Enterprise Cloud Security Market Overview

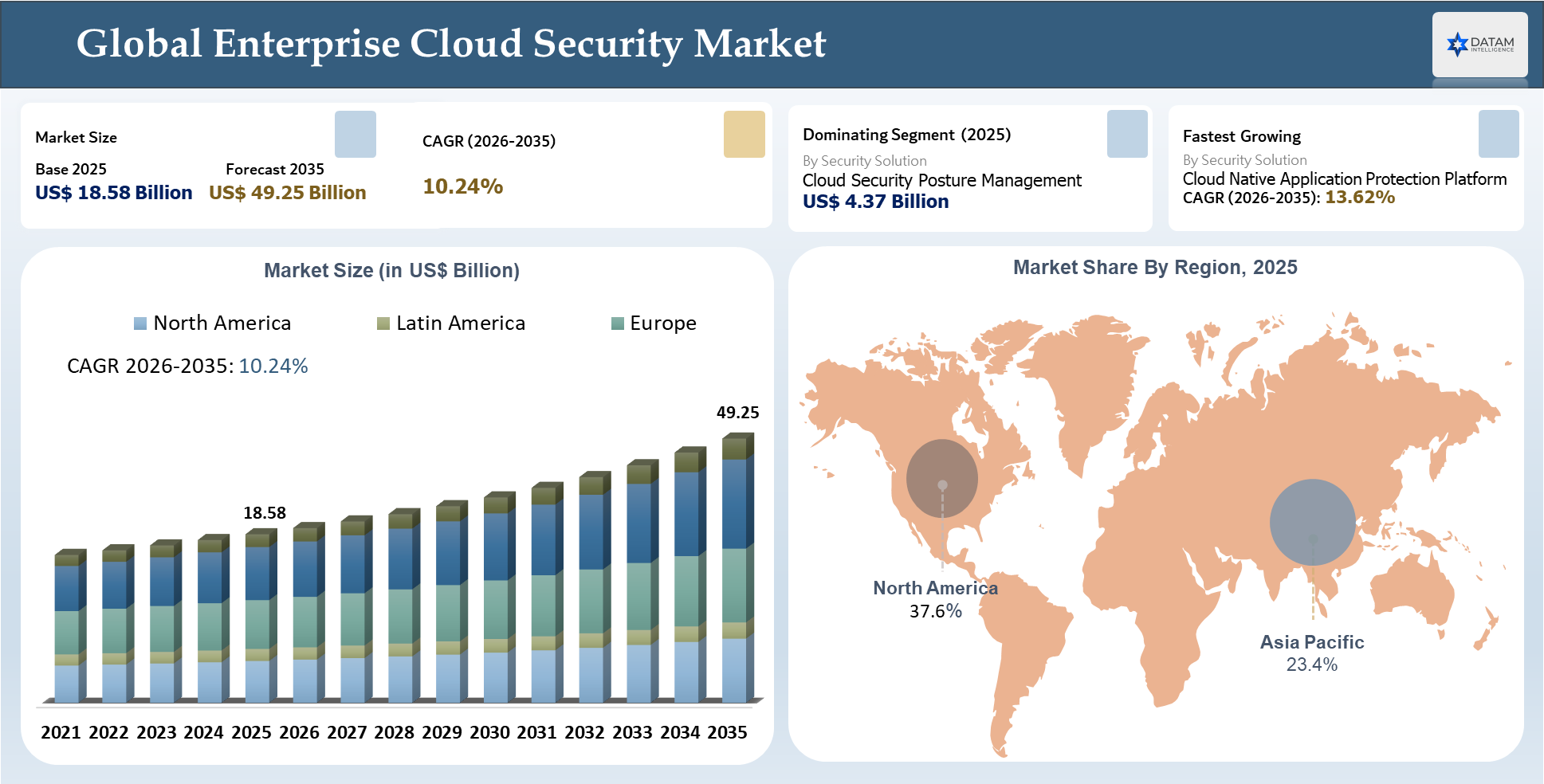

The Global Enterprise Cloud Security Market stood at US$ 18.58 Billion in 2025 and is expected to reach US$ 49.25 Billion by 2035, growing with a CAGR of 10.24% during the forecast period 2026-2035. Increased demand is fueled by higher use of public cloud, private cloud, hybrid cloud, multi cloud, and SaaS technologies, which creates a growing need for workload protection, identity governance, data security, compliance monitoring, threat detection, and cloud risk management capabilities. The key drivers include increased cloud migration, rising ransomware attacks, regulatory pressures, adoption of hybrid work and the necessity to secure distributed applications, APIs, identities, and confidential business data.

