Carbon Capture Technology Market Size & Share

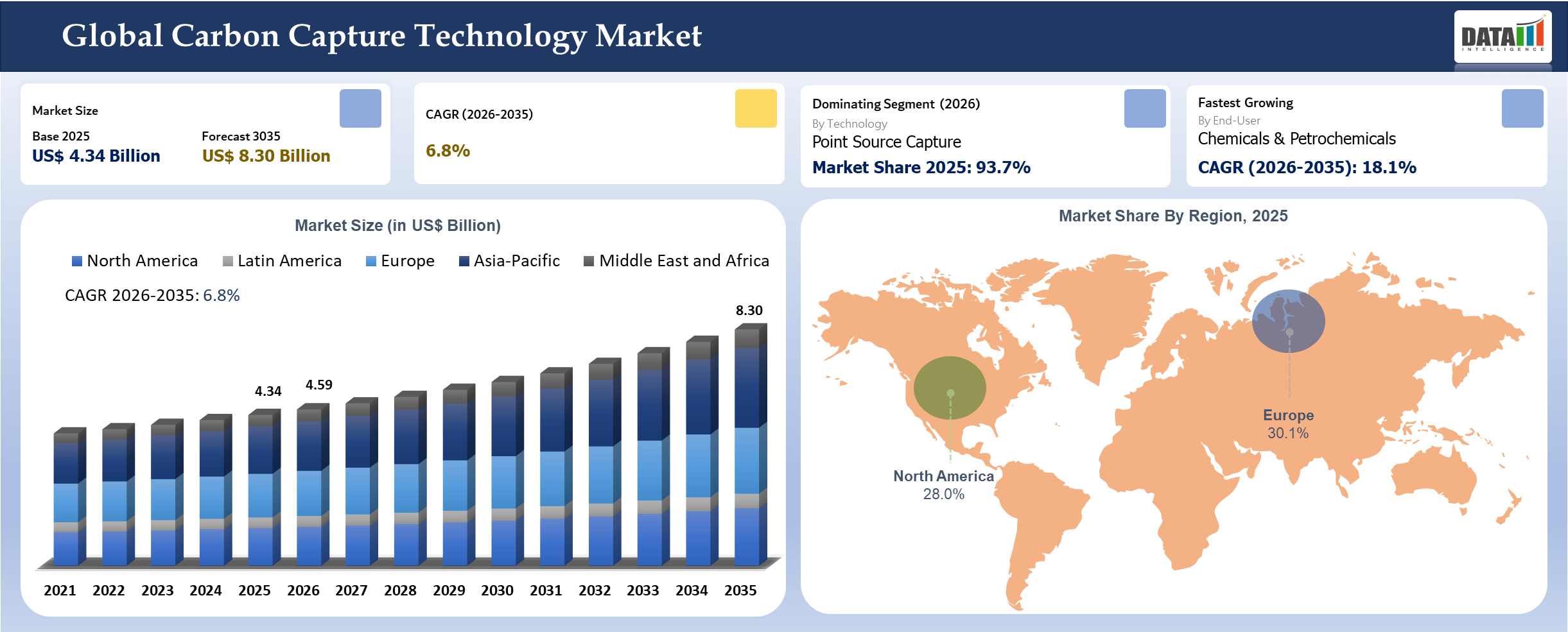

The global carbon capture technology market size reached US$ 4.34 billion in 2025 and is expected to reach US$ 8.30 billion by 2035, growing with a CAGR of 6.8% during the forecast period 2026-2035.

Owing to roadmap for the climate set out by the IEA and IPCC more attention is drawn towards decarbonization efforts. CCUS technologies have gained importance in sectors where decarbonization is critical such as cement, steel and chemical industries.

According to the International Energy Agency, more than 50 million tons per annum (MTPA) of CO₂ capture capacity will add by 2030, with the additional number of ongoing projects, the cumulative capacity will reach over 430 MTPA by 2030. Market is growing due to favorable regulatory conditions such as U.S. 45Q tax credits or European Innovation Fund, in addition to other mandatory policies regarding industrial decarbonization. An increasing number of corporations aiming for net-zero emissions will contribute to more investments into carbon capture.

