Cobalt Recycling Market Size

The global Cobalt Recycling market reached US$ 1,600 million in 2025 and is expected to reach US$ 5,777.3 million by 2035, growing with a CAGR of 13.7% during the forecast period 2026-2035, due to the rapid phase-out of lithium-ion batteries from applications such as electric vehicles, energy storage solutions, and consumer electronics, resulting in ample availability of feedstock for secondary cobalt extraction. Innovations in hydrometallurgy and direct recycling methods have enabled efficient extraction and manufacturing of battery-grade cobalt compounds. Growing focus on critical minerals security, localization of the supply chain, and less reliance on primary cobalt mining operations have contributed to the development of the market. Market players are developing closed-loop recycling networks and collaborations with battery manufacturers and automotive original equipment manufacturers (OEMs) to access stable supplies of raw materials. Feedstock collection difficulties, cobalt price volatility, and complexities associated with processing varied types of battery chemistries affect the dynamics of the market

Key Takeaways

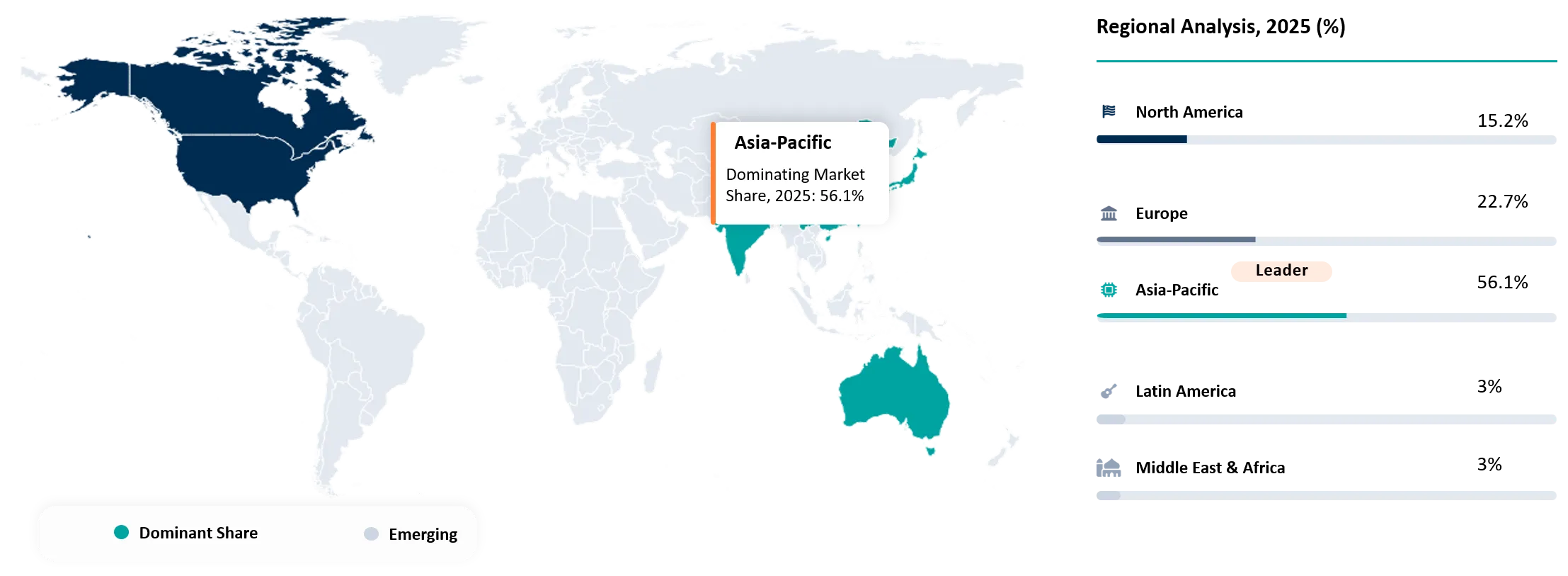

- Asia-Pacific region is deaminating the cobalt recycling market with the market share at 56.1% of the global market in 2025.

- Under Technology Type, Hydrometallurgical Recycling was the major technology in this market with a market share of 58.0% in 2025, due to the reason that Hydrometallurgical recycling has metal recovery rates of more than 95%.

