India is moving from capacity catch up to infrastructure scale up

India’s data Center sector has entered a faster build out phase as cloud migration, artificial intelligence, digital public infrastructure and enterprise digitisation combine into a single demand cycle. The country now produces a large share of global data activity, yet its hosted data Center capacity remains far lower than mature markets. This gap is creating one of the strongest digital infrastructure opportunities in Asia.

Key market signals for India data Center sector

| Metric | 2026 baseline or latest value | Market implication |

| Installed data Center capacity | About 1,900 MW in FY26 | India has moved into a faster build out cycle |

| Market size | About USD 1.7 billion in FY26, projected near USD 6.8 billion by FY30 | India can gain share as domestic hosting deepens |

| AI workload requirement | AI workloads may need 400 to 600 MW of incremental capacity by 2027 | GPU density will reshape design, cooling and power systems |

| Edge demand | Edge data Center demand can exceed 200 MW by 2027 to 2028 | 5G, latency sensitive apps and AI inference will push regional deployments |

| Monthly mobile data use | More than 31 GB per user in 2026 | Consumer traffic growth keeps expanding the demand base |

Download the AI Data Centers Market Sample Report

Gain a competitive edge with a comprehensive preview of the AI Data Centers market. Download your free AI Data Centers Market sample report today to access key market insights, detailed segmentation data, and a snapshot of our robust research methodology.

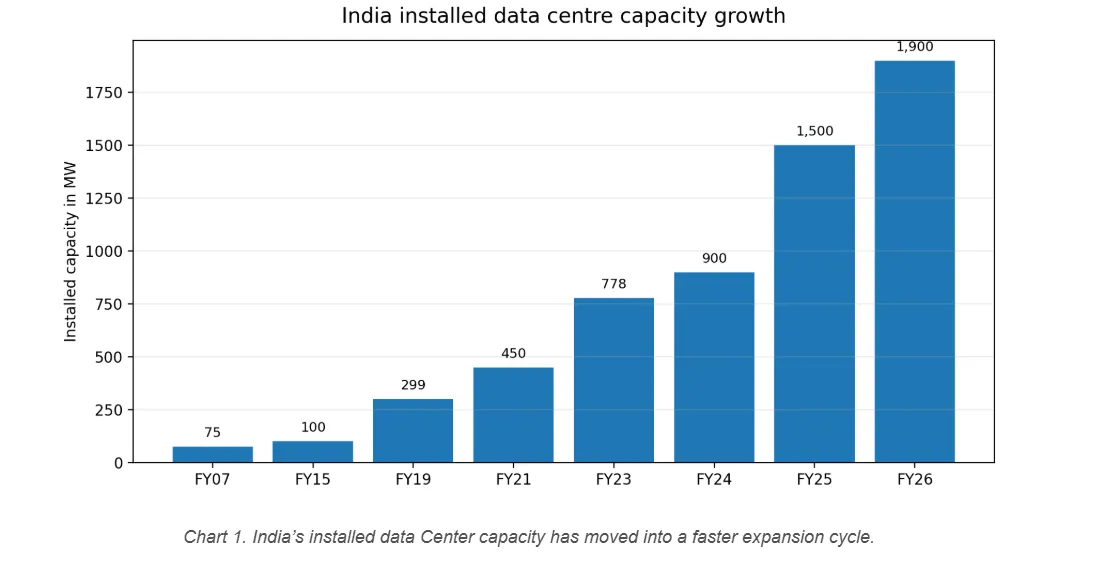

Installed data Center capacity in India has expanded sharply from about 778 MW in FY23 to nearly 1,900 MW in FY26. The sector has moved beyond a colocation led base toward hyperscale campuses, AI ready facilities and high density cloud infrastructure. Mumbai, Chennai, Bengaluru and Delhi NCR remain the main capacity hubs, while Hyderabad, Pune and selected Tier 2 locations are gaining attention because of land availability, power access and state incentives.

Chart 1. India’s installed data Center capacity has moved into a faster expansion cycle.

AI and cloud demand are changing the economics of data Center growth

The next wave of demand is different from the last one because it is more power intensive. Traditional enterprise applications required reliable storage, backup and cloud migration capacity. AI workloads require dense GPU clusters, high bandwidth networks, liquid cooling and stronger power redundancy. This changes the economics of every megawatt added to the market.

