Carbon Capture, Utilization, and Storage (CCUS) Testing Market Overview

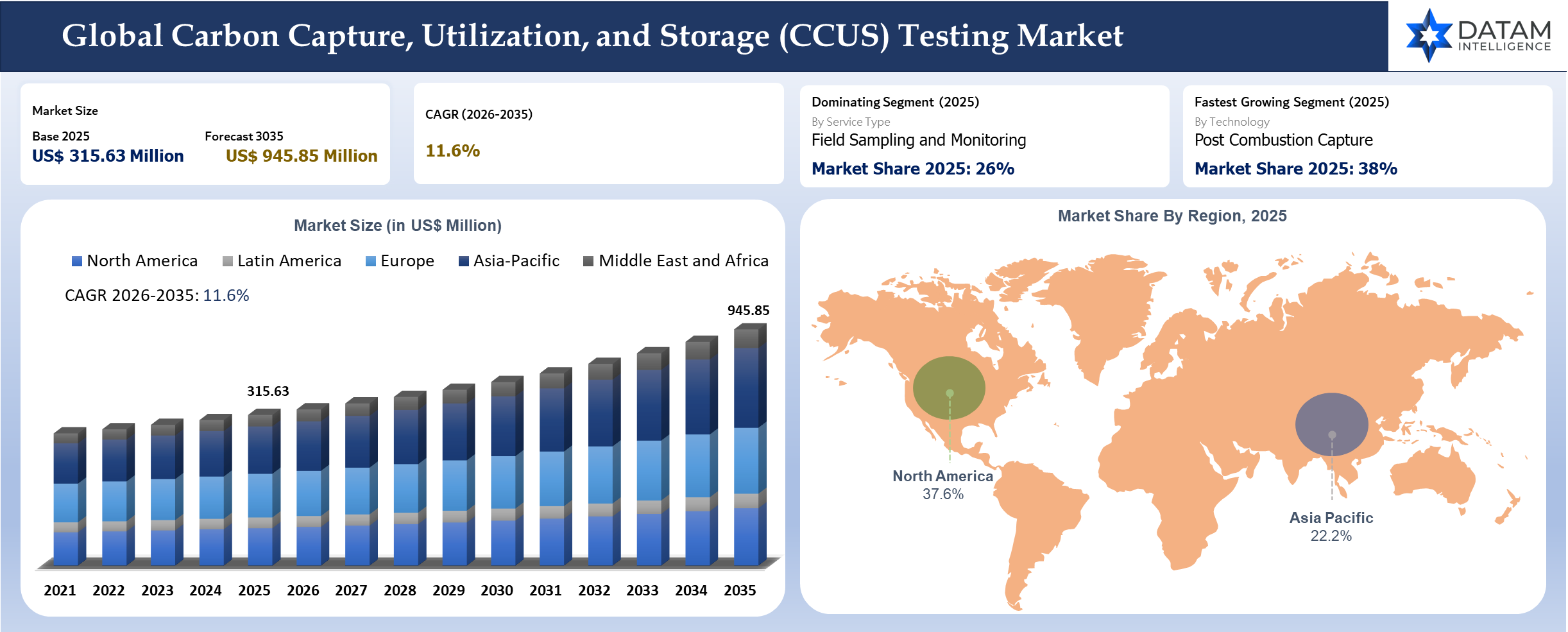

The global carbon capture, utilization and storage (CCUS) testing market reached US$ 315.63 million in 2025 and is expected to reach US$ 945.85 million by 2035, growing with a CAGR of 11.6% during the forecast period 2026-2035. Increasing efforts from organizations and government institutions in the direction of decarbonization to achieve climate goals set is supporting the market. As the number of large-scale CCUS projects is growing fast, it is becoming increasingly important to provide efficient testing solutions such as carbon dioxide capture effectiveness testing, material integrity, leakage detection, and monitoring and verification (MMV). Testing is important in terms of pipeline and geological storage safety and reliability amid increasing environmental regulations implemented by government bodies.

Governments and regulatory bodies are playing a crucial role in shaping the CCUS testing market through policy frameworks, funding initiatives and international collaborations. For instance, the European Commission has introduced the Net-Zero Industry Act and supports cross-border CO₂ transport and storage projects, necessitating standardized testing and certification protocols across Europe.

Carbon Capture, Utilization and Storage (CCUS) Testing Industry Trends and Strategic Insights

- Field Sampling and Monitoring is the most commercially important segment because it aligns with current buying behavior, installed base requirements and near term scaling feasibility.

- Vendors that combine product depth, application support and faster commercialization pathways are best positioned to defend share.

