off-take opportunities

- Validation of electrolyzers will continue to be a major revenue stream as PEM, alkaline, solid oxide, and anion-exchange electrolyzers will need testing for efficiency, robustness, product purity, and degradation before commercial-scale deployment

- Testing of safety and infrastructure requirements for hydrogen will grow with hydrogen moving into hydrogen storage, pipelines, fueling stations, export, and industrial applications.

- Government policy-driven adoption will boost testing requirements in particular, where green hydrogen policy support measures such as hydrogen incentives, blending programs, mobility initiatives, industry decarbonization schemes, and export certification will become a key part of projects' commercial viability..

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 647.89 Million | |

| 2035 Projected Market Size | US$ 8850 Million | |

| CAGR (2026-2035) | 29.95% | |

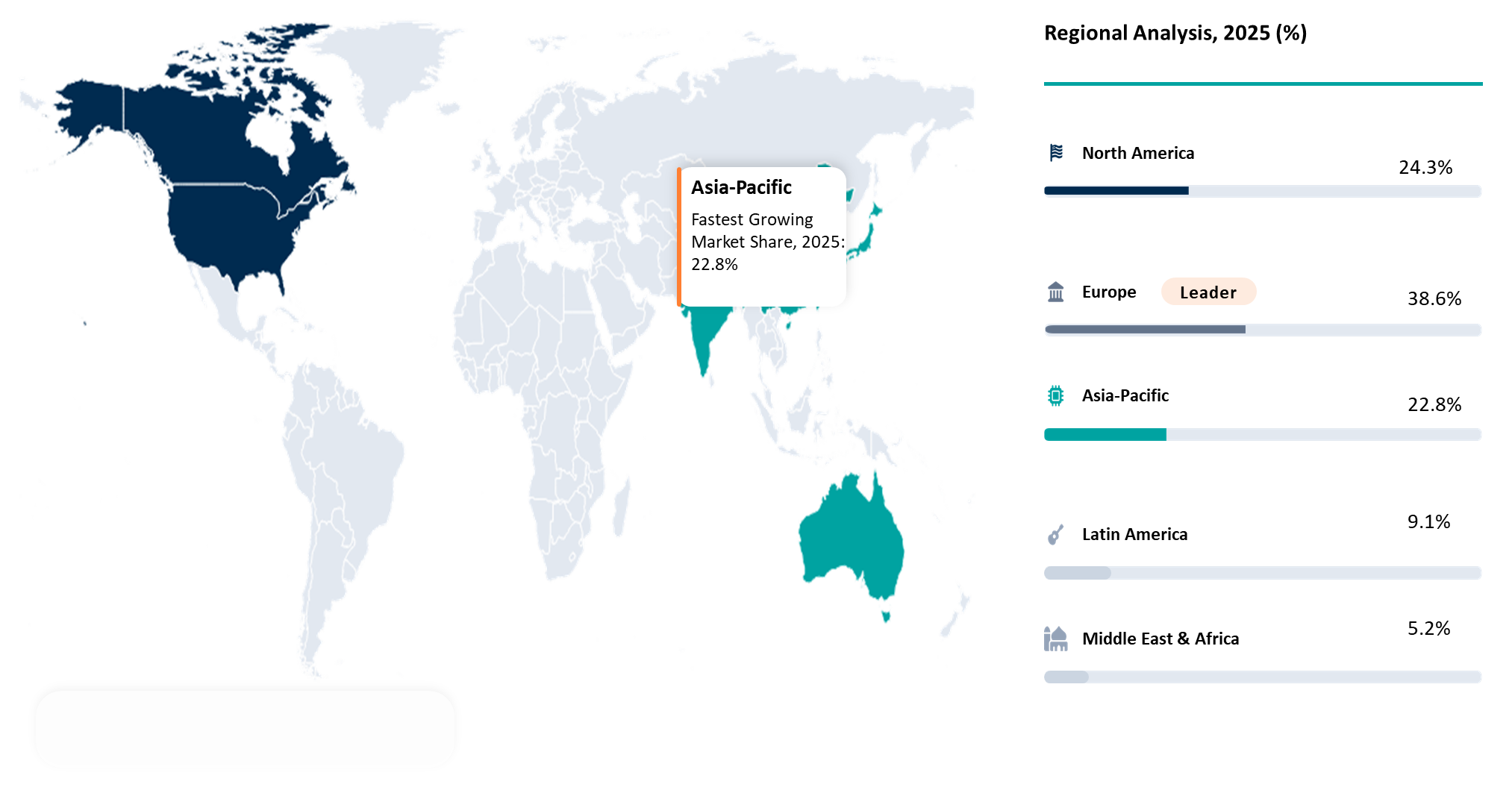

| Largest Market | Europe | |

| Fastest Growing Market | Asia-Pacific | |

| By Testing Scope | Hydrogen Quality and Purity Testing, Electrolyzer Performance Validation, Safety and Leak Detection Testing, Materials Compatibility Testing, Pressure and Mechanical Integrity Testing, Environmental and Durability Testing, Regulatory Compliance Testing | |

