Direct Air Capture (DAC) Market Overview

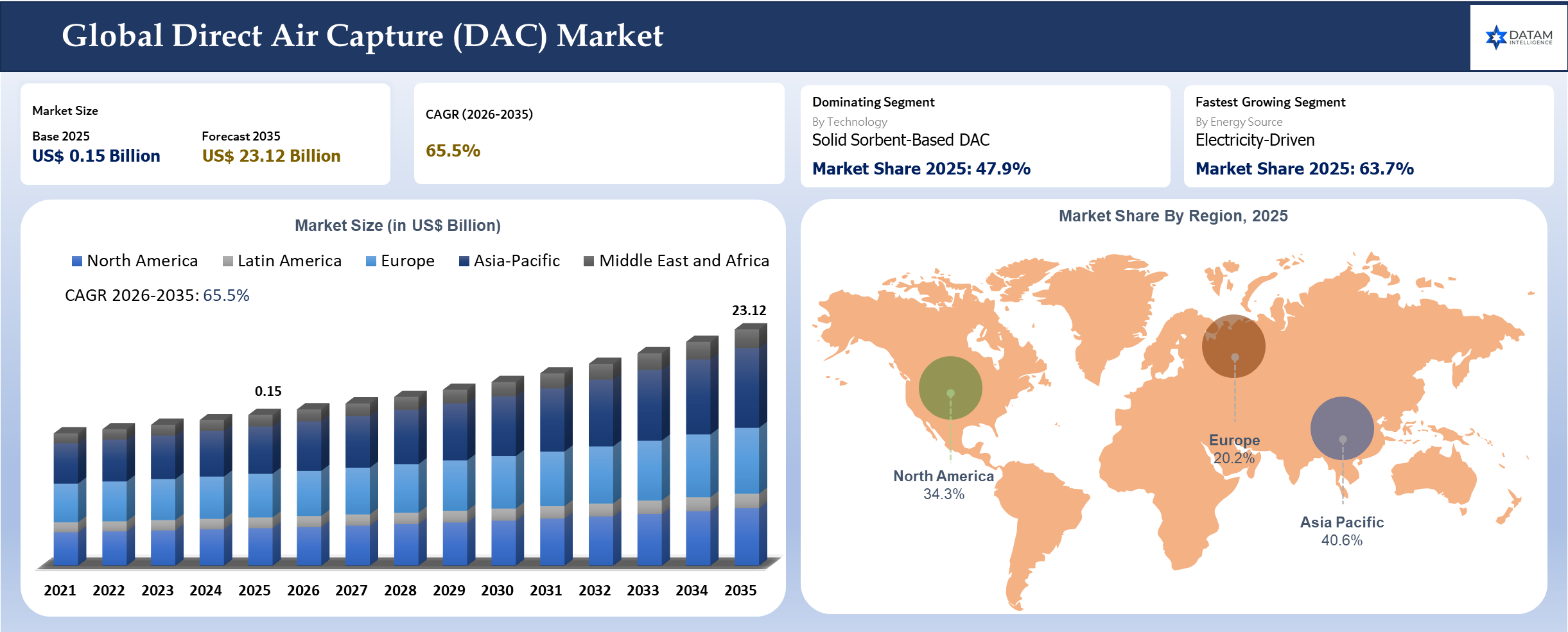

The global Direct Air Capture (DAC) Market reached US$ 0.15 billion in 2025 and is expected to reach US$ 23.12 billion by 2035, growing with a CAGR of 65.5% during the forecast period 2026-2035. DAC technology has rapidly evolved into a vital component of climate technologies, as policymakers and companies strive to achieve their net-zero targets in hard-to-abate sectors such as aviation, cement and chemicals. The market would be boosted by increased ambition in carbon dioxide removal and financial support programs.

As per International Energy Agency, the world requires the development of more than 85 million metric tons per year of DAC capacity from below 0.01 million metric tons of carbon dioxide to realize its net-zero targets. With the ongoing development of carbon markets and carbon prices across the world, DAC technology is transitioning from an innovative technology to a significant part of the global decarbonization strategy.

