Self-Driving Cars Market Overview

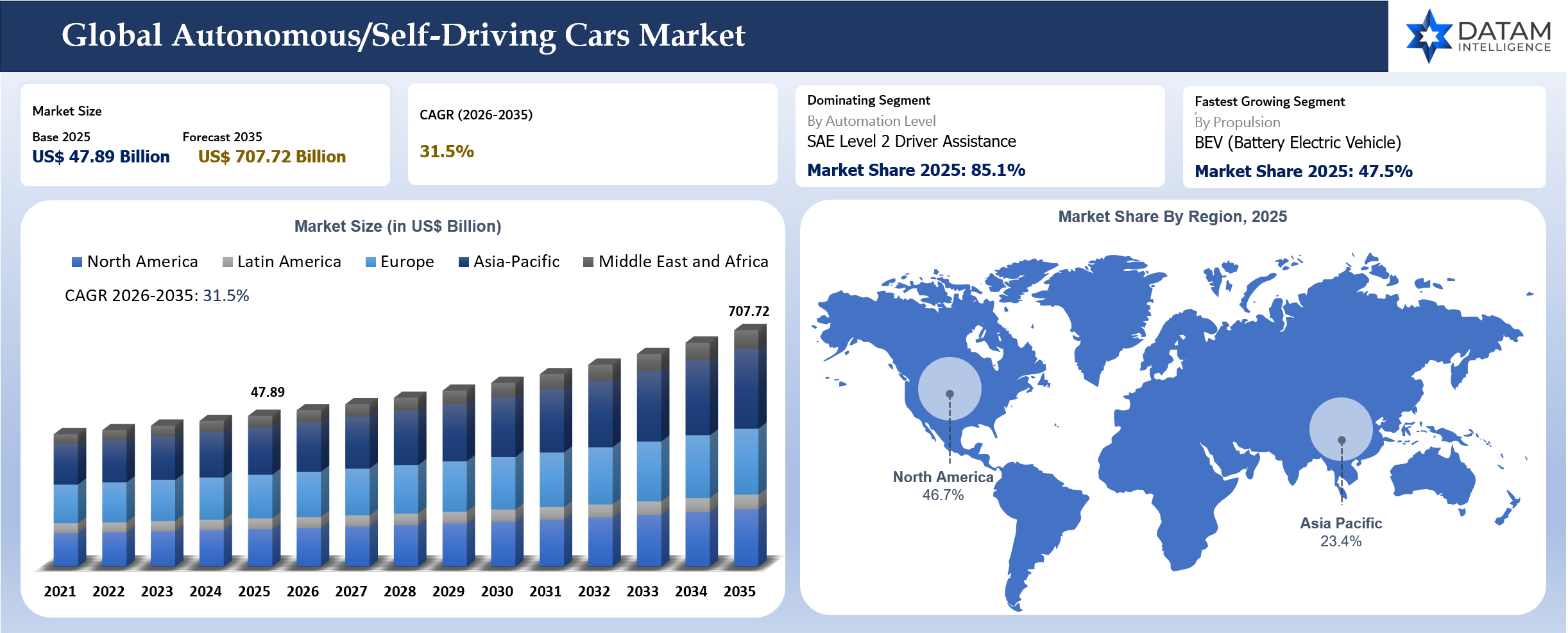

The global self-driving car market reached US$ 47.89 billion in 2025 and is expected to reach US$ 707.72 billion by 2035, growing with a CAGR of 31.5% during the forecast period 2026-2035. The market is entering a more selective and commercially disciplined phase. Earlier industry expectations treated autonomy as a broad transition that would move quickly from driver assistance to fully driverless vehicles. Current adoption is more practical. Automakers are scaling L2 (Level 2) supervised systems across passenger cars, a smaller number of premium OEMs are deploying L3 (Level 3) conditional automated driving in approved operating domains and robotaxi operators are building L4 (Level 4) commercial fleets city by city.

A single technology is not shaping market demand. Sensor costs, software validation, ODD (Operational Design Domain) limits, safety recalls, mapping requirements, driver monitoring rules, insurance exposure and city-level approvals now decide what can be sold and where it can operate. Passenger cars with supervised automated driving features create the largest revenue base because paid software packages, hardware-ready vehicles and subscription models scale across high-volume OEM platforms. L4 robotaxi services remain strategically important but are concentrated in a limited number of cities and must be sized separately from privately owned vehicle sales.

Waymo remains one of the most visible L4 robotaxi operators in the U.S., but its 2026 operating profile shows the commercial deployment is still tied to city-level approvals, weather controls, software remedies and defined ODD (Operational Design Domain) boundaries. The company continues to expand autonomous ride-hailing access across selected metro areas while recent NHTSA recall actions and weather-related service pauses highlight the need for disciplined fleet governance. Tesla, Mercedes-Benz, GM, Ford, Toyota, Honda, Nissan, BYD, XPeng, NIO, Mobileye, Zoox, Pony AI and WeRide are commercially relevant in different layers of the market.

China, the U.S., Germany, Japan and South Korea are the most important competitive centers because vehicle production, EV adoption, ADAS (Advanced Driver Assistance System) software development and regulatory testing frameworks are concentrated in these markets. China is scaling domestic intelligent-driving platforms rapidly through EV brands and local technology suppliers. The U.S. leads in robotaxi deployment through Waymo and in supervised software scale through Tesla and GM. Germany anchors regulated L3 deployment through Mercedes-Benz DRIVE PILOT. Japan and South Korea are progressing through safety-first OEM deployment and highly controlled automated driving programs.