- The total deployment of EV battery in terms of GWh was at 1.2 TWh in 2025, marking a yearly growth rate of 30%, thus providing a higher future feedstock for cobalt recycling.

- LFP batteries constituted about 50% of the total global EV batteries used in 2025, whereas the previous number was about 30%, influencing future cobalt recovery volumes.

- The share held by China in the Asia Pacific cobalt recycling market stood at 65.9% in 2025, owing to its vast battery recycling infrastructure.

Cobalt Recycling Market Industry Trends and Strategic Insight

- Hydrometallurgical and direct recycling processes are attracting significant investment due to the capability of recovering high-quality battery-grade cobalt from secondary resources with higher efficiency than pyrometallurgy.

- ESG requirements and traceability are becoming important competitive advantages, which is motivating recyclers to implement sophisticated traceability and chain-of-custody systems that provide ethically sourced products. Recycled cobalt that can be traced back to its source is gaining more and more popularity in the automotive and electronics industries.

- Black mass processing represents one of the upcoming growth areas for companies investing in capacity development and refinery technology in order to achieve maximum extraction of cobalt. Such investments are made out of the need to obtain maximum value from the lithium ion batteries.

- The rise of lithium iron phosphate (LFP) batteries is pushing recyclers to diversify beyond cobalt-focused streams and adapt to changing material mixes. Companies are reshaping their business models to process a broader range of battery chemistries while sustaining profitability amid shifting cobalt intensity.

- Recycling cobalt has become a strategy employed by governments and industry leaders as a means to diversify their sources and strengthen their domestic security of critical minerals through the establishment of recycling facilities that will form a crucial component of their battery materials procurement systems.

Cobalt Recycling Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 1,600 Million | |

| 2035 Projected Market Size | US$ 5,777.3 Million | |

| CAGR (2026-2035) | 13.7% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Europe | |

| By Source | End-of-Life Lithium-Ion Batteries, Battery Manufacturing Scrap, Industrial Catalysts, Superalloys & Metal Scrap, Electronic Waste (E-Waste), Others | |

| By Technology Type | Hydrometallurgical Recycling, Pyrometallurgical Recycling, Direct Recycling, Mechanical Recycling | |

| By Product Type | Cobalt Sulfate, Cobalt Oxide, Cobalt Metal, Mixed Cobalt Compounds, Others | |

| By Application | Lithium-Ion Battery Manufacturing, Superalloys, Catalysts, Magnetic Materials, Specialty Chemicals, Others | |

| By End-Use | Electric Vehicles (EVs), Energy Storage Systems (ESS), Consumer Electronics, Aerospace & Defense, Industrial Manufacturing, Chemical Industry, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Cobalt Recycling Market Disruption Analysis

Transition Toward Low-Cobalt Battery Chemistries Reshaping the Cobalt Recycling Market

The most significant disruption in the cobalt recycling market is the increasing move away from cobalt-rich battery chemistries such as NMC and NCA to LFP batteries that use minimal cobalt. The adoption of LFP battery technology is changing the economic dynamics of feedstock sourcing for the recyclers in the long run. The trend of using LFP batteries is gaining momentum due to the increasing focus of battery producers on reducing costs, ensuring resilience, and decreasing dependency on critical raw materials. However, the disruptions became worse in 2025, when LFP batteries edged out the nickel-based batteries and emerged as the largest type of EV batteries worldwide. As the EV Magazine reported in the industry, LFP battery installations for EVs in 2025 jumped by about 43%, making it larger in number than the nickel-based battery installations for the very first time. In China, which happens to be the largest market in the world for EVs and battery usage, over 80% of all the EVs sold in 2025 had LFP batteries installed in them.

As the world witnessed a total of 1.2 TWh worth of deployment for electric vehicle battery capacity in 2025, registering a 30% year-on-year growth rate, according to the International Energy Agency, the percentage of batteries having less cobalt content is becoming increasingly higher compared to their predecessors. In addition, industry predictions are suggesting that LFP's share of total electric vehicle batteries deployed globally may rise from around 48% during recent years to almost 65% by 2029, according to Reuters.