| By Value Chain Stage | Feedwater and Input Assessment, Electrolysis Process Validation, Hydrogen Output Verification, Compression and Conditioning, Storage and Handling, Transportation and Distribution, Dispensing and End-Use Interface | |

| By Technology Tested | Proton Exchange Membrane Electrolyzers, Alkaline Electrolyzers, Solid Oxide Electrolyzers, Anion Exchange Membrane Electrolyzers, Fuel Cell Systems, Others | |

| By Service Model | Laboratory Testing Services, Field Testing and Inspection Services, Calibration and Measurement Services, Certification and Compliance Services, Failure Analysis and Root Cause Assessment, Technical Advisory Services | |

| By End User | Green Hydrogen Project Developers, Electrolyzer Manufacturers, Fuel Cell Manufacturers, Industrial Gas Companies, Energy Utilities, Hydrogen Infrastructure Operators, Industrial Hydrogen Consumers, Testing Inspection and Certification Bodies | |

| By Business Model | Carbon Credit Sales, Long Term Offtake Agreements, Carbon Removal as a Service, Integrated Capture and Storage Projects, Marketplace and Aggregator Model, and Others | |

| By Application Area | Industrial Process Decarbonization, Hydrogen Mobility and Fuel Cells, Renewable Energy Storage, Refining and Chemical Processing, Green Steel and Metals Production, Power Generation and Grid Balancing, Hydrogen Export and Trading | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

