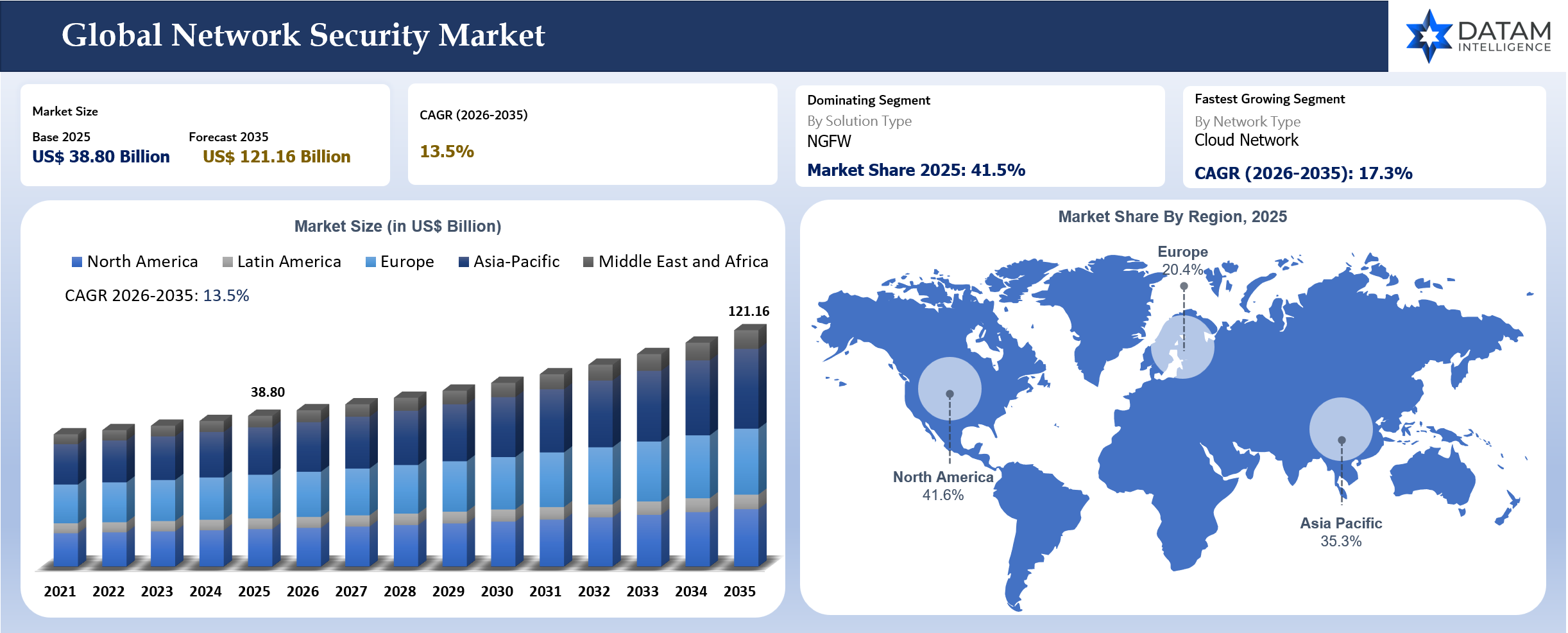

Network Security Market Size

The global network security market reached US$ 38.80 billion in 2025 and is expected to reach US$ 121.16 billion by 2035, growing at a CAGR of 13.5% during 2026 to 2035. Enterprise network security is being redesigned because users, applications and workloads no longer sit behind a simple perimeter. Traffic now moves across branches, SaaS platforms, public cloud, private data centers, remote devices, industrial sites and telecom networks. Buyers are therefore shifting from firewall-only strategies toward NGFW, SASE, SSE, ZTNA, NDR, DDoS protection, NAC and cloud network security.

