Green Hydrogen Market Growth

Capital is moving into hydrogen not as a speculative climate bet, but as a structured infrastructure play tied to industrial decarbonization, energy security, and long-term fuel substitution. As large-scale projects transition from feasibility to execution, the Green Hydrogen market size 2026 and beyond reflects a shift from pilot deployments to bankable assets with defined offtake.

Historic years considered are 2023 and 2024, with 2025 as the base year and projections running through 2035. As policy incentives, project financing models, and industrial demand converge, this market is becoming central to long-term energy transition strategies across regions.

Market Scope

| Metric | Details |

| Market Size (2025) | US$ 11.05 Billion |

| Market Size (2035) | US$ 168.37 Billion |

| CAGR (2026–2035) | 6.80% |

| Historic Years | 2023–2024 |

| Base Year | 2025 |

| Forecast Period | 2026–2035 |

| Segments Covered | Technology, Renewable Source, Production Capacity, Delivery Mode, Storage & Conditioning, Ownership, Application, End-User, Region |

| Leading Region | Europe |

| Fastest Growing Region | Asia-Pacific |

For More Detailed information Request for Sample

Key Takeaways

- Europe accounted for 43.28% of global revenue in 2025, supported by strong hydrogen policy incentives and carbon pricing frameworks.

- Alkaline electrolyzers held 62.87% share, reflecting cost advantage and deployment readiness for large-scale projects.

- Green Hydrogen market forecast 2035 indicates over 15x growth from 2025 levels, signaling long-term infrastructure opportunity.

- Project pipeline expansion is accelerating, with multi-billion-dollar developments in Africa and Europe gaining institutional funding.

- Asia-Pacific is the fastest-growing region, driven by national missions in India, China, Japan, and South Korea.

- Pricing and adoption trends remain tied to renewable electricity costs, making location strategy critical for ROI.

- Industrial demand from steel, chemicals, and mobility sectors is shaping early offtake agreements, reducing project risk.

Demand Signals and Growth Drivers

Policy Incentives and Net-Zero Commitments

The strongest growth driver for green hydrogen remains policy-backed decarbonization mandates. National hydrogen roadmaps across Europe, Asia-Pacific, and the Middle East are translating climate commitments into tangible procurement and infrastructure investments.

Carbon pricing systems and production incentives are improving the green hydrogen levelized cost outlook, narrowing the gap with grey hydrogen and making projects financially viable.

India’s target of 5 MMT annual production by 2030 and large-scale renewable deployment exemplify how policy is directly shaping demand visibility.

Industrial Decarbonization Demand

Heavy industries are emerging as anchor customers. Steel manufacturing, ammonia production, refining, and chemicals are actively integrating hydrogen into their energy mix.

Hydrogen’s high energy density and zero-emission profile make it particularly suitable for:

- Long-haul transport

- Industrial heat applications

- Grid balancing and energy storage

These sectors are entering long-term supply agreements, which are critical for project bankability.

Pricing, Cost Structure and Adoption Trends

Capex and Opex Dynamics

Green hydrogen economics are driven by two primary variables:

- Capex Drivers

- Electrolyzer cost and efficiency

- Renewable energy infrastructure

- Storage and transport systems

- Opex Drivers

- Electricity cost, often 60–70% of total production cost

- Maintenance of electrolyzer systems

- Water sourcing and processing

Declining renewable energy prices and electrolyzer innovation are gradually improving cost competitiveness. However, pricing and adoption trends remain highly region-specific, depending on access to low-cost solar and wind resources.

Technology Comparison and Deployment Strategy

Electrolyzer Landscape

- Alkaline Electrolyzers (AEL)

Dominant with 62.87% share due to low cost and proven reliability. Best suited for large-scale, steady-state production. - Proton Exchange Membrane (PEM)

Offers flexibility and faster response times, making it suitable for variable renewable integration. - Solid Oxide Electrolyzers (SOEC)

High efficiency potential, particularly in industrial waste heat environments, though still in early commercialization. - Emerging Technologies (AEM, Biomass Pyrolysis)

Target cost reduction and alternative feedstock utilization.

From a procurement standpoint, AEL dominates current project pipelines, while PEM and SOEC are gaining traction in advanced deployments.