Direct Air Capture (DAC) Industry Trends and Strategic Insights

- The adoption of a net-zero target by 2050 requires increasing the current capacity of direct air capture from below 0.01 million tons to over 1 billion tons annually, highlighting the extent of development potential.

- Technologies for the removal of carbon dioxide, including direct air capture, will be required to provide around 5 to 10 gigatons of carbon dioxide removal annually up to the middle of the century.

Direct Air Capture Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 0.15 Billion | |

| 2035 Projected Market Size | US$ 23.12 Billion | |

| CAGR (2026-2035) | 65.5% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | North America | |

| By Technology | Solid Sorbent-Based DAC, Liquid Solvent-Based DAC, Electrochemical DAC, Membrane-Based DAC, Hybrid (Integrated DAC Systems | |

| By Energy Source | Electricity-Driven, Thermal (Heat) Driven, Hybrid Energy Systems | |

| By Application | Carbon Storage, Carbon Utilization | |

| By End-User | Oil & Gas, Power & Utilities, Chemical & Petrochemical, Food & Beverage, Automotive & Mobility, Aviation, Maritime, Steel, Cement, Refineries, Pulp & Paper, Carbon Management & Storage Developers, Others | |

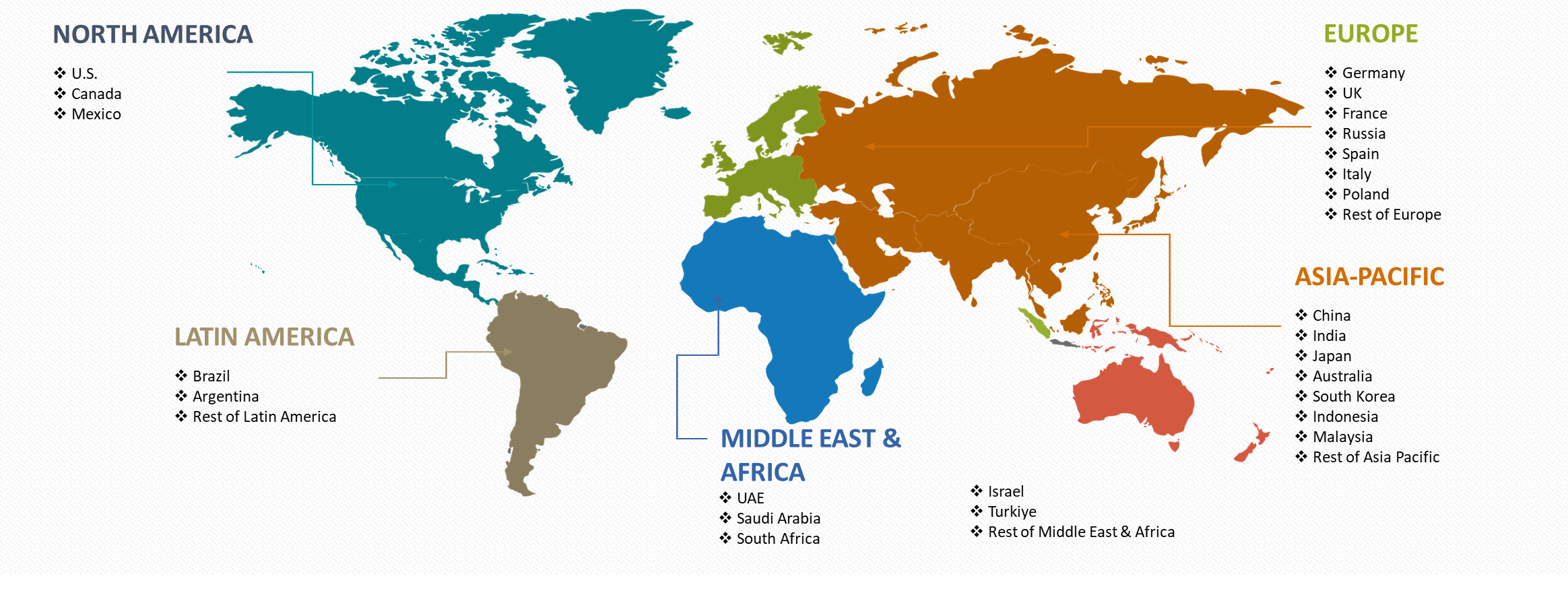

| By Region | North America | USA, Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Disruption Analysis