The industry trends include adoption of zero trust principles, cloud-native application security, DevSecOps integration, advanced threat detection using artificial intelligence, managed security services and platform consolidation. Cloud Security Posture Management will remain at the top of the list in terms of vendor success because of its ability to identify configuration vulnerabilities, compliance issues and exposed cloud resources. Growth rate is likely to be higher for Cloud Native Application Protection Platform due to enterprises' move towards integrated solutions encompassing posture management, workload protection, container security, identity risk management and real-time threat detection. Complexity of cloud environment, integration difficulties, lack of professionals and high costs of implementing solutions may hinder further market development.

AI Impact Analysis

In the Global Enterprise Cloud Security Market, artificial intelligence is expected to become a prominent growth facilitator owing to growing complexity in the cloud, identity-based attacks, configuration errors, ransomware attacks, and high frequency of security alerts in hybrid and multi cloud environments. By leveraging artificial intelligence, cloud security solutions can help businesses identify unusual activity by users, detect exposed cloud workload identities, prioritize cloud vulnerability management, implement cloud policies automatically, and minimize investigation time. Security operations teams will leverage AI to enhance capabilities such as threat intelligence, cloud posture management, incident response, compliance management, and real-time risk scoring. This becomes important for large-scale enterprises that are managing distributed applications, APIs, containers, software-as-a-service platforms, and confidential data in multiple clouds.

On the other hand, the adoption of artificial intelligence is changing vendor competition dynamics as companies are transforming from rule-based monitoring and analytics to advanced approaches of predictive analytics, automation, and context-aware security. Enterprises will prefer cloud-native security vendors offering integrated solutions combining CNAPP, CSPM, CWPP, CIEM, SIEM, XDR, and zero trust platforms. Yet AI has the potential to raise risks for enterprises as cyber criminals use generative AI for their nefarious purposes like phishing, malware generation, and automated reconnaissance.

Enterprise Cloud Security Industry Trends and Strategic Insights

- Security solution capability remains the most crucial factor in commercialization, as organizations are increasingly looking at ways to secure their cloud workloads, applications, APIs, identities, data, network, and multi-cloud environments.

- There is growing interest in cloud security platforms that deliver capabilities such as cloud risk visibility, configuration management, cloud workload protection, identity governance and administration, compliance monitoring, threat detection, remediation automation, and DevSecOps integration.