Green Hydrogen Project Pipeline Snapshot

| Region | Project Type | Investment Signal | Strategic Objective |

| Europe | Industrial hydrogen platforms | €30 million+ investments | Cement and heavy industry decarbonization |

| Africa | Hydrogen + Ammonia mega projects | US$10+ billion pipeline | Export-oriented hydrogen economy |

| North America | Power plant integration | Utility-scale deployments | Grid reliability and storage |

| Asia-Pacific | National hydrogen missions | Multi-billion public funding | Energy security and industrial growth |

The green hydrogen project pipeline is expanding rapidly, with increasing participation from development banks, private equity, and sovereign funds.

Segmentation Insights

Segmented by technology (Alkaline Electrolyzer, PEM, SOEC, AEM, Biomass Pyrolysis), by renewable source (solar, wind, hydropower, biomass, hybrid, nuclear-powered electrolysis), by production capacity, delivery mode, storage & conditioning, ownership, application, end-user, and by region - share, trends, and forecast to 2035.

Technology Leadership

Alkaline systems dominate due to cost efficiency and scalability, particularly for projects exceeding 100 MW capacity. Their established supply chain reduces procurement risk for large developers.

End-Use Expansion

Key end-users include:

- Industrial manufacturing and chemicals

- Oil and gas refining

- Power and utilities

- Mobility OEMs and fuel cell integrators

Industrial feedstock remains the largest revenue contributor, but mobility and grid applications are emerging as high-growth segments.

Regional Analysis and Strategic Positioning

Europe: Policy-Driven Market Leadership

Europe leads with 43.28% market share, supported by:

- Strong regulatory frameworks such as EU Hydrogen Strategy

- Carbon pricing under EU ETS

- Established industrial demand

Germany, Spain, and the Netherlands are investing heavily in electrolyzer capacity and hydrogen infrastructure, positioning the region as both a producer and exporter.

Asia-Pacific: Scale and Speed Advantage

Asia-Pacific is the fastest-growing region, driven by:

- India’s National Green Hydrogen Mission

- China’s 2021–2035 hydrogen development strategy

- Japan and South Korea’s large-scale demonstration projects

The region benefits from low-cost renewable resources and strong industrial demand, enabling competitive production economics.

North America: Incentive-Led Expansion

The U.S. market is shaped by:

- Production tax credits under federal policy

- Utility-led hydrogen integration projects

- Growing interest in hydrogen for grid reliability

North America’s strength lies in innovation and infrastructure integration, particularly in power generation and mobility.

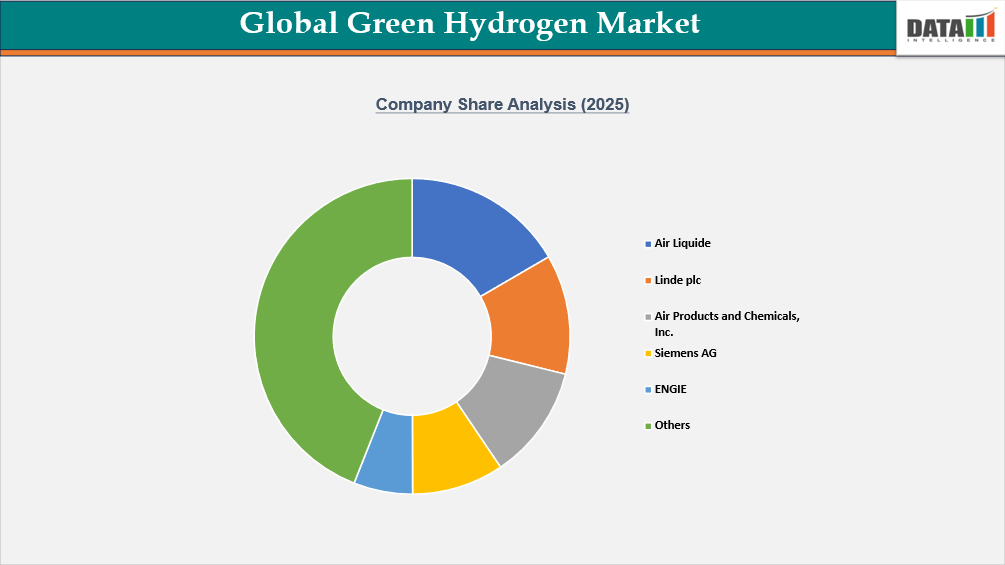

Competitive Landscape and Company Strategy

The Green Hydrogen top companies are competing across the entire value chain, from production to distribution.

Key players include:

- Siemens AG

- Linde PLC

- Air Liquide Engineering & Construction

- Nel ASA

- Cummins Inc

- Air Products and Chemicals, Inc.

