Blood Based Biomarkers Market Overview

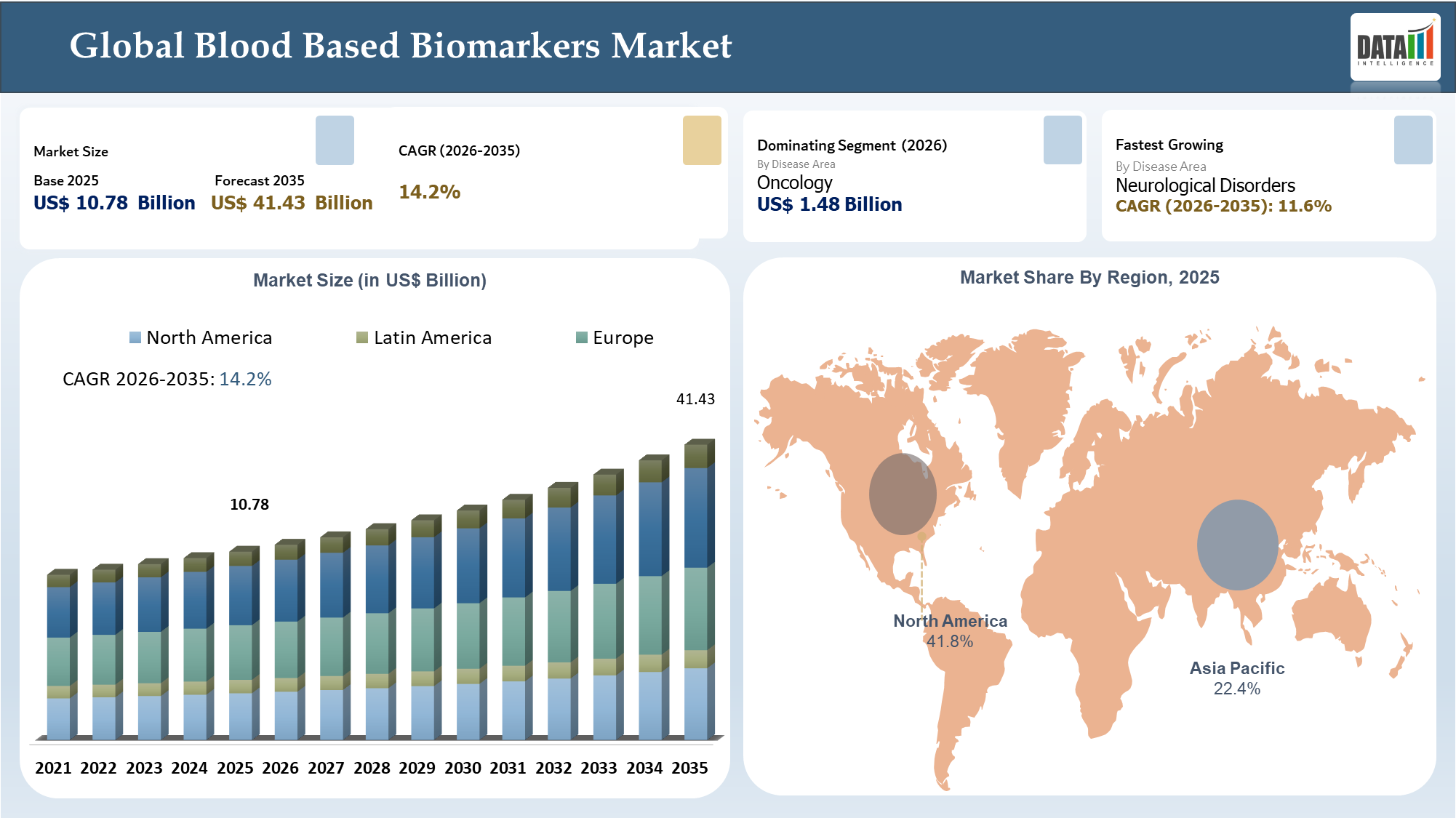

The Global Blood Based Biomarkers Market reached US$ 10.78 billion in 2025 and is expected to reach US$ 41.43 billion by 2035, growing with a CAGR 14.2% during the forecast period 2026-2035. The Blood Based Biomarkers Market is expected to become an important element of precision diagnostics as the trend shifts away from invasive symptoms-based testing towards minimally invasive predictive and longitudinal monitoring.

