Introduction: Batteries Are No Longer Just a Cell Manufacturing Business

The global battery industry is entering a new phase between 2026 and 2035. For many years, the market was mainly discussed around battery cells, chemistry improvements and electric vehicle adoption. That view is now too narrow. Batteries have become the center of a much larger industrial value chain that connects raw materials, advanced chemicals, cell components, battery management systems, thermal control, electric vehicles, charging infrastructure, stationary energy storage, recycling and circular economy models.

This shift is important because the next decade of battery growth will not be decided only by which company produces the most cells. It will be shaped by who controls the supply of critical minerals, who develops safer and cheaper chemistries, who builds reliable battery packs, who scales fast-charging networks, who manages battery data and who recovers materials at the end of battery life.

Electric vehicles remain the largest commercial driver for battery demand, but they are no longer the only major demand center. Battery adoption is also expanding across renewable energy storage, grid-scale energy systems, data center backup, residential storage, industrial power backup, medical devices, rail, drones, electric aviation and consumer electronics. This widening application base is turning the battery market into one of the most strategic technology ecosystems of the 2026–2035 decade.

Request for Analyst Call For Battery Industry

Why the Battery Industry Is Becoming a Full Value-Chain Market

The battery industry is becoming a full value-chain market because batteries now influence energy security, automotive competitiveness, renewable power integration, industrial electrification, and digital infrastructure reliability. A battery is not just an energy storage device anymore. It is a strategic platform that supports mobility, power flexibility, and decarbonization.

This is why countries and companies are moving beyond simple battery imports. Governments are supporting local battery materials processing, cell manufacturing, recycling plants, and EV charging networks. Automakers are entering long-term supply agreements for lithium, nickel, graphite, and cathode materials. Energy companies are investing in grid-scale storage. Technology companies are using batteries to support backup power for data centers and AI infrastructure.