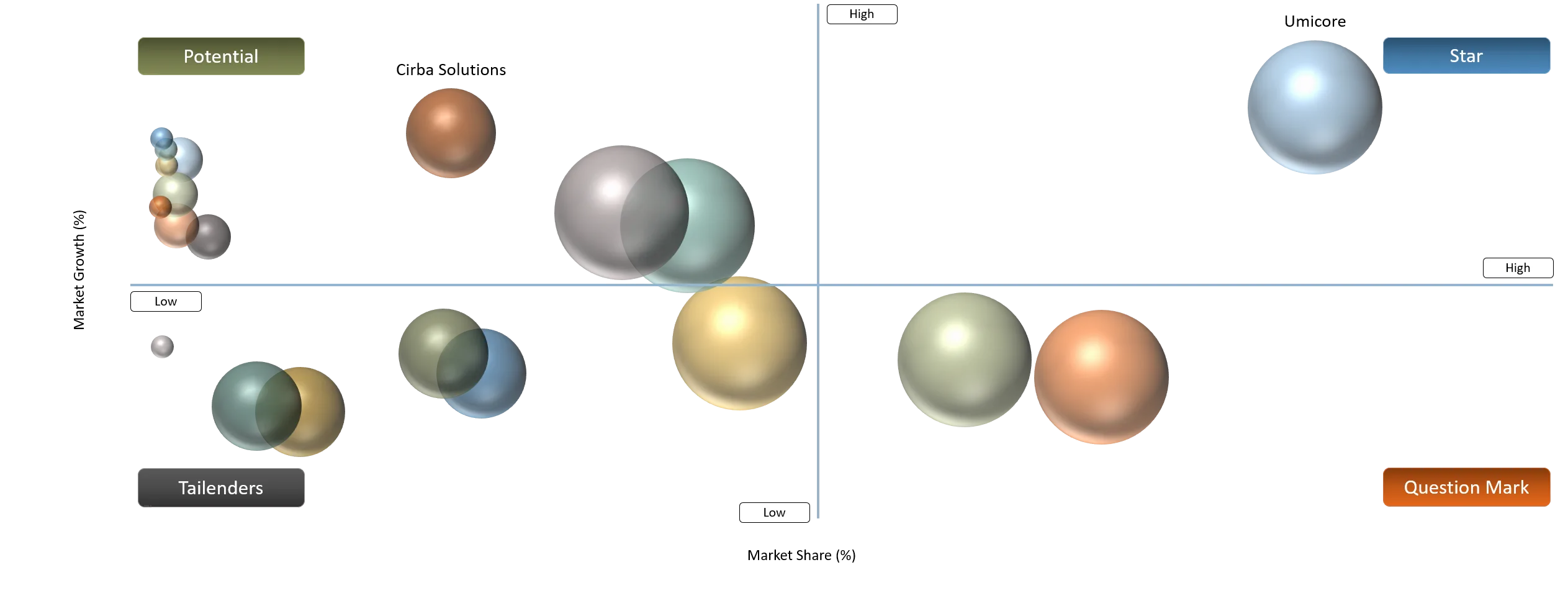

Cobalt Recycling Market BCG Matrix: Company Evaluation

Stars such as Umicore, Glencore, Redwood Materials, and GEM Co., Ltd., as these firms have the capabilities for extensive cobalt recycling, refinery capacity, and integration along the battery material supply chain. Such stars can take advantage of economies of scale, strategic collaborations with battery producers and automakers, and the production of battery-grade cobalt chemicals. Question Marks include Li-Cycle, Ascend Elements, Ecobat, Brunp Recycling, and Fortum because even though they have started to expand their capacity to recycle batteries and formed strategic alliances, they have not yet become profitable. They are aggressively developing battery recycling facilities and black mass processing plants to increase their market share.

Potential Players are Cirba Solutions, American Battery Technology Company, SungEel HiTech, SK Tes, and Lohum. The companies have been improving their standing through regional expansion, technological advancement, and greater involvement in the process of EV battery recycling. Tailenders include RecycLiCo Battery Materials due to the fact that their commercialization has not been very widespread in comparison to other global recyclers. Despite the fact that they have unique recycling processes and recover battery materials, their scale of operation is far behind that of the leading companies.

