EV Charging Infrastructure Market Overview

According to DMI analysis, the global EV charging infrastructure market was valued at US$56.85 billion in 2025 and is expected to reach US$1,936.81 billion in 2035, growing at a CAGR of 32.8% during the forecast period (2026–2035). The global EV charging infrastructure market is entering a high-growth phase driven by accelerating EV adoption, large-scale government funding, and rapid advances in fast-charging and grid-interactive technologies. By 2025, the global stock of electric vehicles had surpassed 30 million units, creating unprecedented demand for both residential and public charging networks. AC charging remains the backbone of global installations, accounting for nearly 68–72% of all chargers in operation, supported by strong penetration of home and workplace charging. In parallel, DC fast-charging capacity is expanding rapidly, growing at an annual rate of nearly 30–35%, as nations prioritize highway electrification and commercial fleets shift to high-power charging solutions to maintain operational uptime.

Massive public-sector investments are reshaping the market’s trajectory. Across Europe, China, and India, cumulative funding for EV charging infrastructure has exceeded US$120 billion between 2022 and 2025, enabling the deployment of high-density charging corridors, interoperability standards, and renewable-powered hubs. Utility participation is also rising, with grid-interactive charging programs projected to reduce local grid reinforcement costs by up to 25%, while unlocking new monetization channels through demand-response and V2G services. With renewable energy now contributing over 28% of global electricity generation, the integration of smart energy management and bidirectional charging positions the EV charging infrastructure market for sustained, long-term expansion.

EV Charging Infrastructure Market Industry Trends and Strategic Insights

- North America leads the global EV charging infrastructure market, capturing the largest revenue share of 40.01% in 2024.

- By charging type segment, AC charging leads the global EV charging infrastructure market, capturing the largest revenue share of 60.7% in 2024.

EV Charging Infrastructure Market Key Takeaways

- North America accounted for 40.01% of global revenue, supported by large-scale federal funding programs and mature charging ecosystems.

- AC charging represented 60.7% of market revenue in 2024, reinforcing its role as the primary charging technology for residential and workplace applications.

- More than 1.3 million public charging points were added globally during 2024, highlighting continued infrastructure expansion.

- Public and private investment commitments exceeded US$120 billion between 2022 and 2025 across major EV markets.

- Grid-interactive charging solutions have the potential to reduce utility infrastructure upgrade costs by 20% to 30%.

- Asia-Pacific remains the fastest-growing region due to China's charging scale, India's policy support, and Southeast Asia's expanding electrification programs.

- Future profitability is expected to increasingly depend on charger utilization rates, energy management services, interoperability platforms, and recurring software revenues rather than charger installation volume alone.

EV Charging Infrastructure Market Scope

| Metrics | Details |

| Market Size (2025) | US$56.85 Billion |

| Market Size (2035) | US$1,936.81 Billion |

| CAGR (2026-2035) | 32.80% |

| Historic Years | 2023-2024 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Segments Covered | Charger Type, Charging Type, Connector Type, Connectivity, End User, Region |

| Leading Region | North America |

| Fastest Growing Region | Asia-Pacific |

EV Charging Infrastructure Market Dynamics

Grid-Interactive Charging & Utility Monetization Opportunities

Grid-interactive charging is rapidly emerging as one of the strongest drivers shaping the EV charging infrastructure market, as utilities and charge point operators increasingly recognize the economic value of bidirectional energy flow, demand-response participation, and dynamic grid balancing. As EV adoption accelerates, surpassing 25 million EVs globally on the road by 2025, the cumulative storage potential of EV batteries represents a massive distributed energy resource. Utilities are leveraging this through vehicle-to-grid (V2G) and vehicle-to-home (V2H) programs, enabling EVs to supply power back to the grid during peak demand. Early pilot programs in Europe and the US show that V2G-enabled EVs can earn US$400–US$1,000 per vehicle annually for providing grid services, creating new revenue streams for both fleet operators and utilities.

At the grid level, the rising penetration of renewable energy, now contributing over 30% of total electricity in several advanced markets, increases the need for flexible storage to stabilize intermittency. Smart, grid-interactive chargers help utilities smooth load curves through time-of-use pricing, automated charging scheduling, and peak shaving. The economic impact is significant: utility-managed smart charging can reduce grid upgrade costs by 20–30%, while optimized charging can lower system-wide peak demand by 5–15%. As charging networks scale, monetization opportunities in energy trading, frequency regulation, and demand-response markets are making grid-interactive charging a critical growth engine for the global EV charging infrastructure market.