Carbon Capture Technology Industry Trends and Strategic Insights

- Fast-paced growth in observed in industrial carbon capture, with the cement and steel sector coming up as the key players; for instance, Heidelberg Materials' Brevik facility (Norway) aims to capture around 400,000 tons of CO2 per annum from 2025 onwards.

- DAC technology is also progressing well and many firms are investing in this technology, such as Climeworks and Occidental Petroleum; Occidental's STRATOS project in Texas plans to capture about 500,000 tons of CO2 per year.

Carbon Capture Technology Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 4.34 Billion | |

| 2035 Projected Market Size | US$ 8.30 Billion | |

| CAGR (2026-2035) | 6.8% | |

| Largest Market | Europe | |

| Fastest Growing Market | Asia-Pacific | |

| By Technology | Point Source Capture, Carbon Dioxide Removal Capture | |

| By Capture Mechanism | Chemical Absorption, Physical Absorption, Adsorption, Membrane Separation, Cryogenic Separation, Calcium Looping, Chemical Looping, Electrochemical Separation, Mineralization and Mineral Looping | |

| By Offering Model | Technology License and Process Design, Modular Skid Systems, Major Process Equipment, Compression Dehydration and Liquefaction, FEED and Pilot Testing, EPC and Integration, O and M and Media Replacement, Carbon Removal as a Service | |

| By Source Stream and Concentration | Atmospheric Air, Very Low Concentration Below 4 Percent, Low Concentration 4 to 15 Percent, Medium Concentration 15 to 40 Percent, High Concentration Above 40 Percent | |

| By Deployment Basis | Retrofit Brownfield, New Build and Integrated Design, Hub Linked Cluster Projects, Standalone Single Site Projects | |

| By Installation Environment | Onshore, Offshore, Marine Onboard Carbon Capture | |

| By Annual Capture Capacity | Point Source and BECCS, DAC | |

| By Technology Maturity | Commercial at Scale, Early Commercial | |

| By End-User | Power Generation, Hydrogen and Ammonia, Refining, Natural Gas, Processing and LNG, Chemicals and Petrochemicals, Cement and Lime, Iron and Steel, Waste to Energy, Pulp and Paper, Ethanol and Bioethanol, Glass and Ceramics, DAC Project Developers, BECCS Project Developers | |

