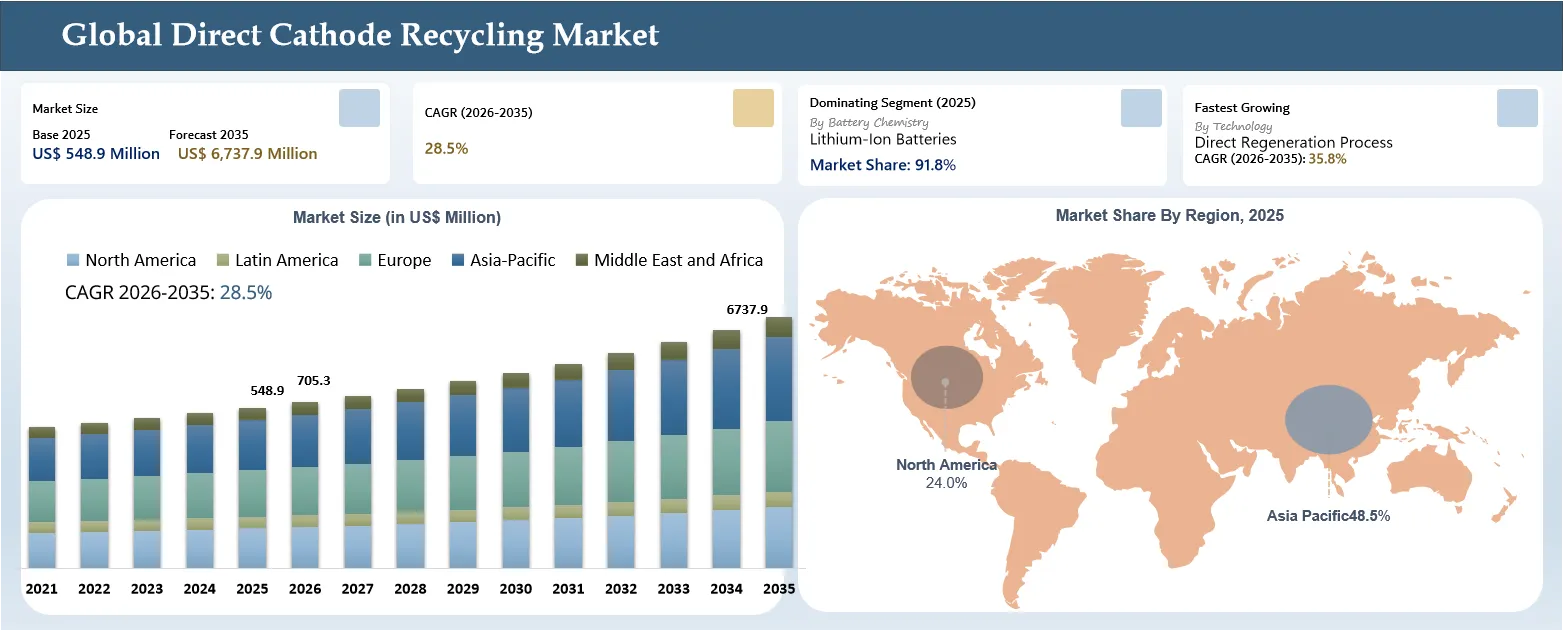

Direct Cathode Recycling Market Size & Forecast

The global Direct Cathode Recycling market reached USD 548.9 million in 2025 and is expected to reach USD 6,737.9 million by 2035, growing with a CAGR of 28.5% during the forecast period 2026-2035, due to the growing demand for recycling of batteries owing to the increasing requirement for closed-loop battery material recovery systems that facilitate the regeneration of cathode active materials without any alteration in their physical and chemical nature. Direct cathode recycling systems are becoming more popular as manufacturers and automakers are looking for alternatives to traditional recycling methods, which entail the disintegration of the battery material and high energy consumption.

Increasing use of electric cars, growth in production capacities for lithium-ion batteries, and the issues associated with critical minerals like lithium, nickel, cobalt, and manganese are driving the popularity of direct recycling systems. This technology facilitates the extraction of highly valued cathode materials such as NMC, LFP, and LCO via relithiation, thermal restoration, and surface regeneration to directly utilize them in battery manufacture. Redwood Materials, Ascend Elements, and Li-Cycle are among the companies contributing to the improvement of recycling abilities for the sustainable battery supply chain. However, technology scalability, feedstock consistency, process standardization, and compatibility with the current battery manufacturing ecosystem are some of the crucial aspects influencing the market development.