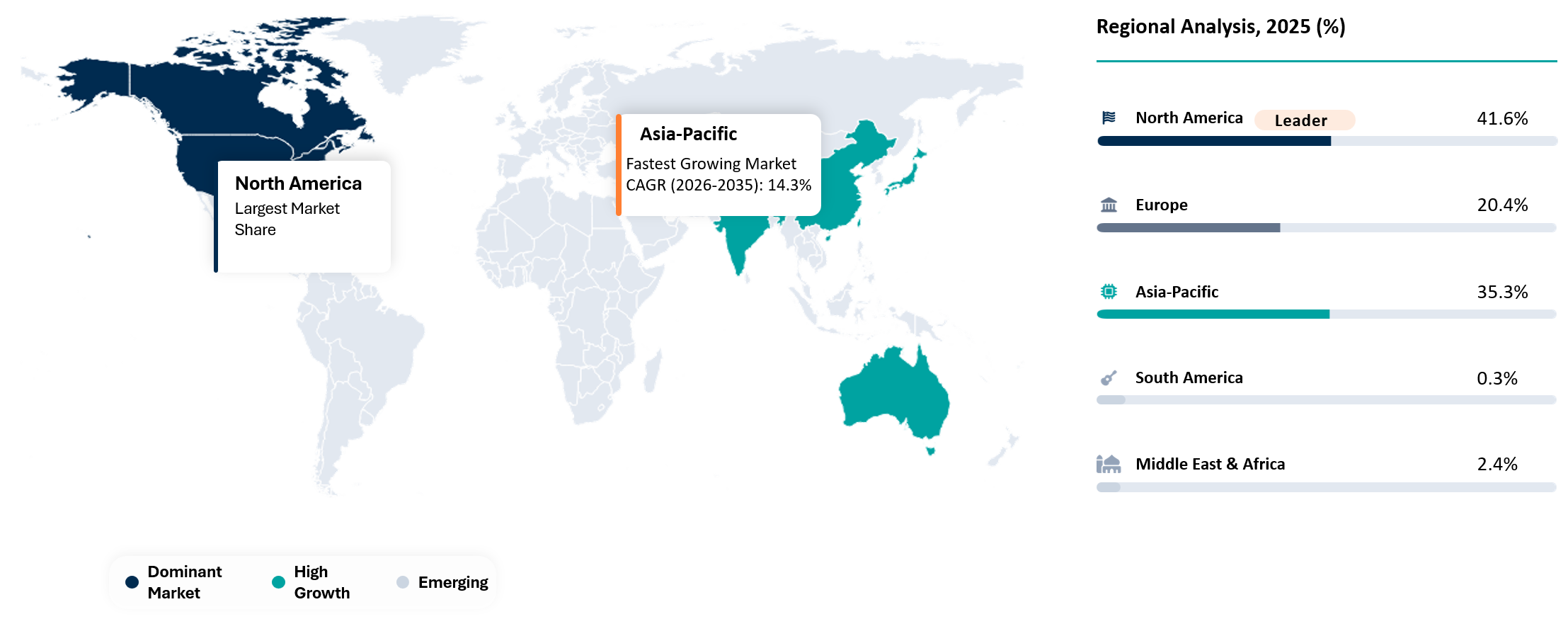

North America remains the largest market because cybersecurity budgets, cloud adoption and advanced enterprise security programs are mature. Asia-Pacific is the fastest-growing region as India, China, Japan, South Korea, Australia and Southeast Asia invest in cloud networks, telecom modernization, secure access and industrial cybersecurity. Supplier differentiation will depend on hybrid deployment support, unified policy, low latency, encrypted traffic visibility, cloud points of presence, AI-assisted firewall operations and predictable pricing.

Network Security Market Scope

| Metrics | Details | |

| Market Size in 2025 | US$ 38.80 Billion | |

| Market Size by 2035 | US$ 121.16 Billion | |

| CAGR During 2026 to 2035 | 13.5% | |

| Largest Region in 2025 | North America, 41.6% market share in 2025 | |

| Fastest Growing Region | Asia-Pacific, 14.3% CAGR between 2026 and 2035 | |

| Key Regional Shift | Asia-Pacific is expected to increase from 35.3% market share in 2025 to 37.6% market share by 2035 | |

| Leading Solution Type | NGFW (Next-Generation Firewall) | |

| Fastest Growing Solution Type | SASE (Secure Access Service Edge) | |

| Leading Network Type | Enterprise Network | |

| Fastest Growing Network Type | Cloud Network | |

| Market Maturity | Growth Stage | |

| Key Buying Question | Which platform can secure users, branches, cloud workloads and data centers with consistent policy? | |

| By Component | Solution, Services | |

| By Solution Type | Firewall, NGFW, IDS, IPS, Secure Web Gateway, VPN, ZTNA, SASE, SSE, NDR, DDoS Protection, NAC, Network Sandbox, DNS Security, SD-WAN Security, Others | |

| By Deployment Mode | Cloud, On Premises, Hybrid | |

| By Network Type | Enterprise Network, Cloud Network, Data Center Network, Industrial Network, Telecom Network, Branch Network, Remote Access Network, Others | |

| By End-User | BFSI, IT and Telecom, Government and Public Sector, Healthcare and Life Sciences, Manufacturing, Energy and Utilities, Retail and E-Commerce, Education, Transportation and Logistics, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Key Takeaways

- North America remained the largest regional market with 41.6% market share in 2025, supported by strong enterprise spending on NGFW, SASE, SSE, DDoS protection and secure access modernization.

- Asia-Pacific is the fastest-growing region with 14.3% CAGR between 2026 and 2035 and is expected to increase from 35.3% market share in 2025 to 37.6% market share by 2035.

- Europe represented a high-value market with 20.4% market share in 2025, supported by cyber resilience regulations, critical infrastructure protection and secure access upgrades across regulated industries.

- NGFW remains the leading solution type because firewalls continue to anchor traffic inspection, segmentation, threat prevention and secure branch connectivity across hybrid environments.

- SASE is expected to be the fastest-growing solution area as enterprises move security inspection closer to users, SaaS applications and cloud workloads.

- Enterprise network remains the leading network type because large organizations still need consistent security across branches, data centers, cloud, remote users and partner access.

- Supplier differentiation is moving toward unified policy, low latency, global cloud coverage, AI-assisted network analysis, OT visibility, DDoS resilience and hybrid deployment support.

Why Does This Report Matter In 2026?

Network security matters in 2026 because enterprise traffic no longer follows the old data-center route. Employees connect from offices, homes, mobile devices and branch locations. Applications run across SaaS, private data centers and public cloud. Traditional perimeter tools cannot protect every traffic path without creating blind spots or poor user experience.

SASE, SSE and ZTNA are becoming strategic because they match the way users now access applications. VPN replacement is a major priority for many enterprises because broad network access creates unnecessary exposure. Buyers want identity-aware access, cloud-delivered inspection, secure web gateways and data protection that works consistently across distributed environments.

The network security market is also becoming more operationally complex. Firewalls still matter, but buyers also need cloud firewalls, NDR, DDoS protection, NAC, DNS security and secure SD-WAN. Procurement teams are evaluating performance, latency, bandwidth pricing, policy consistency, migration risk and managed service support. A strong market study must therefore assess architecture change rather than only firewall appliance demand.

Strategic Indicators For Network Security

High Regulation Impact

Network security is strongly influenced by cyber resilience, data protection, critical infrastructure and sector-specific compliance rules. BFSI, healthcare, government, telecom, manufacturing and energy organizations require segmentation, access control, secure remote access, threat detection and audit-ready logs. Network security platforms help demonstrate control over traffic, users, workloads and sensitive systems.

Critical infrastructure rules are becoming more important. Utilities, transport systems, hospitals and public agencies must protect operational networks and service continuity. Network segmentation, intrusion prevention, remote access control and monitoring are key compliance tools. Buyers in these sectors prefer vendors with proven enterprise deployments, security certifications and strong support.

Data protection laws also influence secure access architecture. Enterprises need to limit who can reach applications and sensitive data. ZTNA, SSE and identity-aware policy help reduce excessive network access. Network security is therefore linked with privacy, compliance and business continuity.

High Investment Activity

Investment is concentrated in NGFW, SASE, SSE, ZTNA, cloud firewalls, NDR, secure SD-WAN, DDoS mitigation and OT network security. Firewall vendors are expanding into cloud-delivered security, while cloud-native vendors are expanding into enterprise access and traffic inspection. Platform convergence is one of the strongest investment themes.

