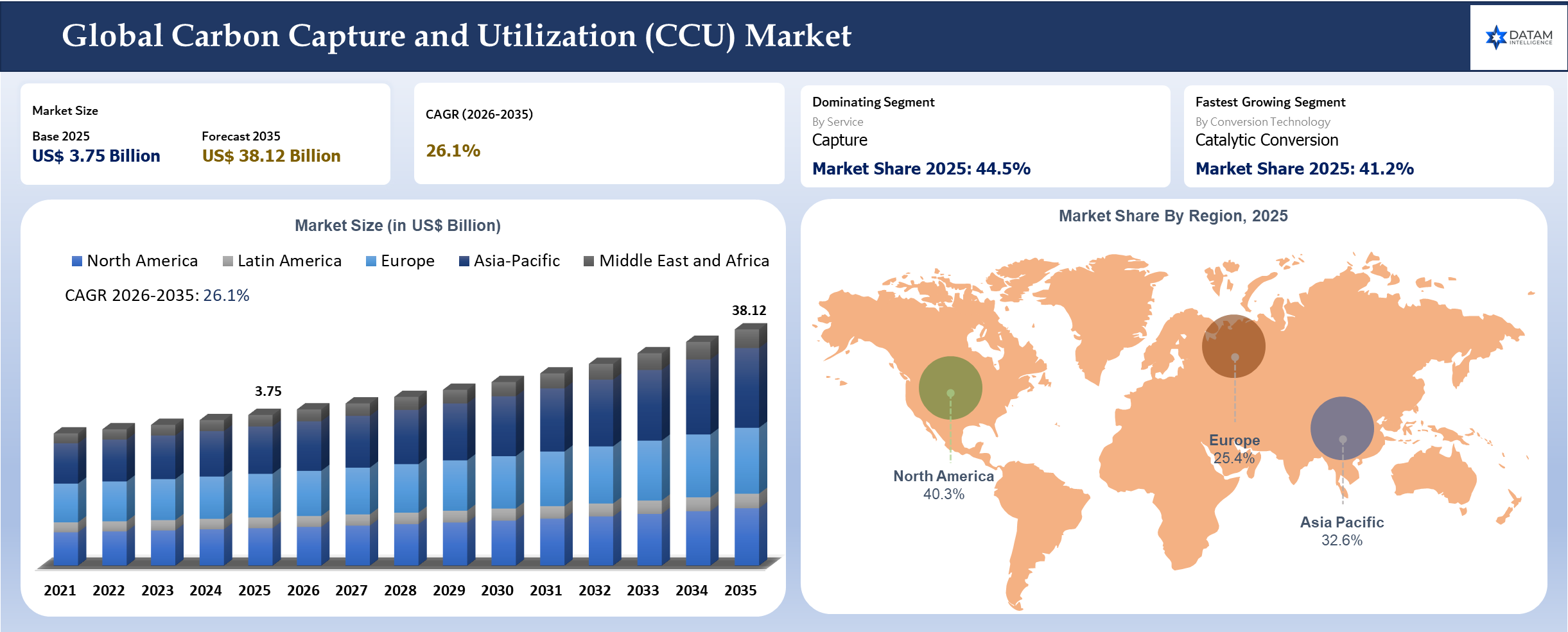

Carbon Capture and Utilization Market Size

The global Carbon Capture and Utilization market size reached US$ 3.75 billion in 2025 and is expected to reach US$ 38.12 billion by 2035, growing with a CAGR of 26.1% during the forecast period 2026-2035. Higher emitting sectors, such as the cement, steel and chemicals sectors, are now implementing CCU technologies, which make it possible to transform CO₂ to fuels, chemicals and construction materials as a way of cutting down on emissions as well as making money in the process. Global capacity for capturing CO₂ annually through projects in development amounts to more than 400 million tons and it is growing at a rapid rate due to government policies and firms going green.

Key Takeaways

- The CCU market is projected for strong long-term growth, rising from USD 3.75 billion in 2025 to USD 38.12 billion by 2035, at a 26.1% CAGR during 2026 to 2035.

- CCU adoption is being driven by hard-to-abate industries, especially cement, steel, and chemicals, where captured CO₂ can be converted into fuels, chemicals, and construction materials. Cement and steel alone generate nearly 20% of global CO₂ emissions, making them key demand centers for CCU deployment.