Direct Cathode Recycling Market Overview

Key Takeaways

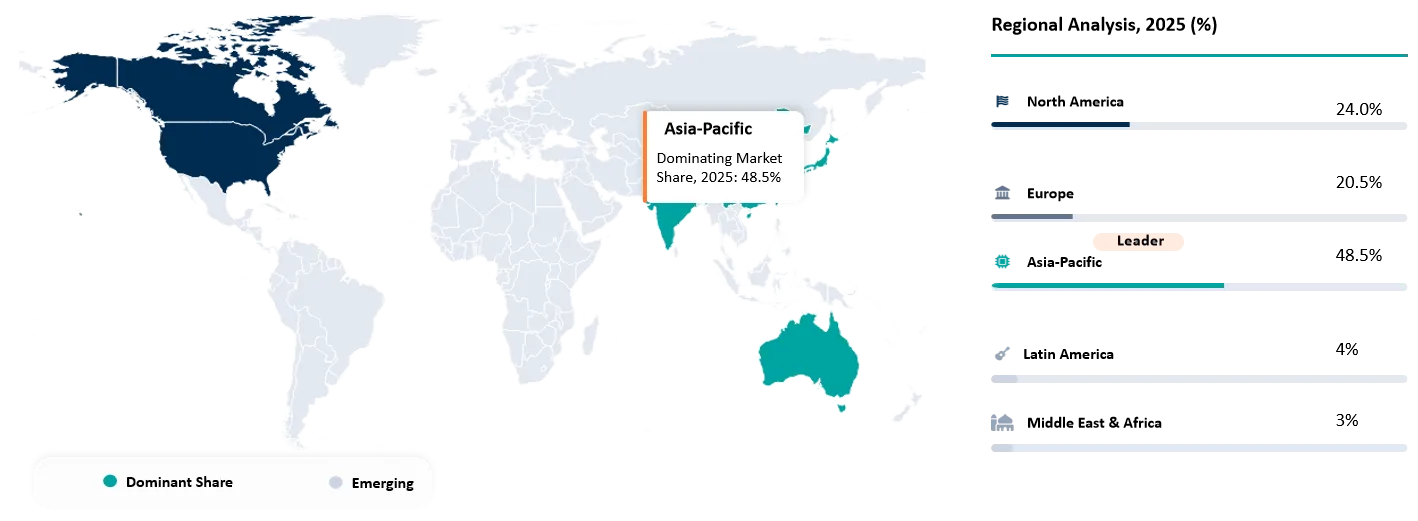

- Asia Pacific region carved out its position as the world's dominant region, due to its capture of 48.5% market share in 2025. This huge share comes from the region’s high-quality manufacturing centers and recycling facilities.

- Lithium-ion batteries enjoyed unchallenged domination over the segment that deals with battery chemistry within the market in 2025. The particular segment was responsible for an astonishingly high market share of 91.8%.

- In addition, China is the dominant player for activities in the region and represents an 85% market share of cathode active material globally. Additionally, the country is expected to hold 58.4% of the entire Asia Pacific market share in 2025.

- Insecurities in the supply of and price volatility in critical minerals used in batteries has the highest growth impact potential at 31%, while scaling of gigafactories globally with their high-quality manufacturing scrap adds a growth impact of 27%.

Direct Cathode Recycling Market Industry Trends and Strategic Insigh

- The battery recycling sector is shifting from high-energy-consuming hydrometallurgy and pyrometallurgy methods toward direct cathode recovery using relithiation, defect engineering, and surface reconstruction techniques to sustain the active materials' structures.

- Recycling strategies are increasingly becoming customized for distinct cathode materials – NMC, LCO, and LFP - with direct recycling processes already having been improved to address the problems of lithium depletion, phase change, and fracturing.

- The rising adoption of LFP batteries in both electric vehicles and energy storage systems has increased the need for innovative techniques in direct recycling that are not focused on extracting just nickel and cobalt but instead can efficiently regenerate the lithium in aged cathodes.

- Battery recyclers are integrating AI, machine learning, and automation into their processes, along with characterization techniques such as electron microscopy and spectroscopy, to allow data-driven process control through accurate degradation assessment and regeneration optimization to yield manufacturing-quality cathodes.