DDoS protection is receiving stronger investment because digital services, e-commerce, banking and public platforms must remain available during attacks. Network downtime directly affects revenue and customer trust. Buyers increasingly view DDoS mitigation as part of core resilience planning rather than an optional service.

NDR and OT security are also attracting investment. Many industrial and healthcare devices cannot run endpoint agents. Passive traffic monitoring gives security teams’ visibility without disrupting operations. Demand will grow where uptime and legacy device compatibility matter.

Supply Chain Disruption

Network security supply-chain risk includes hardware appliance lead times, silicon availability, cloud service reliability, software update quality and global point-of-presence availability. Firewall refresh projects can be delayed when hardware supply is constrained. Cloud-delivered security creates a different dependency because user access can be affected if vendor infrastructure has outages.

Hybrid environments increase complexity. Enterprises may depend on physical firewalls, virtual firewalls, cloud points of presence, secure web gateways and identity integrations at the same time. A failure in any layer can affect connectivity or inspection. Buyers increasingly review vendor resilience, service-level commitments and global support before selecting platforms.

Security update reliability is also critical. Firewalls and gateways sit at key control points. A faulty update can disrupt traffic or weaken protection. Procurement teams prefer vendors with staged update controls, strong support and clear mitigation guidance during vulnerabilities.

Pricing Volatility

Network security pricing is moving from appliance-heavy capital spending toward recurring subscriptions based on users, bandwidth, cloud inspection, threat prevention modules, DDoS capacity and managed services. Cloud-delivered security can reduce appliance dependence, but high traffic volumes can increase operating expense.

SASE and SSE pricing is especially sensitive to bandwidth and user count. Global enterprises need predictable cost across regions and traffic patterns. Buyers are asking more questions about inspection limits, data retention, advanced modules and overage charges. Transparent pricing is becoming a competitive advantage.

Hardware-led pricing remains important in data centers, industrial networks and branch environments. High-performance firewalls, ruggedized devices and cloud firewalls all carry different cost models. Procurement teams need total cost comparisons across appliance refresh, cloud subscription, bandwidth, support and operations staffing.

Procurement Pressure

Network buyers are under pressure to modernize without breaking connectivity. Firewall replacement, VPN migration, branch redesign and cloud security deployment can affect business uptime. A poorly executed change can stop employees from accessing applications or disrupt customer-facing services. Migration support is therefore a major buying factor.

Latency is another procurement concern. Cloud-delivered inspection must protect users without slowing applications. Global coverage, routing efficiency and point-of-presence density matter. Buyers in financial services, healthcare, manufacturing and technology often require proof-of-performance testing before rollout.

Policy consistency is also important. Large enterprises operate many locations, cloud environments and user groups. Security teams want consistent policies across physical firewalls, virtual firewalls, cloud firewalls, SASE and remote access. Vendors that simplify policy management can reduce misconfiguration risk.

New Technology Adoption

Technology adoption is strongest in SASE, SSE, ZTNA, cloud firewalls, AI-assisted firewall management, NDR analytics, encrypted traffic visibility and software-defined segmentation. Cloud-delivered secure access is replacing older VPN models where users only need application access rather than full network access.

AI is gaining practical use in network operations. Firewall rules, segmentation policies and traffic alerts can become difficult to manage. AI-assisted tools can help identify misconfigurations, summarize incidents and recommend policy changes. Buyers will adopt these features when recommendations are explainable and auditable.

Encrypted traffic inspection is evolving. More traffic is encrypted, which reduces visibility. Vendors are developing approaches to identify threats while balancing privacy, performance and decryption cost. Enterprises need strategies that match regulatory obligations and user experience requirements.

Regional Expansion Opportunity

North America remains the largest network security market because enterprise cloud adoption, cybersecurity spending and digital service exposure are mature. The U.S. is the strongest country market due to large BFSI, technology, healthcare, retail and government demand. Canada and Mexico continue to expand through regulated industry and manufacturing security needs.

Asia-Pacific is the fastest-growing region. India, China, Japan, South Korea, Australia and Southeast Asia are investing in telecom modernization, cloud networks, smart manufacturing, digital banking and public-sector security. Secure access and cloud firewall demand will grow quickly as applications move away from traditional data centers.

Europe remains a premium market with strong regulatory pressure and critical infrastructure protection needs. Buyers in Germany, UK, France, Italy, Spain and the Nordics evaluate network security through compliance, resilience, data handling and supplier trust. Growth is steady but slower than Asia-Pacific because the region is more mature.

Government Policy Support

Government policy supports network security through critical infrastructure programs, public-sector cyber modernization, telecom resilience initiatives and zero trust adoption guidance. Agencies need secure access, segmentation, remote work protection and DDoS resilience. Public-sector demand often influences private sector benchmarks.

Telecom and digital infrastructure investments also support network security spending. 5G, cloud services and national digital platforms require stronger network protection. Secure traffic routing, application access control and network monitoring become essential as public services digitize.

Industrial policy can support OT network security. Manufacturing, energy, transport and water infrastructure need segmentation and passive monitoring. Governments are pushing operators to improve resilience against cyber disruption. Network security vendors with OT-ready offerings will benefit.

AI Impact Analysis

AI is improving network security through traffic anomaly detection, incident summarization, policy optimization, firewall rule analysis and faster response workflows. Enterprise networks generate large volumes of logs, flows, DNS activity and access events. AI can help identify unusual communication patterns and prioritize alerts that matter.

Firewall management is a strong AI use case. Rule bases often become complex over years of changes. Misconfigurations can create exposure or disrupt traffic. AI-assisted policy analysis can identify redundant rules, risky access and conflicts, which reduces human error and helps security teams maintain cleaner policy.

NDR also benefits from AI because it relies on behavioral analysis. Lateral movement, command-and-control traffic, unusual protocol use and data exfiltration may not match static signatures. AI can detect deviations from normal traffic patterns and support faster investigation.

AI must remain governed. Automated blocking or policy changes can disrupt business operations. Buyers will favor AI that explains findings, provides recommended actions and allows human approval for high-impact changes. Trust and auditability will decide adoption speed.

