eVTOL Aircraft Market Overview

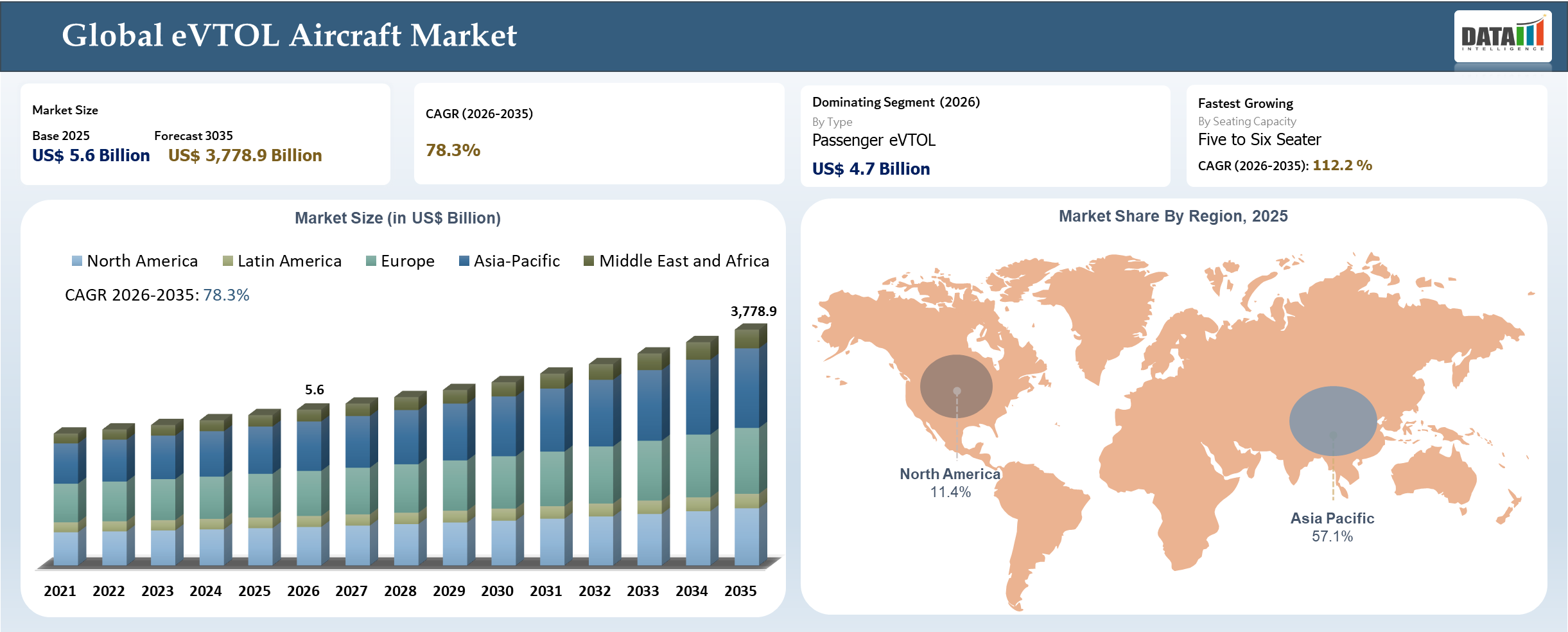

The global eVTOL aircraft market reached US$ 5.6 billion in 2026 and is expected to reach US$ 3,778.9 billion by 2035, growing with a CAGR of 78.3% during the forecast period 2032-2035. It will make a big impact on the way we think about air travel in cities and surrounding areas. It is happening because of technology like electric motors, computers that can fly planes and materials that are very light.

It is simpler compared to regular helicopters because they do not have complicated gear systems, which means they can have many small motors that help keep them safe if one motor stops working. According to NASA, electric motors are better than motors because they are more reliable and make less noise and also cause pollution, which is important for cities.

eVTOL Aircraft Industry Trends and Strategic Insights

- Several governments are supporting companies in developing vertical take-off and landing (VTOL) flying cars by providing financial assistance and regulatory guidance. For example, US Air Force has a program called Agility Prime that is helping these companies get their vertical take-off and landing aircraft certified to fly.

- For vertical take-off and landing flying cars to achieve long-term success, companies must ensure compliance with standardized global regulations, develop airport infrastructure compatible with their operations and achieve cost-efficient manufacturing across all types of electric vertical take-off and land flying car.

