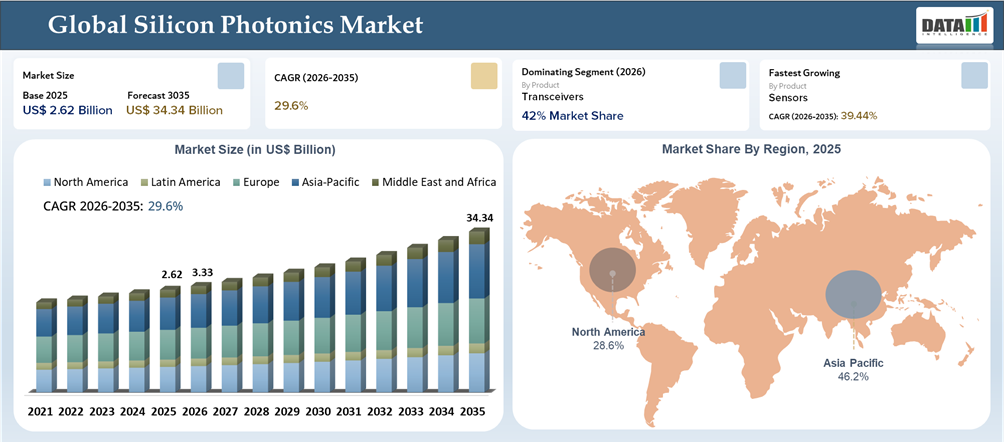

Silicon Photonics Market Size & Share

The global Silicon Photonics Market reached US$ 2.62 billion in 2025 and is expected to reach US$ 34.34 billion by 2035, growing with a CAGR of 29.6% during the forecast period 2026-2035.

Silicon photonics addresses the architectural limitations of today's computer and communication systems since electrical interconnects cannot meet the requirements of increased bandwidth, reduced latency, increased power consumption, and higher density of AI clusters, hyperscale data centers, and advanced telecommunications infrastructures. Silicon photonics has advantages such as range extension, bandwidth density enhancement, latency reduction, and power efficiency improvement, and it is produced through the process of CMOS-based semiconductors that makes it scalable relative to many conventional discrete optics technologies.

Silicon Photonics Industry Trends and Strategic Insights

- AI and HPC implementations increasing demand for ultra high bandwidth interconnects

- Electrical-to-optical interconnects becoming increasingly common in hyperscale data centers

- Closer integration between photonics technology and CMOS manufacturing for cost reduction

- Excellent collaboration between semiconductor companies and cloud service providers

- Increased use in telecommunication networks for 5g and long-distance communication

- Increased emphasis on energy-efficient data transmission systems

- Silicon photonics expanding its reach into sensing and medical sectors

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 2.62 Billion | |

| 2035 Projected Market Size | US$ 34.34 Billion | |

| CAGR (2026-2035) | 29.6% | |

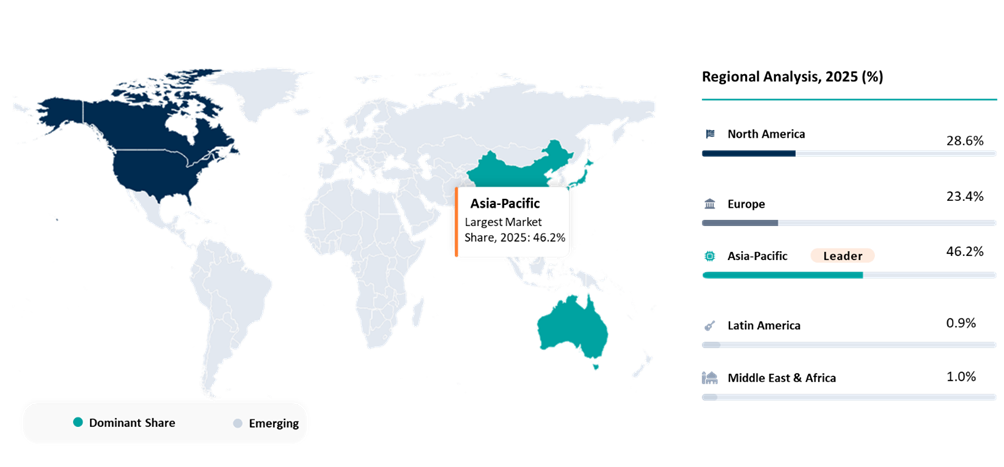

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Product | Transceivers, Optical Connectivity and Link Products, Optical Components, Sensors, Services (Foundry, Design, Assembly and Test Services) and Others | |