Carbon Capture, Utilization and Storage Testing Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 315.63 Million | |

| 2035 Projected Market Size | US$ 945.85 Million | |

| CAGR (2026-2035) | 11.6% | |

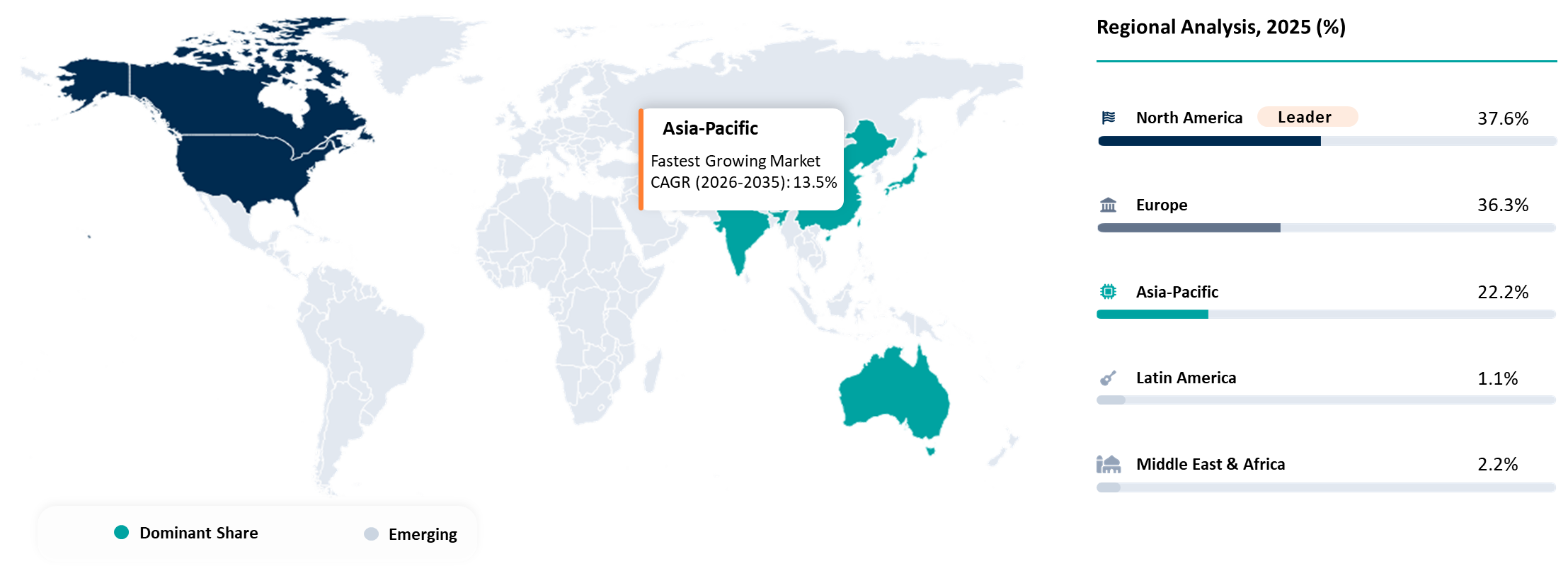

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Service | Laboratory Testing, Pilot Plant Testing, Field Sampling and Monitoring, Material Qualification, Leak Detection and Integrity Testing | |

| By Testing Phase | Pre FEED and Feasibility, Pilot and Demonstration, Construction and Commissioning, Operational Monitoring, Post Closure Monitoring | |

| By Technology | Post Combustion Capture, Pre Combustion Capture, Oxy Fuel Combustion, Direct Air Capture, Carbon Mineralization and Utilization | |

| By Test Focus | Solvent and Sorbent Performance, CO2 Stream Quality, Pipeline and, Materials Compatibility, Reservoir Characterization, MRV and Leak Monitoring | |

| By End-User | Oil and Gas, Power Generation, Cement, Chemicals and Refining, Steel and Other Hard to Abate Industries | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Disruption Analysis

The greatest threat to CCUS testing products development does not lie in any particular innovation, but rather in the evolution of how value is measured. Increasingly, customers seek out offerings that deliver tangible value through improvements in metrics such as uptime, compliance, efficiency, reach, longevity, effectiveness, productivity or total cost of ownership. It creates an increased challenge for players who previously only competed on technical specifications.

A convergence of hardware, materials, software, analysis, services and compliance necessitates more integration and collaboration between providers. It also means higher switching costs once the vendor is deeply entrenched within the customer's workflow. The end result is that past-generation broad-line product lines risk being made irrelevant unless they are supplemented with innovative solutions. However, newcomers may succeed provided they address a clearer problem, enter via a smaller niche or rely on a quicker time-to-market.

