Aromatase Inhibitor Drug Class Market Overview

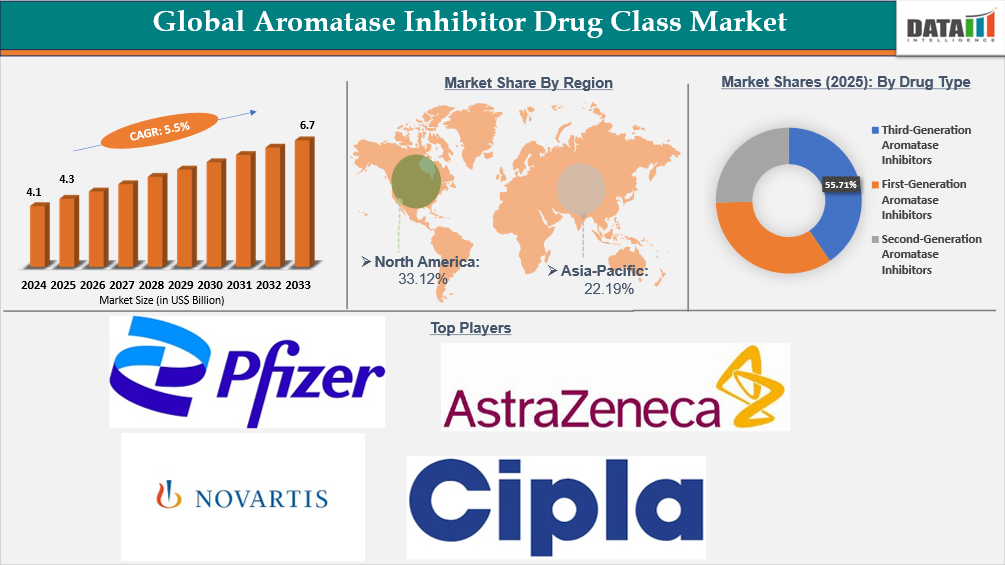

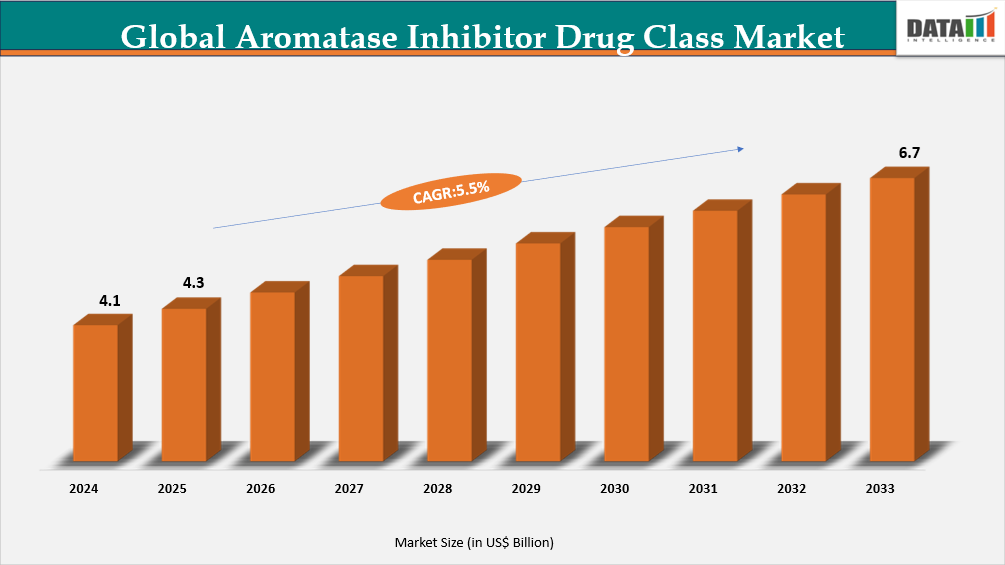

The global aromatase inhibitor drug class market reached US$4.1 Billion in 2024, rising to US$4.3 Billion in 2025 and is expected to reach US$6.7 Billion by 2033, growing at a CAGR of 5.5% from 2026 to 2033.

The global aromatase inhibitor drug class market is anchored in the high burden of hormone receptor-positive breast cancer, the most common subtype, accounting for nearly 60% of all female breast cancer cases in the U.S. population according to SEER data. With an estimated 2.3 million new breast cancer cases and 670,000 deaths worldwide in 2022 reported by the World Health Organization, the role of endocrine therapies including aromatase inhibitors remains critical in disease management.

