Robotaxi Market

Global Robotaxi Market Expected to Reach US$ 198.6 Billion by 2033

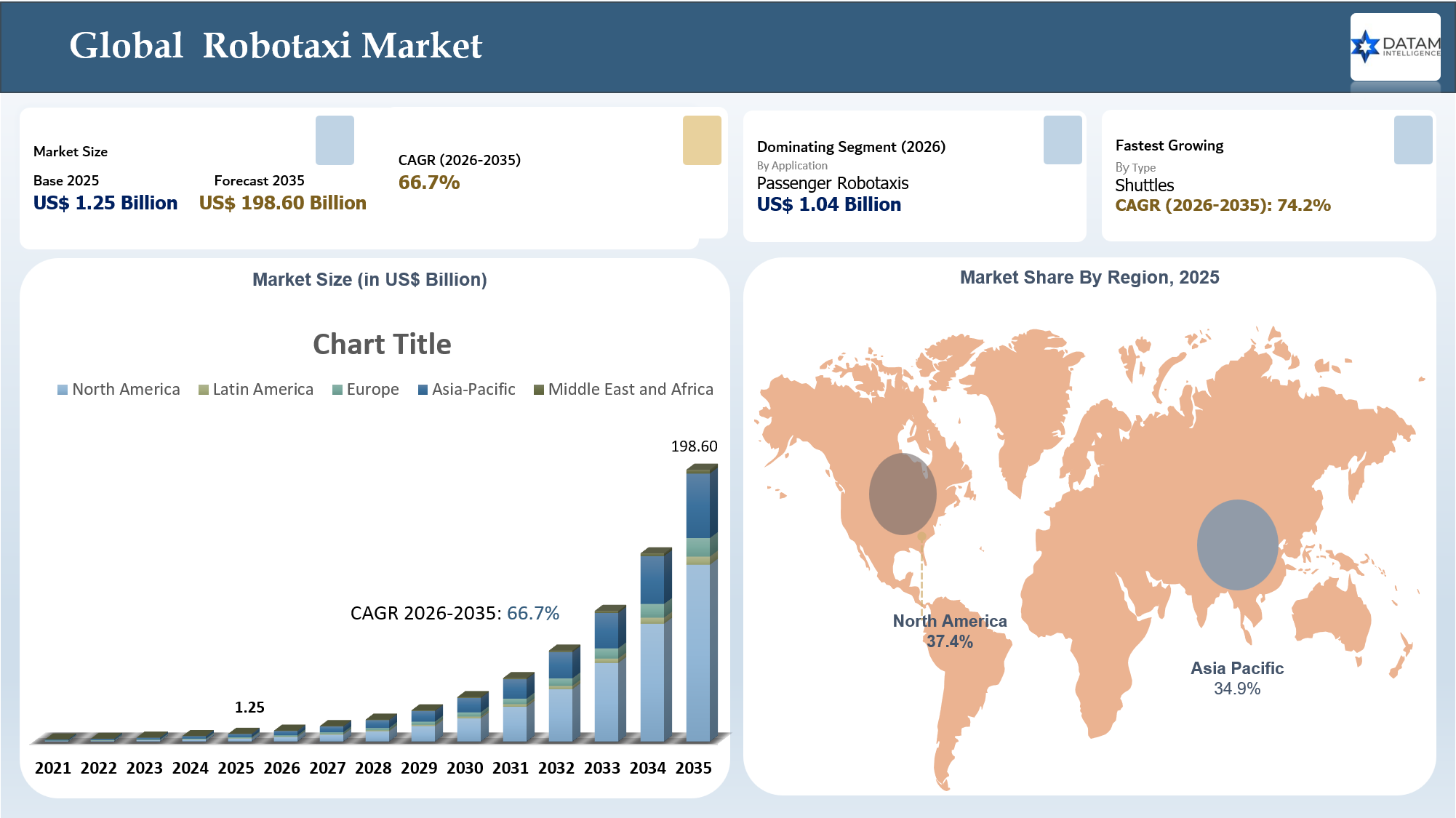

The global robotaxi market was valued at US$ 1.25 billion in 2025 and is projected to grow to US$ 198.6 billion by 2033, expanding at a CAGR of 66.7% during the robotaxi forecast period (2026–2035).

The Global Robotaxi Market is emerging as one of the fastest-growing segments within the autonomous mobility and intelligent transportation ecosystem, driven by rapid advancements in autonomous driving technology, artificial intelligence (AI), electric vehicles (EVs), and Mobility-as-a-Service (MaaS) platforms. Leading companies including Waymo, Tesla, Baidu Apollo Go, Pony.ai, WeRide, Zoox, and Motional are accelerating commercial deployments across the United States, China, Japan, South Korea, Germany, and the United Kingdom as governments expand regulatory frameworks for autonomous transportation.

As the industry transitions from pilot programs to large-scale commercialization, robotaxis are expected to reshape urban mobility economics by reducing transportation costs, improving fleet utilization, addressing driver shortages, and supporting smart city initiatives. This report provides comprehensive insights into robotaxi market size, share, growth forecasts, competitive landscape, technology trends, regulatory developments, investment opportunities, and strategic market outlook, enabling investors, automotive OEMs, technology providers, mobility operators, and policymakers to identify high-growth opportunities and make informed business decisions.

ROBOTAXI MARKET REPORT

Robotaxis are rapidly transforming the future of urban mobility by integrating autonomous driving technology, electric vehicles (EVs), artificial intelligence (AI), and smart transportation ecosystems. Governments, automotive OEMs, mobility startups, and technology giants are aggressively investing in fully autonomous ride-hailing services to reduce transportation costs, improve urban traffic efficiency, lower emissions, and address driver shortages.