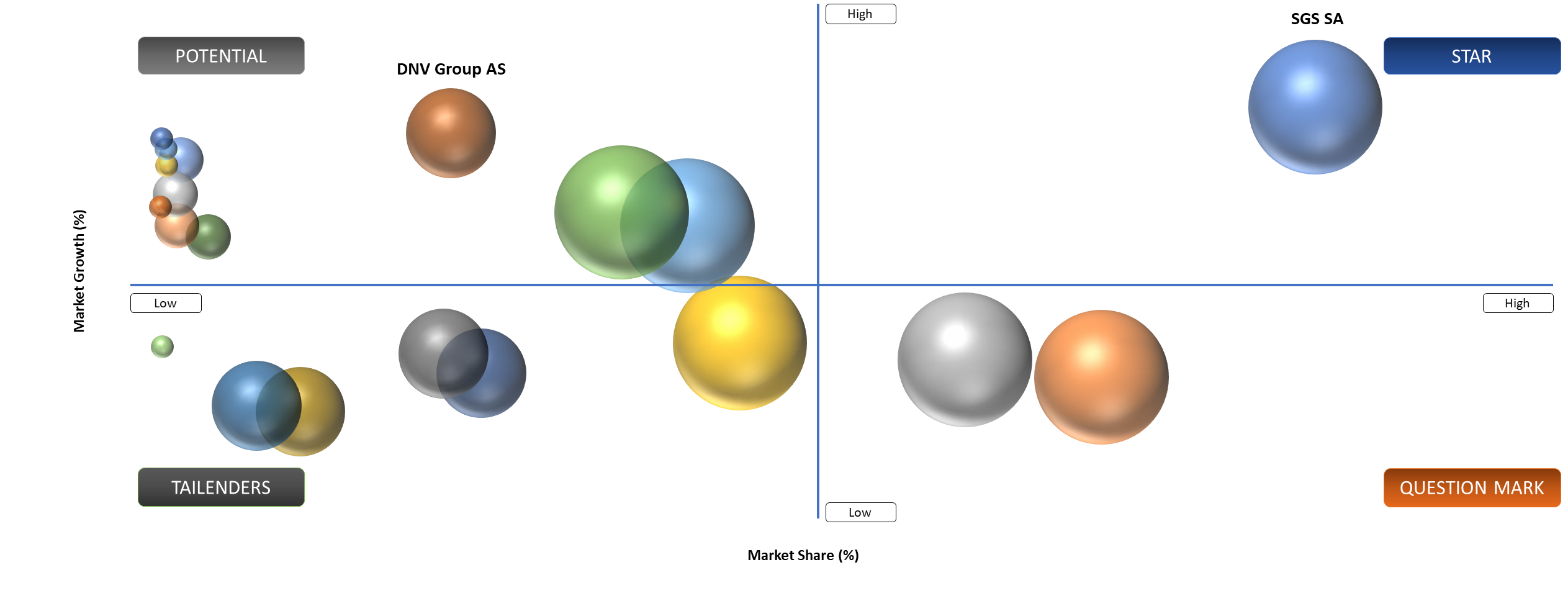

BCG Matrix: Company Evaluation

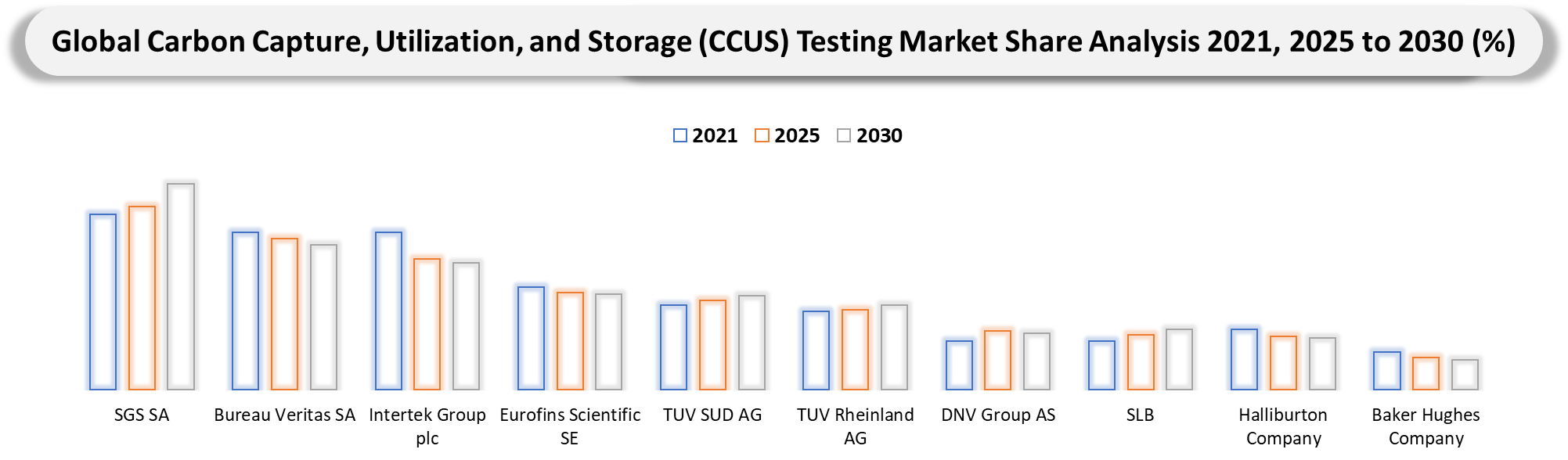

In BCG terms, the most likely Stars in the carbon capture, utilization and storage (CCUS) testing market are vendors that combine visible revenue momentum with a strong technology or channel position. In most cases, the lead group includes SGS SA, Bureau Veritas SA and Intertek Group plc because these companies influence product standards, customer qualification cycles and investment direction.

Market Dynamics

Rapid increase in FEED, pilot and early commercial CCUS projects that need bankable testing and monitoring data

Buyers increasingly want solutions that can be justified not only on technical fit, but also on payback, reliability and execution speed. It makes the driver commercially meaningful because it influences both first-time adoption and repeat purchase behavior. The improvement in market sizing feasibility links directly to measurable demand pools such as installed equipment, fleet renewal, production capacity, testing volumes, crop area, subscriber base or project pipelines, depending on the market.

On the supply side, the driver rewards vendors that can standardize what should be standardized while still allowing enough application-specific customization. Companies protect margins, shorten sales cycles and create more scalable channel strategies. Over the medium term, the strength of this driver should support both premium and volume segments. Premium tiers benefit from performance differentiation, while volume tiers benefit from wider adoption and replacement demand. The balance is one reason the market remains attractive even as competition intensifies.

Project delays caused by uncertain economics and slow permitting

Project are getting delayed due to uncertain economics and slow permitting. Even where demand is present, this issue can delay qualification, limit addressable volume or compress willingness to pay. In practical terms, it affects how quickly suppliers can convert interest into repeat orders.