This is made possible due to the capability of detecting molecular, protein and metabolic biomarkers from plasma, serum and whole blood samples, which aids in early diagnosis, selection of optimal therapy, risk stratification and evaluation of the efficacy of the treatment received. The development of the sector is being heavily impacted by the field of oncology, in particular due to advancements in the areas of liquid biopsy, circulating tumor DNA and minimal residual disease monitoring. The market growth is further encouraged by the growing number of people with chronic illnesses, increased interest in prevention and need for repeated diagnostic tests. New technologies such as PCR, NGS, proteomics and multi-omics significantly contribute to improving the accuracy and efficiency of the process. In addition, other indications, including cardiovascular diseases, neurology and autoimmune conditions, are expected to be considered in the future.

AI Impact Analysis

AI is gaining traction as a value accelerator within the Blood Based Biomarkers Market through its contribution to enhancing the efficiency and effectiveness of interpreting biomarker data. Blood-based biomarker tests can produce extensive amounts of genomic, proteomic, metabolomics and clinical data that require careful interpretation. The application of AI allows for the discovery of subtle biomarker correlations, risk prediction of diseases and improvements in sensitivity and specificity for early detection.

Within the field of oncology, AI is utilized in ctDNA sequencing, tumor profiling, risk of recurrence, and response to treatment prediction. Within neurology, the use of AI allows for the integration of multiple blood-based biomarkers, such as pTau, amyloid and neurofilaments, alongside other patient information, to provide an improved early-stage disease assessment. AI can assist pharmaceutical companies through better patient stratification, more efficient clinical trials, and companion diagnostics creation.

Overall, AI is transforming the role of blood-based biomarkers from singular test results to more advanced and intelligent multi-biomarker predictions.

Blood Based Biomarkers Market Industry Trends and Strategic Insights

- Blood Based Biomarkers Market trends have been growing due to the trend in healthcare towards non-invasive diagnosis based on early and precision medicine.

- The oncology segment continues to be the largest one owing to liquid biopsy, ctDNA, companion diagnostics, MRD analysis and recurrence detection.

- Neurological disorders have emerged as an important new market for blood-based biomarkers because of increasing need for Alzheimer’s and neurodegenerative diseases.

- North America is currently dominating this market owing to high diagnostics infrastructure, adoption of cancer diagnostics technology and large number of biomarker firms in the region.

- Technologies such as NGS, PCR, immunoassays and proteomics are increasingly offering better sensitivity and scalability.

- High platform costs, lack of reimbursement coverage and clinical validation continue to pose significant barriers.

- Future growth will be determined by use of multiple biomarkers, AI support, preventive tests and precision medicine..