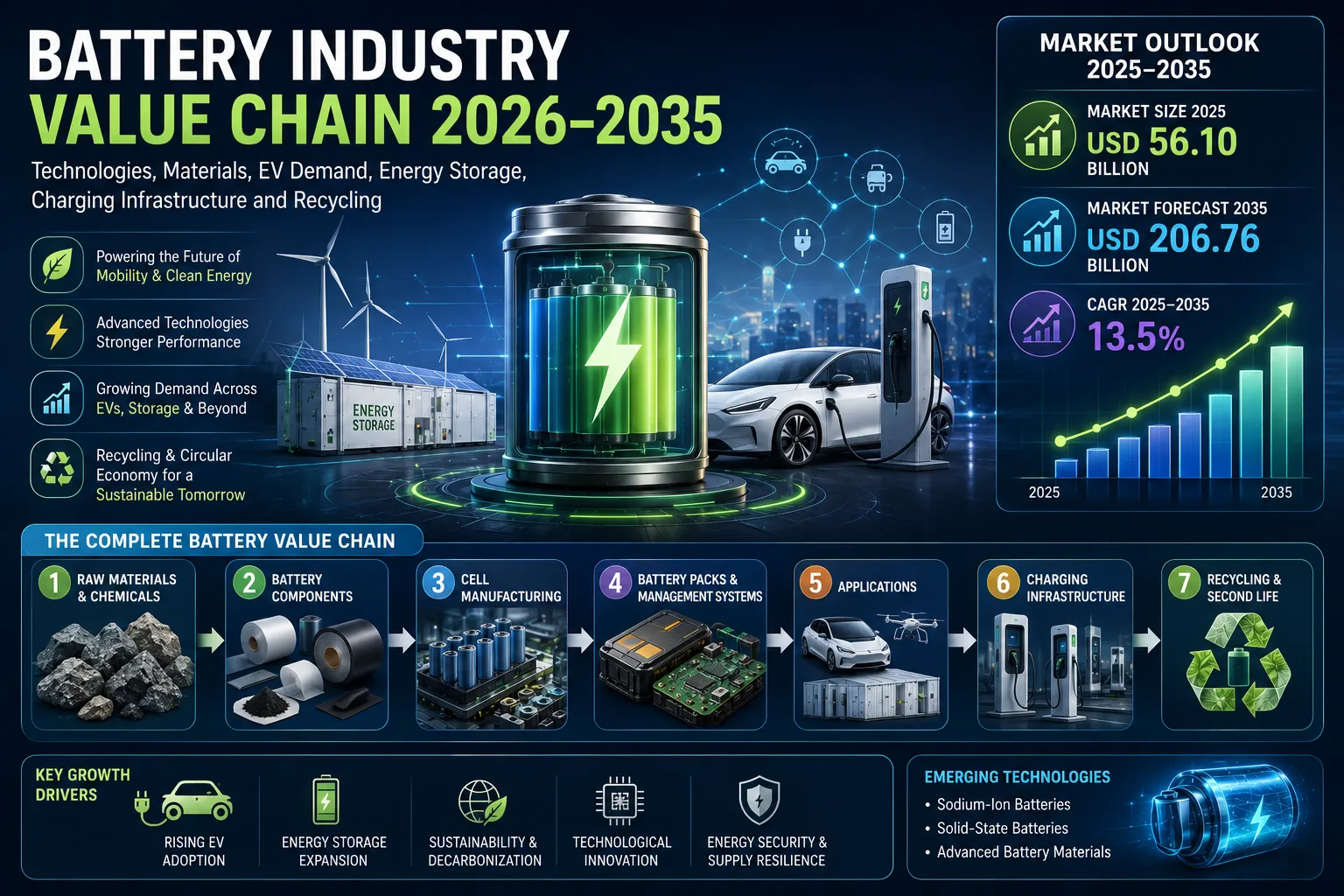

The battery market now includes multiple high-value layers:

- Raw materials and chemicals decide cost, supply security and battery performance.

- Cell chemistries decide energy density, safety, charging speed and application suitability.

- Components such as separators, electrolytes and current collectors decide battery reliability and lifecycle.

- Battery management systems and sensors decide safety, monitoring and performance control.

- Thermal management systems decide fast-charging capability and protection from overheating.

- Charging infrastructure and smart grids decide how fast EV adoption can scale.

- Recycling and second-life applications decide long-term raw material availability and environmental compliance.

This is why the battery industry should be viewed as a connected ecosystem, not as a single product market.

Lithium-Ion Remains the Commercial Backbone of the Battery Economy

Lithium-ion batteries will continue to remain the commercial backbone of the global battery economy through 2035. The reason is simple: lithium-ion has scale, manufacturing maturity, proven performance and strong adoption across electric vehicles, consumer electronics and energy storage systems.

The global Lithium Ion Battery Market is expected to grow from USD 56.10 billion in 2025 to USD 206.76 billion by 2035, expanding at a 13.5% CAGR. This growth reflects the strong demand coming from EVs, stationary storage, electronics, industrial systems and backup power applications.

Within lithium-ion, different chemistries are finding different roles. Lithium iron phosphate batteries, commonly known as LFP batteries, are gaining strong traction in mass-market electric vehicles and stationary storage because they offer better cost stability, longer cycle life and improved safety. LFP is especially attractive for grid storage, entry-level EVs, commercial vehicles and regions where affordability matters.

On the other hand, NMC and NCA batteries remain important for premium electric vehicles where higher energy density, longer driving range and performance are key purchase factors. These chemistries are still widely used in high-end EV platforms, although they are more exposed to raw material price volatility because of their dependence on nickel and cobalt.

Lithium-ion also continues to support consumer electronics, medical devices, industrial equipment and renewable storage. However, the market faces three major challenges: raw material dependency, safety risk and end-of-life waste. The next phase of lithium-ion growth will not come only from making more batteries. It will come from making safer, cheaper, more recyclable and more application-specific batteries.

