Skin Cancer Market Size & Industry Outlook

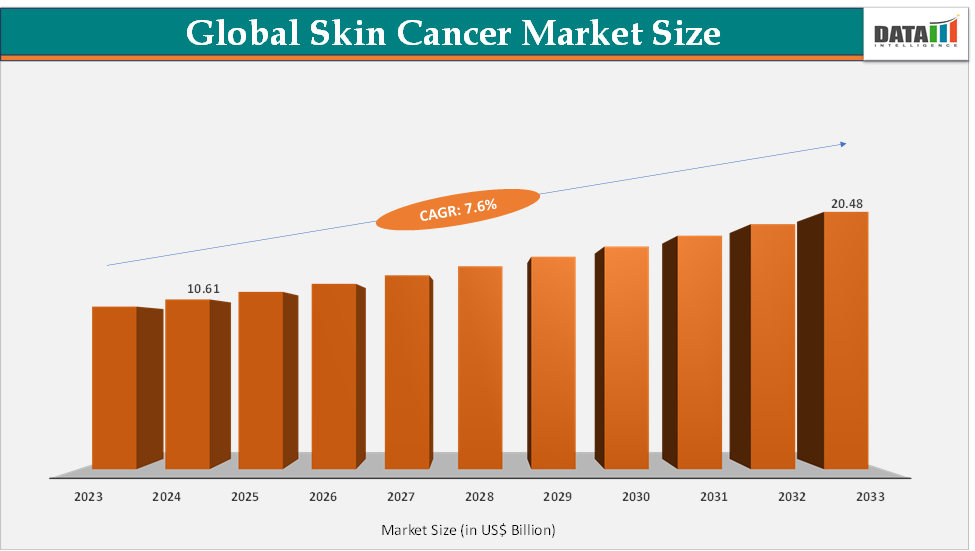

The global skin cancer market size reached US$ 10.61 Billion in 2024 from US$ 9.92 Billion in 2023 and is expected to reach US$ 20.48 Billion by 2033, growing at a CAGR of 7.6% during the forecast period 2025-2033.

The market is evolving rapidly, driven by rising global incidence of melanoma and non-melanoma cases due to increased UV exposure, aging populations, and improved screening awareness. Immunotherapies like PD-1 inhibitors, BRAF/MEK targeted regimens, and hedgehog pathway inhibitors are transforming standards of care, while novel modalities such as mRNA vaccines and TIL therapies are progressing through clinical trials. Alongside these advances, the growing role of teledermatology and digital health tools highlights a shift toward earlier intervention and decentralized care delivery.

Key Market Trends & Insights

Key trends shaping the skin cancer market include the integration of AI and digital health tools, with solutions like AI-powered dermatoscopes and teledermatology platforms gaining adoption for early detection and remote triage. In therapeutics, immuno-oncology continues to dominate, with PD-1 inhibitors expanding into earlier-stage melanoma and combination regimens showing durable survival benefits.

Targeted therapies like BRAF/MEK inhibitors and hedgehog pathway drugs remain critical in biomarker-driven care, while emerging modalities such as mRNA vaccines and tumor-infiltrating lymphocyte (TIL) therapies are advancing through late-stage clinical trials.

There is also a notable push toward adjuvant and neoadjuvant therapy adoption in high-risk patients, reflecting a shift to earlier intervention strategies. Finally, the market is witnessing strong growth, supported by patient demand for less invasive, cost-effective treatment pathways.