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 10.78 Billion | |

| 2035 Projected Market Size | US$ 41.43 Billion | |

| CAGR (2026-2035) | 14.2% | |

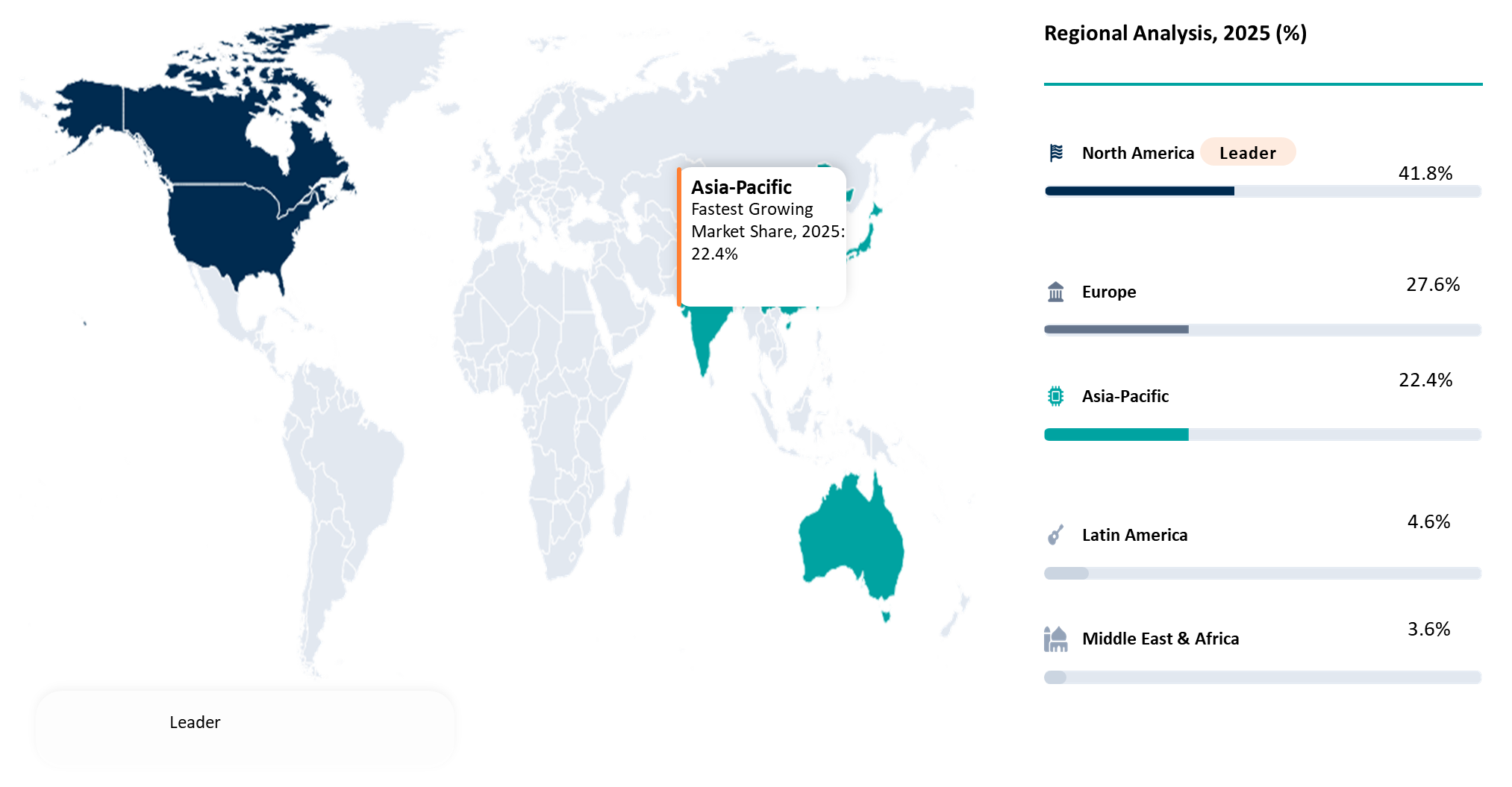

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Biomarker Type | Genomic Biomarkers, Proteomic Biomarkers, Metabolomic Biomarkers, Epigenetic Biomarkers, Cell Free DNA, Circulating Tumor DNA, Circulating Tumor Cells, Multi Biomarker Panels, Others | |

| By Disease Area | Oncology, Cardiovascular Diseases, Neurological Disorders, Infectious Diseases, Autoimmune Diseases, Metabolic Disorders, Prenatal Health, Others | |

| By Application | Screening, Diagnosis, Risk Stratification, Prognosis, Therapy Selection, Companion Diagnostics, Treatment Monitoring, Recurrence Monitoring, Others | |

| By Technology | PCR, NGS, ELISA, Immunoassays, Mass Spectrometry, Proteomics Platforms, Others | |

| By Sample Type | Plasma, Serum, Whole Blood | |

| By End User | Hospitals, Diagnostic Laboratories, Cancer Centers, Pharma and Biotechnology Companies, CROs, Research Institutes | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

