Quantum Sensors Market Growth

Quantum sensing is transitioning from lab-scale physics to deployable infrastructure across defense, aerospace, energy exploration, and precision industries. What makes this market strategically important today is not just growth, but timing. Governments and Tier-1 industrial players are actively funding and testing systems that are already demonstrating measurable ROI in navigation, subsurface mapping, and ultra-precise measurement.

The commercial inflection point is being driven by national quantum programs, defense procurement, and increasing demand for precision sensing in semiconductor, photonics, and advanced electronics ecosystems. The reader should view this market through an investment lens where early positioning aligns with long-cycle government contracts and high-margin instrumentation markets.

Market Scope

| Metric | Details |

| Market Size 2025 | USD 892.78 Million |

| Market Size 2035 | USD 3,904.61 Million |

| CAGR | 15.90% |

| Historic Years | 2023-2024 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Segments Covered | Platform, Product Type, Application, Region |

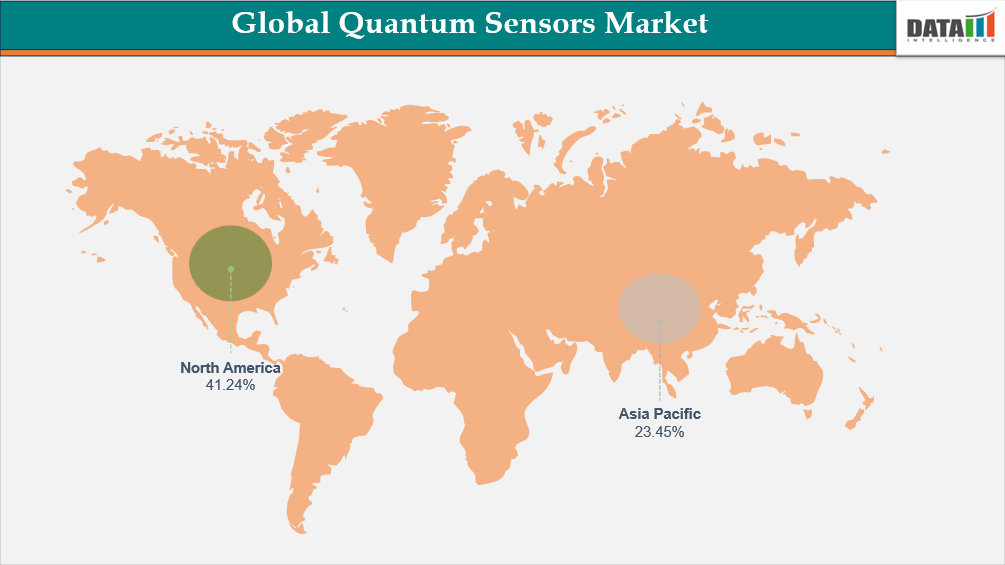

| Leading Region | North America |

| Fastest Growing Region | Asia-Pacific |

For More Information Request For Sample

Key Takeaways

- The Quantum Sensors market forecast for 2035 at USD 3.90 billion reflects strong government-backed demand rather than purely commercial scaling.

- Defense and aerospace programs are the earliest large-volume buyers, particularly for quantum navigation and atomic clocks.

- The Quantum Sensors market size in 2026 crossing USD 1.03 billion signals transition from pilot deployments to structured procurement cycles.

- Asia-Pacific is emerging as the fastest-growing region due to aggressive quantum technology investments in China and India.

- Supply chain constraints in photonic components, diamond substrates, and cold-atom systems are influencing pricing and adoption timelines.

- Premium pricing remains sustainable due to high accuracy and mission-critical applications, particularly in defense and geophysical exploration.

Demand Momentum and Growth Drivers

Defense Procurement and GPS-Denied Navigation

One of the most decisive Quantum Sensors growth drivers is the shift toward resilient navigation systems. Military forces are actively investing in quantum accelerometers, gyroscopes, and atomic clocks to operate in environments where GPS signals are unreliable or compromised.

Programs from the US Air Force Research Lab and the UK Ministry of Defence demonstrate that quantum inertial navigation systems are moving into operational testing. These systems provide significantly longer precision retention compared to classical sensors, making them critical for next-generation defense platforms.

Subsurface Exploration and Energy Sector ROI

Quantum gravimeters are gaining traction in oil and gas, geothermal exploration, and civil engineering due to their ability to map underground structures without invasive drilling. The EU’s EQUIP-G initiative highlights how portable quantum gravimeters are being deployed for large-scale resource mapping.

This is a clear example of direct ROI where quantum sensors reduce exploration costs while improving accuracy, making them attractive for energy and mining companies.

Expansion into Semiconductor and Photonics Ecosystems

Quantum sensors are increasingly linked to semiconductor and photonics innovation, especially in applications such as nanoscale imaging, wafer inspection, and material characterization. Companies like Qnami and M Squared Lasers are advancing quantum-enabled measurement tools that align with next-generation chip manufacturing.

As node scaling becomes more complex, the need for ultra-precise measurement tools is driving demand from semiconductor fabs and research labs.

Supply Chain, Materials, and Manufacturing Constraints

The Quantum Sensors market is deeply dependent on specialized materials and fabrication ecosystems, creating a non-traditional supply chain compared to classical sensors.

Material Bottlenecks

Key materials such as NV-diamond substrates, ultra-pure photonic components, and cold-atom systems face limited global supply. These materials require highly controlled manufacturing environments, which restrict scalability.