Sodium-Ion and Solid-State Batteries Are Creating the Next Growth Layer

Sodium-ion and solid-state batteries are often described as future replacements for lithium-ion batteries. In reality, they are better understood as complementary technologies. They will not replace lithium-ion across all applications in the near term, but they will create new growth layers in specific segments where lithium-ion has limitations.

Sodium-Ion Batteries: A Low-Cost and Supply-Security Alternative

Sodium-ion batteries are gaining attention because sodium is more abundant and less geographically concentrated than lithium. This gives sodium-ion technology a strong strategic position in markets where cost, safety and supply security matter more than maximum energy density.

The Sodium Ion Battery Market is projected to grow from USD 1,263.70 million in 2025 to USD 8,643.11 million by 2035, at around 21.2% CAGR. This strong growth outlook reflects rising interest in low-cost storage, two-wheelers, entry-level EVs, backup power and grid applications.

Sodium-ion batteries may be especially useful for:

- Low-cost stationary energy storage

- Cold-climate applications

- Two-wheelers and three-wheelers

- Entry-level electric vehicles

- Telecom and industrial backup power

- Grid-scale storage where cost is more important than range

The technology is still developing in terms of commercial scale, supply chain maturity and performance optimization. However, its long-term value lies in reducing lithium dependency and providing an alternative chemistry for cost-sensitive markets.

Solid-State Batteries: High Energy Density and Safety Potential

Solid-state batteries represent one of the most important long-term technology shifts in the battery sector. Instead of using liquid electrolytes, solid-state batteries use solid electrolytes, which can improve safety and support higher energy density.

DataM Intelligence lists the Solid State Battery Market at US$1.58 billion in 2025, projected to reach US$15.4 billion by 2033, growing at a 30.8% CAGR.

Solid-state batteries are particularly attractive for premium electric vehicles, high-performance mobility, aerospace, defense, medical devices and applications where safety and energy density are critical. However, commercialization remains complex. Manufacturing cost, scalability, interface stability and cycle life are still major challenges.

This is why solid-state batteries should not be viewed as an immediate mass-market replacement for lithium-ion. They are more likely to enter premium and specialized applications first before scaling into broader EV and storage markets.

Battery Materials Are Becoming Strategic Energy Security Assets

Battery materials are now at the center of global energy security. The reason is clear: materials decide battery cost, range, charging speed, safety, supply stability and manufacturing competitiveness.

A battery company cannot scale without reliable access to cathode materials, anode materials, electrolytes, separators, current collectors, additives and battery-grade lithium compounds. This has made the Battery Material Market one of the most strategic parts of the battery ecosystem.

Cathode materials such as LFP, NMC, NCA, LMO and advanced cathode chemistries directly influence energy density, lifecycle and cost. LFP is gaining strong share in affordable EVs and energy storage, while nickel-rich cathodes continue to serve high-performance EVs. At the same time, companies are working on cobalt reduction, manganese-rich chemistries and high-voltage cathodes to improve performance and reduce supply risk.

Anode materials are also changing. Natural graphite and synthetic graphite remain dominant, but silicon-based anodes are gaining attention because they can improve energy density and charging performance. Lithium metal anodes are also being explored for solid-state batteries and next-generation high-energy systems.

Electrolytes and additives are becoming more important as battery makers try to improve safety, fast charging, low-temperature performance and cycle life. Separators and coating technologies are also critical because they help prevent short circuits and improve thermal stability.

Regional localization is another major trend. China has a strong position in battery materials processing, but the US, Europe, Japan, South Korea and India are increasing investment in domestic and regional supply chains. Between 2026 and 2035, battery materials will increasingly be treated not only as industrial inputs but as strategic national assets.

Request for Analyst Call for Battery Industry according to your Business Requirement

Components, BMS and Thermal Management Are Moving to the Center of Battery Design

As battery packs become larger, faster-charging and more powerful, the systems around the cell are becoming just as important as the cell itself. Battery safety, efficiency and lifecycle are now controlled by components, software, electronics and thermal systems.