The involvement of government-led projects, such as those led by the International Energy Agency and domestic ventures like USA DAC hubs, is transforming the technology from laboratory-based experiments to large-scale installations. The disruption caused by innovation is being experienced through innovative techniques that include solid sorbents, mineralization and electrochemistry, greatly reducing the energy requirement and per-ton cost.

Firms such as Skytree and Avnos are developing compact and low-water consumption DAC plants, solving some of the challenges that have plagued the technology. Moreover, the increasing interest in voluntary carbon markets and corporations’ pledges for net-zero emissions, including companies like Microsoft, is changing the dynamics of demand through carbon removal contracts. Nonetheless, the potential for disruption still exists owing to the lack of carbon pricing certainty, insufficient transport and storage infrastructure and regulatory changes, among others.

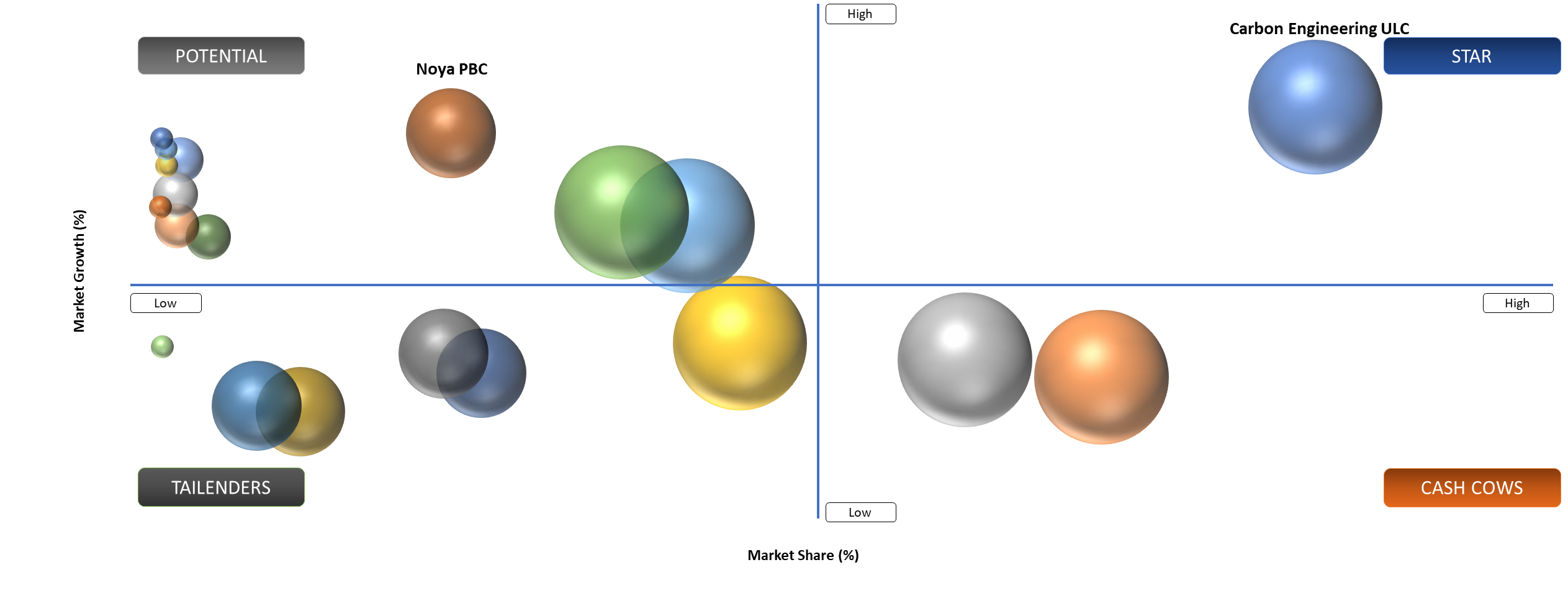

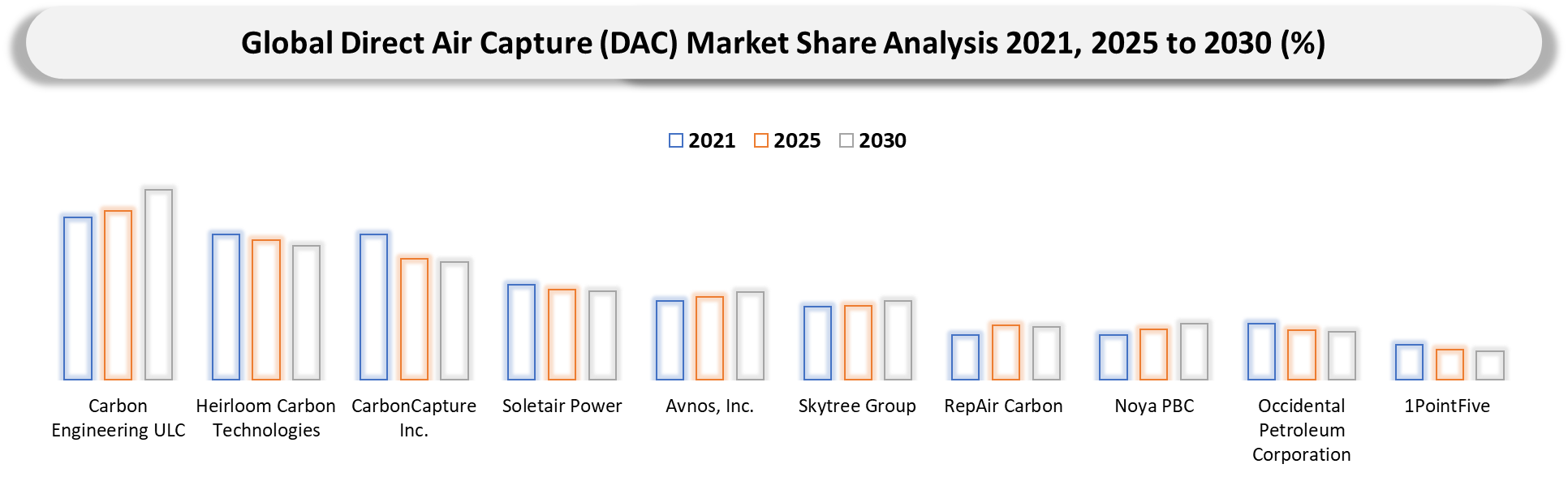

BCG Matrix: Company Evaluation

Among Stars are Climeworks and Carbon Engineering, who excel in both technological viability and large pipeline projects, along with partnerships with energy corporations. The companies profit from increasing regulatory support in terms of federal government investment under the DAC hubs program run by USA Department of Energy. The Potentials group includes companies like Heirloom Carbon Technologies and Noya PBC, having an innovative, yet highly cost-effective strategy for DAC, but still being at early stages of commercialization. Question Marks are few because of the infancy of the sector, although diversified companies like Occidental Petroleum have a steady revenue stream from oil operations.

Direct Air Capture Market Dynamics

Rising Corporate Demand for Carbon Removal Credits

Companies with significant corporate influence have been investing billions into carbon capture purchases to attain their net-zero targets. For example, companies such as Microsoft and Alphabet Inc. have engaged in long-term deals with DAC companies to buy carbon credits through carbon removal. In 2023, Microsoft contracted more than 1.4 million tons of carbon removal from different technologies, which include DAC projects, to achieve its aim of becoming carbon negative by the year 2030. Additionally, the Frontier Climate scheme that includes companies such as Stripe, Shopify and Meta, among others, has promised close to $1 billion in carbon removal purchases, generating demand signals for DAC firms.