Key Takeaways

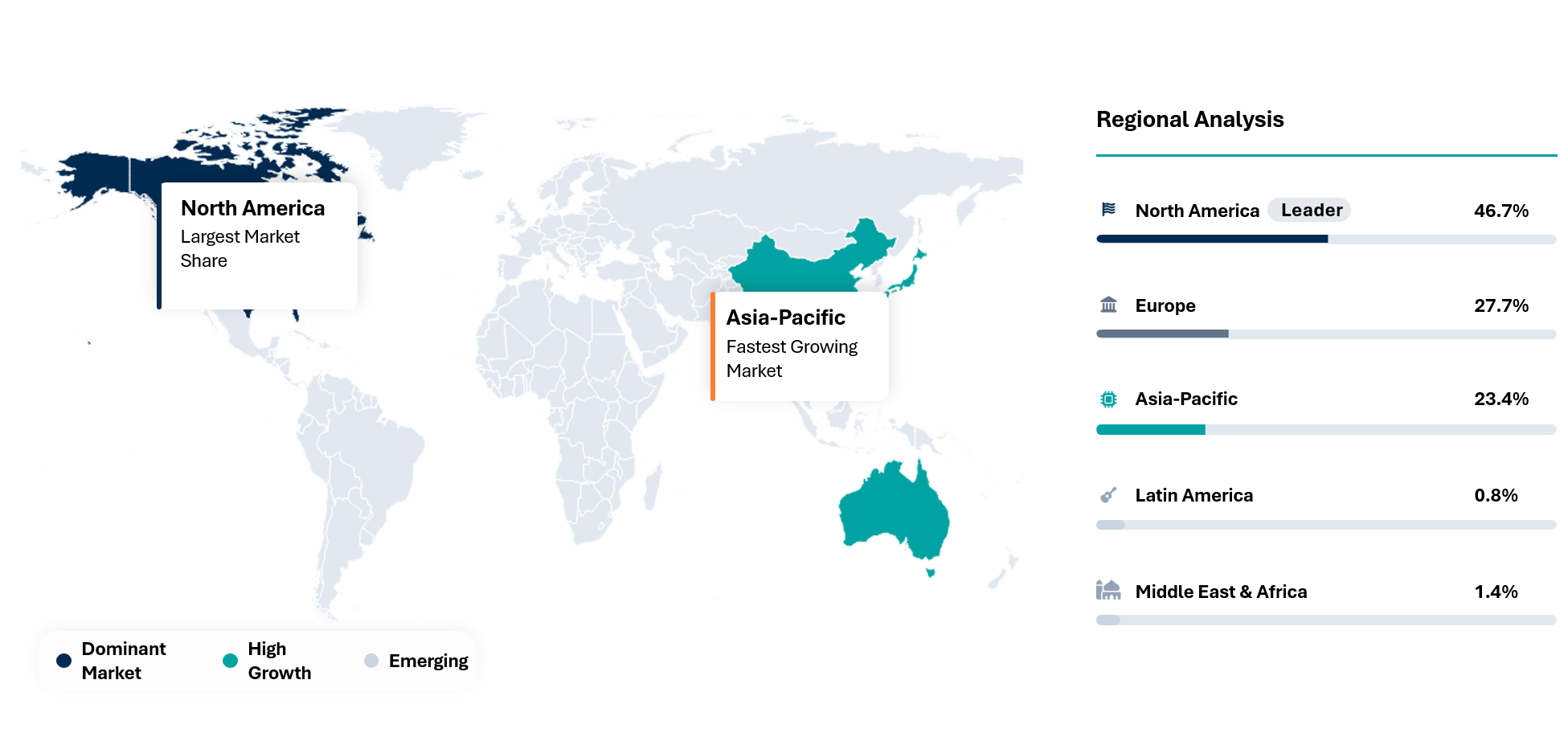

- North America dominated the global self-driving cars market with 46.7% share in 2025, supported by active robotaxi deployments, strong ADAS software monetization, higher consumer awareness of hands-free driving and the presence of leading technology developers, OEMs and autonomous mobility operators.

- Asia-Pacific is the fastest-growing region with a projected CAGR of 35.0% during 2026-2035, driven by rapid EV adoption, intelligent-driving competition among Chinese automakers, smart mobility pilots, semiconductor strength in Japan and South Korea and rising investment in connected vehicle platforms.

- SAE Level 2 driver assistance dominated the market with 85.1% share in 2025, as supervised highway assistance, adaptive cruise control, lane centering, automated lane change and hands-free eyes-on systems are already available across a wide range of passenger vehicles.

- L3 and L4 systems remain smaller but strategically important because they represent the transition from driver-supervised convenience features toward conditionally automated driving and geofenced robotaxi operations.

- BEV (Battery Electric Vehicle) platforms represented the fastest-growing propulsion category with 47.5% share in 2025 and are forecast to grow at 39.0% CAGR during 2026-2035, supported by centralized vehicle architectures, OTA software updates, high sensor integration and strong adoption of intelligent-driving features across EV models.

- Passenger cars will continue to dominate vehicle type demand because OEM-installed automated-driving features can be integrated across mass-market, premium and luxury models through trims, software packages and subscription-based upgrades.

- Robotaxi services are gaining strategic visibility in selected cities, but commercial expansion depends on service-area approvals, fleet utilization, weather readiness, remote support, safety performance and customer trust.

- Supplier differentiation is moving from sensor count toward validated software behavior, driver monitoring, safety documentation, ODD (Operational Design Domain) clarity, regulatory approval and real-world operating performance.

Self-Driving Cars Industry Trends and Strategic Insights

- OEMs are moving autonomy commercialization toward paid software, subscription packages and premium trims. Hardware is increasingly embedded during vehicle production while revenue is captured through activation, renewal or upgrade models.