- The global project pipeline is scaling rapidly, with projects in development representing more than 400 million tons of annual CO₂ capture capacity. This reflects stronger policy support, corporate decarbonization commitments, and commercialization of carbon-to-methanol and mineralization technologies.

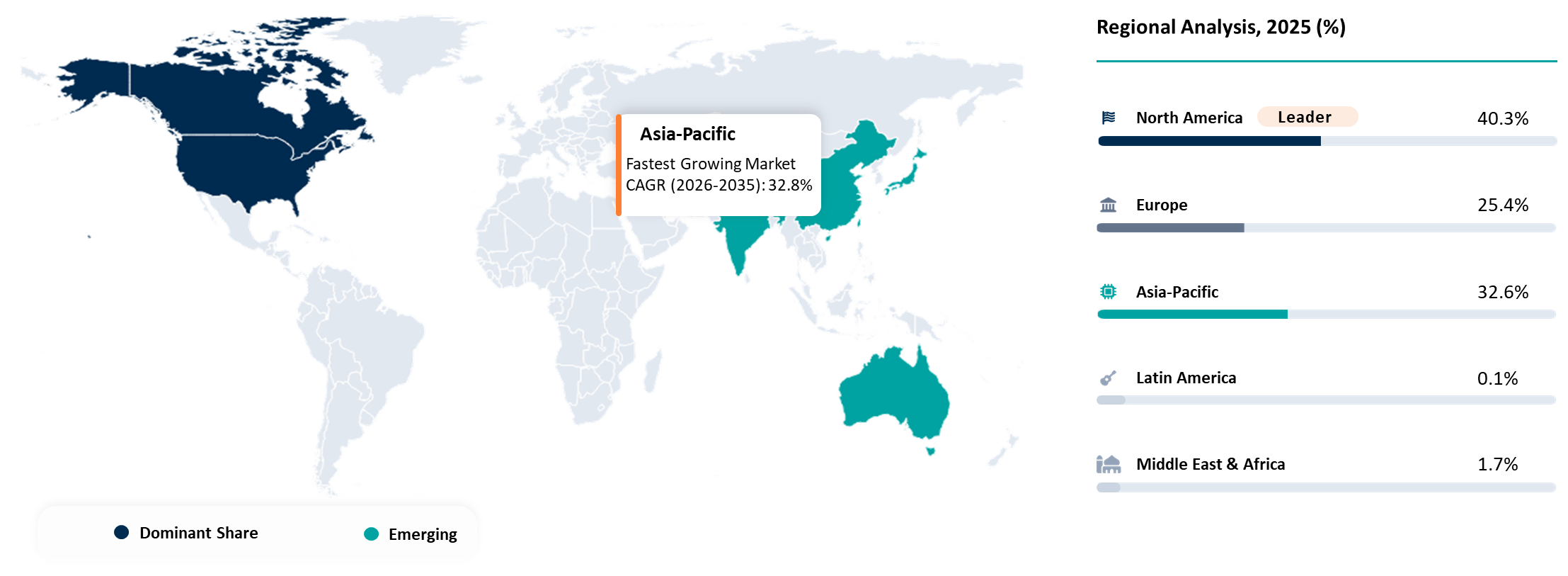

- North America is the largest market, while Asia-Pacific is the fastest-growing region. The US is especially important, supported by the 45Q tax credit, which offers up to USD 85 per ton for captured CO₂ and USD 60 per ton for carbon utilization. The report also notes that over 40% of planned global carbon capture capacity is based in the US.

- Construction materials are becoming a commercially attractive CCU pathway. CO₂ mineralization enables permanent carbon storage in concrete and aggregates while improving material performance. Recent developments in 2025 and 2026 from CarbonBuilt, CarbiCrete, Carbon Upcycling Technologies, O.C.O Technology, and MCi Carbon show increasing commercialization of CO₂-based cement, concrete, and aggregate solutions.