Endocrine resistance driven by ESR1 mutations occurs in roughly 20–40% of metastatic HR+ breast cancer patients following aromatase inhibitor therapy, underscoring unmet medical need for next-generation therapies. In the U.S. alone, approximately 200,000 patients receive first-line endocrine treatments targeting HR+ disease, frequently involving aromatase inhibitors in combination regimens. Global demographic shifts and rising breast cancer incidence projections, expected to reach 3.2 million new cases annually by 2050, support sustained growth and innovation in aromatase inhibitor use and related endocrine oncology treatments.

Aromatase Inhibitor Drug Class Industry Trends and Strategic Insights

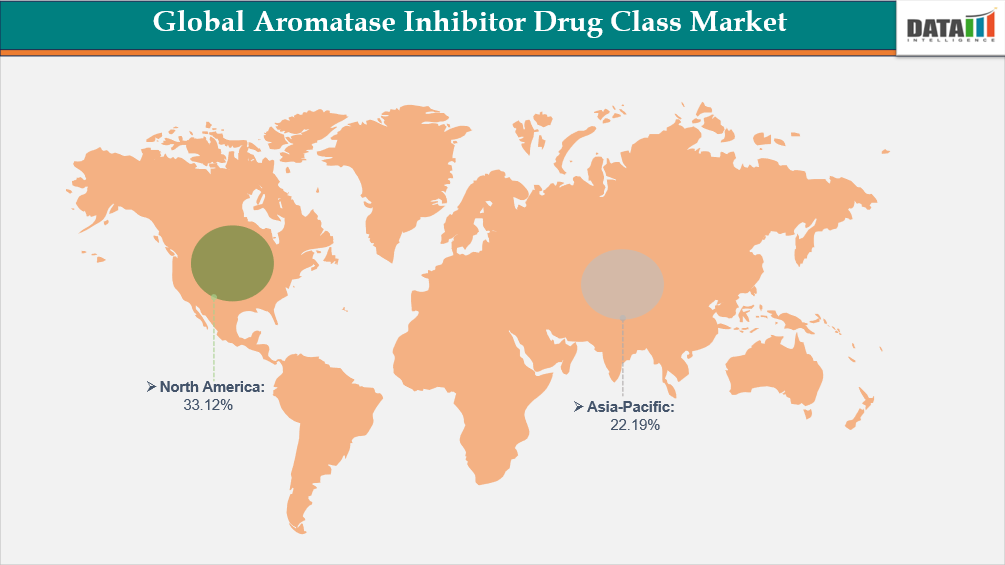

- North America leads the global aromatase inhibitor drug class market, capturing the largest revenue share of 33.12% in 2025.

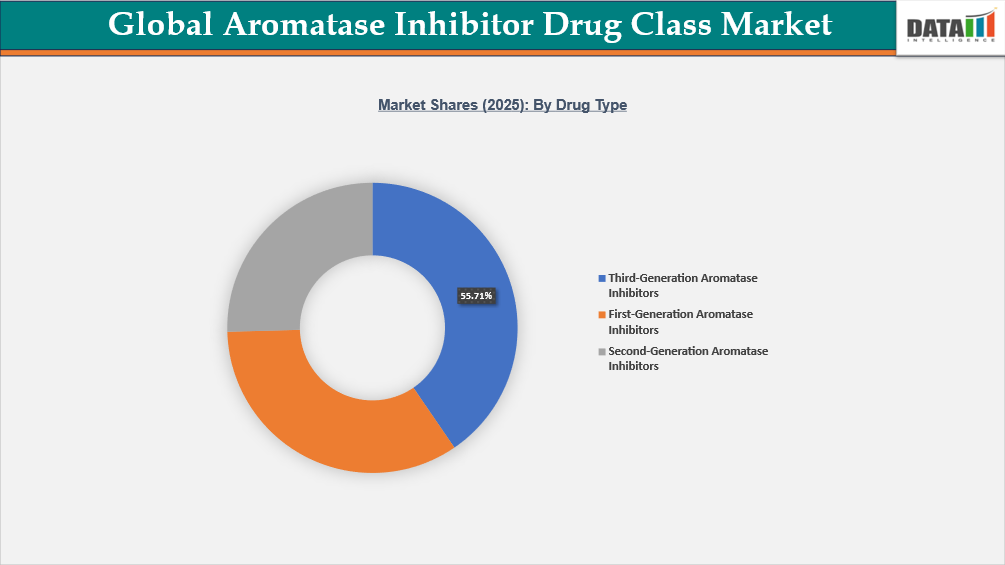

- By Drug Type segment, third-generation aromatase inhibitors led the global aromatase inhibitor drug class market, capturing the largest revenue share of 55.71% in 2025.