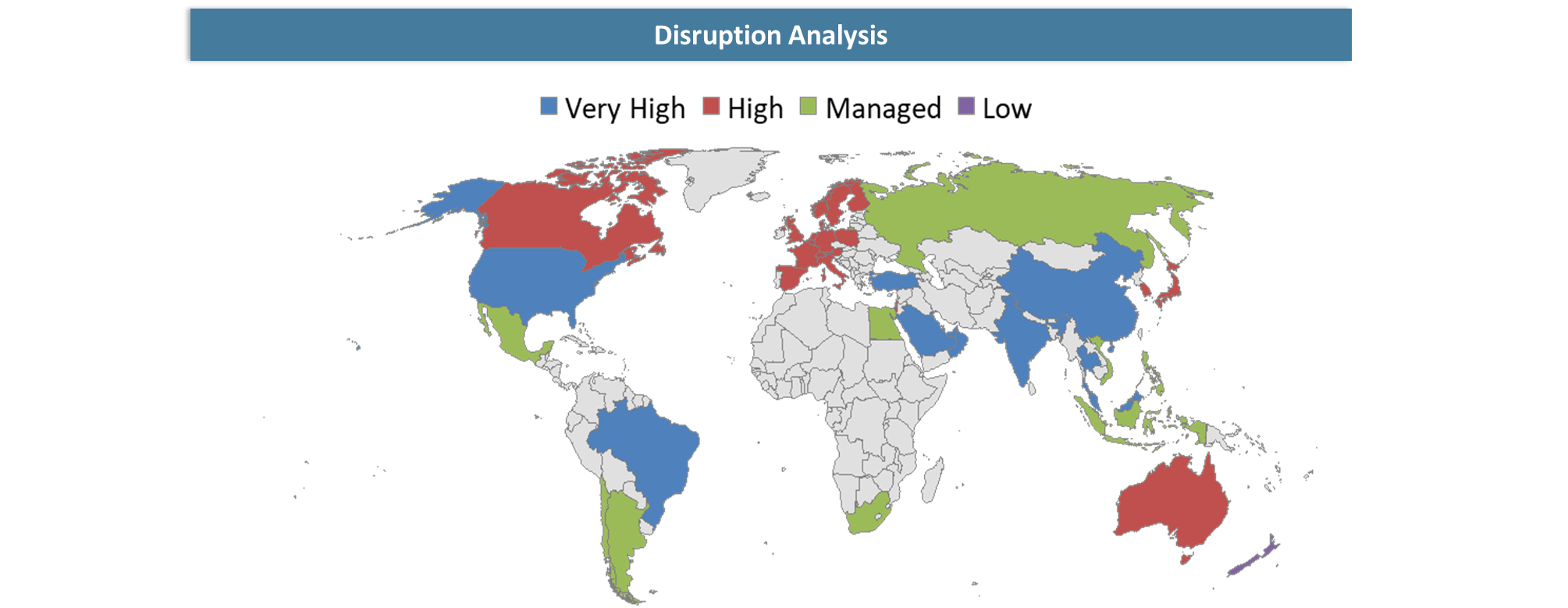

Disruption Analysis

Shift from Invasive Diagnostics to Continuous Precision Monitoring

Blood based biomarkers are revolutionizing the diagnostics sector in terms of transforming the approach of clinicians towards the diagnosis from being invasive and sporadic to a minimally-invasive, repetitive and evidence-based practice. The major disruption that has occurred in diagnostics through the use of blood based biomarkers is happening in the field of oncology where, for instance, liquid biopsy is competing with traditional tissue biopsy using ctDNA for tumor profiling, selection of treatment modalities, identification of resistance to therapy, early detection of cancer recurrence, and monitoring of minimum residual diseases. There is also significant disruption in the field of neurology with the introduction of blood based biomarkers to reduce the dependence of diagnosing diseases such as Alzheimer’s among others on costly procedures such as imaging and CSF testing. The use of multi-biomarker panels, proteomics, and artificial intelligence in diagnostics is shifting the paradigm from one-biomarker diagnostics to predictive, risk-based, and precision medicine diagnostics.