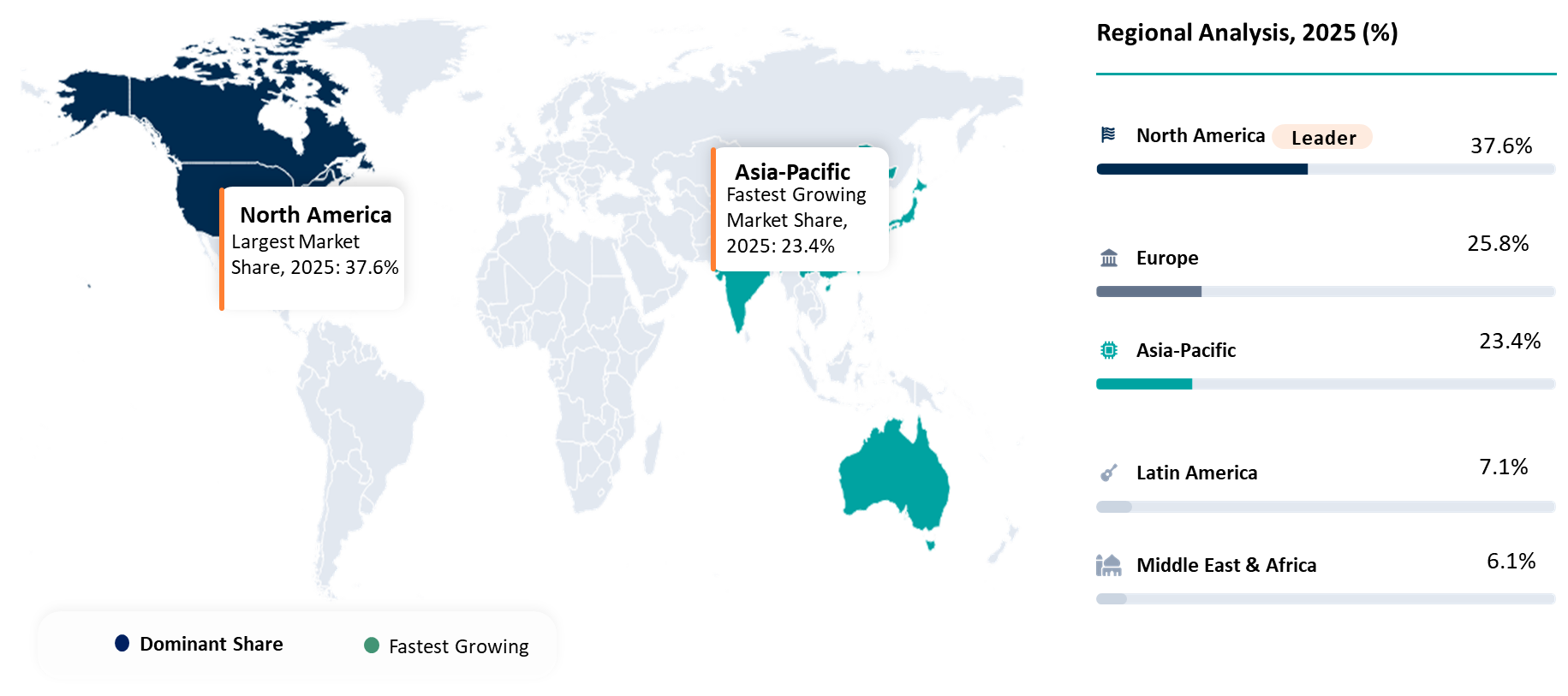

- North America emerges as the dominant region in the market, backed by its mature cloud computing usage, higher cybersecurity investments, presence of cloud security vendors, well-established enterprise IT infrastructure, and adoption of zero trust security, Cloud Native Application Protection Platforms (CNAPP), Secure Access Service Edge (SASE), and artificial intelligence-based threat detection solutions.

- The successful vendors would have more to offer than point products alone, like cloud security platforms, AI-powered risk prioritization, multi-cloud visibility, compliance dashboards, security services alliances, and hyperscaler and enterprise-friendly implementations.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 18.58 Billion | |

| 2035 Projected Market Size | US$ 49.25 Billion | |

| CAGR (2026-2035) | 10.24% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Security Solution | Cloud Security Posture Management, Cloud Workload Protection Platform, Cloud Access Security Broker, Cloud Infrastructure Entitlement Management, Cloud Native Application Protection Platform, Cloud Data Loss Prevention, Cloud Identity and Access Management, Cloud Encryption and Key Management, Cloud Network Security, Cloud Threat Detection and Response, Secure Access Service Edge, Zero Trust Cloud Security, and Others | |

| By Deployment Environment | Public Cloud, Private Cloud, Hybrid Cloud, and Multi Cloud | |

| By Enterprise Size | Large Enterprises, Medium Enterprises, and Small Enterprises | |

| By Deployment Architecture | Agent Based Security, Agentless Security, API Based Security, Proxy Based Security, Platform Integrated Security, and Others | |

| By End User | BFSI, IT and Telecom, Healthcare and Life Sciences, Retail and Ecommerce, Manufacturing, Government and Defense, Energy and Utilities, Education, Media and Entertainment, and Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Disruption Analysis

Cloud-Native Security Disruption Reshaping Enterprise Risk, Identity Protection and Platform Consolidation

The enterprise cloud security market is currently experiencing massive disruption due to the transition of companies from perimetrical security to cloud-native, identity-focused, and platform-driven protection solutions. The proliferation of hybrid cloud, multi-cloud, SaaS applications, containers, APIs, and remote access has contributed to an increase in the attack surface area within enterprises, rendering old-school security products ineffective. Cloud misconfigurations, exposed workloads, overprivileged permissions, and identity threats have become some of the biggest risks that are driving enterprises towards implementing continuous monitoring, automated remediation, and dynamic risk prioritization.

