Digital Wound Care Management Market Size & Industry Outlook

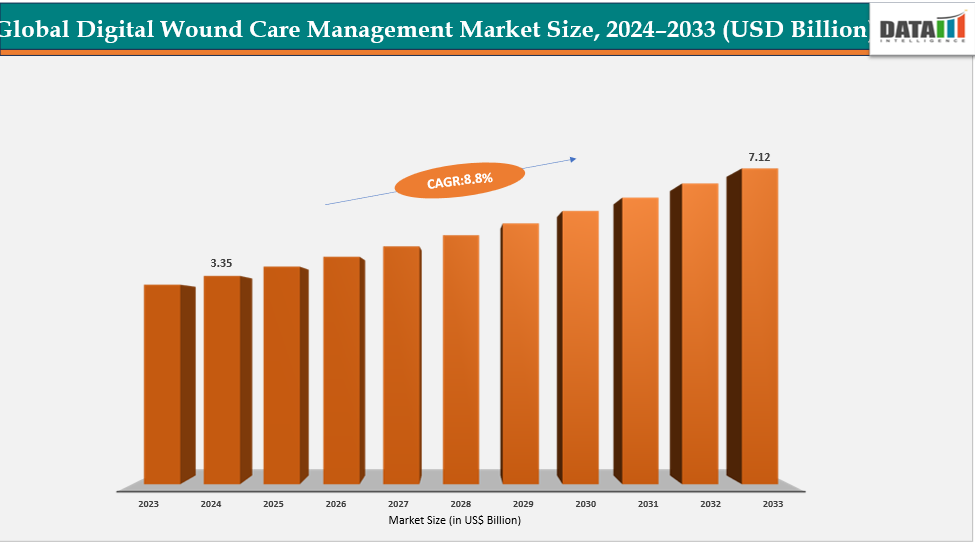

The global digital wound care management market size reached US$ 3.64 Billion in 2025 is expected to reach US$ 7.12 Billion by 2033, growing at a CAGR of 8.8% during the forecast period 2026-2033.

The global digital wound care management market is witnessing strong growth, primarily driven by the rising burden of chronic wounds such as diabetic foot ulcers, venous leg ulcers, and pressure injuries, fueled by an aging population and increasing diabetes prevalence. At the same time, the adoption of AI-powered wound imaging, digital platforms, and telehealth solutions is transforming traditional wound care by enabling accurate measurement, standardized assessment, and remote monitoring.

For instance, in 2025, Swift Medical’s Swift Skin and Wound platform and MolecuLight’s i:X fluorescence imaging device are increasingly being deployed across hospitals and wound care clinics to improve diagnostic precision and enhance patient outcomes.

However, barriers such as high device costs, inconsistent reimbursement, and integration challenges with hospital EHR systems remain key restraints. Despite this, opportunities lie in the integration of predictive analytics, machine learning, and the expanding role of home healthcare and remote patient monitoring, positioning the market for robust long-term growth.

Key Market Trends & Insights

The global digital wound care management market is transforming with the integration of artificial intelligence, machine learning, and mobile health apps. Telehealth and remote patient monitoring are gaining popularity, reducing healthcare costs and enabling care delivery beyond traditional hospitals. Vendors are focusing on EHR interoperability and cloud-based platforms for seamless data sharing. Advanced imaging devices like fluorescence-based diagnostics are also being adopted, providing real-time insights into bacterial burden and wound healing progress. These trends align with the growth of digital health ecosystems.