CCU Market Overview

Governments are encouraging the adoption of CCU through incentives provided to firms, such as billions of US dollars invested by US Department of Energy in carbon management hubs and carbon capture technologies. On their part, companies are increasing their investment in R&D with the aim of improving efficiency and reducing prices of CCU. Utilization technologies, such as carbon-to-methanol and mineralization technologies, are already being marketed following pilot projects. Technology is now gaining popularity since it reduces emissions as well as creates profits for firms, hence shifting from environmental technologies to crucial parts of circular carbon economies.

Carbon Capture and Utilization (CCU) Industry Trends and Strategic Insights

- Sectors such as cement and steel generate nearly 20% of all global CO₂ emissions and CCU technology is appealing owing to the possible emission cuts and recycling benefits.

- The manufacture of synthetic fuel from captured CO₂ is growing in popularity, with European pilot projects targeting annual production of over 100,000 tons of e-fuel using renewable hydrogen.

CCU Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 3.75 Billion | |

| 2035 Projected Market Size | US$ 38.12 Billion | |

| CAGR (2026-2035) | 26.1% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Service | Capture, Purification and Conditioning, Compression and Liquefaction, Transportation for Utilization, Utilization | |

| By Conversion Technology | Catalytic Conversion, Biocatalytic, Mineralization, Direct Use Without Conversion | |

| By Source of Captured Carbon | Industrial Point Sources, Biogenic Sources, DAC for Utilization | |

| By Utilization Pathway | Direct Use, Chemical Conversion, Fuel Conversion, Mineralization and Building Materials, Biological Conversion, Enhanced Recovery and Process Use | |

| By Product Form | Gas, Liquid, Solid | |

| By End Product | Fuels, Chemicals, Polymers, Building Materials, Food and Beverage, Carbon Dioxide, Agriculture Inputs, Industrial Gases, Others | |

| By Carbon Purity Requirement | Low Purity Industrial Grade, Medium Purity Process Grade, High Purity, Food and Beverage Grade, Ultra-High Purity Specialty Grade | |

| By Project Scale | Pilot and Demonstration, Commercial Small Scale, Commercial Large Scale | |

| By End-User | Chemical and Petrochemical, Fuel Producers, Building Materials, Food and Beverage, Agriculture, Oil and Gas, Aviation, Automotive and, Mobility, Maritime, Power and Utilities, Others | |

| By Region | North America | USA, Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Türkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Disruption Analysis

Capture techniques that utilize modular solvents, solid sorbents and electrochemical transformation processes have become increasingly cost-effective and efficient, posing a threat to conventional amine-based technologies. Companies such as Clime works and Carbon Engineering are revolutionizing the process of carbon acquisition by integrating direct air capture processes into their products. Tax credits and other policy instruments, as well as carbon pricing, are influencing the flow of investments and speeding up the commercialization process. Cross-industry integration by combining carbon capture and utilization technologies with hydrogen and fuel production, among others, is creating new disruptions in business models. Technology digitization and artificial intelligence optimize the process of carbon capture. Nevertheless, infrastructure issues, expensive capital investments and CO₂ market uncertainties still pose substantial challenges.