- Robotaxi providers are learning that city selection matters as much as technology. Favorable weather, road geometry, regulatory cooperation, airport access, fleet charging and public acceptance can determine deployment economics.

- L3 systems are creating a new liability conversation. Customers can only pay premium prices when the OEM clearly defines when the vehicle is responsible and when the driver must take back control.

Self Driving Car Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 47.89 Billion | |

| 2035 Projected Market Size | US$ 707.72 Billion | |

| CAGR (2026-2035) | 31.5% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Automation Level | SAE Level 2 Driver Assistance, SAE Level 3 Conditional Automated Driving, SAE Level 4 High Automated Driving | |

| By Vehicle Body Style | Sedans, Hatchbacks, SUVs (Sport Utility Vehicles), MPVs (Multi-Purpose Vehicles), Purpose Built Robotaxis | |

| By Propulsion | BEV (Battery Electric Vehicle), HEV (Hybrid Electric Vehicle), PHEV (Plug In Hybrid Electric Vehicle), ICE (Internal Combustion Engine) | |

| By Commercial Model | Privately Owned Vehicles, Software Subscription Enabled Vehicles, Fleet Owned Ride Hailing Vehicles, Corporate and Government Fleet Vehicles | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Why does this report matter in 2026?

Autonomous driving entered 2026 with a sharper commercial reality. Feature availability is expanding but the industry is being judged by safety performance, real deployment economics and regulatory credibility rather than future promises. Buyers, investors and suppliers need a view that separates supervised automation revenue from conditional automation and fleet-based robotaxi revenue.

A major development is the shift from technology demonstration to operating-risk management. Robotaxi providers can be technically advanced and still face service pauses due to weather, flooding, emergency response concerns or software recalls. OEMs can sell advanced driver assistance at scale but still need to communicate driver responsibility clearly.

Customers need a practical market view in 2026 because procurement, partnership and investment choices are becoming more fragmented. Automakers must decide whether to build in-house software, partner with technology suppliers or license platform capabilities. Sensor companies must decide which architectures will scale. Fleet operators must evaluate which cities and operating domains can generate utilization. Regulators must assess whether safety cases are mature enough for broader deployment.

Strategic Indicators For Self-Driving Cars

High Regulation Impact

Regulation is one of the strongest market controls because autonomous driving changes responsibility for driving behavior. L2 systems remain driver-supervised and depend heavily on driver monitoring, labeling and consumer communication. L3 systems require clearer legal treatment because the vehicle can perform the dynamic driving task within a defined domain. L4 robotaxi fleets require permits, safety reporting, city coordination and operating restrictions. Recalls and software remedies show that regulators are treating ADS (Automated Driving System) software as a safety-critical product. Companies that document safety cases, incident responses and software update discipline will be better positioned than firms relying on marketing claims.

High Investment Activity

Investment is concentrated in AI driving stacks, simulation, validation fleets, high-performance compute, sensor fusion, LiDAR, autonomous radar, mapping and city-level fleet operations. Automakers are spending on automated driving as part of broader software-defined vehicle programs. Robotaxi firms require capital for vehicles, depot operations, charging, teleoperations, support teams and regulatory engagement. Supplier investment is also moving toward perception chips, domain controllers, driver monitoring and software toolchains. The strongest activity appears where OEMs can reuse platforms across multiple models or where fleet operators can achieve dense utilization in cities with favorable deployment conditions.

Supply Chain Disruption

Autonomous driving hardware depends on cameras, radar, LiDAR, ultrasonic sensors, domain controllers, GPUs, memory, connectivity modules and automotive-grade power electronics. Disruption occurs when semiconductor shortages, export controls, software validation delays or sensor cost pressures affect production schedules. Robotaxi operators face a different supply chain problem because every vehicle must be equipped, maintained, cleaned, charged and supported as part of a fleet. Hardware substitution is difficult after validation because even small sensor or compute changes can trigger new safety testing. Suppliers with automotive-qualified components, predictable production capacity and software compatibility have stronger negotiating power.

Pricing Volatility

Pricing is moving away from a simple vehicle hardware premium. OEMs increasingly monetize driver assistance through options, subscription packages, software unlocks and premium trims. Sensor and compute costs remain significant but the buyer’s willingness to pay depends on feature reliability, operating domain and perceived convenience. Robotaxi pricing is tied to fleet utilization, city density, charging cost, insurance cost, maintenance and regulatory overhead. A temporary service pause can reduce revenue without reducing fixed costs. Better pricing analysis should separate vehicle sales, software subscriptions, fleet ride revenue and licensing income.

Procurement Pressure

Automakers face pressure to deliver advanced driving features without increasing warranty risk or creating unclear consumer expectations. Procurement teams are evaluating sensor vendors, compute suppliers and software partners on cost, validation history, safety documentation, cybersecurity readiness and production maturity. Fleet operators evaluate vehicle platforms on uptime, cleaning cycles, charging compatibility, remote support and total cost per ride. Insurance and legal teams are now part of the buying conversation because software behavior can affect liability. Suppliers that offer evidence-backed safety performance and long-term software support can defend premium pricing.

New Technology Adoption

Technology adoption is strongest where it reduces driver workload in clearly defined conditions. Highway hands-free driving, traffic-jam assistance, automated parking and geofenced robotaxi services have stronger near-term adoption than unrestricted autonomy. AI is improving perception, route planning and prediction but validation remains the bottleneck. Simulation, scenario libraries, closed-course testing and real-world miles are all required to build confidence. Multi-sensor redundancy is gaining support in L3 and L4 programs, while camera-dominant approaches continue in high-volume L2 systems. OTA updates are essential but also create governance pressure because safety performance can change after sale.