Market Scope

| Metrics | Details | |

| 2026 Market Size | US$ 5.7 Billion | |

| 2035 Projected Market Size | US$ 3,855.1 Billion | |

| CAGR (2032-2035) | 78.5% | |

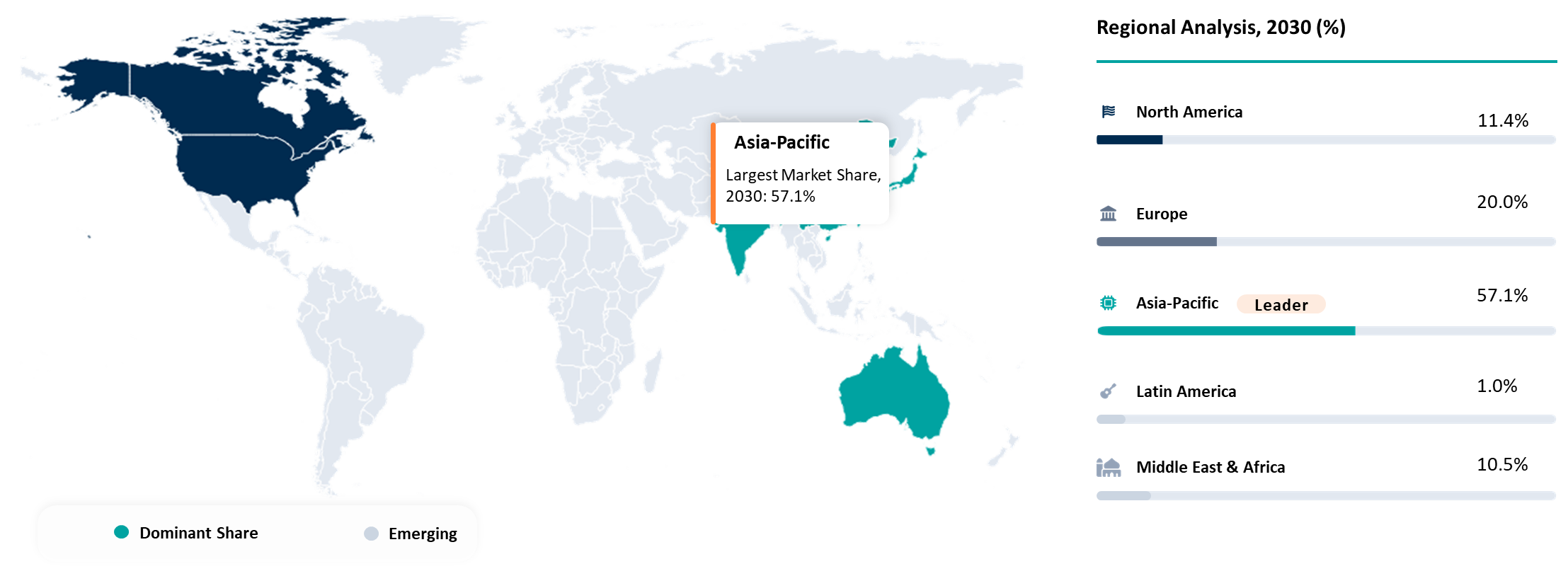

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Middle East and Africa | |

| By Type | Passenger eVTOL, Cargo eVTOL and Emergency & Special Mission eVTOL | |

| By Mode of Operation | Piloted, Autonomous, and Semi Autonomous | |

| By Seating Capacity | Single Seater, Two Seater, Three to Four Seater, Five to Six Seater, and More than Six Seater | |

| By Lift Technology Architecture | Multirotor, Lift & Cruise, Tiltrotor, Tiltwing, Ducted Fan, and Hybrid Configurations | |

| By Propulsion Type | Fully Electric, Hybrid Electric, and Hydrogen Fuel Cell | |

| By Range | Short Range (<50 km), Medium Range (50–150 km), and Long Range (>150 km) | |

| By Maximum Take-Off Weight (MTOW) | Less than 1,000 kg, 1,000–2,000 kg, and More than 2,000 kg | |

| By Battery Capacity (kWh Bands) | Below 100 kWh, 100–200 kWh, 200–350 kWh, 350–500 kWh, and Above 500 kWh | |

| By Certification Status | Concept Design Phase, Prototype (Flight Testing Phase), Pre-Certification (Type Certification in Progress), Certified (Type Certified Aircraft), and Commercial Operations Approved | |

| By Production Capacity Level (Annual Units) | R&D & Prototype Only (<10 units per year), Low-Rate Initial Production (10–100 units per year), Scaled Production (100–500 units per year), and Mass Production (>500 units per year) | |

| By Cruise Speed | Below 150 km per hour, 150 to 250 km per hour, and Above 250 km per hour | |