One of the biggest disruptors in this field is the consolidation of point solutions into cloud security platforms. Enterprises are abandoning isolated products in favor of integrated platforms that can offer posture management, workload protection, identity governance, data protection, threat detection, and compliance solutions under one roof. AI is further fueling disruptions within the industry as it helps deliver fast anomaly detection, predictive threat analytics, and automated incident response. On the downside, generative AI is helping attackers automate phishing campaigns, reconnaissance operations, and malware development. Therefore, cloud security providers are differentiating themselves through automation capabilities, intelligence, integration capabilities, cloud-native security coverage, and operational simplicity.

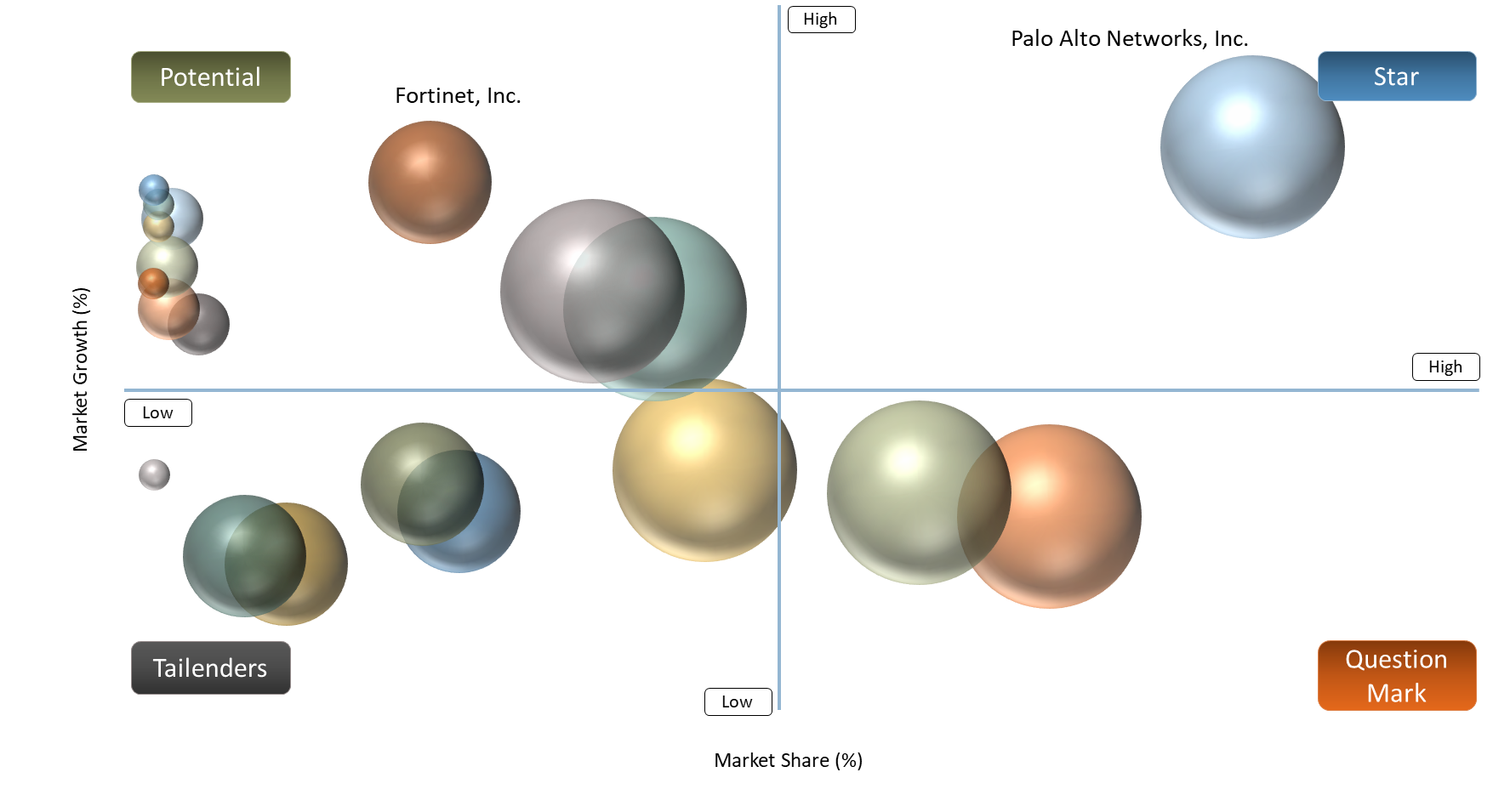

BCG Matrix: Company Evaluation

As for the BCG matrix, Stars will be the players in the Global Enterprise Cloud Security Market with substantial global presence, robust portfolio of cloud security, and strong enterprise adoption along with sophisticated capabilities in cloud native security, zero-trust, AI-based threat intelligence, workload security, and risk/compliance automation. Palo Alto Networks, Inc., Microsoft Corporation, CrowdStrike Holdings, Inc., Zscaler, Inc., Wiz, Inc. and Cloudflare, Inc. can qualify as Stars by virtue of their innovation power, customer base growth and ability to mitigate cloud security challenges.

Cash Cows will be mature companies within the cybersecurity and cloud infrastructure industry with strong relationships with enterprises, revenue streams and significant customer base. Fortinet, Inc., Cisco Systems, Inc., Trend Micro Incorporated, Check Point Software Technologies Ltd., Broadcom Inc., Google LLC and Amazon Web Services, Inc. would qualify as Cash Cows based on their legacy security products, cloud integrations, regulatory needs and enterprise contractual relationship.

Question Marks will be niche vendors with growth prospects but with relatively lower scale when compared to platforms. Netskope, Inc. and Orca Security Ltd. belong to this segment where their future growth depends on enterprise uptake, geographies served, channel support, and platform integrations.

Market Dynamics

Rising Cloud Migration Increasing Enterprise Exposure to Cyber Risks

