Global Optical Interconnect in AI Data Centers Market Overview

AI infrastructure is no longer constrained by compute alone. Data movement has become the defining bottleneck, and this is precisely where the optical interconnect in AI data centers market is gaining strategic importance. As hyperscale operators scale GPU clusters into tens of thousands of nodes, optical connectivity is replacing copper at an accelerated pace to ensure bandwidth density, latency control, and power efficiency.

With over 80% of hyperscale data center links already transitioning to optical interconnects, this market is no longer emerging. It is becoming foundational infrastructure. Massive capital expenditure, nearly USD 200 billion in 2025 by leading hyperscalers, is directly translating into demand for high-speed optical modules, co-packaged optics, and silicon photonics.

From an investment standpoint, the timing is critical. The market is shifting from early adoption to large-scale standardization, where procurement decisions made today will define network architecture for the next decade.

Market Scope

| Metric | Details |

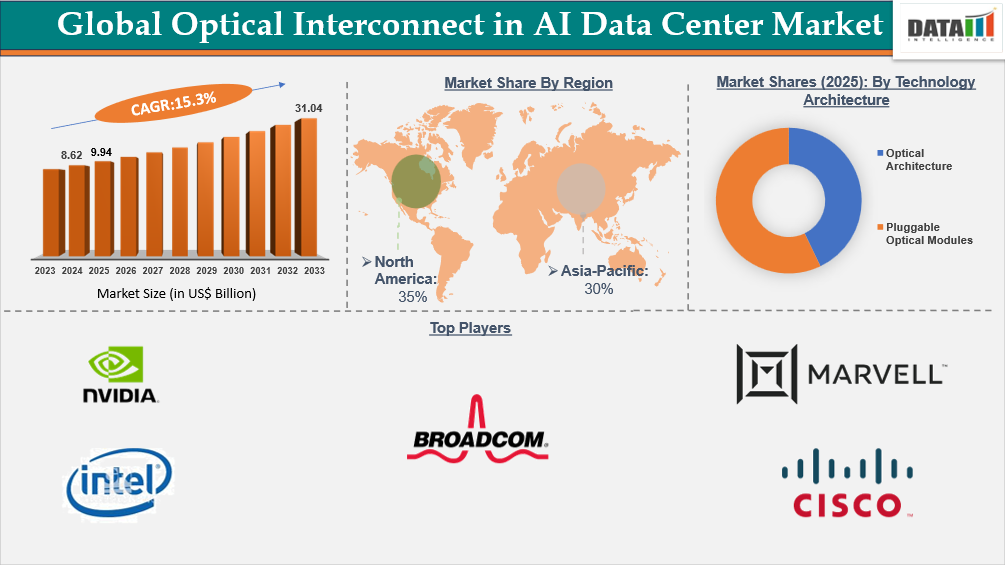

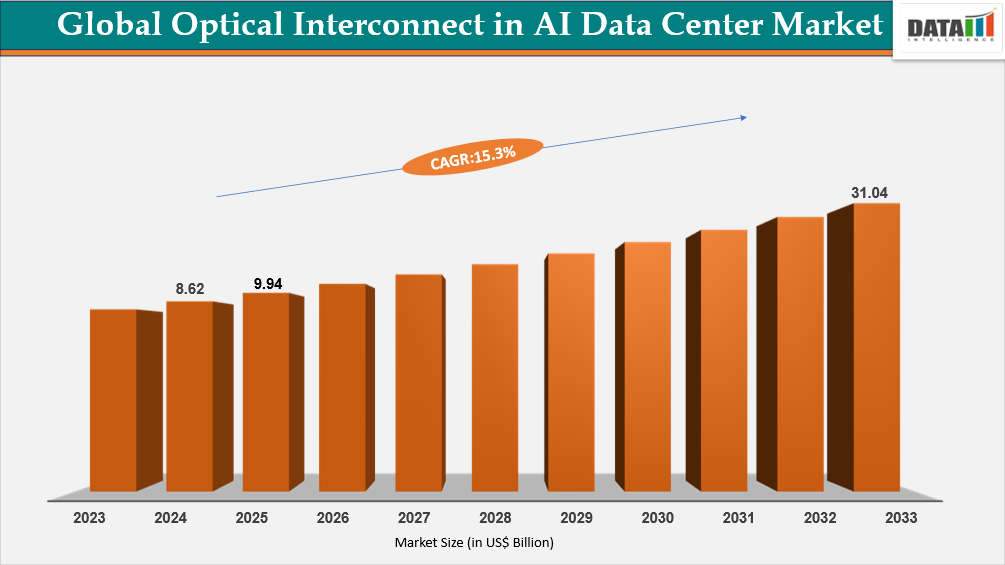

| Market Size (2025) | USD 9.94 Billion |

| Market Size (2035) | USD 41.09 Billion |

| CAGR | 15.30% |

| Historic Years | 2023–2024 |

| Base Year | 2025 |

| Forecast Period | 2026–2035 |

| Segments Covered | Technology Architecture, Interface Protocol, Bandwidth, Wavelength, Fiber Type, Distance |

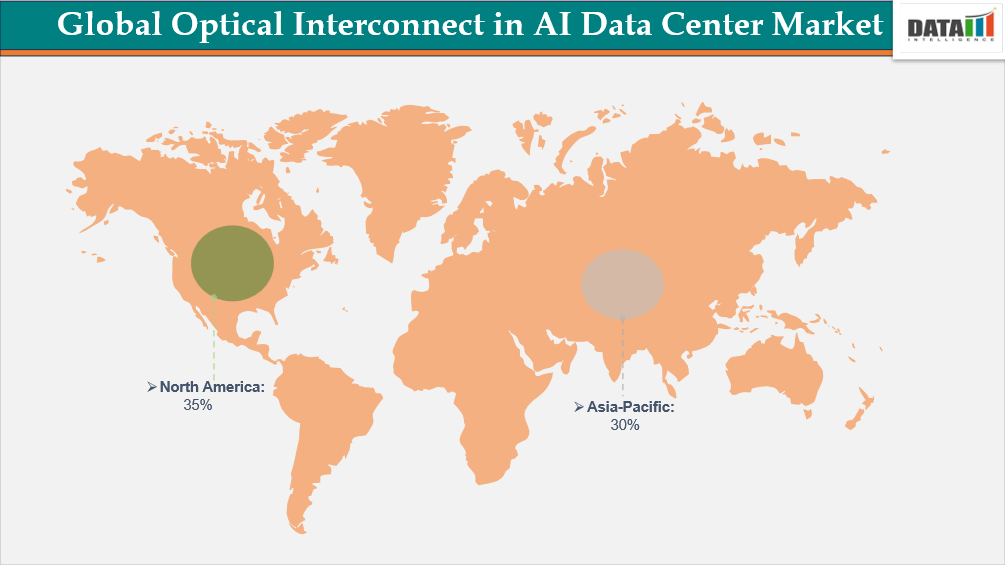

| Leading Region | North America |

| Fastest Growing Region | Asia-Pacific |

For More detailed Information, Request for Sample

Key Takeaways

- Optical interconnects have crossed the tipping point with 80%+ penetration in hyperscale data center links, signaling structural replacement of copper infrastructure.