| By Component | Lasers, Modulators, Photo Detectors, Passive Building Blocks, Electronic and Packaging Enablers | |

| By Wavelength Band | 850 nm, 1260 to 1360 nm O band, 1525 to 1565 nm C band, 1565 to 1625 nm L band and 2000 to 7000 nm Mid IR. | |

| By Application | Data centers and HPC, Telecommunication, Military and Defense, Aerospace and Space, Medical and Life Science, Automotive and Mobility, Industrial and Energy, Quantum and Scientific and Others. | |

| By Packaging Architecture | Pluggable, On-Board Optics, Near Packaged Optics, Co Packaged Optics and Optical IO Chiplets. | |

| By Integration Approach | Monolithic SiPh, Hybrid integration and Heterogeneous integration | |

| By Wafer Size | 200 mm and 300 mm | |

| By End-User | Hyperscalers and Cloud Providers, Telecom Operators, Network Equipment Vendors, Defense Integrators, Healthcare and Diagnostics, Automotive OEM and Tier 1, Industrial OEM and Research and Public Sector | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

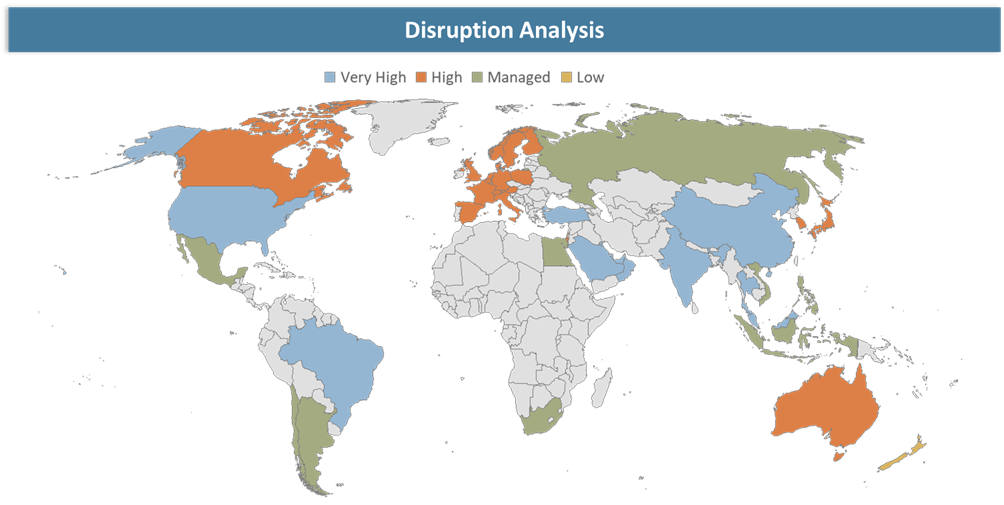

Disruption Analysis

Shift from electrical scaling to optical scaling

The technology disrupts existing interconnect economics due to its impact on the scaling of bandwidth within and across servers, switches and racks. In traditional designs, bandwidth scalability has been highly dependent on faster electrical signaling, retimers, copper assemblies with increased thicknesses and cooling costs. Such strategies become less effective at extremely high speeds. With silicon photonics, more bandwidth is incorporated using optical connections to minimize insertion losses, better manage energy per bit transfer and ensure longer reaches without increasing board density.

The most notable disruption happens with AI and hyperscale data center designs. The bigger the cluster size, the more critical it becomes to have optical interconnect for scale-out fabrics, communication between accelerators and inter-switch connections. Consequently, this drives the need for higher-speed 800G and 1.6T transceivers, optical engines and co-packaged optics. This puts pressure on copper interconnect incumbents, optics vendors that do not integrate well and system companies that are unprepared for photonics-enriched designs.

Disruption is also taking place at the supply chain and value chain levels. Semiconductor foundries, substrate providers, packaging technology experts, laser makers, DSP chip suppliers and switch ASIC suppliers are increasingly being integrated into the same chain. Consequently, the competitive advantage is moving from the capabilities of each discrete part to readiness of the system, yield and platform manufacture.