The United States, China, Japan, South Korea and India are emerging as the most influential markets for robotaxi deployment due to increasing smart city investments, favorable autonomous vehicle regulations, rapid EV adoption, and rising demand for Mobility-as-a-Service (MaaS) platforms.

Robotaxi Market Executive Summary

The robotaxi industry is transitioning from pilot-stage deployment toward scalable commercial operations. Advances in AI-powered autonomous navigation, sensor fusion, high-definition mapping, 5G connectivity, and electric mobility are accelerating commercialization worldwide.

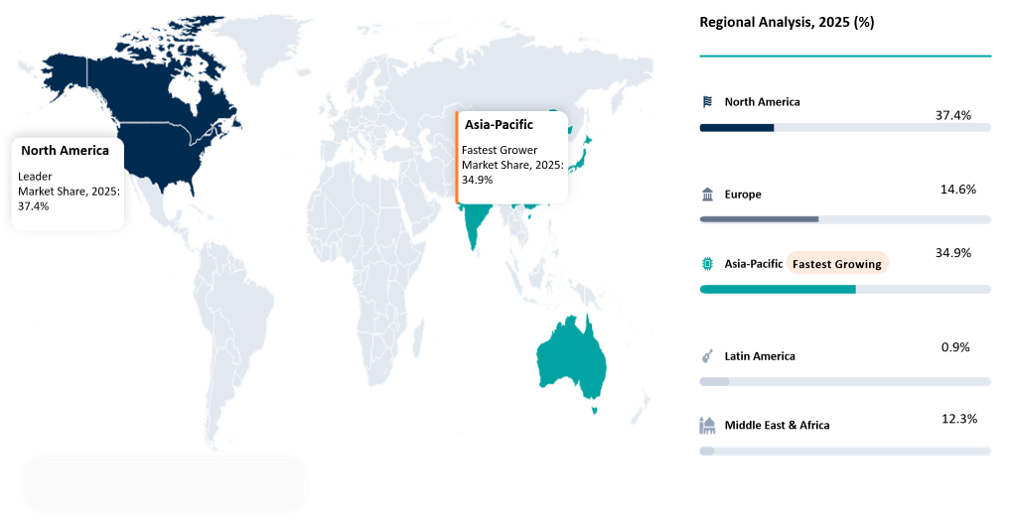

North America currently dominates the global market due to strong autonomous driving R&D investments and supportive testing environments. Asia-Pacific is projected to witness the fastest growth due to aggressive deployment activities in China, Japan, and South Korea.

The market is witnessing intense competition among technology firms, automotive OEMs, ride-hailing platforms, and AI startups aiming to establish leadership in autonomous urban transportation.

Key market participants are increasingly focusing on:

- Autonomous fleet scaling

- AI-driven navigation systems

- Safety validation frameworks

- Smart city integration

- Commercial ride-hailing partnerships

- Electric robotaxi ecosystems

- Subscription-based mobility services

Key Takeaways

- Asia-Pacific accounted for around 34.9% market share in 2025 and is projected to grow at the fastest CAGR of 70.3% through 2025 driven by Chinese regulations. China is developing a commercially aggressive regulation model. Its nationwide AV regulation was enacted on April 1, 2025, and city-specific commercial demonstration permits are appearing as Shanghai began granting permits in 2025, allowing companies like Baidu, Pony.ai to commercialize robotaxi services within tier-1 Chinese cities.

- North America held approximately 37.4% market share in 2025. Regulation is changing from are AVs allowed to "how quickly can fleets industrialize. NHTSA's 2025 AV Framework started the process of streamlining exemptions for non-traditional vehicles, and initiated rulemakings to update the Federal Motor Vehicle Safety Standards (FMVSS) for ADS vehicles, which is critical because pure ride-hailing vehicles with no steering wheel, pedals or mirrors require a regulatory pathway rather than simply city permission.

- However, transparency may be declining as deployment ramps up. NHTSA currently requires ADS/Level 2 systems to report crashes, but the 2025 changes and debates around reporting requirement imply a decrease in public visibility of AV failure modes as fleets grow.

- Dubai seeks to be the neutral international testbed. RTA granted trial permits/MOUs to Baidu, WeRide, Pony.ai in 2025, with targeted commercial driverless launch in 2026 making it the gateway for Chinese AV firms to conduct their business outside China.

- The vehicle race has moved beyond retrofitted EVs towards integrated designs. Zoox publicly tested a steer-wheel free vehicle in Las Vegas, the Tesla Cybercab and Lucid-Nuro-Uber's production-intent vehicle show the market is maturing towards vehicle-platform competition instead of just software stacks.

- Uber is quietly emerging as a de facto robotaxi operating system. Uber does not intend to build an AV stack but instead has partnered with many companies like Lucid/Nuro, WeRide, Wayve, Waabi etc., and is also using its existing manually driven rides for data collection for training its AVs. This has positioned Uber as the fleet-demand, data and ridership layer for robotaxis.

- 2026 deployments are concentrating around tourist-friendly, sun-belt states with flexible regulations. These cities like Las Vegas, Miami, Austin, Dubai, Atlanta and other cities in TX appear repeatedly due to high demand for services, permissive local regulations, mapping value and the general ease of operations (weather conditions in TX cities will eventually prove challenging).

- Actual maturity is diverging widely from claims of scale. Waymo is operating at nearly hundreds of thousands of rides per week, Zoox is still in early public testing/free pilot phase, Tesla operates with small fleets of cautiously tested vehicles and Chinese firms are expanding but are at high risk of systemic failure/outages. What we are seeing is that there is no "winner-takes-all" scenario yet, the market in 2026 will test reliability, city operations and public trust.