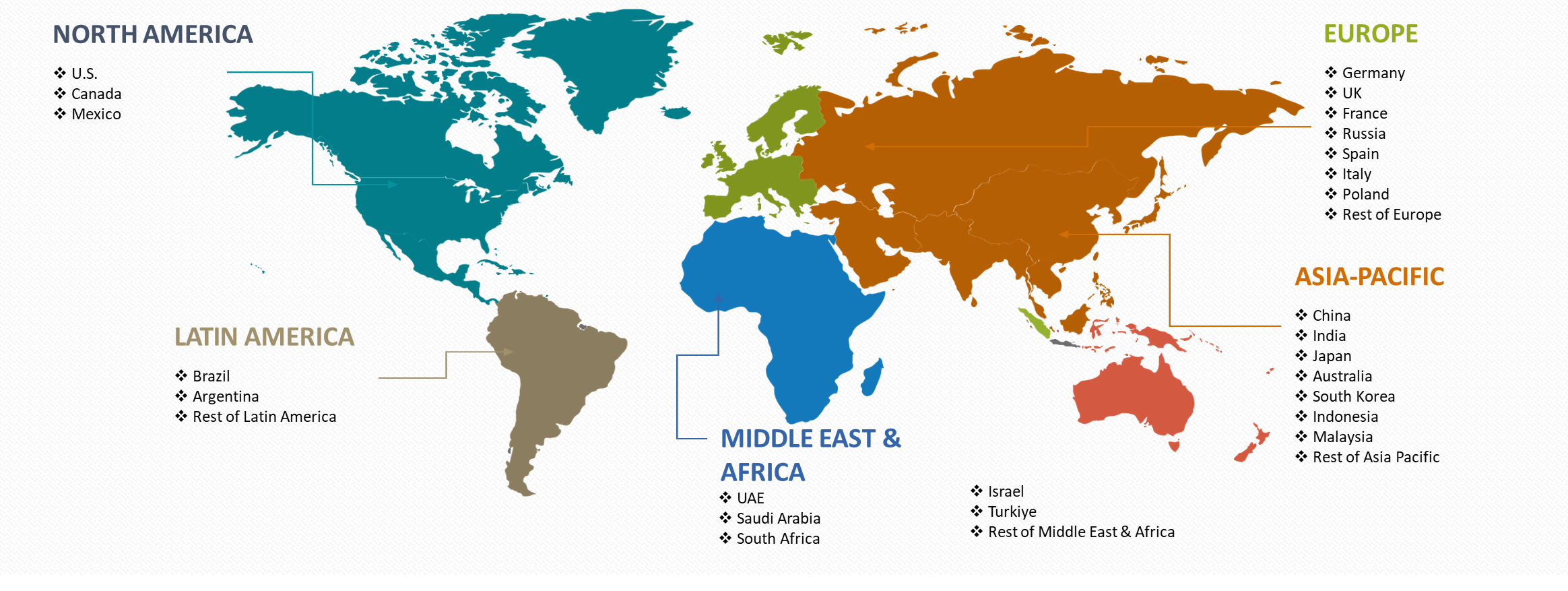

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

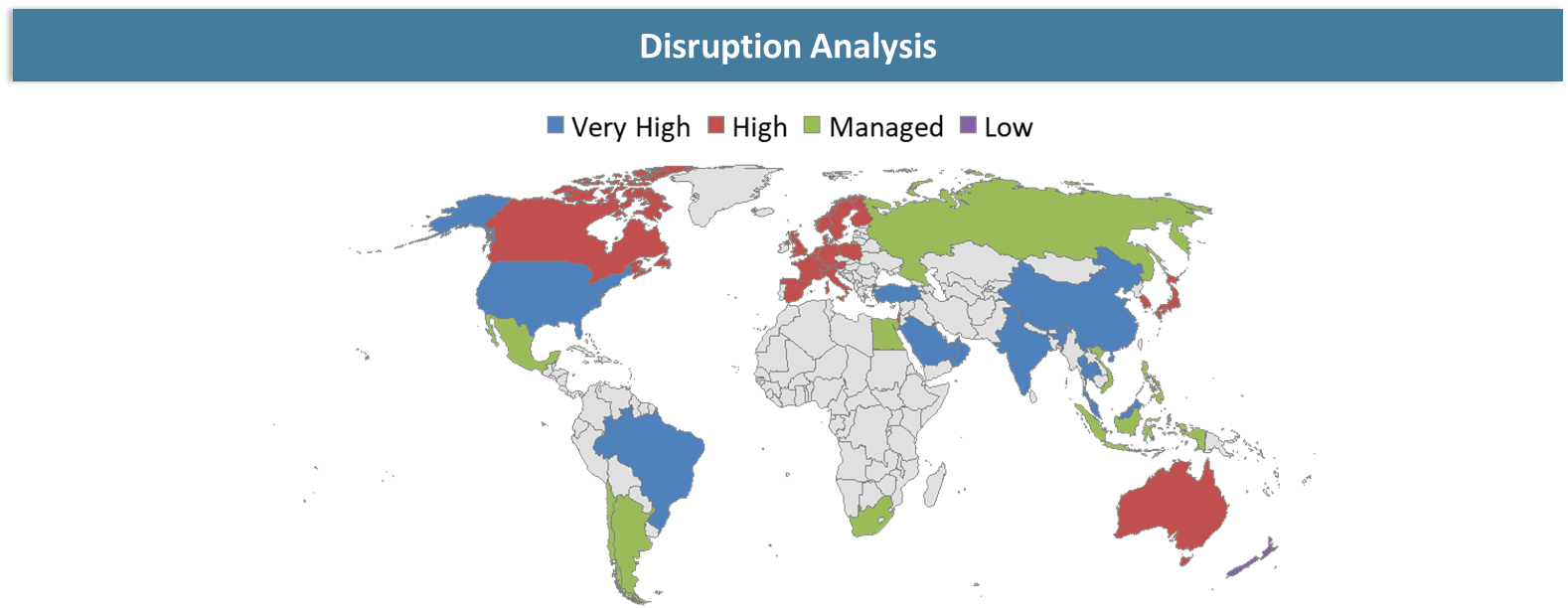

Disruption Analysis

The carbon capture technology market is currently experiencing disruptions through innovations, policy accelerations and new business models. Some of the innovations that are disrupting the market include direct air capture, new solvents and modularization in carbon capture technology. New market players such as Chevron Corporation and Equinor have entered the market to integrate their value chains with CCS technology.