- Regulatory mandates on recycled content, traceability, and lifecycle management with battery passports and carbon reporting are driving the adoption of direct cathode recycling by forcing manufacturers to incorporate recycled material into their manufacturing processes and keep track of their supply chains.

Direct Cathode Recycling Market Scope

| Metrics | Details | |

| 2025 Market Size | USD 548.9 Million | |

| 2035 Projected Market Size | USD 6737.9 Million | |

| CAGR (2026-2035) | 28.5% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | North America | |

| By Battery Chemistry | Lithium-Ion Batteries, Nickel-Metal Hydride (NiMH) Batteries, Lead-Acid Batteries, Others | |

| By Technology | Direct Regeneration Process, Hydrometallurgical Process, Pyrometallurgical Process, Mechanical Recycling Process, Others | |

| By Battery Source | Electric Vehicle (EV) Batteries, Battery Manufacturing Scrap, Consumer Electronics Batteries, Industrial Batteries | |

| By Application | Automotive, Consumer Electronics, Energy Storage Systems (ESS), Industrial Applications, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Direct Cathode Recycling Market Disruption Analysis

Variability in Battery Feedstock Availability and Composition Disrupting Direct Cathode Recycling Standardization

Disruption in the Direct Cathode Recycling Market comes mainly from the rising complexities in the variety of lithium-ion battery chemistries that go into the recycling process. The rapid increase in the use of various kinds of cathode types, such as NMC, LFP, LCO, and NCA, is posing challenges for recycling companies in developing processes that can produce consistent battery-grade materials. The movement towards diversified battery architecture has been leading to disturbances in standard recycling procedures due to the impacts of variations in cathode composition, electrode architecture, cell structure, and degradation on material recovery effectiveness and regeneration needs. LFP batteries have been gaining popularity because of their reduced cost and enhanced safety features, but they have less valuable metals than NMC batteries and thus need special methods for direct regeneration in order to make the process economically feasible. The U.S. Department of Energy emphasizes that battery chemistry and design remain key challenges for designing scalable recycling systems.

Since most EV batteries are still operating within the first cycle of operation, recyclers have been counting on battery production scraps as raw materials since they provide a clean and reliable source of materials, but do not completely meet the future recycling demands. According to the International Renewable Energy Agency, it estimates that significant amounts of decommissioned EV batteries will be entering the recycling stream after 2030.