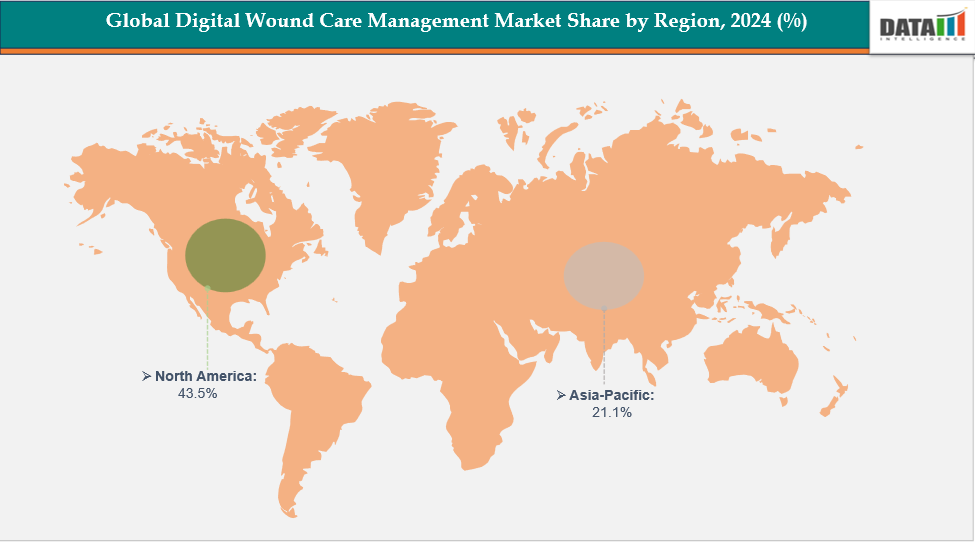

North America is expected to dominate the digital wound care management market with the largest revenue share of 43.5% .

The Asia Pacific is the fastest-growing region and is expected to grow at the fastest with revenue share of 21.1% over the forecast period.

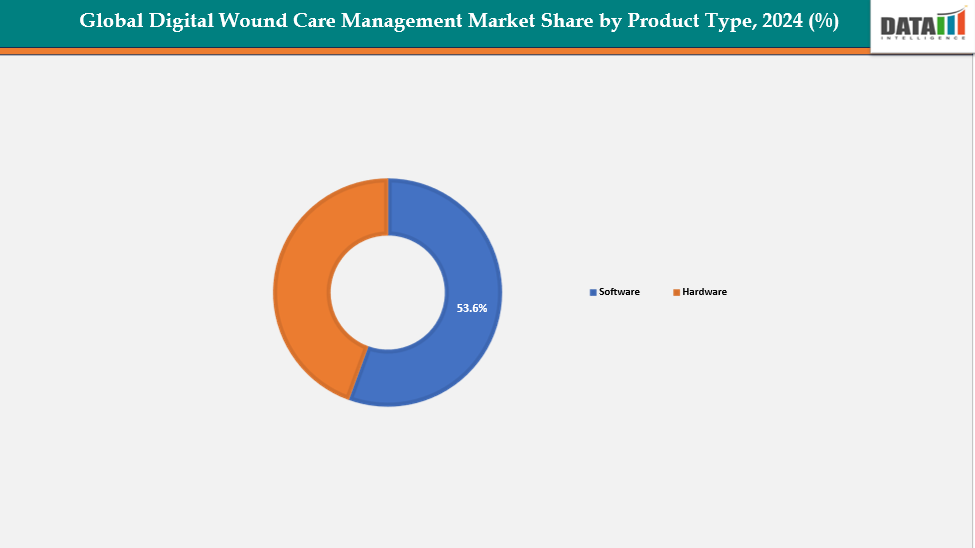

Based on product type, the herbal extracts segments led the market with the largest revenue share of 53.6%.

The major market players in the digital wound care management market are Smith+ Nephew, Swift Medical Inc, Healogics, LLC., 3M, Essity Aktiebolag (publ)., MolecuLight Inc., Net Health Systems, Inc., WoundZoom, Ekare Inc, Joerns Healthcare and among others.

