Market Overview

Battery validation is becoming a strategic bottleneck in the global electrification race. As EV production, grid storage deployment, and battery innovation accelerate, testing infrastructure is no longer a support function but a core investment area.

The timing of investment is closely tied to EV production scaling and policy-driven battery localization. With EV sales surpassing 14 million units and global battery manufacturing capacity moving toward multi-terawatt-hour scale, testing equipment demand is directly linked to production throughput. However, adoption is constrained by high calibration costs, long procurement cycles, and evolving regulatory standards.

Market Scope

| Metric | Details |

| Market Size (2026) | US$ 875.44 million |

| Market Size (2035) | US$ 1,409.78 Million |

| CAGR | 5.40% |

| Historic Years | 2023-2024 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Segments Covered | Equipment Type, Testing Type, Component, Application, End-User, Region |

| Leading Region | Asia-Pacific |

| Fastest Growing Region | North America |

For more details on this report : Request for Sample

Key Takeaways

- Demand is production-linked: Battery manufacturing expansion from 3 TWh in 2024 toward 9 TWh by 2030 directly multiplies testing system requirements.

- 2026 market size crosses US$ 875 million, signaling steady but infrastructure-dependent growth rather than exponential expansion.

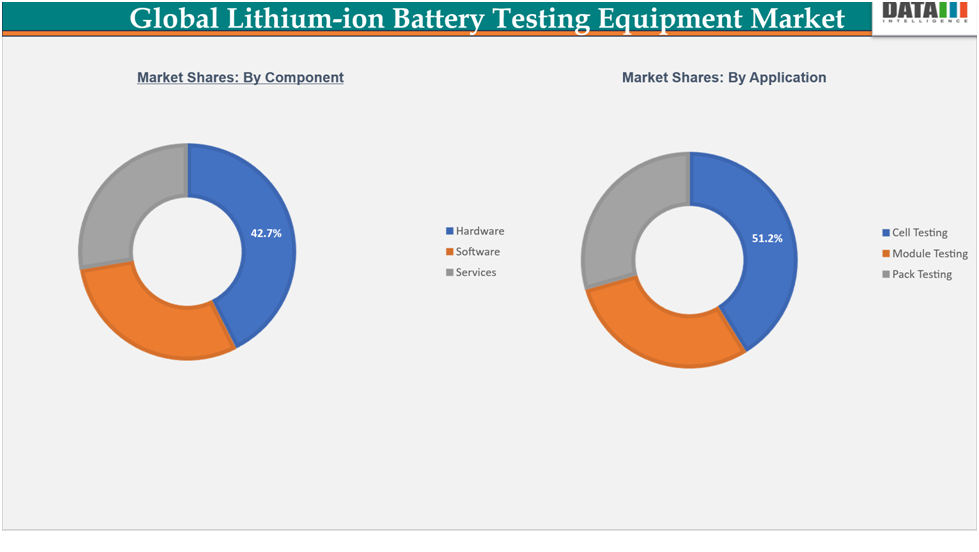

- Hardware dominates with 42.7% share, led by battery cyclers and formation systems critical for gigafactory operations.