Regional Expansion Opportunity

The U.S. offers robotaxi scale in selected cities and strong software ecosystems. China offers large EV volumes and rapid consumer adoption of intelligent driving features. Germany offers premium L3 credibility through regulated deployment. Japan offers controlled mobility environments, aging-population mobility needs and strong OEM engineering discipline. South Korea provides EV, electronics and sensor supply chain strength. UAE and Saudi Arabia are attractive for pilot fleets and controlled smart-city mobility projects but need careful treatment because commercial scale remains limited.

Government Policy Support

Government policy supports the market through safety frameworks, connected mobility programs, EV incentives, smart city projects, semiconductor funding and digital infrastructure investments. Policy does not automatically create autonomous driving revenue. It lowers the barrier for testing, data collection, road readiness and fleet trials. U.S. state-level rules remain important because robotaxi permits are often local or state controlled. European rules are more structured around type approval and safety requirements. China combines central industrial policy with rapid local pilot zones. Japan emphasizes safety-first deployment and public-private mobility programs.

Import Export and Pricing Intelligence

Global trade flows in autonomous vehicle systems are dominated by sensor modules, AI compute hardware, and automotive-grade semiconductors rather than complete vehicles. China exports LiDAR and mid-tier autonomy hardware, while the U.S. and Taiwan dominate high-end chip imports and re-export ecosystems through OEM integration hubs.

Pricing structures are shifting from hardware-centric to software-defined autonomy monetization. OEMs increasingly bundle autonomy features into subscription models. Cost pressures stem from semiconductor scarcity, LiDAR integration costs, and regulatory compliance overheads, creating significant regional pricing divergence between North America, Europe, and Asia-Pacific markets.

| HS Code | Reporter | Trade Flow | 2025 Trade Value | Interpretation |

| 870380 | UK | Import | USD 17.7 Million | Demand for premium electric passenger vehicles that support ADAS and autonomous-ready features is booming in UK |

| 870380 | USA | Import | USD 15.9 Million | U.S. has selective demand for advanced BEV platforms alongside strong domestic autonomous mobility activity. |

| 870380 | Belgium | Import | USD 13.9 Million | Belgium acts as a European entry and distribution hub for connected and ADAS-enabled BEV platforms. |

| 870380 | Germany | Export | USD 45.5 Million | Germany strength local production in premium electric vehicles with advanced driver assistance and L3-ready engineering. |

| 870380 | China | Export | USD 36.4 Million | China strengthens global supply of BEVs with intelligent-driving features, OTA software and sensor-rich configurations. |

Company Coverage Preview

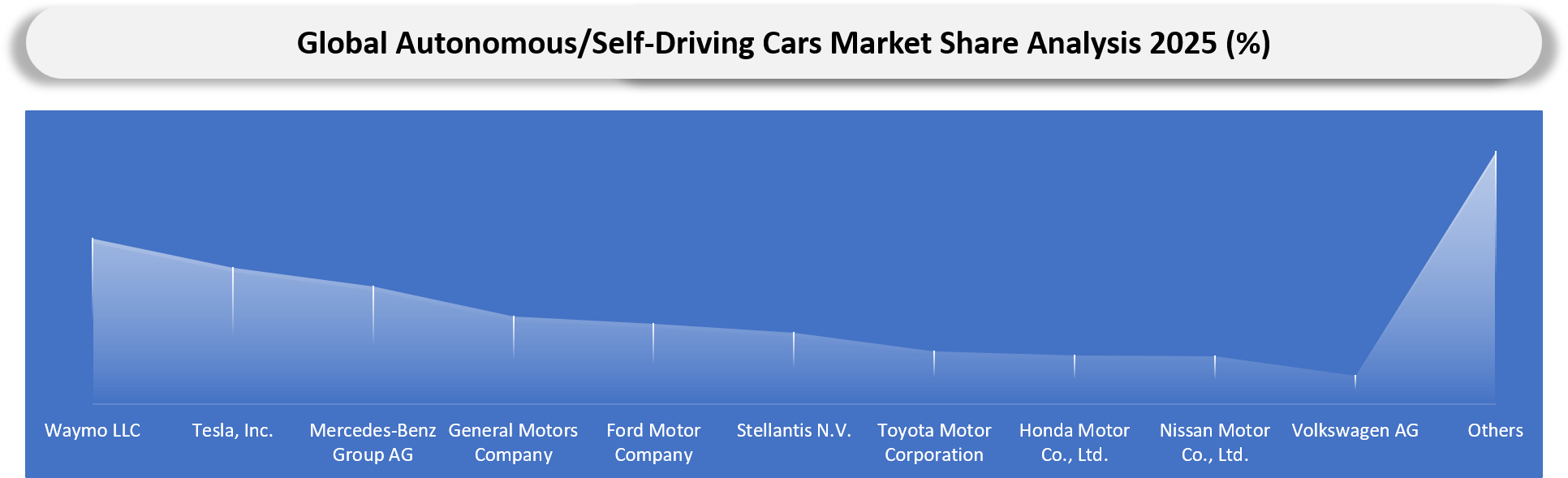

Tesla, Inc. is one of the most important companies to profile because it has commercialized supervised automated driving features at scale across a large connected vehicle fleet. Tesla’s advantage comes from software distribution, OTA updates, vehicle data collection and direct customer monetization through FSD (Full Self Driving) Supervised subscriptions or purchases. Tesla should be benchmarked as a high-volume L2 supervised automation player rather than as an L4 robotaxi operator unless commercial driverless service revenue becomes measurable.