Robotaxi Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 1.25 Billion | |

| Market Size (2033) | US$ 198.6 Billion | |

| CAGR | 66.7% | |

| Base Year | 2025 | |

| Fastest Growing Region | Asia-Pacific | |

| Leading Technology | Level 4 Autonomous Driving | |

| Dominant Propulsion | Electric Vehicle | |

| Major Markets 2025 | USA, China, Saudi Arabia, UAE, Japan, UK, Croatia, Singapore | |

| Major Markets 2035 | USA, China, Japan, South Korea, Germany, UK, France | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Why Robotaxi Market Matters in 2026

The global transportation industry is undergoing a major technological transformation.

Robotaxis are expected to redefine urban mobility economics by reducing operational costs, eliminating driver dependency, improving road safety, and enabling highly scalable shared mobility ecosystems.

Several macroeconomic and technological factors are driving market growth:

- Rising urban congestion worldwide

- Growing demand for autonomous public transportation

- Expansion of smart city infrastructure

- Increasing EV adoption globally

- AI and machine learning advancements

- Improved sensor accuracy and declining lidar costs

- Government investments in autonomous mobility programs

- Transportation labor shortages

- Consumer demand for affordable ride-sharing services

The year 2026 is expected to represent a major commercialization milestone as several companies expand beyond pilot operations into large-scale autonomous ride-hailing deployments.

Robotaxi Market Drivers and Restraints

Drivers

Rapid Advancements in Autonomous Driving Technologies

Artificial intelligence, machine learning, lidar, radar, computer vision, and sensor fusion technologies are significantly improving autonomous driving capabilities. AI-powered navigation systems are enabling real-time decision-making and improving passenger safety.

Increasing Urban Mobility Challenges

Urban congestion, rising transportation costs, and inefficient public transit systems are driving demand for autonomous ride-sharing solutions.

Expansion of Electric Vehicle Infrastructure

Most robotaxi fleets are being developed using electric vehicle architectures due to lower operating costs, sustainability advantages, and favorable government incentives.

Government Support for Smart Mobility

Governments across the USA, China, Japan, South Korea, and Europe are supporting autonomous mobility pilots through regulatory sandboxes and smart city investments.

Restraints

Regulatory Uncertainty

Autonomous driving laws, liability frameworks, cybersecurity regulations, and safety approvals remain inconsistent across countries.

High Initial Deployment Costs

Advanced sensors, AI computing hardware, HD mapping systems, and fleet infrastructure continue to increase deployment costs.

Cybersecurity & Data Privacy Risks

Connected autonomous vehicles face growing concerns regarding cyberattacks, passenger data privacy, and software vulnerabilities.

Opportunities

Mobility-as-a-Service (MaaS)

Robotaxis are expected to become a major component of digital mobility ecosystems integrating ride-sharing, autonomous transportation, and subscription-based mobility platforms.

Emerging Markets Expansion

India, Southeast Asia, and Middle Eastern smart cities are expected to create high-growth opportunities over the next decade.

Autonomous Logistics Applications

Robotaxi technologies are increasingly being adapted for autonomous delivery, logistics, and last-mile transportation applications.

Robotaxi Market Trends

AI-Powered Fleet Optimization

Fleet operators are increasingly adopting predictive analytics and AI-based route optimization systems to improve operational efficiency.

Shift Toward Fully Electric Robotaxi Fleets

Sustainability initiatives and EV mandates are accelerating the deployment of fully electric autonomous fleets.

Strategic Partnerships Accelerating Commercialization

Technology firms, automotive manufacturers, and ride-hailing companies are collaborating to accelerate market entry.

Subscription-Based Autonomous Mobility Models

Companies are exploring monthly mobility subscription services to improve recurring revenue streams.

Expansion of Autonomous Ride-Hailing Zones

Several cities are increasing the size of autonomous operating zones as safety performance improves.

Robotaxi Market vs Autonomous Vehicle Market

| Metric | Robotaxi Market | Autonomous Vehicle Market |

|---|---|---|

| Purpose | Ride-hailing | Multiple applications |

| Growth Rate | Higher | Moderate |

| Deployment | Urban fleets | Broad vehicle categories |

| Key Companies | Waymo, Tesla | OEMs + Tech firms |

Robotaxi Market Technology Landscape

Core Technologies Powering Robotaxis

Artificial Intelligence & Deep Learning

AI algorithms enable object detection, path planning, passenger safety management, and real-time navigation.

Sensor Fusion Systems

Robotaxis combine lidar, radar, ultrasonic sensors, cameras, and GPS systems to achieve accurate environmental perception.

HD Mapping & Localization

High-definition maps provide centimeter-level accuracy for autonomous navigation.

5G Connectivity

Low-latency communication supports vehicle-to-everything (V2X) connectivity and cloud-based fleet coordination.

Edge Computing

Real-time data processing improves autonomous response times and reduces cloud dependency.

Global Robotaxi Market Regulatory Framework Analysis

United States - Autonomous Vehicle Regulatory Framework

The United States remains one of the most advanced markets for autonomous vehicle (AV) testing and commercial deployment. AV regulation is governed through a combination of federal safety oversight by the National Highway Traffic Safety Administration (NHTSA) and state-level deployment laws. States such as California, Arizona, Texas, and Florida permit commercial Level 4 robotaxi operations under geo-fenced environments and reporting-based compliance frameworks. This decentralized regulatory approach has enabled rapid testing and commercialization while maintaining safety oversight.

China - Autonomous Vehicle Regulatory Framework

China has accelerated robotaxi approvals through strong government-backed smart mobility initiatives and national AI development strategies. The country operates a centrally coordinated but city-executed regulatory framework, where municipalities issue testing, demonstration, and commercial operation permits. Cities including Beijing, Wuhan, Shanghai, and Shenzhen now allow paid fully driverless robotaxi services within designated government-supervised operating zones. This supportive regulatory environment has positioned China as a global leader in autonomous mobility deployment.

