Nuclear Medicine Radioisotopes Market Size and Overview

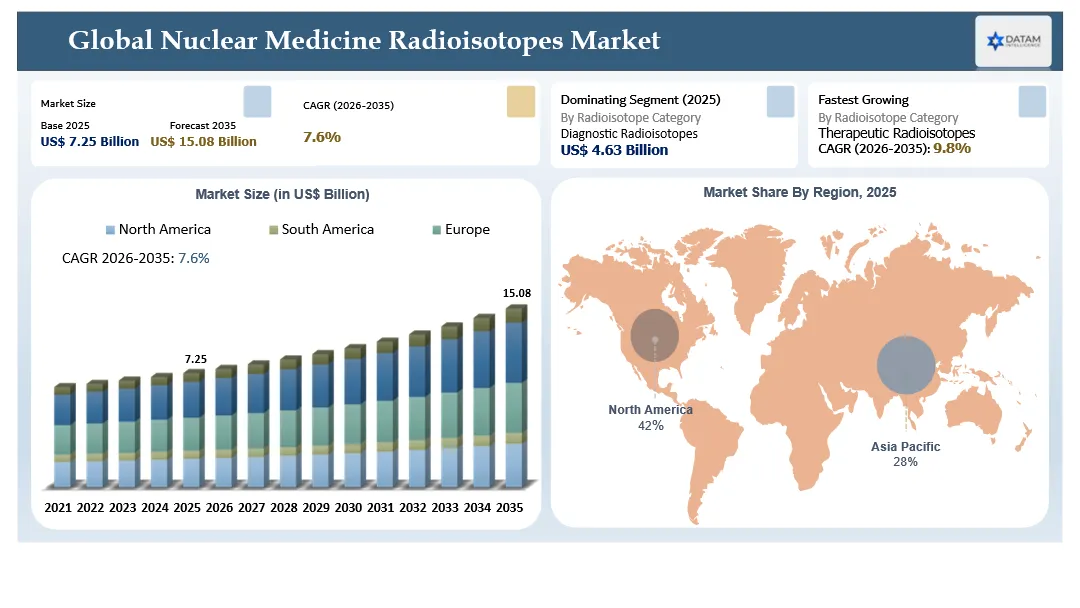

The global nuclear medicine radioisotopes market reached an estimated US$ 7.25 billion in 2025 and is projected to reach approximately US$ 15.08 billion by 2035, expanding at a CAGR of 7.6% during 2026-2035. The market is moving from a diagnostic-isotope model centered on technetium-99m and fluorine-18 toward a broader ecosystem that includes theranostic imaging, lutetium-177 radioligand therapy and targeted alpha therapy using actinium-225 and other emerging isotopes.

Demand is increasingly determined by treatment capacity and isotope supply security. Diagnostic procedures create recurring high-volume demand, while therapeutic isotopes generate higher value per patient and require tightly controlled manufacturing, radiolabeling and scheduling. Growth therefore depends on both clinical adoption and the construction of resilient production networks capable of supplying short-lived materials without interruption.

The US$ 450 million TerraPower Isotopes Bellwether Laboratory in Philadelphia provides a visible example of this investment cycle. The planned 250,000-square-foot facility is dedicated to actinium-225 production and is expected to create about 225 permanent jobs and 500 construction jobs. Its location at the redeveloped former Philadelphia refinery shows how isotope manufacturing is becoming a strategic life-sciences infrastructure category. The broader Bellwether District is planned for 14 million square feet of industrial, manufacturing and logistics space, approximately 19,000 jobs and an estimated US$ 40 million in annual tax revenue at full build-out.

For buyers, the market question is no longer limited to the price of an isotope dose. Hospitals, radiopharmacies and pharmaceutical developers need visibility into production route, radionuclidic purity, release testing, available activity, shipment radius, treatment scheduling, regulatory status and continuity of supply. Investors need to distinguish between high-volume diagnostic networks and higher-margin therapeutic isotope platforms.

| Metric | Details |

| 2025 Market Size | US$ 7.25 Billion |

| 2035 Projected Market Size | US$ 15.08 Billion |

| CAGR 2026-2035 | 7.6% |

| Largest Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Largest Isotope Category | Diagnostic isotopes led by Tc-99m/Mo-99 and F-18 |

| Fastest Growing Category | Therapeutic isotopes led by Lu-177 and Ac-225 |

| Core Opportunity | Production capacity, radiopharmacy networks, theranostics and targeted alpha therapy |

Nuclear Medicine Radioisotopes Market Key Takeaways

- The market is shifting toward therapeutic isotopes as radioligand therapy moves into larger oncology populations and pharmaceutical companies reserve isotope capacity earlier in development.