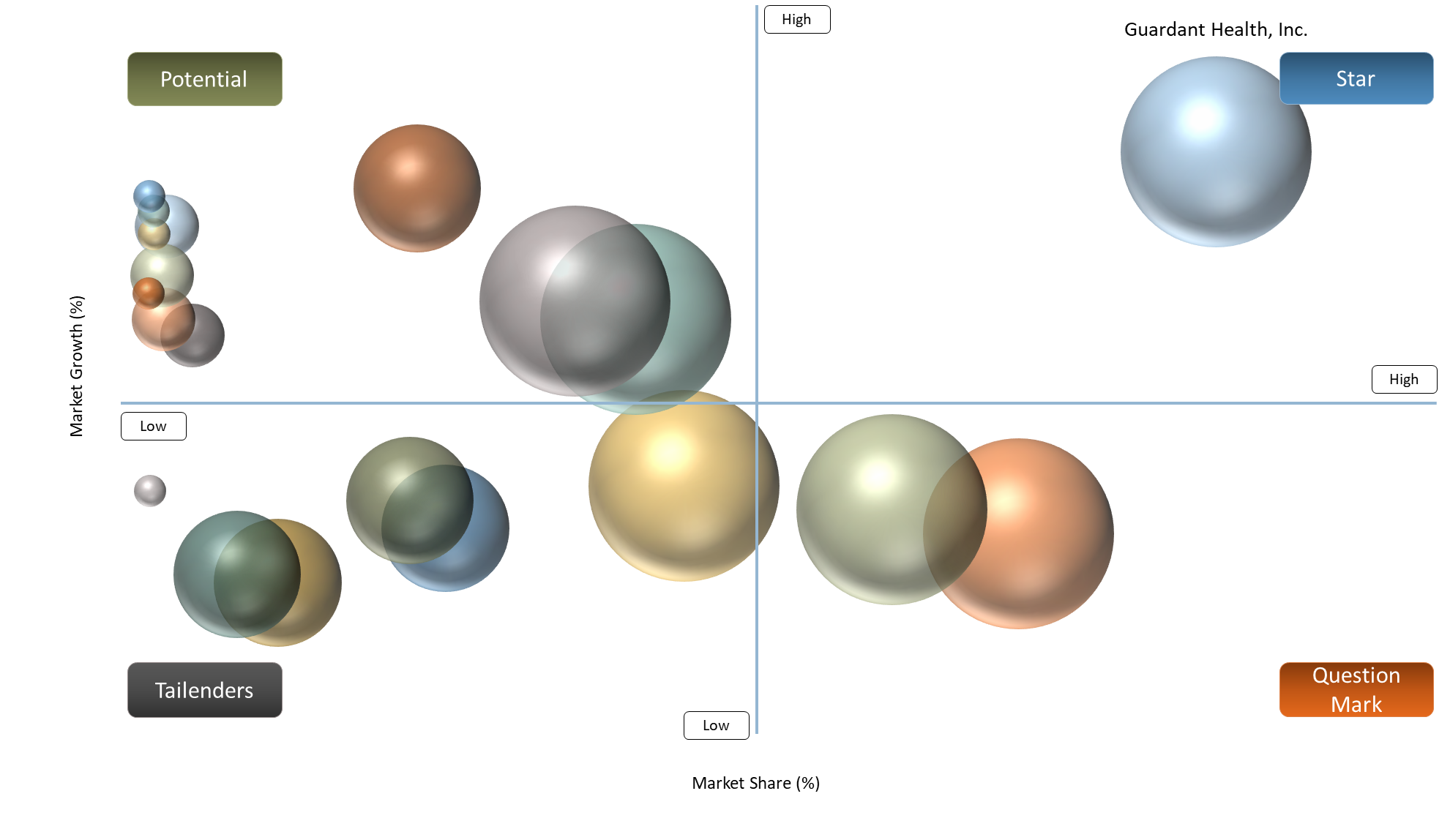

BCG Matrix: Company Evaluation

The analysis in the company evaluation for the Blood Based Biomarkers Market provides a distinct separation amongst leaders, established diagnostics players, innovators and platform enablers within the industry. Guardant Health, GRAIL, Natera, Foundation Medicine and Tempus are classified as growth leaders because of their significant emphasis on liquid biopsy, ctDNA, MRD, multi-cancer early detection and artificial intelligence in precision oncology. Roche, Abbott, Siemens Healthineers, Thermo Fisher Scientific, QIAGEN, bioMérieux and Beckman Coulter remain strategically positioned owing to comprehensive product portfolios in diagnostics, international lab network reach, existing technology platforms and regular revenue streams from reagents. Freenome, Personalis, Exact Sciences, Sysmex, Labcorp and Quest Diagnostics are expanding players that have considerable growth potential, especially with the increasing use of blood-based screening tests, neurological markers and advanced cancer surveillance applications. Bio-Rad Laboratories and Illumina provide vital support to innovating firms as part of their platforms and services that facilitate biomarker discovery, sequencing and assay processes.