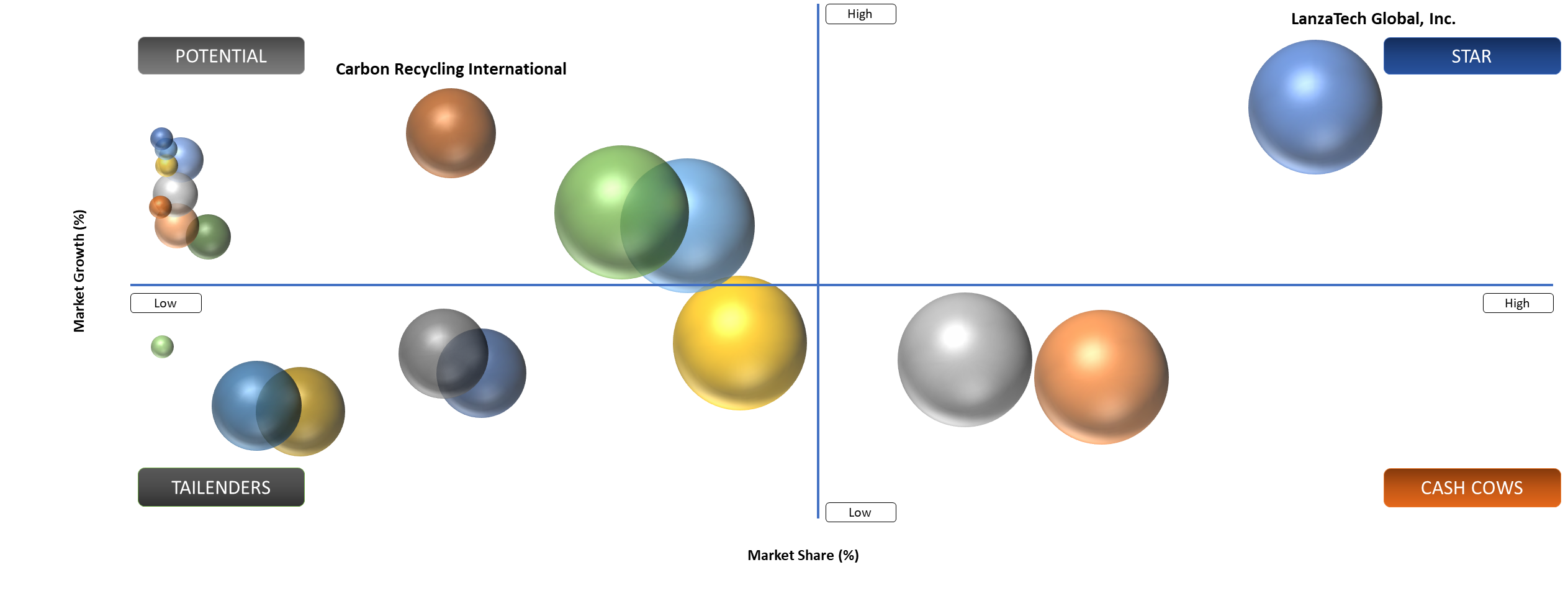

BCG Matrix: Company Evaluation

Star companies are actively investing in CCU hubs on a large scale, along with industry collaborations, given their robust financial power and policy support. Potentials are demonstrated by existing industrial gas and chemicals companies, including Linde plc and Air Liquide, earning steady incomes from the use of carbon for enhanced oil recovery and synthesis of chemicals. Question Mark companies are innovative startups like Carbon Clean and Twelve that have scalable technologies but are still unsure about commercial viability and cost-effectiveness.

Market Dynamics

Rising Demand for Carbon-Derived Products

The rise of CCU results from the growing need for sustainable fuels, chemicals and building materials produced via CO₂ capture. The industries continue developing methods to transform the emitted CO₂ into methanol, aviation fuels and polymer material, which follows the circular economy model. The demand for green hydrogen required for fuel creation may exceed 500 million tons per year in 2050, which will positively influence CCU-based fuel production. Additionally, many companies operating in the building sector use CO₂ mineralization processes to create low-emission concrete products that store carbon permanently.

High Costs and Energy Intensity as Key Barriers

The use of CCU technology presents several problems, including high costs of capital and energy. Capturing carbon dioxide and then turning it into a usable product requires a lot of energy, even more so when the process is combined with hydrogen production. According to the IPCC report, Carbon Utilization technology uses a lot of energy and thus needs low-carbon energy sources to achieve reductions in carbon emissions. Furthermore, there is no standard pricing system for carbon in different regions, hence posing a risk for investors.

Segmentation Analysis

The global Carbon Capture and Utilization (CCU) market is segmented based on the service, conversion technology, source of captured carbon, utilization pathway, product form, end product, carbon purity requirement, project scale, end-user and region.

Chemicals and Fuels Segment Leads Adoption

Chemicals and synthetic fuel production represent the highest technical sector regarding CCU technology application due to the need for decarbonization of aviation, marine and industrial transport. Big oil companies have been testing CCU technology to transform CO₂ into methanol and fuels, such as jet fuel, designed to decrease life cycle greenhouse gas emissions. Several projects within the framework of Mission Innovation program in 2024 will be devoted to the scale-up of carbon utilization technologies. Such projects will help replace fossil feedstocks with recycled carbon-based materials.