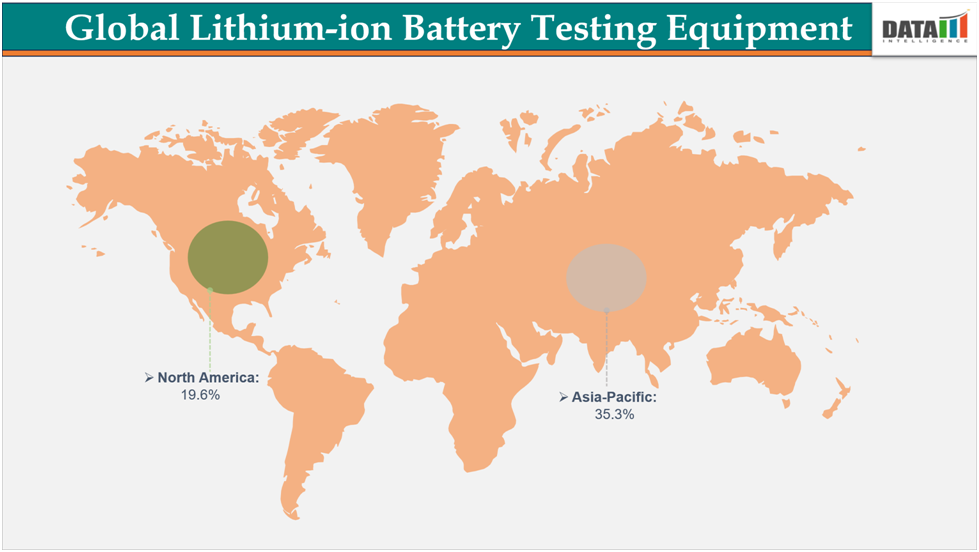

- Asia-Pacific holds 35.3% market share, anchored in China, Japan, South Korea, and India’s policy-backed battery ecosystems.

- North America, with 19.6% share, is accelerating due to federal funding and localization strategies.

- Lithium-Ion Battery Testing Equipment pricing and adoption trends highlight calibration costs contributing up to 10–15% of ownership expenses.

- Compliance-driven demand is intensifying due to EU, US, and China safety regulations, making testing non-negotiable for market entry.

Demand Drivers Linked to EV and Energy Storage Expansion

The primary Lithium-Ion Battery Testing Equipment growth drivers are rooted in EV production scaling and grid storage deployment. Each battery cell, module, and pack must undergo multi-stage validation including performance, lifecycle, and safety testing.

Government-backed programs are reinforcing this demand:

- US initiatives supporting battery manufacturing and validation infrastructure

- EU Battery Regulation enforcing lifecycle traceability and safety compliance

- China’s GB/T standards mandating extensive reliability testing

These frameworks are pushing manufacturers toward high-throughput, automated testing systems capable of handling gigafactory-scale volumes.

Hardware-Software Stack and Automation ROI

The testing ecosystem is evolving into an integrated stack:

- Core hardware: Battery cyclers, environmental chambers, analyzers

- Software layer: Data acquisition, analytics, test automation platforms

- Integration layer: Pack-level emulation, BMS validation systems

- Service layer: Calibration, maintenance, and lifecycle support

From an ROI perspective, automation reduces manual intervention, improves throughput, and ensures compliance consistency. However, ROI realization depends on utilization rates and production scale, making large manufacturers the primary adopters.

Adoption Barriers and Cost Pressures

Despite strong demand, several constraints shape market expansion:

Calibration and Maintenance Burden

Precision testing systems require frequent calibration to meet ppm-level accuracy. Annual service and recalibration costs can account for 10–15% of total ownership, limiting adoption among smaller players.

Capital-Intensive Deployment

High upfront costs for integrated testing systems, especially those combining thermal, electrical, and safety validation, create procurement delays.

Standardization Complexity

Diverse regulatory frameworks across regions increase system customization requirements, adding to cost and complexity.

Supply Chain and Infrastructure Outlook

The Lithium-Ion Battery Testing Equipment supply chain analysis reveals tight coupling with battery manufacturing ecosystems. Equipment demand scales with:

- Gigafactory construction timelines

- Raw material availability (lithium, cobalt, nickel)

- Localization policies for battery production

Infrastructure policy is playing a decisive role. Incentives for domestic battery manufacturing are indirectly driving testing equipment procurement.

Emerging Opportunity Areas

Charging Infrastructure and Validation Demand

The rise in EV charging networks is increasing the need for Lithium-Ion Battery Testing Equipment charging infrastructure demand, particularly for validating battery performance under fast-charging conditions.

Recycling and Second-Life Testing

The Lithium-Ion Battery Testing Equipment recycling and second-life opportunity is gaining traction. As battery recycling ecosystems develop, testing equipment is required to assess residual capacity and safety for reused batteries.