| By Charging Infrastructure | Battery Electric Charging, Hydrogen Refueling, and Hybrid Fuel Systems | |

| By Ownership Model | Fleet Based Operations, Private Ownership, and Government Procurement | |

| By Aircraft Price (ASP Band) | Below US$ 1.5 Billion, US$ 1.5 – 3 Billion, US$ 3 – 5 Billion, and Above US$ 5 Billion | |

| By Application | Air Taxi Passenger Transport, Cargo and Logistics, Defense and Military, Medical Evacuation Air Ambulance, Personal Mobility, and Tourism and Leisure Flights | |

| By End-User | Commercial Operators, Fleet Aggregators, Government & Defense, Emergency Services, and Private Owners | |

| By Region | North America | USA, Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Norway, Netherlands, Sweden, Denmark, Belgium, Switzerland, Austria, Poland, Finland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Egypt, Turkey, Qatar, Kuwait, Oman, Bahrain | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

AI Impact Analysis

The development of Artificial Intelligence technology is becoming increasingly important for accelerating the process of bringing eVTOL aircraft into mass production, especially in facilitating their autonomous and semi-autonomous operation. Flight control systems based on AI are reducing reliance on pilots while ensuring safe and efficient flights in congested urban areas. In addition, advanced AI solutions can be used in air traffic management systems that will help coordinate flights at low altitudes, which is essential for the successful implementation of urban air mobility on a massive scale.

Moreover, AI technology is revolutionizing fleet management and operation processes by optimizing the maintenance process and fleet performance. Machine learning-based predictive analytics is increasing aircraft efficiency by minimizing downtime and maximizing their use, which is particularly important for start-ups with small fleets of planes. Furthermore, AI is helping develop effective forecasting, routing, and pricing strategies for air taxi companies.

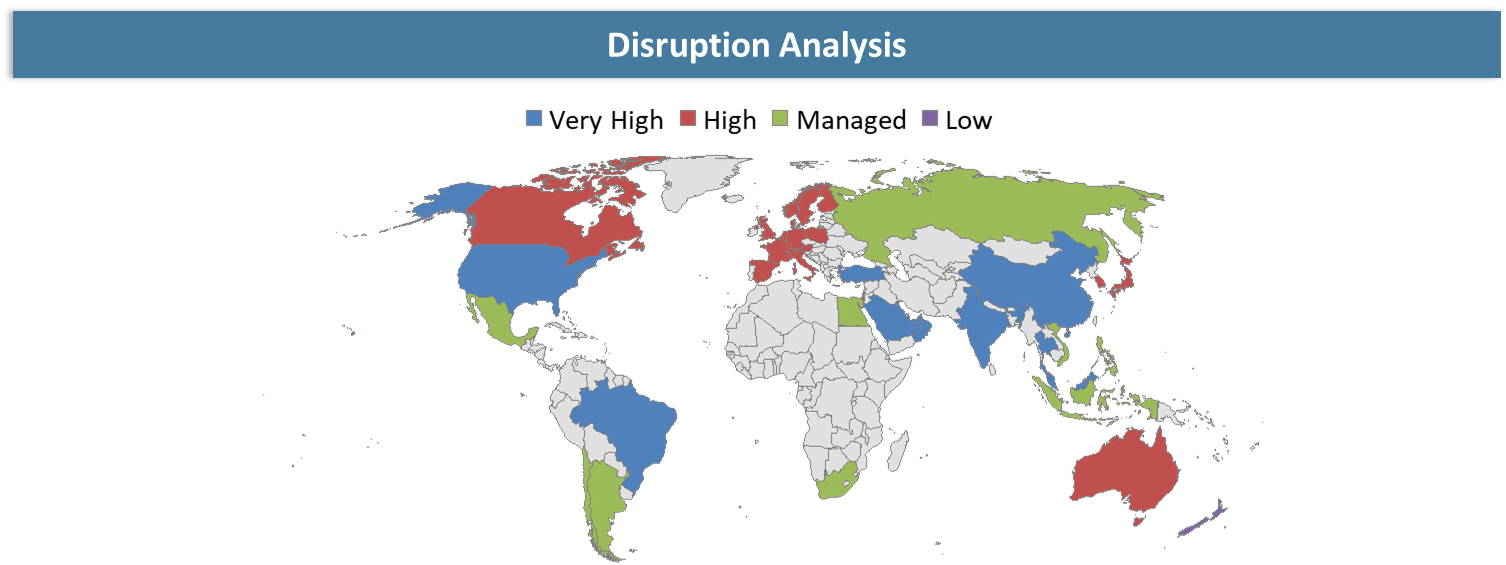

Disruption Analysis

EVTOL aircraft will disrupt traditional transportation and aviation industries through the introduction of the next generation of transportation modes that move freely in the air above ground transport infrastructure challenges. Unlike the typical aviation model that operates in an extensive airport-based model, eVTOL aircraft have adopted the vertiport concept where eVTOL aircraft connect points within a city to another. In addition, the adoption of such vehicles is set to redefine the economic dynamics of mobility through reduced travel times and introduction of new premium transportation categories.

