Alzheimer’s Disease Therapeutics Size

The global alzheimer’s disease therapeutics market size reached US$ 5.38 billion in 2025 and is expected to reach US$ 17.98 billion by 2033, growing at a CAGR of 14.32 % during the forecast period 2026-2033.

The global Alzheimer’s disease therapeutics market is witnessing a structural transition from symptomatic management toward disease-modifying treatments, driven by advancements in neurobiology, biomarker-based diagnostics, and monoclonal antibody development. Traditionally dominated by cholinesterase inhibitors and NMDA receptor antagonists, the market is now evolving with the introduction of anti-amyloid therapies targeting underlying disease pathology. Growing aging populations, particularly in North America, Europe, and parts of Asia-Pacific, continue to increase the patient pool, thereby sustaining long-term demand for therapeutic interventions. Additionally, improved diagnostic capabilities, including PET imaging and cerebrospinal fluid biomarkers, are enabling earlier detection and expanding the addressable treatment population. Pharmaceutical companies are intensifying R&D investments, with a strong pipeline focused on amyloid, tau, and neuroinflammation pathways. However, factors such as high treatment costs, safety concerns, and reimbursement challenges may influence adoption rates. Overall, the market is poised for significant growth, supported by innovation, regulatory momentum, and increasing clinical awareness.

For more details on this report – Request for Sample

Alzheimer’s Disease Therapeutics Dynamics

Rising Prevalence of Alzheimer's Disease

The growing prevalence of Alzheimer’s disease is poised to be a major driver of the healthcare market in the coming years. With aging populations, the number of Alzheimer’s cases is rising rapidly, creating an urgent demand for improved diagnostic tools, effective treatments, and comprehensive care solutions. Alzheimer’s affects approximately 50-60% of people suffering from dementia.

For instance, according to CSIR-NIScPR, Alzheimer's disease presents a significant global health burden in 2023, with the latest estimates indicating that more than 57.4 million people are currently affected by the condition. The Global Burden of Disease Study (GBDS) 2019 predicts that between 2019 and 2050, the number of dementia cases will increase by a staggering 166%, impacting approximately 152.8 million individuals. These projections align closely with those made by the World Health Organization (WHO), highlighting the growing prevalence of the disease and its substantial impact on global healthcare systems.

According to the Alzheimer’s Disease International Organization estimated that, the number of individuals with dementia will reach about 78 million in 2030 and 139 million in 2050. With the increasing dementia, the individuals with alzheimer’s is expected to grow, increasing the demand for alzheimer’s therapeutics and further driving the market growth.

This trend is prompting increased investment from pharmaceutical companies, healthcare providers, and biotech firms focused on developing innovative therapies and early detection methods. At the same time, governments and private organizations are boosting funding for public awareness, caregiver support, and long-term care infrastructure.

As a result, the Alzheimer’s care ecosystem is expanding, presenting both a pressing public health challenge and a significant opportunity for growth across multiple sectors of the healthcare industry.

Regulatory and Approval Challenges

Regulatory and approval challenges pose a significant barrier to the growth of the Alzheimer’s disease therapeutics market. Developing drugs for Alzheimer’s is particularly complex due to the disease’s slow and variable progression, which makes it difficult to demonstrate clear clinical benefits in trials. Regulatory bodies such as the FDA and EMA require extensive data to prove not only safety but also long-term efficacy, often through large, multi-year Phase III studies. These requirements significantly extend development timelines and increase costs, while offering no guarantee of approval.