The buildout momentum is triggering industry coordination aimed at improving user experience and network scale. For example, the Spark alliance, comprising Atlante, Electra, Fastned and Ionity, was announced in April 2025 to develop one of Europe's largest, most dependable and interoperable fast-charging networks for EVs. The network connects more than 1,700 charging stations and 11,000 high-power charging (HPC) points throughout 25 European nations, enabling ultra-fast charging and interoperable payment through member apps. This signals the market shift from fragmented networks to platform ecosystems, improving utilization and accelerating consumer trust.

Investment Drivers Reshaping the EV Charging Infrastructure Industry

Charging Networks Are Becoming Energy Platforms

The EV charging industry is evolving beyond hardware deployment toward integrated energy ecosystems. Smart charging systems now allow operators to optimize charging schedules, participate in demand-response programs, and monetize distributed energy resources.

Vehicle-to-grid and vehicle-to-home technologies are becoming increasingly attractive to utilities seeking grid flexibility. Pilot programs indicate that V2G-enabled vehicles can generate annual revenues ranging from US$400 to US$1,000 per vehicle through participation in grid services markets.

As renewable energy penetration continues to increase globally, charging stations are becoming critical energy assets capable of balancing electricity demand while supporting decarbonization objectives.

Government Policy Remains a Core Growth Catalyst

Infrastructure policy continues to accelerate deployment. Programs such as the United States NEVI initiative, India's PM E-DRIVE framework, Canada's ZEVIP program, and Europe's charging corridor investments are directing billions toward charging infrastructure expansion.

Governments increasingly view charging infrastructure as a strategic economic asset rather than a transportation accessory, leading to supportive regulations, public funding mechanisms, and interoperability mandates.

Fleet Electrification Is Creating Large-Scale Demand

Commercial fleet operators represent one of the strongest demand engines within the EV Charging Infrastructure market forecast 2035.

Logistics providers, ride-hailing operators, transit authorities, and last-mile delivery fleets require high-capacity charging infrastructure capable of supporting intensive daily utilization. Depot charging, corridor charging, and dedicated commercial hubs are becoming major investment categories across developed and emerging markets.

Pricing, Adoption Trends and Infrastructure Economics

EV Charging Infrastructure pricing and adoption trends are increasingly influenced by charger utilization rates, electricity pricing, and software-enabled energy optimization.

While AC charging remains cost-effective due to lower installation requirements, DC fast charging requires significantly higher capital expenditures, grid upgrades, and energy management systems.

Charging operators are increasingly shifting toward recurring revenue models that include:

- Charging-as-a-service

- Energy management subscriptions

- Fleet charging solutions

- Demand-response participation

- Software licensing

- Grid services monetization

This transition is expected to improve profitability and reduce reliance on pure hardware sales.

Charging Ecosystem Map: How the Industry Value Chain Is Evolving

The charging ecosystem has become highly interconnected and includes multiple stakeholder groups:

Automakers (OEMs)

Tesla, traditional automakers, and emerging EV manufacturers increasingly influence charging standards and network development strategies.

Charging Equipment Manufacturers

Companies develop AC chargers, DC fast chargers, power electronics, connectors, and software platforms.

Charge Point Operators (CPOs)

Network operators deploy and manage charging stations while generating revenue through charging services and subscriptions.

Utilities

Utilities provide grid integration, smart charging programs, renewable energy sourcing, and V2G monetization opportunities.

Software Providers

Energy management platforms, charger monitoring systems, payment solutions, and interoperability services are becoming critical competitive differentiators.

OEM Partnerships and Industry Collaboration

Partnership-driven expansion has become a defining characteristic of the market.

The Spark Alliance announced in 2025 demonstrates the growing importance of interoperable charging networks. The collaboration connects more than 1,700 charging stations and over 11,000 high-power charging points across Europe.

Similarly, Tesla's expansion of NACS compatibility is encouraging standardization across charging networks and reducing consumer concerns around charging accessibility.

These collaborations improve charger utilization, reduce network fragmentation, and accelerate EV adoption by simplifying the customer experience.