Battery management systems, or BMS, are essential for monitoring voltage, current, temperature, state of charge, state of health and fault conditions. A good BMS improves battery safety, prevents overcharging, supports balancing and extends battery life. This makes the Battery Management Systems Market and Battery Management Integrated Circuit Market critical for EVs, energy storage systems and industrial battery applications.

Thermal management is another fast-growing area. EV batteries, fast-charging systems, data center backup batteries and high-power storage systems all generate heat. Poor thermal control can reduce performance, shorten battery life and create safety risks. Testing equipment is also becoming more valuable. Battery manufacturers must test safety, durability, charge-discharge behavior, abuse tolerance and lifecycle performance. As batteries enter more regulated and safety-sensitive applications, the Lithium Ion Battery Testing Equipment Market is expected to benefit.

Battery packaging, interconnects, nickel-plated steel strips, sensors and pack-level integration are also becoming higher-value areas. Buyers increasingly prefer suppliers that can support advanced battery system integration, not just individual components. This trend supports the growth of the Battery Components Market and related component ecosystems.

EV Batteries Are Now Connected to Charging Infrastructure, Smart Grids and Battery Swapping

Electric vehicle battery demand cannot be separated from charging infrastructure. A better battery is useful only when the charging ecosystem can support it. This is why EV batteries, charging stations, smart grids, power modules, cables, wireless charging and battery swapping are now becoming part of one connected market.

Ultra-fast charging is one of the most important growth areas. Fast-charging networks need batteries that can accept high power without overheating or degrading quickly. This creates demand for better thermal management, improved battery chemistry, advanced BMS and high-quality charging components. Markets such as Ultra Fast EV Charging Dispensers Market and Hypercharger Market are closely tied to this trend.

EV charging smart grids are also becoming more important. As millions of EVs connect to power networks, utilities need systems that can manage demand, reduce peak load, optimize charging times and support renewable energy integration. This supports the EV Charging Smart Grids Market. Battery swapping and battery-as-a-service models are also gaining relevance in commercial fleets, two-wheelers, three-wheelers and selected urban mobility systems. Wireless and inductive charging are still developing, but they can become important for premium vehicles, public transport, autonomous vehicles, industrial robots and electric aircraft interfaces. This connects battery demand with the Wireless Charging Market and Inductive Charging Market.

Battery Energy Storage Systems Are Expanding Beyond Renewable Backup

Battery energy storage systems are no longer used only as backup systems for renewable energy. They are becoming active grid assets that support peak shaving, frequency regulation, load shifting, renewable integration and power reliability.

The Battery Energy Storage System Market is expanding because power grids need more flexibility. Solar and wind generation are variable, and batteries help store excess power when generation is high and release it when demand rises. This makes batteries essential for renewable-heavy power systems.

Grid-scale batteries are growing quickly, especially where renewable energy capacity is expanding. LFP lithium-ion batteries currently dominate many stationary storage projects because of their cost, safety and cycle life advantages. However, sodium-ion, flow batteries and other advanced chemistries may gain share in specific long-duration or cost-sensitive storage applications over time.

Residential energy storage is another growth area. Homeowners are using battery systems with rooftop solar to reduce electricity bills, improve backup power and increase energy independence. This supports the Residential Energy Storage Market and Solar Inverter and Battery Market.

Data centers are also becoming an important demand source. As AI workloads and digital infrastructure expand, data centers need reliable backup power and energy management solutions. Batteries can support backup systems, reduce diesel generator dependence and improve power resilience.

Hybrid energy storage systems are also gaining attention because different technologies can serve different power and duration requirements.

Battery Recycling Is Becoming a Raw Material Security Strategy

Battery recycling is becoming one of the most important business opportunities in the battery value chain. The reason is not only environmental compliance. Recycling is now directly linked to raw material security, cost control and circular supply chains.

