Global Reaction Wheel Market Size

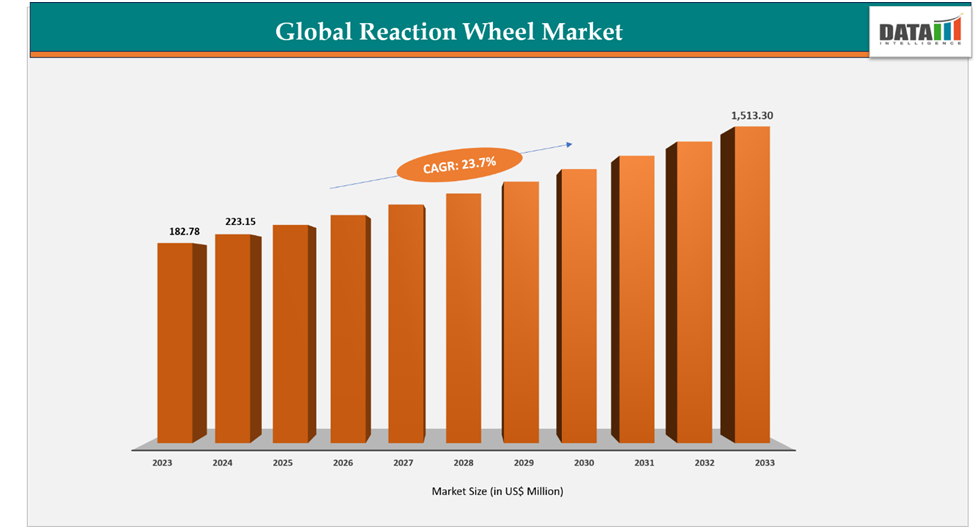

The global reaction wheel market reached US$276.03 million in 2025 and is expected to reach US$2.31 billion by 2035, growing at a CAGR of 23.7% during the forecast period 2026–2035. The global reaction wheel market is growing steadily, driven by rising satellite deployments, expanding private investments, and government-led space programs. Demand for compact, reliable, and high-performance systems is increasing across CubeSats, microsatellites, and deep-space missions.

In 2024, a record 2,695 satellites were launched via 259 missions, with the U.S. holding 65% of the global launch share and 69% of satellite manufacturing revenue. Key players like Honeywell Aerospace, Blue Canyon Technologies, and Collins Aerospace dominate, supporting commercial constellations, defense missions, and NASA projects. Strong R&D, government funding, and private-sector scale ensure the U.S. remains the global leader in reaction wheel technology.

In 2025, Japan launched the Michibiki-6 satellite aboard the new H3 rocket, expanding the QZSS navigation system. Japan also demonstrated world-class reliability with the Hayabusa-2 asteroid mission, which used a four-reaction-wheel control system. With growing investments in navigation, Earth observation, and science missions, Japan is emerging as a key market focused on compact, efficient reaction wheels for both domestic and international projects.

Key Takeaways

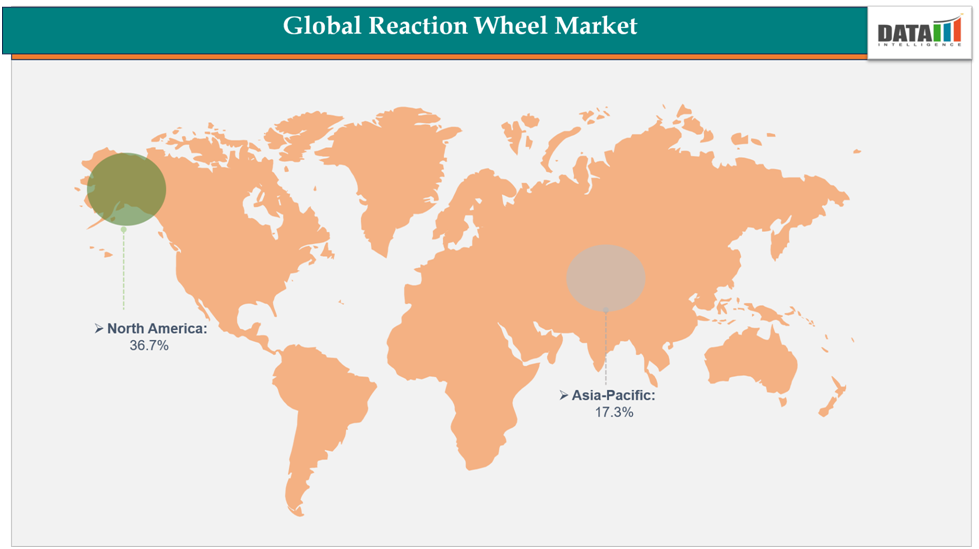

- North America accounted for approximately 36.7% of global revenue in 2024, supported by strong satellite manufacturing capabilities, defense spending, and commercial launch activity.