A further disruption brought about by the adoption of eVTOL aircraft is the convergence of automotive and aviation. The introduction of these vehicles means that there is competition between traditional OEMs and aviation firms in addition to newer start-up enterprises. There is also an element of challenging the regulations through innovations that need to be introduced. EVTOL aircraft have forced aviation authorities to create new certification regimes based on electricity-powered eVTOL aircraft and autonomous systems.

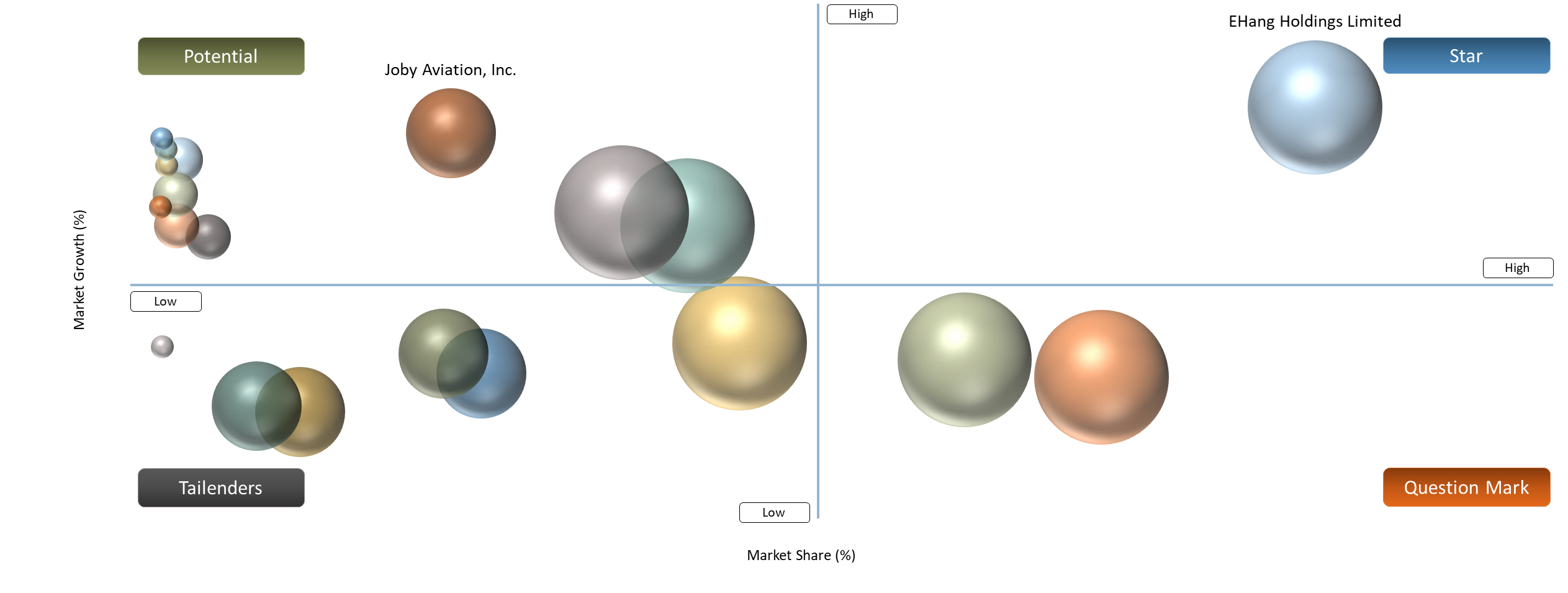

BCG Matrix: Company Evaluation

The competitive structure of the eVTOL aircraft industry can be successfully assessed by means of applying BCG matrix analysis based on technology maturity and commercialization preparedness of organizations. Stars refer to commercial organizations with successful regulatory compliance and imminent capability of commercial deployments, especially those that enter commercial markets at the earliest stage possible. They are set to dominate the market during the phase of commercial deployments of eVTOL aircraft.

Emerging players refer to innovative companies whose commercial success is currently lacking because their main objective lies in research & development activities. Their future market position is contingent upon certification and funding success. Examples of emerging players involve companies involved in developing niche application such as road cars or personal mobility. On the other hand, the Pervasive Players category involves well-funded aerospace and auto companies that have taken up positions in the flying car industry.