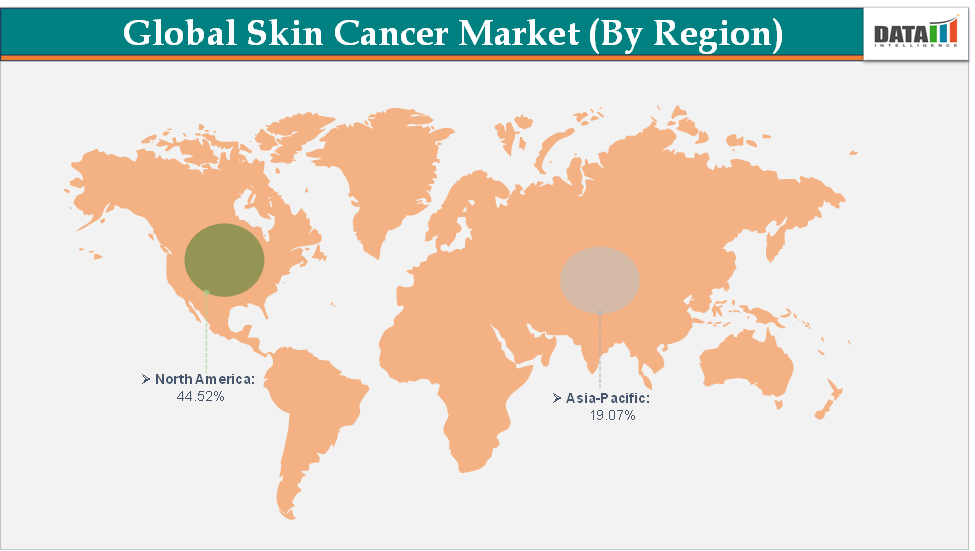

North America dominates the skin cancer market with the largest revenue share of 44.52% in 2024.

The Asia Pacific is the fastest-growing region and is expected to grow at the fastest CAGR of 7.1% over the forecast period.

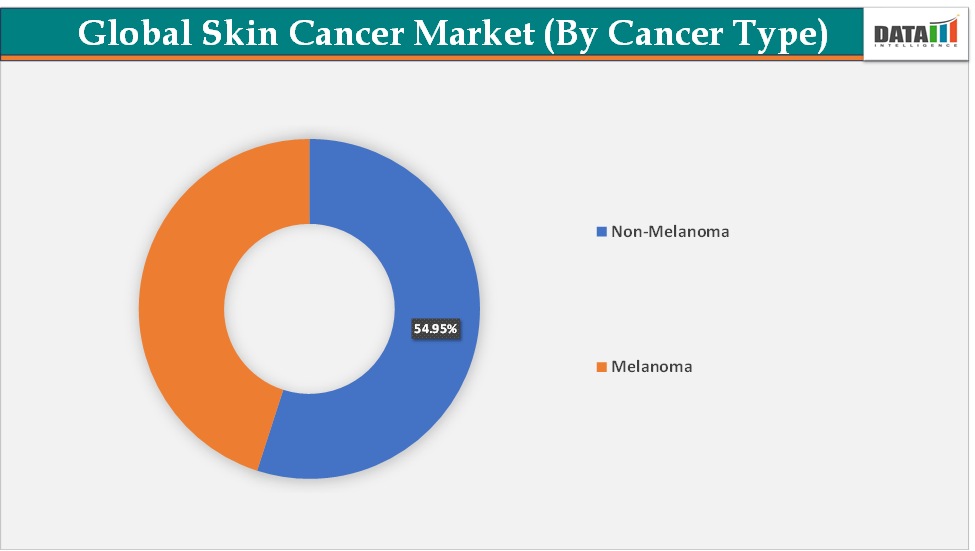

Based on cancer type, the non-melanoma segment led the market with the largest revenue share of 54.95% in 2024.

The major market players in the skin cancer market are Merck & Co., Inc., Amgen, Inc., Pfizer Inc., Genentech USA, Inc., Regeneron Pharmaceuticals, Inc., Bristol-Myers Squibb Company, Sun Pharmaceutical Industries, Inc., Immunocore Ltd., IOVANCE Biotherapeutics, Inc., and Incyte among others

Market Size & Forecast

2024 Market Size: US$ 10.61 Billion

2033 Projected Market Size: US$ 20.48 Billion

CAGR (2025–2033): 7.6%

North America: Largest market in 2024

Asia Pacific: Fastest-growing market

For more details on this report – Request for Sample

Market Dynamics

Drivers:

The rising incidence of skin cancer cases is significantly driving the skin cancer market growth

The global burden of skin cancer is rising alarmingly new cases surged, for instance, according to the Skin Cancer Foundation, in the U.S., more than 9,500 people are diagnosed with skin cancer every day. More than two people die of the disease every hour. Actinic keratosis is the most common precancer, it affects more than 58 million Americans. This surge in cases is fueling unprecedented demand for market.