Cobalt Recycling Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Increasing the adoption of closed-loop battery supply chains by OEMs and manufacturers through recycling to obtain cobalt and ensure security of their material, and minimize purchasing risks. | 32% | Very High

| EV Batteries, Battery Manufacturing, Energy Storage Systems | Strengthens critical mineral security, reduces raw material procurement risk, and accelerates circular economy adoption |

Technology developments in direct recycling and hydrometallurgy have increased efficiency in recycling, which makes recycled cobalt equally competitive with mined cobalt. | 26% | High

| Battery-Grade Cobalt Sulfate Production, Black Mass Processing | Improves recovery yields, lowers processing costs, and enhances commercial viability of recycled materials |

Less energy needed and fewer emissions compared to the mining of cobalt from natural deposits have encouraged the recycling of cobalt for the achievement of business goals. | 19% | Medium-High | Sustainable Battery Manufacturing, ESG Compliance Programs | Supports decarbonization targets and reduces lifecycle carbon footprint of battery materials |

A rising number of gigafactories ensures that the availability of high-quality production scrap for recycling will remain consistent. | 18% | Medium-High | Battery Manufacturing Scrap Recycling, Cathode Material Recovery | Creates stable feedstock availability and improves recycler utilization rates |

The ESG standards, along with the requirements of responsible sourcing, are pressuring both automakers and electronics companies to use recycled cobalt as part of environmental support. | 14% | Medium | Automotive, Consumer Electronics, Energy Storage Supply Chains | Enhances supply-chain transparency, regulatory compliance, and sustainable procurement strategies |

Increasing the adoption of closed-loop battery supply chains by OEMs and manufacturers through recycling to obtain cobalt and ensure security of their material, and minimize purchasing risks.

The growing implementation of closed-loop cobalt supply chains is one of the main factors that contribute to boosting the development of the cobalt recycling market. The growing involvement of automobile original equipment manufacturers (OEMs), battery producers, and cathode producers in recycling as part of procurement is driven by the necessity to ensure sustainable access to minerals, decrease dependency on primary mining, and avoid raw materials price fluctuations. Thus, recycling helps create alternative supplies of cobalt. This movement received a major boost in 2025 and 2026 because battery producers increased their investment in recycling alliances and material recovery systems. The global electric vehicles sales recorded by the International Energy Agency (IEA) were over 17 million in 2025, which is a 25% growth compared to the previous year, thus making the need for sourcing cobalt more apparent. Additionally, according to the IEA, the global battery manufacturing capacity went beyond 3 TWh in 2025, thus producing large amounts of production scrap that can be used in a closed-loop system of recycling. The more batteries get produced, the more producers seek to recycle cobalt from the waste generated during the manufacturing process.

Furthermore, according to the International Energy Agency (IEA), battery recycling could supply up to 10% of global critical mineral demand for battery manufacturing by 2030, highlighting the growing strategic importance of recycled cobalt within future battery supply chains. As a result, closed-loop material recovery is evolving from a sustainability initiative into a core procurement and supply-chain strategy across the global battery industry. For instance, in 2025, the Government of India, via its Ministry of Mines, has launched an incentive scheme of ₹1,500 crores under the National Critical Minerals Mission to facilitate the recycling of critical minerals, including cobalt, lithium, nickel, rare earth metals, and platinum group metals from e-waste, spent lithium-ion batteries, catalytic converters, and alloy scrap.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

Volatility in cobalt prices can hinder recycling profitability, particularly at lower levels. | 8% | Recycling Economics & Profit Margins | Battery-Grade Cobalt Sulfate Production, Black Mass Processing

| Reduces investment attractiveness, delays capacity expansion, and weakens competitiveness of recycled cobalt against primary mined supply |

Increased adoption of LFP and cobalt-light batteries poses a risk to cobalt recovery volumes over time. | 12% | Long-Term Feedstock Value & Cobalt Recovery Potential | EV Battery Recycling, Cathode Material Recovery | Creates structural reduction in recoverable cobalt volumes, forcing recyclers to diversify into lithium, nickel, and graphite recovery streams |

Disparate collection systems increase logistical expenses and affect feedstock stability. | 9% | Feedstock Collection & Reverse Logistics | End-of-Life Battery Collection, Battery Waste Aggregation | Limits feedstock availability, increases operating costs, and reduces facility utilization rates across recycling networks |

Reliance on imported waste exposes recyclers to trade and geopolitical risks. | 7% | Supply Chain Security & Material Availability

| Black Mass Imports, Battery Scrap Processing | Increases exposure to export restrictions, trade barriers, and geopolitical disruptions, encouraging regional localization of recycling infrastructure |

Increased adoption of LFP and cobalt-light batteries poses a risk to cobalt recovery volumes over time