Market Dynamics

Massive capital injections from automotive OEMs and venture capital firms

The eVTOL ecosystem is experiencing unprecedented capital inflows, driven by both traditional automotive OEMs and venture capital investors, signaling strong institutional confidence in the sector’s long-term viability. Automotive OEMs are facing structural disruption pressures electrification, automation and shared mobility. Flying cars represent a strategic adjacency, allowing OEMs to extend their mobility portfolios beyond ground transportation into aerial domains. The diversification is not opportunistic but defensive, aimed at maintaining relevance in a rapidly evolving mobility landscape.

Venture capital firms are aggressively investing in eVTOL startups due to the sector’s high innovation intensity and platform scalability potential. Unlike incremental automotive innovations, flying cars represent a category defining technology, capable of creating entirely new markets such as aerial ride-hailing, intercity air taxis and drone logistics.

Large-scale funding is enabling rapid prototyping and pilot deployments, which are essential for regulatory certification and public acceptance. The transition from concept to commercialization in aviation is capital-intensive and sustained funding ensures that companies can navigate long development cycles and stringent safety requirements. Flying cars are positioned at the intersection of aerospace, automotive and technology sectors, making them attractive for diversified investment portfolios. The narrative of “next-generation mobility” further enhances investor appetite, particularly in regions prioritizing smart city development.

Technical risks regarding thermal runaway and energy storage system failures

Battery technology remains the backbone and Achilles’ heel of flying cars. Most eVTOL aircraft rely on high-density lithium-ion battery systems, which introduce significant safety risks related to thermal runaway, a condition where battery cells overheat uncontrollably, potentially leading to fire or explosion. Institutions such as National Transportation Safety Board and International Civil Aviation Organization emphasize that aviation-grade energy systems must meet far stricter reliability and redundancy standards than automotive applications. Unlike ground vehicles, eVTOL aircraft operate in three-dimensional space where system failure has immediate catastrophic implications, leaving little margin for error.

Thermal runaway risks are exacerbated by high power density requirements. eVTOLs must deliver substantial bursts of energy during vertical take-off and landing phases, placing extreme stress on battery cells. This leads to accelerated degradation, reduced lifecycle and increased probability of failure. Furthermore, environmental conditions such as temperature fluctuations, humidity and vibration further impact battery performance and reliability.

Fire suppression in airborne battery systems also remains a challenge. Traditional aviation fuel fires are well-understood, but lithium battery fires behave differently often requiring specialized containment strategies. Aircraft design must incorporate redundant battery modules, thermal insulation and fail-safe isolation systems, increase weight and reduce payload efficiency.

Segment Analysis

The global eVTOL aircraft market is segmented based on type, mode of operation, seating capacity, lift technology architecture, propulsion type, range, maximum take-off weight (MTOW), battery capacity (kWh Bands), certification status, production capacity level (annual inputs), cruise speed, charging infrastructure, ownership model, aircraft price (ASP band), application, end-user and region.

Strategic Evolution and Operational Frameworks of Passenger eVTOL Mobility

Passenger eVTOL platforms are converging around 3-5 passenger capacity configurations, aligned with early-stage urban air taxi economics and regulatory frameworks. According to NASA, most near-term eVTOL flying cars are being built to carry up to five passengers, including the pilot and typically operate within a 60-mile range, which reflects the current battery limitations and the industry’s emphasis on short, frequent trips.

Fully electric systems lead early deployments due to lower mechanical complexity and reduced noise footprints, while hybrid-electric variants are gaining traction to address range and payload constraints.

It aligns with broader aviation decarbonization objectives, as eVTOL platforms are expected to generate significantly lower noise and emissions compared to conventional rotorcraft, enabling regulatory acceptance in dense urban environments.

Passenger eVTOLs are increasingly influenced by compatibility with vertiport networks, air traffic management systems and digital connectivity frameworks. It is positioned to redefine short-distance passenger transport through a combination of technological innovation, sustained investment and ecosystem-wide collaboration.

Geographical Penetration

Strengthening of regulatory landscape and government action plans supporting eVTOL aircraft requirements

North America eVTOL aircraft market is one of the largest and fastest-growing markets globally, will account for around 11% of the total market in 2030.

USA eVTOL Aircraft Market Trends

US Department of Transportation initiated a three-year pilot program for the early deployment of flying cars across various US regions, including New York, Texas and Florida. It marks the transition from prototype testing to controlled real-world operations, covering both passenger and cargo applications. Aircraft in this program will fly without full certification from the Federal Aviation Administration, under strict regulatory conditions. It reflects a phased commercialization strategy, allowing operational validation while certification processes are still underway, without bypassing safety requirements.