EV Charging Infrastructure Market Segmentation Analysis

Segmented by Charger Type (Slow Charger, Fast Charger), by Charging Type (AC, DC), by Connector Type (CHAdeMO, CCS, Others), by Connectivity (Connected Charging Stations, Non-connected Charging Stations), by End User (Commercial, Residential), and by Region, Share, Trends, and Forecast to 2035.

Commercial Charging Continues to Generate Significant Revenue Opportunities

Commercial charging infrastructure remains a cornerstone of industry expansion.

Fleet operators require dependable charging access to maximize vehicle utilization and minimize downtime. The commercial segment benefits from higher charger utilization rates, greater charging frequency, and stronger long-term revenue visibility compared to residential installations.

Investments by energy companies, logistics operators, and charging networks continue to focus on high-traffic commercial locations, freight corridors, transportation hubs, and workplace charging facilities.

AC Charging Maintains Market Leadership

AC charging accounted for 60.7% of market revenue in 2024 and remains the dominant charging type globally.

Lower installation costs, widespread residential deployment, and compatibility with daily commuting patterns continue to support demand. Home charging remains the preferred solution for a large portion of EV owners, reinforcing AC charging's leading market position.

DC Fast Charging represents the growth engine.

DC charging is expected to record the fastest growth through 2035.

Ultra-fast charging systems delivering 50 kW to 350 kW are increasingly essential for commercial fleets, long-distance travel, and public charging networks. As charging times continue to decline, DC infrastructure is becoming a critical enabler of mass EV adoption.

Battery Chemistry Trends and Charging Infrastructure Implications

Battery chemistry developments are increasingly influencing charging infrastructure requirements.

Lithium Iron Phosphate (LFP) batteries are gaining popularity due to cost advantages and safety characteristics. Their widespread adoption supports large-scale charging deployment across passenger vehicles and commercial fleets.

Nickel Manganese Cobalt (NMC) batteries continue to dominate premium EV segments where higher energy density and longer driving range remain priorities.

The growth of high-voltage battery architectures is creating demand for ultra-fast charging networks capable of supporting next-generation charging speeds and minimizing downtime.

Recycling Loop and Second-Life Opportunity

An emerging opportunity within the EV Charging Infrastructure market involves battery recycling and second-life energy storage applications.

Retired EV batteries can be repurposed for stationary energy storage systems integrated with charging stations. These systems help reduce peak demand charges, improve renewable energy utilization, and support grid resilience.

As EV battery volumes increase during the forecast period, second-life storage solutions could become an important economic component of charging hub development.

Battery recycling infrastructure is also expected to strengthen supply chain security by recovering critical materials required for future electrification programs.

EV Charging Infrastructure Market Regional Analysis

North America EV Charging Infrastructure Market

North America remains the leading regional market, supported by strong consumer adoption, federal funding initiatives, utility investments, and a highly developed charging ecosystem.

The United States continues to dominate regional demand due to accelerating EV sales, NEVI funding allocations, corporate fleet electrification, and the growing adoption of NACS charging standards.

Canada is also experiencing robust growth supported by national charging deployment targets, renewable energy integration, and provincial electrification programs.

Europe EV Charging Infrastructure Market

Europe maintains a strong position due to aggressive emissions reduction targets, extensive charging corridor development, and regulatory support for zero-emission transportation.

Cross-border interoperability initiatives and high-power charging investments are enabling long-distance EV travel throughout the region.

The emergence of collaborative charging networks such as Spark highlights Europe's focus on network reliability and user convenience.

Asia-Pacific EV Charging Infrastructure Market

Asia-Pacific represents the fastest-growing EV Charging Infrastructure market.

China continues to dominate deployment volumes, charger manufacturing, and charging technology innovation. The country remains the benchmark for large-scale charging rollout and network utilization.

India is becoming a significant growth engine through public funding, highway charging deployment, and increasing adoption of electric two-wheelers, three-wheelers, and commercial vehicles.

Southeast Asian markets are creating attractive opportunities as urban mobility electrification accelerates across major metropolitan areas.

EV Charging Infrastructure Market Supply Chain Analysis

Supply chain performance increasingly affects infrastructure deployment timelines and project economics.

