Green Ammonia Market Overview

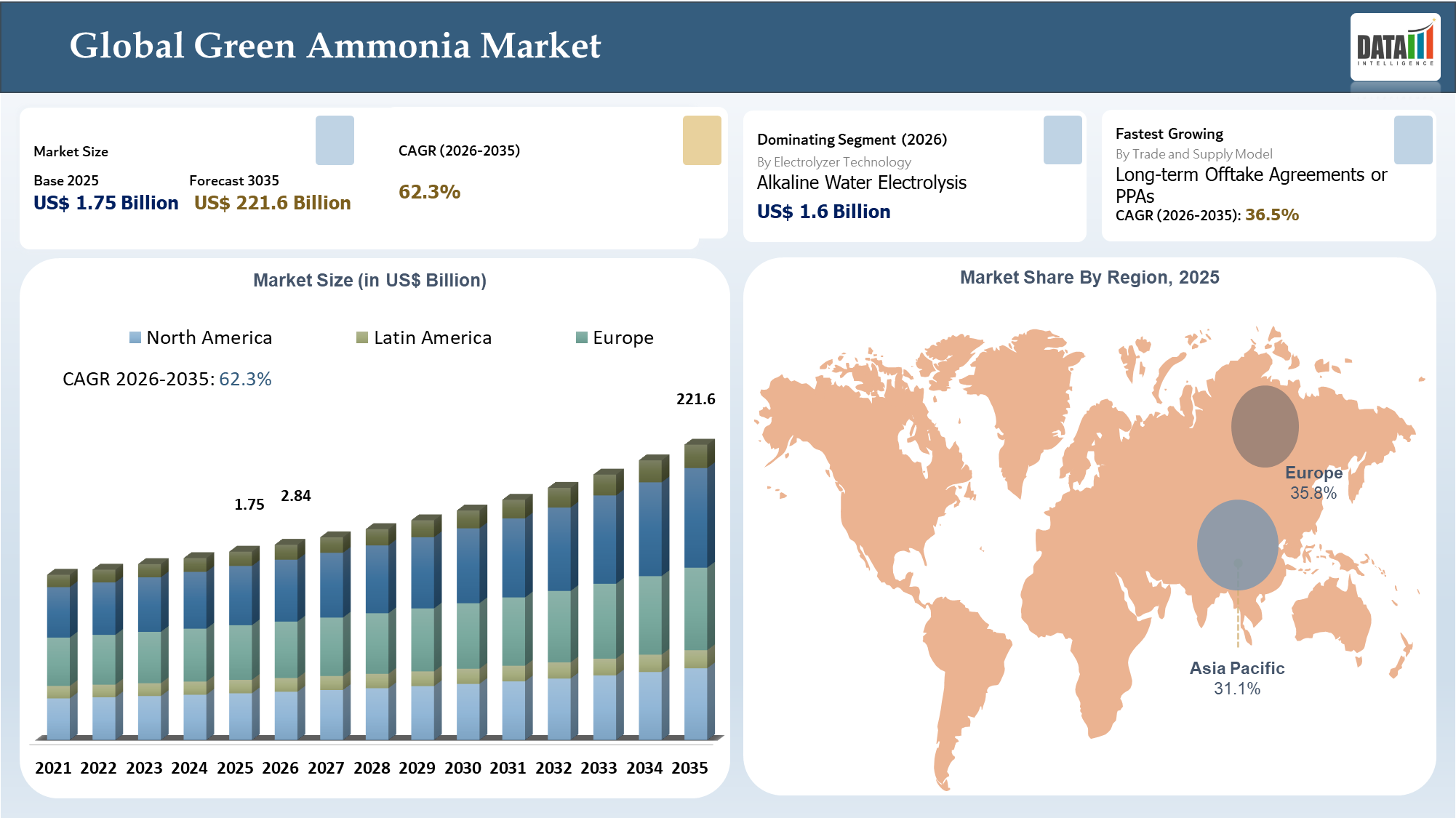

The global green ammonia market reached US$ 1.75 billion in 2025 and is expected to reach US$ 221.6 billion by 2035, growing with a CAGR of 62.3% during the forecast period 2026-2035. There have been many changes occurring in the market because companies have been changing their operations from fossil-based ammonia towards low-carbon ammonia based on the use of clean energy and green hydrogen. Green Ammonia Market Growth has been propelled by the increase in demand for sustainable fertilizers, ammonia as a hydrogen carrier, as well as a marine fuel. It has also been influenced by the investments that firms have been making in export-oriented energy. Green Ammonia Market Analysis shows that this industry is still very ecosystem-centric in nature since the generation of value has been taking place through renewables, electrolyzers, ammonia, and process technology for Haber Bosch. These three together have provided for the decarbonization pathways of various applications such as fertilizers, shipping, and industrial feedstock. Some of the value centers within this sector have included the electrolyzer, integration of ammonia synthesis, storage, transport, and infrastructure developments. Adjacent technology innovations, especially involving fuel cells, have been playing an important role in influencing Green Ammonia Market Trends.

Green Ammonia Industry Trends and Strategic Insight

- Increasingly, Export-Led Project Development: Projects that focus on producing green ammonia in low-cost renewable regions for export along established corridors to Europe and Asia have become more common.

- First Commercial Application in Fertilizer Decarbonization: The quickest path to commercialization will be the replacement of regular ammonia in fertilizers followed by its utilization in transportation and power generation.

- Long-Term Offtake Agreements Have Become Vital: Having long-term sales agreements in place has become essential in securing financing due to any additional cost incurred from green ammonia production.

- Power-to-Ammonia Approach Preferred: Combining renewable power production, electrochemical conversion, energy storage, and ammonia synthesis process are preferred due to better cost management.

- Technological Partnerships Key to Competitive Advantages: Companies specializing in providing electrolyzers, engineering and procurement contractors, and ammonia processes are key partners in energy projects.

- Asia and Middle East Will Lead in Green Ammonia Production: Countries in these regions will see lower costs from renewable energy leading to future market growth in green ammonia.

- Applications in Shipping and Hydrogen Carriers Will Fuel Growth: Although fertilizers remain the largest segment, transportation fuels and hydrogen carriers are the major long-term market drivers..

Green Ammonia Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 1.75 Billion | |