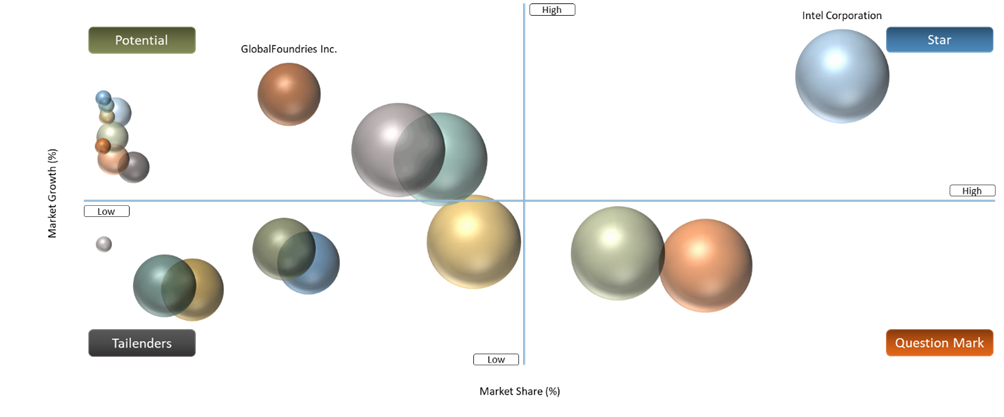

BCG Matrix: Company Evaluation

Silicon photonics competitors could be categorized by commercial success and strategic capability. Market share, as used here, refers to relevance in terms of adoption in cloud, AI and telecom optics infrastructures, while business strength refers to capabilities in manufacturing, packaging, ecosystem partners and platform integration.

Stars: High strategic momentum and strong relevance in AI and high speed optical scaling. These companies are shaping next generation architectures or ecosystem roadmaps.

Question Mark: Strong market presence, large customer access and broad product leverage across optics, switching, or system integration.

Potential: Technology rich challengers building optical I O or photonic fabric positions, with strong upside but smaller current commercial base.

Tailenders: Important ecosystem participants with selective strengths in components, design tools, foundry capability, or platform enablement rather than dominant end market share.

Market Dynamics

AI training, AI inference, cloud networking and high-performance computing

Modern accelerator clusters demand very high bandwidths, low latency and reliable signal integrity over greater physical distances within the servers, between racks and even clusters. Silicon photonics provides an immediate solution for this demand since it makes possible the development of miniaturized optical interconnects capable of delivering higher bandwidth while remaining more efficient than their all-electrical counterparts.

The need is most apparent within data centers and high-performance computing, especially in light of the transition from 400G to 800G and beyond to 1.6T speeds that are significantly accelerating upgrade timelines. Operators of hyperscale facilities and AI infrastructure developers are placing premium emphasis on systems that will deliver lower watts per bit, maximize front-panel density and avoid generating excess heat. This is creating new opportunities for both transceivers and photonic engines, which will facilitate the design of next-generation switches and compute nodes.

Packaging Complexity and Laser Integration Cost

The main limitation of the market does not lie in demand but in the difficulty associated with the construction of reliable and scalable systems that integrate photonic chips with lasers, electronics, heat control, advanced packaging techniques and testing procedures. Any inefficiency in manufacturing yield or assembly processes may result in increased costs or other issues associated with scalability.

The incorporation of a laser source is also crucial. Many designs in silicon photonics still require heterogeneous lasers, which results in additional costs associated with packaging or increased bill of materials, as well as complicated qualification procedures. All these aspects may discourage users from adopting the technology or pose additional problems to providers of chips.

Segment Analysis

The global silicon photonics market is segmented based on services, component, wavelength band, packaging architecture, integration approach, wafer size, end-user and region.

Among product categories, transceivers represent the most commercially mature and quantifiable segment because they sit at the direct interface between silicon photonics innovation and deployable network hardware. Silicon photonics transceivers are widely used in data centers, cloud interconnects and telecom transport because they offer high port density, scalable lane speed roadmaps and more favorable power efficiency at high data rates.

The segment benefits from a clear migration path from 100G and 400G into 800G and 1.6T generations. As operators move toward higher bandwidth fabrics, transceivers built on silicon photonics platforms are increasingly preferred for their manufacturability and ability to integrate multiple optical functions in compact form factors. This makes the transceivers segment the logical lead segment for market sizing, while components such as modulators, lasers and photodetectors act as enabling layers that scale with module adoption.