Waymo LLC is the most important company for L4 robotaxi service coverage because it operates a fleet-based autonomous ride-hailing model. Its USP is a purpose-built ADS stack supported by mapping, simulation, real-world operating experience and geofenced deployment discipline. Waymo’s market share should be counted in robotaxi services and autonomous ride-hailing revenue, not passenger car sales. Recent recall activity and service limitations should be included as a risk note rather than a reason to exclude the company from the market.

AI Impact Analysis

AI is central to perception, prediction, planning, simulation and driver monitoring. Autonomous driving systems need to interpret lanes, vehicles, pedestrians, cyclists, traffic signals, emergency vehicles, road debris and unusual behavior. Better AI models can improve recognition and prediction but they do not remove the need for validation. The commercial value of AI is therefore measured by safer behavior inside a defined operating domain rather than broad claims of autonomy.

AI also changes the economics of development. Simulation can generate rare scenarios that would be difficult to collect on roads. Synthetic data can help train perception systems. Fleet data can improve edge cases when governed properly. Companies with large data pipelines and closed-loop validation infrastructure have an advantage because every deployed vehicle can contribute to improvement. Regulatory scrutiny will rise as software updates change behavior after sale.

Generative AI and agentic systems may support engineering workflows, labeling, scenario generation, customer support and fleet operations. Direct control of safety-critical driving behavior will remain heavily validated and constrained. Customers and regulators will not accept black-box behavior without safety cases, audit trails and performance evidence. AI will therefore be a market enabler but also a governance challenge.

Disruption Analysis

Disruption is coming from the separation of vehicle ownership and mobility service revenue. Robotaxi fleets can create recurring ride revenue without selling cars to consumers, while OEMs can create recurring software revenue from vehicles already sold. The market therefore needs two commercial models: privately owned vehicles with automated driving features and fleet-owned autonomous services.

Another disruption is the shift from hardware specification to software confidence. A vehicle with more sensors does not automatically win if the software stack cannot be validated, updated and explained. Conversely, a lower-cost architecture may scale faster in consumer vehicles but may face limits in L3 or L4 operating domains. Buyers are increasingly evaluating safety performance; update cadence and feature usability rather than sensor count alone.

Public trust is a commercial variable. Incidents, recalls and confusing feature names can slow adoption even when technology improves. Companies that communicate operating limits clearly will build stronger long-term adoption. Firms that overstate capabilities may face regulatory action and consumer backlash.

BCG Matrix: Company Evaluation

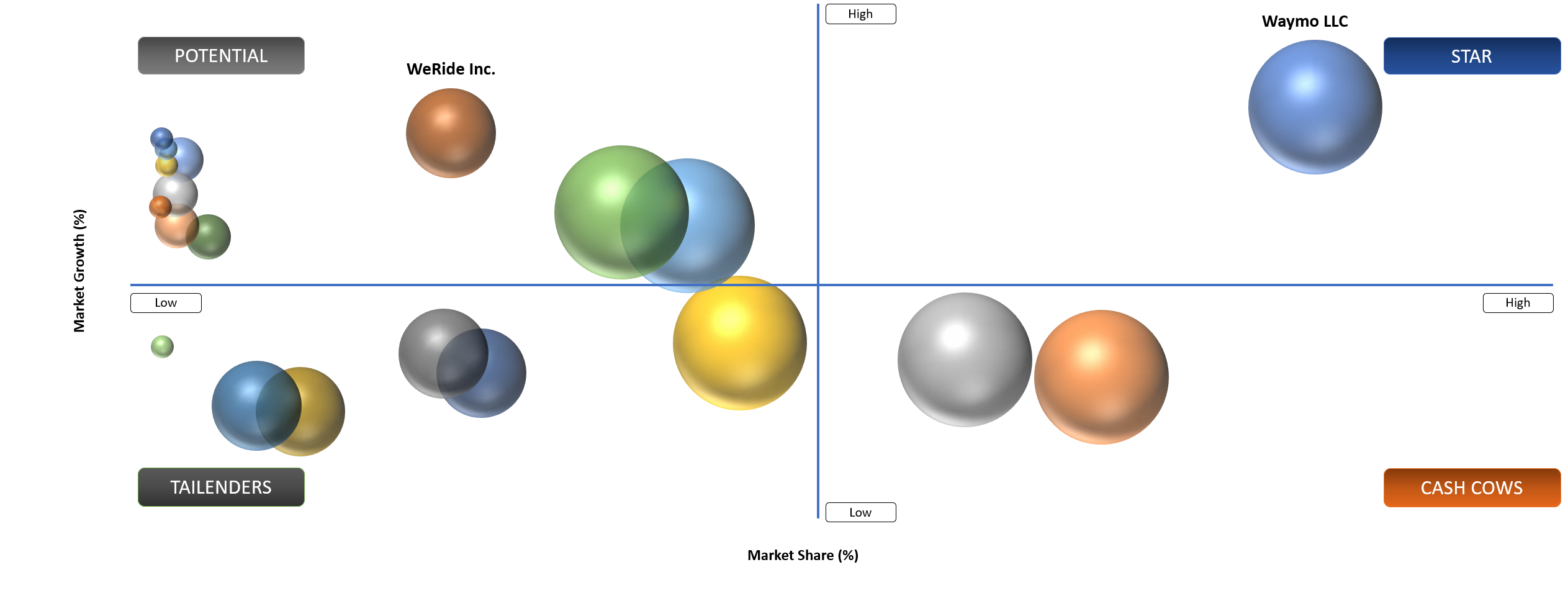

STAR

Star players include Tesla, Waymo, Mercedes-Benz, Mobileye, GM, Ford, Toyota and leading Chinese EV companies such as BYD, XPeng and NIO because they combine commercialization pathways with software, vehicle integration or fleet operations. Tesla leads supervised feature scale. Waymo leads L4 robotaxi commercialization. Mercedes-Benz leads regulated L3 credibility. Mobileye supports OEM platform adoption through technology licensing. Star players should be evaluated by revenue model, operating domain, deployment scale, safety evidence, regulatory readiness and software update discipline rather than by broad autonomy claims.