- North America leads through nuclear medicine procedure volume, pharmaceutical pipelines, radiopharmacy infrastructure and new production investment.

- Asia-Pacific is the fastest growing region as China, India, Japan, South Korea and Australia expand PET infrastructure, oncology capacity and domestic isotope production.

- Technetium-99m remains the largest volume isotope because SPECT continues to support cardiology, oncology, bone and organ imaging.

- Lutetium-177 is the strongest near-term therapeutic growth platform, while actinium-225 represents a high-value capacity-constrained opportunity in targeted alpha therapy.

- The Philadelphia Ac-225 project demonstrates that isotope scarcity can support hundreds of millions of dollars in dedicated manufacturing investment.

- Short half-lives make location, scheduling and logistics part of product value. Regional production and radiopharmacy density directly influence clinical adoption.

- Pharmaceutical developers are increasingly using isotope reservation, manufacturing partnerships and long-term offtake agreements to reduce clinical and launch risk.

Nuclear Medicine Radioisotopes Industry Trends and Strategic Insights

- Theranostics is linking diagnostic imaging and therapy through the same molecular target, creating paired demand for imaging and therapeutic isotopes.

- Radiopharmaceutical pipelines are increasing competition for Lu-177, Ac-225, Pb-212 and specialized precursor materials.

- Cyclotron networks are expanding because regional production improves resilience for F-18, C-11, N-13, O-15, Cu-64 and Zr-89.

- Non-uranium and non-reactor production routes are receiving more attention as buyers seek lower dependence on aging research reactors.

- Centralized radiopharmacies are becoming platform operators that combine dose preparation, quality control, logistics, data and regulatory services.

- Hospital investment is shifting toward dedicated theranostic centers with hot cells, shielding, dosimetry, waste management and trained clinical teams.

Why Does This Report Matter in 2026?

In 2026, nuclear medicine radioisotopes are becoming a strategic manufacturing and healthcare-capacity issue. The expansion of radioligand therapy has exposed constraints in isotope supply, sterile fill-finish capacity, hospital treatment slots and qualified personnel. A therapy cannot scale solely because it receives regulatory approval. Commercial adoption also requires isotope production, validated radiolabeling, dependable shipment, radiation-safe administration and patient scheduling.

This report converts those constraints into investable opportunity areas. It identifies where new reactors, accelerators, cyclotrons, generators, radiopharmacies and contract manufacturing facilities are needed. It also assesses which isotopes have credible clinical demand, where capacity is concentrated and which supply models can support regional expansion.

Nuclear Medicine Radioisotopes Market White Space and Investment Opportunities

- Dedicated Ac-225 production facilities, purification systems and distribution networks for targeted alpha therapy.

- Lu-177 production and radiolabeling capacity linked to prostate cancer, neuroendocrine tumor and pipeline indications.

- Regional cyclotron and radiopharmacy networks serving cities without reliable access to short-lived PET isotopes.

- Generator platforms for Ga-68, Rb-82 and other isotopes that reduce dependence on nearby cyclotrons.

- Contract development and manufacturing organizations specializing in radioactive APIs, sterile preparation and clinical supply.

- Digital scheduling and dose-management platforms connecting producers, radiopharmacies, hospitals and patient appointments.

- Dosimetry, radiation safety, waste handling and staff training services for new theranostic centers.

- Brownfield conversion into secure, regulated isotope manufacturing campuses, as demonstrated by the Bellwether project in Philadelphia.

Nuclear Medicine Radioisotopes Future Market Transformation

The market is expected to evolve into a networked radionuclide platform industry. Diagnostic isotopes will remain essential, but value creation will increasingly come from therapeutic isotopes, proprietary ligands, manufacturing integration and capacity assurance. Pharmaceutical companies will compete for access to isotopes before pivotal trials, and producers will move closer to drug developers through co-development, reservation and offtake structures.

Production will become more diversified. Reactor supply will remain important for Mo-99 and selected therapeutic isotopes, while accelerators, cyclotrons and generators will expand. The winning model will combine high-purity production, redundant sites, regulatory support, rapid release testing and dependable logistics.