Leading manufacturers such as Archer Aviation, Joby Aviation, Beta Technologies and Electra.aero are actively participating, leveraging prior test flight experience and advancing toward certification milestones. It underscores US as a key innovation and deployment hub for advanced air mobility. It focuses on high-value use cases, including urban air taxi services, regional passenger transport, cargo logistics and emergency response. Operations are expected to utilize decentralized takeoff and landing infrastructure, enabling closer proximity to end-users and improving last-mile connectivity.

Canada eVTOL Aircraft Market Outlook

Canada is built on a foundation of rules and safety. The Canadian Aviation Regulations, led by Transport Canada, set a standard for the industry. For example, the Air Taxi Operations standard has requirements for certification, operations, aircraft systems and pilot training. Rules will help shape the future of flying cars in Canada.

Horizon Aircraft is making progress with its Cavorite X7 program. The program has done flight tests and aims to be ready for commercial use by 2026. It is a step from testing to real-world use. The flying car market in Canada prefers electric aircraft, which can go further, carry more and operate well in various conditions. Its focus is likely to help Canada with transportation, moving goods, medical help and defense.

Mexico eVTOL Aircraft Market Analysis

Mexico is supported by a regulatory framework led by the Federal Civil Aviation Agency under the Secretariat of Infrastructure, Communications and Transport. Recent reforms align with global aviation standards while balancing safety and operational flexibility, enhancing market accessibility and enabling smoother entry for eVTOL and air taxi operators.

It holds a strong advantage as an aerospace manufacturing hub, supported by the presence of Bombardier, Safran and Honeywell. A large, skilled engineering workforce and strengthening academia-industry collaboration further position the country to capture value across manufacturing, talent development and regional eVTOL operations.

Market is expected to be driven by different sectors, including city transportation, delivery, emergency medical services, tourism and connecting regions. It makes flying cars commercially viable and could have a bigger economic impact. Market expansion remains contingent on resolving critical gaps in UAM-specific regulations, vertiport infrastructure and energy systems. Mexico is positioning itself as a commercialization-driven market with strong potential to emerge as a regional hub for advanced air mobility, supported by regulatory alignment and cost efficiency.

Competitive Landscape

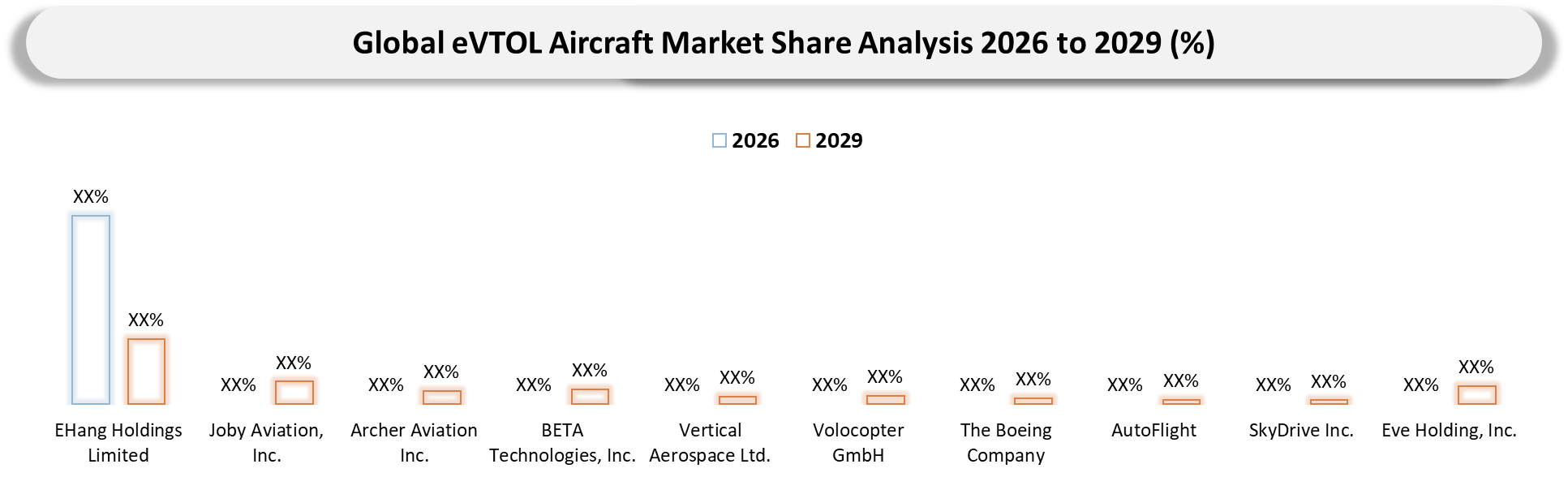

- Globally, only a handful of players have achieved flight tests due to stringent certification processes and UAM launches.