| 2035 Projected Market Size | US$ 221.6 Billion | |

| CAGR (2026-2035) | 62.3% | |

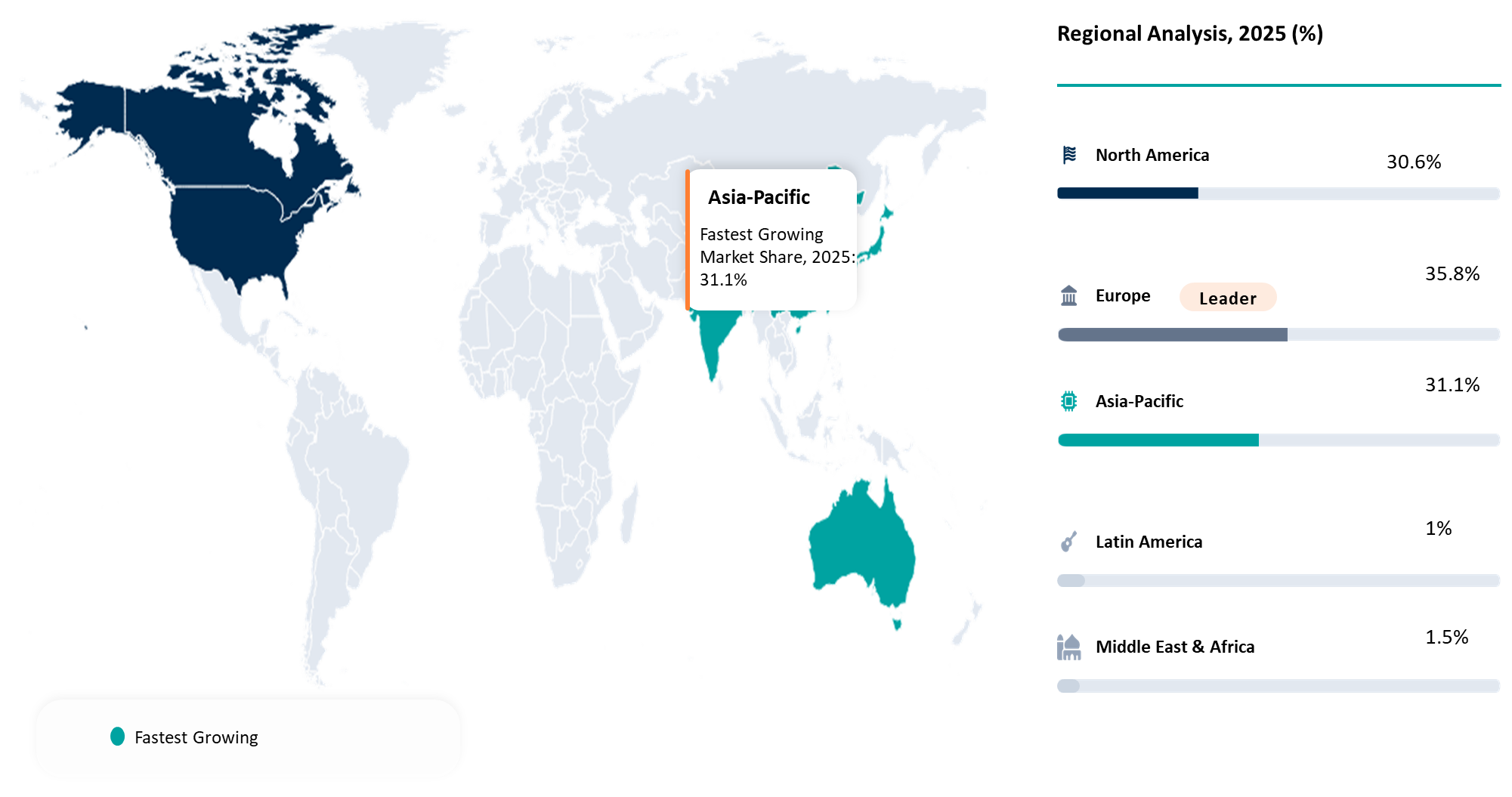

| Largest Market | Europe | |

| Fastest Growing Market | Asia-Pacific | |

| By Electrolyzer Technology | Alkaline Water Electrolysis, Proton Exchange Membrane, Solid Oxide Electrolysis, Anion Exchange Membrane, Others | |

| By Energy Source | Solar Energy, Wind Energy (Onshore, Offshore), Hydropower, Hybrid, Others | |

| By Production Scale | Pilot Scale, Small Scale, Commercial Scale, Large Scale | |

| By Trade and Supply Model | Domestic Production and Consumption, Import-Based Supply, Long-Term Offtake Agreements or PPAs | |

| By Usage | Captive, Merchant | |

| By Purity Grade | 99% to 99.5%, More than 99.5% | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