Market Dynamics

Growing Demand for Early Disease Detection

Growing demand for the early diagnosis of disease will become one of the key drivers in the Blood Based Biomarkers Market due to the changing healthcare model from the traditional reactive approach to prevention and personalized medicine. The use of blood based biomarkers enables early diagnosis of various diseases even at the stage when any symptoms have not appeared yet, thereby contributing to a quicker response to a possible threat. This is especially true for such areas as oncology, cardiovascular diseases and neurological disorders, where the late diagnosis leads to increased costs and mortality rates.

The application of blood based tests represents a minimally invasive method allowing its integration into routine medical procedures as screening, monitoring and even population-based testing. In contrast to the traditional biopsy of tissues and visualization diagnostics, blood based biomarkers make routine health check-ups more convenient and accessible.

Health care professionals have recognized that early identification will lower the cost of hospitalization, increase the efficiency of treatment, and also help cut the cost associated with long-term treatment. Similarly, pharmaceuticals companies are making efforts towards development of such biomarker-based screening process where they can identify individuals with a high chance of suffering from diseases so that they can be treated accordingly.

High Cost of Advanced Biomarker Platforms

One of the major limitations faced by the market for Blood Based Biomarkers is the high costs associated with the use of advanced technologies such as NGS, digital PCR, mass spectrometry, high throughput proteomics and multi-omics. These are relatively expensive, not only in terms of equipment but also specialized reagents and advanced lab infrastructure, which translates into higher per test cost.

Many laboratories have found it difficult to justify the ROI due to low patient volume or uncertain reimbursement policies. Besides the above factors, the costs related to maintenance of instrumentation, purchasing of software licenses and data interpretation further add up. Therefore, for smaller laboratories as well as routine testing, the application of advanced biomarker tests faces financial obstacles.

Moreover, the same issue arises from the perspective of patients themselves because they face huge upfront costs without proper insurance. Thus, although technologically feasible and clinically effective, Blood Based Biomarkers will continue to be available to only select few until the platform costs decrease.

Segmentation Analysis

The Global Blood Based Biomarkers Market is segmented based on the biomarker type, disease area, application, technology, sample type, end user, and region/countries.

Rising Global Cancer Burden and Precision Oncology Adoption Strengthening Oncology Segment Leadership

The most notable division in the Blood Based Biomarkers Market Size report is the oncology segment. This is driven by the massive population of cancer patients, unmet needs for accurate diagnosis, and increased interest in repeatable molecular analysis. According to Bray et al., there are nearly 20 million new cancer diagnoses and 9.7 million cancer fatalities worldwide in 2022. Meanwhile, the number of cases is expected to rise to 35.3 million annually by 2050.

As such, oncology remains crucial to Diagnostic Biomarkers Market Analysis. Blood based biomarkers play an essential role in the screening, tumor profile creation, choice of treatment methods, evaluation of treatment efficacy, diagnosis of disease recurrence, and minimal residual disease detection. The oncology sector is particularly relevant in cancer conditions with high morbidity rates, such as lung, breast, colon, and prostate cancers.

Consistent with Liquid Biopsy Market Growth, oncology relies on blood-based biomarkers like ctDNA, CTCs, cfDNA, and exosomes. Such biomarkers enable healthcare professionals to track the evolution of tumors, identify resistance mutations, and select personalized treatment strategies. Regarding Clinical Biomarker Market Trends and Precision Medicine Diagnostics Forecast, the focus in oncology is moving away from one-time diagnosis toward continuous cancer treatment.

Geographical Penetration

Strong Precision Medicine Infrastructure and High Cancer Testing Demand Driving North America Market Leadership

North America is anticipated to hold the largest market share for the Blood-Based Biomarkers Market due to high cancer diagnosis demand, sophisticated diagnostic facilities, and fast adoption of precision medicine diagnostics. In 2024, the U.S. alone is estimated to witness 2,001,140 new cancer cases and 611,720 cancer deaths.

North America also constitutes a leading player in Liquid Biopsy Market Growth, which uses FDA approved blood-based biomarkers like Guardant360 CDx and FoundationOne Liquid CDx for tumor genomics profiling and companion diagnostics using blood samples.