OEM Partnerships and Integrated Solutions

Equipment vendors are increasingly forming partnerships with automotive OEMs and battery manufacturers to deliver customized, end-to-end testing solutions.

Segmentation Analysis

Segmented by equipment type (battery cyclers, analyzers, charge/discharge testers, environmental chambers, life testers), by testing type (performance, safety, environmental, lifecycle), by component (hardware, software, services), by application (cell, module, pack testing), by end-user, and by region - share, trends, and forecast to 2035.

Component Insights

Hardware leads the market with 42.7% share, driven by the scaling need for:

- High-throughput battery cyclers

- Automated formation and aging systems

- Integrated environmental testing setups

Software and services are gaining importance as manufacturers seek data-driven insights and lifecycle management capabilities.

Application Trends

- Cell testing dominates early-stage validation

- Module and pack testing are expanding rapidly with EV integration

- End-users span automotive, energy storage, and consumer electronics sectors

Regional Analysis

Asia-Pacific

Asia-Pacific leads the Lithium-Ion Battery Testing Equipment regional analysis with 35.3% market share in 2024. Strong government backing, including China’s multi-billion-dollar subsidies and India’s ACC PLI scheme, is driving large-scale battery manufacturing and testing infrastructure deployment.

Japan and South Korea are investing heavily in next-generation battery R&D, further increasing demand for advanced testing systems.

North America

North America is the fastest-growing region, supported by over US$ 7 billion in federal funding for battery supply chains. EV adoption targets and infrastructure investments are accelerating testing equipment demand, particularly in automotive and energy storage applications.

Europe

Europe’s growth is compliance-driven. The EU Battery Regulation is enforcing strict safety, traceability, and recycling standards, compelling manufacturers to deploy integrated, multi-stage testing platforms across gigafactories.

Competitive Landscape

The Lithium-Ion Battery Testing Equipment vendor landscape includes:

- Arbin Instruments, Inc.

- Chroma ATE Inc.

- Bio-Logic Science Instruments SAS

- Digatron Power Electronics GmbH

- Gamry Instruments, Inc.

- Hioki E.E. Corporation

- Neware Technology Limited

- PEC NV

- Megger Group Limited

- Keysight Technologies, Inc.

Strategy and Positioning

- Keysight Technologies focuses on high-precision measurement platforms and partnerships with EV and energy companies.

- Arbin emphasizes integrated, turnkey systems with advanced measurement accuracy and thermal integration.

- Vendors are differentiating through automation, system integration, and compliance-ready solutions rather than standalone equipment.

Recent Developments

In May 2026, Chroma ATE Inc. expanded its lithium-ion battery testing solutions with advanced high-precision testing systems for EV and energy storage applications. The initiative focuses on accuracy and scalability. This supports battery quality assurance.

In April 2026, Keysight Technologies, Inc. introduced next-generation battery testing equipment with enhanced automation and data analytics capabilities. The development improves testing efficiency and reliability. This benefits manufacturers.

In March 2026, Arbin Instruments strengthened its battery testing portfolio with high-performance systems for research and production environments. The innovation focuses on flexibility and precision. This supports advanced battery development.

Report Benefits

This report supports:

- Manufacturers in aligning testing capacity with production scaling

- Investors in identifying infrastructure-driven growth opportunities

- Technology providers in understanding integration and automation trends

- Procurement teams in evaluating cost, ROI, and vendor capabilities

- Strategy teams in tracking regulatory and regional demand shifts

Target Audience

- Battery manufacturers and gigafactory operators

- Automotive OEMs and EV manufacturers

- Energy storage system providers

- Testing equipment manufacturers

- Government and regulatory bodies

- Investors and infrastructure funds

The global lithium-ion battery testing equipment market report delivers a detailed analysis with 78 key tables, more than 79visually impactful figures, and 239 pages of expert insights, providing a complete view of the market landscape.