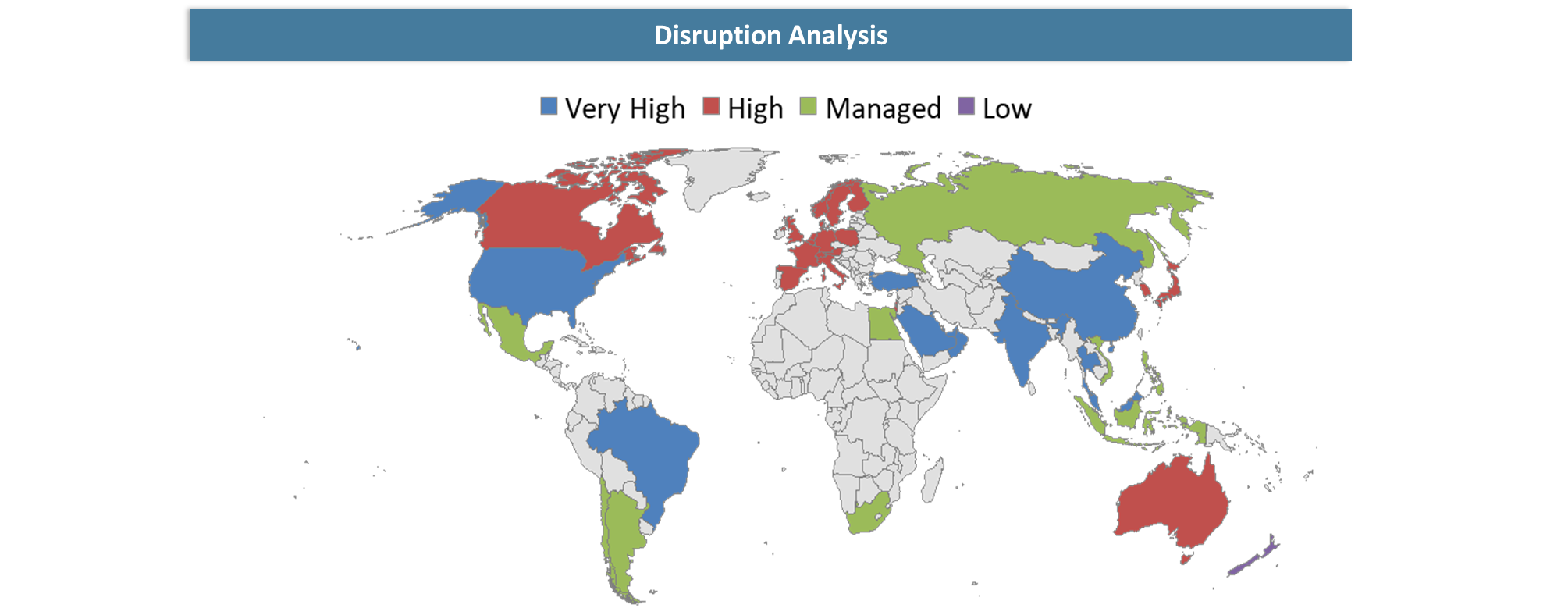

Green Ammonia Market Disruption Analysis

Shift from Conventional Fossil-Based Ammonia to Renewable Hydrogen-Based Production Reshaping Industry Economics

The disruptive forces driving changes in the Green Ammonia Market include the switch from traditional ammonia production methods to renewable hydrogen with the Haber Bosch method. These changes are affecting the business models of organizations engaged in ammonia production because they are facing competition from energy solutions associated with clean power generation, export-oriented business operations, and low carbon footprint purchases. With the growth of the Green Ammonia Market, those firms capable of integrating their processes with renewable energy sources, owning electrolyzers, and being able to utilize the available infrastructure are expected to take an increasingly larger Green Ammonia Market Share. Such trends have become one of the most important aspects of Green Ammonia Market Analysis and the future developments of Green Ammonia Market Trends.