Key supply chain dependencies include:

- Power electronics

- Semiconductors

- Charging cables and connectors

- Transformers

- Switchgear systems

- Battery storage components

- Critical minerals

Raw material volatility can influence charger manufacturing costs and project returns. Companies that secure resilient supplier networks and localized production capabilities are expected to gain competitive advantages.

EV Charging Infrastructure Market Competitive Landscape

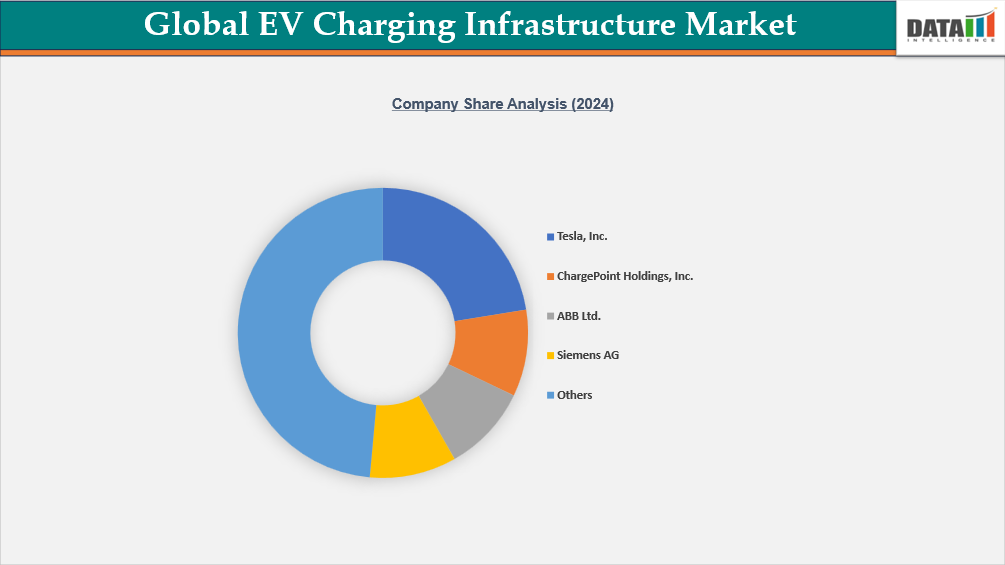

- The global EV charging infrastructure market is highly competitive, characterized by a strong presence of multinational corporations alongside rapidly growing regional operators. Leading companies such as ABB Ltd, ChargePoint Holdings, Inc., Tesla, Inc., Siemens AG, Schneider Electric SE, EVgo Services LLC, Blink Charging Co., IONITY GmbH, and Alfen N.V. maintain market leadership through advanced charging technologies, high-power DC fast-charging solutions, and continuous investments in renewable integration, smart charging software, and R&D.

- Many players are expanding their geographic footprint through strategic partnerships with utilities, automakers, fleet operators, and commercial property developers. These collaborations are enabling large-scale deployment of charging hubs, interoperability across networks, improved payment systems, and seamless integration of energy management and vehicle-to-grid (V2G) capabilities, supporting accelerated global EV adoption.

- Market competition is driven by growing demand for fast-charging infrastructure, the rise of electric fleets, and policy incentives supporting electrification across major economies. Leadership in the EV charging sector increasingly depends on grid-interactive technologies, operational reliability, charging speed differentiation, and cost-efficient infrastructure deployment, all of which shape long-term growth and competitive positioning within the global EV charging infrastructure market.

Investment & Funding Landscape

IONITY GmbH has emerged as one of Europe’s most capital-intensive EV charging networks, backed by strong automotive consortium support. In 2025, the company secured up to €600 million in record financing, marking one of the largest single funding events in the public fast-charging space. This investment is directed toward accelerating the rollout of high-power charging (HPC) sites across Europe, enabling the company to scale its network to thousands of stations through 2030. The financing reflects strategic confidence in IONITY’s cross-border ultra-fast charging model, which is critical for long-distance EV travel across the European Union. The new capital infusion also positions IONITY to compete more aggressively with oil-major-backed networks and state-subsidized charging programs across the region.