Disruption Analysis

SASE and SSE are disrupting the old perimeter model. Remote users and SaaS applications do not fit a data-center backhaul architecture. Cloud-delivered security inspection allows organizations to protect users closer to applications while reducing reliance on legacy VPN. The shift affects firewall refresh cycles and branch network designs.

ZTNA is disrupting VPN access. Legacy VPN often gives users broad network access after authentication. ZTNA limits access to specific applications based on identity, device posture and risk. Enterprises are adopting ZTNA to reduce lateral movement exposure and improve user access control.

NDR is disrupting endpoint-only monitoring in environments with unmanaged devices. OT networks, IoT environments, healthcare devices and industrial systems often cannot run endpoint agents. Passive network monitoring provides visibility without interfering with operations, making NDR a strong complement to endpoint and firewall controls.

Cloud firewalls are changing data center security strategies. Workloads move across public cloud, private cloud and containers. Security teams need policy consistency across physical, virtual and cloud environments. Vendors that provide unified management across these environments can capture platform demand.

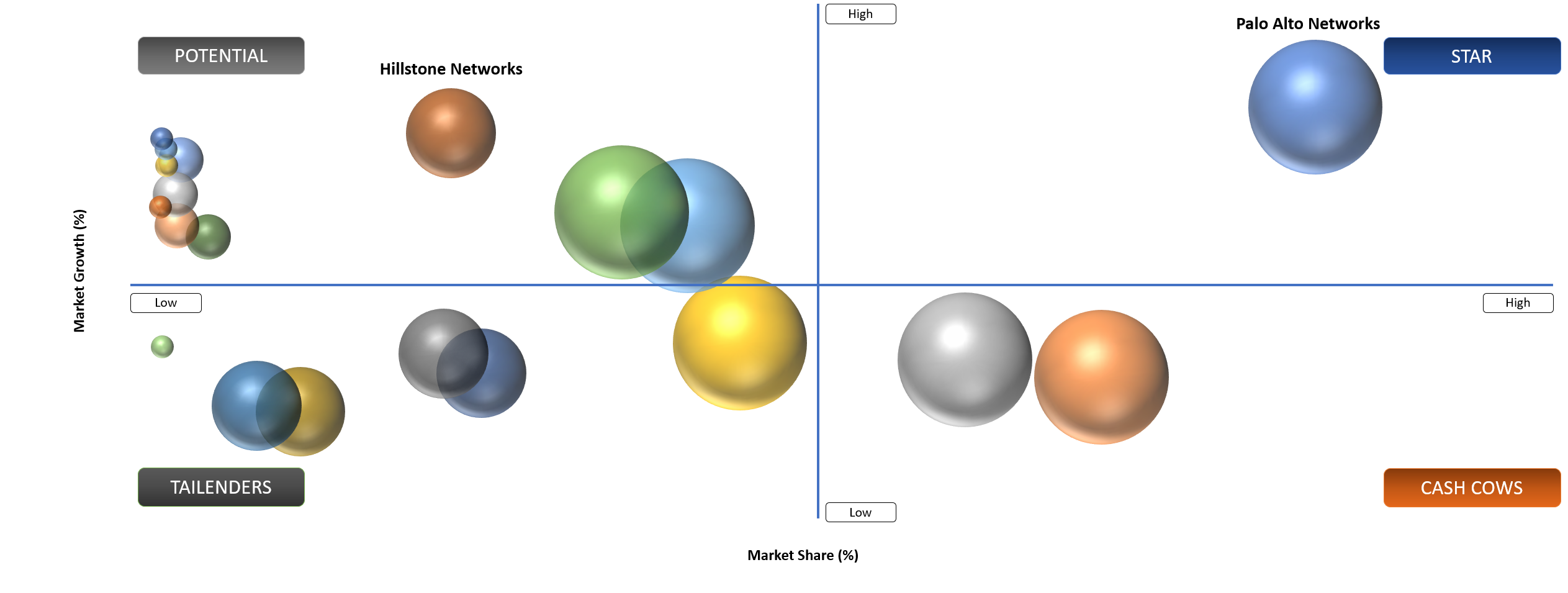

BCG Matrix: Company Evaluation

Star

Star players include Palo Alto Networks, Inc., Fortinet, Inc., Cisco Systems, Inc., Check Point Software Technologies Ltd., Zscaler, Inc., Cloudflare, Inc., Netskope, Inc., Akamai Technologies, Inc. and F5, Inc. The companies have strong enterprise visibility, broad platform capabilities and meaningful exposure across firewall, SASE, SSE, DDoS protection, cloud network security and secure access.

Potential

Potential companies include Hillstone Networks Co., Ltd., SonicWall Inc. and WatchGuard Technologies, Inc. Hillstone can grow through cost-competitive enterprise firewall and network detection offerings in selected regions. SonicWall can gain share among SMEs and distributed organizations through firewall refresh and secure access products. WatchGuard can expand through channel-led network security bundles for SMEs that need simpler deployment and predictable cost.

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact | Demand Concentration | Impacted Use Case | Strategic Impact |

Hybrid Cloud Traffic Forces Network Security Redesign | High | Global Enterprises | SASE, SSE and Cloud Firewalls | Drives architecture modernization |

ZTNA Replaces Legacy VPN Access | High | Remote Workforce | Secure Application Access | Reduces broad network exposure |

DDoS Risk Increases Digital Service Resilience Spending | Medium To High | BFSI, E-Commerce and Telecom | DDoS Protection | Supports always-on digital service protection |

OT and IoT Networks Need Agentless Visibility | Medium | Manufacturing and Healthcare | NDR and NAC | Expands passive monitoring demand |

Hybrid Cloud Traffic Forces Network Security Redesign

Hybrid cloud has changed how enterprise traffic moves. Employees access SaaS applications directly, workloads run in public and private clouds and branches need secure connectivity without routing all traffic through a central data center. Old perimeter models cannot secure this pattern efficiently. Network security buyers now need cloud-delivered inspection, application-level access and consistent policy.