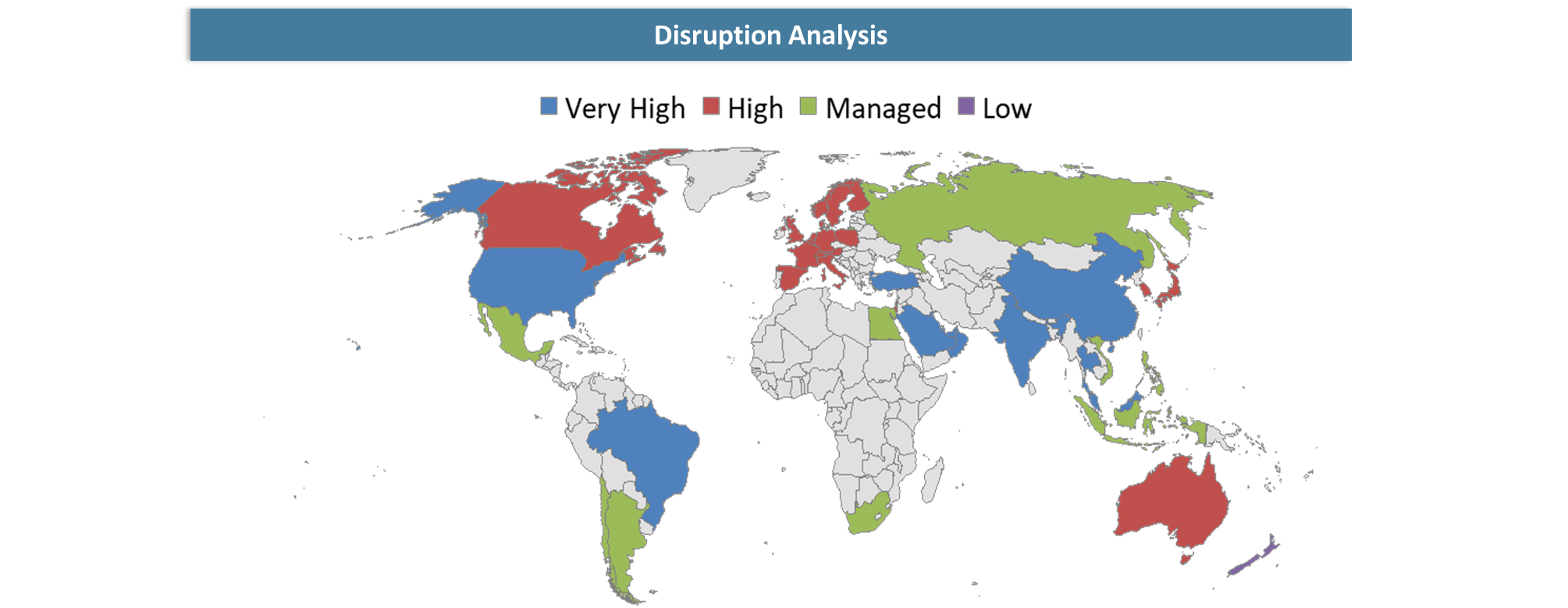

Disruption Analysis

AI-Enabled Certification and Digital Assurance Are Redefining Green Hydrogen Testing

Disruption in the Green Hydrogen Testing Market involves the move away from the conventional model of manual and periodic tests towards the continuous use of sensors and analysis of data to ensure safety and effectiveness through the production, storage, transportation, and utilization phases of the hydrogen value chain. Larger hydrogen projects require efficient verification of the parameters including the hydrogen’s purity, its carbon intensity, efficiency of the electrolyzer, its potential leakages, pressure changes, and suitability of materials. It becomes increasingly difficult to provide laboratory-based solutions to such needs especially for large-scale projects, exportation, mobility infrastructure, and industrial off-takers. Disruptors of the market, therefore, should be TIC companies able to offer both laboratory services and field inspections, certifications, and digital monitoring among other capabilities. For clients, the key benefit lies in the provision of continuous insights regarding risks, faster readiness, and minimal downtime.