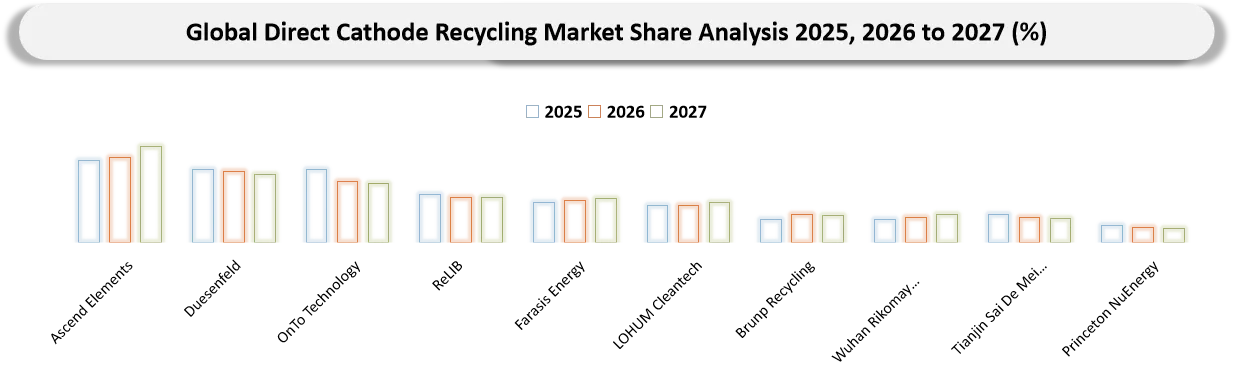

Direct Cathode Recycling Market BCG Matrix: Company Evaluation

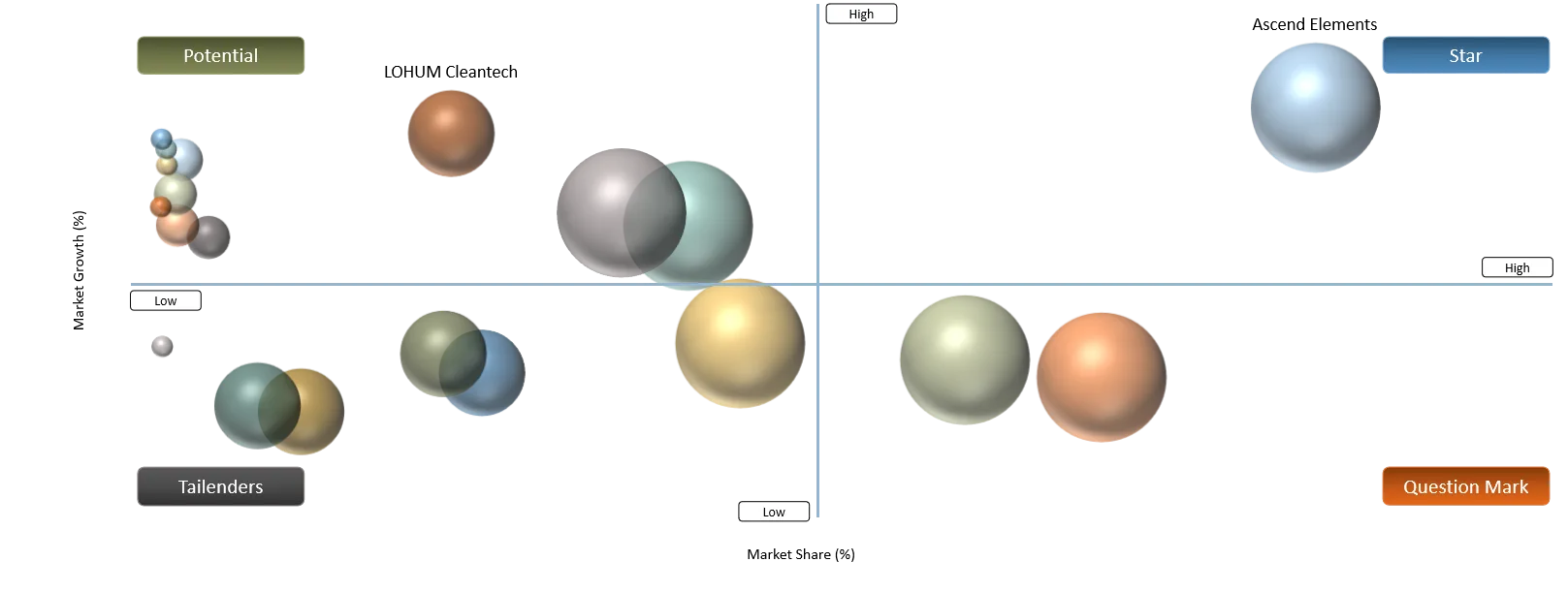

Stars include Ascend Elements and Farasis Energy because of their technological strength, strategic alliances, and increasing presence in the closed-loop battery ecosystem. Ascend Elements has cathode regeneration technology through its Hydro-to-CathodeTM technology, which allows the company to produce recycled cathode active materials for the manufacture of lithium-ion batteries. Farasis Energy has gained strength in its role as a battery manufacturer, focusing increasingly on the battery lifecycle. Question Marks include OnTo Technology, Princeton NuEnergy, and Wuhan Rikomay New Energy Co., Ltd. The reason behind classifying these firms as Question Marks is that, despite having differentiated direct recycling technology, these companies are still working on the process of achieving large-scale commercialization. OnTo Technology and Princeton NuEnergy are using cathode rejuvenation and plasma-assisted direct recycling techniques, respectively, whereas Wuhan Rikomay can regenerate batteries directly, especially LFP cathodes.

Potential group includes LOHUM Cleantech, Tianjin Sai De Mei New Energy Technology Co., Ltd., and Brunp Recycling. These firms are working on recovering and regenerating battery materials and thus have an advantage due to the increasing demand for lithium-ion battery recycling facilities. Tailenders include Duesenfeld and ReLIB, which are classified as Tailenders because of their relatively smaller market presence when it comes to the direct cathode recycling business. Duesenfeld is highly knowledgeable about green lithium-ion battery recycling but is more oriented towards recycling processes as opposed to the cathode recycling business.