Tax credits and carbon prices are among the policies that have sped up the process of carbon capture technology in geographical locations such as North America and Europe, offering new players an opportunity to play catch-up with existing ones. Collaboration between technology providers and companies that emit carbon will facilitate the growth of ecosystems. Market disruptions for carbon capture technology can result from costs involved, insufficient infrastructure and carbon storage.

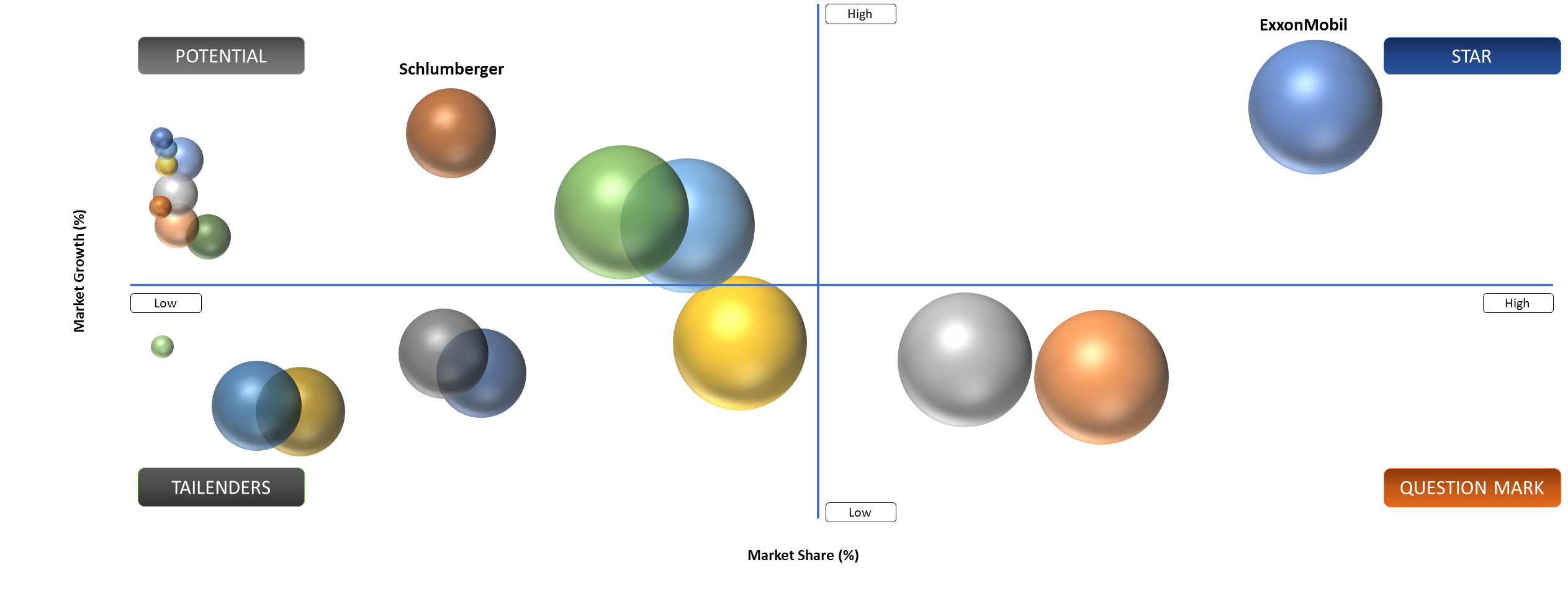

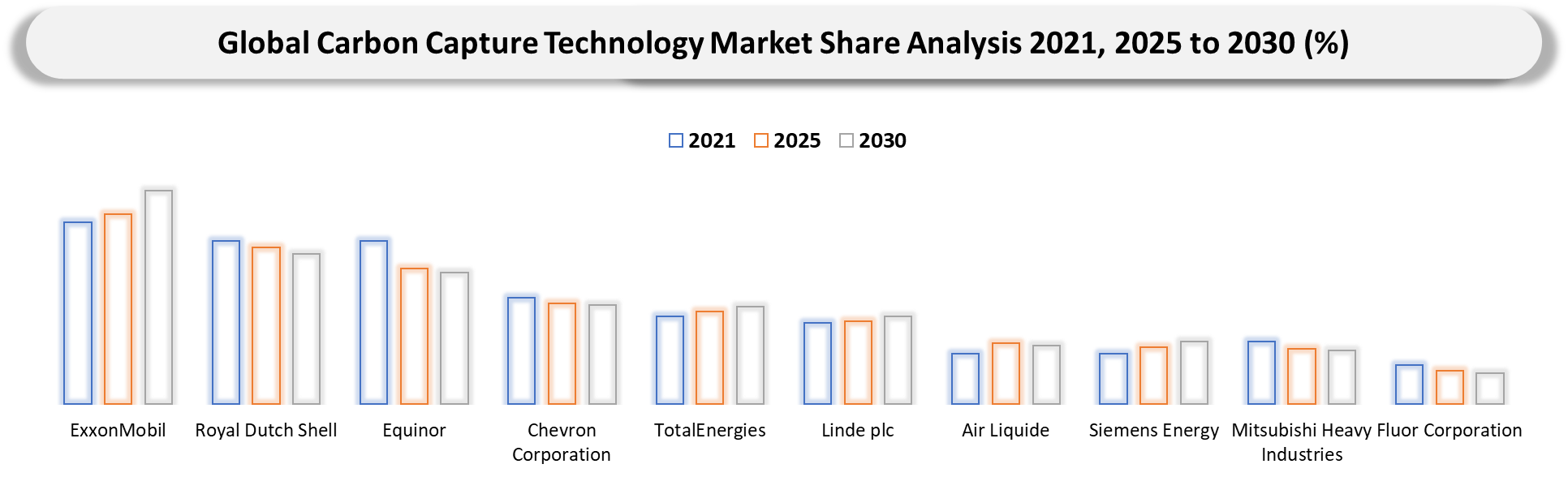

BCG Matrix: Company Evaluation

Maturity of technology, scalability of projects and policy-induced demand products are key influencers. The Stars category includes firms like ExxonMobil, Shell plc and TotalEnergies that are making massive investments in CCS hubs owing to the incentives provided by the government along with their decarbonization ambitions.

Companies including Air Liquide and Linde plc belong to the category of Potential firms because of the presence of stable income streams owing to the provision of gas processing services and carbon capture facilities. Question Marks include firms such as Siemens Energy and Mitsubishi Heavy Industries as they are improving their carbon capture technology; however, owing to the high capital costs and changing regulatory environment, there are certain uncertainties involved.

Carbon Capture Technology Market Dynamics

Rising Adoption Across Hard-to-Abate Industrial Sectors

CCS technology adoption rates are increasing in sectors where electrification or switching fuels is impossible. According to the IEA, around 7-8% of total global CO₂ emissions come from the cement manufacturing process alone. Holcim and Heidelberg Materials are some of the corporations that are developing plants capable of adopting CCS technology in Europe and North America. In 2025, the Heidelberg Materials received more than €200 million funding from the EU Innovation Fund for their CCS projects. The steel industry is adopting CCUS technology alongside hydrogen-based techniques, which is the case in Europe and Japan. All these indicate the use of CCUS to facilitate industrial activities despite the reduction in emissions' intensity, which is essential in jurisdictions that have high carbon prices due to an effective pricing mechanism such as EU ETS.

High Capital Costs and Infrastructure Gaps

While carbon capture has been gaining considerable momentum, several key economic and logistical challenges have emerged for its implementation. For instance, the cost for capturing CO₂ ranges from US$40 to above US$120 per tonne of CO₂, according to the data published by the International Energy Agency (IEA).