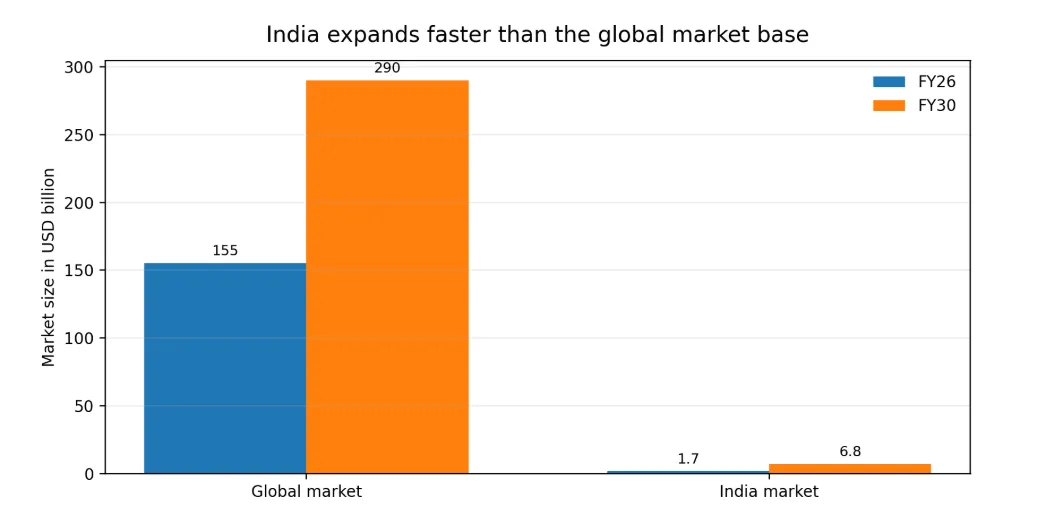

India’s data Center market size is projected to expand from about USD 1.7 billion in FY26 to about USD 6.8 billion by FY30 and to over USD 14.9 billion by FY2035. This implies that India’s share of the global data Center market can move from roughly 2% in 2026 to nearly 5% by FY30 and over 10% by FY2035. The absolute market remains smaller than the major countries in the Americas, Europe and the broader Asia Pacific region, although the growth curve is becoming more attractive because India still has significant under penetration.

Chart 2. India remains a small base market today, although its projected growth is faster than the global average.

AI native facilities are redefining design standards

AI centric data Centers represent a full redesign of conventional facilities. They require heavier floor loading, higher ceiling clearance, denser racks, stronger power distribution and advanced cooling. Rack density is moving from low power enterprise racks toward 30 to 80 kW typical AI racks, with some specialised configurations moving much higher. This creates new requirements for structural design, electrical equipment, chilled water systems, liquid cooling loops and monitoring software.

The shift also changes how operators think about utilisation. In an AI facility, installed capacity is less important than deployable capacity. Power availability, cooling efficiency and network design decide whether a site can support GPU clusters at commercial scale. This is why operators are focusing on facilities that can support direct to chip liquid cooling, immersion cooling, redundant UPS systems, high speed optical connectivity and lower PUE targets.

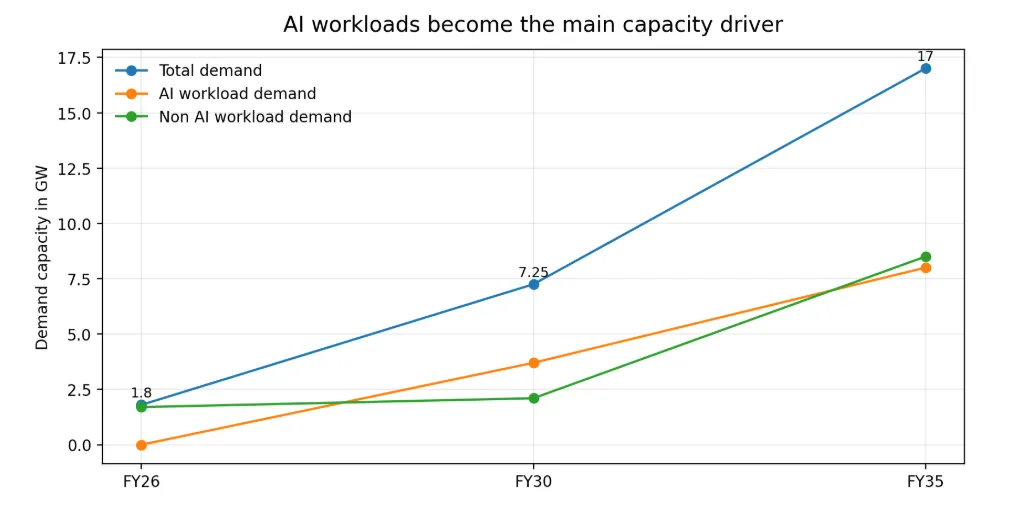

Chart 3. AI workloads are expected to become the largest contributor to future capacity demand.

Power access is becoming the main site selection factor

Power is now the central constraint in the India data Center sector. AI workloads require five to ten times more power intensity than many traditional cloud use cases. That pushes operators to prioritise grid interconnection, renewable energy procurement, on site backup architecture and long term power cost visibility before committing to new campuses.

India has a competitive advantage because power costs in several locations remain lower than many regional markets. The country has also scaled renewable energy capacity, which matters as hyperscalers and colocation operators move toward stronger sustainability commitments. However, the challenge is execution. Grid upgrades, timely approvals and clean power access will decide which states win the next round of data Center investment.