This epidemiology rise is fueling adoption of checkpoint inhibitors such as pembrolizumab and nivolumab, which are now used not only in advanced melanoma but also in adjuvant and neoadjuvant settings, broadening their market share. Similarly, BRAF/MEK targeted therapies like dabrafenib plus trametinib are in strong demand for biomarker-positive melanoma patients, while hedgehog pathway inhibitors such as vismodegib and sonidegib address advanced basal cell carcinoma cases that are inoperable.

Even topical agents like imiquimod and 5-fluorouracil are seeing heightened usage in non-melanoma cancers due to increased diagnoses at early stage. Moreover, clinical innovation pipelines, such as mRNA-based melanoma vaccines, tumor-infiltrating lymphocyte (TIL) therapies, and intralesional oncolytic viruses are positioned to capture expanding patient segments as incidence continues to rise. Thus, the growing prevalence of skin cancer is not only creating a larger treated population but also driving the rapid uptake and diversification of therapeutic products across oncology markets.

Restraints:

The high cost of advanced therapies is hampering the growth of the skin cancer market

The high cost of advanced therapies remains a major restraint in the skin cancer market, significantly limiting access and adoption despite their proven clinical benefits. Modern treatments such as immune checkpoint inhibitors (pembrolizumab, nivolumab) and targeted agents (BRAF/MEK inhibitors for melanoma or hedgehog inhibitors like vismodegib for basal cell carcinoma) can cost patients and healthcare systems, placing immense financial pressure on payers and families.

For instance, according to the Skin Cancer Foundation, the annual cost of treating skin cancers in the U.S. is estimated at $8.1 billion, about $4.8 billion for nonmelanoma skin cancers and $3.3 billion for melanoma. These high costs not only hinder equitable patient access but also slow down market penetration in emerging economies, where incidence is rising but advanced care infrastructure and funding remain inadequate. As a result, while innovation is expanding therapeutic options, the pricing barrier acts as a drag on overall market growth, reinforcing the need for sustainable pricing models, broader reimbursement frameworks, and the development of cost-effective alternatives.

Skin Cancer Market Segment Analysis

The global skin cancer market is segmented based on cancer type, treatment, end-user, and region.

Cancer Type:

The non-melanoma segment is dominating the skin cancer market with a 54.95% share in 2024

The non-melanoma skin cancer segment, comprising primarily basal cell carcinoma (BCC) and cutaneous squamous cell carcinoma (cSCC), dominates the skin cancer market by sheer incidence and treatment volume, even though melanoma attracts more R&D and premium therapeutics. Globally, NMSCs account for nearly 90% of all skin cancer diagnoses, with the American Cancer Society estimating 3.6 million new BCC cases and 1.8 million new cSCC cases annually in the U.S. alone. This overwhelming caseload drives consistent demand for market.

For advanced cases, systemic therapies like hedgehog pathway inhibitors (vismodegib, sonidegib) have opened a new therapeutic avenue, addressing previously untreatable BCCs, though high costs limit broad use. The NMSC segment also benefits from field cancerization management, where large areas of sun-damaged skin are treated to prevent progression to invasive disease, further fueling use of topicals and PDT.