For example, the United States needs at least 30,000 more miles of CO₂ transportation pipelines to be constructed by 2050 in order to reach its net-zero objectives, states Princeton University. In addition, lengthy permit processes along with resistance from the community towards the construction of carbon sinks may result in project delays. It presents an added problem for the investors, especially in locations where carbon pricing is unreliable.

Carbon Capture Technology Market Segmentation Analysis

The global carbon capture technology market is segmented based on the technology, capture mechanism, offering model, source stream and concentration, deployment basis, installation environment, annual capture capacity, technology maturity, end-user and region.

Oil & Gas Sector Leads Technology Deployment

The use of carbon capture technology continues to be the primary focus of the oil and gas industry, utilizing CCUS for EOR processes and emissions reduction. Some of the important companies which have been making substantial investments in CCUS include ExxonMobil, Shell and TotalEnergies. For example, the plan by ExxonMobil to build a CCS hub in Houston by 2024 and reach a target capacity of 100 Mtpa of CO2 storage by 2040 is well known. For instance, Shell is making progress on its Porthos project in the Netherlands that aims to sequester 2.5 Mtpa CO2 from Rotterdam industrial facilities each year.

Direct Air Capture and Carbon Utilization Gain Traction

Innovative carbon capture technology includes direct air capture and carbon utilization. They help to increase carbon capture beyond point-source emissions by capturing carbon dioxide from the atmosphere and enabling negative emissions. The "Mammoth" plant of Climeworks operational in 2024 in Iceland will be capable of capturing 36,000 tons of CO₂ per year, representing one of the world's most advanced DAC plants.

Moreover, emerging carbon utilization technology turning CO₂ into fuels, chemicals and construction materials is rapidly developing. The Carbon Cure Technologies Company has utilized CO₂ injection technology in the concrete manufacturing process, resulting in a permanent fixation of CO₂ and strengthening the material. As per estimates from the Global CCS Institute, utilizations may represent up to 10% of applications of captured CO₂ by 2030 in chemicals and synthetic fuels.

Carbon Capture Technology Market Geographical Penetration

North America Leads in Enterprise Adoption and Platform Investment

North America has been leading the world in the application of CCS technologies owing to effective policy support and existing infrastructure, besides being among the first adopters. Indeed, more than 40% of global operating CCS capacity belongs to the United States and is facilitated by the extended 45Q tax credit that provides up to US$85 per ton of captured and sequestered carbon dioxide. In addition, Canada has been implementing projects under its Investment Tax Credit (ITC) that covers up to 50% of capital expenses incurred on the capture equipment. The most notable hubs for CCS applications are currently forming in Texas and Alberta, where shared facilities for CO₂ transportation and storage minimize costs and improve scalability.

U.S. Carbon capture technology Market Outlook

Carbon capture technology development in North America is mostly due to industrial decarbonization requirements and federal subsidies, while the U.S. leads the world in the creation of carbon capture projects. According to information from the U.S. Department of Energy, more than US$12 billion worth of funds will be invested into carbon management technologies because of recent infrastructure laws passed in the U.S., focusing on CCUS hubs. Moreover, the IEA notes that the U.S. alone accounts for 38% of planned carbon capture capacity globally, with most projects carried out by firms like ExxonMobil and Chevron Corporation. Increased 45Q tax credit of up to $85 per captured ton of CO₂ has boosted the economic viability of projects.

Canada Carbon capture technology Market Outlook

Even though the carbon capture technology implemented in Canada may not be on the same scale as the one used in the United States, the country is quickly becoming a leader in CCUS implementation due to strong governmental policies and industrial activity. Specifically, there is an investment tax credit providing coverage of up to 50% of capital expenses for CCUS facilities. Moreover, there are provincial projects in Alberta aimed at implementing large storage facilities. As per information provided by the Ministry of Natural Resources of Canada, more than 3 billion Canadian dollars have been invested into CCUS implementation thus far. One of those projects, Shell’s Quest, has successfully stored 8 million tons of CO₂. Additionally, there are plans to build carbon capture facilities in the oil sands industry.