POTENTIAL

Potential players include Zoox, Pony AI, WeRide, selected Chinese intelligent driving platforms, autonomous shuttle developers and OEMs still building internal software-defined vehicle capabilities. These companies can scale where city permits, fleet utilization, OEM partnerships or differentiated operating domains support revenue. Potential players should not be valued only by pilot announcements. Better indicators include paid rides, active fleet size, approved operating areas, vehicle uptime, customer retention, software update performance and cost per mile.

Self Driving Car Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Increasing Investments in AI, Sensor Fusion, and Advanced Driver Assistance Technologies | 5.20% | North America, China, Western Europe, Japan, and South Korea automotive innovation hubs | Autonomous navigation, collision avoidance, adaptive driving systems and predictive mobility platforms | Accelerates commercialization of Level 3 and Level 4 autonomous vehicle ecosystems |

Expanding Government Support for Smart Mobility and Autonomous Vehicle Testing Regulations | 4.90% | U.S., China, Germany, UAE, Singapore, and Nordic smart transportation corridors | Robotaxi deployment, connected infrastructure, autonomous public transportation and intelligent traffic management | Strengthens regulatory readiness and supports large-scale autonomous mobility adoption |

Rising Collaboration Between Automotive OEMs, Technology Firms, and Semiconductor Companies | 4.60% | Global EV manufacturers, AI software developers, and semiconductor ecosystems | Autonomous driving software stacks, high-performance computing platforms and in-vehicle AI processing | Enhances innovation speed and improves scalability of self-driving vehicle platforms |

Growing Demand for Connected Electric Mobility and Shared Autonomous Transportation Services | 4.30% | Urban mobility networks across Asia-Pacific, North America, and Europe | Autonomous ride-hailing, fleet management, logistics automation and last-mile transportation | Supports transition toward mobility-as-a-service and reduces long-term transportation costs |

Highway Automation And Robotaxi Services Are Creating Two Different Growth Engines

Highway automation is scaling because OEMs can integrate it into consumer vehicles and offer immediate convenience. Drivers understand the use case such as less fatigue on mapped highways, better lane centering and smoother adaptive cruise control. The economics work because the same feature can be sold across thousands or millions of vehicles.

Robotaxi services grow differently. A robotaxi operator must win city access, manage fleets, operate depots, handle charging, support riders and respond to unusual events. Revenue depends on utilization and service reliability. A robotaxi fleet can have high strategic value but lower near-term volume than OEM-installed L2 software. Premium automakers can charge for conditional automation but must satisfy stronger redundancy and regulatory standards. Growth will be slower than L2 but more valuable per vehicle where the feature is approved.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

High Development and Sensor Integration Costs | 4.60% | Vehicle manufacturing economics and technology affordability | Level 4 and Level 5 autonomous vehicle deployment | Restricts large-scale commercialization and delays mass-market adoption of self-driving vehicles |

Regulatory Uncertainty and Lack of Global Safety Standards | 4.10% | Autonomous driving approvals and compliance frameworks | Cross-border autonomous mobility operations, robo-taxi services | Slows deployment timelines and increases operational complexity for OEMs and mobility providers |

Cybersecurity Risks and Data Privacy Concerns | 3.90% | Connected vehicle security and data management systems | Vehicle-to-everything (V2X) communication, autonomous fleet operations | Increases investment requirements for secure software architecture and real-time threat mitigation |

Limited High-Definition Mapping and Infrastructure Readiness | 3.70% | Smart transportation infrastructure and road ecosystem compatibility | Urban autonomous navigation, highway pilot systems | Reduces operational efficiency and constrains autonomous vehicle scalability across emerging regions |

Safety Validation And Public Trust Remain The Strongest Restraints

Autonomous driving faces a much higher trust requirement than most vehicle features because a software error can affect passengers, pedestrians, cyclists and surrounding vehicles. Every recall or unusual incident receives broad attention. Companies must prove that the system understands unusual weather, emergency vehicles, construction zones and human behavior.

Driver misuse is especially important in L2 systems. Hands-free or supervised features can create overconfidence when branding is unclear. Strong driver monitoring, transparent feature naming and clear operating limits are becoming part of the market requirement.

Robotaxi fleets face public trust issues city by city. A service may work well in one metro area and struggle in another due to weather, road rules or local opposition. Commercial expansion will therefore be gradual even for technically capable companies.

Self Driving Car Market Analysis

The global Self-Driving cars market is segmented based on the automation level, vehicle body style, propulsion, commercial model and region.

L2 Supervised Driving Remains The Revenue Backbone While L4 Robotaxis Define Strategic Upside

L2 supervised driving is the most commercially scalable part of the market because it can be sold as a software feature on privately owned vehicles. Tesla FSD Supervised, GM Super Cruise, Ford BlueCruise, Toyota Teammate, Nissan ProPILOT and Hyundai Highway Driving Assist show how automakers package convenience, safety and software differentiation. The driver remains responsible but the feature can command premium pricing.

Hands-free eyes-on systems are especially attractive because they offer visible customer value without requiring the legal complexity of L3. Mapped highways, driver monitoring and software updates create a defensible product boundary. OEMs can expand coverage over time and use subscriptions to extend revenue after the vehicle sale.