The restraint is especially relevant for client specific sizing because it narrows which subsegments are immediately feasible to quantify. Markets with fragmented standards, uncertain regulation or limited infrastructure often show strong headline potential but weaker short term commercialization depth. It means the best sizing models need to prioritize segments where spending intent is visible and execution barriers are lower. Suppliers that address this restraint through application engineering, local partnerships, compliance support or operating cost reductions should outperform peers.

Segmentation Analysis

The global carbon capture, utilization, and storage (CCUS) testing market is segmented based on the service, testing phase, technology, test focus, end user and region.

Testing Service Determines How CCUS Projects Actually Reach Bankability

Service is the most commercially useful way to interpret this market, and laboratory testing and field and pilot testing are the two sub-segments that best explain where current demand and future monetization are concentrating. Service is the most useful way to read the CCUS testing market because the value of testing changes across the project lifecycle. Laboratory testing helps screen materials, solvents, membranes, and process behavior early, while field and pilot testing determine whether a project can withstand investor, regulator and offtake scrutiny.

CCUS developers are moving away from slide deck stage optimism. Performance verification, impurity handling, corrosion behavior, monitoring protocols and site-specific risk modeling are becoming harder commercial gates, which is why both laboratory and pilot testing have moved closer to the center of project decision making.

Geographical Penetration

North America Carbon Capture, Utilization and Storage (CCUS) Testing Market Landscape

North America leads the CCUS testing market because the region combines project pipelines, public incentives and a mature engineering ecosystem. The volume of proposed projects has pushed testing from a technical support function into a major commercial screening tool.

The region is also where monitoring and verification standards are being scrutinized most closely. As projects move toward investment decisions, testing around storage integrity, impurity handling and measurement quality is becoming indispensable. A defining regional issue is project realism. Developers can no longer rely on generic capture assumptions or broad policy enthusiasm; they need data that stands up under financing, permitting and operational review.