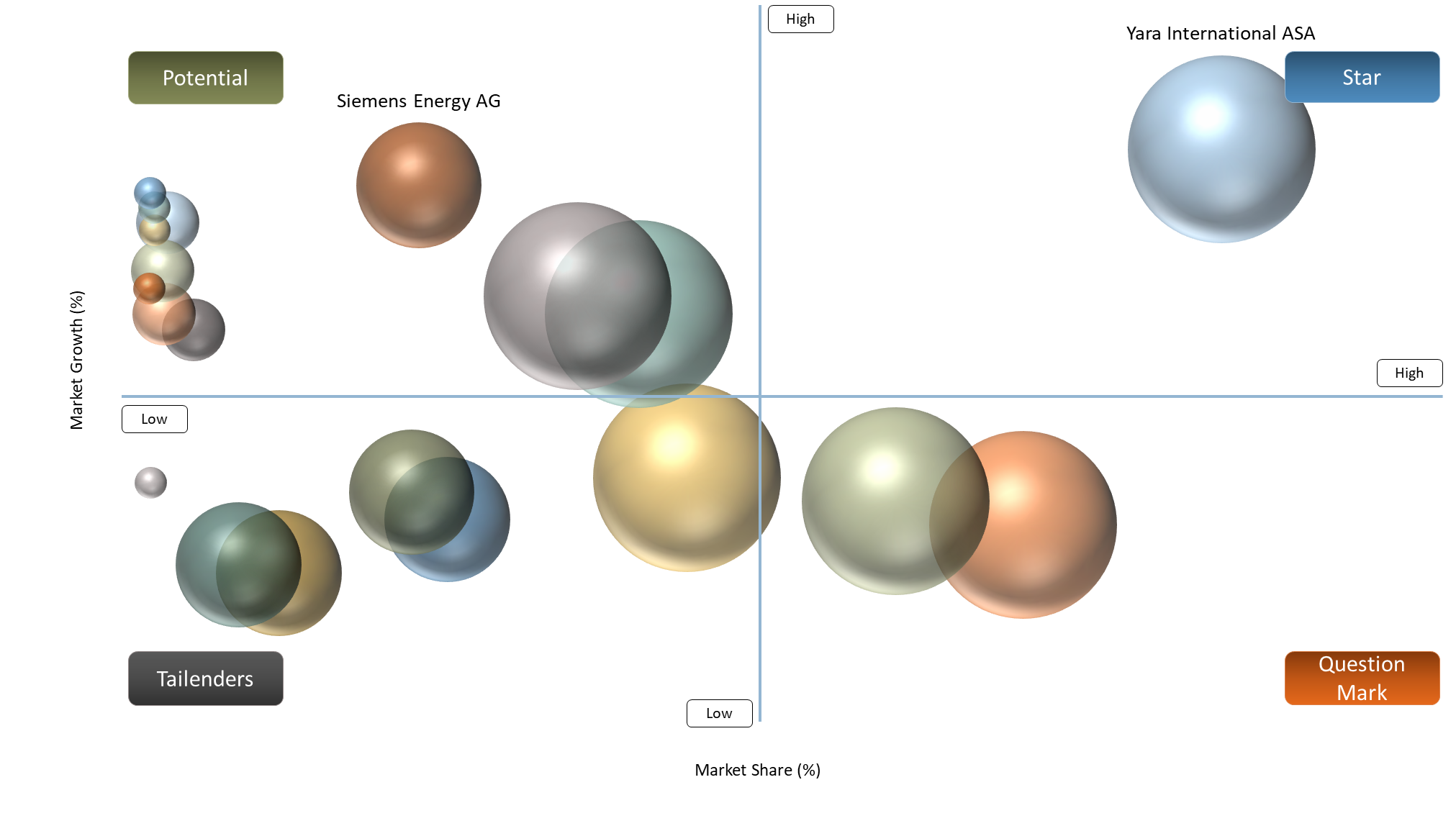

Green Ammonia Market BCG Matrix: Company Evaluation

Green Ammonia Market involves players like ammonia manufacturers, renewable energy project developers, electrolyzer manufacturers, and providers of Haber Bosch technologies. The dominant companies in Green Ammonia Market include Yara International ASA, CF Industries Holdings Inc., Air Products and Chemicals Inc., Fertiglobe plc, and OCI Global owing to their established ammonia manufacturing capacity and higher Green Ammonia Market share. On the other hand, firms such as ENGIE SA, Masdar, ACME Cleantech Solutions Pvt Ltd, AM Green BV, and NTPC Limited are contributing through clean energy and energy solution projects.

In a BCG-style Green Ammonia Market Analysis, Yara International ASA, CF Industries Holdings Inc., Air Products and Chemicals Inc., Fertiglobe plc, and OCI Global can be treated as Stars due to stronger scale and commercial presence. ENGIE SA, Masdar, ACME Cleantech Solutions Pvt Ltd, AM Green BV, and NTPC Limited fit Question Mark due to high growth potential but lower realized share. thyssenkrupp nucera, Haldor Topsoe A/S, Nel ASA, and Siemens Energy AG fit Potential, as they influence Green Ammonia Market Trends through electrolyzers, hydrogen systems, and broader industrial platforms, including company profile Siemens Energy and related fuel cells capabilities.

Green Ammonia Market Dynamics

Fertilizer producers are under pressure to decarbonize embedded ammonia emissions

There is increasing pressure on fertilizer manufacturers to decrease the carbon intensity of ammonia, the main ingredient of nitrogen-based fertilizers that is responsible for most of the carbon emissions because it uses hydrogen derived from natural gas. The pressure for agricultural value chains to become more sustainable is becoming stricter as there are stricter regulations set by government bodies and food corporations. Fertilizer manufacturers must make sure their products are environmentally friendly and even have certifications in green ammonia to comply with the standards set by agribusiness firms and food retailers. As large-scale agribusiness firms and food retailers start focusing more on reducing their carbon emissions, they will need to use more environmentally friendly fertilizers.