Basal cell carcinoma is far more common than squamous cell carcinoma. About 80% of non-melanoma skin cancers are basal cell carcinoma. Thus, it is the most common malignancy in the United States, with substantial associated morbidity and cost and relatively small but significant mortality. Treatment for non-melanoma skin cancer is usually successful, as unlike the other types of cancer, there's a significantly lower risk of cancer spreading to other parts of the body. Treatment for non-melanoma skin cancer is successful in approximately 90% of cases. Hence, the increasing rates of non-melanoma skin cancer and its success rates after treatment will drive the market's growth in the forecast period.

End-User:

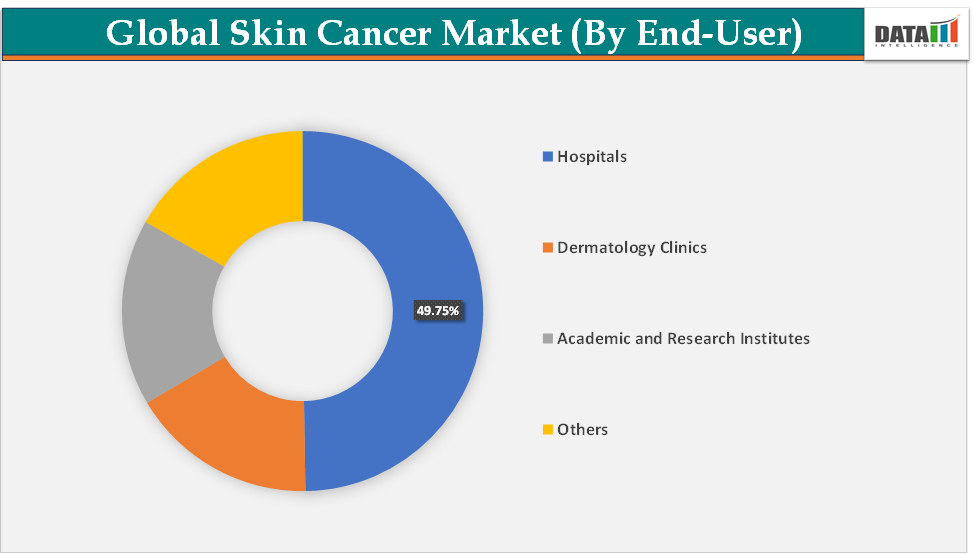

The hospitals segment is dominating the skin cancer market with a 49.75% share in 2024

The hospitals segment is dominating the global skin cancer market due to its central role in diagnosis, treatment, and post-treatment care, supported by advanced infrastructure and multidisciplinary expertise. Hospitals handle the bulk of skin biopsies and histopathology tests, which are critical for confirming melanoma and non-melanoma cases, and they are typically well-equipped to improve diagnostic accuracy. In terms of therapeutics, hospitals dominate because they are the only settings capable of administering advanced immunotherapies like pembrolizumab (Keytruda) and nivolumab (Opdivo), or targeted therapies such as dabrafenib plus trametinib for BRAF-mutant melanoma.

Hospitals also manage patients on hedgehog inhibitors (vismodegib, sonidegib) for advanced basal cell carcinoma, which require close monitoring due to safety concerns. In countries like the US, hospitals lead large-scale screening programs and awareness campaigns, which drive early detection and patient referrals. Additionally, hospitals are the hub for clinical trials of cutting-edge modalities like mRNA melanoma vaccines, TIL therapies, and oncolytic viruses, further strengthening their market dominance. Given their concentration of specialized oncologists, dermatologists, pathologists, and advanced technologies, hospitals not only dominate patient care pathways but also capture the largest revenue share in the skin cancer market, making them the cornerstone of both diagnostic and therapeutic growth.

Market Geographical Analysis

North America is expected to dominate the global skin cancer market with a 44.52% in 2024

North America dominates the global skin cancer market due to its high disease prevalence, advanced healthcare infrastructure, and strong adoption of innovative diagnostics and therapeutics. The US dominates the market in the North America region with an 86.12% share in 2024, and it records some of the highest incidence rates globally, with the Skin Cancer Foundation projecting about 212,200 new melanoma cases in 2025, alongside millions of non-melanoma cases annually, making skin cancer the most common cancer in the country. This enormous patient pool drives steady demand for the market, with North America accounting for the largest installed base of digital dermatoscopes, reflectance confocal microscopy (RCM), and optical coherence tomography (OCT) systems.