The rapid increase in the migration of enterprises to the cloud is driving growth in the Global Enterprise Cloud Security Market. This is because many businesses are now migrating their applications, workloads, databases, development environments and critical business processes from their in-house infrastructure onto public, private, hybrid and multi-clouds. While this is proving beneficial for enterprises in terms of increased scalability, agility and cost-effectiveness, the migration also increases the enterprise attack surface due to misconfigurations in storage, exposure to APIs, excessive user privileges, insecure workloads, shadow clouds and lack of visibility. Traditional perimeter security systems will prove insufficient in this environment, as enterprises will be working on multiple clouds and Software as a Service (SaaS) solutions.

As a result, enterprises are looking to invest in cloud security products that enhance visibility, identity controls, data security, compliance management, threat detection and incident response. In regulated industries such as banking, financial services, and insurance (BFSI), health care, government, information technology (IT) and manufacturing, securing sensitive data and ensuring audit readiness is critical.

Complex Cloud Architectures Creating Integration and Visibility Challenges

The increasing complexity of cloud architectures emerges as another critical constraint for the global enterprise cloud security market. Enterprises have begun adopting public clouds, private clouds, hybrid clouds, multi-clouds, Software-as-a-Service (SaaS) apps, containers, and API services. Each environment has unique security mechanisms, authentication schemes, logging facilities, compliance considerations, and configuration practices. The result is fragmented visibility, making it hard for security experts to assess assets, detect misconfigurations, user permissions, and vulnerabilities in real time. Enterprises may also employ multiple security solutions that fail to communicate with one another, which results in duplicated alerts, operational inefficiencies, and delayed incident response processes.

However, the situation gets worse for large corporations that deploy legacy systems, have complex dependencies between applications, and rely on distributed computing facilities. Security professionals may find it challenging to enforce uniform policies throughout cloud providers, development processes, and organizational units. Delays in integration, limited availability of cloud security talent, and absence of centralized governance can make cloud security initiatives ineffective. Consequently, enterprises are forced to curtail their expansion plans or invest in expensive implementations.

Segment Analysis

The Global Enterprise Cloud Security Market is segmented based on security solution, deployment environment, enterprise size, deployment architecture, end user and region.