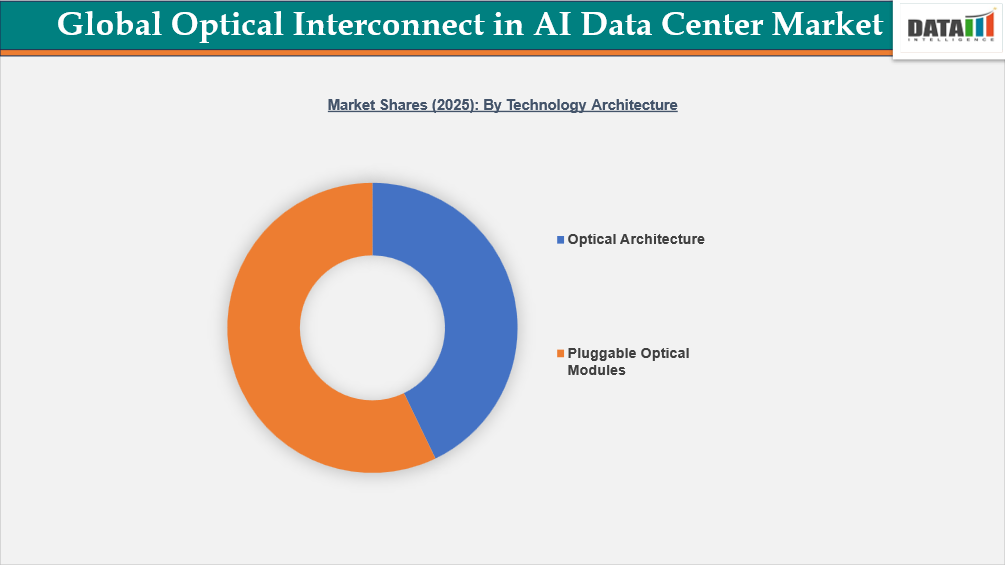

- Pluggable optical modules command 50% market share in 2025, reflecting strong preference for modular and upgradeable architectures.

- Co-packaged optics already account for 37%, indicating rapid adoption in high-performance AI clusters.

- Asia-Pacific holds 25 share and is the fastest-growing region, driven by aggressive infrastructure expansion in China and India.

- North America leads with 35% market share, supported by hyperscale cloud dominance and early adoption of advanced photonics.

- Hyperscaler capex growth of 40%+ in 2025 is directly accelerating optical interconnect deployment cycles.

- Power efficiency improvements of up to 70% in silicon photonics solutions are redefining total cost of ownership for operators.

Market Dynamics

Explosive Growth in AI and High-Performance Computing Demands

The rapid expansion of AI model training, GPU-intensive HPC workloads, and cloud-based AI services is driving strong demand for high-bandwidth, low-latency optical interconnects in data centers worldwide. Hyperscalers and enterprise customers are deploying pluggable optical modules and coherent transceivers to ensure scalable connectivity, energy efficiency, and consistent performance across multi-GPU and multi-node AI clusters. Advanced optical solutions are increasingly essential to support AI workloads that require massive throughput with minimal latency, which copper interconnects cannot efficiently provide.

For instance, in March 2025, Fujitsu, a Japan-based technology company, unveiled its 1FINITY P300 800G ZR/ZR+ coherent pluggable transceiver, designed for high-performance optical networking with reduced power per bit and scalable speeds. Fujitsu highlighted that rising AI and cloud workloads are driving the need for greater speed, capacity, and flexibility across data center networks. This launch demonstrates how next-generation optical interconnects are critical to supporting AI, HPC, and large-scale compute infrastructure, meeting the increasing bandwidth and latency demands of modern workloads.

Technical Complexity in Manufacturing and Assembly Processes

The optical interconnect market faces challenges due to technical complexity in manufacturing and assembly, particularly for high-speed pluggable modules and co-packaged optics. Producing advanced transceivers and silicon photonics solutions requires precise alignment, sophisticated DSP integration, and rigorous testing, which increases capital expenditure and production lead times. Some smaller suppliers struggle to scale production, causing hyperscale and enterprise customers to be cautious about long-term supply reliability and performance consistency.

The complexity makes companies favor established vendors and large-scale manufacturers with mature assembly lines and proven quality control. Extended fabrication cycles, supply chain bottlenecks for high-end components, and the need for advanced optical testing further constrain smaller players, limiting their ability to respond quickly to surges in AI and HPC demand. Customers increasingly rely on partners that can guarantee high-volume, low-defect production for mission-critical data center deployments.

Segmentation Analysis

The global optical interconnect in AI data center market is segmented based on technology architecture, interface protocol, aggregate bandwidth, wavelength technology, fiber type, reach or distance, and region.