Nuclear Medicine Radioisotopes Market Buyer Decision-Making Criteria

Buyers evaluate suppliers based on available activity, radionuclidic purity, specific activity, batch consistency, GMP compliance, regulatory documentation, shipment reliability, shelf life, waste profile and technical support. Pharmaceutical companies also assess scale-up capability, reservation rights, geographic redundancy, clinical-trial support and commercial-launch readiness. Hospitals prioritize delivery windows, dose flexibility, reimbursement, staff workload and the ability to coordinate imaging or treatment appointments.

| Criterion | Buyer Question | Commercial Implication |

| Radionuclidic and chemical purity | Does the material meet product and clinical specifications? | Determines qualification, patient safety and usable yield. |

| Supply reliability | Can the supplier deliver during outages or transport disruption? | Drives dual sourcing and reservation agreements. |

| GMP documentation | Are release testing, traceability and deviation controls adequate? | Critical for clinical trials and commercial drug supply. |

| Logistics radius | Can activity arrive within the required decay window? | Defines addressable hospitals and radiopharmacies. |

| Commercial scale readiness | Can output expand with indication and patient growth? | Influences pharmaceutical launch risk. |

| Technical support | Can the supplier support labeling, dosimetry and regulatory filings? | Raises switching costs and partnership value. |

Nuclear Medicine Radioisotopes Market Economic and Investment Analysis

The market has two distinct investment profiles. Diagnostic isotope infrastructure relies on high procedure volumes, dense delivery routes and efficient radiopharmacy operations. Therapeutic isotope infrastructure carries higher manufacturing complexity and lower initial volume, but it can support greater value per dose and long-term pharmaceutical contracts. Capital allocation is therefore moving toward facilities that can support multiple isotopes, several radioligand programs and both clinical and commercial production.

TerraPower Isotopes’ US$ 450 million Philadelphia project is a major capacity signal for Ac-225. The 250,000-square-foot facility is intended to address a bottleneck that limits targeted alpha therapy trials and future commercialization. The project is also expected to support 225 permanent positions and 500 construction jobs, indicating that isotope capacity can become an anchor for regional life-sciences manufacturing.

Nuclear Medicine Radioisotopes Market Investment Trends

- Large-scale investment in Ac-225, Lu-177 and Pb-212 production to serve radioligand pipelines.

- Expansion of radiopharmacy networks and same-day distribution around metropolitan treatment clusters.

- New hot-cell, shielding, automated dispensing and quality-control equipment for hospital and contract manufacturing sites.

- Long-term isotope reservation agreements that improve bankability for new production facilities.

- Localization programs intended to reduce dependence on imported Mo-99, generators or therapeutic isotopes.

- Acquisition of radiopharmaceutical developers and manufacturing assets by pharmaceutical and healthcare companies.

Nuclear Medicine Radioisotopes Market Strategic Indicators

High Regulation Impact

Licensing, radiation safety, GMP controls, transport rules and product-specific approvals influence every stage from target irradiation to patient administration.

High Investment Activity

Capacity spending is strongest in therapeutic isotope production, radiopharmaceutical manufacturing, radiopharmacy distribution and treatment-center infrastructure.

Supply Chain Disruption

A reactor outage, target shortage, processing interruption or transport delay can cancel procedures because many isotopes cannot be stockpiled for long periods.

Pricing and Contracting Pressure

Pricing reflects isotope scarcity, activity, purity, logistics and contract certainty. Therapeutic suppliers increasingly seek multi-year commitments.

New Technology Adoption

Accelerator production, automated radiochemistry, digital dosimetry, AI-assisted imaging and theranostic pairing are changing the value chain.

Regional Expansion Opportunity

North America and Europe lead current capacity, while Asia-Pacific offers the strongest expansion potential through new hospitals and localized production.

Government Policy Support

National isotope strategies, research reactor funding, accelerator programs and cancer-care investment can reduce supply dependence.