Cloud Native Application Protection Platform Leads Enterprise Demand as Organizations Shift Toward Integrated Cloud Risk Management

Cloud Native Application Protection Platform (CNAPP) is likely to become one of the most promising markets in the Global Enterprise Cloud Security Market due to the rising need for a unified solution that can protect applications, workloads, containers, APIs, identities, and cloud infrastructure. With their growing adoption of cloud computing in hybrid and multicloud deployments, companies tend to struggle with fragmented visibility, redundant alerts, and challenges to identify and prioritize potential threats. This is where CNAPP becomes relevant, providing comprehensive security features including cloud posture management, workload protection, vulnerability scanning, identity risk assessment, compliance assurance, and runtime threat protection.

Enterprises are becoming more interested in CNAPP since it offers better support for security teams as well as DevSecOps practices. Specifically, it enables the identification of vulnerabilities early on and improves the protection of cloud native applications, monitoring of production workloads, and lowering risk levels associated with overly privileged users and vulnerable assets. Furthermore, in highly regulated industries like BFSI, healthcare, government, IT and manufacturing, the use of CNAPP will improve audit-readiness and continuous compliance. Since enterprises are gradually shifting from using various point solutions to adopting unified security platforms, CNAPP could receive greater budget allocation in the coming years.

Geographical Penetration

North America Leads Enterprise Cloud Security Adoption Through Mature Cloud Infrastructure and Advanced Cybersecurity Investments

North America currently dominates the enterprise cloud security market, thanks to its highly developed cloud adoption, significant investment in cybersecurity measures, and dominance of cloud security solution providers, hyperscalers, and managed security service providers. North American enterprises are embracing public cloud computing, hybrid clouds, multi cloud computing, and software-as-a-service in large numbers, hence the high requirement for comprehensive solutions to safeguard their workloads, identities, data, APIs, and applications. Besides the well-developed digital infrastructure of North America, early embrace of zero trust architecture, cloud-native application protection, and artificial intelligence-based threat detection add impetus to the region's dominance.

Regulatory compliance requirements also drive the demand for cloud security solutions among organizations in key industries such as BFSI, healthcare, governments, retail, and critical infrastructure providers. Companies are making efforts to enhance cloud security in order to ensure regulatory compliance, reduce exposure to data breaches, enforce effective identity governance, and improve overall visibility in their cloud environments. Rising challenges from ransomware attacks, cloud configuration issues, third-party access, and lack of skilled personnel in cybersecurity push enterprises to seek integrated solutions, managed security services, and automated risk management capabilities.

U.S Enterprise Cloud Security Market Trends

There is a transition happening within the U.S. enterprise cloud security market, wherein enterprises are shifting from spending on compliance-focused cybersecurity towards making strategic investments in resilience as they expand their digital transformation, migrate workloads to the cloud, embrace software-as-a-service solutions and perform hybrid workforce operations. There is a strong emphasis by security professionals on building a resilient posture, through cloud-native and zero-trust architectures and identity management practices, which will help enterprises defend distributed applications, workloads, APIs, sensitive data and privileged access in multi-cloud environments.

The importance of AI-powered threat detection, automation and continuous governance in the boardroom continues to grow amid escalating costs of breaches. The latest findings from IBM’s 2025 Cost of a Data Breach report indicate that the average cost of a data breach in the U.S. amounted to USD 10.22 million. Consequently, regulated industries, including BFSI, healthcare, government agencies, retail, and technology, are making significant investments in cloud compliance, cloud security, data protection, DevSecOps security, and managed cloud security services.

Japan Enterprise Cloud Security Market Outlook

Japan Enterprise Cloud Security Market is showing promise owing to increased efforts towards digital transformation, cloud migration, adoption of AI and hybrid workspace modernization. Demand for cloud security solutions is growing among BFSI, manufacturing, healthcare, IT, telecoms, government and critical infrastructure organizations in order to strengthen their cloud workload security, identity and access management, application security, API security and data security. Cloud security products that enable compliance, risk management, identity governance, threat detection and business continuity across hybrid and multi-cloud environments have become more relevant to Japanese enterprises.

Furthermore, government-driven digitalization initiatives will further contribute to the market. The digitalization initiative launched by the Digital Agency of Japan is ongoing, whereas the national cybersecurity strategy focuses on increasing capability and improving coordination in handling cybersecurity incidents among public organizations. Cloud and AI infrastructure investments in Japan are on the rise; for example, Microsoft recently announced an investment of $2.9bn to increase its cloud and AI infrastructure capacity in Japan by 2025. Overall, the outlook of the Japan Enterprise Cloud Security Market looks promising due to increased cyber risks, dependency on suppliers and regulatory requirements.