Foundry and Advanced Packaging Landscape

Unlike conventional semiconductor devices, quantum sensors rely on hybrid manufacturing models combining:

- Photonics fabrication

- Atomic physics systems

- Precision vacuum and cryogenic packaging

There is increasing reliance on specialized foundries and OSAT players capable of handling photonic integration and advanced packaging. This creates longer production cycles and higher costs, influencing Quantum Sensors pricing and adoption trends.

Integration Challenges

Integrating quantum sensors into existing platforms such as aircraft, satellites, and autonomous vehicles requires significant engineering adaptation. This limits rapid scaling but strengthens long-term vendor lock-in and pricing power.

Segmentation Analysis with Strategic Interpretation

Segmented by platform (Neutral Atoms, Trapped Ions, Nuclear Magnetic Resonance, Optomechanics, Photons, Superconducting (SQUID), Others), by product type (Atomic Clocks, Quantum Gravimeters, Quantum Magnetometers, Quantum Accelerometers, Quantum Gyroscopes, Others), by application (Aerospace & Defense, Automotive, Oil & Gas, Healthcare, Others), and by Region - Share, Trends, and Forecast to 2035.

Product Leadership Driven by Atomic Clocks and Gravimeters

Atomic clocks and quantum gravimeters are among the most commercially mature segments. Atomic clocks underpin navigation and timing systems, while gravimeters are widely used in geophysical applications.

Aerospace and Defense as the Anchor Segment

Aerospace and defense dominate due to mission-critical requirements. Quantum sensors provide capabilities such as:

- Drift-free navigation

- Submarine detection via magnetometry

- Underground mapping for ISR systems

This segment benefits from long-term contracts and high entry barriers.

Automotive Emerging with Autonomous Systems

The automotive sector is gradually adopting quantum sensors for advanced driver assistance and autonomous navigation. While still in early stages, demand is tied to the need for higher precision than conventional sensors can offer.

Quantum Sensors Regional Analysis

North America: Procurement-Led Market Leadership

North America leads the Quantum Sensors market due to strong defense funding and advanced R&D ecosystems. The US drives demand through agencies such as DARPA and the Air Force, with companies like Boeing, Honeywell, and Raytheon integrating quantum sensing technologies.

The region benefits from a mature supplier ecosystem and early adoption of quantum navigation and timing systems.

Europe: Industrial and Scientific Deployment Strength

Europe’s growth is supported by coordinated initiatives such as the EU Quantum Flagship and EQUIP-G. Countries like France, Germany, and the UK are focusing on:

- Geophysical sensing

- Aerospace applications

- Environmental monitoring

European companies are particularly strong in gravimetry and cold-atom technologies, making the region a leader in scientific-grade sensors.

Asia-Pacific: Fastest Growth Driven by National Programs

Asia-Pacific is the fastest-growing region in the Quantum Sensors regional analysis. China is investing heavily in quantum navigation and metrology, while India’s National Quantum Mission is supporting domestic innovation.

The region is also emerging as a manufacturing hub, supported by government funding and increasing participation from semiconductor and electronics industries.

Competitive Landscape and Company Strategy

The Quantum Sensors top companies operate across two distinct groups:

Industrial and Instrumentation Leaders

Companies such as Robert Bosch GmbH, LI-COR, Campbell Scientific, OTT HydroMet, and AOSense leverage existing industrial networks to commercialize quantum sensors in environmental monitoring and industrial applications.

Quantum-Native Innovators

Firms like Muquans and Qnami focus on high-performance, science-grade sensors. These companies lead in innovation and maintain strong pricing power due to product differentiation.

Strategic Direction

- Partnerships between industrial firms and quantum startups are accelerating commercialization

- Companies are focusing on application-specific solutions rather than generic sensor platforms

- Premium pricing models are sustained by high accuracy and limited competition

Recent Developments

In May 2026, Honeywell International Inc. expanded its quantum sensing technologies for navigation and timing applications. The initiative focuses on ultra-precise measurement capabilities. This supports aerospace and defense systems.

In April 2026, Qnami AG introduced advanced quantum sensors for nanoscale magnetic imaging. The development enhances sensitivity and resolution. This benefits research and semiconductor applications.

In March 2026, Infleqtion (ColdQuanta) strengthened its quantum sensing portfolio with cold-atom-based sensors for positioning and navigation. The innovation focuses on high accuracy and stability. This supports next-generation technologies.

Investment Outlook and Opportunities

Investors should view this market through the lens of long-cycle adoption and high-margin instrumentation.

Semiconductor and Electronics Integration

Opportunities are emerging in wafer inspection, nanoscale imaging, and photonics-based sensing, particularly as semiconductor nodes become more complex.

Defense and Aerospace Contracts

Government contracts offer stable revenue streams, making defense-focused quantum sensor companies attractive for long-term investment.

Energy and Infrastructure Applications

Quantum gravimetry and magnetometry provide measurable cost savings in resource exploration, creating strong adoption potential in oil, gas, and geothermal sectors.

Regulatory and Commercial Risk Factors

Quantum sensors fall under dual-use regulations, particularly in the US and Europe. Export controls and licensing requirements can limit international expansion.

Lack of standardization across regions also creates compliance challenges. However, evolving regulatory frameworks are expected to support broader commercialization while maintaining security controls.

Report Benefits

This report enables:

- Manufacturers to understand product positioning and pricing strategies

- Investors to identify high-growth segments and funding opportunities

- Suppliers to navigate material and component demand trends

- Technology companies to align with semiconductor and photonics integration needs

- Procurement teams to evaluate ROI and vendor capabilities

Target Audience

- Aerospace and defense contractors

- Semiconductor and photonics companies

- Industrial instrumentation manufacturers

- Energy and mining companies

- Government agencies and research institutions

- Venture capital and private equity firms

- Advanced electronics and automotive OEMs