Commercially viable cross segmentation is best represented by By Product and By Application, with Transceivers under Data Centers and High Performance Computing as the strongest addressable combination. This cross is the most quantifiable because product shipments, lane speed migration, cloud capex and switch upgrade cycles can all be linked to actual deployment demand.

Geographical Penetration

North America Silicon Photonics Market Value

North America has a large hyperscale cloud spend base, advanced AI infrastructure rollouts, network equipment requirements and early adoption of high-speed optical interconnects. It also boasts several market players that can drive market development and foster design wins, including those in semiconductors, networking solutions, optical subsystems and AI compute capabilities.

In the region, companies are focusing on data center and HPC applications. Big cloud customers and platform makers are working on ambitious plans for developing 800G, 1.6T, optical engines and CPOs, resulting in high demand for transceivers, modulators, lasers, detectors and switch-based photonic platforms.

United States Silicon Photonics Market Trends

U.S. dominates in the region due to its significant investment in the infrastructure for artificial intelligence, cloud computing services and semiconductor technology. It boasts of some of the major players in products and ecosystems such as Intel, Cisco, Broadcom, NVIDIA, Marvell and optical I/O startup companies. With AI cluster scaling, high speed pluggable optics, co-packaging optics and photonic interconnect architectures are being pioneered by U.S. In addition, the country has very robust capability in design, packaging and semiconductor research that facilitates both volume deployment and future innovations.

Canada Silicon Photonics Market Outlook

Canada is witnessing steady growth supported by increasing data center investments, favorable government policies, expansion of digital infrastructure, telecom and photonics research base and role in advanced semiconductor and optical design collaboration. Canadian demand is linked to network infrastructure modernization, research intensive photonics development and cross border participation in North American cloud and telecom supply chains.

Over the forecast period, Canada is expected to benefit from spillover demand associated with AI infrastructure expansion and optical networking upgrades. While the market base is narrower, growth can remain attractive in specialized optical modules, research grade photonic integration and selected telecom and sensing applications.

Competitive Landscape

- Silicon photonics industry is known to be intensely competitive owing to the presence of leading semiconductor players, networking firms and start-ups. The main competition trends include innovations, collaboration and acquisition among other things to gain more market position. The players are investing in research and development to improve integration features, lower costs of production and broaden applications. Competitive landscape is also influenced by collaboration between semiconductor players and cloud services in developing customized photonic components.

- Key players include Intel Corporation, Cisco Systems, Inc., Broadcom Inc., Marvell Technology, Inc., Coherent Corp., Lumentum Holdings Inc., GlobalFoundries Inc., STMicroelectronics N.V., NVIDIA Corporation, Nokia Corporation, Hamamatsu Photonics K.K., NEC Corporation, Sumitomo Electric Industries, Ltd., Mitsubishi Electric Corporation, Ayar Labs, Ciena Corporation, Eoptolink Technology Inc., Ltd., Accelink Technology Co., Ltd., InnoLight Technology and Nippon Telegraph and Telephone Corporation.

Key Developments

- March 2026: NVIDIA Corporation partnered with Coherent Corp. to design optical components for future data center systems, with NVIDIA stating that silicon photonics was essential for scaling AI infrastructure.

- March 2026: NVIDIA Corporation partnered with Marvell Technology, Inc. in NVLink Fusion and mentioned the use of silicon photonics for collaboration on the next-generation infrastructure.

- March 2026: Cisco Systems, Inc. revealed new products such as 1.6 terabits per second OSFP and 800G low power optics using Cisco Silicon Photonics technology, solidifying its plans for AI-enabled network solutions.

- March 2026: Coherent Corp. demonstrated innovations such as 1.6T, 3.2T and future 12.8T architecture including silicon photonics and co-packaged optics technologies for future AI scale networks.

- March 2026: Marvell Technology, Inc. featured customer sampling of Ara X, Ara T, Petra and Aquila M optical DSPs and expanded its OFC 2026 connectivity showcase with offerings in optical engines and AI data center infrastructures.

- May 2025: Broadcom Inc. revealed its third-generation co-packaged optics offering with 200G per lane throughput, which is an indication that the industry is ready for scaling up and out networks for the next generation of AI.