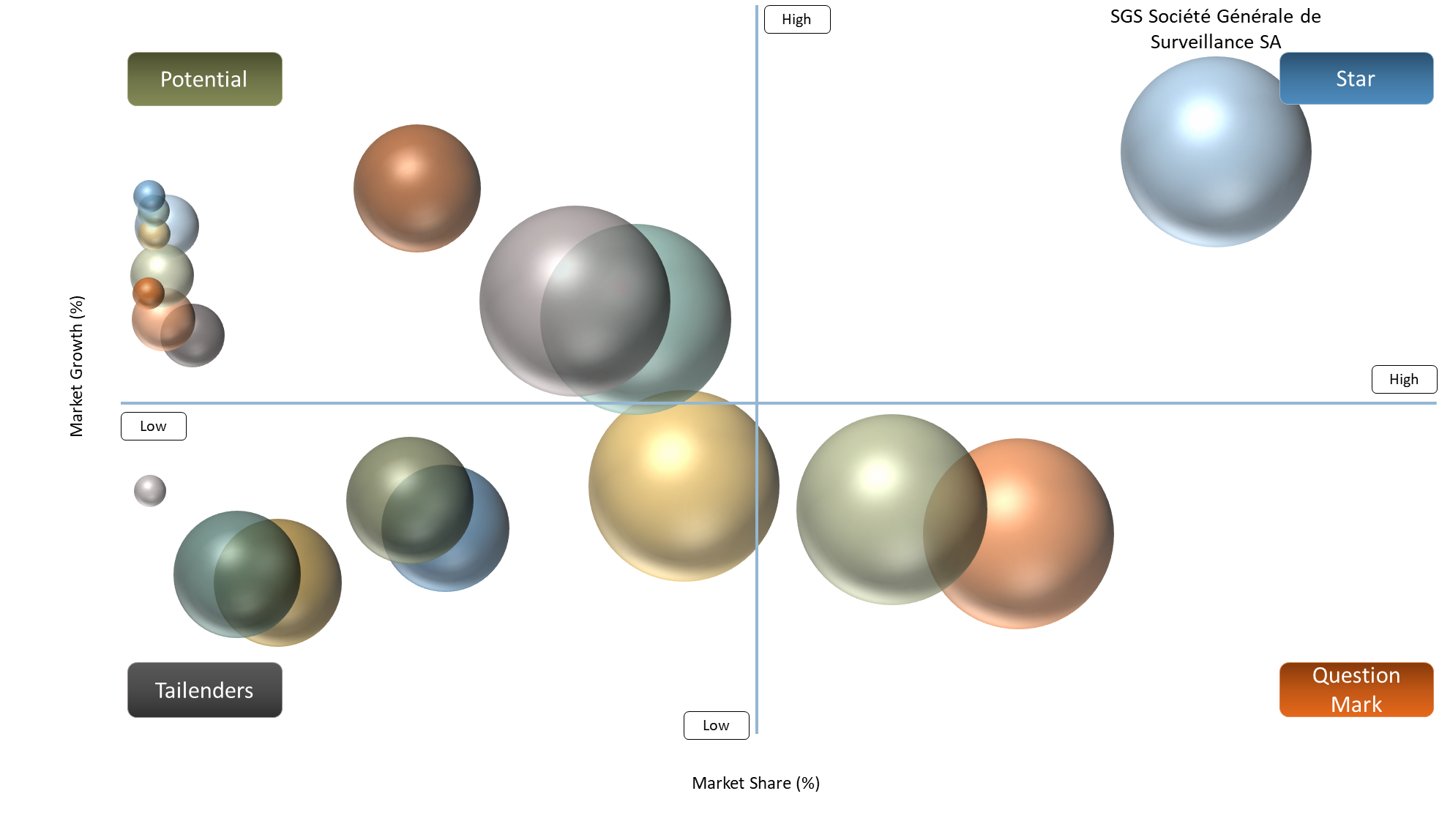

BCG Matrix: Company Evaluation

SGS Société Générale de Surveillance SA, Bureau Veritas, Intertek, TÜV SÜD AG, DNV AS and TÜV Rheinland constitute the most competitive set of players owing to their global TIC presence, hydrogen certification experience, laboratory facilities and capability to facilitate multi-country green hydrogen projects.

The DEKRA, TÜV NORD GROUP, UL LLC and LRQA Group Limited are solid and reputable competitors given their well-established portfolio of safety, certification, audit and compliance services. The potential for these firms lies in their ability to capitalize on recurring demand for hydrogen equipment approval, infrastructure safety assessment, refueling stations inspection, QA and lifecycle testing as green hydrogen projects transition towards production.

Applus+, Kiwa, RINA S.p.A. and Element Materials Technology provide an excellent portfolio of specialized testing services particularly for hydrogen pipeline and pressure systems testing, hydrogen components testing, materials compatibility and failure analysis. This presents the opportunity for these firms to build a robust testing infrastructure around green hydrogen applications.

AVL has an innovative position in terms of technology, with a specialization in electrolysis, fuel cells, hydrogen-based powertrains, and system performance validation. Such a position will be more relevant for OEMs, technology providers, and research and development firms than for firms requiring inspection and testing.

Market Dynamics

Renewable Hydrogen Certification and Carbon-Intensity Verification Are Driving Third-Party Testing Requirements

Certification of renewable hydrogen and carbon-intensity verification are emerging as key motivators for the green hydrogen testing market since project developers have to demonstrate their ability to produce hydrogen from renewables along with meeting certain emission thresholds. In this scenario, buyers, regulatory authorities, investors, and off-takers are demanding proof for hydrogen production that includes the source of electricity, production process, and carbon emissions along with the grade of the product. Hence, there would be a need for companies involved in hydrogen testing, inspections, and certifications who can certify the purity of hydrogen, efficiency of electrolyzers, carbon emissions, and metering along with other parameters. The introduction of RFNBOs under the European Union, clean hydrogen tax credits, national hydrogen certification, and export requirements are expected to drive green hydrogen projects into undergoing third-party testing and certification services.