Global Aromatase Inhibitor Drug Class Market Size and Future Outlook

- 2025 Market Size: US$4.3 Billion

- 2033 Projected Market Size: US$6.7 Billion

- CAGR (2026–2033): 5.5%

- Dominating Market: North America

Fastest Growing Market: Asia-Pacific

Source : DataM Intelligence

For More Detailed information Request for Sample

Market Dynamics

Growing Adoption of Targeted Endocrine Therapies

The growing adoption of targeted endocrine therapies is a key driver for the aromatase inhibitor drug class, which is recommended as first-line treatment for hormone receptor-positive breast cancer by leading oncology bodies such as the National Comprehensive Cancer Network (NCCN) and ESMO. According to the U.S. National Cancer Institute (SEER Program), hormone receptor-positive disease represents approximately 70–75% of all diagnosed breast cancer cases.

The use of aromatase inhibitors has further expanded through combination endocrine regimens, particularly with CDK4/6 inhibitors in advanced and metastatic settings. Treatment pattern studies referenced by the U.S. FDA and NCI indicate that over 80% of first-line metastatic HR-positive breast cancer patients in developed healthcare systems receive an AI-based combination therapy.

Additionally, research published by the National Institutes of Health (NIH) reports that ESR1 mutations emerge in approximately 20–40% of patients following prolonged aromatase inhibitor exposure, reinforcing continued optimization rather than displacement of AI therapy. These trends firmly position aromatase inhibitors as a foundational component of modern targeted endocrine treatment strategies.

Segmentation Analysis

The global aromatase inhibitor drug class market is segmented based on drug type, mechanism, therapeutic indication, route of administration, line of therapy, treatment modality, distribution channel and region.

Rising Demand for Third-Generation Aromatase Inhibitors Driven by Clinical Superiority and Standard-of-Care Adoption

Third-generation aromatase inhibitors such as letrozole, anastrozole, and exemestane have become the standard of care in hormone receptor-positive breast cancer due to their superior efficacy and tolerability compared with earlier agents. Clinical trials and guideline updates referenced by the National Comprehensive Cancer Network (NCCN) show third-generation AIs significantly improve disease-free survival versus tamoxifen in postmenopausal women, driving widespread adoption. According to U.S. National Cancer Institute (SEER) data, hormone receptor-positive breast cancer accounts for roughly 70–75% of all breast cancer cases, intensifying demand for effective third-generation endocrine therapies.

The global shift toward personalized oncology care has further elevated demand, with real-world treatment patterns indicating that over 60% of postmenopausal patients now initiate therapy with a third-generation AI, as reported in NIH-supported clinical registries. Third-generation AIs are also a cornerstone of combination regimens, such as with CDK4/6 inhibitors, used in approximately 80% of first-line metastatic HR+ cases, according to treatment utilization studies cited by the U.S. FDA. Robust clinical evidence and expanded use in both early and advanced disease settings continue to bolster market demand for these agents worldwide.

Geographical Penetration

Largest Market:

Demand for Aromatase Inhibitor Drug Class Market in North America

North America’s demand for aromatase inhibitors is underpinned by the high prevalence of hormone receptor-positive breast cancer, which constitutes the majority of cases among women diagnosed with breast cancer. In U.S. women aged 20–49 years, about 61.5% of invasive breast cancers are estrogen receptor (ER)-positive/progesterone receptor (PR)-positive, highlighting the large eligible population for endocrine therapies including AIs.

Trends from U.S. cancer registries show ER-positive breast cancer incidence continuing to rise annually, with a steady increase in hormone-driven disease over the past decade. Strong integration of AIs into standard practice, especially alongside targeted agents, reflects early adoption and guideline consonance across major healthcare systems in the region.

U.S. Aromatase Inhibitor Drug Class Market Outlook

In the U.S., breast cancer remains a leading health concern, with hormone receptor-positive disease a predominant subtype driving demand for aromatase inhibitors. National registry data indicate that among women with breast cancer, ER+/PR+ tumors represent over 60% of cases, underscoring the sizeable population treated with endocrine therapy.