SASE and SSE adoption is expanding because enterprises want secure access closer to users and applications. Secure web gateway, cloud access controls, ZTNA and data protection can reduce backhaul and improve user experience. Buyers want security that follows users rather than security tied only to corporate locations.

Cloud network security is also becoming essential. Workloads move across AWS, Microsoft Azure, Google Cloud and private environments. Security teams need visibility and policy control across these environments. Cloud firewalls and virtual firewalls are growing because traditional appliances cannot protect every workload path.

Hybrid network redesign creates opportunity for vendors that can simplify management. Enterprises do not want separate policy models for branch firewalls, cloud firewalls, remote users and data centers. Vendors with unified management and consistent policy enforcement can capture larger platform deals.

Restraint Impact Analysis

| Restraint | Drag On Market Growth | Primary Impact Area | Impacted Use Case | Strategic Impact |

Appliance Refresh Cycles Slow Cloud Security Migration | High | Large Enterprises | Firewall and SASE Migration | Extends hybrid deployment periods |

Bandwidth-Based SASE Pricing Creates Budget Pressure | Medium To High | Cloud Inspection | Remote Access and SaaS Traffic | Raises total cost scrutiny |

Encrypted Traffic Inspection Increases Latency Risk | Medium | User Experience | Secure Web Gateway | Requires careful performance design |

Firewall Rule Sprawl Creates Misconfiguration Exposure | Medium | Security Operations | Segmentation and Access Control | Drives policy automation demand |

Appliance Refresh Cycles Slow Cloud Security Migration

Many enterprises still depend on firewall appliances, VPN concentrators, branch routers and data center security hardware. Replacement cycles can take years because security controls are deeply tied to routing, uptime and compliance. Even when SASE or cloud firewalls offer strong value, migration must be staged carefully.

Bandwidth-based pricing can restrain cloud security adoption. Enterprises with heavy SaaS, collaboration and data traffic may face higher costs than expected if inspection volume grows. Buyers need transparent pricing and traffic modelling before moving large user populations to cloud-delivered security.

Latency concerns also matter. Security inspection must not slow business applications. Poor user experience can create resistance from employees and business units. Vendors with strong global cloud infrastructure and optimized routing will have an advantage.

Firewall rule sprawl remains a major operational burden. Large organizations often have years of accumulated rules, exceptions and outdated access paths. Cleaning this up takes time and carries business risk. Network security modernization therefore requires governance, not only technology replacement.

Segmentation Analysis

NGFW Will Remain The Core Enterprise Network Security Control

NGFW remains the largest solution because enterprises still need traffic inspection, application control, intrusion prevention, segmentation and secure branch connectivity. Firewalls continue to sit at important control points in data centers, campuses, branches, cloud environments and industrial networks. Even as SASE grows, NGFW remains a foundation layer.

Data centers and high-throughput environments require predictable inspection performance. Physical and virtual firewalls support workloads that cannot rely only on cloud-delivered security. Advanced threat prevention, application visibility, identity integration and encrypted traffic handling remain central buyer requirements.

Branch networks also depend on NGFW. Distributed offices need local security, SD-WAN integration, web filtering and secure connectivity. Fortinet and Cisco have strong relevance in this area because security and networking convergence is a practical branch requirement.

Cloud NGFW is extending the category. Public cloud workloads need firewall controls that work inside cloud-native environments. Buyers want consistent policies across on-premises and cloud networks. Vendors that provide unified management across physical, virtual and cloud firewalls will maintain leadership.

SASE Is Reshaping Secure Remote Access

SASE is one of the fastest-growing solution areas because users and applications are distributed. Enterprises want secure web gateway, cloud access security, ZTNA and data protection delivered through cloud points of presence. The architecture can reduce backhaul and simplify remote access.

SASE adoption is strongest among companies with distributed workforces, branch networks and heavy SaaS use. Employees need secure and fast access from many locations. Legacy VPN can create broad network exposure and poor user experience. ZTNA and SSE improve control by granting application-specific access.

Competition is intense because firewall vendors, secure web gateway specialists, cloud networking companies and zero trust vendors are all pursuing the same budget. Buyers evaluate latency, global coverage, identity integration, data protection, policy management and migration support.

SASE will not eliminate all appliances. Many organizations will run hybrid models for years, especially where data centers, OT networks or high-throughput traffic remain important. Vendors that support hybrid migration will capture more realistic enterprise demand.

NDR Is Gaining Importance In Agentless Environments

NDR is gaining attention because many devices cannot run endpoint agents. OT equipment, medical devices, IoT sensors, printers, cameras and legacy systems often remain invisible to endpoint tools. Network traffic analysis helps detect suspicious communication without installing software on every device.

Manufacturing and healthcare are strong use cases. Production equipment and clinical devices require uptime and may not support modern endpoint agents. Passive monitoring can identify lateral movement, unusual protocols, unauthorized connections and command-and-control traffic without disrupting operations.

NDR also supports cloud and data center security. East-west traffic can reveal movement between workloads after initial compromise. Security teams need visibility into internal traffic, not only north-south perimeter flows. NDR helps identify behavior that firewalls may not block.

Integration determines value. NDR alerts must feed into SIEM, SOAR, XDR and incident response workflows. A separate dashboard can increase alert fatigue. Vendors that integrate network detections with endpoint and identity signals will gain stronger adoption.

DDoS Protection Is Moving Into Core Digital Resilience

DDoS protection is becoming a core resilience requirement as organizations rely on digital services for banking, e-commerce, healthcare, public services, gaming and telecom operations. Attackers can use volumetric floods, application-layer attacks and bot traffic to disrupt customer access. Availability is now part of security.

BFSI, telecom, cloud providers and e-commerce companies are leading buyers. Downtime can directly affect revenue and trust. DDoS mitigation must handle high-volume attacks while preserving legitimate traffic. Buyers evaluate scrubbing capacity, global network reach, automation and response support.

DDoS protection also matters for public sector and healthcare. Service disruption can affect citizens and patients. Organizations increasingly include DDoS protection in broader cyber resilience planning. Network security vendors with integrated DDoS and application protection can capture larger budgets.