Limited Specialized Testing Laboratories Can Delay Validation and Certification Timelines

The certification of renewable hydrogen and carbon intensity measurement are gaining momentum as major drivers of the Green Hydrogen Testing Market because, during the project development stage, developers must prove their competence to generate hydrogen using renewable energy resources along with satisfying particular emission standards. In this case, customers, regulating agencies, financiers, and offtakers will require evidence of hydrogen generation that should include power source, method of production, carbon emissions, as well as quality of the commodity. Therefore, there will be a demand for hydrogen testing organizations capable of certifying hydrogen purity, electrolyzer performance, carbon emissions, measurement, and other variables. The development of Renewable Fuel Number-Based Obligations (RFNBOs) by the European Union, hydrogen tax credits, national hydrogen certification, and exportation requirements will likely propel green hydrogen projects to seek third-party testing and certification services.

Segmentation Analysis

The Global Green Hydrogen Testing Market is segmented based on the testing scope, value chain stage, technology tested, service model, end user, application area, and region/countries.

Hydrogen Quality and Purity Testing Leads the Market as Strict Fuel-Grade Standards Drive Compliance Demand

Hydrogen Quality and Purity Testing will remain dominant in the Green Hydrogen Testing Market due to stringent requirements for impurities in fuel cell and mobility grade hydrogen. According to the ISO 14687:2019 standard, hydrogen fuel should have a minimum purity index of 99.97%, while total impurity content other than hydrogen gas will be restricted to 300 μmol/mol, with 5 μmol/mol each of water and oxygen, 100 μmol/mol methane, and 2 μmol/mol total hydrocarbons other than methane. Such stringency demands a thorough purity test to ensure that hydrogen meets the required quality before distribution through refueling stations, fuel cells, storages, pipelines, exports, and offtake contracts. The market relevance is also growing in Europe since the EU mandates at least 70% greenhouse gas savings for renewable hydrogen production.

Geographical Penetration

North America’s Hydrogen Hub Expansion and Carbon-Intensity Compliance Strengthen Testing Demand

The market for hydrogen testing in North America consists of the USA hydrogen hub, clean hydrogen investment in Canada and renewable hydrogen development potential in Mexico, resulting in increased demand from more than one country. The USA Regional Clean Hydrogen Hubs initiative aims at constructing a nationwide hydrogen network for production, consumption, and logistics, hence driving increased demand for hydrogen purity testing, commissioning tests, hydrogen storage, delivery, and end-use testing services.

Moreover, Canada provides regional depth with about 80 low-carbon hydrogen projects and over US$100 billion investment potential in the region, leading to increased demand for testing carbon intensity reduction, electrolysis validation, export certification, and industrial hydrogen application. Lastly, Mexico increases the value of the regional demand for the testing services due to abundant renewable energy potential for green hydrogen production and energy storage.

U.S. Green Hydrogen Testing Market Trends

U.S. Green Hydrogen Testing Market is experiencing rapid growth due to the transition of green hydrogen projects from conceptualization to validation of their feasibility. The US DOE's Regional Clean Hydrogen Hubs program aims at establishing a nationwide network of hydrogen producers, consumers, and associated infrastructures in production, storage, transportation, and application. This, in turn, would drive the demand for testing of hydrogen purity, electrolyzer efficiency, hydrogen storage safety, hydrogen pipeline integrity, and project validation.

The key market driver includes a total of US$7 billion federal investment into seven regional clean hydrogen hubs through funding from over US$40 billion in selected project cost share that would necessitate rigorous testing and certification processes during development, installation, and operation of projects. Moreover, the US DOE's Clean Hydrogen Production Standard aims at targeting the reduction of lifecycle emissions of ≤4.0 kg CO2e per kg H2, hence validating the production cycle and carbon intensity.