Competitive Landscape

The Global Enterprise Cloud Security Market is characterized by intense competition, whereby legacy cybersecurity firms, hyperscale cloud service providers, and emerging cloud-native security companies compete for securing enterprise applications, data, identities, and workloads in hybrid and multi-cloud environments. Leading enterprises include Palo Alto Networks, Inc., Microsoft Corporation, CrowdStrike Holdings, Inc., Fortinet, Inc., Zscaler, Inc., Cisco Systems, Inc., Trend Micro Incorporated, Check Point Software Technologies Ltd., Broadcom Inc., Google LLC, Amazon Web Services, Inc., Cloudflare, Inc., Netskope, Inc., Wiz, Inc. and Orca Security Ltd. Firms are consolidating their market positions using cloud-based integrated security platforms, artificial intelligence-based threat analysis, cloud workload protection, zero trust security, SASE, CNAPP, and identity governance solutions.

There is a transition from individual security solutions to a unified cloud security platform that simplifies operations, enhances visibility, and prioritizes risks in real-time. Large-scale companies enjoy a significant advantage because of their extensive customer base, corporate trust, extensive cybersecurity portfolio, and robust partner ecosystem. Cloud-native security firms such as Wiz, Orca Security, and Netskope are gaining popularity due to their innovations in cloud-native security, agentless monitoring, cloud access protection, and risk management solutions. Differentiation among vendors is influenced by automation capabilities, integration, multi-cloud support, DevSecOps, threat intelligence, and regulatory compliance.

Key Developments

- March 2026: Google Cloud completed the acquisition of Wiz, strengthening its cloud and AI security portfolio while retaining the Wiz brand under Google Cloud.

- March 2026: Zscaler collaborated with NVIDIA to integrate Zscaler AI Guard with NVIDIA NeMo Guardrails, supporting stronger security controls for generative AI applications in cloud environments.

- February 2026: Orca Security added Tencent Cloud support, expanding its agentless CNAPP coverage across AWS, Azure, Google Cloud, Oracle Cloud, Alibaba Cloud and Tencent Cloud environments.

- October 2025: Palo Alto Networks introduced Cortex Cloud 2.0, expanding CNAPP capabilities with AI agents, unified Cloud Command Center and cloud detection and response enhancements.

- October 2025: CrowdStrike launched its Fall 2025 release, positioning the Falcon platform for agentic security operations with AI-ready data, intelligence and AI-powered security agents.

- July 2025: Orca Security expanded runtime security to hybrid and private cloud environments, strengthening its agentless-first cloud security platform for broader enterprise deployments.

- February 2025: Palo Alto Networks introduced Cortex Cloud, combining Prisma Cloud with Cortex cloud detection and response to deliver real-time cloud security, AI-powered prioritization and automated remediation.

- February 2025: Orca Security launched new application security capabilities to unify security, DevOps and development teams for lifecycle-based cloud-native application protection.

- August 2024: Fortinet completed the acquisition of Lacework, adding cloud security and CNAPP capabilities to strengthen its enterprise cloud security portfolio.

- June 2024: Zscaler announced a collaboration with NVIDIA to accelerate AI-powered copilot technologies and security-centric enterprise services.

- April 2024: Cisco announced Cisco Hypershield, an AI-native security architecture designed to protect data centers and cloud environments, with general availability expected in August 2024.

White Space Opportunities

The Enterprise Cloud Security Market holds promising white space opportunities as companies evolve from basic cloud security to an integrated, automated, and industry-specific security approach. There is a significant opportunity in AI workload security, with the adoption of generative AI models, machine learning models, and cloud AI infrastructure, which require protection from data exfiltration, model mismanagement, untrusted access, and adversary attacks. Identity-first cloud security also offers compelling opportunities, driven by challenges such as excessive privileges, unmanaged identities, and service account risks.