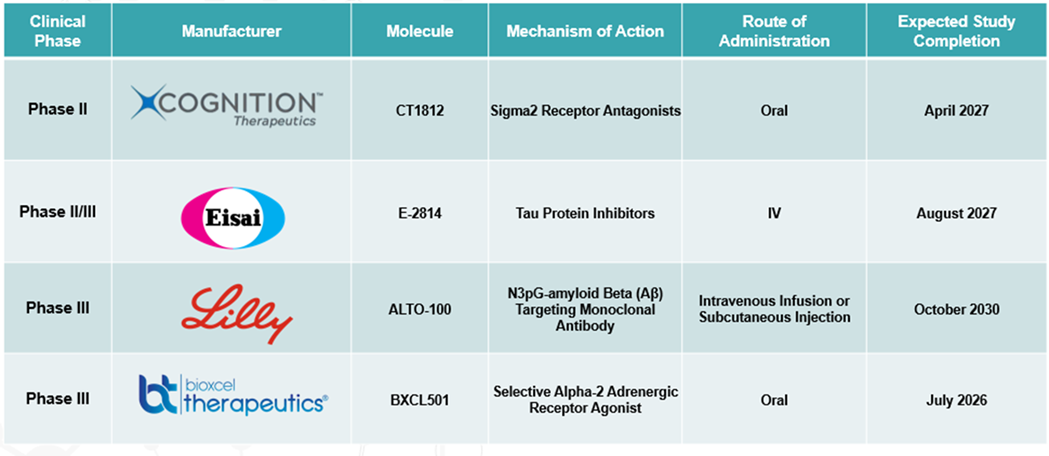

Alzheimer’s Disease Therapeutics Pipeline Analysis

Top phase III pipeline products for Alzheimer’s disease:

Alzheimer’s Disease Therapeutics Segment Analysis

The global alzheimer’s disease therapeutics market is segmented based on stage, drug class, and region.

Drug Class:

The cholinesterase inhibitors segment is expected to dominate the alzheimer’s disease therapeutics market with the highest market share

The cholinesterase inhibitors segment is expected to remain dominant in the alzheimer’s disease therapeutics market due to their established efficacy, affordability, and broad clinical application. Drugs like donepezil, rivastigmine, and galantamine work by inhibiting the breakdown of acetylcholine, a neurotransmitter crucial for memory and cognitive function. This mechanism helps alleviate symptoms, particularly in patients with mild to moderate Alzheimer’s, offering modest improvements in cognitive abilities.

The rising global prevalence of Alzheimer’s disease, which is expected to affect over 150 million people by 2050, further strengthens the demand for these therapies.

Additionally, ongoing clinical trials aim to assess its efficacy and safety across various patient populations, ensuring continued innovation within this drug class. The approval of new formulations that reduce gastrointestinal side effects also enhances the market's appeal. As the global prevalence of Alzheimer’s increases, the continued research, effectiveness, and cost-effectiveness of cholinesterase inhibitors will solidify their dominant position in the market.

Alzheimer’s Disease Therapeutics Geographical Analysis

North America is expected to hold a significant position in the global alzheimer’s disease therapeutics market

North America is expected to maintain a dominant position in the global Alzheimer’s disease therapeutics market, driven by several key factors. The growth is supported by a high prevalence of Alzheimer’s, significant investments in research and development. For instance, according to the Alzheimer's Association, an estimated 7.2 million Americans aged 65 and older are living with Alzheimer's disease in 2025, with 74% of them being 75 years or older. By 2050, this number is expected to nearly double, reaching close to 13 million. Approximately 1 in 9 individuals aged 65 and older will be affected by Alzheimer's. Furthermore, the health and long-term care costs for people living with dementia are projected to reach $384 billion in 2025 and nearly $1 trillion by 2050.

The presence of major pharmaceutical companies, favorable reimbursement policies, and strong government support for Alzheimer’s research further bolsters the region's market growth. North America continues to lead in Alzheimer's treatment developments. For instance, in July 2024, Eli Lilly and Company announced that the U.S. Food and Drug Administration had approved Kisunla (donanemab-azbt). This once-monthly injection for early symptomatic Alzheimer's, including mild cognitive impairment (MCI) and mild dementia with confirmed amyloid pathology, is the first amyloid plaque-targeting therapy with evidence supporting stopping treatment after plaque removal.

This breakthrough therapy not only offers potential clinical benefits but also promises lower treatment costs and fewer infusions, further solidifying North America's dominant position in the Alzheimer's therapeutics market. Additionally, advancements in treatment options contribute to North America's market leadership.

Alzheimer’s Disease Therapeutics Top Companies

Top companies in the alzheimer’s disease therapeutics market include Eli Lilly and Company, Eisai Co., Ltd., Biogen Inc., F. Hoffmann-La Roche Ltd., Johnson & Johnson, Novo Nordisk A/S, AbbVie Inc., TauRx Pharmaceuticals Ltd., Alzheon, Inc., Annovis Bio, Inc. among others.