One of the most substantial limitations facing the cobalt recycling industry is the growing trend towards using lithium iron phosphate (LFP) and other lower cobalt batteries. Although there is still a continued expansion of global battery production, the amount of cobalt per battery is shrinking as producers focus on cost-effective and sustainable cathode materials. The challenge here for cobalt recyclers is that the future flows of used batteries will contain less cobalt, posing a threat to recycling profitability. Reinforced by the increased role of LFP batteries in the global market for electric vehicles in 2025, the restriction was even more obvious. According to the International Energy Agency (IEA), LFP batteries made up around 50% of all global EV batteries' needs in 2025, whereas only about 30% before a few years ago. Moreover, in China, the largest market for electric cars, LFP batteries comprised over 70% of electric vehicle battery installation in 2025 because of decreased cobalt intensity in new battery production. Thus, the following waste streams would include less cobalt-containing material for recycling.

Furthermore, industry predictions suggest that there will be further growth in the use of LFP batteries in cars, energy storage units, and commercial transport through 2026 and beyond. For instance, in 2025, Springer Nature, a UK-based private commercial company, released a study conducted by Tsinghua University researchers that showed that the shift from NCM batteries to LFP batteries, in addition to increased battery recycling, would lead to a decline in cumulative cobalt requirements in China by 96% by 2060.

Cobalt Recycling Market Segment Analysis

The global cobalt recycling market is segmented based on source, technology type, product type, application, end-use, and region.

Hydrometallurgical Recycling Dominating the Cobalt Recycling Market Through High Recovery Efficiency and Battery-Grade Material Production

Recycling of cobalt via hydrometallurgical processes is still considered dominant in the technology segment, with the market share of 58% in 2025, and the cobalt recycling market owing to its higher metal recovery efficiencies, higher purity levels achieved by producing battery-grade material, and lesser environmental impact than the traditional pyrometallurgical processes. The process involves the use of chemical and solvent extraction processes to recover cobalt from used lithium-ion batteries, battery production waste, and black mass. Its capacity to recover cobalt, nickel, and lithium efficiently has made it a choice of many companies, including Umicore, Fortum, Ascend Elements, GEM Co., Ltd., and SungEel HiTech.

Hydrometallurgical extraction has become the technology of choice due to its ability to recycle essential battery components at a recycling rate of often more than 95%. It also derives its strong leadership from stringent regulations on sustainability in Europe, North America, and the Asia-Pacific, which lean towards recyclable technologies that focus on recovering critical minerals while reducing greenhouse gas emissions and waste production. This makes hydrometallurgical recycling the most profitable technology segment within the cobalt recycling industry and one that is set to remain dominant through the forecast period.

Cobalt Recycling Market Geographical Penetration

Extensive Battery Manufacturing Ecosystem and Recycling Infrastructure Leadership Driving Asia-Pacific Dominance

Asia Pacific is the dominant region in cobalt recycling with a market share of 56.1% in 2025, due to the battery manufacturing capabilities, electric vehicle manufacturing, battery recycling capabilities, and the critical mineral refining ecosystem that it possesses. China, Japan, and South Korea together have a sizable portion of the world's lithium-ion battery production and processing activities, thus producing considerable amounts of battery manufacturing scraps and used batteries, which can be recycled for cobalt. The presence of major battery recyclers like GEM Co., Ltd., Brunp Recycling, and SungEel HiTech, along with government efforts towards battery circularity, has helped the region to dominate the cobalt recycling market. The major players in the industry, such as GEM Co., Ltd., Brunp Recycling (CATL), and SungEel HiTech, increased their recycling capacities and production of the precursors to meet the increasing demand for recycled cobalt sulfate and other components of batteries.

The region is also characterized by good integration of battery production, cathode manufacturing, refining, and recycling, which allows for an effective recirculation of cobalt back to the process of battery production. For example, in June 2026, N.A.N. GreenMet, a battery recycling and critical minerals recovery firm based in India, along with Silox India, another firm dealing in clean technology and recycling solutions located in India, created a joint venture that would establish India's largest critical minerals recycling. This collaboration would help in collecting strategic metals like cobalt, lithium, nickel, and manganese from discarded lithium-ion batteries.