High Energy Requirements and Cost Constraints

A considerable amount of heat and electricity is required to extract and purify CO₂ through DAC technology, meaning energy sources are an important consideration for such projects. According to the International Energy Agency, the amount of energy required for each ton of CO₂ captured using existing DAC technology varies from 1,500 to 2,500 kWh, based on the technology utilized, there is a need for reliance on clean energy sources to maximize the environmental impact. Furthermore, according to the National Renewable Energy Laboratory, costs associated with DAC vary depending on the maturity level of the technology being used, with less mature technology incurring much higher expenses because of economies of scale limitations.

Direct Air Capture Market Segmentation Analysis

The global Direct Air Capture (DAC) market is segmented based on technology, energy source, application, end-user and region.

Carbon Storage and Utilization Infrastructure Expansion

The captured CO₂ from DACs could either be stored in geological formations or used in different industries to produce fuels and building materials. The Global CCS Institute reported that there were more than 390 projects for CCUS under construction in the world as of 2024, compared to 100 projects in 2020. It should be noted that quick development of transportation and storage infrastructure is necessary for the advancement of DACs. Some oil and gas firms are capitalizing on their subsurface engineering expertise to construct carbon dioxide storage facilities. North America and the North Sea are some of the locations where carbon dioxide storage facilities are developed.

Technology Innovation and Modular Deployment Trends

Rapid development in technology is helping to make DAC operations efficient and scalable. Businesses are working towards the development of new-generation sorbents, modular systems and automation processes to increase efficiency and decrease the cost associated with DAC implementation. Modular systems enable DAC plants to be scaled efficiently to make them suitable for deployment at different places, such as industrial zones and areas where renewable energy sources can be easily accessed. Various research organizations and governmental bodies are funding new research initiatives in an effort to bring more innovations in the field of DAC technology.