Japan – Autonomous Vehicle Regulatory Framework

Japan is prioritizing autonomous mobility solutions to address labor shortages, aging demographics, and transportation accessibility challenges. The government amended the Road Traffic Act and Road Transport Vehicle Act to permit Level 4 autonomous driving in designated operating areas. Japan's regulatory framework remains conservative and safety-focused, emphasizing remote monitoring, public safety validation, and phased commercialization. This measured approach supports innovation while maintaining public trust in autonomous technologies.

South Korea - Autonomous Vehicle Regulatory Framework

South Korea is making significant investments in AI-powered transportation infrastructure and autonomous driving research and development. The country operates a smart-city-oriented regulatory framework that includes designated autonomous driving zones and temporary operation permits for testing and deployment. Government-backed mobility innovation programs and urban pilot projects continue to support the commercialization of autonomous vehicles and robotaxi services across key metropolitan areas.

Germany – Autonomous Vehicle Regulatory Framework

Germany has established one of Europe's most advanced regulatory frameworks for autonomous driving through its 2021 Autonomous Driving Act. The legislation permits Level 4 autonomous vehicles to operate within defined operating areas, subject to strict safety and certification requirements. Operators must maintain technical supervision systems and comply with comprehensive regulatory standards. Germany's framework serves as a benchmark for autonomous vehicle regulation within the European Union.

United Kingdom - Autonomous Vehicle Regulatory Framework

The United Kingdom has introduced a comprehensive legal structure for self-driving vehicles through the Automated Vehicles Act. The framework establishes clear authorization procedures, safety requirements, and liability allocation mechanisms for autonomous vehicle operators and manufacturers. Government-supported pilot programs are facilitating commercial robotaxi deployment, with broader commercialization expected as the regulatory ecosystem continues to mature.

France - Autonomous Vehicle Regulatory Framework

France permits autonomous vehicle operations under tightly controlled regulatory approvals, with a primary focus on public transportation services and autonomous shuttle pilots. The framework emphasizes rigorous safety validation, operator oversight, and controlled deployment environments before wider commercialization. France's gradual approach aims to ensure safe integration of autonomous mobility solutions into urban transportation networks while supporting long-term innovation.

Value Chain Analysis

The robotaxi market value chain includes:

- Sensor Manufacturers

- AI Software Developers

- Automotive OEMs

- EV Battery Suppliers

- HD Mapping Providers

- Connectivity Providers

- Fleet Operators

- Ride-Hailing Platforms

- Smart City Infrastructure Providers

- End Users

Porters Five Forces

| Metrics | Details |

| Threat of New Entrants | Moderate |

| Bargaining Power of Suppliers | High |

| Bargaining Power of Buyers | Moderate |

| Threat of Substitutes | Moderate |

| Competitive Rivalry | Very High |

The robotaxi industry remains highly competitive due to rapid innovation cycles and aggressive investment activity.

Pricing Analysis

Robotaxi deployment costs vary significantly depending on:

- Sensor configuration

- Autonomous software complexity

- EV battery capacity

- Fleet size

- Geographic operating environment

- Regulatory compliance requirements

Average robotaxi deployment costs currently remain higher than traditional ride-sharing fleets, but long-term operating economics are expected to improve significantly through driverless operations.

Segment Analysis

By Vehicle Type

- Cars

- Shuttles

- Vans

Cars Segment Dominates the Market

Passenger autonomous cars account for the largest market share due to increasing urban ride-hailing demand and large-scale deployment programs.

By Propulsion

- Electric Vehicle (EV)

- Hybrid Vehicle

- Fuel Cell Vehicle

- ICE Vehicles

Electric Vehicle Segment Leads Market Growth

Electric robotaxis dominate due to lower maintenance costs, government incentives, and sustainability targets.

By Level of Autonomy

- Level 3

- Level 4

- Level 5

Level 4 Segment Holds Largest Share

Level 4 autonomous systems currently represent the most commercially viable technology for urban robotaxi deployment.

By Application

- Passenger Transportation

- Shared Mobility

- Logistics & Delivery

Passenger Transportation Leads Revenue Generation

Urban ride-hailing applications continue to dominate commercial deployment activities.

Regional Market Analysis

North America Robotaxi Market

North America remains the dominant market due to strong AI innovation ecosystems, regulatory support, and aggressive commercial testing.

The United States leads the regional market through major companies including Waymo, Cruise, Tesla, Zoox, and Motional.

Major deployment cities include:

- San Francisco

- Phoenix

- Austin

- Las Vegas

- Los Angeles

Asia-Pacific Robotaxi Market

Asia-Pacific is expected to register the fastest CAGR during the forecast period.

China leads large-scale commercial deployment activities through companies such as Baidu Apollo Go, Pony.ai, and WeRide.

Japan, Singapore and South Korea are rapidly investing in autonomous transportation infrastructure.

India represents a major future growth opportunity due to:

- Smart city projects

- EV ecosystem expansion

- Urban mobility demand

- AI startup growth

Europe Robotaxi Market

Europe is witnessing growing adoption supported by sustainability regulations and smart mobility investments.

Germany, France, and the UK are leading autonomous mobility pilot programs. But Croatia and Switzerland have passed regulatory approvals quickly and have surged in robotaxi adoption.

Latin America Market Outlook

Latin America is gradually exploring autonomous mobility through urban transportation modernization initiatives although regulations and pilot programs lag behind other regions.

Middle East & Africa Market Outlook

Middle Eastern smart city developments are expected to create long-term robotaxi deployment opportunities. Saudi Arabia and UAE are already entrenched in pilot programs and robotaxi adoption.

Competitive Landscape

The robotaxi market is highly competitive and innovation-intensive.