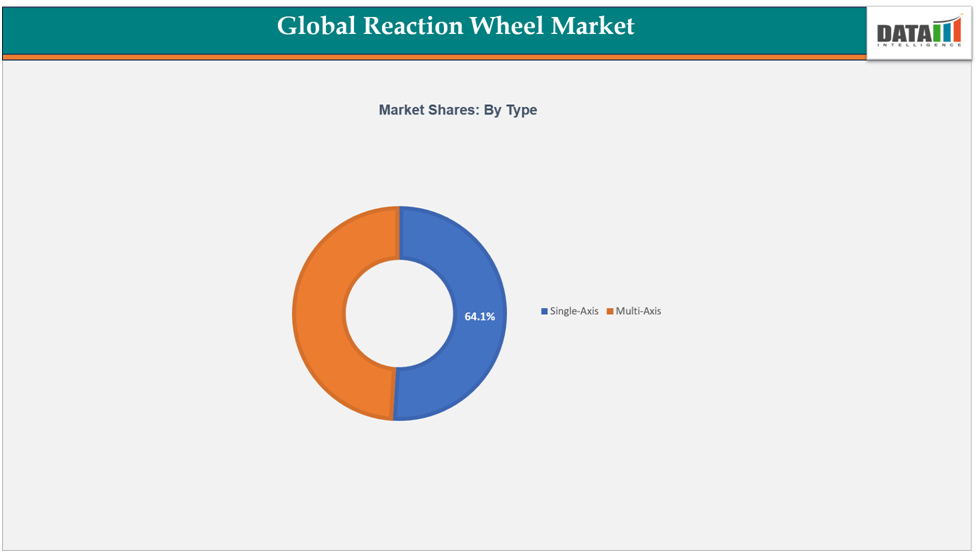

- The Single-Axis segment captured 64.1% market share, highlighting its continued importance across communication, navigation, and Earth observation missions.

- The market is expected to expand from US$ 276.03 million in 2025 to US$ 2.31 billion by 2035, reflecting substantial demand growth from satellite constellations and space exploration programs.

- Asia-Pacific represents the fastest-growing regional opportunity due to increasing investments from China, Japan, and India in domestic space infrastructure.

- Commercial operators are emerging as major purchasers of reaction wheel systems as broadband satellite constellations continue expanding.

- Reliability improvement remains a key competitive differentiator, with manufacturers focusing on vibration reduction, redundancy architecture, and extended operational life.

- Defense modernization and sovereign space capabilities are creating sustained procurement opportunities for Reaction Wheel top companies across multiple regions.

Market Scope

| Metrics | Details |

| Market Size (2025) | US$ 276.03 Million |

| Market Size (2035) | US$ 2.31 Billion |

| CAGR (2026-2035) | 23.70% |

| Historic Years | 2023-2024 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Segments Covered | Type, Satellite Type, Angular Momentum, End User, Region |

| Leading Region | North America |

| Fastest Growing Region | Asia-Pacific |

Growth Catalysts Reshaping Industry Demand

Small Satellite Programs Continue to Expand Procurement Volumes

The strongest demand signal for the reaction wheel industry comes from the rapid deployment of CubeSats, nanosatellites, and microsatellites. These platforms require highly compact attitude control systems capable of maintaining stable pointing accuracy despite strict size and power constraints.

Earth observation, secure communications, climate monitoring, navigation, and intelligence missions increasingly rely on small satellite architectures. Organizations such as Planet Labs and ISRO have demonstrated the operational value of reaction-wheel-equipped satellites for precision imaging and mission performance. As constellation operators scale deployments into hundreds or thousands of satellites, reaction wheel procurement volumes are expected to rise significantly.

Defense and National Security Space Programs Drive Premium Demand

Defense agencies increasingly require resilient spacecraft capable of operating in contested environments. Precision orientation control is essential for reconnaissance, missile warning, surveillance, and secure communication systems.

Governments across North America, Europe, and Asia-Pacific are allocating larger budgets toward indigenous space capabilities. This trend benefits manufacturers capable of delivering high-reliability reaction wheels with enhanced fault tolerance and mission longevity.

Deep-Space Exploration Raises Performance Requirements

Interplanetary missions, scientific exploration programs, and advanced navigation systems require highly reliable attitude control technologies. Japan's Hayabusa-2 mission demonstrated the importance of sophisticated reaction wheel architectures for long-duration space missions.