There is another area for exploration in SME-focused cloud security, where small and medium-sized enterprises seek cost-effective and simple deployment solutions with managed security capabilities. The sovereign cloud and compliance-driven security market segments hold potential for growth, especially within regulatory industries such as BFSI, healthcare, governments, and critical infrastructures. Vendors can leverage their offerings through cloud-native application protection, API security, Kubernetes security, automated remediation, agentless visibility, and compliance dashboards for specific industries. In the buyer's journey, there is a growing need for fewer tools and quick decision-making on risk issues. Platforms that offer visibility, prioritization, automation, and advisory services will be attractive.

DMI Opinion

According to DataM, the biggest challenge in the Global Enterprise Cloud Security Market is not to generate demand but the capability of vendors to integrate their cloud security offerings to make them scalable and enterprise-ready solutions. Increasingly, the market favors the providers that focus on more comprehensive solutions by bringing together visibility, risk prioritization, identity governance, workload protection, compliance automation, threat detection, incident response, and multi cloud management under one platform.

On the other hand, organizations are looking at vendor capabilities in managing cloud misconfiguration risks, permissions, APIs, containers, data protection, DevSecOps, and real-time monitoring across various clouds (public, private, hybrid and multi cloud). Sectors like BFSI, healthcare, government, IT, and manufacturing are particularly interested in solutions that improve audit readiness, data governance, and business continuity and resilience.

While some players continue to compete on price or specific features, such a strategy could prove unsustainable in the long run, especially considering that the market is moving towards consolidation and automation. Vendors offering cloud-native, AI-based threat detection capabilities and compliance dashboard solutions will likely emerge stronger in the coming years.

Why Choose DataM?

- Tracking Innovation in Cloud Security: Tracks the development of various cloud security technologies such as cloud security posture management, cloud workload protection, cloud native application protection platform, cloud access security brokers, cloud infrastructure entitlement management, cloud data loss prevention, encryption, identity security, zero trust cloud security, and threat detection platforms among others.

- Analysis of Security Performance and Enterprise Suitability: Analyzes the performance of various cloud security solutions in a range of cloud computing environments including public cloud, private cloud, hybrid cloud, and multi-cloud. The study evaluates the visibility capabilities, misconfiguration detection, workload protection, identity risk control, data protection, automation of compliance, runtime threat detection, API security, container security, and other capabilities.

- Real-Life Implementation Cases for Enterprise Cloud Security: Provides insights into implementation cases related to enterprise cloud security in areas such as data protection, cloud compliance, identity governance, application security, workload protection, cloud network security, DevSecOps security, incident response, ransomware prevention, and continuous monitoring.

- Market Trends & Industry Evolution: Highlights various trends including increased multi-cloud usage, elevated cloud misconfiguration risks, development of AI-powered attacks, growing regulatory requirements, zero trust approach, proliferation of CNAPP, moving from point products to full-fledged cloud security platforms and the need for real-time risk management of clouds.

- Competitive Strategies: Highlights competitive tactics adopted by top cloud security vendors in order to establish themselves in the market through consolidation, AI-powered threats identification, cloud-native security, identity-first security approach, partnerships for managed security, DevSecOps enablement, acquisition tactics, collaboration with hyperscalers and entry into regulated sectors.

- Pricing and Market Access: Analyses pricing structures ranging from subscription-based models, workload pricing, user pricing, cloud consumption related pricing, enterprise licensing models, managed security service models and bundled cloud security platforms. The report also analyzes vendor positioning, channel partnerships, system integration firms’ impact and buyer preferences.

- Market Opportunities and Growth: Emphasizes growth opportunities arising from cloud migration, hybrid workforce, SaaS solutions, compliance requirements, ransomware prevention, identity risks, containerization, AI-based workload security, and demands from BFSI, healthcare, IT & telecom, public sector, manufacturing, and retail verticals. Offers recommendations for vendors, investors, and enterprise customers regarding market entry, product positioning, strategic partnerships, and portfolio enhancement.

Target Audience 2026

- Cloud security solution providers

- Cybersecurity software vendors

- Cloud service providers and hyperscalers

- Managed security service providers

- System integrators and IT consulting firms

- Chief information security officers and security teams

- Cloud architecture and DevSecOps teams

- BFSI, healthcare, IT and telecom enterprises

- Government, defense, and regulated industry buyers

- Private equity, venture capital, and technology investors