Direct Cathode Recycling Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Increasing uneasiness regarding the accessibility and volatile prices of certain critical minerals for batteries, is motivating industries to implement direct recycling of cathode active materials. | 31% | High in EV batteries, battery cell manufacturing, and cathode material production | Electric vehicles (EVs), stationary energy storage systems (ESS), battery material refining | Reduces dependence on virgin lithium, nickel, cobalt, and manganese while improving supply-chain resilience and raw material security. |

The ability to retain the material value effectively helps improve the recycling economics. As opposed to hydrometallurgy and pyrometallurgy, direct cathode recycling maintains the crystal structure of cathode active material and avoids degradation. | 26% | High in NMC, LFP, and LCO cathode regeneration | Cathode active material (CAM) manufacturing, battery remanufacturing, closed-loop battery production | Enhances recovery value, lowers energy consumption, and enables production of battery-grade recycled cathode materials with lower processing costs. |

Innovations that continue to take place in relithiation, crystalline structure recovery, surface engineering, and defect correction bring regenerated cathodes closer to their virgin performance level. | 22% | Medium to High in advanced battery R&D, premium EV batteries, and next-generation battery production | High-performance EV batteries, premium energy storage systems, advanced lithium-ion cell manufacturing | Accelerates commercialization of direct cathode recycling by improving electrochemical performance, cycle life, and industry acceptance of regenerated cathode materials. |

Growth in battery gigafactories worldwide is producing larger quantities of high-grade manufacturing scrap that forms a reliable and clean source of material for direct cathode recycling. | 27% | Very High in battery gigafactories and integrated cell manufacturing facilities | Battery manufacturing scrap recycling, cathode precursor production, closed-loop manufacturing ecosystems | Ensures a stable supply of high-purity feedstock, improves recycling efficiency, reduces processing complexity, and strengthens localized circular battery supply chains. |

Growth in battery gigafactories worldwide is producing larger quantities of high-grade manufacturing scrap that forms a reliable and clean source of material for direct cathode recycling

The fast growth of lithium-ion battery gigafactories will be the key catalyst for the growth of the Direct Cathode Recycling market because increased production provides large amounts of high-quality manufacturing scraps that can be used to recycle the cathodes. Unlike end-of-life batteries, manufacturing scraps include uninstalled electrode coatings, non-conforming batteries, and residuals from the cathode manufacturing process, which have little contamination and can be used in the recycling process. According to the International Energy Agency, the total lithium-ion battery manufacturing capacity worldwide grew above 4 TWh in 2025, which is about 30% higher than in 2024, while the manufacturing capacity in the US and EU grew by 50% year over year. According to the International Energy Agency, the global battery manufacturing capacity surpassed 3 TWh in 2024 and will grow to reach about 6.5 TWh from planned projects in 2030, whereby the share of China's manufacturing capacity globally stood at 85% in 2024. Modern gigafactories with a capacity of 50 GWh can produce as many as 10 million battery cells per day in a cylindrical form and therefore, are expected to produce considerable amounts of scrap during electrode coating, cell assembly, and quality control processes.

This type of by-product from the battery manufacturing process is an excellent source of cathode materials and can benefit direct cathode recyclers through higher efficiency, reduced costs, and faster commercialization of a closed-loop battery manufacturing ecosystem. For example, in October 2025, the Electrochemical Society (ECS) Meeting Abstracts published a study that emphasized the fact that the fast growth of manufacturing processes of lithium-ion batteries is leading to the creation of huge quantities of high-quality manufacturing scrap. The article also stressed the importance of using such minimally degraded material as a feedstock for the direct recycling of cathodes, which will allow the reuse of cathode material.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

An increasing number of chemistries for lithium-ion batteries, in addition to differences in cell designs, makes it more challenging to implement direct recycling. | 21% | Process standardization, feedstock sorting, and cathode regeneration efficiency

| Multi-chemistry EV battery recycling (NMC, LFP, NCA, LCO), battery manufacturing scrap | Increases operational complexity, requires chemistry-specific recycling workflows, and slows commercialization of universal direct cathode recycling platforms. |

The lack of uniform industry standards for cathode recycling processes, as well as the lack of quality standards for recycled cathode materials, makes the whole process quite problematic for battery companies. | 18% | Material qualification, certification, and quality assurance | Battery-grade cathode active material (CAM) production, EV battery manufacturing | Delays industry adoption due to lengthy qualification cycles and creates uncertainty regarding acceptance of regenerated cathode materials by cell manufacturers. |