As EV batteries reach end of life, recycling can recover lithium, nickel, cobalt, manganese, copper, aluminum and graphite. These recovered materials can be reused in new battery production, reducing dependence on mining and imported raw materials.

Second-life battery applications are also emerging. EV batteries that no longer meet vehicle performance standards can still be used in stationary storage, backup power and low-demand applications. This creates an additional value layer before final recycling.

Regulatory pressure is also increasing. Governments are pushing for battery traceability, responsible sourcing, recycling targets and lower lifecycle emissions. This will encourage partnerships between automakers, cell manufacturers, recycling companies and material suppliers.

The circular battery economy will become a major competitive theme by 2035. Companies that can recover and reuse valuable materials efficiently will have an advantage in cost, sustainability and supply security. This supports the Circular Battery Economy Market and Circular Economy in Battery Recycling Market.

Top Companies and Competitive Themes in the Battery Ecosystem

The battery ecosystem is too broad for a simple top 10 company list. Different companies lead different layers of the value chain. The strongest competitive positions are emerging across cell manufacturing, materials, recycling, electronics, components, energy storage and charging infrastructure.

Cell Manufacturers

Major cell manufacturers include CATL, BYD, LG Energy Solution, Panasonic Energy, Samsung SDI and SK On. These companies are competing on manufacturing scale, chemistry innovation, automotive partnerships, cost reduction and global production capacity.

CATL and BYD have strong positions in China and global EV battery supply. LG Energy Solution, Samsung SDI and SK On are deeply connected to global automakers, especially in North America, Europe and Asia. Panasonic Energy remains important in high-performance EV batteries and long-term automotive relationships.

Material Suppliers

Battery material companies such as Albemarle, SQM, Umicore, BASF, POSCO Future M and Syrah Resources are important because they supply lithium compounds, cathode materials, anode materials and other critical inputs.

The material supplier landscape is becoming more strategic as automakers and cell makers seek long-term supply agreements. Battery material companies that can offer regional supply, responsible sourcing and advanced material technologies will remain highly relevant.

Battery Recycling Companies

Battery recycling companies such as Redwood Materials, Li-Cycle, Ascend Elements, Umicore and Glencore are helping build circular battery supply chains. Their role is becoming more important as EV battery volumes rise and governments push for recycled material use.

Recycling companies are no longer positioned only as waste processors. They are becoming future suppliers of critical battery materials.

BMS and Component Companies

Electronics and component companies such as Infineon, Analog Devices, NXP, Texas Instruments, Sensata and TE Connectivity play a major role in battery safety, monitoring, sensing, power electronics and connectivity.

As batteries become smarter and more software-controlled, these component suppliers will become more important in EVs, stationary storage, industrial batteries and charging systems.

Energy Storage and Charging Ecosystem

Companies such as Tesla Energy, Fluence, Sungrow, ABB, Siemens and Schneider Electric are important in energy storage, grid integration, charging infrastructure, power conversion and energy management.

Their role highlights an important point: the battery market is not only about cells. It is also about power systems, grid connectivity, digital energy management and infrastructure deployment.

Request for Analyst Call for Battery Industry according to your Business Requirement

What Battery Market Buyers Should Track Between 2026 and 2035

Between 2026 and 2035, battery market buyers should track the full value chain instead of focusing only on battery prices. The most important questions will be about chemistry readiness, supply chain security, safety, recyclability and infrastructure compatibility.

Buyers should closely monitor which chemistries are scaling fastest. Lithium-ion will remain dominant, but LFP, sodium-ion and solid-state batteries will each serve different use cases. No single chemistry will win every market.

Supply chain localization will also be critical. Regions that build local battery materials processing, cell production, recycling and charging infrastructure will have stronger control over cost and availability.