The green ammonia price premium remains too high for unsubsidized demand

Green ammonia market still faces an important challenge when it comes to commercialization, as its production costs tend to be higher compared to those of regular ammonia produced using fossil fuel-derived hydrogen. This is primarily due to the high cost of renewable energy sources, higher cost of installation for electrolysers, underutilization, and additional costs related to storage and transportation facilities. In markets that are sensitive towards price changes such as the fertilizer, power, and maritime industry, consumers are less likely to pay extra without any form of subsidy, carbon price adjustment, tax breaks, or a green procurement policy.

Green Ammonia Market Segmentation Analysis

The global Green Ammonia Market is segmented based on the electrolyzer technology, energy source, production scale, application, trade and supply model, usage, purity grade and region/countries.

Alkaline Water Electrolysis Driving Scalable Hydrogen Supply for Green Ammonia Production

Alkaline Water Electrolysis is likely to be dominant in the Green Ammonia Market Size and Green Ammonia Market Share, as it represents the best-proven technology path for large-scale hydrogen production required for the manufacture of ammonia. According to IEA, world electrolyzer capacity from water electrolysis grew up to 2 GW by 2024, and over 1 GW was brought online by July 2025; this demonstrates rapid growth in the number of scalable electrolyzers used to generate clean energy. As far as the Green Ammonia Market Analysis is concerned, AEL is recommended for projects related to bulk volumes due to the fact that green ammonia is produced via renewable hydrogen in conjunction with the conventional Haber-Bosch cycle. As stated by Siemens Energy, typical capacities at an ammonia plant range from 500 to 1,500 metric tons per day, and replacing 200 MTPD with green hydrogen would require at least 150-200 MW of renewable energy sources and a corresponding electrolyzer capacity. Hence, there are good prospects for Green Ammonia Market Growth based on AEL technology. In turn, Green Ammonia Market Trends encompass not only integration into industrial decarbonization platforms and hydrogen systems but also adjacent technologies such as fuel cells.

Green Ammonia Market Geographical Penetration

Asia-Pacific Leading Green Ammonia Scale-Up Through Renewable Resource Advantage and Export-Oriented Hydrogen Strategies

In comparison with other regions, Asia-Pacific is considered to be the region showing the highest level of aggressiveness in Green Ammonia Market Growth due to its rich renewable energy resources, government support in hydrogen missions, and increased demand for energy solutions. The countries like Australia, India, Japan, and South Korea are implementing various green ammonia programs with the focus not only on domestic consumption but also on exporting energy solutions. Although the region has already proved its presence in conventional ammonia and fertilizers, it tends to implement renewable hydrogen in the Haber Bosch process for producing low carbon ammonia.

One of the strengths of Asia-Pacific in Green Ammonia Market Analysis is a systemic approach towards developing all processes from renewable power production to electrolysis, ammonia synthesis, and infrastructure for exports. It allows the governments of Asia-Pacific to invest actively into their hydrogen missions, green fuels, and industrial decarbonization processes in order to increase the deployment of their fertilizers, shipping sector, and power solutions. In addition, the region enjoys some competitive costs in solar/wind power.

Also, the Asia Pacific region is emerging as a key player in hydrogen and ammonia technology due to its favorable industrial ecosystems and involvement of international and regional companies. Synergies with neighboring technologies, including fuel cell technology, hydrogen storage, and energy technology (mentioned under the profile of a company like Siemens Energy), make it even more promising. With growing pipeline projects, export deals, and infrastructure expansion, Asia Pacific is set to play an influential role in shaping the future Green Ammonia Market Share and Green Ammonia Market Trends.

China Green Ammonia Market Trends

China appears to be one of the most crucial nations in the narrative around Green Ammonia Market Growth. This comes from China’s ability to develop large amounts of renewable energy, manufacture advanced electrolyzers, and develop policies that support the decarbonization of its industries with hydrogen technologies. In turn, such efforts help enhance future Green Ammonia Market Size by cutting down equipment costs and promoting rapid scaling of projects. Indeed, according to the IEA, an ambitious 500 MW electrolyser project had been commissioned in China in 2025.

One of the most significant strengths of China in terms of Green Ammonia Market Analysis is the systems-level development. Specifically, in the development of hydrogen technology in Jilin Province, official project documents have disclosed plans for integrated green hydrogen, methanol, and ammonia projects, including a project with an 800 MW wind farm, 200 MWp solar capacity, 150 MW/300 MWh energy storage capacity, and 600,000 tons of green ammonia per year.