- Major players are focusing on:

- AI software development

- Autonomous safety validation

- Fleet scaling

- Strategic partnerships

- International expansion

- EV integration

Key Companies

- Waymo

- Tesla

- Baidu Apollo Go

- Cruise

- Pony.ao

- WeRide

- Motional

- AutoX

- Zoox

- DiDi

- Mobileye

- Uber

- Lucid

- Nuro

- Verra Mobility

- MOAI

- Grab

- Bolt Go

- Kakao

- Mav Mobility

Competitor Benchmarking

| Company | Core Strength | Deployment Focus | Competitive Advantage |

| Waymo | Autonomous software | USA | Advanced AI driving stack |

| Baidu Apollo Go | Large-scale deployment | China | Smart city integration |

| Tesla | Vision-based autonomy | Global | FSD ecosystem |

| Cruise | Urban ride-hailing | USA | GM manufacturing support |

| Pony.ai | Cross-border expansion | USA & China | Multi-scenario autonomy |

| Motional | Ride-hailing integration | USA & Asia | Strategic partnerships |

| Zoox | Purpose-built robotaxis | USA | Vehicle design innovation |

| Company | Core Strength | Deployment Focus | Competitive Advantage |

How Big is the Robotaxi Market?

The global robotaxi market is emerging as one of the most dynamic segments within the future mobility ecosystem, supported by rapid advancements in autonomous driving technology, artificial intelligence, and connected vehicle infrastructure. Commercial deployments are expanding across major urban centers as autonomous ride-hailing services move beyond pilot programs and into large-scale operational environments.

Robotaxi market growth is being driven by significant investments from automotive manufacturers, autonomous technology developers, and mobility service providers seeking to reduce transportation costs and improve urban mobility efficiency. Companies such as Waymo, Tesla, Baidu Apollo Go, Pony.ai, and WeRide are accelerating the commercialization of robotaxi services through continuous improvements in autonomous software, sensor technologies, and fleet management systems.

North America currently accounts for a substantial share of global market activity, supported by advanced autonomous vehicle testing frameworks and strong investment in smart transportation initiatives. At the same time, Asia-Pacific is emerging as the fastest-growing regional market, led by large-scale deployments in China and increasing government-backed autonomous mobility programs in Japan, South Korea, and India.

As regulatory frameworks mature and consumer acceptance increases, robotaxis are expected to play a central role in the future of Mobility-as-a-Service (MaaS), creating significant opportunities across ride-hailing, public transportation, airport transfers, and last-mile mobility applications. The market's long-term expansion is expected to be supported by the convergence of autonomous driving, electrification, and AI-powered transportation networks.

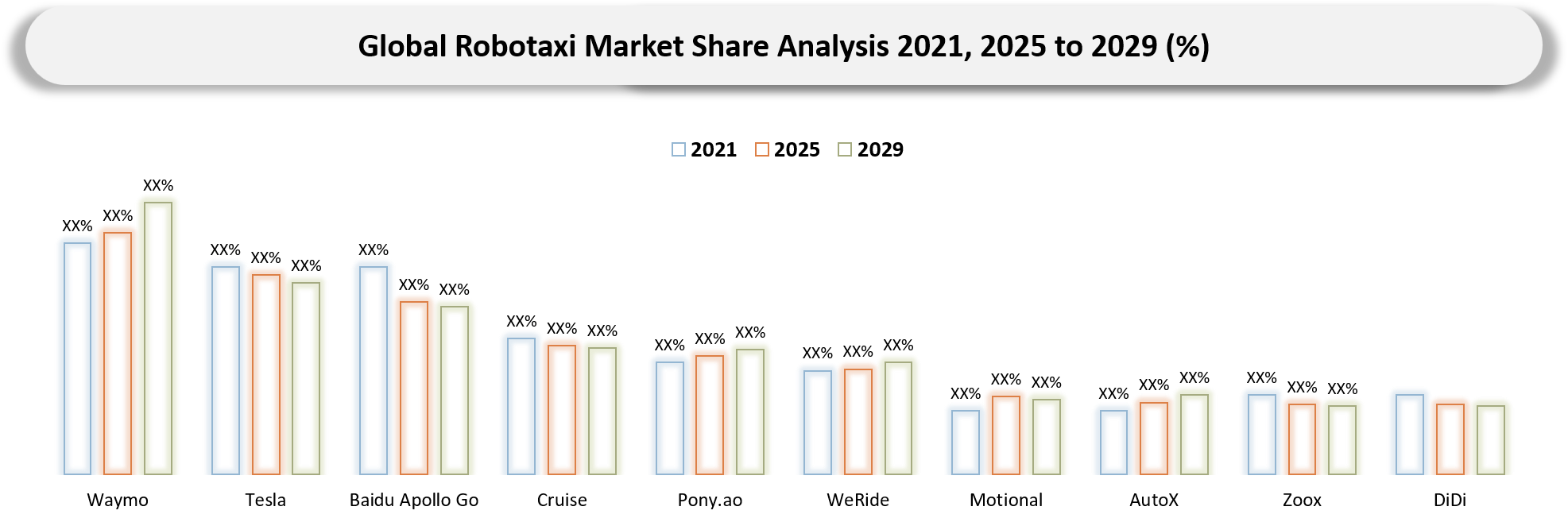

Robotaxi Market Share Analysis

The robotaxi market remains highly competitive, with market share influenced by autonomous driving maturity, commercial deployment scale, regulatory approvals, fleet expansion strategy, technology partnerships, and geographic presence. Unlike traditional automotive markets, robotaxi market share is not determined only by vehicle sales, but also by ride volume, operational cities, autonomous miles driven, platform partnerships, and fleet utilization.