Rising Demand for High-Speed, Energy-Efficient Pluggable Optical Modules in AI and Data Centers

Pluggable optical modules are seeing strong adoption with 50% share in market as AI and high-performance data centers demand high-bandwidth, low-latency interconnects for workloads like model training, real-time analytics, and HPC simulations. They offer modularity, interoperability, and energy efficiency, enabling dense multi-GPU and storage clusters to operate consistently. Hyperscale cloud providers, finance, media, and research sectors are increasingly deploying these modules to scale infrastructure while optimizing power and cost. The architecture ensures flexible upgrades and broad compatibility across servers and switches.

For instance, in December 2025, GIGALIGHT, a China-based optical transceiver manufacturer, introduced its 800G OSFP HYBRID optical interconnect portfolio, including OSFP-PHO DR8 and OSFP HYBRID PSM8-AOC modules. The HYBRID design reduces power by up to 30% and latency by roughly 50% versus full-DSP modules. The company also plans a 1.6T OSFP224 HYBRID module in Q2 2026, reflecting ongoing innovation. These launches highlight how pluggable optics continue to meet the performance and efficiency demands of next-generation AI data centers.

Growth in Co‑Packaged Optics (CPO) Fueled by AI Scalability and Interconnect Performance Needs

Co-Packaged Optics (CPO) is rapidly gaining adoption with 37% share as AI and high-performance computing workloads exceed the bandwidth and power limits of traditional optical and electrical links. By integrating photonic interconnects directly with switching ASICs and accelerator silicon, CPO enables ultra-high bandwidth, lower latency, and improved power efficiency. This architecture supports chip-to-chip communication across large AI clusters, making it critical for hyperscale data centers and enterprise HPC environments. Growing model sizes and compute fabrics are driving hyperscalers to adopt CPO for next-generation infrastructure.

For instance, in January 2026, Lightmatter, a U.S.-based photonic interconnect innovator, partnered with Global Unichip Corp. (GUC) to produce Passage™ 3D CPO solutions for AI hyperscalers. The collaboration combines Lightmatter’s photonic platform with GUC’s ASIC design to deliver high-bandwidth, energy-efficient interconnects for large AI workloads. These developments demonstrate a shift from prototypes to scalable, manufacturable CPO platforms, positioning CPO as the fastest-growing optical architecture in AI data centers.

Geographical Penetration

Rapid Digital and Telecom Expansion Fuels Optical Interconnect Growth in Asia-Pacific

The Asia‑Pacific region is the fastest-growing market with 30% share for optical interconnect technology, driven by rapid digital transformation, hyperscale data center expansion, and investments in 5G and AI infrastructure. Countries such as China, India, Japan, and South Korea are scaling cloud and telecom networks to support high-bandwidth, low-latency workloads in AI, HPC, and enterprise applications. The region’s growth is fueled by strong government programs and local manufacturing capacity for optical modules and photonic components.

For instance, in March 2025, Accelink Technology, a China-based optical transceiver company, upgraded its 1.6T OSFP224 optical transceiver at OFC 2025, featuring a 3 nm DSP for ultra-high-speed pluggable connectivity in AI and hyperscale data centers. The launch highlights the rapid adoption and production scaling by regional players like Accelink, Zhongji Innolight, and Eoptolink to meet surging demand across Asia‑Pacific.

China Optical Interconnects in AI Data Center Market Outlook

China is a major growth hub in the optical interconnect market as hyperscale cloud, telecom, and AI infrastructure investments accelerate demand for high‑bandwidth, low‑latency connectivity. Domestic companies are advancing production of advanced optical transceivers and silicon photonics to support AI, HPC, and cloud workloads that require scalable, energy‑efficient data transport solutions across data centers and network backbones. Government programs and optical ecosystem partnerships further support China’s rapid adoption of next‑generation interconnect technology.

For instance, in March 2025, Eoptolink Technology, a China‑based optical transceiver provider, launched its Gen2 1.6T OSFP and OSFP‑RHS transceiver family at OFC 2025, featuring 3 nm DSP‑enabled modules that improve power efficiency and support enhanced monitoring for ultra‑high‑speed applications. These cutting‑edge products demonstrate China’s focus on scaling local hardware innovation to meet surging demand from hyperscale and enterprise networks.