In addition to this, there is the presence of a robust clean energy, energy solutions, and hydrogen equipment industrial base in China, which makes it advantageous in terms of long-term Green Ammonia Market Trends in the context of renewable hydrogen paired with Haber Bosch processes.

India Green Ammonia Market Outlook

One of the key markets becoming aggressive in the Green Ammonia Market Growth narrative is India. The Indian government's support for policies, low-cost renewable energy, and efforts to make India the center for green hydrogen and derivatives have played an instrumental role behind this trend. As part of its National Green Hydrogen Mission, the Indian government has targeted the production of 5 million metric tons of green hydrogen per year by 2030 through the development of approximately 125 gigawatts of new renewable energy capacity, laying the foundation for future Green Ammonia Market Size growth.

An important advantage in the analysis of the Green Ammonia market in India lies in the fact that green ammonia is not considered as an independent item but a complete chain of the production of energy, including electrolysis, storage, ports, and demand from industries is being created at one go. There are a number of projects related to ammonia present in the database maintained by the Government, which include companies like ACME and Adani, and projects being developed in various stages in states like Odisha, Karnataka, Tamil Nadu, and Gujarat.

India also reaps the advantages of declining prices in renewable energy and increasing institutional backing for the use of hydrogen in manufacturing. By 2025, the total solar capacity in India had grown to 132.85 GW and wind power to 53.99 GW, making renewable hydrogen cost-effective for ammonia synthesis. The above developments have implications for Green Ammonia Market Trends, particularly those related to exports, industrial de-carbonization, and synergy with other technologies such as hydrogen mobility and fuel cells.

Green Ammonia Market Competitive Landscape

- The market consists of four inter-related group of participants that include ammonia producers, renewable energy & projects developers, electrolyzer and hydrogen technology providers, and ammonia synthesis and process technology companies. Some of the main players in Green Ammonia Market include Yara International ASA, CF Industries Holdings Inc., Air Products and Chemicals Inc., Fertiglobe plc, OCI Global, ACME Cleantech Solutions Pvt Ltd, AM Green BV, ENGIE SA, NTPC Limited, and Masdar. Simultaneously, thyssenkrupp nucera, Haldor Topsoe A/S, Nel ASA, and Siemens Energy AG occupy important positions in this market by means of providing electrolyzers systems, hydrogen technologies, process engineering, and Haber Bosch for green ammonia production. Therefore, according to the Green Ammonia Market Analysis, competitiveness of the market is strongly ecosystem-oriented and is not determined by a winner-takes-all principle. Competitiveness of market participants will gradually be defined by their access to inexpensive renewable energy, secure offtake, infrastructural opportunities, proven technologies, and clean energy integration with ammonia production and global supply chains. In general, it should significantly affect Green Ammonia Market Size, Green Ammonia Market Share, Green Ammonia Market Growth, and further Green Ammonia Market Trends.

- Some of the key market participants within the Green Ammonia Market are Yara International ASA, CF Industries Holdings Inc., Air Products and Chemicals Inc., Fertiglobe plc, ACME Cleantech Solutions Pvt Ltd, AM Green BV, ENGIE SA, NTPC Limited, Masdar, thyssenkrupp nucera, OCI Global, Haldor Topsoe A/S, Nel ASA, and Siemens Energy AG. These firms are currently active within the realms of renewable hydrogen production, ammonia production, implementation of projects, construction of export facilities, industrial de-carbonation, and applications of low emission fertilizers. Their business strategies revolve around the scaling of renewable ammonia production, electrolysis system optimization, improvement of the Haber Bosch process for renewable feedstock, and development of comprehensive energy systems for fertilizer production, marine fuel, hydrogen transportation, and other power-related purposes. In this respect, players with a diverse portfolio of technologies, ammonia logistics, and company profiles such as Siemens Energy, hydrogen systems, and even fuel cell systems can become key Green Ammonia Market Share holders..

Key Developments in Green Ammonia Market

- July 2026: Yara International ASA advanced its global green ammonia strategy by expanding renewable ammonia production initiatives to support low-carbon fertilizer production and clean energy applications.

- July 2026: CF Industries Holdings, Inc. continued developing large-scale low-carbon ammonia projects through investments in clean hydrogen and carbon reduction technologies across its production facilities.