Key Developments

- April 2026 – Eli Lilly and Eisai expanding disease-modifying Alzheimer’s therapies

Eli Lilly and Company and Eisai Co., Ltd. advanced commercialization and clinical expansion of amyloid-targeting therapies aimed at slowing cognitive decline in early Alzheimer’s patients. - March 2026 – Biogen and Roche strengthening biomarker-based treatment strategies

Biogen Inc. and F. Hoffmann-La Roche Ltd. increased focus on blood-based biomarkers, imaging diagnostics, and precision treatment selection to improve early intervention outcomes. - February 2026 – AbbVie and Novo Nordisk accelerating neurodegeneration R&D

AbbVie Inc. and Novo Nordisk A/S expanded research programs targeting inflammation, metabolic pathways, and neuroprotection for next-generation Alzheimer’s therapeutics. - January2026 – Emerging biotech firms progressing novel tau and cognitive therapies

Companies such as TauRx Pharmaceuticals, Alzheon, and Annovis Bio advanced clinical development of tau-targeting agents and therapies focused on cognition improvement. - In January 2026, Novartis strengthened its Alzheimer’s disease pipeline through a US$1.7 billion licensing agreement with SciNeuro. Through this partnership, Novartis gained access to next-generation antibody therapies designed to improve brain delivery, reflecting the growing strategic focus of major pharmaceutical companies on advanced therapeutic approaches beyond conventional amyloid-targeting mechanisms.

- In January 2026, The U.S. FDA accepted the supplemental Biologics License Application for LEQEMBI IQLIK as a subcutaneous starting-dose option for early Alzheimer’s disease. Eisai and Biogen received Priority Review for the filing, with a PDUFA action date set for May 24, 2026. This development is expected to improve treatment convenience by supporting a more accessible at-home administration pathway and reducing reliance on infusion-based settings.

Alzheimer’s Disease Therapeutics Scope

| Metrics | Details | |

| CAGR | 14.32 % | |

| Market Size Available for Years | 2022-2033 | |

| Estimation Forecast Period | 2025-2033 | |

| Revenue Units | Value (US$ Bn) | |

| Segments Covered | Stage | Early-stage Alzheimer's (Mild), Middle-stage Alzheimer's (Moderate), Late-stage Alzheimer's (Severe) |

| Drug Class | Cholinesterase Inhibitors, NMDA Receptor Antagonists, Combination Drugs, Immunotherapy | |

| Regions Covered | North America, Europe, Asia-Pacific, South America, and the Middle East & Africa | |

Why Purchase the Report?

- Pipeline & Innovations: Reviews ongoing clinical trials, product pipelines, and forecasts upcoming advancements in medical devices and pharmaceuticals.

- Product Performance & Market Positioning: Analyze product performance, market positioning, and growth potential to optimize strategies.

- Real-World Evidence: Integrates patient feedback and data into product development for improved outcomes.

- Physician Preferences & Health System Impact: Examines healthcare provider behaviors and the impact of health system mergers on adoption strategies.

- Market Updates & Industry Changes: Covers recent regulatory changes, new policies, and emerging technologies.

- Competitive Strategies: Analyzes competitor strategies, market share, and emerging players.

- Pricing & Market Access: Reviews pricing models, reimbursement trends, and market access strategies.

- Market Entry & Expansion: Identifies optimal strategies for entering new markets and partnerships.

- Regional Growth & Investment: Highlights high-growth regions and investment opportunities.

- Supply Chain Optimization: Assesses supply chain risks and distribution strategies for efficient product delivery.

- Sustainability & Regulatory Impact: Focuses on eco-friendly practices and evolving regulations in healthcare.

- Post-market Surveillance: Uses post-market data to enhance product safety and access.

- Pharmacoeconomics & Value-Based Pricing: Analyzes the shift to value-based pricing and data-driven decision-making in R&D.

The global alzheimer’s disease therapeutics market report delivers a detailed analysis with 57 key tables, more than 46 visually impactful figures, and 168 pages of expert insights, providing a complete view of the market landscape.

Target Audience

- Manufacturers: Pharmaceutical, Medical Device, Biotech Companies, Contract Manufacturers, Distributors, Hospitals.

- Regulatory & Policy: Compliance Officers, Government, Health Economists, Market Access Specialists.

- Technology & Innovation: AI/Robotics Providers, R&D Professionals, Clinical Trial Managers, Pharmacovigilance Experts.

- Investors: Healthcare Investors, Venture Fund Investors, Pharma Marketing & Sales.

- Consulting & Advisory: Healthcare Consultants, Industry Associations, Analysts.

- Supply Chain: Distribution and Supply Chain Managers.

- Consumers & Advocacy: Patients, Advocacy Groups, Insurance Companies.

- Academic & Research: Academic Institutions.