Construction Materials Applications Gain Traction

Utilization of captured CO₂ in building materials is becoming increasingly recognized as a commercially feasible route for CCU technology. The application of carbon mineralization techniques enables the permanent storage of CO₂ within concrete and aggregates while increasing the hardness of these materials. The Global Cement and Concrete Association highlights that the potential reduction of greenhouse gas emissions can reach up to 40% through the adoption of low-carbon cement and integration of CCU technologies.

Geographical Penetration

North America Focuses on Innovation and Scale-Up

CCU innovations are currently experiencing tremendous growth in North America because of federal financial support, tax credits and private industry involvement. The most significant factor has been the 45Q tax credit of USA, which gives incentives of as much as US$85 per ton of CO₂ captured for any use whatsoever. The Department of Energy in USA has been instrumental in financing projects that involve the use of CO₂ as fuel and even construction material. In Canada, there are government-sponsored projects aimed at developing CCU technologies.

USA Carbon Capture and Utilization (CCU) Market Trends

CCU systems in North America are largely concentrated within USA, which is driving the adoption of the technology through policies and industry-led innovations in decarbonization across several industries, including power generation, hydrogen and manufacturing. The new expanded 45Q tax credit at up to $85 per ton for carbon capture and $60 per ton for carbon utilization, is stimulating investments, with some notable players such as ExxonMobil and Occidental Petroleum involved in developing projects that involve incorporating captured CO₂ into synthetic fuels and other low-emission products. Over 40% of planned capacity for carbon capture globally is based in USA and an increasing percentage involves carbon utilization for applications like concrete and e-fuels.