Digital India, 5G and data localisation are widening the demand base

Demand is no longer coming only from large enterprises and cloud providers. India’s digital economy is expanding rapidly due to digital payments, e governance, streaming, ecommerce, software as a service and public digital infrastructure. Government projections indicate that the digital economy could contribute nearly one fifth of national income by 2030, creating a much larger base for data storage and processing demand.

5G is also changing the market. India has crossed 31 GB of average monthly mobile data usage per user, while 5G traffic is growing quickly across the country. Low latency applications, video platforms, online gaming, AI inference and industrial use cases will increase the need for edge data Centers and regional nodes closer to end users. Data localisation rules add another demand layer by encouraging more onshore storage for regulated and personal data.

The supplier ecosystem is entering a localisation opportunity

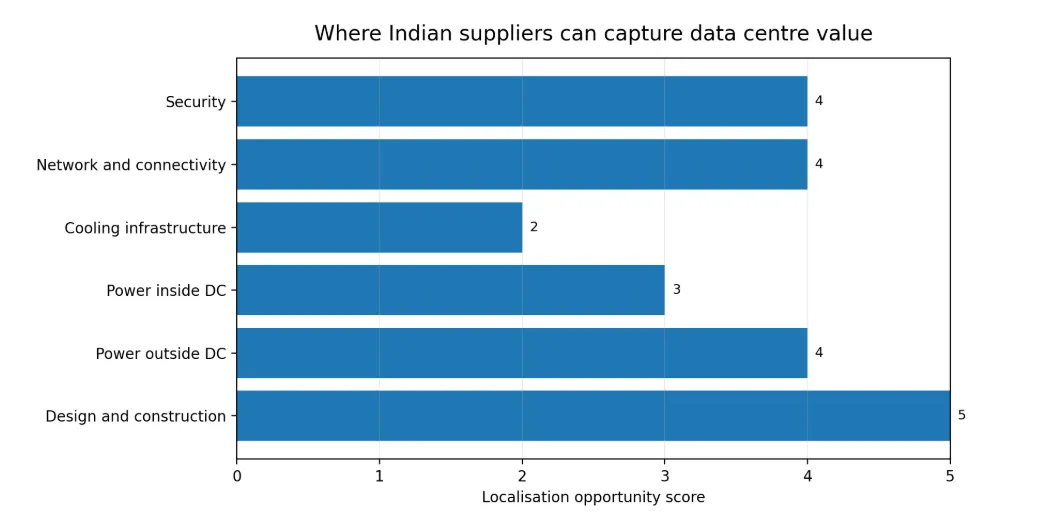

The data Center boom creates a major opportunity for Indian suppliers across construction, power infrastructure, cooling, network connectivity and security. Some segments already have strong domestic participation. Civil construction, design engineering, fibre optic cable manufacturing and selected security components can be localised further as project pipelines expand.

Cooling infrastructure is one of the most important white spaces. Precision cooling, CRAC and CRAH units, chillers and liquid cooling systems still depend heavily on global technology suppliers. As AI native facilities move toward high density racks, Indian suppliers have an opportunity to partner with global specialists, localise manufacturing and build after sales service capability. Power infrastructure also offers strong potential, especially in transformers, switchgear, modular UPS systems and renewable integration at the grid connection point.

Chart 4. Supplier localisation potential is strongest where domestic capability can combine with global technical partnerships.

Green data Centers are becoming a commercial requirement

Sustainability is becoming a core operating requirement because data Centers consume large amounts of electricity and water. Operators are adopting renewable power purchase agreements, better airflow management, advanced cooling, energy efficient power distribution and sustainability tracking. The goal is to reduce emissions intensity while meeting the higher power needs of AI workloads.

Green data Center strategy in India will be shaped by four areas. The first is renewable energy procurement. The second is energy efficient cooling. The third is water use management. The fourth is integrated monitoring through DCIM platforms. Operators that can combine cost effective power with strong sustainability performance will be better positioned with hyperscale customers, enterprise clients and regulators.

India’s data Center market is moving toward an integrated infrastructure powerhouse

India’s data Center sector is no longer only a real estate or colocation story. It is becoming a strategic infrastructure market linked to AI, cloud, digital sovereignty, energy systems and industrial supply chains. The next phase will reward operators that secure power early, build AI ready facilities, localise supplier networks and manage sustainability risks at scale.

The market opportunity is significant because India combines fast digital demand growth with relatively lower construction costs, a deep technology talent pool and improving state level policy support. The challenge is that capacity growth must be matched by grid readiness, cooling innovation, skilled operations and faster permitting. If these constraints are managed well, India can move from an emerging data Center hub to one of the most important digital infrastructure markets in the world.

Relevant DataM Intelligence reports for further research

2. Data Center Construction Market

3. Data Center Liquid Cooling Market