Material price volatility will remain a major risk. Lithium, nickel, cobalt, graphite and manganese markets can directly affect battery economics. Companies with diversified sourcing and recycling access will be better positioned.

Battery components are also becoming higher-margin opportunities. BMS chips, sensors, separators, electrolytes, thermal systems, testing equipment and packaging technologies will gain importance as battery systems become more advanced.

Recycling and second-life models should be watched closely. These areas can reduce raw material dependency and create new revenue opportunities across EV and energy storage markets.

Charging technologies will also shape battery demand. Ultra-fast charging, smart grids, wireless charging and battery swapping will influence how batteries are designed and deployed.

Finally, safety-first battery design will become essential in EVs, aviation, medical devices, data centers and grid-scale storage. Battery buyers will increasingly prefer suppliers that can prove performance, safety, compliance and lifecycle value.

Conclusion: The Battery Market Is Becoming an Industrial Ecosystem

The battery industry from 2026 to 2035 will be defined by integration. Cell manufacturing will remain important, but the real growth story will be across the full value chain: materials, components, BMS, thermal systems, charging infrastructure, energy storage and recycling.

Lithium-ion will continue to dominate commercial applications, while sodium-ion and solid-state batteries will create new opportunities in cost-sensitive and high-performance segments. Battery materials will become strategic assets. BMS and thermal management will become central to safety and performance. EV charging and smart grids will decide how fast electric mobility can scale. Battery recycling will become a major source of raw material security.

For companies, investors and market buyers, the biggest opportunity is not only to participate in battery demand growth. It is to understand where value is moving inside the battery ecosystem. The winners of the next decade will be the companies that connect technology, materials, infrastructure and circular economy models into one scalable battery strategy.

Frequently Asked Questions (FAQs)

What is the battery industry value chain?

The battery industry value chain includes raw materials, battery chemicals, cathode and anode materials, electrolytes, separators, cell manufacturing, battery packs, BMS, thermal management, charging infrastructure, energy storage systems and recycling.

Which battery technology will grow fastest between 2026 and 2035?

Solid-state and sodium-ion batteries are expected to grow faster from a smaller base, while lithium-ion batteries will continue to dominate in terms of total commercial demand.

Will sodium-ion batteries replace lithium-ion batteries?

Sodium-ion batteries are unlikely to fully replace lithium-ion batteries in the near term. They are more likely to complement lithium-ion in low-cost storage, entry-level EVs, backup power and grid applications.

Why are solid-state batteries important for electric vehicles?

Solid-state batteries are important because they can offer higher energy density, better safety and improved performance potential. However, large-scale commercialization still depends on cost reduction and manufacturing scalability.

What materials are used in EV batteries?

EV batteries commonly use cathode materials such as LFP, NMC and NCA; anode materials such as graphite and silicon-based materials; electrolytes, separators, current collectors, additives and battery-grade lithium compounds.

Why is battery recycling important for the battery supply chain?

Battery recycling helps recover critical materials such as lithium, nickel, cobalt, copper and graphite. This reduces raw material dependency, supports circular supply chains and improves long-term battery sustainability.

What is the role of BMS in battery safety?

A battery management system monitors voltage, temperature, current, charge level and battery health. It helps prevent overcharging, overheating, imbalance and unsafe operating conditions.

How is EV charging infrastructure connected to battery demand?

EV charging infrastructure directly affects EV adoption. Fast chargers, smart grids, charging cables, power modules and battery swapping systems all influence how EV batteries are designed, used and scaled.

Which battery markets are growing because of renewable energy?

Battery energy storage systems, grid-scale batteries, residential energy storage, solar inverter and battery systems, hybrid energy storage and renewable energy storage markets are growing due to renewable energy adoption.

What are the major investment opportunities in the battery ecosystem?

Major opportunities include battery materials, lithium-ion recycling, sodium-ion batteries, solid-state batteries, BMS chips, thermal management systems, EV charging infrastructure, grid-scale storage and circular battery economy solutions.