Market Size & Forecast

2025 Market Size: US$ 3.64 Billion

2033 Projected Market Size: US$ 7.12 Billion

CAGR (2025–2033): 8.8%

North America: Largest market

Asia Pacific: Fastest-growing market

For more details on this report – Request for Sample

Market Dynamics

Drivers:

The rising prevalence of chronic wounds is significantly driving the digital wound care management market growth

The rising prevalence of chronic wounds such as diabetic foot ulcers, venous leg ulcers, and pressure ulcers is a major driver of the Global Digital Wound Care Management Market. With the growing aging population and increasing cases of diabetes and obesity, the burden of long-healing wounds has surged, creating a strong demand for advanced wound monitoring and management solutions. Chronic wounds often require continuous assessment and frequent follow-up, which traditional care methods struggle to deliver efficiently.

For instance, in 2024, the overall prevalence of chronic wounds was 1.89 per 1000 (19/10003) population. The prevalence of wounds in urban areas was 1.57 per 1000 (11/6984) population, while that in rural communities was 2.64 per 1000 (8/3019) population.

Restraints:

Interoperability issues with existing hospital EHR systems are hampering the growth of the digital wound care management market

Interoperability issues with existing hospital EHR systems present a significant challenge in the Global Digital Wound Care Management Market. Many digital wound imaging platforms and AI-based assessment tools generate valuable data, but integration with hospital IT infrastructure often requires custom interfaces or additional middleware, leading to workflow disruptions and added costs. This lack of seamless data exchange hampers clinicians’ ability to access a unified patient record, delaying decision-making and reducing the efficiency of care delivery. For instance, several healthcare providers using Net Health’s Tissue Analytics platform have highlighted the need for smoother EHR integration to fully leverage wound data across multidisciplinary teams.

Digital Wound Care Management Market, Segment Analysis

The global digital wound care management market is segmented based on product type, wound type, end user, and region.

Product Type:

The software segment is dominating the digital wound care management market with a 53.6% share

The software segment is witnessing strong growth, driven by the rising adoption of AI-powered wound assessment platforms, telehealth solutions, and cloud-based documentation tools that streamline clinical workflows and enhance accuracy. Hospitals and wound care clinics increasingly prefer digital software solutions as they enable real-time wound measurement, predictive analytics, and remote patient monitoring, reducing the need for frequent in-person visits. Integration with EHR systems further boosts efficiency by providing clinicians with comprehensive patient data in one platform.

For instance, in June 2025, Vital Wound Care has launched a free web-based Wound Assessment App as part of its expansion of mobile wound care services, aiming to improve access to treatment by delivering care directly to patients' homes, especially those with mobility or transportation limitations.

The chronic wounds from the wound type is expected to grow in the digital wound care management market with a 54.2% share

The chronic wounds segment is a key growth driver in the digital wound care management market, fueled by the rising incidence of diabetic foot ulcers, pressure ulcers, and venous leg ulcers linked to an aging population, diabetes, and obesity. These wounds require long-term monitoring, frequent assessments, and standardized documentation, which traditional care methods struggle to provide efficiently. Digital platforms enable clinicians to capture accurate wound measurements, track healing progress, and use AI-driven analytics to predict complications, thereby improving patient outcomes.

For instance, in June 2024, Chronic wounds, including diabetic ulcers and pressure injuries, have a poorer five-year survival rate than other serious diseases and cost an estimated $28 billion annually in the U.S. Treating wounds is expensive, with researchers from the Keck School of Medicine of USC and the California Institute of Technology developed advanced technologies to revolutionize wound care. These technologies include smart bandages that automatically respond to changing wound conditions, providing continuous data on healing and potential complications, and enabling real-time delivery of medications or treatments.

Geographical Analysis

North America is expected to dominate the global digital wound care management market with a 43.5%

The North American market for digital wound care management is growing due to the high prevalence of chronic wounds, aging population, and lifestyle diseases. Advanced digital health technologies, such as AI-powered wound imaging and cloud-based platforms, are being adopted to standardize wound assessment and provide remote care. Government initiatives and favorable reimbursement policies are also driving the adoption of these solutions. Hospitals and clinics in North America are utilizing these technologies to improve patient outcomes, reduce readmissions, and optimize workflow efficiency.