China Cobalt Recycling Market Trends

China holds a strong dominance in the Asia-Pacific region when it comes to the cobalt recycling industry because of its highly integrated battery production chain, strong refining capacity, and robust infrastructure in terms of battery recycling. One of the advantages that China enjoys is the existence of leading cobalt recyclers and battery material producers like GEM Co., Ltd., BRUNP Recycling (CATL), and Huayou Cobalt. The integration of the battery production chain and cathode production, refining, and recycling helps to recover and integrate cobalt back into battery supply chains. China was said to account for about 70% of the global total capacity for battery production as per the International Energy Agency (IEA), while in addition having over 11 million sales of electric vehicles in 2025. This has allowed it to sustain its position of accounting for 65.9% of the Asia Pacific cobalt recycling market.

For example, in December 2025, Zhejiang Huayou Cobalt Co., Ltd., a Chinese-based company specializing in the manufacturing of battery raw materials and cobalt-based products, and Encory GmbH, a German-based company operating within the circular economy sector, formed a joint venture to create a circular battery recycling system in China. This partnership entails the creation of facilities for recycling and regenerating batteries that will allow the extraction of important raw materials from the used lithium-ion batteries, such as cobalt, nickel, and lithium.

India Cobalt Recycling Market Outlook

India is emerging as one of the fastest-growing countries in the Asia-Pacific region in terms of the cobalt recycling market because of the fast adoption of electric vehicles, increasing capacity for the manufacture of lithium-ion batteries, favorable battery waste management policies, and investment in critical mineral extraction facilities. India is currently working on building its own battery recycling infrastructure that would help in reducing reliance on battery components from abroad and increase supply chain security. Lohum, Attero, and many other recycling companies have been increasing their capacity for battery collection, black mass processing, and extraction of battery-grade materials. As per the International Energy Agency (IEA), India has been witnessing one of the most rapid rates of growth in the electric vehicle market segment, with 75% increase year on year to a total of 165,000, accounting for almost 4% of total car sales in 2025. About 60% of sales of electric cars were manufactured within the country by local car manufacturers, including Tata and Mahindra.

Thus, India is expected to show the highest growth rate in the Asia-Pacific cobalt recycling market at 17–19% CAGR from 2026 to 2035. For instance, in July 2025, VinFast Auto India, which is a subsidiary company of the Vietnam-based electric vehicle manufacturing company, formed a strategic alliance with BatX Energies, which is an India-based battery recycling and recovery of critical minerals company, to provide high-voltage battery recycling, material recovery, and repurposing services.

Cobalt Recycling Market Competitive Landscape

- The market is comprised of three major categories of participants: integrated battery materials recyclers and refiners, battery recycling technology providers, and circular economy-focused battery supply chain players. Market leaders include Umicore, GEM Co., Ltd., BRUNP Recycling, Glencore, and SungEel HiTech, which dominate the market due to their high capacity of cobalt recovery, refining capacities, and tight integration into the supply chains of battery and cathode producers. Companies such as Redwood Materials, Li-Cycle, Ascend Elements, Fortum, and Cirba Solutions specialize in hydrometallurgy processes, black mass recovery, and closed-loop battery recycling systems. At the same time, Ecobat, American Battery Technology Company, SK Tes, RecycLiCo Battery Materials, and Lohum are developing regional recycling networks and advanced materials recovery technologies in response to increasing demand for sustainable critical minerals.

- Key players in the industry are Umicore, Glencore, Redwood Materials, Li-Cycle, Ecobat, GEM Co., Ltd., BRUNP Recycling, Fortum, Cirba Solutions, Ascend Elements, American Battery Technology Company, SungEel HiTech, SK Tes, RecycLiCo Battery Materials, and Lohum.

Key Developments

- September 2025: Zhejiang Huayou Cobalt Co., Ltd., a China-based battery materials and cobalt producer, and LG Energy Solution, a South Korea-based battery manufacturer, have reinforced their strategic alliance in order to facilitate a closed-loop EV battery ecosystem by means of battery recycling, cathode material production, and minerals recovery.

- January 2025: Samsung Electronics, a South Korea-based manufacturer of consumer electronic devices, introduced a new method of recycling cobalt, which helps recycle cobalt from old Galaxy device batteries and factory waste.

- April 2026: NavPrakriti International Pvt. Ltd., an India-based battery recycling and critical minerals recovery company, announced an investment of more than ₹100 crore in setting up a critical minerals refining plant in Odisha.