In terms of Diagnostic Biomarkers Market Analysis, North America enjoys a dominant market position owing to the presence of companies like Guardant Health, GRAIL, Natera, Foundation Medicine, Labcorp, and Quest Diagnostics. Adoption of ctDNA, MRD assays, blood biomarkers for Alzheimer's disease, and multi-omics platform is aiding in bolstering its market position. North America also enjoys support from various initiatives aimed at developing a precision medicine ecosystem. For instance, the NIH launched its 'All of Us' project, aimed at assembling a 1 million-member precision medicine research group.

U.S. Blood Based Biomarkers Market Trends

The U.S. emerges as a significant growth contributor within the Blood Based Biomarkers Market owing to the presence of a vibrant ecosystem of molecular diagnostics firms, reference laboratories, cancer research institutes, and precision medicine initiatives. The U.S. has seen a high degree of adoption of blood-based tests in the field of oncology, cardiovascular disease, infectious disease, and neurological conditions, thanks to sophisticated laboratory setups and physicians' awareness.

One of the major growth drivers will be the increasing deployment of ctDNA and liquid biopsy testing services in selecting therapies, assessing treatment response, conducting MRD analysis, and detecting tumor recurrence. Moreover, there is an active clinical trial environment in which blood-based biomarkers are becoming common in patient stratification and developing companion diagnostics.

On the other hand, growing interest in biomarker discovery in Alzheimer's disease, multi-cancer screening, and artificial intelligence (AI)-enabled biomarker interpretation is likely to expand the application base of blood-based biomarker testing. The growing involvement of firms like Guardant Health, Natera, GRAIL, Foundation Medicine, LabCorp, and Quest Diagnostics provides a further boost to this trend.

Canada Blood Based Biomarkers Market Outlook

Canada has proven to be a promising growth market for blood-based biomarkers due to its increasing burden of cancer, aging population, and increasing use of precision medicine. As of 2024, there have been 247,100 new cancer diagnoses and 88,100 cancer deaths in Canada, resulting in a high demand for biomarker-driven cancer screening, treatment selection, and disease monitoring.

Additionally, Canada has a rising requirement for neurological biomarker testing because 771,939 people had dementia in the country as of January 1, 2025, and more than 1 million Canadians are projected to have dementia by 2030.

The country's market will be further bolstered by national initiatives in Canada that encourage the implementation of genomic testing and biomarker assays. Canada is a significant market for oncology liquid biopsy tests, Alzheimer's blood biomarker tests, and precision medicine.

Competitive Landscape

- The Blood-Based Biomarkers Market witnesses intense competition due to high level of innovations and growth opportunities. The competitors include specialized Liquid Biopsy players, established Diagnostics, Molecular testing and Technology Platform Players. Guardant Health, Inc., GRAIL, Inc., Natera, Inc., Foundation Medicine, Inc. and Tempus are leading the market trend by focusing on ctDNA testing, Multi Cancer Early Detection, MRD Testing and Artificial Intelligence-powered precision oncology. They are disrupting the market space by shifting focus towards early-stage diagnostics, biomarker-based monitoring and diagnosis.

- Some of the prominent players like F. Hoffmann-La Roche Ltd, Abbott, Siemens Healthcare Private Limited, Thermo Fisher Scientific Inc., QIAGEN, bioMérieux and Beckman Coulter, Inc. retain their competitiveness with global laboratory network, broad diagnostic offerings, high installed instrument base and robust clinical presence. This enables them to bring their products to market faster and also gain better adoption from physicians. Other players Illumina, Inc. and Bio-Rad Laboratories, Inc. have played important roles as enabling technology platforms for sequencing and Polymerase Chain Reaction (PCR)-based tests along with biomarker assays. Sysmex Europe SE., Freenome Holdings, Inc., Labcorp, Quest Diagnostics Incorporated., Exact Sciences Corporation. and Personalis, Inc. continue to grow with their biomarker testing capabilities.

- The competitive landscape now focuses on clinical validation proficiency, financial backing, assay accuracy, informatics proficiency, and the confidence of physicians along with pharmaceutical industry partnerships. The firms able to generate solid data, operate efficient testing ecosystems and integrate precision medicine will become dominant players going forward.

Key Developments

- July 2024 - Foundation Medicine, Inc. received FDA approval for FoundationOne Liquid CDx as a companion diagnostic for AKEEGA, supporting blood-based genomic profiling in advanced prostate cancer.