Japan Optical Interconnects in AI Data Center Market Trends

Japan is emerging as an important regional market for optical interconnects, driven by data center expansion, 5G deployment, and enterprise AI applications. Japanese operators and technology firms are focusing on energy-efficient, high-capacity optical solutions to enhance network scalability and sustainability. Investments in advanced optical modules and photonics integration are supporting next-generation computing and cloud workloads nationwide.

For instance, in October 2025, SoftBank Corp., Japan-based telecom operator, partnered with Cisco Systems G.K. to deploy an all-optical metro network in Osaka, delivering 400 GbE-capable links to support AI services and enterprise traffic. The project highlights Japan’s commitment to high-performance, low-power optical infrastructure with plans for nationwide expansion by 2027.

Rising Hyperscale Adoption of Performance-Intensive Workloads in North America

North America is the dominant region with 35% share in the global optical interconnect market, driven by hyperscale adoption of AI/ML, HPC, and real-time analytics workloads. Enterprises and cloud providers are expanding high-speed fiber and optical connectivity to meet growing demands for low-latency, high-bandwidth data transfer across AI clusters. Industries such as hyperscale cloud, finance, media, and scientific research rely on advanced optical solutions to efficiently scale compute-intensive operations and improve performance.

For instance, in January 2026, Amphenol, a U.S.-based interconnect solutions company, completed its acquisition of CommScope’s Connectivity and Cable Solutions (CCS) business, adding extensive fiber optic interconnect capabilities for data center, IT, and communications networks. The acquisition expands Amphenol’s portfolio and workforce, reinforcing North America’s leadership in deploying next-generation optical interconnects for large-scale AI, HPC, and cloud infrastructures.

U.S. Optical Interconnects in AI Data Center Market Insights

The U.S. remains a core growth hub for optical interconnects as enterprises and hyperscalers pursue high-bandwidth, low-latency AI and HPC workloads. Providers are integrating advanced silicon photonics and co-packaged optics into data centers to scale compute-intensive applications efficiently. Companies and cloud operators are investing heavily in next-generation optical modules and connectivity solutions to meet rising demand, particularly in hyperscale, finance, media, and scientific research sectors. This trend supports seamless deployment of large-scale AI clusters and high-performance computing infrastructure across the country.

For instance, in May 2025, AMD, a U.S.-based semiconductor company, acquired Enosemi, a photonic integrated circuit firm, to accelerate development of co-packaged optics (CPO) for AI systems. The acquisition strengthens AMD’s portfolio in energy-efficient, high-speed optical interconnects for chip-to-chip and data center networking. It highlights how U.S. companies are combining compute, photonics, and networking innovations to meet growing AI and HPC demands, reinforcing the region’s leadership in next-generation optical infrastructure.

Canada Optical Interconnects in AI Data Center Industry Growth

Canada is emerging as a key growth region in the optical interconnect market, driven by increasing demand for high-speed, low-latency connectivity in AI and data center workloads. Hyperscale cloud expansions, 400G/800G Ethernet adoption, and government-backed photonics R&D are supporting the development of energy-efficient, high-bandwidth optical solutions for HPC and enterprise applications. Canadian research centers and innovation hubs are actively advancing photonic integrated circuits to scale next-generation AI infrastructure.

For instance, in December 2025, Canada partnered with the U.K.’s CSA Catapult and C2MI to develop a co-packaged optical engine for AI data centers. The project combines Canadian photonics fabrication expertise with U.K. integration capabilities to deliver high-bandwidth, low-latency, and energy-efficient interconnects, highlighting Canada’s growing role in the global optical interconnect ecosystem.