The clinical patterns show increasing use of aromatase inhibitors as first-line therapy, often in combination regimens, reflecting broad clinician confidence and payer support for AI-based endocrine strategies. Contemporary survival and recurrence risk data further validate extended AI use to suppress estrogen-driven tumor proliferation beyond initial treatment. Together, these factors support a strong outlook for the U.S. aromatase inhibitor market, anchored in pervasive hormone receptor-positive disease burden and evolving clinical protocols.

Canada Aromatase Inhibitor Drug Class Market Trends

In Canada, breast cancer is the most frequently diagnosed cancer among women, with about 1 in 8 females expected to develop breast cancer during their lifetime according to federal public health data. Approximately 64.8% of breast cancers in Ontario are hormone receptor-positive HER2-negative, a patient group routinely managed with endocrine therapies including aromatase inhibitors. Provincial treatment pattern analyses show substantial adoption of systemic endocrine therapy, with aromatase inhibitors used widely relative to alternative hormone agents, highlighting their role in Canada’s standard oncology care pathway and sustained therapeutic demand.

Fastest Growing Market:

Asia-Pacific Records the Fastest Growth in the Aromatase Inhibitor Drug Class Market

Asia-Pacific is recording accelerated demand for aromatase inhibitors as breast cancer incidence rises across the region, with latest data showing breast cancer remains the most common cancer among women and rates increasing year-on-year. According to OECD/WHO reporting, high-income Asia-Pacific countries had age-standardized incidence rates of up to 76–100+ per 100,000 women, with rapid increases observed in China, India, Japan, and Korea.

Asia still trails Western rates but incidence has climbed significantly due to changing lifestyles and aging populations. Regional therapeutic adoption is supported by expanded oncology infrastructure and guideline-based endocrine therapy integration. This combination of rising epidemiology and treatment access positions the region as the fastest-growing aromatase inhibitor market globally.

India Aromatase Inhibitor Drug Class Market Insights

India’s breast cancer burden continues to grow, with cancer registries estimating over 1.56 million total new cancer cases in 2024, of which a large proportion are female cases that include breast cancer as the leading site. Hormone receptor-positive breast cancer, the primary indication for aromatase inhibitors, is rising, supported by national registry trends that show increasing incidence across states.

Lifetime risk statistics indicate a substantial portion of the female population faces breast cancer, with many cases detected at later stages due to screening gaps. Expansion of oncology centres and public health initiatives to improve early diagnosis is enhancing uptake of standard endocrine regimens, including aromatase inhibitors. Continued increases in incidence and improved access to therapy are expected to drive stronger demand for these drugs.

China Aromatase Inhibitor Drug Class Market Industry Growth

In China, cancer registry analyses estimate over 3.24 million new cancer cases in 2024, with female cancers contributing significantly, and breast cancer representing a major share of female malignancies. Although breast cancer incidence in China is lower in rate per 100,000 compared with Western countries, the absolute number of cases remains high due to the country’s large population.

The age-standardized incidence of cancers has increased among women, adding to demand for established endocrine therapies including aromatase inhibitors. Government programs and broader insurance coverage improvements support access to oncology drugs, while growing screening and early detection play roles in enhancing treatment uptake. These structural and demographic factors are contributing to China’s expanding role in the global aromatase inhibitor market.