Pricing and service quality are key decision factors. Buyers need clarity on attack capacity, always-on protection, on-demand mitigation and service-level commitments. Weak DDoS protection can become visible very quickly during a real attack.

Market Segmentation

- By Component

- Solution

- Services

- By Solution Type

- Firewall

- NGFW (Next-Generation Firewall)

- IDS (Intrusion Detection System)

- IPS (Intrusion Prevention System)

- Secure Web Gateway

- VPN (Virtual Private Network)

- ZTNA (Zero Trust Network Access)

- SASE (Secure Access Service Edge)

- SSE (Security Service Edge)

- NDR (Network Detection and Response)

- DDoS Protection

- NAC (Network Access Control)

- Network Sandbox

- DNS Security

- SD-WAN Security

- Others

- By Deployment Mode

- Cloud

- On Premises

- Hybrid

- By Network Type

- Enterprise Network

- Cloud Network

- Data Center Network

- Industrial Network

- Telecom Network

- Branch Network

- Remote Access Network

- Others

- By End-User

- BFSI

- IT and Telecom

- Government and Public Sector

- Healthcare and Life Sciences

- Manufacturing

- Energy and Utilities

- Retail and E-Commerce

- Education

- Transportation and Logistics

- Others

Geographical Penetration

North America Network Security Market Trends

North America led the network security market with 41.6% market share in 2025 and is expected to retain 41.6% market share by 2035. The region has mature enterprise cybersecurity budgets, strong cloud adoption and high exposure to ransomware, DDoS attacks and data breach risk. Buyers are actively modernizing NGFW, SASE, DDoS protection and NDR deployments.

The U.S. is the strongest country market. BFSI, healthcare, technology, government, retail and cloud service providers invest heavily in network security. Enterprises are replacing VPN access with ZTNA, expanding secure web gateway coverage and adopting cloud firewalls for multi-cloud workloads. Network security is tied directly to business continuity and customer trust.

Canada is a high-value market for regulated industries, public sector and financial services. Buyers prioritize compliance, supplier trust and secure remote access. Managed security service providers play an important role for mid-sized organizations.

Mexico is expanding through manufacturing, logistics, retail and financial services digitization. Secure branch networks, industrial cybersecurity and managed firewall services are important growth areas. Vendors with strong channel partners and cost-effective bundles can gain share.

Asia-Pacific Network Security Market Outlook

Asia-Pacific is the fastest-growing region with 14.3% CAGR between 2026 and 2035. The region is expected to increase from 35.3% market share in 2025 to 37.6% market share by 2035. Growth is driven by cloud adoption, telecom modernization, digital government, manufacturing digitization and secure access demand.

China has large demand across telecom, cloud infrastructure, financial services, manufacturing and public sector. Domestic vendors and global players compete in a market shaped by localization and data rules. Network security spending is high because enterprise and public infrastructure digitization require stronger traffic control.

India is growing quickly because banks, IT services firms, telecom operators, government agencies and digital platforms are investing in secure access and cloud security. SASE, firewalls, DDoS protection and managed network security are gaining demand. Price sensitivity remains important, but security maturity is rising.

Japan and South Korea remain premium markets. Buyers prioritize reliability, low latency, documentation and long-term vendor trust. Manufacturing, finance, telecom and government sectors are key demand centers. Cloud migration and OT security will support future growth.

U.S. Network Security Market Landscape

The U.S. is the largest country market because enterprises run complex distributed networks across branches, cloud, remote users and data centers. Security teams need NGFW, SASE, DDoS protection, ZTNA, NDR and cloud firewalls that work together. Platform consolidation is a major buying theme.

Financial services buyers prioritize resilience, data protection and strict access control. Healthcare buyers need non-disruptive network visibility and secure remote access. Technology companies need cloud-native security and high-performance data center protection. Government agencies need auditability and segmentation.

DDoS protection is especially important for U.S. digital services. E-commerce platforms, gaming, banking and public services require strong availability. Buyers want automated mitigation, global capacity and clear service-level commitments. U.S. also drives innovation in AI-assisted firewall operations. Enterprises want help managing complex policies and reducing misconfiguration. Vendors that connect AI recommendations with governance and audit trails will gain adoption.

India Network Security Market Trends

India’s network security market is expanding through digital banking, telecom, government digitization, IT services, cloud adoption and manufacturing modernization. Enterprises are shifting from perimeter-only firewalls to SASE, ZTNA and managed network security. Public and private sector buyers both need stronger protection for distributed users and cloud applications.

Banks and fintech companies are major buyers. Digital payments and customer-facing platforms require DDoS resilience, secure access and traffic inspection. Network security must support uptime and regulatory readiness. Vendors with local support and integration partners have an advantage.

IT services companies need global network security because employees and customer projects operate across regions. Secure remote access, cloud network protection and endpoint integration are important. SASE adoption will increase as large service providers modernize access architectures. Manufacturing and infrastructure sectors create demand for industrial network visibility. OT environments need segmentation and passive monitoring. NDR and ruggedized network security can gain traction as production networks become more connected.

Japan Network Security Market Growth Outlook

Japan is a high-value market where reliability, documentation and vendor trust shape buying decisions. Enterprises do not want network security changes that create downtime or user friction. Migration planning and support quality are therefore critical.

Manufacturing is a major demand base. Connected factories, engineering systems and supplier networks create exposure. Network segmentation and passive monitoring are important because production environments cannot tolerate disruption. Vendors with OT-ready offerings will gain stronger acceptance.

Financial services and public sector buyers prioritize compliance, resilience and secure access. Cloud adoption is increasing, but buyers often move carefully. Hybrid network security architectures will remain common because legacy systems and on-premises data centers continue to matter.

Japan’s demand for AI-assisted network security will grow, but adoption will depend on explainability. Security teams will use AI for policy analysis and alert prioritization when recommendations are auditable. Vendors that combine AI with strong governance will be better positioned.