Pricing Intelligence

| Pricing Factor | Buyer Impact | Strategic Interpretation |

| Isotope scarcity | Higher reservation and batch pricing | Capacity-constrained isotopes support premium contracts. |

| Half-life | Higher logistics and wastage exposure | Regional production can improve delivered economics. |

| Specific activity and purity | Affects labeling efficiency and dose quality | High-specification supply commands stronger value. |

| Contract duration | Balances security and flexibility | Multi-year commitments can finance capacity expansion. |

| Regulatory package | Reduces buyer qualification burden | Documentation can be a competitive differentiator. |

Nuclear Medicine Radioisotopes Market AI Impact and Disruption Analysis

AI Impact Analysis

AI is beginning to improve nuclear medicine through image reconstruction, lesion detection, treatment planning, dosimetry and production scheduling. In isotope operations, machine learning can forecast dose demand by site, optimize irradiation and processing sequences, identify quality deviations and reduce decay-related waste. In clinical workflows, AI can support patient selection, quantify uptake and standardize response assessment. Suppliers that connect production data with hospital scheduling can improve utilization across a regional network.

Disruption Analysis

Three disruptions will reshape the market. Therapeutic isotopes are shifting value from high-volume diagnostics toward high-value oncology supply. Distributed cyclotron and generator models are reducing dependence on selected centralized routes. Pharmaceutical companies are integrating isotope access into drug-development strategy through acquisitions, partnerships and capacity reservations. These shifts favor platforms that control several stages of the value chain.

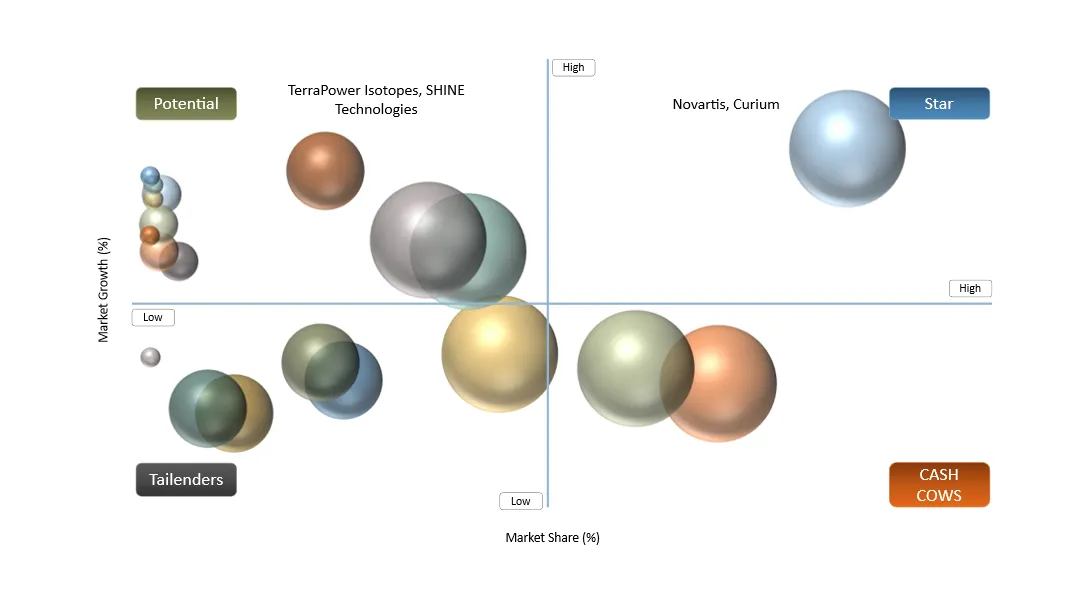

Nuclear Medicine Radioisotopes Market BCG Matrix

| Category | Representative Companies | Strategic Position |

| Stars | Novartis, Curium, Cardinal Health, ITM, Telix | Strong commercial reach, radiopharmaceutical portfolios or integrated supply. |

| Potential Stars | TerraPower Isotopes, SHINE Technologies, NorthStar, BWXT Medical | Capacity expansion and differentiated production technologies. |

| Cash Generators | Established Tc-99m, F-18 and radio pharmacy networks | Recurring diagnostic demand and regional distribution density. |

| Emerging Platforms | Pb-212, Tb-161 and novel alpha-emitter developers | High clinical potential with earlier commercial maturity. |

Nuclear Medicine Radioisotopes Market Dynamics

| Driver | Growth Impact | Demand Concentration | Strategic Impact |

| Radioligand therapy expansion | High | Oncology centers and pharmaceutical pipelines | Raises demand for Lu-177, Ac-225 and manufacturing partnerships. |

| PET and SPECT procedure growth | High | Hospitals and imaging centers | Supports recurring demand for Tc-99m, F-18 and Ga-68. |

| Theranostic adoption | High | Prostate cancer and neuroendocrine tumors | Creates paired diagnostic and therapeutic isotope demand. |

| Production localization | Medium-High | North America, Europe, Asia-Pacific | Reduces import dependence and creates regional infrastructure opportunities. |

| Hospital capacity investment | Medium-High | Cancer centers | Expands treatment slots, hot cells, dosimetry and staffing. |