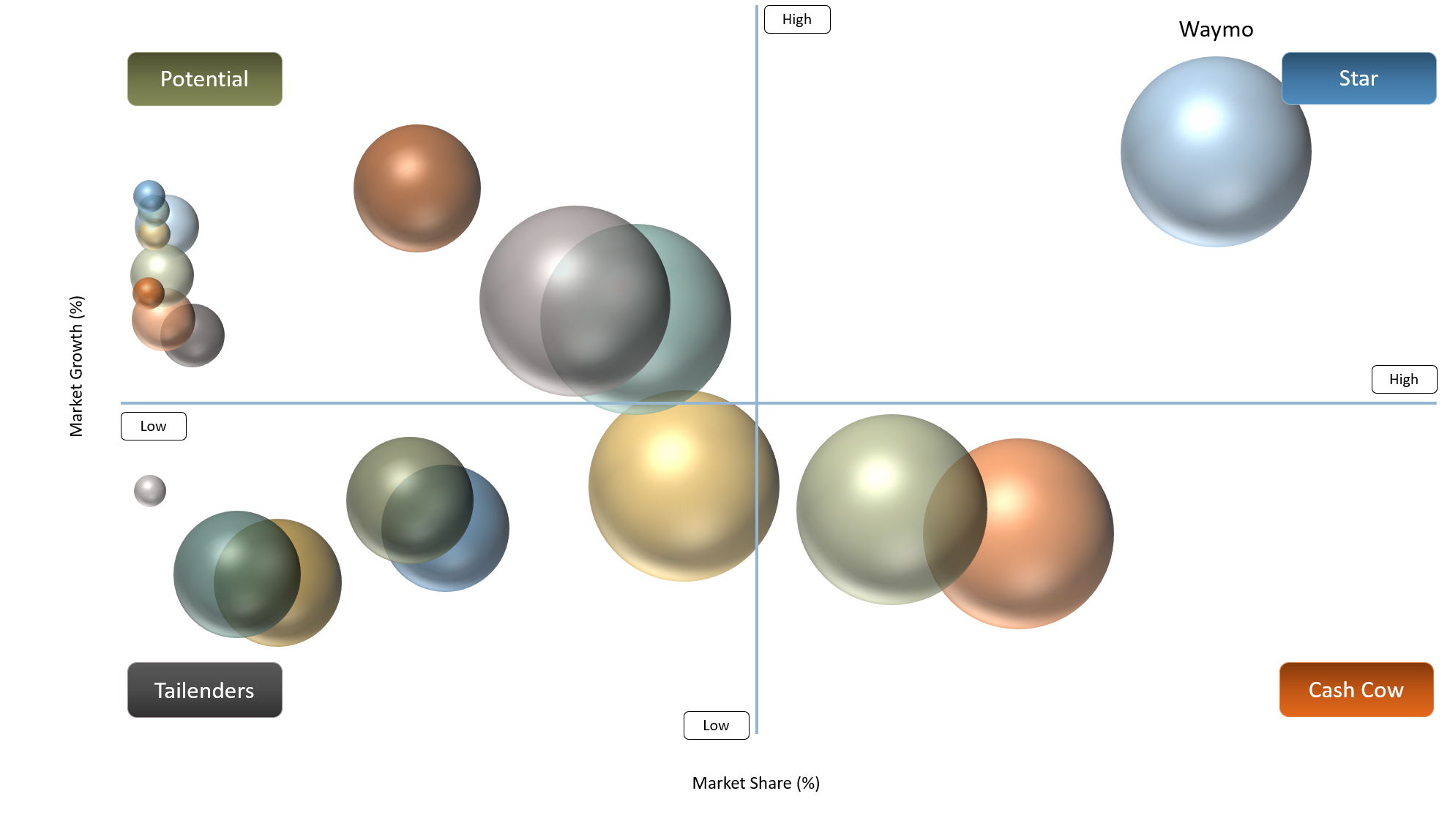

Waymo currently holds a leading position in the robotaxi market, supported by its large-scale commercial operations in the United States, advanced autonomous driving software, and expanding deployment across key urban markets. The company has built strong operational expertise through years of real-world autonomous driving experience and continues to strengthen its leadership through partnerships and city-level expansion.

Baidu Apollo Go is one of the strongest players in China’s robotaxi market, benefiting from government-backed smart mobility initiatives, large-scale urban deployment, and strong integration with China’s autonomous driving ecosystem. The company’s growing commercial presence in cities such as Wuhan, Beijing, Shanghai, and Shenzhen positions it as a major global competitor.

Tesla is emerging as a high-impact competitor in the robotaxi industry due to its large connected vehicle base, camera-based autonomous driving strategy, Full Self-Driving software development, and planned robotaxi commercialization. While Tesla’s robotaxi operations remain in an early stage compared to Waymo and Baidu, its global vehicle scale and software-driven business model could significantly influence future market competition.

Pony.ai and WeRide are also gaining market relevance through commercial permits, cross-border expansion, and autonomous mobility partnerships. These companies are expanding across China, the United States, and the Middle East, making them important challengers in the global robotaxi market.

Zoox is differentiating itself through purpose-built autonomous vehicles designed specifically for robotaxi services. Its vehicle architecture, which does not rely on traditional steering wheels or pedals, reflects the industry’s shift from retrofitted electric vehicles toward dedicated autonomous mobility platforms.

Overall, the robotaxi market is still in an early commercialization phase, and no single company has achieved dominant global market control. Future market share will depend on safety performance, regulatory approvals, cost efficiency, ride-hailing partnerships, fleet scalability, and consumer trust.