- ENGIE

- Uniper SE

- AMEA Power

Strategic Focus Areas

- Vertical integration across renewable power, hydrogen production, and distribution

- Electrolyzer efficiency improvements to reduce cost per kg

- Partnerships with industrial buyers to secure long-term offtake agreements

- Infrastructure expansion including storage and transport solutions

For example, Siemens Energy is positioning itself as a full-stack provider, offering production, storage, and utilization technologies, enabling end-to-end hydrogen ecosystems.

Investment Opportunities Across the Value Chain

For Investors and Infrastructure Funds

The current phase offers entry into:

- Large-scale production assets

- Export-oriented hydrogen hubs

- Integrated renewable-hydrogen projects

For Industrial Buyers

Early adoption enables:

- Long-term cost stability

- Carbon compliance

- Competitive positioning in low-carbon markets

For Technology Providers

Opportunities lie in:

- Electrolyzer innovation

- Storage and transport solutions

- Digital optimization of hydrogen systems

Recent Developments

In May 2026, Air Liquide expanded its green hydrogen projects with large-scale electrolyzer deployments across Europe. The initiative focuses on decarbonizing industrial processes. This supports energy transition goals.

In April 2026, Siemens Energy introduced advanced electrolyzer technologies with improved efficiency and scalability. The development enhances hydrogen production capacity. This benefits renewable energy integration.

In March 2026, Nel ASA strengthened its hydrogen solutions with high-capacity electrolyzer systems for industrial applications. The innovation focuses on cost reduction and performance. This supports large-scale adoption.

Report Benefits

This report supports:

- Manufacturers in identifying cost-efficient production technologies

- Investors in evaluating project pipeline viability and ROI

- Suppliers in aligning with high-growth regions and segments

- Strategy teams in understanding policy incentives and market timing

- Procurement leaders in securing long-term hydrogen supply contracts

What Choose DataM?

- Latest Data & Forecasts – Comprehensive, up-to-date insights and projections through 2033. Coverage includes global value by technology, renewable source, production capacity, delivery mode, storage & conditioning, ownership, application, end-user. Scenario forecasts with region-level splits (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) and sensitivity to factors such as regulatory reclassification and raw-material costs.

- Regulatory Intelligence – Actionable analysis of regulatory frameworks that materially affect Green Hydrogen commercialization, revenue by country, allowable label claims, permitted doses, import/export controls and advertising restrictions.

- Competitive Benchmarking – Standardized profiling and benchmarking of leading pharma and nutraceutical players, contract manufacturers and e-commerce specialists active in the market.

- Geographic & Emerging Market Coverage – Region-by-region market sizing, growth drivers, reimbursement dynamics, cultural/consumer behavior and market access considerations. Focus on high-growth or regulatory-uncertain markets.

- Actionable Strategies – Identify opportunities for launching innovative products, while leveraging strategic partnerships and supply chain integration for maximum ROI.

- Pricing & Cost Analysis – In-depth assessment of price trends, raw material costs and sustainability-driven cost efficiencies across regional markets.

- Expert Analysis – Insights from industry experts such as product specialists, regulatory affairs professionals and key manufacturing companies.

Target Audience

- Energy & Industrial Enterprises: Large industrial players in steel, chemicals, refining, power generation and heavy manufacturing seeking to decarbonize operations through green hydrogen adoption.

- Government, Regulatory & Policy Bodies: National governments, energy ministries, environmental regulators and hydrogen authorities responsible for net-zero targets, subsidies, safety standards and hydrogen infrastructure policies.

- Technology & Innovation Leaders: Electrolyzer manufacturers, renewable energy developers, engineering firms, R&D teams and hydrogen technology innovators advancing production efficiency and cost reduction.

- Investors: Venture capital firms, private equity groups, infrastructure funds, sovereign wealth funds and green finance institutions investing in hydrogen projects and clean energy transitions.

- Consulting & Advisory Firms: Energy consultants, sustainability advisors, engineering consultants and strategy firms supporting hydrogen feasibility studies, project development and regulatory compliance.

- Hydrogen Producers & Supply Chain Players: Renewable power generators, electrolyzer suppliers, EPC contractors, storage providers, transportation companies and hydrogen distribution service providers.

- Energy Buyers & Decision Makers: CIOs, CTOs, sustainability heads, energy managers and procurement leaders evaluating long-term hydrogen offtake agreements and clean fuel alternatives.

- Academic & Research Institutions: Universities, national laboratories and research organizations conducting advanced research in electrolysis, storage technologies, fuel cells and hydrogen applications.