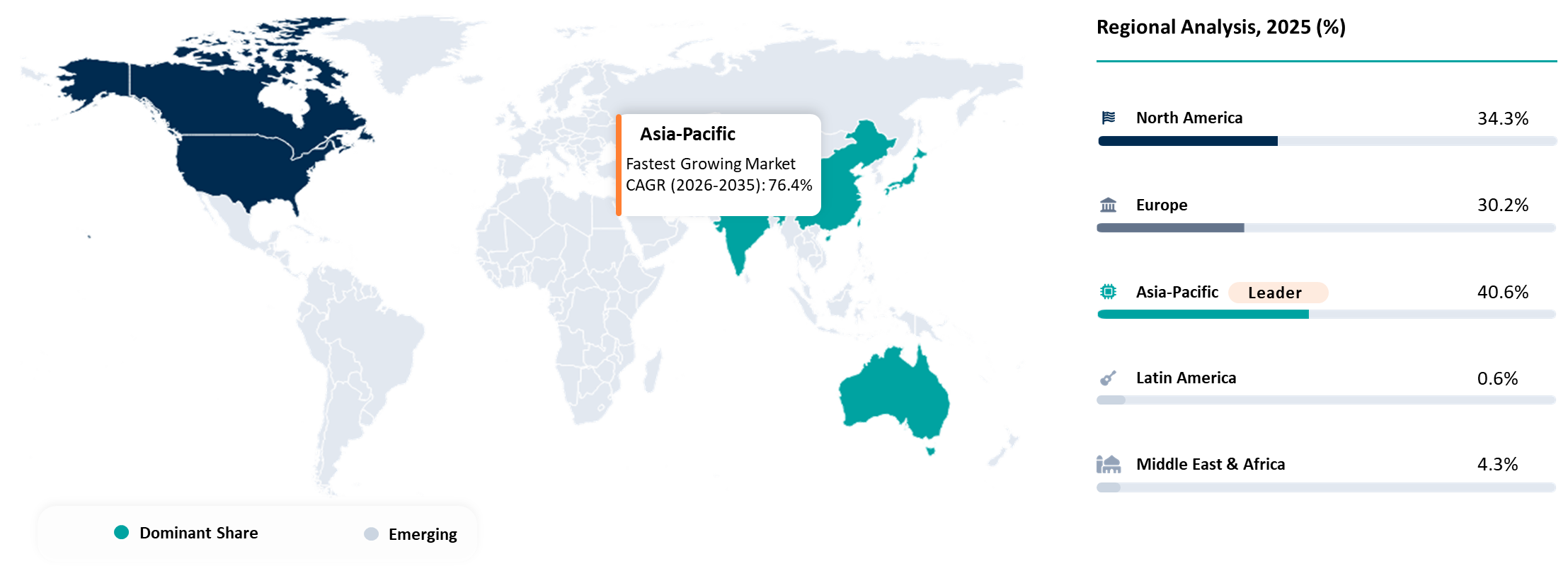

Direct Air Capture Market Geographical Penetration

North America Leads with Policy-Driven Deployment

North America leads the way regarding DAC technology development because of robust backing from both the government and private sectors, along with significant financial support. In particular, the United States is leading DAC developments through incentives, such as the 45Q tax credit, provided by the government. Several hubs of DAC are being planned in states like Texas and Louisiana by USA Department of Energy with the aim of building carbon removal communities in specific regions. Similarly, Canada is progressing in terms of DAC through financial backing for developing technologies related to carbon capture.

USA Direct Air Capture (DAC) Market Trends

The US is the leading state concerning the implementation of DAC technologies owing to high investments in DAC technologies, demands for carbon removal and decarbonization of industries within the country. The US Department of Energy has committed itself to spending USD 3.5 billion on DAC facilities through the DAC Hubs project in Texas and Louisiana. The projects have become some of the most significant governmental financial investments in carbon removal in the entire world.

In addition, large private companies, including Occidental Petroleum Corporation trading under 1PointFive, are constructing facilities that have capacities to remove millions of tons of carbon dioxide for its permanent storage underground. According to the International Energy Agency, the US contributes substantially to the global DAC pipeline owing to various incentives provided by the US government to the companies investing in carbon removal projects, like 45Q credit, entitling the companies to get up to USD 180 for each ton of CO2 captured by DAC. Tech companies have also signed several billion-dollar agreements with DAC companies for carbon removal.

Canada Direct Air Capture (DAC) Market Trends

Canada is becoming a DAC innovation powerhouse thanks to the presence of favorable geological features and the support of the government. The company Carbon Engineering, one of the first pioneers in the DAC industry, has created a solvent-based process, which is currently being commercially implemented in North America.

Moreover, the Canadian government has provided an Investment Tax Credit on 60% of the capital expenses related to DAC facilities, reducing their risk. According to Natural Resources Canada, the country will be focusing on carbon management technologies as a means of achieving its net-zero emissions target in 2050 and DAC will play a key part in this matter. Canada enjoys great CO₂ capacity for underground injection within sedimentary basins located in Alberta. Already, hundreds of millions of dollars have been invested in R&D work involving DAC technologies in Canada through collaboration between public and private sectors.

Direct Air Capture Market Competitive Landscape

- The global DAC market features a mix of innovative startups, engineering firms and large energy companies competing on technology efficiency, cost reduction and scalability.

- Key players include Climeworks, Carbon Engineering, Occidental Petroleum (through its subsidiary 1PointFive), Heirloom Carbon Technologies and Global Thermostat.

- Companies are differentiating through proprietary capture technologies, energy efficiency and integration with carbon storage solutions.

- Strategic partnerships, government funding and long-term carbon removal purchase agreements are becoming key competitive factors, while investments in large-scale DAC hubs and infrastructure are shaping the future industry landscape.

Key Developments of the Direct Air Capture Market

- April 2026: Heirloom Carbon Technologies partners in USA DAC hubs expansion strategy, aligning projects with federal energy policies and scaling commercial carbon removal infrastructure.

- February 2026: Mission Zero Technologies advances electrochemical DAC pilot deployments, focusing on energy-efficient capture and rapid scalability for industrial and commercial applications.