Asia-Pacific: The World’s Fastest-Growing Region

Carbon Capture in Asia-Pacific region is witnessing rapid growth because of industrial emission and de-carbonization goals set by governments in the region. China already has some big CCUS installations in the country. For instance, Sinopec operates the Qilu-Shengli facility that captures 1 Mtpa CO₂ – considered to be the biggest CCUS project in Asia. Similarly, India is joining the CCUS club with plans of using the technology in its refineries and fertilizer plants by companies like the Oil and Natural Gas Corporation and Indian Oil Corporation. The focus of both Japan and South Korea is on transportation of CO₂ across borders and offshore storage of CO₂. As per METI, Japan intends to make the CCUS business chain operational by early 2030s, which includes transporting CO₂ to Southeast Asia for storage.

India Carbon capture technology Market Insights

The rapid development of carbon capture technology in India is influenced by the high level of emissions from industrial plants alongside India’s decarbonization targets. As per the Ministry of Power and NITI Aayog, the adoption of CCUS will be crucial for attaining net zero emissions by 2050 in hard-to-abate sectors such as steel and cement manufacturing. India releases more than 2.6 billion metric tons of CO2 annually (IEA), which creates a huge potential market for carbon capture technology. Carbon capture technology is currently being experimented with in state-owned corporations like Oil and Natural Gas Corporation. Furthermore, NTPC Limited has established a project that intends to transform CO2 into methanol.

China Carbon capture technology Industry Growth

With the biggest industrial emissions of any country, China is at the forefront of CCUS in the Asia-Pacific region owing to its aggressive climate goals and massive industrial scale. As reported by the Global CCS Institute, China currently holds an ever-growing stake in operational and planned CCUS plants, especially those involved in coal-to-chemistry and electricity generation applications. China National Petroleum Corporation and Sinopec have been major investors in the field; one of Sinopec's projects, Qilu-Shengli, captures more than 1 million tons of CO₂ per year. CCUS has also been incorporated into the country’s climate action plan through financial assistance programs and other incentives offered under the country’s Five-Year Plans. By 2024, China had announced several CCUS hubs intended to increase capture capacity.

Carbon Capture Technology Market Competitive Landscape

- The global carbon capture technology market features a competitive landscape led by energy majors, industrial engineering firms and specialized technology providers.

- Key players include ExxonMobil, Shell, Equinor, Chevron Corporation, TotalEnergies, Linde plc, Air Liquide, Siemens Energy, Mitsubishi Heavy Industries, Fluor Corporation, SLB and Halliburton.

- Companies compete on capture efficiency, cost optimization, scalability and integration across the CCUS value chain including transport and storage.

- Strategic focus areas include solvent innovation, carbon utilization pathways, DAC scaling and development of carbon storage hubs.

- Increasing collaboration between governments, emitters and technology providers is reshaping competitive dynamics, with cluster-based models emerging as the dominant deployment strategy globally.

Carbon Capture Technology Market Key Developments

- January 2026: ExxonMobil began commercial CCS operations with CF Industries, capturing two million tons CO₂ annually; additional Gulf Coast projects planned 2026.

- January 2026: Linde partnered with ExxonMobil on new CCS projects targeting industrial emissions capture, with startup plans across United States Gulf Coast facilities.

- January 2026: Schlumberger expanded carbon storage solutions portfolio, leveraging subsurface expertise to accelerate CCUS deployment across oil and gas sector decarbonization initiatives globally.

- January 2026: Halliburton enhanced CCUS service offerings, focusing on reservoir characterization and injection technologies to support large-scale carbon storage project development worldwide.

- January 2026: Baker Hughes expanded carbon capture technology portfolio, aligning with increasing CCUS investments and supporting industrial clients in emissions reduction strategies globally.

- August 2025: Shell, with partners, launched Northern Lights CCS, transporting and storing CO₂ offshore Norway, establishing first full commercial-scale CCS value chain.

- August 2025: Chevron continued CCS scaling ambitions, targeting multi-million tonne capacity projects aligned with industry-wide 2030 capture targets between ten and thirty million.

- August 2025: TotalEnergies participated in first CO₂ injection at Northern Lights, storing emissions 2,600 meters beneath seabed, validating full carbon capture chain.

- March 2025: Equinor advanced Northern Lights Phase 2 expansion, increasing CO₂ storage capacity from 1.5 to minimum five million tons annually.