Asia-Pacific’s Green Hydrogen Industrial Scale-Up Strengthens Testing and Certification Demand

The Asia-Pacific Testing Services for Green Hydrogen Market is experiencing increased interest due to countries such as India, Japan, Australia, China, and South Korea shifting from hydrogen projects on a pilot level to the implementation of projects on an industrial scale including imports, production, mobility, and exports-related projects. India plans to generate 5 MMT (million metric tonnes) of green hydrogen production every year by 2030, utilizing approximately 125 GW of renewable energy, thus requiring testing for hydrogen production electrolyzers, hydrogen purity, emission, and certification. In its plan of implementing hydrogen on a commercial basis, Japan seeks to have hydrogen and ammonia available for domestic use in quantities amounting to 3 million tonnes of supply by 2030, 12 million tonnes by 2040, and 20 million tonnes by 2050, thus requiring testing services for imported hydrogen, hydrogen and ammonia handling, fuel cells, and power generation projects.

Japan Green Hydrogen Testing Market Trends

The Japan Green Hydrogen Testing Market benefits from the presence of an active hydrogen mobility and technology validation environment in the country. By the end of 2024, Japan will have 161 hydrogen refueling stations, positioning itself as one of the leading markets for hydrogen mobility in Asia, which results in the need for hydrogen dispenser testing, pressure testing, leak testing, hydrogen purity testing, and safety testing. Additionally, the Japan Green Innovation Fund has set aside a budget of up to JPY 107.05 billion for the production of hydrogen via water electrolysis using renewable energy sources.

Competitive Landscape

- The Green Hydrogen Testing market is witnessing increased competition, driven by the growth of testing, inspection and certification firms worldwide offering their services and solutions specifically for hydrogen. Some players in the market who have the ability to gain from the growing need for green hydrogen testing include SGS Société Générale de Surveillance SA, Bureau Veritas, Intertek, DEKRA, TÜV SÜD AG, DNV AS, TÜV Rheinland, Applus+, TÜV NORD GROUP, Element Materials Technology, UL LLC, Kiwa, RINA S.p.A., LRQA Group Limited and AVL. Currently, green hydrogen testing is a service-based market; however, the differentiation between competitors will lie in the extent of integrated assurance provided by firms to their clients during the validation of design and commissioning stage as well as certification.

- Leading companies such as SGS Société Générale de Surveillance SA, Bureau Veritas, Intertek, DEKRA, TÜV SÜD AG, DNV AS, TÜV Rheinland and TÜV NORD GROUP have an advantage over others owing to their wide network of laboratories, certifications services, knowledge of regulations, and experience in energy, mobility, industrial gases and infrastructure sector. Specialized companies like Element Materials Technology, UL LLC, Kiwa, RINA S.p.A., LRQA Group Limited and AVL increase competition by offering material testing services, components testing, safety certifications, fuel cell testing services and electrolyzers testing. For the future, it can be expected that competitors who offer a combination of laboratory tests, inspections on-site, digital monitoring services, carbon intensity verification, and hydrogen certifications would become more popular because of green hydrogen testing being required for bankability and commercialization purposes.

Key Developments

- March 2026: DNV AS highlighted gas quality tracking for diversifying gas networks, covering practical challenges around RNG, biomethane and hydrogen blending in pipeline systems. This supports demand for gas quality monitoring, blending validation and pipeline testing services.

- August 2025: RINA S.p.A. and Nikon SLM Solutions signed an LOI to establish H2AM Open Lab for hydrogen applications in additive manufacturing, supporting material and process validation for hydrogen-related sectors.

- July 2025: RINA S.p.A. successfully conducted laboratory testing on steel linepipe materials for Jindal SAW Ltd to assess suitability for hydrogen service, supporting pipeline conversion and hydrogen transportation safety.

- December 2024: DNV AS released DNV-ST-J301, a standard for electrolyser systems, providing technical requirements for certification, safety evaluation and component-level assessment in hydrogen production systems.

- November 2024: AVL expanded AVL FIRE M simulation software to support alkaline electrolyzer cell and stack design optimization, strengthening testing-led development for gas bubble removal, heat dissipation and electrochemical performance.