For instance, in October 2024, Swift Medical, a pioneer in digital wound care, has introduced its new Skin & Wound 2 platform, which has been used for over 50 million patient assessments in various settings. The award-winning platform has been clinically validated with over 22 peer-reviewed publications, demonstrating improved accuracy, equitable AI, and healing rates, making it the gold standard in the digital wound care segment.

US:

The United States is a strong market share of 85.1% in North America due to its mature healthcare IT infrastructure, extensive EHR systems, and large diabetic and elderly population. Digital wound care platforms like Swift Medical's Swift Skin and Wound and Net Health's Tissue Analytics are widely used in hospitals and clinics. The USA's robust regulatory frameworks, healthcare investments, and private-sector innovation facilitate the faster adoption of AI-enabled solutions and integrated care models.

The Asia Pacific region is the fastest-growing region in the global digital wound care management market, with revenue share of 21.1%

The Asia-Pacific region is experiencing rapid growth in digital wound care management due to rising diabetes and chronic wounds, healthcare digitalization, and government initiatives. Rapid urbanization, increased healthcare awareness, and improved hospital infrastructure are driving the adoption of advanced wound care solutions. Countries like China, Japan, and South Korea are investing in AI-powered imaging platforms and telehealth-based wound monitoring programs to improve patient outcomes and reduce hospital resource burden.

For instance, in November 2024, The University of Nottingham Ningbo China (UNNC) has made a groundbreaking advancement in wound care with the development of a battery-free, multifunctional microfluidic Janus wound dressing (MM-JWD).

India:

India is a significant market for wound care solutions is expected to grow with 35.2% due to its high incidence of diabetic foot ulcers and large population. The rapid adoption of telehealth and mobile health platforms is supporting this growth. Digital health startups and technology partnerships are introducing AI-enabled imaging, predictive analytics, and remote patient monitoring to bridge the gap between specialized care and underserved regions. This, combined with government programs promoting digital health, is expanding access to quality wound care and creating significant growth potential for software and hardware solutions in India.

Digital Wound Care Management Market Top Companies

Top companies in the digital wound care management market include Smith+ Nephew, Swift Medical Inc., Healogics, LLC., 3M, Essity Aktiebolag (publ)., MolecuLight Inc.,Net Health Systems, Inc., WoundZoom, Ekare Inc, Joerns Healthcare.

Swift Medical Inc:

Swift Medical is a leading provider of an AI-powered platform for digital wound care management. Its flagship product, Swift Skin and Wound, uses high-resolution imaging and machine learning algorithms to measure wound dimensions, assess tissue type, and predict healing trajectories. This platform supports remote patient monitoring, reducing the need for in-person visits. Swift Medical's solutions are widely used in hospitals, clinics, and home healthcare settings, promoting standardization of wound assessment, improved patient outcomes, and accelerating the shift towards digital wound management.

Key Developments:

In May 2025, Vital Wound Care launched a free, AI-driven, web-based Wound Assessment App as part of its broader expansion of mobile wound care services, further bringing hospital-grade care to homes across Greater Houston.

In September 2024, ChartPath, a leading EHR provider for long-term and post-acute care, has partnered with WoundZoom, an innovator in digital wound management solutions, to enhance wound care management in LTPAC by combining ChartPath's user-friendly platform with WoundZoom's advanced technology.

Digital Wound Care Management Market Scope

Metrics | Details | |

CAGR | 8.8% | |

Market Size Available for Years | 2023-2033 | |

Estimation Forecast Period | 2026-2033 | |

Revenue Units | Value (US$ Bn) | |

Segments Covered | Product Type | Software, Hardware |

Wound Type | Chronic Wounds, Acute Wounds | |

End User | Hospitals, Wound Care Clinics, Others | |

Regions Covered | North America, Europe, Asia-Pacific, South America and the Middle East & Africa | |

The global digital wound care management market report delivers a detailed analysis with 62 key tables, more than 57 visually impactful figures, and 159 pages of expert insights, providing a complete view of the market landscape.