- February 2026: Noya PBC expands pilot projects retrofitting existing cooling towers with DAC systems, reducing capital costs and accelerating infrastructure-based carbon removal adoption.

- February 2026: Soletair Power expands decentralized DAC solutions for buildings, focusing on HVAC-integrated carbon capture to enable distributed urban carbon removal systems.

- March 2026: Skytree Group accelerates deployment of modular DAC units targeting industrial clients, focusing on decentralized CO₂ supply for food and greenhouse sectors.

- January 2026: Carbyon progresses ultra-fast DAC technology using thin-film contactors to reduce costs and enable gigaton-scale carbon removal ambitions.

- January 2026: Heirloom Carbon Technologies expands Louisiana DAC facilities targeting ~320,000 tons annual CO₂ capture, strengthening USA Gulf Coast carbon removal ecosystem.

- January 2026: Occidental Petroleum Corporation continues scaling DAC through 1PointFive subsidiary, leveraging enhanced 45Q tax credits and integrating carbon capture with oil-field operations.

- January 2026: RepAir Carbon advances electrochemical DAC technology commercialization, emphasizing low-energy carbon capture systems targeting scalable industrial decarbonization applications.

Why Choose DataM?

Technological Innovations: Explores advancements in direct air capture (DAC) technologies, including solid sorbent-based systems, liquid solvent-based capture processes, modular DAC units, low-temperature regeneration technologies, renewable energy-powered DAC facilities, waste heat integration, and AI-enabled process optimization, enabling higher carbon capture efficiency, lower energy consumption, scalable deployment, and improved operational performance.

Product Performance & Market Positioning: Evaluates how different companies deliver direct air capture solutions based on key performance parameters such as CO₂ capture efficiency, energy intensity, sorbent durability, regeneration cycles, scalability, operating costs, modularity, and carbon removal permanence, highlighting how leading players differentiate through proprietary capture technologies, optimized system design, and integrated carbon management capabilities.

Real-World Evidence: Highlights the deployment of direct air capture systems across carbon removal projects, industrial decarbonization initiatives, carbon credit programs, sustainable aviation fuel production, synthetic fuel manufacturing, and permanent geological carbon storage applications, demonstrating benefits such as verified atmospheric CO₂ removal, support for net-zero targets, high-quality carbon credits, and long-term climate mitigation.

Market Updates & Industry Changes: Tracks key developments such as commercial DAC plant launches, pilot project expansions, technology advancements in sorbent materials and solvent chemistry, strategic partnerships, government funding programs, carbon removal procurement agreements, and regional investments across North America, Europe, the Middle East, and Asia-Pacific, supporting the commercialization and scale-up of atmospheric carbon removal technologies.

Competitive Strategies: Analyzes how leading companies strengthen their market position through proprietary DAC technology development, strategic collaborations, long-term carbon removal agreements, investments in large-scale capture facilities, integration with carbon storage infrastructure, renewable energy partnerships, and continuous research aimed at reducing capture costs and improving operational efficiency.

Pricing & Market Access: Explains pricing variations based on capture technology, plant capacity, energy source, carbon storage pathway, project scale, operational efficiency, and verification standards, along with market access through carbon removal service providers, industrial partnerships, voluntary carbon markets, government incentive programs, and corporate net-zero procurement initiatives.

Market Entry & Expansion: Identifies growth opportunities driven by increasing global net-zero commitments, rising demand for durable carbon removal, supportive government policies, expansion of carbon markets, growing investments in carbon capture infrastructure, and technological cost reductions, while outlining strategies such as regional project development, strategic partnerships, technology licensing, renewable energy integration, and large-scale commercial deployment.

Target Audience

- Direct Air Capture Technology Developers

- Carbon Capture, Utilization and Storage (CCUS) Companies

- Carbon Removal Project Developers

- Oil & Gas and Energy Companies

- Industrial Manufacturing Companies

- Carbon Credit Developers & Climate Finance Organizations

- Government Agencies & Environmental Regulators