USA Carbon Capture, Utilization and Storage (CCUS) Testing Market Outlook

The USA is the primary market because incentives have created a large project funnel, but that funnel is exposing execution bottlenecks. Testing demand is rising precisely because developers need to de risk capture systems, transport quality and storage plans before capital is committed. Permitting and Class VI storage questions are pushing the market toward stronger evidence packages. Laboratory and pilot work is increasingly being used to support site-specific claims around injectivity, containment and monitoring design. USA is also witnessing a shift from showcase projects to portfolio discipline. Buyers want test programs that help them choose which projects deserve full development rather than simply prove that technology can work under ideal conditions.

Canada Carbon Capture, Utilization and Storage (CCUS) Testing Market Trends

Canada is highly relevant because provincial carbon hub development and industrial decarbonization strategies are creating a strong need for technically credible testing. Alberta continues to anchor much of the commercial interest. The market is notable for its emphasis on integrated project design. Capture, transport and storage cannot be treated as separate boxes, so testing programs increasingly need to address the chain rather than isolated equipment performance. Canada benefits from strong resource and process industry exposure. Oil and gas, power, fertilizer and industrial clusters create a practical environment where testing needs are tied directly to project execution rather than theoretical deployment.

Competitive Landscape

- The competitive landscape is led by a mix of global leaders and focused specialists, with SGS SA, Bureau Veritas SA, Intertek Group plc and Eurofins Scientific SE shaping category standards. Market positioning depends on portfolio breadth, application depth, route to market strength and the ability to support customers after the initial sale.

- The strongest companies are using product upgrades, partnerships, regional manufacturing and selective vertical focus to defend share. As the market matures, leadership is likely to concentrate further around suppliers that can translate technical capability into faster commercialization and stronger customer retention.

Key Developments

- April 2026: INX International Ink Co. advanced low-energy curing ink technologies, reducing emissions intensity, contributing to broader industrial decarbonization and testing alignment.

- March 2026: DIC Corporation expanded sustainable ink R&D programs targeting lower lifecycle emissions, supporting carbon footprint reduction aligned with global decarbonization initiatives.

- February 2026: ACTEGA GmbH expanded its sustainable coatings portfolio, enabling reduced emissions packaging, supporting lifecycle carbon testing and validation frameworks.

- March 2026: Toyo Ink SC Holdings increased investment in carbon-neutral technologies and lifecycle analysis tools, supporting emission quantification and testing ecosystems.

- January 2026: Sun Chemical announced increased investment in eco-efficient formulations, reducing VOC emissions, indirectly supporting carbon measurement and sustainability testing frameworks.

- October 2025: Van Son Ink Corporation strengthened sustainable product portfolio targeting reduced emissions and compliance with environmental testing standards.

- June 2025: Siegwerk Druckfarben AG & Co. KGaA launched circular economy initiatives targeting carbon footprint transparency, supporting downstream testing and validation of sustainable packaging solutions.

- May 2025: T&K TOKA Corporation expanded eco-friendly ink portfolio supporting reduced carbon emissions, aligning with regulatory testing requirements for sustainable materials.

- February 2025: Flint group strengthened sustainability roadmap focusing on low-carbon packaging inks, enhancing compatibility with environmental compliance and emissions testing requirements.

Why Choose DataM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

Target Audience

- Energy & Power Generation Companies: Utilities, independent power producers and operators of fossil fuel plants deploying CCUS testing solutions to evaluate capture efficiency, emissions reduction and system integration feasibility.

- Oil & Gas Companies: Upstream, midstream and downstream players assessing CCUS technologies for enhanced oil recovery (EOR), carbon sequestration validation and compliance with decarbonization targets.

- Industrial Manufacturers: Cement, steel, chemicals and refining industries conducting pilot-scale and full-scale CCUS testing to reduce process emissions and meet regulatory requirements.

- Technology Providers & Engineering Firms: EPC contractors, technology developers and engineering consultants involved in designing, testing and optimizing carbon capture systems and storage infrastructure.

- Government & Regulatory Authorities: Environmental agencies, policy makers and climate-focused institutions overseeing emissions monitoring, regulatory compliance and funding of CCUS pilot and demonstration projects.

- Research Institutions & Academia: Universities, laboratories and research organizations engaged in innovation, performance testing and validation of next-generation carbon capture and utilization technologies.

- Investors & Private Equity Firms: Financial institutions and climate-focused funds evaluating CCUS testing projects, pilot outcomes and scalability potential for long-term investments.

- Storage & Infrastructure Developers: Companies specializing in CO₂ transport, pipeline infrastructure and geological storage (saline aquifers, depleted reservoirs) requiring testing for safety, leakage and long-term viability.

- Environmental & Sustainability Consultants: Advisory firms supporting lifecycle analysis, carbon accounting and ESG compliance through validated CCUS testing frameworks and reporting standards.