As lunar and deep-space exploration programs accelerate, demand for advanced reaction wheels with higher torque capabilities and extended operational lifecycles is expected to increase.

Technology Risks and Reliability Challenges

Despite strong growth prospects, technical limitations remain an important consideration for spacecraft manufacturers and mission planners.

Reaction wheels experience continuous mechanical stress throughout their operational life. Bearing degradation, vibration generation, lubrication challenges, and motor failures can affect spacecraft performance. Historical incidents, including reaction wheel failures on NASA's Kepler mission, illustrate the potential consequences of component malfunction.

Manufacturers continue investing in advanced materials, improved bearing technologies, health monitoring systems, and redundancy architectures to mitigate operational risks and improve mission reliability.

Supply Chain and Manufacturing Ecosystem Analysis

Unlike many conventional aerospace components, reaction wheel manufacturing depends on a highly specialized supply chain that combines precision mechanical engineering, advanced electronics, sensors, and spacecraft-grade materials.

Supply Chain Map

The value chain typically includes:

- Specialty materials suppliers

- Precision bearing manufacturers

- Space-grade electronics providers

- Motor and actuator manufacturers

- Satellite subsystem integrators

- Spacecraft OEMs

- Launch service providers

Material and Component Bottlenecks

Reaction wheel production depends on high-performance bearings, rare-earth magnetic materials, radiation-hardened electronics, and spacecraft-qualified control systems. Supply disruptions affecting aerospace-grade components can extend production timelines and increase procurement costs.

The growing competition for advanced electronics from defense systems, telecommunications infrastructure, and data center hardware may create component allocation challenges across the forecast period.

Advanced Electronics and Packaging Trends

Although reaction wheels are fundamentally electromechanical systems rather than semiconductor-intensive products, increasing onboard intelligence is driving greater use of advanced control electronics, miniaturized sensors, and high-density packaging solutions.

Manufacturers are integrating smarter diagnostics, predictive maintenance functions, and enhanced power management capabilities to improve mission performance and reliability.

Drivers & Restraints

Driver: Increasing Deployment of Small Satellites and CubeSats for Earth Observation, Communications, and Defense

The reaction wheel market has become an essential part of the global satellite ecosystem, providing precise attitude control systems that enable satellites to operate with accuracy and reliability. As the number of small satellite and CubeSat launches grows rapidly, demand for compact yet efficient reaction wheels is accelerating. These systems are indispensable for ensuring image clarity, stable communications, and reliable navigation in space missions.

For instance, Planet Labs expanded its Earth observation fleet with CubeSats fitted with advanced reaction wheel technology, significantly improving stability and imaging performance. Likewise, the Indian Space Research Organisation (ISRO) integrated reaction wheel-equipped satellites into its defense and earth observation missions. Such initiatives reflect how the surge in CubeSat and small satellite programs is boosting the adoption of reaction wheels, cementing their importance in supporting future commercial, scientific, and military missions.

Restraint: Operational Risks Including Vibration, Component Degradation, and Failure Vulnerabilities

While reaction wheels are crucial for satellite stability, they come with inherent technical limitations that pose risks to mission success. Problems such as vibration, bearing wear, and motor malfunctions can reduce performance over time. Since reaction wheels are often single points of failure, a malfunction may compromise or even end a mission unless costly redundancy measures are implemented.

For instance, NASA’s Kepler Space Telescope lost multiple reaction wheels during its mission, which curtailed its observational capacity and demonstrated the fragility of these systems. Similarly, several CubeSats in commercial constellations have experienced early mission termination due to wheel-related failures. These cases illustrate how reliability concerns remain a significant barrier for the reaction wheel market. Without continued advancements in materials, lubrication, and fail-safe design, technical risks are likely to limit wider adoption.

For more details on this report: Request for Sample

Segmentation Analysis

The global reaction wheel market is segmented based on type, satellite type angular momentum, end-user and region.

Type:

The Single-Axis reaction wheel segment is estimated to have 64.1% of the reaction wheel market share.

A key component in satellite attitude and stability control. By providing precise maneuvering along one axis, these wheels are essential for ensuring the accuracy and reliability of missions ranging from Earth observation and navigation to communications and defense applications.

Market expansion in this segment is largely fueled by the rapid rise of CubeSat and nanosatellite programs, where compact, lightweight, and cost-efficient single-axis wheels are the preferred choice. Established players such as Honeywell, Blue Canyon Technologies, and Sinclair Interplanetary (Rocket Lab) hold strong positions with proven technologies, while emerging companies are introducing miniaturized, high-torque solutions tailored to small satellite constellations and research missions.