Blink Charging has relied on consistent capital injections to expand its charging footprint and strengthen its hardware and software portfolio. Between late 2023 and early 2024, Blink raised approximately $113 million through at-the-market (ATM) equity programs, a cost-efficient route that allowed the company to access public markets without traditional underwriting. In addition to this recent capital raising, Blink also benefits from earlier historical funding rounds, grants, and partnerships that support its global expansion strategy. These financing activities strengthen Blink’s ability to scale its Level 2 and DC fast-charging solutions, enhance manufacturing capacity in the United States, and grow its vertically integrated model, which spans equipment, software, and charging services. The company’s reliance on public-market mechanisms highlights investor confidence as well as the capital-intensive nature of EV charging build-out.

| Company | Investment/Funding | Year | Details | |

| IONITY GmbH | Up to €600 (US$689) million (record financing) | 2025 | IONITY secured financing (up to €600M) to expand its ultra-fast charging network across Europe and scale to thousands of sites through 2030. | |

| Blink Charging Co. | $113 million (ATM equity raises) + historical funding rounds | 2023-2024 | Blink conducted cost-effective ATM equity raises (gross proceeds ~$113M between Nov 2023–Feb 2024) and has raised earlier funding across rounds and grants to support growth. | |

EV Charging Infrastructure Market Key Developments

April 2026: The United States increased investments in public EV charging networks and grid modernization projects, supporting wider adoption of electric vehicles and expansion of fast-charging infrastructure across urban and highway corridors.

March 2026: Japan accelerated the deployment of next-generation EV charging stations, including ultra-fast chargers and smart charging solutions, to support the growing transition toward electric mobility.

February 2026: ChargePoint Holdings, Inc. expanded its charging infrastructure portfolio through new deployments and software enhancements designed to improve charging accessibility and network efficiency.

January 2026: Governments worldwide increased funding and policy support for EV charging infrastructure development, encouraging large-scale installation of public, residential, and commercial charging stations.

December 2025: Industry participants accelerated investments in ultra-fast charging technologies and intelligent energy management systems to reduce charging times and improve grid integration capabilities.

November 2025: ABB Ltd. strengthened its EV charging solutions portfolio through advanced fast-charging technologies supporting passenger vehicles, commercial fleets, and public transportation networks.

October 2025: Charging infrastructure providers expanded deployment of smart charging platforms incorporating real-time monitoring, remote management, and energy optimization capabilities.

September 2025: India increased investments in nationwide EV charging infrastructure under electric mobility initiatives, supporting growth of public charging networks and accelerating EV adoption.

July 2025: Tesla, Inc. expanded charging network capabilities through additional fast-charging deployments and infrastructure upgrades to support increasing electric vehicle usage.

May 2025: Utilities and charging network operators strengthened partnerships to integrate renewable energy sources and battery storage systems with EV charging infrastructure, improving sustainability and grid resilience.

March 2025: Technology providers accelerated development of vehicle-to-grid (V2G) and bidirectional charging solutions, enabling electric vehicles to support grid balancing and energy management applications.

January 2025: Governments across North America, Europe, and Asia-Pacific expanded support for transportation electrification programs and charging infrastructure investments, driving long-term growth in the EV charging infrastructure market.

What Sets This Global EV Charging Infrastructure Market Intelligence Report Apart

- Latest Data & Forecasts – Comprehensive, up-to-date insights and projections through 2032. Coverage includes global value by charger type, charging type, connector, connectivity, end-user, and region segments. Scenario forecasts with region-level splits (North America, Europe, Asia-Pacific, South America, Middle East and Africa) and sensitivity to factors such as regulatory reclassification and raw-material costs.

- Regulatory Intelligence – Actionable analysis of regulatory frameworks that materially affect vehicle analytics commercialization, revenue by country, allowable label claims, permitted doses, import/export controls and advertising restrictions.

- Competitive Benchmarking – Standardized profiling and benchmarking of leading pharma and nutraceutical players, contract manufacturers and e-commerce specialists active in the market.

- Geographic & Emerging Market Coverage – Region-by-region market sizing, growth drivers, reimbursement dynamics, cultural/consumer behavior and market access considerations. Focus on high-growth or regulatory-uncertain markets.

- Actionable Strategies – Identify opportunities for launching innovative products, while leveraging strategic partnerships and supply chain integration for maximum ROI.

- Pricing & Cost Analysis – In-depth assessment of price trends, raw material costs and sustainability-driven cost efficiencies across regional markets.

- Expert Analysis – Insights from industry experts such as clinical sleep specialists, regulatory affairs professionals and key manufacturing companies.