Robotaxi Market Share Positioning by Company

| Company | Market Position | Key Strength | Primary Deployment Focus |

|---|---|---|---|

| Waymo | Market Leader | Advanced autonomous driving stack and commercial deployment experience | United States |

| Baidu Apollo Go | Strong Challenger | Large-scale China deployment and smart city integration | China |

| Tesla | Emerging Disruptor | Software ecosystem, connected vehicle fleet, and FSD development | United States / Global |

| Pony.ai | Challenger | Multi-city deployment and regulatory approvals | China and United States |

| WeRide | Challenger | International expansion and autonomous mobility partnerships | China and Middle East |

| Zoox | Niche Innovator | Purpose-built robotaxi vehicle design | United States |

| Motional | Strategic Player | Ride-hailing partnerships and AV technology development | United States and Asia |

| AutoX | Regional Player | Autonomous driving technology and China deployment experience | China |

| Cruise | Rebuilding Player | Urban autonomous ride-hailing experience and OEM backing | United States |

| Mobileye | Technology Enabler | ADAS, autonomous driving systems, and OEM partnerships | Global |

Global Robotaxi Deployment Statistics

Global robotaxi deployment is accelerating as autonomous vehicle companies move from pilot testing toward controlled commercial operations. Deployment activity is currently concentrated in countries with supportive autonomous vehicle regulations, strong AI ecosystems, smart city investments, and high urban mobility demand. The United States and China remain the two most active robotaxi deployment markets, while Japan, South Korea, the United Arab Emirates, Germany, France, and the United Kingdom are advancing through pilot programs, regulatory sandboxes, and controlled operating zones.

The United States leads in commercial robotaxi operations, driven by companies such as Waymo, Tesla, Zoox, and Motional. Key deployment cities include Phoenix, San Francisco, Los Angeles, Austin, Las Vegas, and Atlanta, where robotaxi operators are expanding service areas and testing scalable autonomous ride-hailing models.

China is rapidly expanding robotaxi deployment through city-level permits and government-supported smart mobility programs. Baidu Apollo Go, Pony.ai, WeRide, AutoX, and DiDi are among the major companies operating or testing robotaxi services across Beijing, Wuhan, Shanghai, Shenzhen, Guangzhou, and other major urban centers.

The Middle East is emerging as an international robotaxi testbed, especially in Dubai and Abu Dhabi, where government authorities are supporting autonomous mobility pilots and partnerships with Chinese and global robotaxi companies. Europe is progressing more gradually, with Germany, France, and the United Kingdom focusing on safety validation, public transportation pilots, and regulatory readiness before wider commercial deployment.

Global Robotaxi Deployment Overview

| Company | Key Deployment Markets | Major Cities / Regions | Deployment Status |

| Waymo | United States | Phoenix, San Francisco, Los Angeles, Austin, Atlanta | Commercial operations |

| Baidu Apollo Go | China, UAE | Beijing, Wuhan, Shanghai, Shenzhen, Dubai | Commercial and expansion phase |

| Tesla | United States | Austin and selected U.S. markets | Early commercial / pilot phase |

| Pony.ai | China, United States, Middle East | Beijing, Guangzhou, Shenzhen, California, Dubai | Commercial and pilot operations |

| WeRide | China, UAE, Singapore | Guangzhou, Abu Dhabi, Dubai, Singapore | Commercial and pilot operations |

| Zoox | United States | Las Vegas, San Francisco, Austin, Miami | Pilot / early deployment phase |

| Motional | United States and Asia | Las Vegas and selected ride-hailing markets | Pilot and partnership-led deployment |

| AutoX | China | Shenzhen, Shanghai, Guangzhou | Pilot and commercial testing |

| Cruise | United States | San Francisco and selected U.S. cities | Rebuilding / limited operations |

| DiDi Autonomous Driving | China | Shanghai, Guangzhou and selected Chinese cities | Pilot and testing phase |

| Mobileye | Global | Europe, Middle East, and selected global markets | Technology partnership model |

Robotaxi deployment is expected to expand significantly over the forecast period as regulatory approvals improve, autonomous driving systems become more reliable, and fleet operating economics strengthen. Cities with favorable weather conditions, high ride-hailing demand, smart infrastructure investment, and flexible autonomous vehicle regulations are expected to become the first major robotaxi commercialization hubs.

Robotaxi Market Investment & Funding Analysis

Global investments in autonomous mobility continue to increase significantly.

Major funding areas include:

- AI mobility platforms

- Autonomous fleet software

- EV integration technologies

- Sensor manufacturing

- HD mapping

- Smart transportation infrastructure

Mergers, acquisitions, and strategic alliances are expected to intensify over the next decade.

Strategic Recommendations

For Automotive OEMs

- Accelerate AI and EV integration

- Build strategic autonomous partnerships

- Expand autonomous fleet pilot programs

For Investors

- Focus on scalable AI mobility platforms

- Monitor regulatory advancements closely

- Evaluate long-term fleet economics

For Governments

- Develop autonomous safety frameworks

- Expand smart mobility infrastructure

- Encourage EV charging network expansion

Analyst View

DataM Intelligence Analyst Perspective

The robotaxi market is evolving from a technology validation phase into a commercially scalable mobility ecosystem.

The long-term success of the robotaxi market will depend on:

- Regulatory approvals

- Public safety confidence

- AI reliability improvements

- Fleet operating economics

- EV charging infrastructure expansion

- Strategic mobility partnerships

- Smart transportation integration

The United States continues to lead technological innovation, while China dominates commercial deployment volume. Japan and South Korea are accelerating adoption to address aging populations and mobility efficiency challenges. India is emerging as a high-potential future market supported by smart city investments, growing EV adoption, and AI-driven transportation initiatives.

Companies capable of integrating autonomous software, EV platforms, real-time analytics, and scalable fleet operations will gain significant competitive advantages over the next decade.

Why Buy This Robotaxi Report?

This report helps organizations:

- Understand future autonomous mobility trends

- Identify high-growth investment opportunities

- Benchmark competitors effectively

- Analyze regulatory environments

- Optimize market entry strategies

- Evaluate technology disruptions

- Assess regional growth potential

- Track AI-driven transportation developments

What’s Included in the Robotaxi Report?