Regional advancements are also shaping the market’s growth. The Indian Space Research Organization (ISRO) continues to integrate single-axis wheels into its small satellite initiatives, while Japan’s JAXA invests in innovative control technologies for both Earth observation and interplanetary exploration. Meanwhile, U.S.-based companies retain a leadership edge through cutting-edge R&D and partnerships with global satellite manufacturers and operators.

Looking forward, the single-axis segment is expected to maintain dominance, driven by rising demand from mega-constellations for broadband connectivity and expanding defense satellite programs. Although challenges such as mechanical wear and single-point failure risks remain, advancements in durable materials, redundancy systems, and miniaturization are anticipated to strengthen the growth outlook for this segment.

Geographical Analysis

The North America reaction wheel market was valued at 36.7%market share in 2024

North America stands as a central growth hub for the global reaction wheel market, supported by strong demand from defense, commercial satellite operators, and space exploration programs. The region benefits from NASA’s ongoing missions, private sector mega-constellations, and military-driven satellite expansion. In particular, U.S. firms continue to pioneer advanced reaction wheel technologies that enable precision attitude control for satellites of all sizes, from CubeSats to large spacecraft.

For instance, in 2025, Blue Canyon Technologies, a subsidiary of RTX (NYSE: RTX), recently unveiled its largest reaction wheel to date, the RW16 reaction wheel. Designed to deliver high torque for larger spacecraft, the RW16 highlights North America’s role in advancing next-generation attitude control systems without reliance on external propulsion. Similar innovations are being deployed across Earth observation, navigation, and defense missions, reinforcing the region’s technology leadership.

The Asia-Pacific reaction wheel market was valued at 17.3% market share in 2024

The Asia-Pacific reaction wheel market, by comparison, accounted for 23.05% of global share in 2024, driven by rising satellite programs in China, Japan, and India. Meanwhile, North America remains the largest regional contributor, with the U.S. anchoring market strength through its robust ecosystem of spacecraft integrators, defense contractors, and mission service providers.

Government initiatives such as the CHIPS and Science Act are further enhancing supply chain resilience and supporting domestic space technology manufacturing. While challenges such as high development costs and global competition persist, North America continues to be a cornerstone of the global reaction wheel industry, with its advanced R&D base and focus on reliable, high-performance satellite systems ensuring sustained growth in the years ahead.

Competitive Landscape

The major players in the reaction wheel market include Honeywell International Inc., Blue Canyon Technologies LLC, Moog Inc., Northrop Grumman, Rocket Lab USA, Bradford Space, AAC Clyde Space, New Space Systems, VECTRONIC Aerospace GmbH, Astro- und Feinwerktechnik Adlershof GmbH.

Honeywell International Inc.: Honeywell International Inc. is a leading player in the global reaction wheel market, specializing in advanced spacecraft control and navigation systems that support commercial, defense, and scientific missions. The company’s reaction wheels are engineered to deliver precise satellite attitude control, ensuring stability and accuracy for Earth observation, communications, and deep-space exploration. Its flagship reaction wheel technologies integrate high-torque performance, durability, and fault-tolerant design, making them essential for large spacecraft as well as growing small satellite constellations.

Key Developments

June 2026: The United States increased investments in satellite manufacturing and space exploration programs, supporting demand for advanced reaction wheel systems used in spacecraft attitude control, Earth observation missions, and national security satellites.

May 2026: Japan accelerated development of next-generation satellite technologies and small satellite constellations, strengthening adoption of high-precision reaction wheels for improved spacecraft maneuverability and mission performance.

April 2026: Leading aerospace and space technology companies expanded investments in advanced reaction wheel systems, focusing on enhanced reliability, miniaturization, and high-torque performance for commercial and government space missions.

March 2026: Satellite manufacturers increased deployment of reaction wheel assemblies in low Earth orbit (LEO) satellite constellations, supporting communication, navigation, remote sensing, and scientific research applications.

February 2026: Space technology providers strengthened research and development activities in lightweight materials, precision control systems, and energy-efficient reaction wheel technologies to improve spacecraft stability and operational lifespan.

January 2026: Governments, defense agencies, and commercial space companies expanded investments in space infrastructure, satellite deployment programs, and deep-space exploration initiatives, accelerating demand for advanced spacecraft attitude control solutions and reaction wheel technologies.

The global reaction wheel market report delivers a detailed analysis with 70 key tables, more than 64visually impactful figures, and 195 pages of expert insights, providing a complete view of the market landscape.