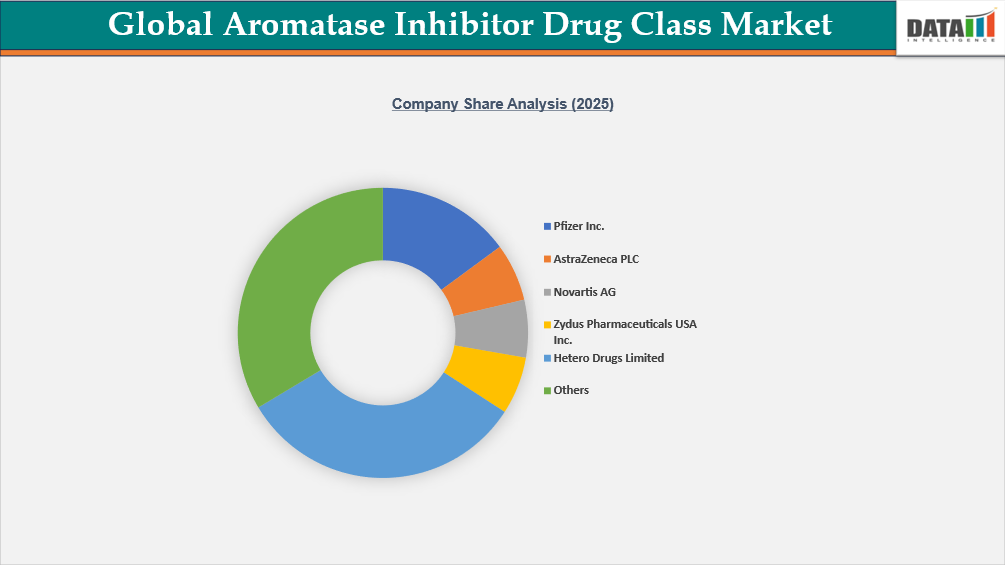

Competitive Landscape

The global aromatase inhibitor market is highly competitive, dominated by major pharmaceutical players such as Pfizer Inc., AstraZeneca PLC, Novartis AG, and Sandoz International GmbH, alongside key generics manufacturers including Dr. Reddy’s Laboratories, Cipla, Hetero Drugs, and Amneal Pharmaceuticals. Companies like Jiangsu Hengrui Pharmaceuticals and Zydus Pharmaceuticals USA are expanding their presence through strategic R&D investments and regional commercialization strategies.

The competition is driven by innovation in next-generation endocrine therapies, patent expirations, and the introduction of combination regimens with CDK4/6 inhibitors. Market leaders leverage extensive global distribution networks and licensing partnerships to enhance accessibility and maintain market share. This dynamic landscape encourages continuous product differentiation, aggressive clinical development, and strategic collaborations to capture growth opportunities in hormone-dependent breast cancer treatment.

Key Developments

- In January 2024, Sermonix Pharmaceuticals and Henlius Biotech have entered a strategic collaboration granting Henlius exclusive rights to develop, manufacture, and commercialize lasofoxifene in China for ER+/HER2- breast cancer. This partnership, including an upfront payment, milestone payments up to US$ 58 million, and royalties, strengthens Henlius’ endocrine therapy portfolio and accelerates clinical development of Phase 3 trials in the region. The deal highlights ongoing investments and collaborations driving growth and innovation within the global aromatase inhibitor and hormone-targeted therapy market.

- In february 2025, AstraZeneca’s camizestrant, a next-generation oral SERD and complete estrogen receptor antagonist, demonstrated statistically significant improvement in progression-free survival in 1st-line HR-positive, HER2-negative advanced breast cancer with emergent ESR1 mutations in the SERENA-6 Phase III trial. The study evaluated switching from standard aromatase inhibitor therapy in combination with CDK4/6 inhibitors, highlighting the potential of novel endocrine therapies to address AI resistance. This development underscores innovation and competitive evolution in the global aromatase inhibitor and hormone-targeted therapy market.

What Sets This Global Aromatase Inhibitor Drug Class Market Intelligence Report Apart

- Latest Data & Forecasts – Comprehensive and up-to-date market intelligence with forecasts through 2033, covering global demand by drug type (steroidal vs non-steroidal), indication, therapy line, and distribution channel, with region-wise analysis across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

- Regulatory Intelligence – In-depth assessment of global pharmaceutical regulatory frameworks impacting aromatase inhibitor development and commercialization, including FDA, EMA, NMPA, PMDA, and CDSCO requirements, clinical trial pathways, labeling standards, patent exclusivity, and post-marketing surveillance.

- Competitive Benchmarking – Structured benchmarking of leading innovator and generic manufacturers based on product portfolios, pipeline strength, geographic reach, pricing strategies, clinical differentiation, and partnerships in endocrine oncology.

- Geographic & Emerging Market Coverage – Regional analysis highlighting breast cancer prevalence, treatment adoption rates, reimbursement environments, and access to endocrine therapies, with special focus on growth opportunities in Asia-Pacific, Latin America, and Middle Eastern markets.

- Actionable Strategies & Cost Dynamics – Strategic insights into lifecycle management, generic entry risks, combination therapy positioning, pricing pressures, and manufacturing cost structures, supported by expert perspectives from oncology specialists, regulatory advisors, and pharmaceutical executives.