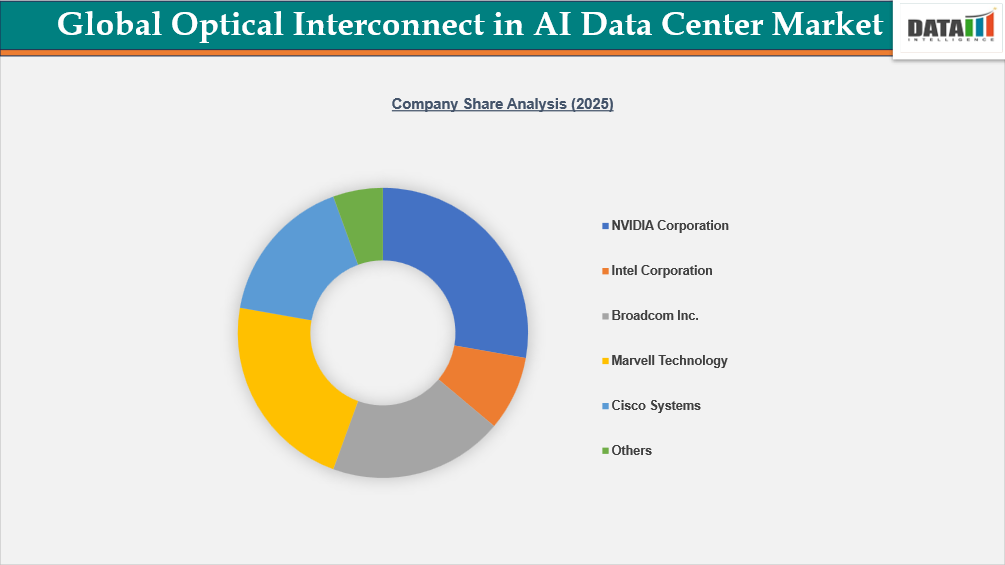

Competitive Landscape

- The global optical interconnect in AI data center market is characterized by a competitive landscape that includes both established and regional players.

- Key players include Oracle, IBM, Lumen Technologies, OVH SAS, Sparkoo Technologies Ireland Co. Limited, Pure Storage, Inc., Limestone Networks, Inc., Rackspace Technology, SAMSUNG SDS INDIA, Scaleway SAS and Zenlayer.

Regulatory and Policy Landscape

Governments across major regions are supporting photonics and semiconductor innovation through funding and infrastructure programs. Policies promoting energy-efficient data centers are indirectly accelerating adoption of optical interconnects.

Trade regulations and supply chain localization strategies are influencing sourcing decisions, particularly in Asia-Pacific and North America.

Strategic Insights and Analyst Perspective

The optical interconnect in AI data centers market is transitioning from component-level competition to platform-level integration. Companies that can combine photonics, compute, and networking into unified solutions will capture the highest value.

Key strategic priorities include:

- Investing in silicon photonics and co-packaged optics

- Building scalable manufacturing capabilities

- Strengthening partnerships with hyperscalers

- Focusing on energy efficiency as a core value proposition

Risk factors include supply chain constraints, high capital requirements, and rapid technology cycles.

Recent Developments

In June 2026, NVIDIA Corporation expanded its optical interconnect solutions for AI data centers with high-speed networking technologies. The initiative focuses on improving data transfer rates and reducing latency. This supports AI workload efficiency.

In May 2026, Intel Corporation strengthened its silicon photonics portfolio with advanced optical interconnects for hyperscale and AI-driven data centers. The development enhances bandwidth and energy efficiency. This benefits cloud providers.

In April 2026, Broadcom Inc. introduced next-generation optical interconnect components with higher data throughput and improved reliability. The development improves network performance. This supports large-scale data processing.

In March 2026, Marvell Technology, Inc. expanded its optical connectivity solutions for AI infrastructure with high-speed data transmission capabilities. The innovation focuses on scalability and performance. This supports data center growth.

Report Benefits

This report enables:

- Manufacturers to align product development with AI infrastructure demand

- Investors to identify high-growth segments and emerging technologies

- Suppliers to understand procurement trends and scale requirements

- Technology companies to position solutions within hyperscale ecosystems

- Strategy teams to evaluate long-term market entry and expansion plans

Why Choose DataM?

- Data-Driven Insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. This approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. This personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. These insights complement and go beyond what is typically available in generic databases.

Target Audience

- Data center operators and hyperscalers

- Optical component manufacturers

- Semiconductor and photonics companies

- Cloud service providers

- Investment firms and venture capitalists

- Enterprise IT and infrastructure teams