- February 2024: TÜV SÜD AG received accreditation for testing and certification of hydrogen generation systems under ISO 22734, supporting safety, quality and performance validation for electrolyzer manufacturers.

- October 2023: RINA S.p.A. advanced the HYDRA project, which includes new hydrogen material testing laboratories in Italy, with civil works planned from end-October 2023 and lab equipment installation targeted by Q3 2025.

- January 2023: DNV AS highlighted that green hydrogen certification may need to cover equipment safety, conformity, ESG criteria, water sourcing and production impacts, reinforcing the role of testing and assurance in international hydrogen trade.

White Space Opportunities

Green Hydrogen Testing Market White Spaces include more than just conventional lab tests and provide ample opportunities for DataM to leverage the market towards ensuring projects’ readiness for certification and end-to-end value chain risk mitigation. While majority of hydrogen test providers offer standard hydrogen purity and safety test, there is a high growth potential in the areas of electrolyzer benchmarking, renewable hydrogen certification, carbon intensity verification, hydrogen storage testing, refueling stations testing, hydrogen blending test, and export-ready hydrogen quality.

The first white space would be the demand for a partner that would help in validating designs, commissioning, certifying and monitoring projects related to electrolyzers for developers, original equipment manufacturer (OEM), utility companies and industries. Test providers who also have capabilities for laboratory testing, field inspection, metering validation, digital monitoring, material compatibility test, and regulations advisory services will find this segment very attractive. The key here would be positioning the services as enablers for green hydrogen banking and commercialization.

DMI Opinion

According to the analysis by DataM, not only the growth in green hydrogen production capacity will drive the Green Hydrogen Testing Market, but also the capability of testing suppliers to assess the quality, safety, performance, and compliance of hydrogen along the value chain. This is because as more projects move from the pilot stage to commercial operation, all stakeholders involved, whether developers, OEMs, utilities, or industries, would demand validated data related to hydrogen purity, electrolyzer efficiency, leakage, pressure, compatibility, metering, and compliance with carbon-intensity targets.

Based on the findings of DataM, hydrogen purity testing, electrolyzer performance testing, hydrogen safety and leak testing, hydrogen storage and pressure system testing, hydrogen refueling infrastructure testing, and renewable hydrogen certification are expected to have the greatest commercial prospects. Firms capable of offering hydrogen-related services such as laboratory testing, field testing, certification, digital solutions, and compliance advice within an integrated solution will gain significant ground. This implies that the appropriate strategy for the market should look at green hydrogen testing as a bankable service.

Why Choose DataM?

- Green Hydrogen Testing and Certification Intelligence: Encompasses green hydrogen purity testing, electrolyzers performance validation, leak detection testing, pressure integrity tests, material compatibility testing, metering validation tests, safety inspection and certification and regulation testing for green hydrogen.

- Positioning of Testing and Certification Companies: Identifies large TIC players in terms of hydrogen testing capability, laboratories capability, field inspections, certification capability, geographical reach, hydrogen standards coverage and ability to offer testing services for commercial projects.

- Market Dynamics and Trends: Considers increased demand for renewable hydrogen certification, project finance, export grade hydrogen certification, electrolyzer testing, safety assurance, hydrogen refueling stations testing, decarbonization through industrial hydrogen and stricter carbon intensity validation.

- Strategies of the Competitors: Considers strategies of the major competitors including services expansion, investment in hydrogen labs, partnerships with electrolyzer manufacturers, certification program development, development of new testing platform, geographical expansion and advisory-based business model.

- Cost of Hydrogen Testing Services and Benchmarking: Considers testing service costs, certification costs, inspection fees, validation costs at laboratories, certification compliance documentation and adoption challenges at project developers, OEMs, utilities and industrial end-users.

Target Audience 2026

- Green Hydrogen Project Developers

- Electrolyzer Manufacturers

- Industrial Gas Companies

- Energy Utilities

- Hydrogen Infrastructure Operators

- Refining and Chemical Companies

- Green Steel and Metals Producers

- Testing Inspection and Certification Companies