Hydrometallurgical recycling, which has more widespread industrial use and existing processes already in place, poses a significant challenge for the competitiveness of direct cathode recycling. | 20% | Technology adoption and commercial competitiveness | Industrial battery recycling, critical mineral recovery, closed-loop battery supply chains | Reduces the pace of direct recycling deployment as established hydrometallurgical infrastructure, proven recovery routes, and existing investments continue to dominate commercial battery recycling. |

Battery producers have to implement major changes in the procedures related to procurement, quality assurance, and the manufacturing process of cathode materials for these processes to be able to include the regenerated cathodes. | 17% | Manufacturing integration and supply chain validation | Gigafactories, cathode manufacturing plants, lithium-ion cell production | Requires process requalification, procurement restructuring, and manufacturing line validation, increasing implementation costs and extending commercialization timelines for regenerated cathode materials. |

An increasing number of chemistries for lithium-ion batteries, in addition to differences in cell designs, makes it more challenging to implement direct recycling

One of the key constraints affecting the development of Direct Cathode Recycling technology is the increasing heterogeneity of lithium-ion battery chemistry and design in different application areas, such as passenger cars, consumer electronics, and energy storage applications. While traditional recycling approaches focus on metal recovery, DCR necessitates cathode regrowth and the recreation of the original cathode crystal structure; thus, chemistry-specific processes should be used. In turn, the fast changeover to several types of cathode chemistries, including LFP, NMC, NCA, and other new battery technologies, complicates the process significantly. According to the IEA Global EV Outlook 2026, LFP batteries made up more than 55% of total global EV battery deployments in 2025, while the share of nickel-based cathode chemistries (NMC/NCA) was around 80% in EVs outside China.

For example, in 2025, Nature Reviews Clean Technology, pointed out that the expanding chemical variety of lithium-ion batteries as well as varying battery cell designs contribute to the growing difficulty of direct recycling. According to the publication, due to such factors, specific chemistry-based methods have to be used to conduct recycling, thus making direct recycling more complicated in terms of feedstock sorting and cathode regeneration.

Direct Cathode Recycling Market Segment Analysis

The global Direct Cathode Recycling market is segmented based on battery chemistry, technology, battery source, application, and region.

Lithium-Ion Batteries Dominate Battery Chemistry Segment Due to Expanding Electric Vehicle and Energy Storage Deployment

The Lithium-Ion Batteries were the largest contributor to the Direct Cathode Recycling Market in terms of market share and held an estimated market share of 91.8% in the year 2025. This segment is dominant due to the increasing adoption of lithium-ion batteries in electric vehicles (EVs), stationary energy storage systems (ESS), and consumer electronics that account for the highest quantity of batteries used in battery manufacturing and are expected to become end-of-life batteries, ideal for direct cathode recycling. The increasing popularity of high-cost cathode chemistries, including NMC, LFP, LCO, and NCA, has been boosting the adoption of direct recycling processes to recycle cathode crystal structures along with battery-grade active materials instead of the recovery of only elemental metals. As per the IEA – Global EV Outlook 2026, the global battery demand crossed 950 GWh in the year 2025, while the global lithium-ion battery manufacturing capacity touched 4 TWh.

At the same time, it should be noted that the study of direct recycling in Nature Reviews Materials (2025) emphasizes the point that lithium-ion batteries are still the main chemistry segment in terms of which cathode regeneration techniques are developed due to the fact that the retention of cathode active materials requires less energy and fewer critical minerals than traditional hydrometallurgical recycling processes. With the development of production systems that include cathodes, recycled batteries will continue to dominate the market.

Direct Cathode Recycling Market Geographical Penetration

Asia-Pacific Dominates the Direct Cathode Recycling Market Through Battery Manufacturing Leadership and Integrated Recycling Infrastructure

The Asia-Pacific region continues to be the leading region within the Direct Cathode Recycling Market because of its unmatched lithium-ion battery manufacturing system, vertical integration of battery value chains, and heavy investments into battery recycling facilities. The Asia-Pacific region represented about 48.5% of the Global Direct Cathode Recycling Market in 2025, which was mainly due to China, Japan, and South Korea being home to the largest battery manufacturers, cathode material makers, and recyclers in the world.