Driver: Radioligand Therapy Is Converting Isotope Supply into Strategic Pharmaceutical Infrastructure

Radioligand therapy links a targeting molecule with a therapeutic radioisotope, allowing radiation to be delivered directly to cells expressing a specific biomarker. As approved therapies expand and late-stage pipelines mature, isotope supply becomes a launch-critical input. Pharmaceutical companies therefore need to secure production, radiolabeling and distribution years before commercialization. This creates recurring opportunities for isotope producers, contract manufacturers and radiopharmacies.

| Restraint | Drag on Growth | Primary Impact | Strategic Effect |

| Short half-life and logistics | High | Dose delivery and scheduling | Limits service radius and raises cancellation risk. |

| Concentrated production | High | Mo-99, Lu-177 and Ac-225 supply | Creates exposure to facility outages and target shortages. |

| High facility investment | Medium-High | New producers and hospitals | Slows market entry and regional capacity expansion. |

| Regulatory complexity | Medium-High | Clinical and commercial supply | Extends qualification and approval timelines. |

| Workforce shortage | Medium | Nuclear medicine departments | Constrains treatment capacity even when isotope is available. |

Restraint: Production Capacity and Clinical Capacity Must Expand Together

Additional isotope output does not automatically translate into patient treatment. Hospitals require licensed facilities, nuclear medicine physicians, pharmacists, technologists, physicists, radiation safety officers and waste-management processes. Therapeutic procedures can occupy treatment rooms for long periods and require coordinated dosimetry and follow-up. Market growth therefore depends on parallel investment in production and care delivery.

Nuclear Medicine Radioisotopes Market Segment Analysis

The market is segmented by radioisotope, modality, application, production route, end user, supply model and region. This expanded structure captures the commercial differences between high-volume diagnostic isotopes, high-value therapeutic isotopes and emerging alpha emitters.

Segmentation by Radioisotope

Diagnostic Radioisotopes

Technetium-99m and its parent molybdenum-99 remain the foundation of SPECT imaging because of broad clinical use and established generator distribution. Fluorine-18 supports PET oncology, neurology and cardiology through radiotracers such as FDG and newer targeted agents. Gallium-68 is central to theranostic imaging in prostate cancer and neuroendocrine tumors. Rubidium-82 supports cardiac PET, while iodine-123, thallium-201, copper-64 and zirconium-89 serve specialized imaging applications.

Therapeutic Radioisotopes

Lutetium-177 leads current therapeutic growth due to established radioligand use and a broad development pipeline. Iodine-131 remains important for thyroid disease. Yttrium-90 and radium-223 maintain selected oncology roles. Actinium-225 is the most strategically constrained emerging isotope because it delivers high-energy alpha radiation over a short tissue range and has attracted dedicated capacity investment. Lead-212 and terbium-161 are emerging platforms that may diversify future therapeutic supply.

Segmentation by Modality

PET is expanding through oncology and neurology tracers, while SPECT retains a large installed base and procedure volume. Targeted beta therapy remains the most commercially developed therapeutic modality. Targeted alpha therapy is earlier but offers high biological potency and is driving investment in Ac-225 and Pb-212. Theranostic pairs connect diagnostic imaging with therapy selection and monitoring.

Segmentation by Application

Oncology is the largest and fastest-evolving application because nuclear medicine supports staging, treatment selection, targeted therapy and response monitoring. Cardiology remains a major diagnostic segment through myocardial perfusion and viability imaging. Neurology is growing through dementia, movement-disorder and brain-tumor imaging. Endocrinology and thyroid applications remain established through iodine isotopes. Bone imaging and inflammatory applications create additional recurring demand.

Segmentation by Production Route

Nuclear reactors remain important for Mo-99 and selected therapeutic isotopes. Cyclotrons support short-lived PET isotopes and are expanding into new production pathways. Linear accelerators and spallation systems can increase access to scarce isotopes such as Ac-225. Generator systems decentralize supply for Tc-99m, Ga-68 and Rb-82. The market is moving toward mixed production portfolios because no single route can serve all isotopes efficiently.