Canada Carbon Capture and Utilization (CCU) Market Trends

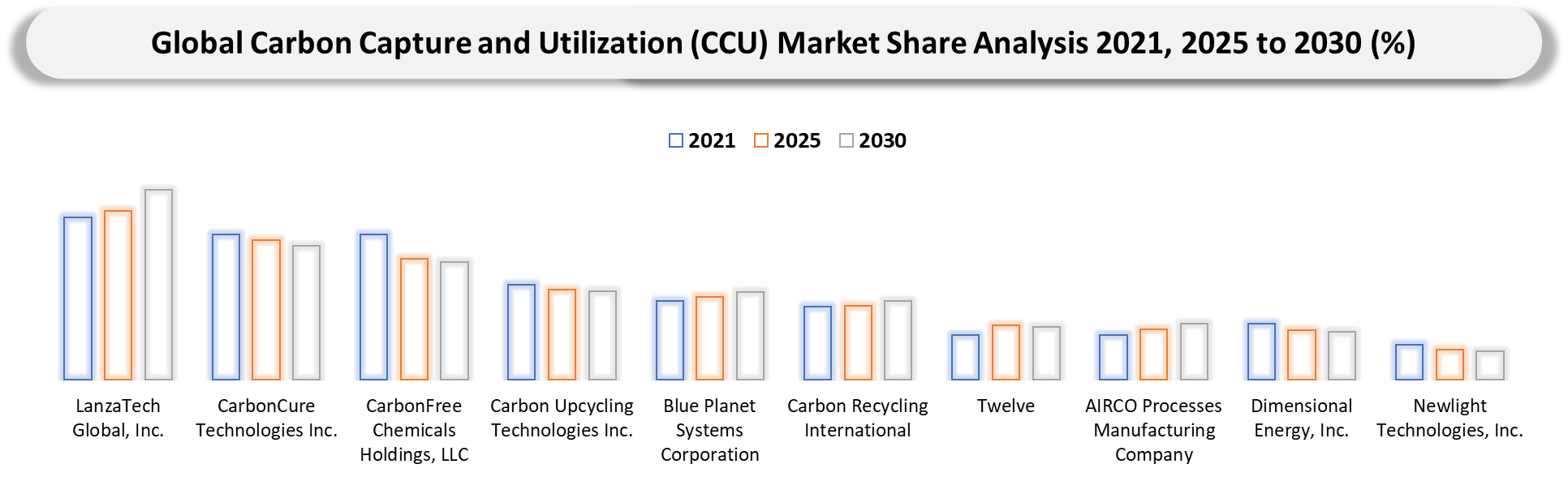

The growth in CCU in Canada is steady due to the robust incentives put forward by the government, clustering and carbon pricing mechanisms. Canada has adopted an Investment Tax Credit that covers up to 60 percent of capital investment cost on CCU and CCS projects while there is a carbon price target of CAD 170 per ton in 2030, promoting utilization economics. The center of the activities is Alberta, which has projects such as Alberta Carbon Trunk Line where captured CO₂ is utilized for enhanced oil recovery and developing new products such as carbon fuels and materials. From the Canadian Natural Resources Canada report, there have been investments by the federal government worth CAD 2.6 billion on carbon capture, utilization and storage technologies from 2021. CarbonCure Technologies has already been commercializing the use of CO₂ mineralization technology for use in concrete. It is used in more than hundred production facilities worldwide. Canada's CCU sector is supported by the collaboration between industry bodies and research institutions such as Canada Energy Regulator.

Competitive Landscape

- The global CCU market features a mix of energy majors, industrial technology providers and innovative startups focused on carbon conversion technologies.

- Key players include Carbon Clean, LanzaTech, CarbonCure Technologies, Climeworks, BASF and Shell plc.

- Companies are competing through proprietary catalysts, carbon conversion efficiency and integration with renewable energy systems.

- Strategic collaborations between energy firms, chemical manufacturers and governments are accelerating commercialization of CO₂-derived products.

- Increasing investments in R&D, particularly in electrochemical conversion and synthetic fuel production, are expected to define the next phase of CCU market evolution.

Key Developments

- April 2026: MCi Carbon Pty Ltd advanced mineral carbonation process converting industrial wastes and CO₂ into construction materials, targeting gigaton-scale carbon utilization potential.

- March 2026: CarbonBuilt, Inc., deployed low-carbon concrete technology utilizing CO₂ mineralization curing, reducing cement usage and emissions in commercial building projects.

- February 2026: CarbiCrete Inc. scaled cement-free concrete manufacturing using captured CO₂ curing, targeting industrial adoption across North American precast concrete markets.

- February 2026: Carbon Upcycling Technologies Inc. accelerated commercialization of CO₂-based cement additives, enhancing material performance while reducing lifecycle emissions in construction sector applications.

- January 2026: O.C.O Technology expanded Accelerated Carbonation Technology for waste-derived aggregates, increasing CO₂ sequestration capacity in infrastructure and construction materials.

- November 2025: Econic Technologies Limited advanced commercialization of CO₂-based polyols for polyurethane manufacturing, enabling reduced fossil feedstock dependence in industrial polymer production.

- October 2025: Newlight Technologies, Inc. increased production of AirCarbon biopolymers derived from captured carbon emissions, expanding partnerships with packaging and consumer goods companies.

September 2025: Dimensional Energy, Inc. demonstrated commercial-scale Fischer-Tropsch systems converting CO₂ into synthetic hydrocarbons, enhancing sustainable aviation fuel supply chains.

Why Choose DataM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

Target Audience

- Energy & Power Generation Companies: Utilities, independent power producers and grid operators deploying CCU technologies to decarbonize fossil fuel-based generation assets.

- Oil & Gas Industry Players: Upstream, midstream and downstream companies integrating CCU for enhanced oil recovery (EOR) and emissions reduction strategies.

- Industrial Manufacturers: Cement, steel, chemicals and refining industries adopting CCU solutions to capture and reuse CO₂ from high-emission processes.

- Technology Providers & Engineering Firms: CCU technology developers, EPC contractors and process engineering companies offering capture, conversion and utilization solutions.

- Government & Regulatory Authorities: Environmental agencies, climate policy makers and public sector bodies driving carbon reduction mandates, incentives and funding programs.

- Investors & Private Equity Firms: Venture capitalists and institutional investors targeting low-carbon technologies, carbon markets and sustainable industrial innovations.

- Research Institutions & Academia: Universities, R&D centers and innovation hubs advancing CCU materials, processes and commercialization pathways.

- Carbon Offtake & End-Use Industries: Companies utilizing captured CO₂ in applications such as synthetic fuels, chemicals, building materials and food & beverage industries.

- Infrastructure & Transport Stakeholders: Pipeline operators, storage developers and logistics providers enabling CO₂ transport, utilization and storage networks.

- Environmental & Sustainability Organizations: NGOs and international bodies advocating for carbon neutrality, emissions reduction and large-scale CCU deployment.