The report provides:

- Market size & forecast analysis

- Regional growth outlook

- Competitive intelligence

- Technology benchmarking

- Pricing analysis

- Regulatory assessment

- Supply chain insights

- Market share analysis

- Investment landscape analysis

- Strategic recommendations

- Emerging trends analysis

- Company profiling

Who Should Buy This Report?

This robotaxi report is ideal for:

- Automotive manufacturers

- EV companies

- Autonomous vehicle startups

- Mobility-as-a-Service providers

- Venture capital firms

- Institutional investors

- Transportation authorities

- AI technology companies

- Smart city planners

- Market intelligence teams

- Government agencies

Key Benefits for Stakeholders

Gain actionable market intelligence:

- Understand future mobility disruptions

- Analyze global deployment strategies

- Evaluate technology innovation trends

- Identify strategic growth opportunities

- Benchmark market competitors

- Improve investment decision-making

Future Outlook of the Robotaxi Industry Beyond 2035

The future outlook of the robotaxi industry beyond 2035 remains highly promising as autonomous mobility continues to evolve from pilot deployments to mainstream transportation networks. Advancements in artificial intelligence, machine learning, sensor technologies, and vehicle-to-everything (V2X) communication are expected to significantly improve the safety, efficiency, and scalability of robotaxi operations worldwide.

Beyond 2035, Level 4 and Level 5 autonomous vehicles are anticipated to become increasingly common across major urban centers, reducing dependence on human drivers and transforming the economics of ride-hailing services. Robotaxi fleets are expected to play a critical role in addressing urban congestion, lowering transportation costs, and improving mobility accessibility for elderly and disabled populations.

The integration of robotaxis with smart city infrastructure is likely to create a connected transportation ecosystem where autonomous vehicles communicate seamlessly with traffic management systems, public transit networks, and digital mobility platforms. Such developments could enable real-time route optimization, reduced travel times, and lower energy consumption across urban transportation systems.

Electric vehicles are expected to remain the preferred platform for robotaxi fleets due to their lower operating costs, reduced maintenance requirements, and alignment with global sustainability goals. As battery technologies continue to improve, robotaxi operators may achieve longer vehicle range, faster charging capabilities, and enhanced fleet utilization rates.

The growing adoption of Mobility-as-a-Service (MaaS) models is also expected to reshape consumer transportation preferences. Instead of owning personal vehicles, many consumers may increasingly rely on autonomous ride-hailing subscriptions that provide convenient, affordable, and on-demand transportation solutions. This shift could contribute to declining vehicle ownership rates in densely populated metropolitan regions.

Furthermore, advances in AI-powered fleet management systems are expected to improve demand forecasting, predictive maintenance, and operational efficiency. Autonomous fleet operators may leverage real-time data analytics to optimize vehicle deployment, minimize downtime, and maximize profitability.

While regulatory challenges, cybersecurity concerns, and public acceptance remain important considerations, continued technological innovation and supportive government policies are expected to accelerate robotaxi adoption over the long term. As autonomous transportation ecosystems mature, the robotaxi industry is projected to become a fundamental component of future urban mobility, supporting safer, smarter, and more sustainable transportation networks worldwide.

Latest Developments

- Amazon-owned Zoox officially launched its public robotaxi service on the Las Vegas Strip in September 2025, marking one of the first commercial deployments of a purpose-built autonomous taxi without steering wheels or pedals. The service operated through the Zoox mobile app and focused on high-density tourist corridors, giving the company a real-world commercialization platform ahead of expansion into San Francisco, Austin, and Miami.

- In June 2025, Waymo launched paid autonomous ride-hailing operations in Atlanta tIn March 2025hrough the Uber app, expanding its U.S. footprint into a fifth major city. The deployment covered roughly 65 square miles and reflected Waymo’s strategy of integrating with established ride-hailing platforms instead of building a standalone consumer ecosystem in every market.

- In March 2025, Baidu’s Apollo Go signed a strategic agreement with Dubai’s Roads and Transport Authority (RTA) to deploy autonomous robotaxis in the UAE. The project planned an initial rollout of 100 fully autonomous vehicles by the end of 2025, scaling toward 1,000 vehicles over several years, making Dubai one of the most aggressive international robotaxi expansion markets outside China and the U.S.

- Tesla launched fully unsupervised robotaxi rides in Austin, Texas in January 2026 using Model Y vehicles without a human safety driver in the front seat. The pilot represented Tesla’s first real commercial robotaxi operation and tested its camera-only Full Self-Driving architecture in live urban environments, though the deployment remained geographically limited and closely monitored. However, latest news suggests the company may potentially be winding down its robotaxi production.

- In July 2025, Uber announced a major partnership with Lucid Motors and Nuro to deploy more than 20,000 autonomous robotaxis over six years. The program combined Lucid Gravity EVs, Nuro’s Level 4 autonomy stack, and Uber’s ride-hailing network into a vertically integrated robotaxi platform, signaling a broader industry shift toward partnerships rather than fully in-house AV ecosystems.

Conclusion

The global robotaxi market is poised for significant long-term transformation as autonomous driving technologies, artificial intelligence, electric mobility, and smart transportation ecosystems continue to evolve.

Governments and enterprises worldwide are prioritizing autonomous urban mobility to improve transportation efficiency, reduce emissions, and support next-generation smart city initiatives.

Companies capable of integrating AI innovation, scalable fleet operations, EV ecosystems, and regulatory compliance are expected to emerge as long-term leaders in the future mobility economy.

The robotaxi market is expected to become one of the most disruptive sectors within the global transportation industry over the next decade.

Related Reports:

Explore More Future Mobility & Autonomous Vehicle Reports

Self-Driving Cars Market

Electric Vehicle Market

Artificial Intelligence Market

Connected Cars Market

EV Charging Infrastructure Market

Vehicle-to-Everything (V2X) Communication Market