North America has been the earliest and fastest adopter of immuno-oncology drugs, with checkpoint inhibitors such as pembrolizumab (Keytruda) and nivolumab (Opdivo) widely prescribed for melanoma and covered under major reimbursement frameworks. Similarly, targeted therapies like dabrafenib/trametinib for BRAF-mutant melanoma and hedgehog inhibitors (vismodegib, sonidegib) for advanced basal cell carcinoma are routinely available, ensuring premium revenue streams for pharmaceutical companies.

Favorable reimbursement, well-structured awareness programs like Skin Cancer Awareness Month, and a high concentration of dermatology specialists create an environment conducive to both diagnostic and therapeutic growth. Collectively, these factors position North America as the largest and most lucrative region in the global skin cancer market, with sustained leadership driven by its combination of high incidence, innovation, and healthcare accessibility.

The Asia Pacific region is the fastest-growing region in the global skin cancer market, with a CAGR of 7.1% in 2024

The Asia Pacific (APAC) region is emerging as the fastest-growing segment of the global skin cancer market, driven by rising incidence, improving healthcare infrastructure, and rapid adoption of innovative therapies and diagnostics. While historically considered a low-incidence region, changing lifestyles, urbanization, and increasing UV exposure are contributing to a sharp rise in both melanoma and non-melanoma cases. For instance, China has reported increasing non-melanoma skin cancer mortality over the last three decades, signaling a significant epidemiological shift.

Growing awareness campaigns across India, Japan, and South Korea are further expanding screening uptake and encouraging preventive care. The region has rapidly adopted immuno-oncology drugs like pembrolizumab and nivolumab, alongside targeted therapies for biomarker-positive melanoma, supported by government-led efforts to expand oncology drug reimbursement. Local companies are also investing in biosimilars and cost-effective generics, making advanced treatments more accessible to a broader population.

Skin Cancer Market Top Companies

Top companies in the skin cancer market include Merck & Co., Inc., Amgen, Inc., Pfizer Inc., Genentech USA, Inc., Regeneron Pharmaceuticals, Inc., Bristol-Myers Squibb Company, Sun Pharmaceutical Industries, Inc., Immunocore Ltd., IOVANCE Biotherapeutics, Inc. and Incyte, among others.

Recent Developments

In May 2025, Intermountain Health has launched a new program to provide tumor-infiltrating lymphocyte (TIL) therapy to treat patients with a type of skin cancer called unresectable or metastatic melanoma that cannot be removed surgically or has spread to other parts of the body. As part of the treatment process, doctors use AMTAGVI, the first and only FDA-approved prescription medication for the treatment of advanced melanoma that has not responded to standard therapies. AMTAGVI activates the patient's own immune system to target and destroy cancer cells and represents a different approach compared to other immunotherapies. Instead of broadly stimulating the immune system, it harnesses a patient's own tumor-specific T cells to directly target and destroy cancer cells.

Skin Cancer Market Scope

Metrics | Details | |

CAGR | 7.6% | |

Market Size Available for Years | 2022-2033 | |

Estimation Forecast Period | 2025-2033 | |

Revenue Units | Value (US$ Bn) | |

Segments Covered | Cancer Type | Non-Melanoma and Melanoma |

Treatment | Immunotherapy, Chemotherapy, Photodynamic Therapy, Targeted Therapy, Radiation Therapy, and Others | |

End-User | Hospitals, Dermatology Clinics, Academic and Research Institutes, and Others | |

Regions Covered | North America, Europe, Asia-Pacific, South America and the Middle East & Africa | |

The global skin cancer market report delivers a detailed analysis with 62 key tables, more than 55 visually impactful figures, and 159 pages of expert insights, providing a complete view of the market landscape.