For instance, in March 2025, Panasonic Energy, a Japan-based company, introduced Japan's first closed-loop battery-to-battery recycling system for lithium-ion batteries used in automobiles in collaboration with Sumitomo Metal Mining. The system uses nickel extracted from battery production scraps produced by Panasonic Energy’s factory in Osaka to be recycled back and used as cathode material in new lithium-ion batteries.

China Direct Cathode Recycling Market Trends

The leading player in the Asia-Pacific Direct Cathode Recycling Market is China, owing to its huge base of lithium-ion battery manufacturing, an integrated battery material supply chain, and established battery recycling facilities. It is predicted that China will contribute approximately 58.4% of the Asia-Pacific Direct Cathode Recycling Market share in 2025. It includes the presence of major battery manufacturers, cathode material manufacturers, and recyclers, such as CATL, GEM, Brunp Recycling, and Ganfeng Lithium. As per IEA – Global EV Outlook 2026, in 2025, China accounted for over 80% of global lithium-ion battery manufacturing capacity, as well as 85% of cathode active material production, and generated a steady stream of high-quality battery manufacturing waste as the preferred feedstock for direct cathode recycling. This battery value chain in the country greatly boosts the adoption of cathode regeneration technologies and leadership in closed-loop battery manufacturing.

For instance, in September 2025, GEM Co., Ltd., a China-based company that specializes in battery recycling and the production of cathode materials, partnered with Ascend Elements to create a local lithium-ion battery recycling and engineered battery materials value chain in Europe. This partnership will help recover essential metals from spent batteries and production scrap and transform them into lithium carbonate, lithium hydroxide, precursor cathode active material (pCAM), and cathode active material (CAM).

India Direct Cathode Recycling Market Outlook

India is anticipated to be the most rapidly growing nation in the Asia Pacific Direct Cathode Recycling Market on account of rising EV penetration, increasing domestic battery production capacity, and government policies aimed at facilitating the circularity of batteries and critical minerals security. The country is forecasted to grow at a CAGR of around 31.6% during 2026 to 2035, owing to rising investments in lithium-ion battery recycling facilities and localization of the battery value chain. As per the Express Network Private Limited (ENPL) – Global EV Outlook 2026, electric car sales rose by almost 45% in 2025 in India, making it one of the most rapidly growing EV markets worldwide. At the same time, India's PLI Scheme for ACC Battery Storage, which aims to reach a capacity target of 50 GWh, is boosting domestic battery production, leading to large volumes of battery manufacturing scrap that can act as feedstock for direct cathode recycling.

For instance, in November 2025, Li-Cycle Circle (Li-Circle), an Indian firm that recycles batteries, inked a Memorandum of Understanding (MoU) with ABR Co., Ltd. of South Korea to commercialize direct recycling technologies for lithium iron phosphate (LFP) batteries in India. This collaboration will involve the regeneration of used LFP cathode active material (CAM) for use in the manufacturing of new batteries by eliminating reliance on traditional methods of recovering metals.

Direct Cathode Recycling Market Competitive Landscape

- The Direct Cathode Recycling Market features three main categories of stakeholders: recyclers of batteries with advanced direct cathode recycling technologies, battery manufacturers and circular economy companies, and regional recycling companies. Among the most prominent innovators within direct cathode regeneration technologies, which are aimed at reforming cathode crystals and creating battery-grade cathode active materials (CAM), are Ascend Elements, Princeton NuEnergy, OnTo Technology, Duesenfeld, and ReLIB. Farasis Energy and LOHUM Cleantech add value to the ecosystem through their integration into battery production, second-life uses, and closed-loop recycling networks, whereas Brunp Recycling, Wuhan Rikomay New Energy Co., Ltd., and Tianjin Sai De Mei New Energy Technology Co., Ltd. have an impact on the ecosystem through regional recycling operations and cathode material recovery.

- Key players include Ascend Elements, Duesenfeld, OnTo Technology, ReLIB, Farasis Energy, LOHUM Cleantech, Brunp Recycling, Wuhan Rikomay New Energy Co., Ltd., Tianjin Sai De Mei New Energy Technology Co., Ltd., and Princeton NuEnergy.

Key Developments

- September 2025: Princeton NuEnergy (PNE) opens its first commercial facility in the United States in Chester, South Carolina, for the direct recycling of lithium-ion batteries using the ABM™ technology.