- May 2026: The Government of India and the European Union introduced a collaborative project worth approximately US$17.3 million (₹169 crores/€15.2 million) to develop cutting-edge technologies for EV battery recycling and critical raw material recovery.

- August 2025: Glencore completed the acquisition of the assets of Li-Cycle Holdings Corp., which includes battery recycling operations and intellectual property. This acquisition allows Glencore to enhance its position within the value chain of battery recycling through increased recovery capabilities of critical battery materials such as cobalt, lithium, and nickel.

- June 2025: LG Energy Solution and Toyota Tsusho Corporation established a joint venture for battery recycling called Green Metals Battery Innovations in North Carolina, United States.

- June 2026: Litus and UWin Nanotech, both companies, entered into a strategic partnership for battery metal recovery and critical minerals processing. The company's partnership will be geared towards developing processes that involve the selective recovery and refining of valuable battery materials such as cobalt, lithium, nickel, and rare earth metals.

Key Procurement Priorities and Buyer Evaluation Criteria

- The organizations making investments in the cobalt recycling industry have started emphasizing on those suppliers who can provide battery-grade cobalt products with high purity, guarantee feed stock availability in the long run, and ensure recovery rates of a consistent nature from end-of-life batteries and manufacturing scrap batteries. The recycling partner should be able to support circular supply chain goals and material quality.

- The decision-making for procurement is being affected by increasing concerns related to mineral security, battery circulatory rules, ESG criteria, and the local battery supply chain. OEMs, battery makers, and cathode companies are more inclined towards recyclers, which can offer them traceable and sustainable sources of cobalt and also reduce reliance on mining activities and geopolitical risks.

- Evaluation criteria of suppliers by buyers include factors such as effectiveness of cobalt extraction, purity of battery-grade cobalt materials, hydrometallurgical processing abilities, supply chain for the feedstock, and environmental regulations, among others. The ability to provide consistently high-purity cobalt sulfate is an important criterion for purchase.

- Recycling companies are increasingly evaluated by procurement departments for their closed-loop recycling facilities, black mass expertise, material tracking methods, carbon footprint reductions, and flexibility of long-term contracts. Collaboration with battery companies, EV makers, and energy storage businesses is seen as an indication of reliable logistics and the commercialization process.

- Buyers also factor into account a supplier’s ability to extract various important materials such as cobalt, lithium, nickel, manganese, and graphite. This helps in extracting materials from batteries. Buyers have started preferring companies that have developed recycling capabilities and process-based platforms that are chemistry-agnostic.

Why Choose DataM?

- Technological Innovations: Explores advancements in Fan-Out Wafer-Level Packaging including high-density RDL, panel-level packaging, and heterogeneous integration, enabling improved performance, reduced power consumption, and smaller form factors for AI, 5G, and high-performance computing applications.

- Product Performance & Market Positioning: Evaluates how different players deliver packaging solutions based on I/O density, thermal performance, miniaturization, and cost efficiency, highlighting how leading companies differentiate through advanced integration and scalability across consumer electronics and automotive applications.

- Real-World Evidence: Highlights adoption of FOWLP in smartphones, wearables, automotive electronics, and AI chips, demonstrating benefits such as enhanced processing speed, reduced footprint, improved energy efficiency, and optimized system-level performance.

- Market Updates & Industry Changes: Tracks key developments such as capacity expansions, new packaging platforms, panel-level innovations, and regional semiconductor investments across Asia-Pacific, North America, and Europe, supporting the shift toward advanced packaging ecosystems.

- Competitive Strategies: Analyzes how leading companies expand through capacity scaling, technology innovation, strategic partnerships, and integration of advanced packaging with chip design to address rising demand from AI and high-performance computing markets.

- Pricing & Market Access: Explains pricing variations based on complexity, wafer size, and integration level, along with access through OSAT providers, foundries, and integrated device manufacturers supporting global supply chains.

- Market Entry & Expansion: Identifies growth opportunities driven by AI, 5G, automotive electronics, and data centers, while outlining strategies such as regional capacity expansion, technology differentiation, and ecosystem partnerships to scale globally.

Target Audience

- Battery Manufacturers & Cell Producers

- Electric Vehicle (EV) Industry

- Battery Recycling & Resource Recovery Companies

- Critical Mineral & Materials Companies

- Energy Storage Industry

- Aerospace & Defense Organizations

- Investors & Financial Institutions