- Top five competitors include EHang Holdings Limited, Joby Aviation, Inc., Eve Holding, Inc., BETA Technologies, Inc. and Archer Aviation Inc., which will collectively account for a total market share of over 71% in 2029.

- Major other participants such as Volocopter GmbH, Vertical Aerospace Ltd. and The Boeing Company have made a significant mark in North American and European regions. Such companies are concentrating more on denser regions of Europe and America for conducting experimental flights to provide air taxi services commercially.

- Key players include EHang Holdings Limited, Joby Aviation, Inc., Archer Aviation Inc., Eve Holding, Inc., Vertical Aerospace Ltd., XPeng Inc., Honda Motor Co., Ltd., BETA Technologies, Inc., Volocopter GmbH, The Boeing Company, AutoFlight, SkyDrive Inc., Lilium GmbH, PAL-V International B.V., Geely Technology Group Co., Ltd., TCab Technology Co., Ltd., Guangzhou Automobile Group Co., Ltd., Jetson AB, Horizon Aircraft Ltd., AMSL Aero Pty Ltd, Airbus SE, Jaunt Air Mobility, LLC, Alauda Aeronautics Pty Ltd, Klein Vision, s.r.o., Overair, Inc., Doroni Aerospace, Inc., LIFT Aircraft Inc., Pivotal Aero, Inc., Elroy Air, Inc., XTI Aerospace, Inc., NFAS, Inc., Ryse Aero Technologies, Inc., Piasecki Aircraft Corporation, PteroDynamics, Inc., Electra.aero, Inc., Ascendance Flight Technologies SAS, Manta Aircraft S.r.l., Dufour Aerospace AG, Samad Aerospace Ltd., SkyFly Technologies Ltd., CycloTech GmbH, FlyNow Aviation GmbH, Crisalion Mobility S.L., Pipistrel d.o.o., Leonardo S.p.A., Sirius Aviation AG, AIR EV Ltd., Shanghai Volant Aerotech Co., Ltd., Bellwether Industries Limited, The ePlane Company, Sarla Aviation Private Limited, BluJ Aerospace Pvt. Ltd., Vela Aero, Muyutian Aviation Technology Jiangsu Co., Ltd., ZeroG Aircraft Industry Hefei Co., Ltd., Guangdong Seagull Flying Car Group Co., Ltd., and United Aircraft Group.

Key Developments

- March 2026: JETSON AB Began customer deliveries of the Jetson ONE personal eVTOL aircraft, marking transition from prototype to real-world use. The single-seat ultralight flying vehicle is positioned for personal air mobility and recreational flying.

- March 2026: Successful flight tests of the first production model of the Joby Aviation electric air taxi have been conducted. It is an important move toward getting approval from FAA, as it allows the aircraft to take off vertically with six rotors and accommodate a crew of one pilot and four passengers.

- March 2026: Generation 6 of the Boeing self-flying, four-passenger eVTOL air taxi is introduced into service. It is intended to facilitate autonomous urban transportation and it is also one of the primary contenders for FAA certification for an autonomous eVTOL carrying passengers.

- March 2026: Archer Aviation Inc. was chosen under the White House eVTOL Integration Pilot Program (eIPP). They will begin their operations in Texas, Florida and New York states. The program is run by US Department of Transportation and FAA and its purpose is to introduce electric taxis and develop regulations for the future commercial use of the aircraft.

- March 2026: SAMSON SKY, LLC signed an MoU with the Tajikistan government for regulation development, training pilots and selling fifty units.

- February 2026: AUTOFLIGHT launched and conducted public test flight of “Matrix”, a 5-tonne eVTOL aircraft, claimed to be the world’s largest flying car, capable of carrying up to 10 passengers or heavy cargo, marking a major scale-up in the flying car market.

- January 2026: XPeng Inc. Initiated test production at a ~10,000 units/year facility and advanced IPO plans, targeting late-2026 deliveries, marking the early industrialization of consumer-oriented eVTOL aircraft.

- January 2026: Horizon Aircraft unveiled key design upgrades for the full-scale Cavorite X7 hybrid eVTOL, including a 12-lift-fan configuration, improved aerodynamics and extended cabin for better passenger comfort. These enhancements focus on improving safety, performance and operational efficiency.