- January 2025: Altilium, a UK-based battery recycling technology company, raised US$5 million in strategic investment to help speed up the construction of the largest EV battery recycling plant in the United Kingdom. This will help in the growth of the EcoCathode™ recycling technology of Altilium, which involves the extraction of recyclable materials from used EV batteries and manufacturing scraps to make CAMs and pCAMs.

- December 2025: GDES launched its RESUBAT project that involved the creation of an innovative lithium-ion battery recycling technology with emphasis on integral battery recycling and cathode recycling technologies.

- March 2025: Novocycle launched the Dry-Direct Recycling technology of lithium-ion batteries through its pilot plant set up in the Netherlands under the Just Transition Fund to develop its unique Dry-Direct Recycling process technology for batteries. The main objective of the project is to recover cathode and anode active materials in high purity condition from used batteries and battery manufacturing wastes.

- January 2026: Honda partnered with Princeton NuEnergy in developing plasma-based direct cathode-to-cathode battery recycling technology for lithium-ion batteries.

Key Procurement Priorities and Buyer Evaluation Criteria

- Procurement decision-making is being affected by the increasing need for closed-loop battery supply chain systems, the use of EVs, battery production capacity increase, critical minerals security, and sustainability laws that require efficient recycling of lithium, nickel, cobalt, manganese, and other key components of batteries.

- The buyers rate the supplier based on the recovery efficiency of the cathode material, regeneration quality, chemical purity, scalability of the process, and capacity of producing recycled cathode materials in line with the requirements of battery manufacturers to make lithium-ion batteries for next-generation applications.

- Procurement choices have become more reliant on partner abilities, involving electric vehicle manufacturers, battery manufacturers, cell makers, and raw material suppliers, since businesses need dependable sources of recycled cathode material to lessen reliance on primary minerals.

- Customers will judge the technology vendors on the basis of manufacturing readiness level, scalability of the recycling plants, automation, quality control processes, and capacity to process bulk battery scrap and end-of-life batteries.

Why Choose DataM?

- Technological Innovations: Explores advancements in direct cathode recycling technologies, including relithiation processes, hydrometallurgical-assisted regeneration, selective cathode recovery, AI-enabled process optimization, and closed-loop recycling systems, enabling preservation of cathode crystal structures, lower energy consumption, and higher recovery efficiency compared to conventional recycling methods.

- Product Performance & Market Positioning: Assesses the ways by which market players distinguish themselves on the basis of the recovery yield of the cathode, purity of regenerated materials, scalability of the process, versatility of feedstock, and cost-efficiency.

- Real-World Evidence: Highlights commercial adoption of direct cathode recycling across EV battery recycling facilities, battery manufacturing plants, and pilot-scale circular supply chains, demonstrating benefits such as reduced carbon emissions, lower raw material dependency, shorter production cycles, and improved retention of critical battery material value.

- Market Updates & Industry Changes: Highlights various developments such as commercialization of direct recycling technologies, strategic collaborations between battery makers and recyclers, pilot plant scaling up, investments in recycling facilities, and changing regulations around battery circularity in North America, Europe, and the Asia-Pacific region.

- Competitive Strategies: Examines the strategies used by top corporations to improve their market standing using technologies for cathode material recycling, cooperation with car manufacturers and battery producers, increasing their recycling capacity, technology licensing, and incorporation into battery supply chains.

- Pricing & Market Access: Discusses how prices are determined by the battery chemistry, feedstock characteristics, efficiency of the process, processing capacity, and properties of the regenerated cathode materials, while considering market access via long-term recycling contracts, battery production collaboration, and mineral recovery systems.

- Market Entry & Expansion: Recognizes areas of growth based on growing EoL EV battery stocks, demands for environmentally friendly battery components, secure sources of minerals, and rigorous environmental laws, as well as ways to expand through developing recycling infrastructure regionally, forming joint ventures, commercializing technologies, and linking with battery production ecosystems.

Target Audience

- Lithium-Ion Battery Manufacturers

- Electric Vehicle (EV) Manufacturers

- Battery Recycling Companies & Material Recovery Providers

- Cathode Active Material (CAM) and Precursor Cathode Active Material (pCAM) Producers

- Battery Gigafactory Developers & Operators

- Energy Storage System (ESS) Manufacturers

- Battery Technology Companies & Research Organizations

Suggestions for Related Report