- June 2026: Air Products and Chemicals, Inc. strengthened its clean hydrogen and green ammonia portfolio by advancing integrated renewable hydrogen projects for global export and industrial decarbonization.

- June 2026: Fertiglobe plc expanded its green ammonia production capabilities through strategic renewable energy projects targeting international shipping and fertilizer markets.

- May 2026: AM Green B.V. accelerated the development of large-scale green ammonia production facilities in India to support global demand for sustainable fuels and hydrogen derivatives.

- May 2026: thyssenkrupp nucera AG advanced its large-scale water electrolysis technologies by securing new projects that support green hydrogen production for ammonia manufacturing.

- April 2026: ENGIE SA continued expanding renewable hydrogen and green ammonia projects through partnerships focused on industrial decarbonization and clean energy exports.

- April 2026: NTPC Limited strengthened its green hydrogen and green ammonia initiatives by progressing renewable energy-based production projects to support India's clean energy transition.

- March 2026: Masdar expanded its global clean energy portfolio by advancing green hydrogen and ammonia projects in collaboration with international partners to accelerate low-carbon fuel production.

Why Choose DataM?

- Technological Developments: Discusses recent developments within the Green Ammonia Market, such as increases in electrolyzer efficiency, the incorporation of renewable energy sources, the optimization of ammonia synthesis using the Haber Bosch process, hydrogen storage technologies, and export capabilities that allow for the efficient production of clean energy.

- Performance and Market Position: Analyzes the positioning of various players involved in the development of green ammonia, technology vendors, and ammonia suppliers. It takes into account project scale, integration of renewable energy sources, type of electrolyzer, purity of ammonia, ability to export, and cost-competitiveness as distinguishing factors within the Green Ammonia Market Analysis.

- Applications of Green Ammonia: Illustrates how green ammonia can be applied in real-world scenarios for fertilizer production with low carbon footprint, power generation, hydrogen transportation, and marine fuel usage. Examples include reduced emissions, increased energy security, renewable energy storage, and reduced reliance on ammonia from fossil fuels.

- Market Trends and Changes in the Industry: Provides information on important trends in the form of new project launches, final investments, export contracts, off-take agreements, hydrogen policies, and renewable energy growth in important regions like Europe, Asia Pacific, China, India, and Middle East.

- Competitive Strategies: Discusses strategies used by prominent players to gain market share through renewable to ammonia projects, strategic collaborations, export facilities at ports, increased electrolyser capacity, and technological innovations in energy solutions and hydrogen systems.

- Pricing & Access to the Market: Describes the pricing mechanisms of the Green Ammonia Market in terms of green electricity price, electrolyzer CAPEX, scale of production, storage, and logistics. The document also highlights regional market access, development of export corridors, policies & subsidies, and contracts that enhance Green Ammonia Market share.

- Market Entry & Expansion: Outlines areas where expansion can take place including export-friendly regions, centers for industrial decarbonization, and countries with low costs of solar and wind energy. The document also highlights strategies that enable companies to expand their global footprint to achieve Green Ammonia Market Growth & Green Ammonia Market Trends.

Target Audience 2026

- Producers of Ammonia and Fertilizers: Manufacturers looking to adopt carbon-free feedstock approaches, ammonia decarbonization methods, and sustainable competitiveness in their fertilizer value chains.

- Renewable Energy Developers and Producers of Hydrogen: Companies engaged in development projects related to integrated clean energy and energy solution concepts such as electrolysis and renewable power-based green ammonia production.

- Shipowners, Shipping Firms and Bunker Operators: Shipowners and bunker providers considering using green ammonia as a fuel for their ships in the coming years.

- End-users Industries: Power producers, chemical companies, oil refineries, and industries that evaluate the prospects of using green ammonia as a fuel source and transportation of hydrogen and other applications.

- Government Bodies and Authorities: Energy ministries, hydrogen missions, trade organizations, and infrastructure authorities that support policy initiatives, green ammonia export centers, and energy transition schemes.

- Technology Providers and EPCs: Electrolyzer providers, process technology licensing bodies, EPC contractors, and companies interested in Haber-Bosch process integration, storage, transportation, and more.

- Institutional Investors and Financing Organizations: Private equity investors, project financiers, and financial institutions tracking the growth of the Green Ammonia Market and project viability.