- January 2026: VOLOCOPTER GMBH Advanced toward EASA certification for VoloXPro light-sport eVTOL, while continuing certification efforts for the VoloCity passenger air taxi. This marks progress toward commercial deployment of urban air mobility services.

- December 2025: Eve Holding, Inc. successful maiden flight of the flying car prototype to validate critical systems such as propulsion, aircraft design and flight-by-wire systems. It marks the start of a more extensive flight testing program leading to certification and introduction into service.

- December 2025: Vertical Aerospace Ltd. launched its latest “Valo” eVTOL flying taxi for urban air mobility and use in passenger transportation, cargo and emergency missions. Features state-of-the-art fly-by-wire flight controls borrowed from military fighters and enhances safety features while also striving to achieve shorter transit times, such as 12 minutes to an airport in an urban setting.

- December 2025: EHang Holdings Limited engaged with Thailand’s government and aviation authorities to accelerate development of an urban air mobility ecosystem, including infrastructure, regulation and deployment of autonomous air taxis in Southeast Asia.

- October 2025: EHang Holdings Limited unveiled its next-generation VT-35 autonomous flying taxi, designed for intercity and cross-region travel. The aircraft expands range capabilities and integrates with existing EH216-S infrastructure, creating a scalable urban + regional air mobility ecosystem.

Why Choose DataM?

- Technological Innovations: Explores the latest advancements in eVTOL aircraft design, including improved hydraulic systems, advanced operator controls, telematics integration, electric and hybrid powertrains and enhanced attachment versatility that are driving higher productivity and lower operating costs across construction and industrial applications.

- Product Performance & Market Positioning: Evaluates how different OEMs perform in real-world construction, landscaping, agriculture and municipal environments. The analysis compares lifting capacity, breakout force, fuel efficiency, durability, operator comfort and attachment compatibility, highlighting how leading manufacturers differentiate themselves globally.

- Real-World Evidence: Highlights practical use cases of eVTOL aircraft across infrastructure development, road maintenance, warehouse handling and smart city projects. It demonstrates measurable improvements in jobsite efficiency, reduced labor dependency, faster material handling and optimized equipment utilization.

- Market Updates & Industry Changes: Tracks important industry developments such as new product launches, electrification initiatives, localized manufacturing expansions, tightening emission standards (Stage V, Tier 4 Final) and shifts in construction spending across major regions, including North America, APAC, China and India.

- Competitive Strategies: Analyzes how leading manufacturers are expanding their footprint through dealer network strengthening, localized production, electric model introductions, strategic partnerships and technology-driven differentiation such as AI-enabled monitoring and autonomous-ready platforms.

- Pricing & Market Access: Explains pricing structures across standard, high-capacity and electric skid steer models, including outright purchase, leasing and rental models. It also reviews regional availability, distribution networks and financing strategies that enhance market penetration.

- Market Entry & Expansion: Identifies growth opportunities in emerging economies driven by infrastructure development, urbanization, smart city programs and expanding rental ecosystems. It also outlines strategies for OEMs to scale operations globally through regional manufacturing hubs and after-sales service optimization.

Target Audience

- Urban Air Mobility Operators & Fleet Aggregators: Air taxi service providers, on-demand mobility platforms and fleet operators planning deployment of eVTOL aircraft for passenger and cargo transport across urban and intercity routes.

- Logistics & Cargo Companies: Express delivery firms, e-commerce logistics providers and last-mile delivery operators exploring cargo eVTOL solutions for high-value, time-sensitive shipments and remote connectivity.

- Government & Aviation Authorities: Civil aviation regulators, urban planning bodies and smart city authorities responsible for airspace management, vertiport infrastructure development and regulatory approvals for flying car operations.

- OEMs & Aerospace Manufacturers: eVTOL developers, aviation OEMs and automotive companies investing in flying car technologies for product development, certification strategies and global expansion.

- Defense & Emergency Service Agencies: Military organizations, disaster response units and medical evacuation providers leveraging eVTOL aircraft for surveillance, rapid response and critical mission operations.

- Infrastructure & Vertiport Developers: Companies involved in building vertiports, charging infrastructure, air traffic management systems and supporting ecosystem for urban air mobility deployment.

- Investors & Private Equity Firms: Venture capital firms, institutional investors and strategic investors tracking early-stage commercialization opportunities and long-term scalability of flying car technologies.

- Technology & AI Solution Providers: Companies offering autonomous flight systems, navigation software, battery technologies and digital platforms supporting the operational ecosystem of eVTOL aircraft.