Segmentation by End User

Hospitals and cancer centers purchase patient-ready doses and invest in treatment infrastructure. Imaging centers create recurring diagnostic demand. Nuclear pharmacies aggregate production, preparation and logistics. Pharmaceutical companies require isotope access for trials and commercial products. Academic institutes support tracer development and early clinical translation. Contract manufacturers provide specialized radiolabeling, sterile filling, quality control and distribution.

Segmentation by Supply Model

Centralized production is efficient for longer-lived isotopes and high-volume processing. Regional radiopharmacy networks reduce delivery distances. On-site cyclotrons support short-lived PET isotopes in high-volume centers. Generator-based supply allows decentralized access without a nearby reactor or cyclotron. Long-term reservation and offtake agreements are becoming more important for therapeutic isotopes because capacity must be secured before launch.

Nuclear Medicine Radioisotopes Market Geographical Penetration

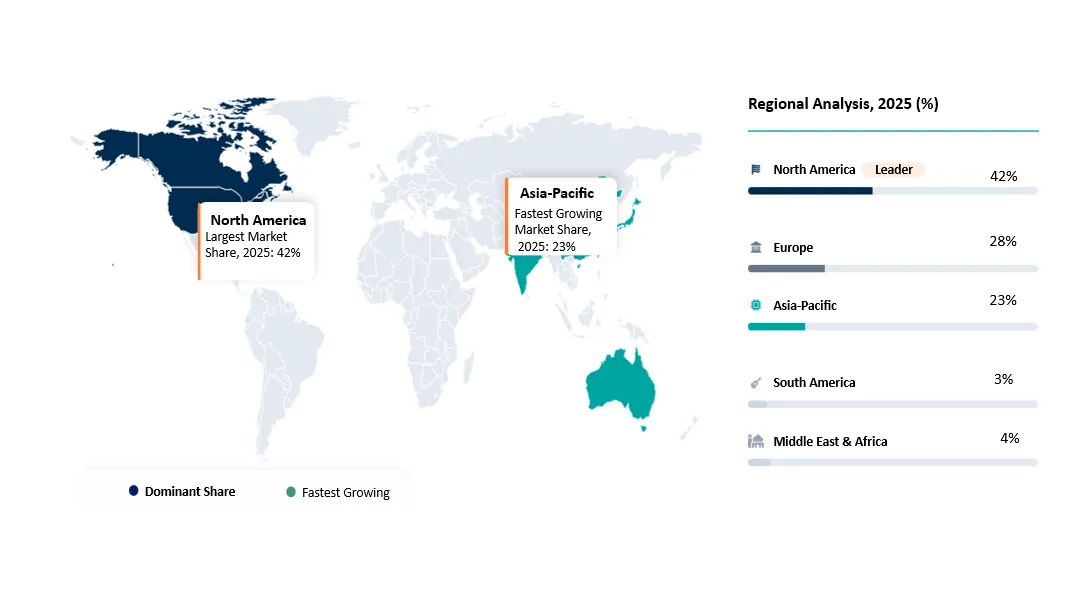

| Region | Indicative 2025 Share | Market Position | Primary Opportunity |

| North America | 42% | Largest | Radioligand therapy, Ac-225 capacity and radiopharmacy networks |

| Europe | 28% | Established production base | Reactor replacement, Lu-177 and cross-border supply resilience |

| Asia-Pacific | 23% | Fastest growing | Cyclotron expansion, hospital infrastructure and localization |

| South America | 3% | Developing | Regional radiopharmacies and oncology access |

| Middle East and Africa | 4% | Emerging | New nuclear medicine centers and imported isotope substitution |

North America Market Outlook

North America leads through large imaging volumes, a dense radiopharmacy network and strong pharmaceutical investment in radioligand therapy. The U.S. opportunity spans Ac-225 production, Lu-177 capacity, contract radiopharmaceutical manufacturing and hospital treatment-center expansion. The Bellwether Laboratory in Philadelphia represents a US$ 450 million commitment to Ac-225 capacity. Canada remains strategically important through reactor expertise, isotope technology and therapeutic isotope initiatives. Mexico offers growth through private imaging networks and cancer-care investment, but supply reliability varies by location.

Europe Market Outlook

Europe has a mature nuclear medicine ecosystem supported by research reactors, isotope processors, radiopharmaceutical companies and university hospitals. Germany, France, the Netherlands, Belgium and the UK are important production or clinical hubs. The key investment themes are reactor replacement, processing redundancy, Lu-177 supply, radioligand manufacturing and cross-border logistics. European policy increasingly emphasizes supply sovereignty because reactor outages can affect multiple countries simultaneously.