Why Choose DataM?

- Technological Innovations: Explores the latest advancements in carbon capture technology design, including next-generation solvent systems, solid sorbents, membrane-based separation, cryogenic capture and direct air capture (DAC) solutions. It also highlights digital optimization, AI-enabled process control, modular plant configurations, electrification of capture units and integration with renewable energy sources, all contributing to higher capture efficiency, reduced energy penalties and lower cost per ton of CO₂ captured.

- Product Performance & Market Positioning: Evaluates how different technology providers perform across industrial applications such as power generation, cement, steel, chemicals and hydrogen production. The analysis compares capture efficiency, energy consumption, scalability, retrofit capability, CO₂ purity levels and lifecycle costs, highlighting how leading players differentiate through proprietary technologies, process integration expertise and project execution capabilities.

- Real-World Evidence: Highlights practical deployment of carbon capture technologies across large-scale projects, including post-combustion capture in thermal power plants, industrial carbon capture in cement and refining facilities and DAC installations. It demonstrates measurable outcomes such as emissions reduction percentages, cost optimization per ton captured, improved compliance with carbon regulations and enhanced sustainability performance for industrial operators.

- Market Updates & Industry Changes: Tracks key industry developments such as commercialization of DAC plants, CCUS (Carbon Capture, Utilization and Storage) hub developments, cross-border CO₂ transport infrastructure and increased government funding and incentives. It also covers evolving regulatory frameworks, carbon pricing mechanisms, net-zero commitments and large-scale investments across regions including North America, Europe, Asia-Pacific, China and India.

- Competitive Strategies: Analyzes how leading companies are strengthening their market position through strategic partnerships, joint ventures, technology licensing agreements and investments in R&D and pilot projects. It also highlights advancements in proprietary capture technologies, integration with hydrogen and bioenergy systems (BECCS) and the use of digital platforms for monitoring, reporting and verification (MRV) of captured carbon.

- Pricing & Market Access: Explains cost structures associated with carbon capture technologies, including capital expenditure (CAPEX), operational expenditure (OPEX), cost per ton of CO₂ captured and transportation/storage costs. It also reviews business models such as carbon capture-as-a-service, government subsidies, carbon credits and emissions trading schemes that improve project viability and market accessibility.

- Market Entry & Expansion: Identifies growth opportunities in emerging and industrializing economies driven by decarbonization targets, industrial emissions reduction mandates and expansion of CCUS infrastructure. It outlines strategies for market participants to scale globally through modular deployment models, regional partnerships, infrastructure integration and leveraging policy incentives to accelerate adoption.

Target Audience 2026

- Energy & Power Generation Companies: Utilities, independent power producers and fossil fuel operators deploying carbon capture systems to reduce emissions from coal, gas and biomass-based power plants.

- Oil & Gas Companies: Upstream, midstream and downstream operators integrating carbon capture, utilization and storage (CCUS) technologies for enhanced oil recovery (EOR) and decarbonization of refining and processing operations.

- Industrial & Manufacturing Sectors: Cement, steel, chemicals and petrochemical manufacturers adopting carbon capture solutions to mitigate hard-to-abate process emissions and comply with environmental regulations.

- Government & Regulatory Authorities: National and regional policymakers, climate agencies and environmental regulators implementing carbon reduction targets, carbon pricing mechanisms and CCUS incentives.

- Technology Providers & OEMs: Engineering firms, equipment manufacturers and technology developers specializing in capture systems, solvents, membranes and carbon transport and storage infrastructure.

- Investors & Financial Institutions: Private equity firms, venture capitalists, infrastructure funds and institutional investors financing large-scale CCUS projects and low-carbon innovation initiatives.

- Carbon Management & Storage Operators: Companies involved in CO₂ transportation, geological storage and carbon utilization, including pipeline operators and storage site developers.

- Research Institutions & Academia: Universities, research labs and innovation hubs advancing next-generation carbon capture materials, processes and cost optimization technologies.

- Consultants & Advisory Firms: Environmental consultants, sustainability advisors and strategy firms providing feasibility studies, regulatory compliance guidance and decarbonization roadmaps.