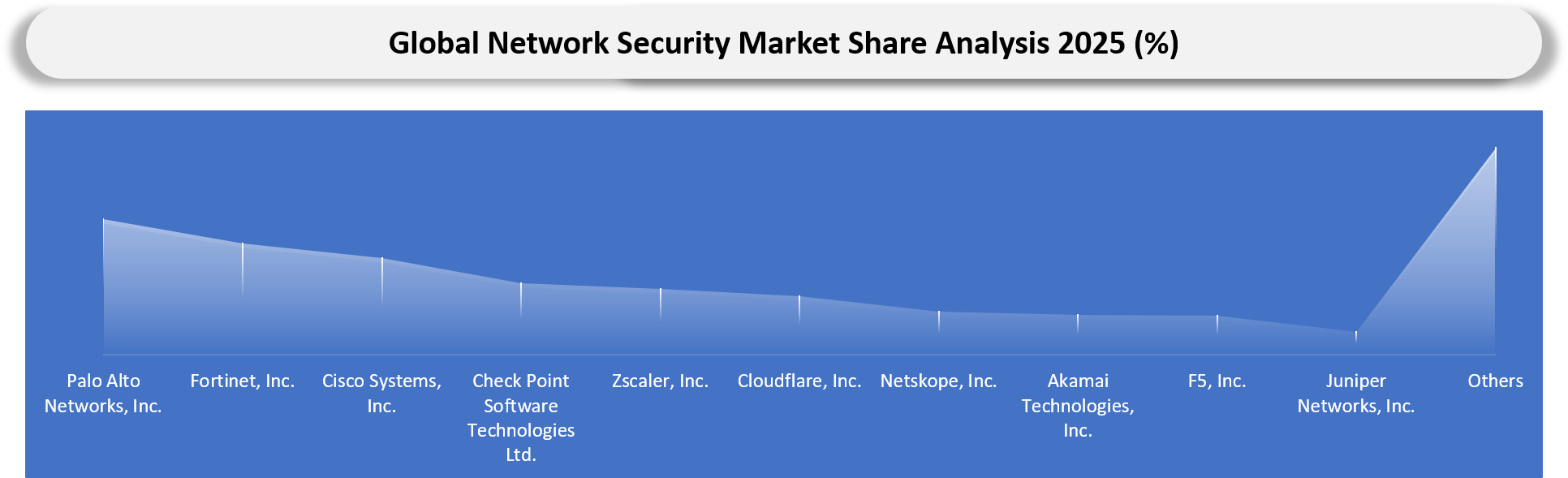

Competitive Landscape

- Competition is split between firewall leaders, cloud-delivered security vendors, SASE and SSE specialists, DDoS providers, NDR companies, OT security vendors and network infrastructure companies. Palo Alto Networks, Fortinet, Cisco and Check Point remain strong in firewall-led network security, while Zscaler, Cloudflare and Netskope compete strongly in cloud-delivered secure access.

- Palo Alto Networks competes through AI-driven network security, NGFW, Prisma SASE, Cloud NGFW and platform consolidation. Fortinet competes through FortiGate, secure SD-WAN, purpose-built security processors and security-networking convergence. Cisco competes through its installed network base, firewall portfolio, Talos threat intelligence and hybrid mesh firewall strategy.

- Cloud-native vendors compete by reducing backhaul and improving user access to SaaS and private applications. Zscaler, Cloudflare and Netskope are relevant where enterprises prioritize SASE, SSE and zero trust access. Their strength depends on global cloud coverage, low latency, data protection and integration with identity providers.

- DDoS and application security providers such as Akamai, Cloudflare and F5 compete where availability and public-facing digital services matter. Their value increases in e-commerce, financial services, gaming, telecom and public-sector digital platforms.

- NDR and OT-focused players compete by solving visibility gaps in unmanaged device environments. Manufacturing, healthcare and utilities need passive monitoring and segmentation. Vendors that integrate NDR with broader security operations can gain share.

- Competitive benchmarking should track throughput, latency, policy consistency, cloud coverage, SASE maturity, DDoS capacity, OT visibility, AI-assisted operations, migration support and pricing transparency.

Key Companies

- Palo Alto Networks, Inc.

- Fortinet, Inc.

- Cisco Systems, Inc.

- Check Point Software Technologies Ltd.

- Zscaler, Inc.

- Cloudflare, Inc.

- Netskope, Inc.

- Akamai Technologies, Inc.

- F5, Inc.

- Juniper Networks, Inc.

- HPE Aruba Networking

- Broadcom Inc.

- Trellix

- Trend Micro Incorporated

- SonicWall Inc.

- WatchGuard Technologies, Inc.

- Forcepoint LLC

- Hillstone Networks Co., Ltd.

- Huawei Technologies Co., Ltd.

- Arista Networks, Inc.

Company Coverage Preview

Palo Alto Networks, Inc. is a leading network security company with NGFW, Prisma SASE, Cloud NGFW, Cortex and Unit 42 capabilities. Its strength lies in AI-driven network security, cloud security integration, zero trust positioning and enterprise platform consolidation. Palo Alto Networks is especially strong among large enterprises that want consistent policy across branch, campus, data center and public cloud.

Fortinet, Inc. competes strongly through FortiGate NGFW, Fortinet Security Fabric, secure SD-WAN, ZTNA, SASE and AI-powered security services. Fortinet’s advantage comes from appliance performance, purpose-built security processors, wide product breadth and branch network penetration. Its offering is relevant for enterprises that want security and networking convergence.

Cisco Systems, Inc. remains important because of its large enterprise networking base and Cisco Secure Firewall portfolio. Cisco’s advantage comes from installed network relationships, Talos threat intelligence, encrypted traffic visibility, hybrid mesh firewall positioning and integration with broader security and networking tools. Cisco remains a strong contender where buyers value network infrastructure continuity.

Zscaler, Cloudflare, Netskope, Check Point, Akamai, F5, Juniper, HPE Aruba, SonicWall and WatchGuard compete across cloud-delivered security, secure web gateway, DDoS protection, firewall appliances, NAC and branch security. Competitive positioning increasingly depends on whether vendors can protect distributed users, cloud applications and hybrid networks with lower operational burden.

Major Pain Points

- VPN migration is complex when applications have inconsistent access requirements.

- SASE pricing can rise with bandwidth, user count and advanced modules.

- Encrypted traffic limits visibility unless inspection is carefully designed.