- March 2025: NVIDIA Corporation introduced Spectrum-X and Quantum-X silicon photonics networking switches capable of connecting millions of graphics processing units within AI factories, reducing energy usage and operational costs.

- March 2025: Marvell Technology, Inc. exhibited a 1.6T silicon photonics light engine to facilitate rack-scale interconnection in AI networks, accelerating the commercialization of optical modules and on-board optics.

- March 2025: Coherent Corp. released a silicon photonics-based 2x400G FR4 Lite optical transceiver for AI data centers and high-speed Ethernet networks.

- March 2025: Coherent Corp. also revealed a live demo of a silicon photonics-based 1.6T DR8 transceiver module employing Marvell optical DSP at OFC 2025.

- September 2025: Coherent Corp. initiated sampling of 400 mW continuous wave lasers suitable for use in co-packaged optics and silicon photonics systems.

- June 2024: Intel Corporation showed off its first fully-integrated optical I/O chiplet for scalable AI, indicating sustained progress towards photonics-based computer interconnects.

Why Choose DataM?

- Technological Innovations: Explores the latest advancements in silicon photonics design, including improved hydraulic systems, advanced operator controls, telematics integration, electric and hybrid powertrains and enhanced attachment versatility that are driving higher productivity and lower operating costs across construction and industrial applications.

- Product Performance & Market Positioning: Evaluates how different OEMs perform in real-world construction, landscaping, agriculture and municipal environments. The analysis compares lifting capacity, breakout force, fuel efficiency, durability, operator comfort and attachment compatibility, highlighting how leading manufacturers differentiate themselves globally.

- Real-World Evidence: Highlights practical use cases of silicon photonics across infrastructure development, road maintenance, warehouse handling and smart city projects. It demonstrates measurable improvements in jobsite efficiency, reduced labor dependency, faster material handling and optimized equipment utilization.

- Market Updates & Industry Changes: Tracks important industry developments such as new product launches, electrification initiatives, localized manufacturing expansions, tightening emission standards (Stage V, Tier 4 Final) and shifts in construction spending across major regions, including North America, APAC, China and India.

- Competitive Strategies: Analyzes how leading manufacturers are expanding their footprint through dealer network strengthening, localized production, electric model introductions, strategic partnerships and technology-driven differentiation such as AI-enabled monitoring and autonomous-ready platforms.

- Pricing & Market Access: Explains pricing structures across standard, high-capacity and electric skid steer models, including outright purchase, leasing and rental models. It also reviews regional availability, distribution networks and financing strategies that enhance market penetration.

- Market Entry & Expansion: Identifies growth opportunities in emerging economies driven by infrastructure development, urbanization, smart city programs and expanding rental ecosystems. It also outlines strategies for OEMs to scale operations globally through regional manufacturing hubs and after-sales service optimization.

Target Audience 2026

- Construction & Infrastructure Companies: EPC contractors, real estate developers, road construction firms and urban infrastructure agencies utilizing compact equipment for site preparation, excavation and material handling.

- Rental & Leasing Companies: Equipment rental providers expanding fleets to meet growing demand for compact, versatile machinery with high utilization rates.

- Agricultural & Landscaping Operators: Farm operators, orchard managers, landscaping firms and municipal maintenance departments using silicon photonics for multipurpose operations.

- Government & Municipal Authorities: Public works departments, urban development authorities and smart city mission teams responsible for infrastructure upgrades and maintenance.

- OEMs & Equipment Manufacturers: Global and regional construction equipment manufacturers seeking competitive intelligence, innovation benchmarking and regional expansion strategies.

- Investors & Private Equity Firms: Investment groups tracking growth in construction equipment manufacturing, rental markets and electrification of compact machinery.

- Dealers & Distribution Networks: Authorized distributors, service providers and aftermarket suppliers involved in sales, financing, spare parts and maintenance services.

Suggestions for Related Report

- Optical Interconnect in AI Data Centers Market

- Photonic Integrated Circuit (PIC) Market

- Photonics-Electronics Convergence Technology Market

- Optical Interconnect Market

- Photonics-Electronics Convergence Technology Market

- Photonics Market

- U.S. Optical Transceivers Market

- Optical Fiber Monitoring Market

- Optical Wavelength Services Market

- Li-Fi Market