Asia-Pacific Market Outlook

Asia-Pacific is the fastest growing region because China, India, Japan, South Korea and Australia are expanding oncology capacity and PET infrastructure. China is increasing domestic isotope and radiopharmaceutical capabilities. India combines a large patient base with nuclear research and cost-efficient pharmaceutical manufacturing. Japan has advanced nuclear medicine adoption and local radiopharmaceutical expertise. Australia is attracting therapeutic isotope and radioligand development activity. Regional investors can target cyclotron networks, hospital partnerships and local generator production.

South America Market Outlook

Brazil and Argentina anchor the region through nuclear research, radiopharmaceutical production and large urban healthcare systems. Growth opportunities include regional radiopharmacy networks, PET access outside major cities and partnerships that reduce dependence on imported isotopes. Clinical adoption is influenced by reimbursement, public hospital budgets and logistics across large territories.

Middle East and Africa Market Outlook

The UAE, Saudi Arabia, Israel, Turkiye and South Africa have the strongest near-term opportunities. Gulf countries are investing in cancer centers and advanced imaging, creating demand for imported isotopes and local cyclotron capacity. South Africa has established isotope production capabilities and can support regional supply. Israel and Turkiye offer clinical expertise and research activity. The wider region requires dependable distribution, workforce training and radiation-safety infrastructure.

Nuclear Medicine Radioisotopes Market Competitive Landscape

- Competition is shifting from individual isotope sales toward integrated production, radiopharmaceutical manufacturing, regulatory support and distribution.

- Large healthcare distributors compete through radiopharmacy scale and hospital reach.

- Pharmaceutical companies are securing isotope access through ownership, partnerships and long-term supply agreements.

- Specialist producers compete on purity, specific activity, production reliability and ability to support clinical-to-commercial scale-up.

- Regional players gain value where short half-lives make local production and distribution essential.

- Ac-225 and other alpha emitters are creating a new competitive layer involving accelerator technology, target material and purification expertise.

Key Companies

- Cardinal Health (United States)

- Curium (France)

- Lantheus Holdings (United States)

- Novartis (Switzerland)

- Bayer (Germany)

- GE HealthCare (United States)

- Jubilant Radiopharma (United States)

- NorthStar Medical Radioisotopes (United States)

- SHINE Technologies (United States)

- NTP Radioisotopes (South Africa)

- Nordion (Canada)

- Eckert & Ziegler (Germany)

- Telix Pharmaceuticals (Australia)

- ITM Isotope Technologies Munich (Germany)

- TerraPower Isotopes (United States)

- Isotope JSC (Hungary)

- China Isotope & Radiation Corporation (China)

- BWXT Medical (Canada)

- IRE / IRE ELiT (Belgium)

- Bruce Power / Isogen (Canada)

Nuclear Medicine Radioisotopes Market Competitive Positioning Matrix

| Company Type | Core Strength | Growth Route |

| Integrated pharmaceutical company | Approved radioligand products and pipeline | Secure isotope supply and expand treatment indications |

| Healthcare distributor / radiopharmacy | Hospital reach and dose logistics | Add therapeutic preparation and digital scheduling |

| Specialist isotope producer | Production technology and purity | Build capacity and sign long-term offtake |

| Contract manufacturer | GMP radiolabeling and sterile operations | Support clinical-to-commercial programs |

| Regional producer | Local delivery advantage | Expand cyclotron, generator and hospital partnerships |

Nuclear Medicine Radioisotopes Market Major Pain Points

- Limited availability of Ac-225 and other alpha emitters.

- Dependence on a small number of reactors or processors for selected isotopes.

- Procedure cancellations caused by shipment delays or production interruptions.

- Limited hospital treatment slots and shortages of trained nuclear medicine staff.

- Complex licensing, transport and waste-management requirements.

- Difficulties scaling radiopharmaceutical manufacturing from trials to commercial demand.

- Reimbursement variation across diagnostic and therapeutic procedures.

- Need for synchronized production, dose release and patient scheduling.

Nuclear Medicine Radioisotopes Market Recent Developments

- June 2026: TerraPower Isotopes highlighted plans for the Bellwether Laboratory in South Philadelphia, a 250,000-square-foot Ac-225 facility supported by approximately US$ 450 million in investment. The project is expected to create around 225 permanent jobs and 500 construction jobs.