L3 conditional automated driving is smaller but strategically important. Mercedes-Benz DRIVE PILOT demonstrates that a premium OEM can sell a feature where the vehicle takes over in defined conditions. Adoption will remain limited by speed limits, road approvals, weather and legal frameworks. Customers will still pay where the convenience is clear and liability is well defined.

L4 robotaxis require a separate commercial lens. Waymo, Zoox, Pony AI and WeRide compete through fleet operation rather than retail vehicle sales. Revenue depends on rides, operating area, vehicle availability and price per trip. L4 also creates a platform opportunity because successful fleets may influence insurance, urban mobility planning and vehicle design.

Purpose built robotaxis are commercially different from adapted passenger cars. They may remove driver controls, optimize cabin space and improve fleet utilization but they require higher regulatory confidence. Adapted vehicles may scale faster because they use existing production platforms. The market will likely contain both models for several years.

Passenger cars will continue to dominate because OEM-installed systems can be fitted across mass-market and premium models. Purpose built robotaxis will remain smaller in unit volume but higher in strategic visibility. Autonomous passenger shuttles should be included only for fixed-route passenger mobility, not as a proxy for bus or public transport markets outside the cars scope.

Geographical Penetration

U.S. Self-Driving Cars Market Landscape

The U.S. market is the most visible for commercial robotaxi deployment and supervised software monetization. Waymo has built paid robotaxi operations in selected metro areas while Tesla has scaled supervised driving software across a large connected vehicle base. GM and Ford compete through mapped-road hands-free systems that fit current consumer expectations more clearly than full autonomy.

State-level regulation matters heavily. California, Arizona, Texas and other states have distinct testing and deployment pathways. City cooperation can determine whether a robotaxi operator gains airport access, service-area expansion or public resistance. Commercial success depends on more than software performance because fleets need charging, maintenance, cleaning, emergency response coordination and rider support.

The U.S. also leads in litigation and recalls visibility. NHTSA software recalls, crash investigations and driver monitoring expectations shape market behavior. Vendors need strong safety data and transparent naming. Overpromising autonomy can become a regulatory and reputational liability.

Japan Self-Driving Cars Market Outlook

Japan’s market is shaped by aging-population mobility needs, dense cities, high safety expectations and strong OEM discipline. Toyota, Honda and Nissan are important players because they combine domestic engineering capability with global vehicle scale. Japan is less likely to rush broad deployment without controlled safety validation.

Autonomous mobility in Japan is attractive for fixed-route, low-speed, elderly mobility and controlled urban operations. Rural transport shortages create a practical policy need. Japanese consumers also place strong trust in reliability and quality, which favors cautious deployment and robust driver assistance systems.

Waymo’s testing activity in Tokyo and partnerships with local mobility operators show that Japan can become an international validation market. Commercial expansion will require alignment with local road behavior, language, insurance and regulatory systems. Japan should be treated as a premium technical market rather than a simple volume market.

China Self-Driving Cars Market Trends

China is one of the most commercially active markets for intelligent-driving features because domestic EV brands are using assisted-driving capability as a visible product differentiator across premium and mid-priced models. BYD, XPeng, NIO, ZEEKR and other brands are using driving assistance as a vehicle differentiation tool. OTA updates and software-defined vehicle strategies are common.

Local policy support and pilot zones help accelerate testing. Chinese cities provide large urban datasets and competitive pressure encourages faster feature rollout. Domestic suppliers also provide LiDAR, cameras, compute platforms and high-resolution mapping capabilities. The result is a market where intelligent driving can become mainstream faster than in many Western markets.

Competition is intense and pricing pressure is real. Features that were once premium may move into mid-priced EVs. Suppliers must prove cost effectiveness and rapid integration. China should be treated as both the largest opportunity and one of the hardest competitive environments.

Competitive Landscape

- Competition is split between OEMs, robotaxi operators, autonomous driving software suppliers, sensor vendors and compute platform providers. Market share must be calculated by business model rather than by one combined list.

- OEMs compete on vehicle-level feature availability, software subscriptions, brand trust and regulatory approval. Robotaxi operators compete on service area, fleet utilization, paid rides, safety record and operating cost.

- Sensor and compute suppliers compete through automotive qualification, performance, cost and ability to support production programs. Software suppliers compete through perception quality, mapping strategy, data scale, safety case evidence and update discipline.

- Competitive benchmarking should track automation level, active markets, vehicle count, paid ride volume, software revenue, subscription adoption, recall history, driver monitoring quality and ODD expansion.

MAJOR PAIN POINTS

- Confusing consumer language around self-driving features creates misuse risk and regulatory exposure.

- L3 and L4 validation is expensive because rare edge cases require simulation, closed-course testing and real-world evidence.

- Robotaxi operations face city-specific scaling limits caused by weather, construction, emergency vehicles, airport access and public acceptance.

- Sensor and compute costs make redundant architectures difficult to push into mass-market vehicles.

- OTA updates improve products but also create governance questions because vehicle behavior can change after sale.

- Insurance and liability models remain unsettled across regions and automation levels.

- Fleet utilization can fall quickly when recalls, weather restrictions or regulatory pauses limit operating hours.

- Supplier selection is difficult because autonomy performance depends on software, hardware, maps and driver monitoring working together.

Recent Developmnets of Self Driving Car Market

- May 2026: Waymo LLC expanded sixth-generation robotaxi deployment, targeting 20 additional cities with lower-cost autonomous sensor architectures.

- May 2026: Tesla, Inc. achieved 10 billion cumulative supervised FSD driving miles globally, accelerating Version 14 autonomous driving software deployment.

- May 2026: Stellantis N.V. partnered with Wayve, targeting 2028 launch of AI-powered supervised hands-free autonomous driving systems.