- Firewall rule sprawl creates misconfiguration risk.

- Branch migration can disrupt connectivity if planning is weak.

- OT and IoT devices often cannot run endpoint agents.

- DDoS attacks can create immediate business and reputational damage.

- Cloud network traffic is difficult to monitor consistently across providers.

- Hybrid deployments require multiple policy models if vendor integration is weak.

- Skilled network security engineers remain difficult to hire and retain.

Recent Developments in Network Secuirty Market

- January 2026: Palo Alto Networks completed its Chronosphere acquisition, strengthening observability and security convergence for cloud and AI-era environments.

- January 2026: Palo Alto Networks patched a PAN-OS vulnerability affecting GlobalProtect Gateway and Portal configurations, reinforcing the importance of rapid update discipline in network edge products.

- March 2026: Fortinet issued patches after reported exploitation of FortiGate vulnerabilities, reinforcing buyer focus on firewall update management, credential rotation and network edge hardening.

- April 2026: Palo Alto Networks announced an agreement to acquire Portkey, expanding security coverage for AI agents and AI application traffic.

- July 2025: Palo Alto Networks announced a US$ 25 billion agreement to acquire CyberArk, strengthening identity security as part of its broader cybersecurity platform strategy.

Analyst View and Opinion

- Network security will remain a strategic platform market because enterprise traffic is distributed across remote users, branches, data centers, SaaS and public cloud.

- NGFW will remain the largest solution area because firewalls still anchor segmentation, traffic inspection and threat prevention across hybrid environments.

- SASE will grow fastest as enterprises move secure access and web inspection closer to users and applications.

- ZTNA will continue replacing broad VPN access where application-level access is practical and identity integration is mature.

- NDR will gain share in OT, healthcare and IoT-heavy environments where endpoint agents cannot be installed.

- DDoS protection will become a core digital resilience requirement for financial services, e-commerce, telecom and public platforms.

- Cloud firewalls will grow as workloads move across public and private cloud environments.

- AI-assisted firewall and policy management will reduce misconfiguration risk, but buyers will demand explainable recommendations and governance.

- Platform consolidation will intensify, but point solutions can still win where they solve latency, DDoS, OT visibility or cloud-specific problems better than broad suites.

- Asia-Pacific will be the strongest growth engine as cloud networks, telecom infrastructure, smart manufacturing, and public-sector digitization expand.

Target Audience

| Industry | Who Should Buy This Report? | Reason To Buy This Report |

| BFSI | CISOs, Network Security Leaders, Risk Teams | Evaluate secure access, DDoS resilience, segmentation and compliance requirements |

| IT and Telecom | Network Architects, Cloud Security Leaders | Track demand for SASE, NGFW, cloud firewalls and DDoS protection |

| Government and Public Sector | Digital Infrastructure Leaders, Cybersecurity Teams | Assess secure access, public-service resilience and critical infrastructure protection |

| Healthcare and Life Sciences | IT Security Teams, Compliance Teams | Understand non-disruptive network monitoring and secure remote access needs |

| Manufacturing | OT Security Leaders, Plant IT Teams | Evaluate segmentation, NDR and industrial network security requirements |

| Retail and E-Commerce | Digital Operations Teams, Security Teams | Assess DDoS protection, secure branches and customer-facing service resilience |

| Investors | Cybersecurity Investors, Technology Funds | Identify platform consolidation and high-growth network security categories |

| Consulting Firms | Cybersecurity Advisory Teams | Support architecture modernization, vendor selection and migration planning |

What DataM Uniquely Provides

- DataM maps network security demand across solution type, deployment mode, network type, End-User and region.

- DataM benchmarks vendors across NGFW, SASE, SSE, ZTNA, NDR, DDoS protection, NAC and cloud firewalls.

- DataM evaluates pricing pressure across appliances, subscriptions, bandwidth, threat modules, DDoS capacity and managed services.

- DataM links network security adoption with hybrid cloud, remote work, OT visibility, DDoS resilience and VPN replacement.

- DataM provides procurement guidance covering latency, migration risk, policy consistency, global coverage, service quality and pricing transparency.

- DataM helps buyers compare firewall-led platforms, cloud-delivered security vendors, and specialized NDR or DDoS providers.

- DataM supports regional opportunity analysis across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa.

- DataM includes trade intelligence indicators for network-connected hardware, security appliances and enterprise infrastructure.

Related Reports

Network security is increasingly converging with Zero Trust frameworks, AI-driven threat detection, security analytics, and managed cybersecurity services as organizations modernize their defenses against ransomware, advanced persistent threats (APTs), and AI-powered cyberattacks. Understanding adjacent security markets helps enterprises build comprehensive cybersecurity strategies, improve threat visibility, and strengthen resilience across hybrid and multi-cloud environments. Explore the following related reports for deeper insights into the technologies shaping the future of enterprise security.

Zero Trust Security Market

As organizations move beyond traditional perimeter-based security models, Zero Trust Architecture is becoming a foundational cybersecurity framework. By continuously verifying users, devices, and applications before granting access, Zero Trust helps reduce lateral movement risks and strengthen enterprise security postures.

Managed Security Services Market

The growing complexity of cyber threats and shortage of skilled cybersecurity professionals are driving demand for managed security services. Organizations increasingly rely on MSSPs for continuous monitoring, threat detection, incident response, and compliance management across enterprise environments.

Security Analytics Market

Security analytics solutions leverage artificial intelligence, machine learning, and behavioral monitoring to identify threats, detect anomalies, and improve incident response. These platforms play a critical role in modern security operations centers (SOCs) by helping organizations gain deeper visibility into network activity.

Artificial Intelligence (AI) in Security Market

Artificial intelligence is transforming cybersecurity through automated threat detection, predictive risk analysis, threat intelligence, and security automation. As cyberattacks become more sophisticated, AI-powered security platforms are becoming essential for proactive defense strategies.

Cyber Security Market

The cybersecurity market encompasses a broad range of technologies and services designed to protect networks, applications, endpoints, cloud environments, and critical infrastructure. Growing cyber threats and digital transformation initiatives continue to drive investments in advanced cybersecurity solutions worldwide.