- March 2026: Reporting on the former Philadelphia Energy Solutions refinery redevelopment described TerraPower Isotopes as an anchor life-sciences tenant at the 1,300-acre Bellwether District. The full district is planned for 14 million square feet and about 19,000 jobs.

- 2025-2026: Radiopharmaceutical developers continued expanding pipelines in prostate cancer, neuroendocrine tumors and other solid tumors, increasing demand for Lu-177, Ac-225 and companion diagnostic isotopes.

- 2025-2026: Isotope producers and healthcare companies increased investment in accelerator-based production, generator systems and regional radiopharmacy capacity to reduce supply concentration.

- 2025-2026: Hospitals and cancer centers expanded theranostic programs, creating demand for hot cells, dosimetry, radiation safety and patient scheduling capabilities.

Analyst View on Nuclear Medicine Radioisotopes Market

- The next phase of growth will be constrained more by production and treatment capacity than by clinical interest.

- Lu-177 will remain the main near-term therapeutic isotope platform, while Ac-225 will attract the most strategic capacity investment.

- Diagnostic isotopes will continue to provide stable procedure volume and distribution economics.

- Companies that combine isotope access, drug development, manufacturing and clinical logistics will capture more value than single-stage suppliers.

- Regional redundancy will become a procurement requirement as pharmaceutical companies and hospitals reduce exposure to single-site failures.

- The strongest investment cases will be facilities backed by long-term pharmaceutical demand or radiopharmacy networks.

Nuclear Medicine Radioisotopes Market Target Audience

| Industry | Who Should Buy This Report? | Reason to Buy |

| Isotope Producers | Reactor, accelerator, cyclotron and generator operators | Assess demand by isotope, region, application and supply model. |

| Pharmaceutical Companies | Radioligand developers, business development and manufacturing teams | Secure isotope access, identify partners and plan launch capacity. |

| Hospitals and Cancer Centers | Nuclear medicine heads, radiopharmacy teams and administrators | Evaluate procedure growth, capacity requirements and supply risk. |

| Radiopharmacies | National and regional pharmacy networks | Identify high-growth therapeutic preparation and distribution opportunities. |

| Equipment Suppliers | Cyclotron, hot-cell, shielding, dispensing and QC companies | Map facility expansion and technology spending. |

| Investors and Consultants | Private equity, infrastructure funds and strategy teams | Screen isotope facilities, radiopharmacy networks and contract manufacturers. |

| Government and Nuclear Agencies | Policy, isotope security and healthcare planners | Assess supply dependence, localization priorities and capacity gaps. |

Why Choose DataM?

- Data-driven analysis of isotope demand, production routes, radiopharmacy coverage and treatment-capacity constraints.

- Post-purchase analyst support to validate assumptions, regional opportunities and supplier strategies.

- Quarterly white papers and case studies covering theranostics, Ac-225, Lu-177, isotope security and radiopharmacy models.

- Annual updates reflecting approvals, capacity projects, clinical pipelines and supply disruptions.

- Detailed emerging-market analysis across Asia-Pacific, the Middle East, South America and Africa.

- Buyer-focused insight connecting isotope availability with commercial launch, hospital adoption and investment requirements.

What DataM Uniquely Provides

- Ten-year forecasts by isotope, modality, application, production route, end user, supply model and region.

- Isotope supply-risk analysis covering production concentration, half-life, logistics, purity and redundancy.

- Therapeutic isotope opportunity mapping across Lu-177, Ac-225, Pb-212, Ra-223 and emerging radionuclides.

- Investment analysis for reactors, accelerators, cyclotrons, generators, radiopharmacies and hospital treatment centers.

- Country-level recommendations for producers, pharmaceutical companies, hospitals and investors.

- Competitive intelligence on partnerships, capacity commitments, pipeline alignment and regional expansion.

Questions This Report Answers

- Which radioisotopes will generate the strongest commercial growth through 2035?

- Where are the largest production and treatment-capacity gaps?

- How will radioligand therapy alter demand for Lu-177, Ac-225 and companion diagnostics?

- Which production routes offer the strongest opportunity for each isotope?

- How should pharmaceutical companies secure isotope capacity before launch?

- Which countries offer the best opportunities for cyclotron networks and regional radiopharmacies?

- What business models can reduce risk for new isotope manufacturing facilities?

- Which companies are best positioned across production, radiopharmacy and radioligand therapy?