- May 2026: XPeng Inc. strengthened XNGP autonomous driving rollout, enhancing nationwide urban navigation-assisted driving capabilities across major Chinese cities.

- April 2026: WeRide Inc. broadened autonomous shuttle and robotaxi deployments, emphasizing scalable urban mobility operations across multiple international transportation corridors.

- March 2026: Zoox, Inc. intensified robotaxi production readiness, scaling bidirectional autonomous vehicle testing across dense urban transportation environments.

- March 2026: General Motors Company continued expanding Super Cruise highway autonomy features, competing aggressively against Tesla’s comprehensive door-to-door FSD capabilities.

- February 2026: Mercedes-Benz Group AG introduced MB.DRIVE ASSIST Pro, replacing DRIVE PILOT with advanced Level 2++ automated driving capabilities.

- January 2026: Volkswagen AG intensified autonomous vehicle software integration through Cariad, enhancing AI-powered mobility and next-generation automated driving architecture development.

- January 2026: ZEEKR Intelligent Technology Holding Limited supported Waymo’s sixth-generation robotaxi manufacturing expansion with dedicated autonomous mobility vehicle production.

ANALYST VIEW / OPINION

- Rapid commercialization will remain constrained by edge-case safety validation, making fully autonomous Level 5 deployment a long-term horizon despite aggressive pilot programs.

- Regulatory fragmentation across North America, Europe, and Asia-Pacific will continue to slow global scaling, forcing OEMs to adopt region-specific autonomy stacks.

- Robo-taxi services will emerge as the primary revenue-generating use case before private autonomous vehicle ownership becomes mainstream.

- High-definition mapping dependency is expected to gradually decline as AI-driven “mapless autonomy” architectures gain maturity and reduce operational costs.

- Sensor fusion (LiDAR, radar, camera) will remain critical in the near term, but cost reduction in solid-state LiDAR is expected to reshape vehicle BOM economics.

- Autonomous trucking and logistics applications are likely to achieve earlier profitability than passenger vehicles due to controlled highway environments and predictable routes.

- AI compute limitations and energy efficiency constraints will become key bottlenecks, pushing automotive OEMs toward specialized edge AI chip partnerships.

- Insurance and liability frameworks will evolve into product-based risk models, shifting responsibility from drivers to OEMs and autonomous software providers.

- Data acquisition and real-world driving miles will remain a dominant competitive advantage, favoring incumbents with large fleet deployment capabilities.

- Strategic consolidation in the autonomous vehicle ecosystem is expected to intensify as smaller AI startups struggle with capital intensity and long development cycles.

TARGET AUDIENCE

| INDUSTRY | WHO SHOULD BUY THIS REPORT? | REASON TO BUY THIS REPORT |

| Automotive OEMs & EV Manufacturers | Autonomous Driving Program Teams, Vehicle Engineering Heads, Mobility Innovation Managers | Analyze adoption trends of autonomous driving platforms, ADAS integration and software-defined vehicle architectures |

| Autonomous Vehicle Technology Providers | AI Engineering Teams, Sensor Fusion Specialists, Product Development Managers | Evaluate LiDAR, radar, camera and AI-based perception technologies shaping self-driving vehicle ecosystems |

| Semiconductor & AI Chip Manufacturers | Automotive Chip Design Teams, Embedded AI Engineers, Strategic Business Units | Assess growing demand for high-performance automotive processors, edge AI chips and autonomous computing platforms |

| Mobility-as-a-Service (MaaS) & Ride-Hailing Companies | Fleet Automation Teams, Smart Mobility Strategists, Operations Directors | Understand commercialization opportunities for robotaxis, autonomous fleet management and shared mobility services |

| Logistics & Autonomous Delivery Companies | Supply Chain Automation Teams, Fleet Operations Managers, Warehouse Robotics Engineers | Evaluate self-driving vehicle adoption for last-mile delivery, freight transport and logistics optimization |

| Smart City & Infrastructure Development Organizations | Urban Mobility Planners, Intelligent Transportation System Teams, Infrastructure Consultants | Analyze infrastructure requirements for connected roads, V2X communication and autonomous traffic ecosystems |

| Telecom & Connectivity Providers | 5G Automotive Solution Teams, Network Infrastructure Engineers, IoT Strategy Departments | Study demand for ultra-low latency communication, vehicle connectivity and real-time autonomous navigation support |

| Automotive Software & Cybersecurity Companies | Vehicle Software Architects, Cybersecurity Specialists, OTA Update Teams | Assess software safety, cybersecurity frameworks and OTA capabilities required for autonomous vehicle operations |

| Government Transportation & Regulatory Authorities | Transport Policy Makers, Smart Mobility Authorities, Road Safety Departments | Support autonomous vehicle regulations, road safety initiatives and national smart transportation modernization programs |

| Investors, Venture Capital & Consulting Firms | Mobility Investment Analysts, Automotive Consultants, Market Intelligence Teams | Evaluate market growth opportunities, competitive positioning and future investment potential in autonomous mobility technologies |

WHY CHOOSE DATAM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

WHAT DATAM UNIQUELY PROVIDES

- Deep autonomy stack segmentation across perception, planning, and control layers

- OEM-level benchmarking of Level-2 to Level-4 deployment maturity curves

- Real-world robotaxi fleet operational intelligence and utilization metrics

- Regulatory mapping across U.S., EU, China, and Japan autonomy frameworks

- Sensor ecosystem cost breakdown including LiDAR, radar, and vision systems

- AI compute infrastructure dependency analysis across OEMs and tech firms

- Scenario-based commercialization forecasting tied to geofenced deployment zones