- November 2024 - Foundation Medicine, Inc. received FDA approval for FoundationOne Liquid CDx as the first companion diagnostic to identify NSCLC patients eligible for TEPMETKO.

- April 2025 - Natera, Inc. launched its ultra-sensitive Signatera Genome MRD test for pan-cancer minimal residual disease monitoring using ctDNA detection.

- September 2025 - F. Hoffmann-La Roche Ltd received FDA clearance for Elecsys pTau181, a blood-based Alzheimer’s biomarker test for primary-care assessment.

- October 2025 - GRAIL, Inc. reported PATHFINDER 2 results showing that the Galleri multi-cancer early detection blood test increased cancer detection when added to standard screening.

White Space Opportunities

DataM perceives huge whitespace opportunities available in the Blood Based Biomarkers Market outside conventional diagnosis. While most competitors may be concentrating on oncology liquid biopsy, ctDNA testing, and companion diagnostics, untapped fields like neurological disorders, autoimmune diseases, metabolic disorders, preventive screenings, recurrence monitoring, and multiplexed biomarker panels have plenty of scope for growth. All these applications require high sensitivity and clinical validation and reusability by a blood-based test.

There is an important opportunity that can make a player very successful depending on their product offering. A company that offers complete biomarker discovery, assay design, advanced algorithms, clinical validation, physician reporting, and even insurance reimbursement can expect success in the market. Players who have a model for providing testing services for hospitals, diagnostic labs, pharmaceuticals, and preventive healthcare companies can expect significant success.

DMI Opinion

According to DataM, the growth of the Blood Based Biomarkers Market is not solely dependent upon the availability of tests but rather upon their ability to offer clinically validated, accurate, and actionable diagnostic insights. This industry is moving away from traditional single-biomarker testing toward blood-based tests that enable early detection, therapy selection, therapeutic monitoring, and recurrence monitoring.

Based on the analysis conducted by DataM, it can be seen that the biggest potential lies in fields like Oncology liquid biopsy tests, MRD monitoring, Multi-Cancer Early Detection Tests, Alzheimer’s Blood Biomarkers, and Multi-Biomarker Panels. Companies offering tests that exhibit superior performance parameters such as sensitivity, specificity, repeatability, turnaround times, and high clinical value will have an upper hand. Hence, the best way to approach this market would be to consider it a precision diagnostics and clinical decision support market.

Why Choose DataM?

- Biomarker and Diagnostic Innovation: Discusses innovations in ctDNA, cfDNA, CTCs, protein biomarkers, genomics biomarkers, panel of biomarkers, liquid biopsy, MRD tests, companion diagnostics and blood-based disease monitoring.

- Competitive Positioning of Major Companies: Reviews leading companies considering their test menu, clinical validation, assay sensitivity, regulatory status, reimbursement options, laboratory capacity, technology platforms, and disease focus areas.

- Key Trends & Dynamics: Highlights important trends, including minimally invasive diagnostics, early detection of diseases, use of precision medicine, growth in oncology liquid biopsy, Alzheimer’s blood biomarkers and AI-assisted biomarker analysis.

- Strategies by Major Players: Highlights business strategies employed by leading companies, which include partnerships, FDA approvals, companion diagnostics collaborations, clinical studies, expansion of laboratories, biomarker discovery and commercialization strategies.

- Pricing of Blood Based Biomarkers Test: Offers insights into test pricing, reimbursement mechanisms, payer support, laboratory testing cost, geographical availability and adoption challenges in major markets.

Target Audience

- Diagnostic and molecular testing companies

- Liquid biopsy and precision diagnostics providers

- Hospitals and integrated healthcare systems

- Diagnostic laboratories and reference labs

- Oncology centers and cancer care networks

- Pharmaceutical and biotechnology companies

- Companion diagnostic developers

- Clinical research organizations and trial sponsors

- Genomics, proteomics and multi-omics platform providers

- AI-driven healthcare analytics companies

- Neurology and cardiovascular diagnostic providers

- Preventive healthcare and screening program operators

- Regulatory, reimbursement and healthcare policy stakeholders

- Investors, private equity and venture capital firms

- Healthcare consulting and life sciences advisory firms

- Academic research institutes and biomarker discovery centers

- Precision medicine and translational research organizations

- Laboratory equipment and assay kit manufacturers